Embed Size (px)

DESCRIPTION

CREDIT MANAGEMENT AT SERICULTURIST’S CUM FARMER’S SERVICE CO-OPERATIVE BANK LIMITED”

Citation preview

A Project ReportOn

“CREDIT MANAGEMENT AT SERICULTURIST’S CUM FARMER’S SERVICE CO-OPERATIVE BANK LIMITED”

Submitted by

CHANDRA .GSUSN: 1SP11MBA09

Under the guidance of

Internal Guide External GuideMs .Preethi .M S, Lecturer Mr. Narayanaswamy Dept of Management Studies Manager SCFS CO-Operative Bank S.E.A.C.E.T, Bangalore-560049 Hoskote-562114

Definition and Meaning of co-Operative Banking:

A co-operative bank is a co-operative organization engaged in banking function of acceptance and deposit and lending credits.

The co-operative bank and societies perform and importance role in meeting in requirements of people in rural areas co-operative banks of district entities by themselves with separate jurisdictions and independent of board of directors.

Aims of co-operative banks Types of Co-Operative Banks: Agriculture co-operative banks. Non-agriculture co-operative banks.

INDUSTRY PROFILE

Backgrund and Inception: S.C.F.S co-operative bank limited is a premier private sector Indian bank with a heritage of over 36 years and over 3 million satisfied customers.

Started in the date 13/09/1976 as the name of Sericulture’s cum farmer’s service Co-operative Bank, Hoskote town in the date of 26/02/1998.

Vision & Mission: Mission Statement “obviously accepting the deposits and lending it to its

customers, as and when the depositors demand for their money giving back to them.”

COMPANY PROFILE

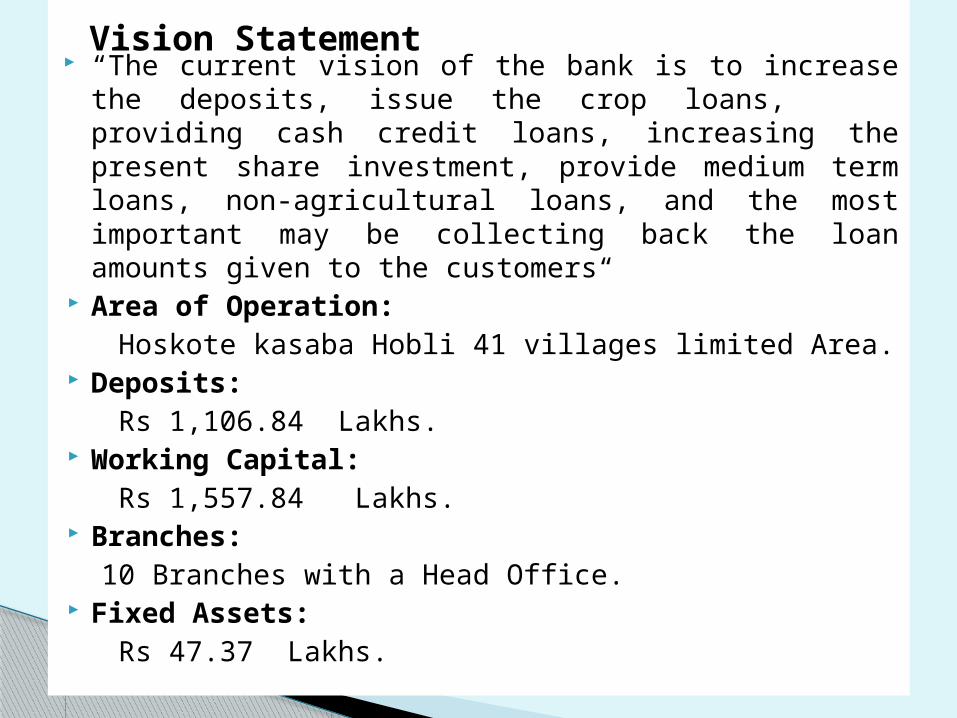

“The current vision of the bank is to increase the deposits, issue the crop loans, providing cash credit loans, increasing the present share investment, provide medium term loans, non-agricultural loans, and the most important may be collecting back the loan amounts given to the customers“

Area of Operation: Hoskote kasaba Hobli 41 villages limited Area. Deposits: Rs 1,106.84 Lakhs. Working Capital: Rs 1,557.84 Lakhs. Branches: 10 Branches with a Head Office. Fixed Assets: Rs 47.37 Lakhs.

Vision Statement

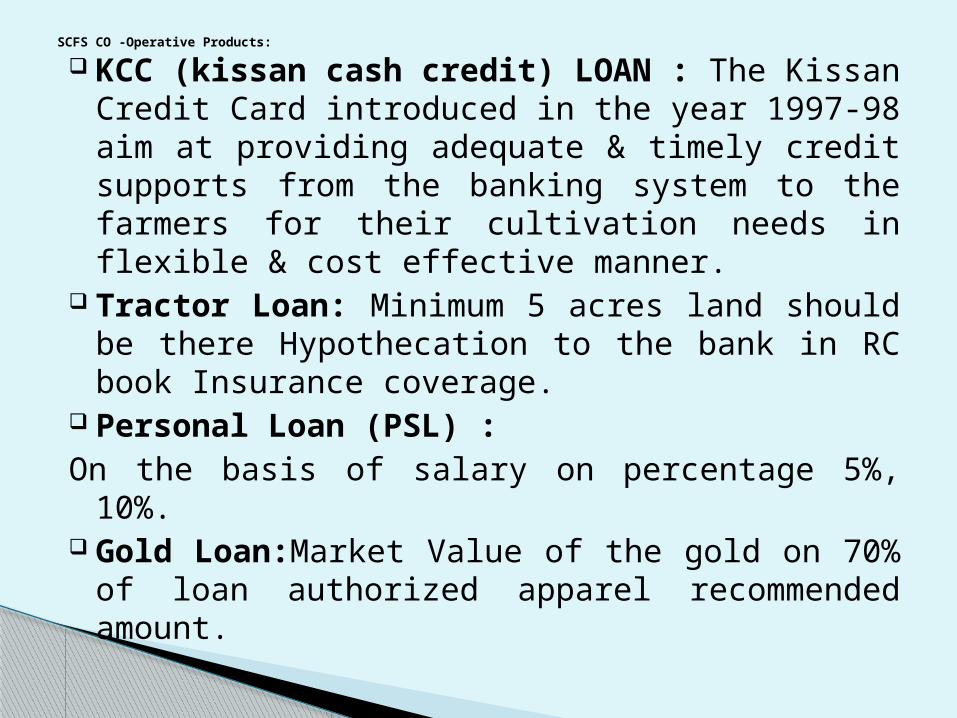

KCC (kissan cash credit) LOAN : The Kissan Credit Card introduced in the year 1997-98 aim at providing adequate & timely credit supports from the banking system to the farmers for their cultivation needs in flexible & cost effective manner.

Tractor Loan: Minimum 5 acres land should be there Hypothecation to the bank in RC book Insurance coverage.

Personal Loan (PSL) :On the basis of salary on percentage 5%, 10%. Gold Loan:Market Value of the gold on 70% of

loan authorized apparel recommended amount.

SCFS CO -Operative Products:

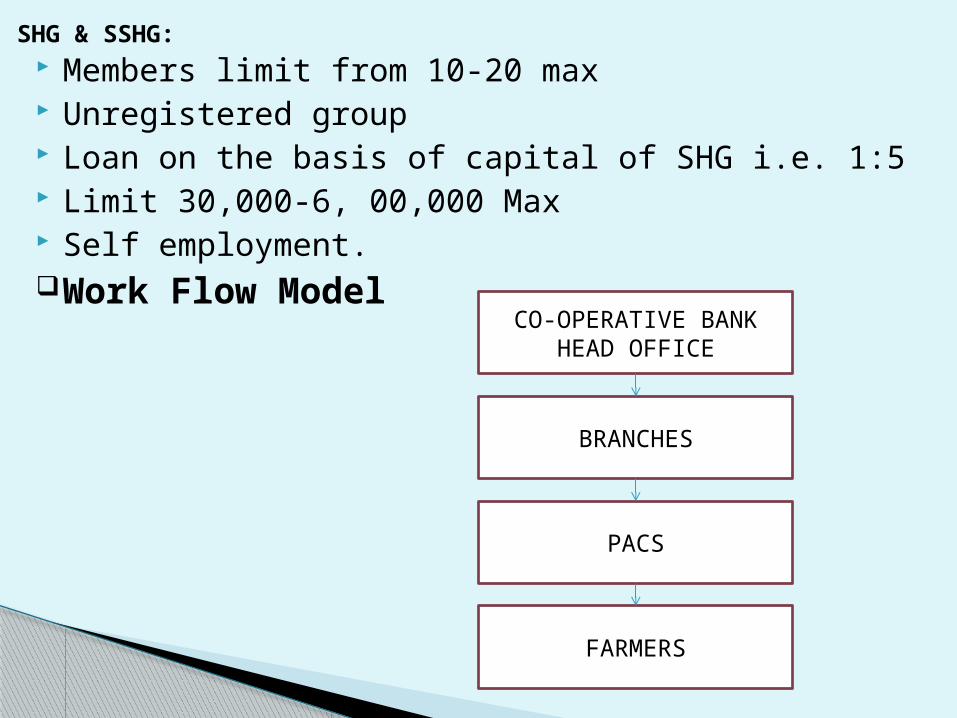

Members limit from 10-20 max Unregistered group Loan on the basis of capital of SHG i.e. 1:5 Limit 30,000-6, 00,000 Max Self employment.Work Flow Model

SHG & SSHG:

CO-OPERATIVE BANK HEAD OFFICE

BRANCHES

PACS

FARMERS

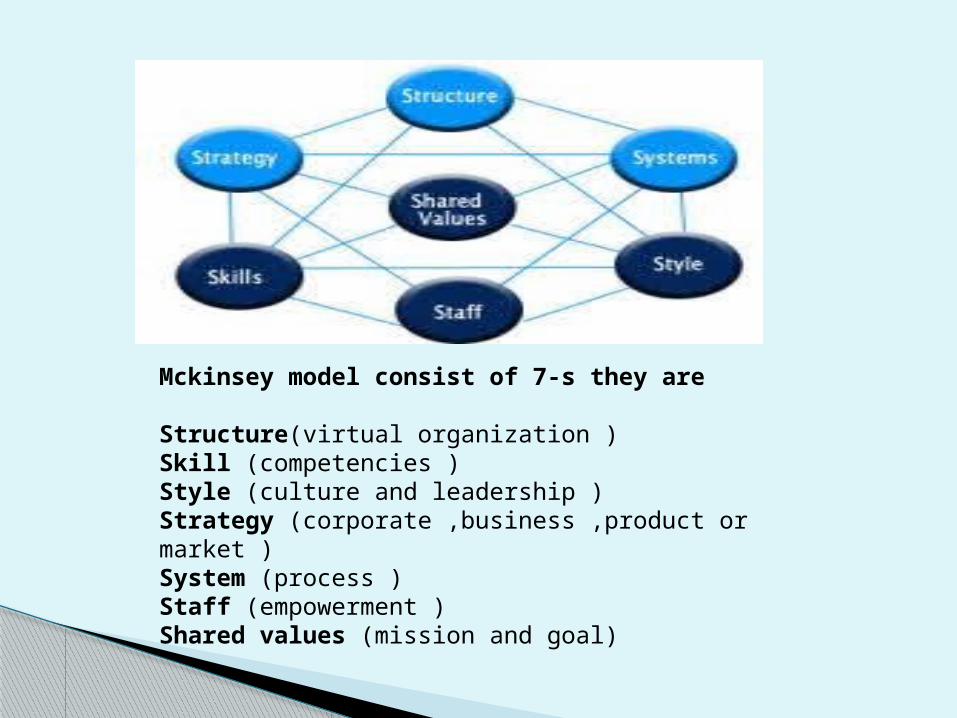

MCKENSY’S 7S FRAMEWORK

Mckinsey model consist of 7-s they are Structure(virtual organization )Skill (competencies )Style (culture and leadership )Strategy (corporate ,business ,product or market )System (process )Staff (empowerment )Shared values (mission and goal)

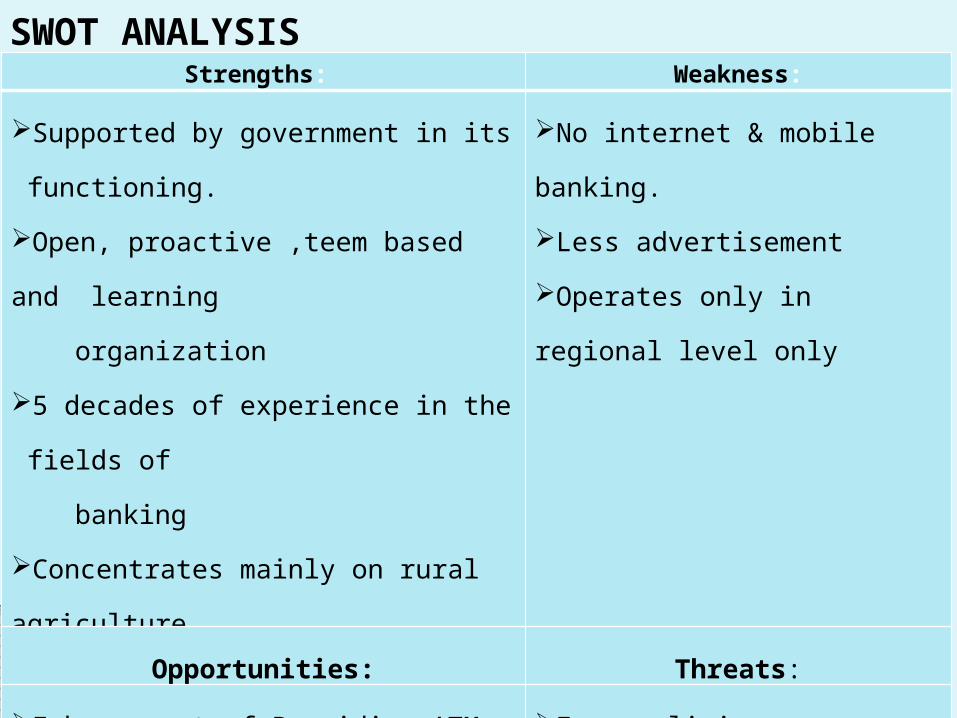

SWOT ANALYSIS Strengths: Weakness:

Supported by government in its functioning.

Open, proactive ,teem based and learning

organization

5 decades of experience in the fields of

banking

Concentrates mainly on rural agriculture

development

No internet & mobile banking.

Less advertisement

Operates only in regional level only

Opportunities: Threats:

Enhancement of Providing ATM facilities

Providing internet and mobile

banking facilities

Providing life insurance schemes

Easy policies

Less documentation for different

types of loans

Updating facility to their customers

LEARNING EXPERIENCE Project work is the practical orientation program which every

student has to undergo as per part the academy .This work enriches the practical knowledge, about the functioning of the organization. The scope of the project covers the various aspects of an organization like how they work authority responsibility, distribution and functioning of different departments.

It was a great opportunity for me to carry out a project work with Co-operative Bank. During this period I was exposed to many of the banking concepts, terms, process and systems. Concepts which I learnt during my academy theoretically were been experienced practically in the bank.

Basic management concepts such as planning, organizing, directing and controlling were implemented smoothly in the bank.

GENERAL INTRODUCTION Introduction to Finance: Finance is a life-blood of every business. At present, we cannot think of an economy without money

because an economy without money cannot function as effectively, efficiently and smoothly. Meaning of Finance: Finance is the master key, which provides access to all the

resources for being employed in manufacturing activities. Finance is the art raising and spending of money.

Every business concern requires money or finance to commence its operations to continue its operations and for expansion or growth.

Introduction to Credit Management:

Advances play an important role in the gross earnings and net profit of

banks.

The basic function of a bank irrespective of type is to enable individuals &

business enterprise to purchase of goods & services.

Consumers demand credit to acquire goods for which they pay on a future

date.

Function of modern banks, lending with security is the most important

function.

The proper management of loans & advances is known as

“MANAGEMENT OF LOANS & ADVANCES IN BANKS”.

Credit management not only plays an important role in

gross earnings of banks, but also promotes the economic

development of the country.

All type of business activity including trade, industry &

agriculture depends on bank finance. Banks assists in

creating more employment & thus helps in raising the

standard of living.

Credit quality of the bank is one of the most important

criteria in establishing the credit worthiness of a bank

Scope of the Study:

The study “CREDIT MANAGEMENT” aims to covering the process of financing

and managing credit. The study of credit management is applied in banking and

financial institutions.

The scope of the study is limited to the data of THE S.C.F.S CO-OPERATIVE

BANK LIMITED.

The scope of the Credit Management of the S.C.F.S Co-operative Bank covers the

Comparison , of assets and liability of current year with the previous five years.

The study is exclusively conducted at THE S.C.F.S CO-OPERATIVE BANK

LIMITED.

The study is confined to finance department.

The study is limited only to Comparative analysis, Comprehensive analysis,

and growth analysis.

Objective of the Study

Self-help and co-operation among the members and

depositors of bank.

study the position of various loans and advances.

Study the policy of borrow or raise money.

Study the various types of loans schemes offered and to

analyze their growth.

Study about the reasons contributing towards the growth of

the loans and advances.

Methodology and Data Collection: For analysis of investment structure, many methods are available such

as comparative financial position of the bank, profit and loss account, balance sheet etc,

The technique selected for the study includes table & graphs relating to the credit methodology.

Sources of Data:There are two type of sources of data collection Viz;.

Primary data. Secondary data. Primary Data:Short interviews with the branch managers, Employees and customers

of the branch. Secondary Data:

Accounting records like registers, annual records, and audit reports and inspection files are the internal secondary data.

A manual, journals, magazines and text book is collection the external secondary data.

FINDINGS, SUGGESTION, AND CONCLUSION

SUMMARY OF FINDINGS:

The bank has no regular participation in call money markets; it is

mainly dependent on the surpluses of the bank.

The bank is not maintaining any particular fund flow statement.

The bank’s total expenses are met out of profits made.

It is observed that Saving Deposits and Fixed Deposits constitute a

major part of total deposits.

The bank has to concentrate more on recurring deposits, saving

SHG deposits.

Continue…….

PRIMARY OF FINDINGS:

It is observed that the credit operation is fluctuation in recovery.

The bank shows various sales increasing in year by year.

The bank recovery in year by year continuously increasing.

Fixed & saving bank deposits are continuously increasing their deposits.

Saving SHG deposits are continuously increasing in their deposits year by year.

In comprehensive analysis, the fixed, saving deposit is varying year by year.

To observe the loans are increasing in vehicle, gold loan and gradual increase in

kissan credit card

The SCFS co operative banks interest rate 13% of overall loans except kissan

credit card interest rate only 1%.

The percentage of growth of the SCFS Co-operative Bank has been

fluctuating year by year.

The loans provided by the bank such as Gold loan and vehicle loan are

rapidly increasing constantly. The bank has to concentrate more towards on

short-term loans, medium term loans and long-term loans.

SUGGESTION:

The bank should attract more and more on recurring deposits, saving SHG

deposits by providing good services when compared to the other banks.

The bank should provide its customer advanced services such as E-

banking, Tele-Banking, ATMs services Etc., so that more and more

customers are attracted. That helps the bank to lend to higher level and in

turn will result in increasingly its profitability.

The bank should increase its facility towards short-term

loans to maximum extent, so that it makes possible for the

bank to increase its profitability.

The bank should increase its branches throughout the state

for its future growth. So that it may help the bank to extends

its valuable services to the customers.

The Hoskote SCFS co-operative Banks must provide ATMs

services to provide better services to customers.

If the bank has to attract more customers and more

transaction by providing good services to the customer

The bank can provide advances and loans to the general public for

the following purposes:

Small-scale and cottage industries.

Self-employed person or young entrepreneurs.

Increase short-term and long-term deposits by providing higher

rate of interest.

The procedure in sanctioning the loan is to be reduced.

The bank has to provide agriculture loan at interest rate for all

agricultural activities.

CONCLUSION: The credit management process carried The credit department

thoroughly analysis the credit requirement of the company and the capacity to service the debt.

The credit appraisal passes through various stages and evaluations before it is appraised. In early days lending were provided in less numbers because the formalities for sanctioning and the interest rates were too high. However, after globalization the banks have reduced the formalities as well as interest rates on various loans and advances.

The system module of SCFS co-operative bank at present is functioning well. It gave me a good insight in to the whole process of sanctioning loan and difficulties that are faced in dealing with the client.

?

Thank you