Embed Size (px)

DESCRIPTION

Change Imperative within the Food & Drink Industry. FDII Annual Conference April 27 th , 2006. 1. Deloitte. Audit. Tax. Consulting. Corporate Finance. Deloitte Overview. Deloitte has been advising clients since 1845 12 consecutive years of revenue growth - PowerPoint PPT Presentation

Citation preview

1

Change Imperative within the Food & Drink Industry.FDII Annual Conference

April 27th, 2006

2 ©2006 Deloitte. All rights reserved19 Apr 2023

3 ©2006 Deloitte. All rights reserved19 Apr 2023

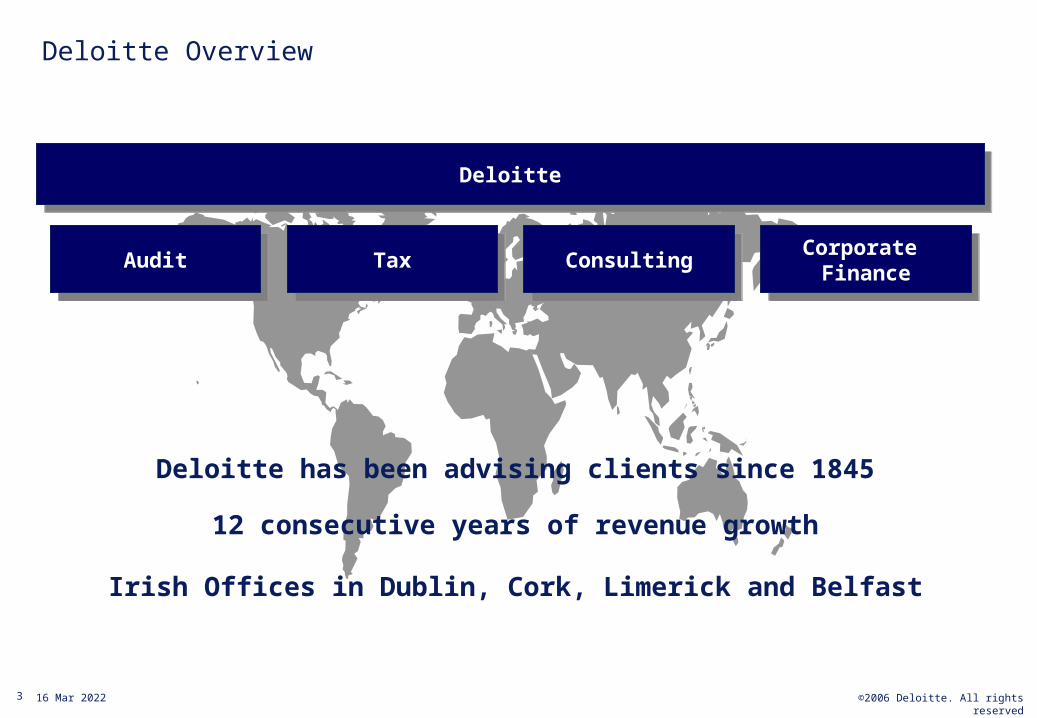

Deloitte has been advising clients since 1845

12 consecutive years of revenue growth

Irish Offices in Dublin, Cork, Limerick and Belfast

Deloitte Overview

DeloitteDeloitte

Corporate Finance

Corporate FinanceConsultingConsultingTaxTaxAuditAudit

4 ©2006 Deloitte. All rights reserved19 Apr 2023

Clients in the Food and Beverage Industry

5 ©2006 Deloitte. All rights reserved19 Apr 2023

Check out Deloitte.com for our latest publications

Deloitte - “Famous for Food”

6 ©2006 Deloitte. All rights reserved19 Apr 2023

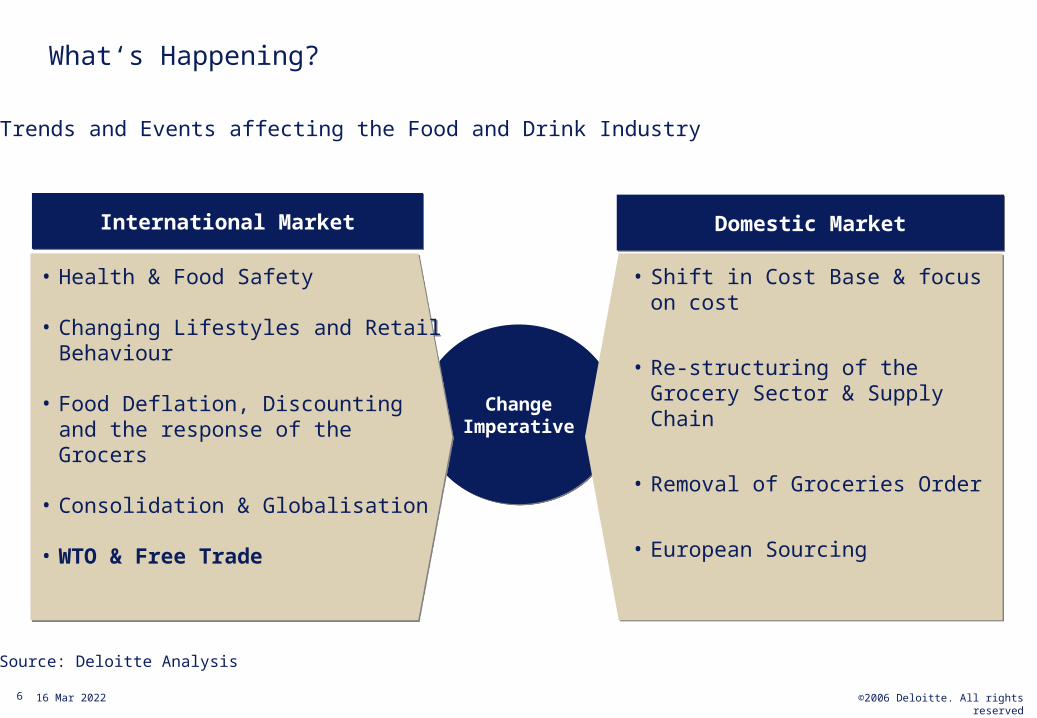

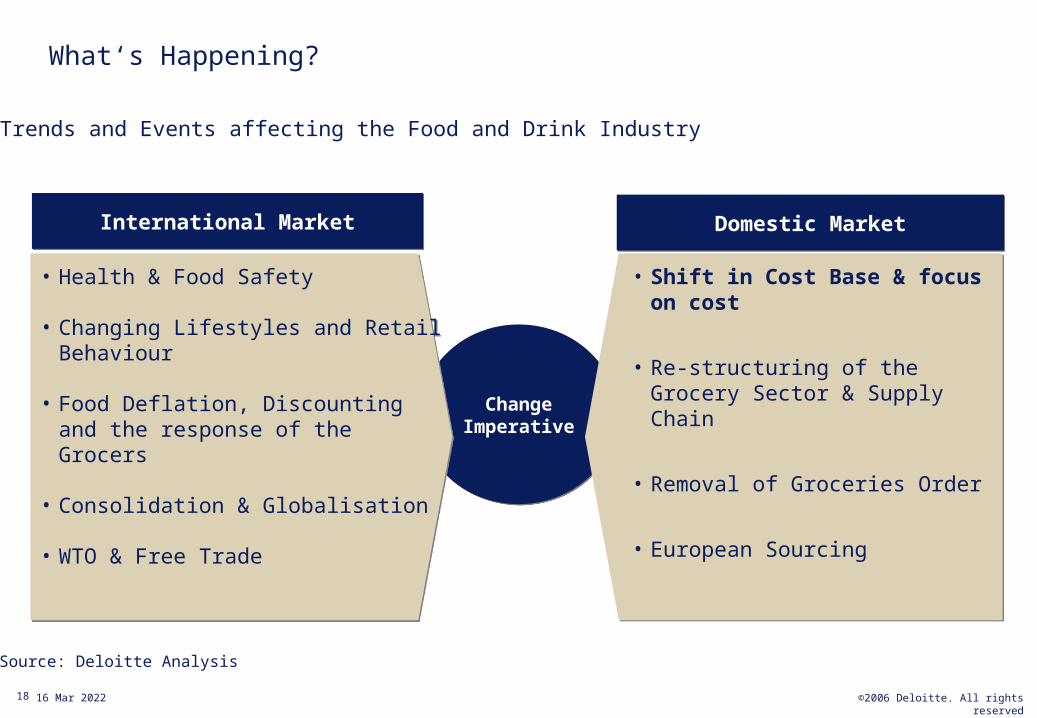

What‘s Happening?

Change Imperative

Change Imperative

• Health & Food Safety

• Changing Lifestyles and Retail Behaviour

• Food Deflation, Discounting and the response of the Grocers

• Consolidation & Globalisation

• WTO & Free Trade

• Health & Food Safety

• Changing Lifestyles and Retail Behaviour

• Food Deflation, Discounting and the response of the Grocers

• Consolidation & Globalisation

• WTO & Free Trade

• Shift in Cost Base & focus on cost

• Re-structuring of the Grocery Sector & Supply Chain

• Removal of Groceries Order

• European Sourcing

• Shift in Cost Base & focus on cost

• Re-structuring of the Grocery Sector & Supply Chain

• Removal of Groceries Order

• European Sourcing

International MarketInternational Market Domestic MarketDomestic Market

Trends and Events affecting the Food and Drink Industry

Source: Deloitte Analysis

7 ©2006 Deloitte. All rights reserved19 Apr 2023

8 ©2006 Deloitte. All rights reserved19 Apr 2023

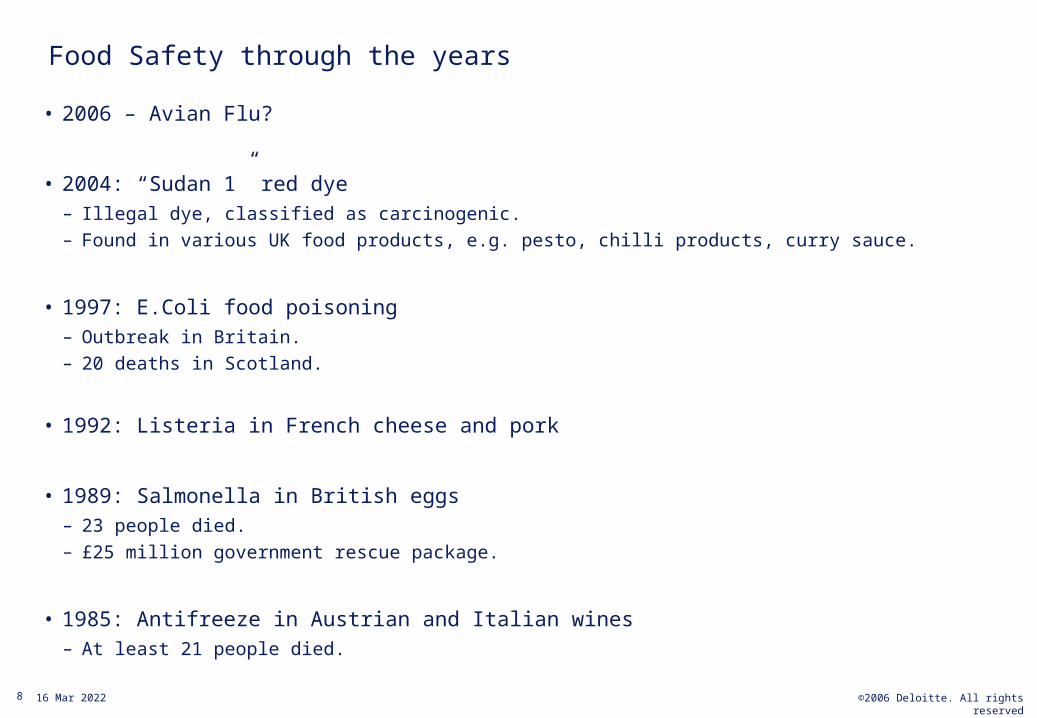

Food Safety through the years

• 2006 – Avian Flu?

• 2004: “Sudan 1” red dye– Illegal dye, classified as carcinogenic.– Found in various UK food products, e.g. pesto, chilli products, curry sauce.

• 1997: E.Coli food poisoning– Outbreak in Britain.– 20 deaths in Scotland.

• 1992: Listeria in French cheese and pork

• 1989: Salmonella in British eggs– 23 people died.– £25 million government rescue package.

• 1985: Antifreeze in Austrian and Italian wines– At least 21 people died.

9 ©2006 Deloitte. All rights reserved19 Apr 2023

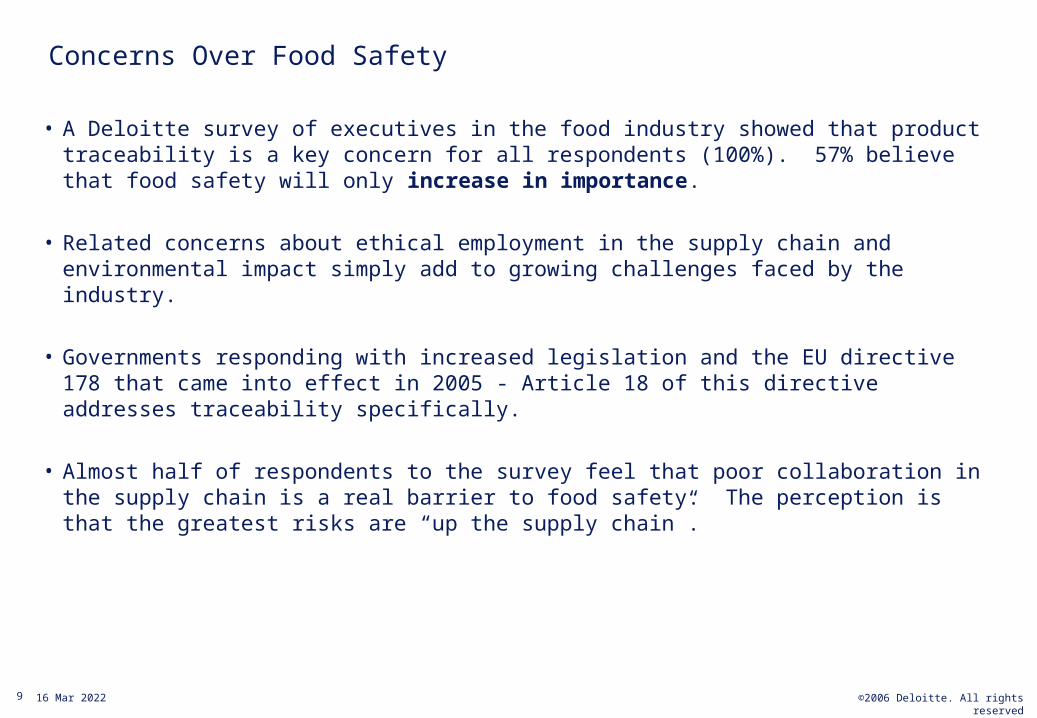

Concerns Over Food Safety

• A Deloitte survey of executives in the food industry showed that product traceability is a key concern for all respondents (100%). 57% believe that food safety will only increase in importance.

• Related concerns about ethical employment in the supply chain and environmental impact simply add to growing challenges faced by the industry.

• Governments responding with increased legislation and the EU directive 178 that came into effect in 2005 - Article 18 of this directive addresses traceability specifically.

• Almost half of respondents to the survey feel that poor collaboration in the supply chain is a real barrier to food safety. The perception is that the greatest risks are “up the supply chain”.

10 ©2006 Deloitte. All rights reserved19 Apr 2023

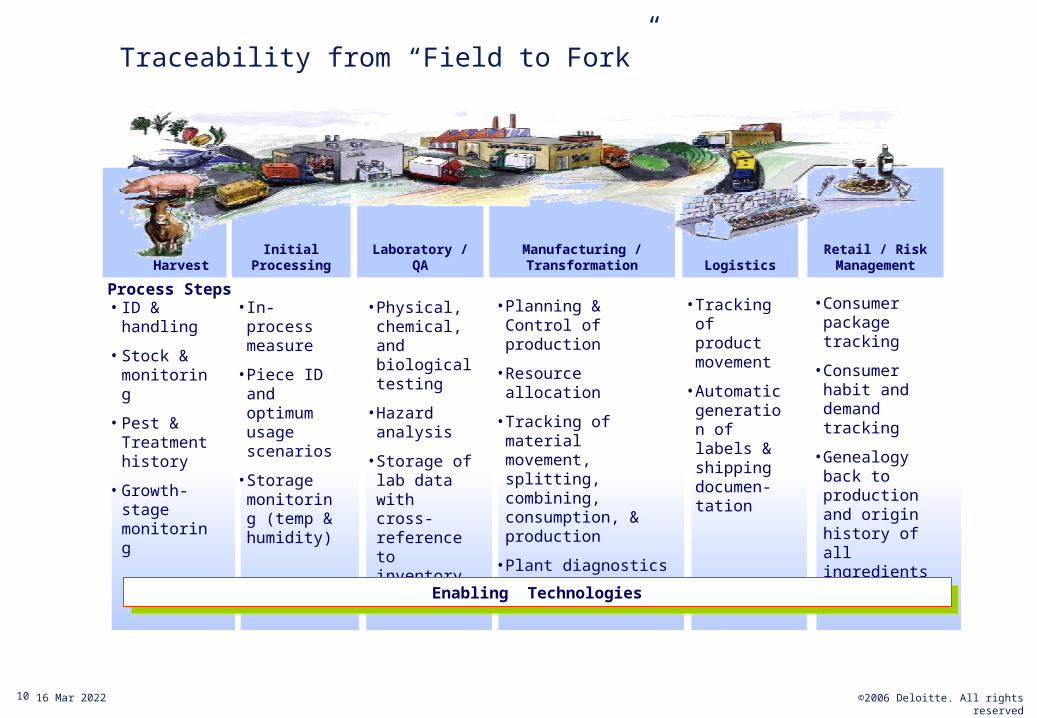

Initial ProcessingHarvest

Laboratory /QA Logistics

Retail / RiskManagement

Manufacturing /Transformation

• ID & handling

• Stock & monitoring

• Pest & Treatment history

• Growth-stage monitoring

•In-process measure

•Piece ID and optimum usage scenarios

•Storage monitoring (temp & humidity)

•Physical, chemical, and biological testing

•Hazard analysis

•Storage of lab data with cross-reference to inventory

•Planning & Control of production

•Resource allocation

•Tracking of material movement, splitting, combining, consumption, & production

•Plant diagnostics and online HACCP & SPC/SQC

•Tracking of product movement

•Automatic generation of labels & shipping documen-tation

•Consumer package tracking

•Consumer habit and demand tracking

•Genealogy back to production and origin history of all ingredients

Enabling TechnologiesEnabling Technologies

Process Steps

Traceability from “Field to Fork”

11 ©2006 Deloitte. All rights reserved19 Apr 2023

12 ©2006 Deloitte. All rights reserved19 Apr 2023

International Trends – Changing Lifestyles and Retail Behaviour

• Convenience Shopping – “Food on the Go”

– Prepared Foods / Meal Solutions

– Eating Out

• Retailer Brands

• Innovation

• Successful Collaboration & Account Management

13 ©2006 Deloitte. All rights reserved19 Apr 2023

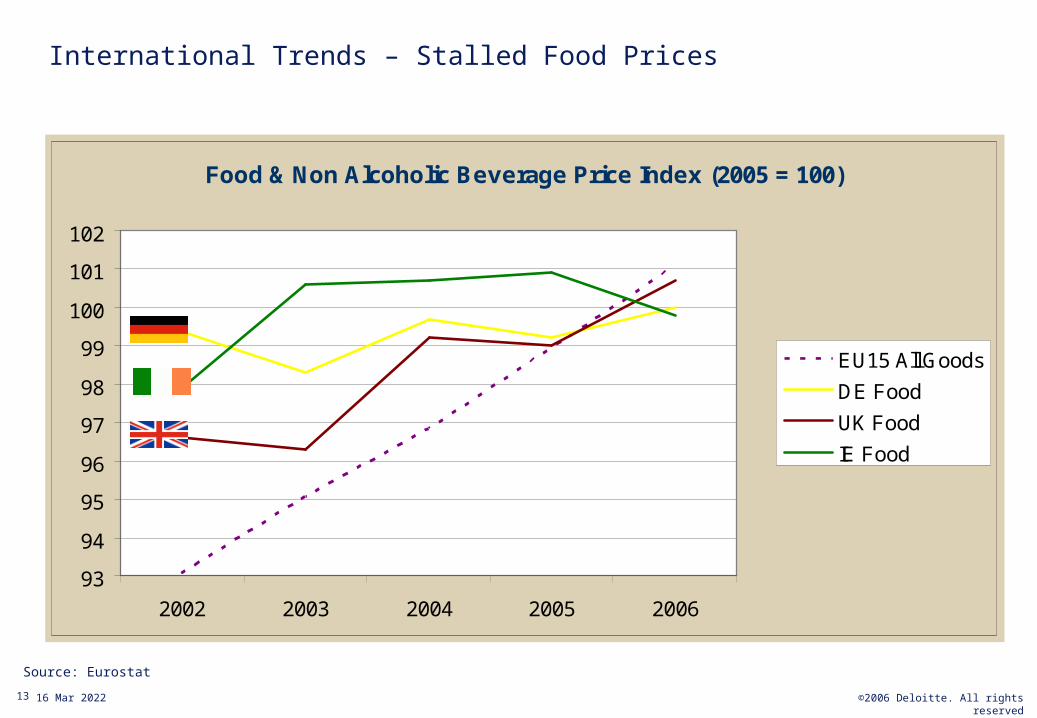

Food & Non Alcoholic Beverage Price Index (2005 = 100)

93

94

95

96

97

98

99

100

101

102

2002 2003 2004 2005 2006

EU15 All Goods

DE Food

UK Food

IE Food

International Trends – Stalled Food Prices

Source: Eurostat

14 ©2006 Deloitte. All rights reserved19 Apr 2023

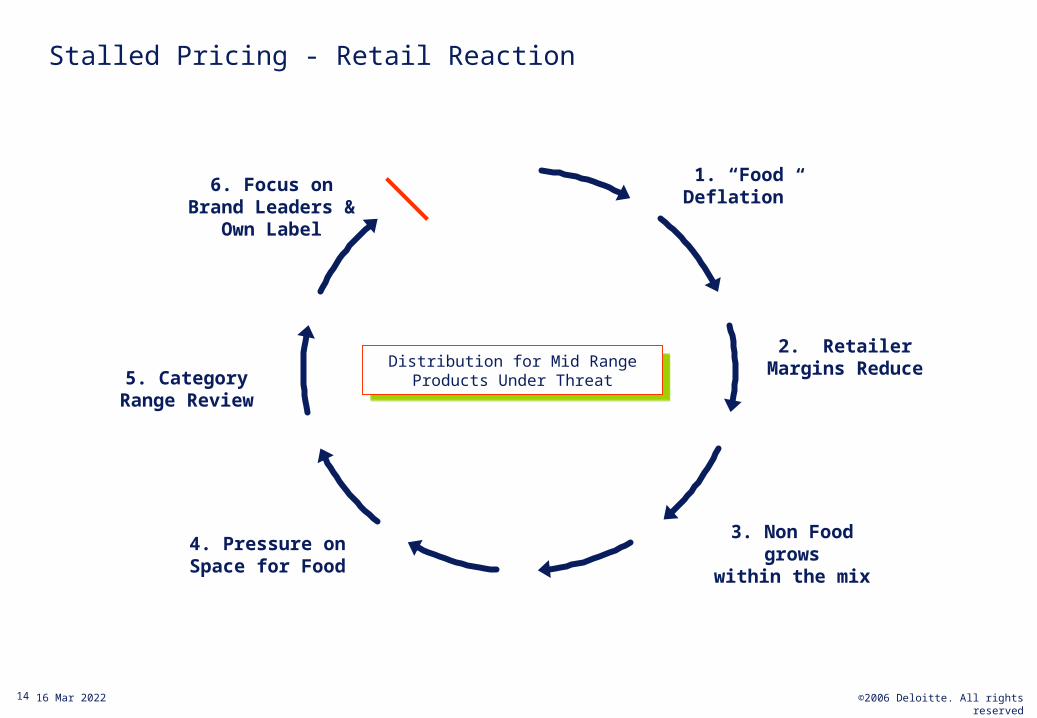

Stalled Pricing - Retail Reaction

1. “Food Deflation”

2. Retailer Margins Reduce

3. Non Food grows

within the mix

4. Pressure on Space for Food

5. Category Range Review

6. Focus on Brand Leaders &

Own Label

Distribution for Mid Range Products Under Threat

Distribution for Mid Range Products Under Threat

15 ©2006 Deloitte. All rights reserved19 Apr 2023

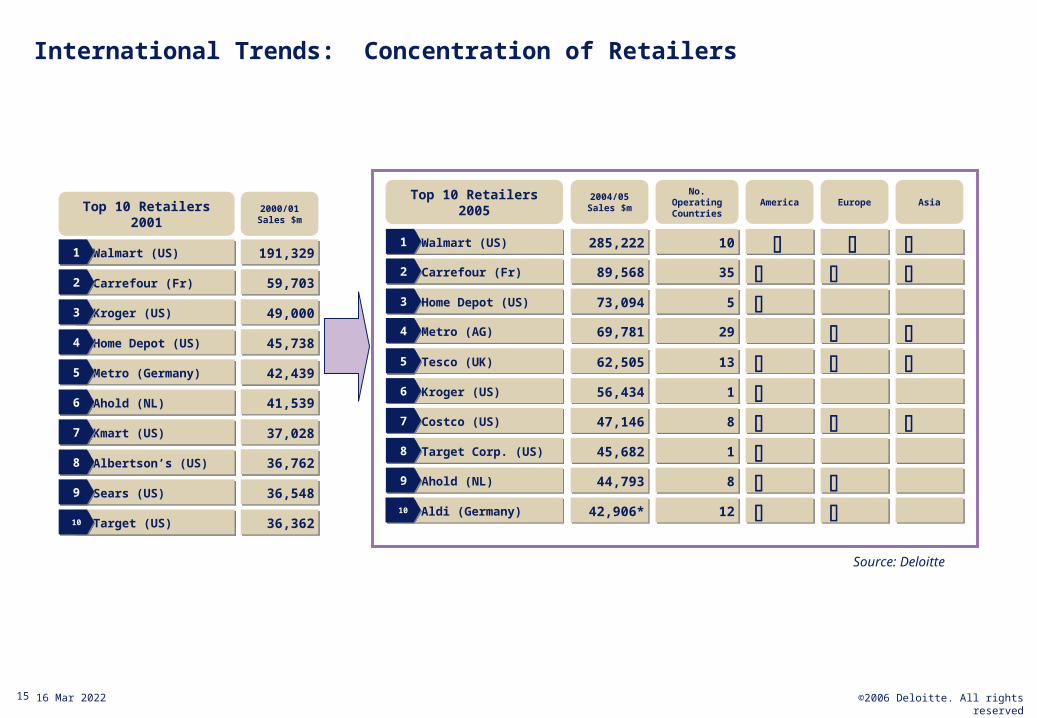

International Trends: Concentration of Retailers

Carrefour (Fr)Carrefour (Fr)22

Home Depot (US)Home Depot (US)33

Metro (AG)Metro (AG)44

Tesco (UK)Tesco (UK)55

Kroger (US)Kroger (US)66

Costco (US)Costco (US)77

Target Corp. (US)Target Corp. (US)88

Ahold (NL)Ahold (NL)99

Aldi (Germany)Aldi (Germany)1010

Walmart (US)Walmart (US)11 285,222285,222

89,56889,568

73,09473,094

69,78169,781

62,50562,505

56,43456,434

47,14647,146

45,68245,682

44,79344,793

42,906*42,906*

Top 10 Retailers 2005

2004/05 Sales $m

Source: Deloitte

1010

3535

55

2929

1313

11

88

11

88

1212

No. Operating Countries

America

Europe

Asia

Top 10 Retailers 2001

Walmart (US)Walmart (US)11

Carrefour (Fr)Carrefour (Fr)22

Kroger (US)Kroger (US)33

Home Depot (US)Home Depot (US)44

Metro (Germany)Metro (Germany)55

Ahold (NL)Ahold (NL)66

Kmart (US)Kmart (US)77

Albertson’s (US)Albertson’s (US)88

Sears (US)Sears (US)99

Target (US)Target (US)1010

191,329191,329

59,70359,703

49,00049,000

45,73845,738

42,43942,439

41,53941,539

37,02837,028

36,76236,762

36,54836,548

36,36236,362

2000/01 Sales $m

16 ©2006 Deloitte. All rights reserved19 Apr 2023

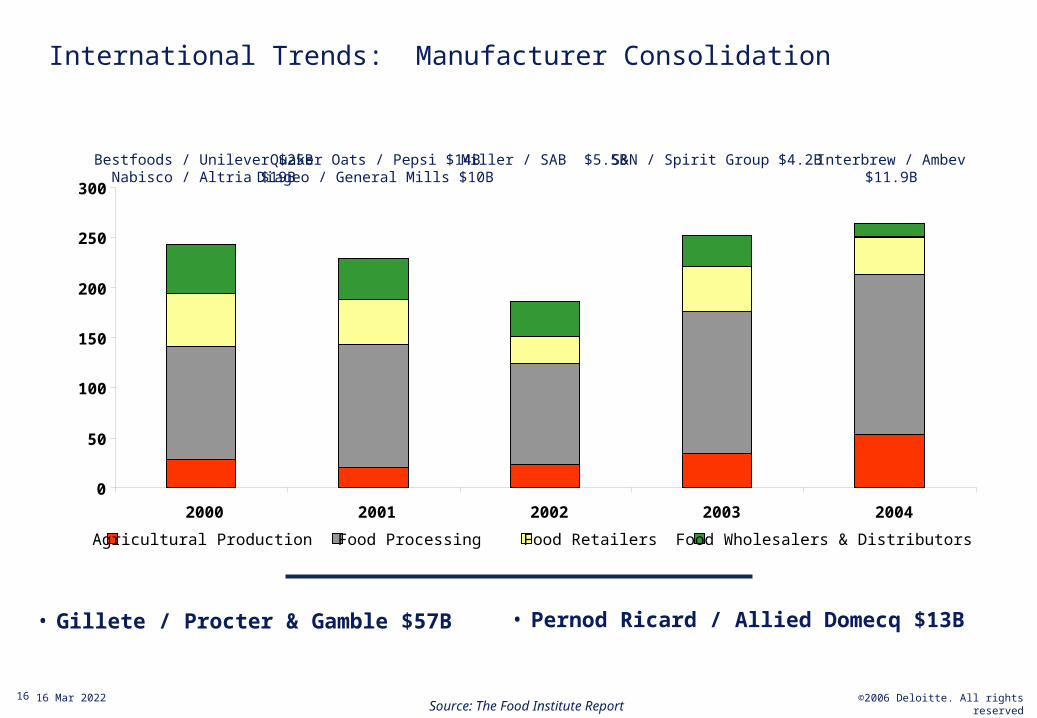

0

50

100

150

200

250

300

2000 2001 2002 2003 2004

Agricultural Production Food Processing Food Retailers Food Wholesalers & Distributors

International Trends: Manufacturer Consolidation

• Gillete / Procter & Gamble $57B

Source: The Food Institute Report

Bestfoods / Unilever $25BNabisco / Altria $19B

Quaker Oats / Pepsi $14BDiageo / General Mills $10B

Miller / SAB $5.5B Interbrew / Ambev $11.9BS&N / Spirit Group $4.2B

• Pernod Ricard / Allied Domecq $13B

17 ©2006 Deloitte. All rights reserved19 Apr 2023

International Trends: Imperatives for FDII Members

• “Best in Class” Supply Chain Integrity

• Continued Focus on Innovation

• Brilliant Customer Relationships– Account Management

– International / Global Partner?

• Be Prepared for the Opportunities & Threats from Consolidation– Local, Mid - Range Brands are available!!

– Loss of Agency Rights

– Competition for Shelf Space

18 ©2006 Deloitte. All rights reserved19 Apr 2023

What‘s Happening?

Change Imperative

Change Imperative

• Health & Food Safety

• Changing Lifestyles and Retail Behaviour

• Food Deflation, Discounting and the response of the Grocers

• Consolidation & Globalisation

• WTO & Free Trade

• Health & Food Safety

• Changing Lifestyles and Retail Behaviour

• Food Deflation, Discounting and the response of the Grocers

• Consolidation & Globalisation

• WTO & Free Trade

• Shift in Cost Base & focus on cost

• Re-structuring of the Grocery Sector & Supply Chain

• Removal of Groceries Order

• European Sourcing

• Shift in Cost Base & focus on cost

• Re-structuring of the Grocery Sector & Supply Chain

• Removal of Groceries Order

• European Sourcing

International MarketInternational Market Domestic MarketDomestic Market

Trends and Events affecting the Food and Drink Industry

Source: Deloitte Analysis

19 ©2006 Deloitte. All rights reserved19 Apr 2023

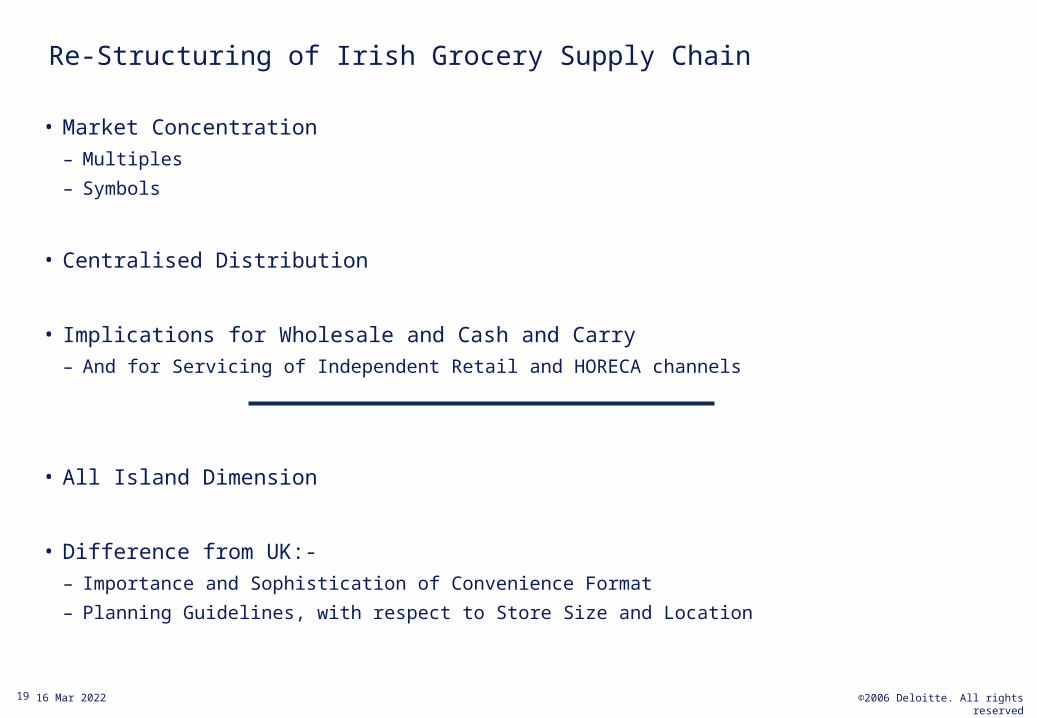

Re-Structuring of Irish Grocery Supply Chain

• Market Concentration– Multiples

– Symbols

• Centralised Distribution

• Implications for Wholesale and Cash and Carry– And for Servicing of Independent Retail and HORECA channels

• All Island Dimension

• Difference from UK:-– Importance and Sophistication of Convenience Format

– Planning Guidelines, with respect to Store Size and Location

20 ©2006 Deloitte. All rights reserved19 Apr 2023

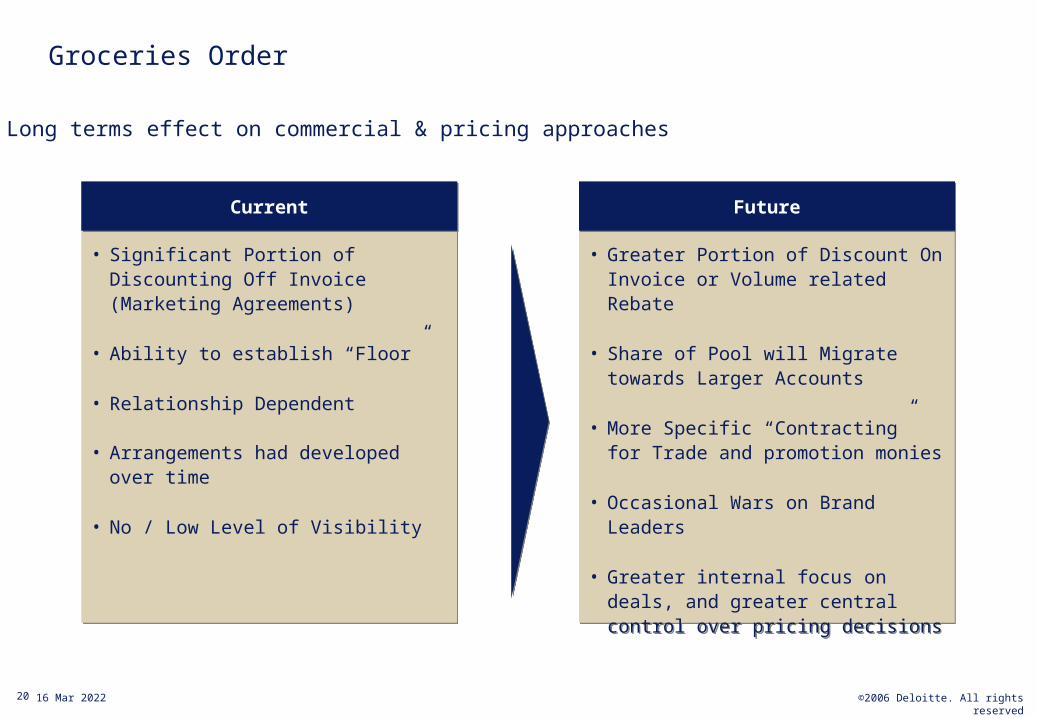

Groceries Order

Long terms effect on commercial & pricing approaches

• Significant Portion of Discounting Off Invoice (Marketing Agreements)

• Ability to establish “Floor”

• Relationship Dependent

• Arrangements had developed over time

• No / Low Level of Visibility

• Significant Portion of Discounting Off Invoice (Marketing Agreements)

• Ability to establish “Floor”

• Relationship Dependent

• Arrangements had developed over time

• No / Low Level of Visibility

CurrentCurrent

• Greater Portion of Discount On Invoice or Volume related Rebate

• Share of Pool will Migrate towards Larger Accounts

• More Specific “Contracting” for Trade and promotion monies

• Occasional Wars on Brand Leaders

• Greater internal focus on deals, and greater central control over pricing decisions

• Greater Portion of Discount On Invoice or Volume related Rebate

• Share of Pool will Migrate towards Larger Accounts

• More Specific “Contracting” for Trade and promotion monies

• Occasional Wars on Brand Leaders

• Greater internal focus on deals, and greater central control over pricing decisions

FutureFuture

21 ©2006 Deloitte. All rights reserved19 Apr 2023

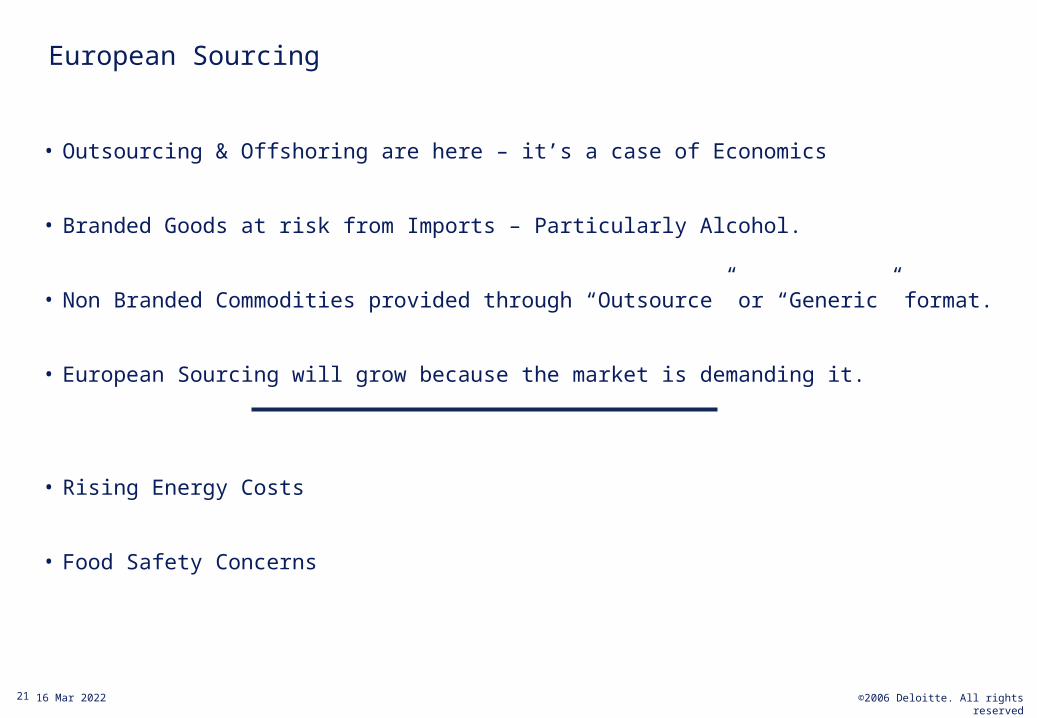

European Sourcing

• Outsourcing & Offshoring are here – it’s a case of Economics

• Branded Goods at risk from Imports – Particularly Alcohol.

• Non Branded Commodities provided through “Outsource” or “Generic” format.

• European Sourcing will grow because the market is demanding it.

• Rising Energy Costs

• Food Safety Concerns

22 ©2006 Deloitte. All rights reserved19 Apr 2023

23 ©2006 Deloitte. All rights reserved19 Apr 2023

Domestic Trends: Imperatives for FDII Members

• Cost Leadership is a MUST

• Restructure your Operating Model to reflect the changed environment– Supply Chain

– Sales & Customer Service

• Sophisticated Pricing Approach

• Embrace European Sourcing Opportunities and Threats– Be proactive!!

24 ©2006 Deloitte. All rights reserved19 Apr 2023

25 ©2006 Deloitte. All rights reserved19 Apr 2023

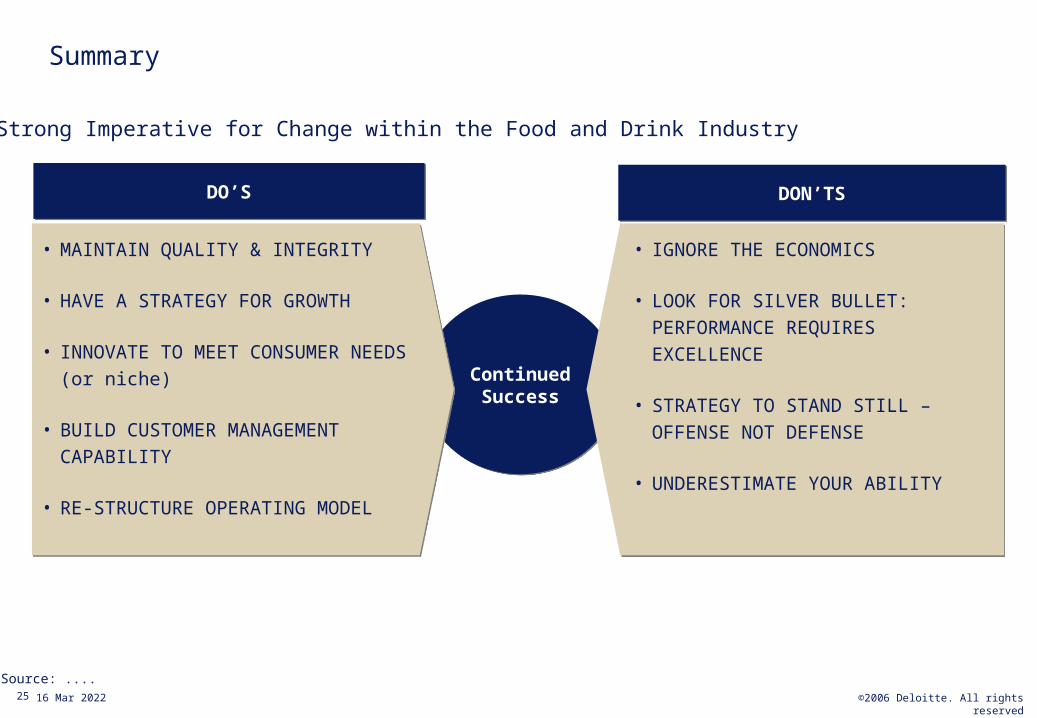

Summary

Continued Success

Continued Success

• MAINTAIN QUALITY & INTEGRITY

• HAVE A STRATEGY FOR GROWTH

• INNOVATE TO MEET CONSUMER NEEDS (or niche)

• BUILD CUSTOMER MANAGEMENT CAPABILITY

• RE-STRUCTURE OPERATING MODEL

• MAINTAIN QUALITY & INTEGRITY

• HAVE A STRATEGY FOR GROWTH

• INNOVATE TO MEET CONSUMER NEEDS (or niche)

• BUILD CUSTOMER MANAGEMENT CAPABILITY

• RE-STRUCTURE OPERATING MODEL

• IGNORE THE ECONOMICS

• LOOK FOR SILVER BULLET: PERFORMANCE REQUIRES EXCELLENCE

• STRATEGY TO STAND STILL – OFFENSE NOT DEFENSE

• UNDERESTIMATE YOUR ABILITY

• IGNORE THE ECONOMICS

• LOOK FOR SILVER BULLET: PERFORMANCE REQUIRES EXCELLENCE

• STRATEGY TO STAND STILL – OFFENSE NOT DEFENSE

• UNDERESTIMATE YOUR ABILITY

DO’SDO’S DON’TSDON’TS

Strong Imperative for Change within the Food and Drink Industry

Source: ....

26 ©2006 Deloitte. All rights reserved19 Apr 2023

27 ©2006 Deloitte. All rights reserved19 Apr 2023