Embed Size (px)

Citation preview

Changing the wheels whilst driving along Realigning sales and service networks with market developments and future customer needs

Andrew Tongue Research Director, ICDP

Norges Bilbransjeforbund, Wednesday 9th April 2014, Oslo

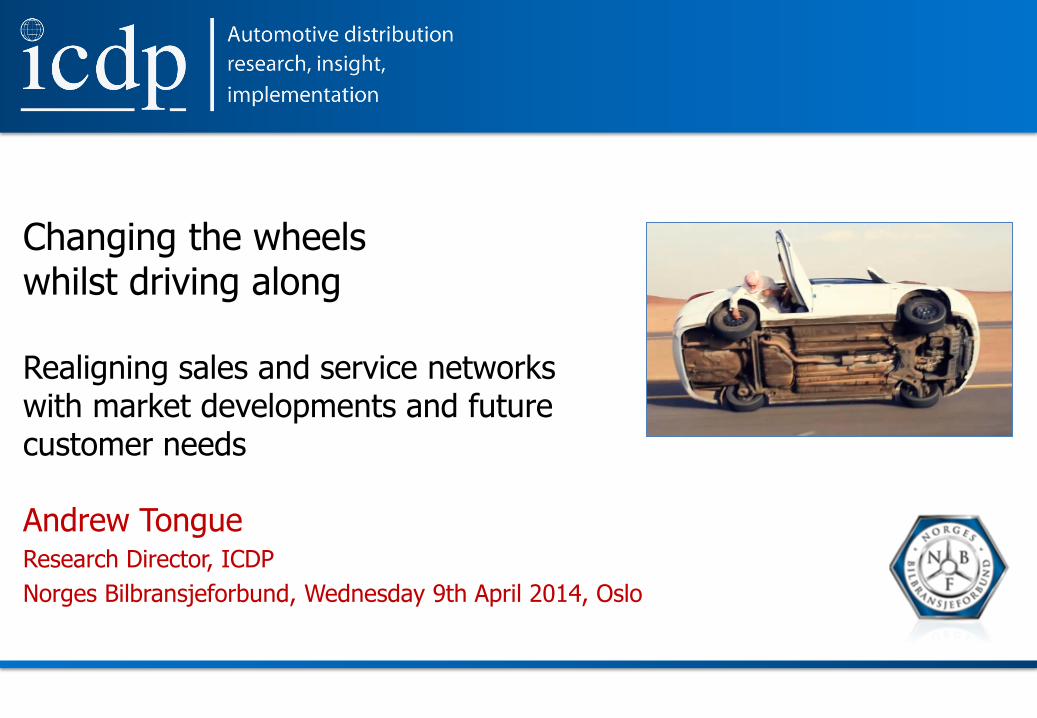

ICDP is a unique cross-auto industry research and consulting organisation focused on improving retailing and distribution, with cross-industry membership and support

Mainly European, plus Australia and expanding

globally

Research, consultancy, data services, education

and events

Sales and aftersales; manufacturers, dealers and

suppliers, associations

Members correct as of March 2014

2014 Pilot Programme

2

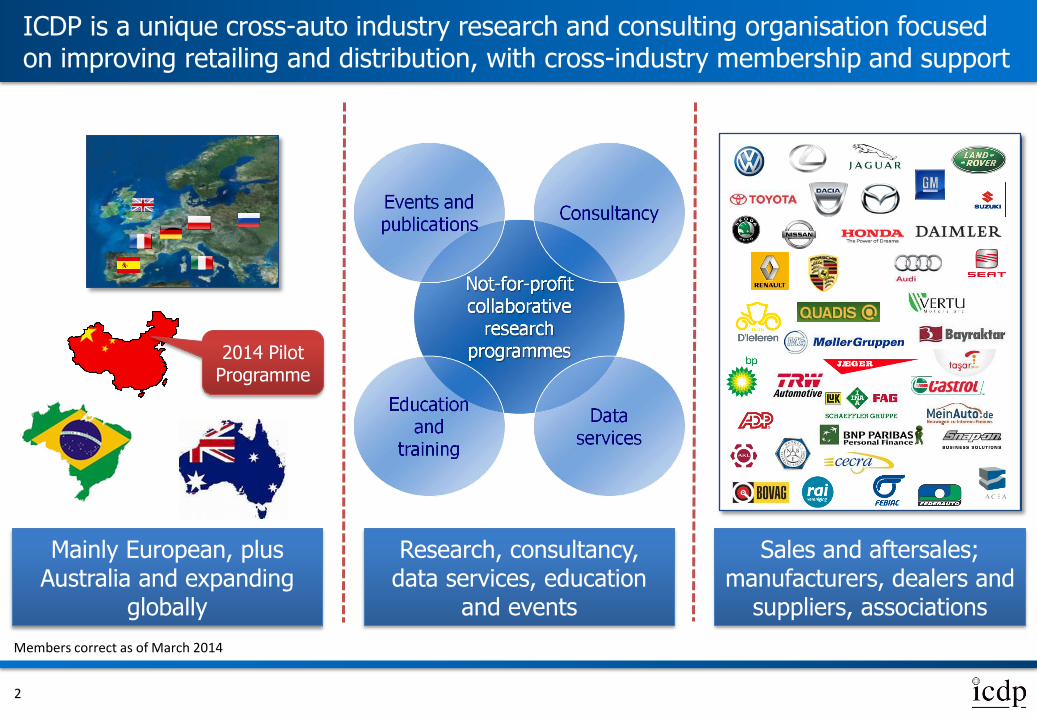

ICDP’s 2014-2015 programme focus: helping players within automotive distribution and retail plan and implement change

• Market pressures • Customer behaviour • Car usage and

service requirements • Digital world

• New approaches • New entrants • New structures • New roles and

processes

3

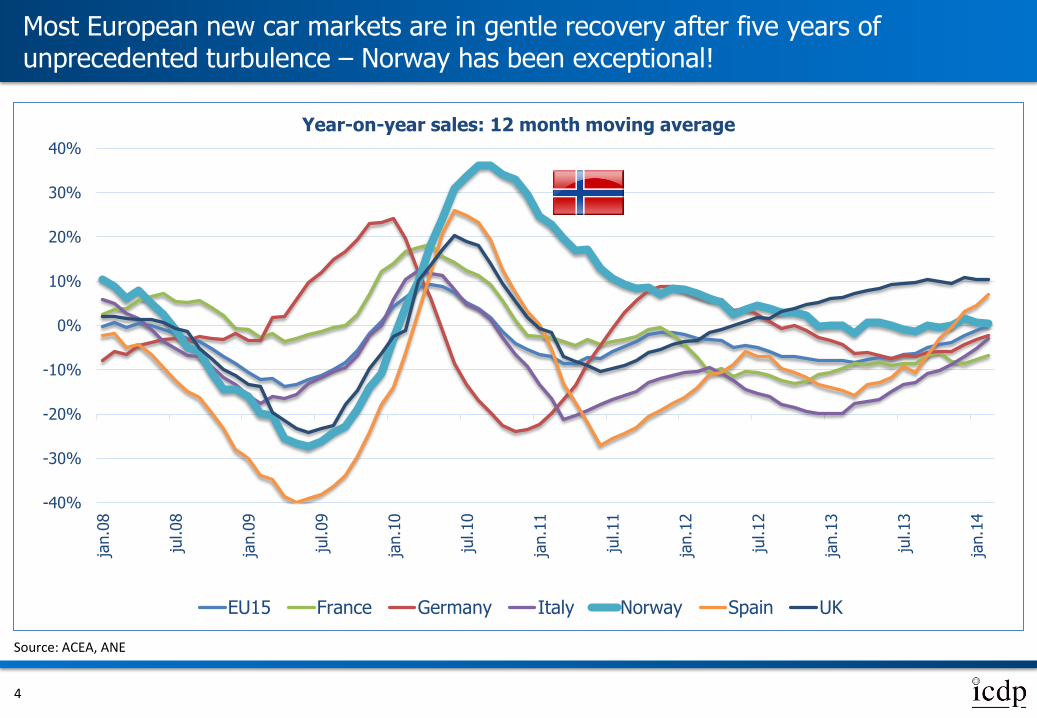

Most European new car markets are in gentle recovery after five years of unprecedented turbulence – Norway has been exceptional!

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

jan.0

8

jul.08

jan.0

9

jul.09

jan.1

0

jul.10

jan.1

1

jul.11

jan.1

2

jul.12

jan.1

3

jul.13

jan.1

4

Year-on-year sales: 12 month moving average

EU15 France Germany Italy Norway Spain UK

4

Source: ACEA, ANE

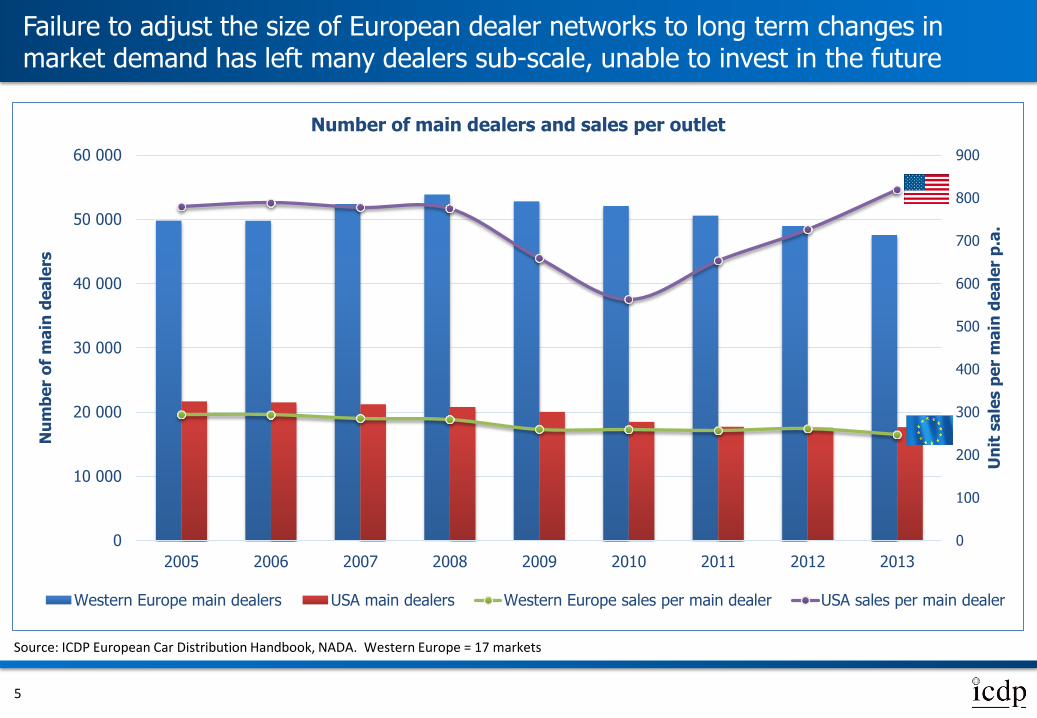

Failure to adjust the size of European dealer networks to long term changes in market demand has left many dealers sub-scale, unable to invest in the future

0

100

200

300

400

500

600

700

800

900

0

10 000

20 000

30 000

40 000

50 000

60 000

2005 2006 2007 2008 2009 2010 2011 2012 2013

Un

it s

ale

s p

er

ma

in d

ea

ler

p.a

.

Nu

mb

er

of

ma

in d

ea

lers

Number of main dealers and sales per outlet

Western Europe main dealers USA main dealers Western Europe sales per main dealer USA sales per main dealer

Source: ICDP European Car Distribution Handbook, NADA. Western Europe = 17 markets

5

The Western European new car buyer today follows a very different journey to that which would have been typical even 5 years ago; sales networks will have to adapt

Starts looking 5-6 weeks before

purchase

Visited supplying dealer twice and one competitive

brand dealer once Felt well-

prepared before any dealer visit

Conducted research on the internet

Bought with finance, part

exchanged old car

Goes back to the same dealer for

aftersales

Made one dealer contact before

visiting (typically by phone) Research included

finance and part-ex

59% contact a

dealer before visiting

42% research

finance or part

exchange online

For 36% the second

dealer visit is same brand

Grew by 22% from 2010 to 2012

59% felt well

informed before any dealer visit

75% of consumers remain loyal to supplying

dealer

Source: ICDP Consumer Survey 2013, Google reports

Owns a brand to which he/she feels quite loyal,

less dealer loyal 81% of

consumers brand loyal, 60% dealer

loyal

64% use finance,

57% part exchange

6

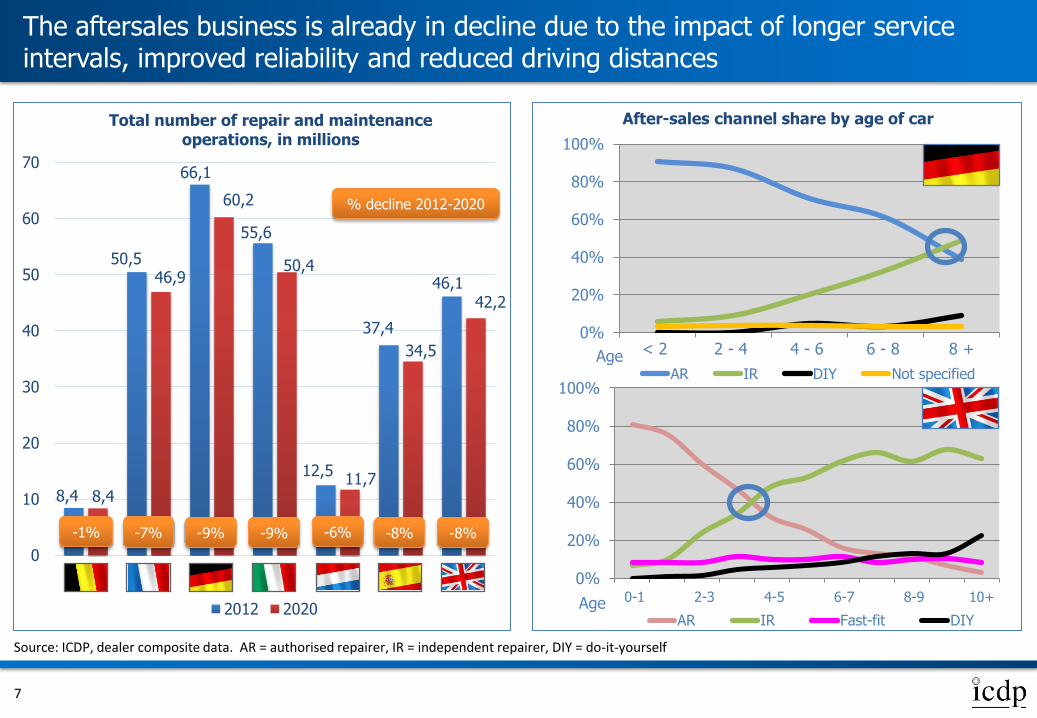

The aftersales business is already in decline due to the impact of longer service intervals, improved reliability and reduced driving distances

Source: ICDP, dealer composite data. AR = authorised repairer, IR = independent repairer, DIY = do-it-yourself

0%

20%

40%

60%

80%

100%

0-1 2-3 4-5 6-7 8-9 10+Age AR IR Fast-fit DIY

0%

20%

40%

60%

80%

100%

< 2 2 - 4 4 - 6 6 - 8 8 +Age AR IR DIY Not specified

After-sales channel share by age of car

8,4

50,5

66,1

55,6

12,5

37,4

46,1

8,4

46,9

60,2

50,4

11,7

34,5

42,2

0

10

20

30

40

50

60

70

Total number of repair and maintenance operations, in millions

2012 2020

-1% -7%

% decline 2012-2020

-9% -9% -6% -8% -8%

7

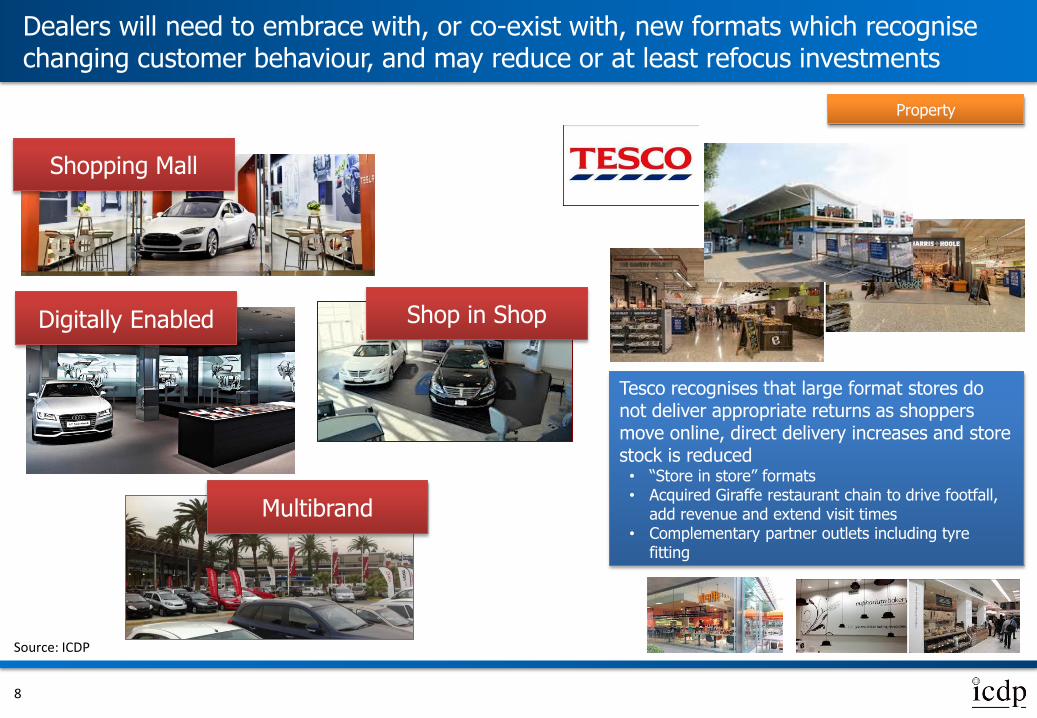

Dealers will need to embrace with, or co-exist with, new formats which recognise changing customer behaviour, and may reduce or at least refocus investments

Property

Multibrand

Digitally Enabled

Shopping Mall

Shop in Shop

Source: ICDP

Tesco recognises that large format stores do not deliver appropriate returns as shoppers move online, direct delivery increases and store stock is reduced • “Store in store” formats • Acquired Giraffe restaurant chain to drive footfall,

add revenue and extend visit times • Complementary partner outlets including tyre

fitting

8

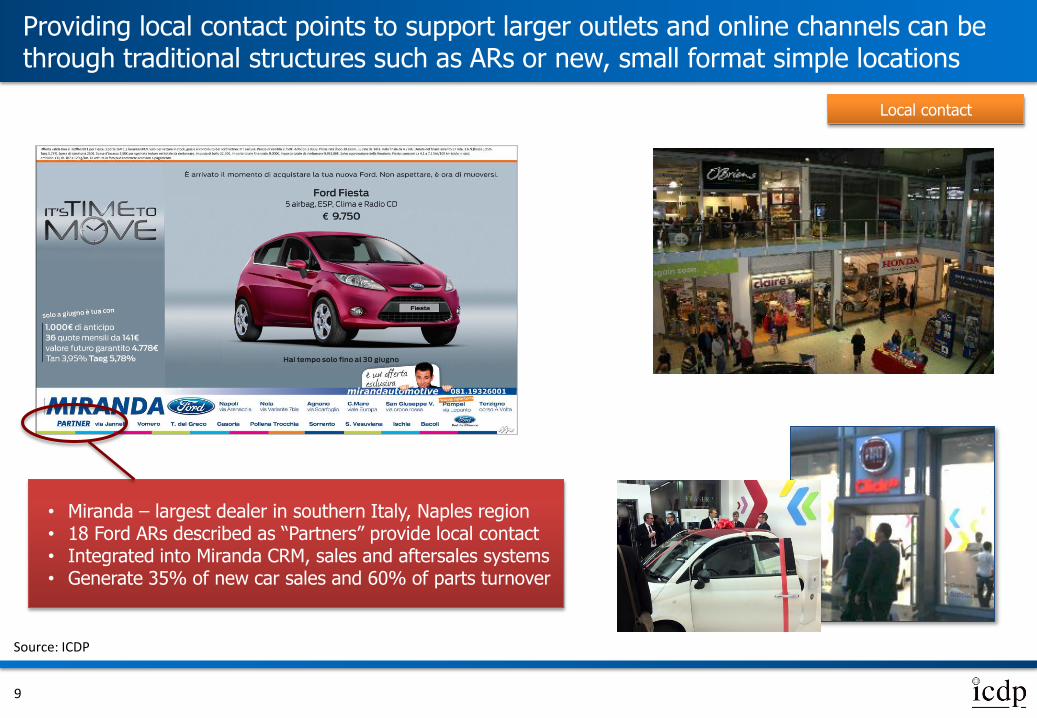

Providing local contact points to support larger outlets and online channels can be through traditional structures such as ARs or new, small format simple locations

Local contact

• Miranda – largest dealer in southern Italy, Naples region • 18 Ford ARs described as “Partners” provide local contact • Integrated into Miranda CRM, sales and aftersales systems • Generate 35% of new car sales and 60% of parts turnover

Source: ICDP

9

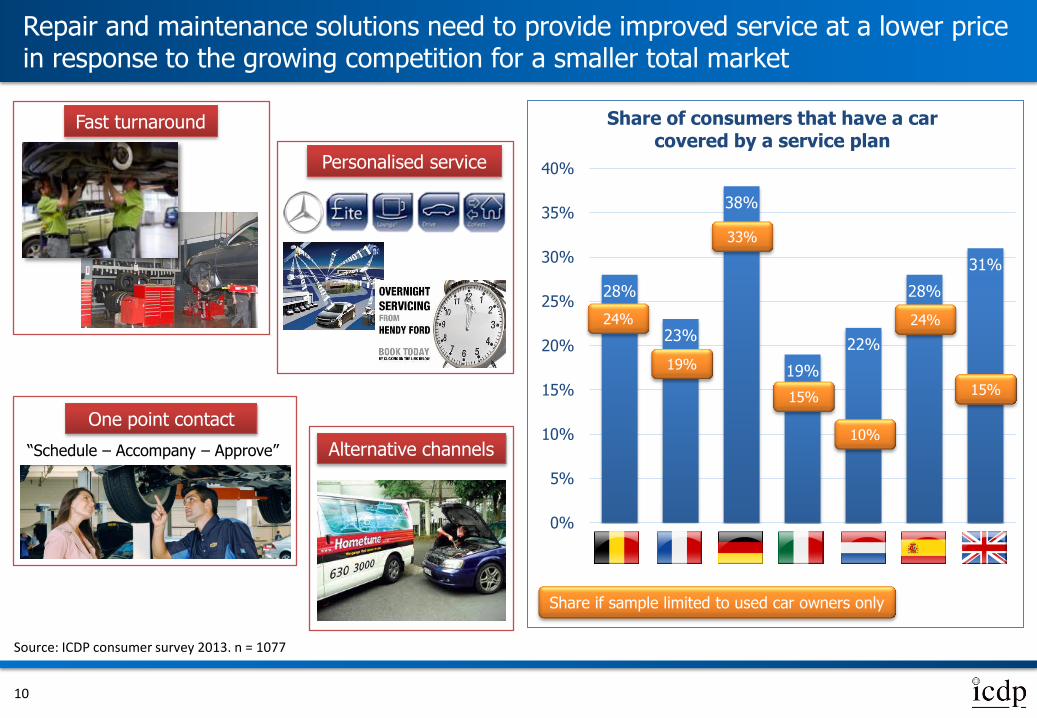

Repair and maintenance solutions need to provide improved service at a lower price in response to the growing competition for a smaller total market

10

28%

23%

38%

19%

22%

28%

31%

0%

5%

10%

15%

20%

25%

30%

35%

40%

Share of consumers that have a car covered by a service plan

19%

Share if sample limited to used car owners only

24%

33%

15%

10%

24%

15%

Source: ICDP consumer survey 2013. n = 1077

Fast turnaround

“Schedule – Accompany – Approve”

One point contact

Alternative channels

Personalised service

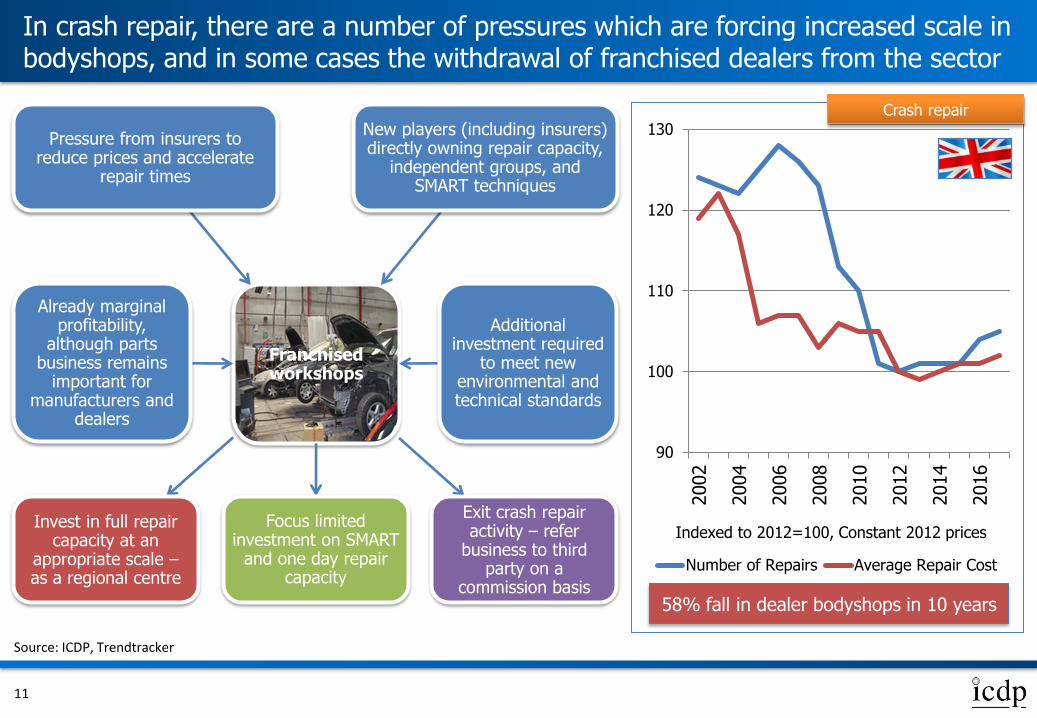

In crash repair, there are a number of pressures which are forcing increased scale in bodyshops, and in some cases the withdrawal of franchised dealers from the sector

Franchised workshops

Pressure from insurers to reduce prices and accelerate

repair times

New players (including insurers) directly owning repair capacity,

independent groups, and SMART techniques

Already marginal profitability,

although parts business remains

important for manufacturers and

dealers

Additional investment required

to meet new environmental and technical standards

Invest in full repair capacity at an

appropriate scale – as a regional centre

Focus limited investment on SMART

and one day repair capacity

Exit crash repair activity – refer

business to third party on a

commission basis

90

100

110

120

130

2002

2004

2006

2008

2010

2012

2014

2016

Number of Repairs Average Repair Cost

Indexed to 2012=100, Constant 2012 prices

Source: ICDP, Trendtracker

Crash repair

11

58% fall in dealer bodyshops in 10 years

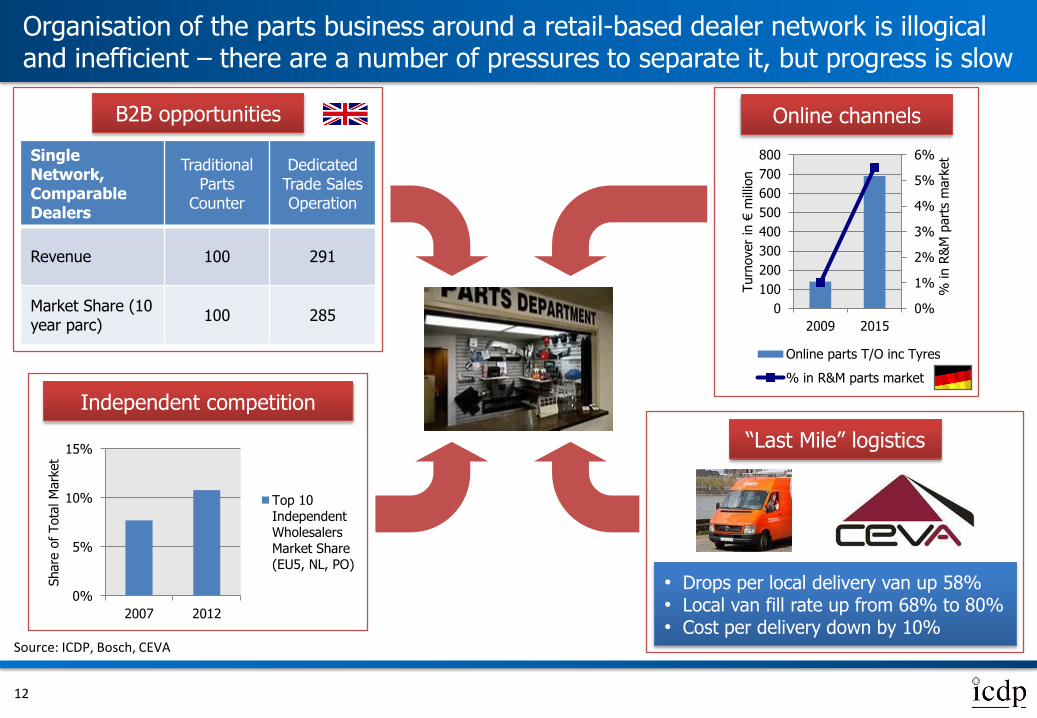

Organisation of the parts business around a retail-based dealer network is illogical and inefficient – there are a number of pressures to separate it, but progress is slow

Single Network, Comparable Dealers

Traditional Parts

Counter

Dedicated Trade Sales Operation

Revenue 100 291

Market Share (10 year parc)

100 285

Source: ICDP, Bosch, CEVA

B2B opportunities

Independent competition

0%

5%

10%

15%

2007 2012

Share

of Tota

l M

ark

et

Top 10

IndependentWholesalers

Market Share(EU5, NL, PO)

0%

1%

2%

3%

4%

5%

6%

0

100

200

300

400

500

600

700

800

2009 2015

% in R

&M

part

s m

ark

et

Turn

over

in €

mill

ion

Online parts T/O inc Tyres

% in R&M parts market

Online channels

• Drops per local delivery van up 58% • Local van fill rate up from 68% to 80% • Cost per delivery down by 10%

“Last Mile” logistics

12

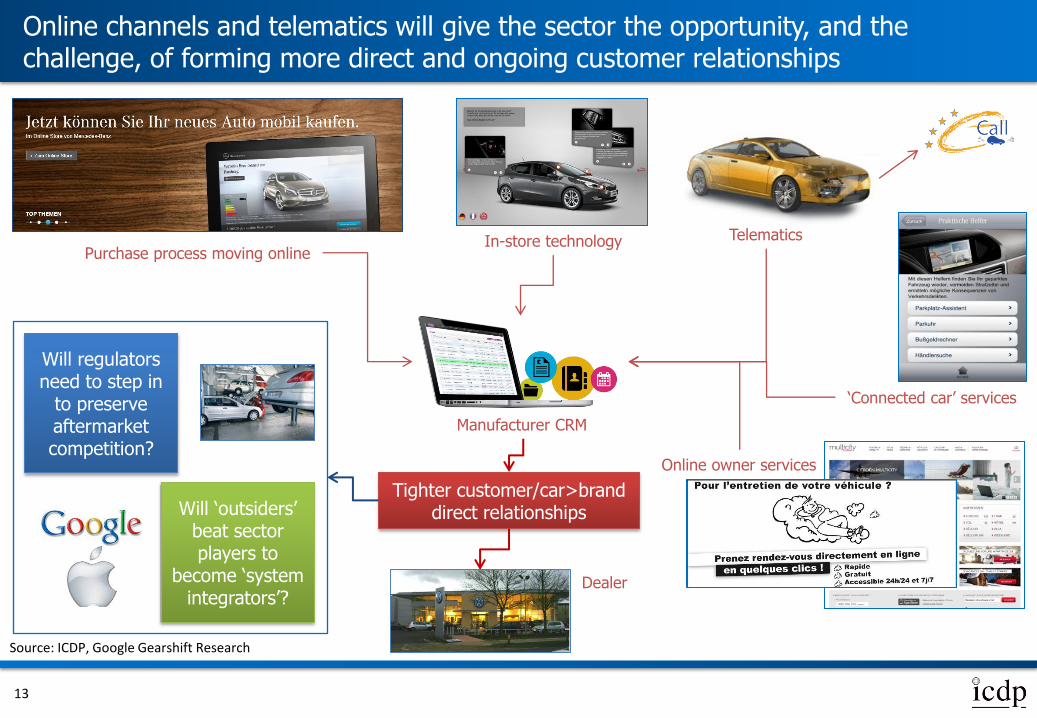

Online channels and telematics will give the sector the opportunity, and the challenge, of forming more direct and ongoing customer relationships

Source: ICDP, Google Gearshift Research

Purchase process moving online Telematics

‘Connected car’ services

In-store technology

Online owner services

Tighter customer/car>brand direct relationships

13

Manufacturer CRM

Dealer

Will regulators need to step in

to preserve aftermarket competition?

Will ‘outsiders’ beat sector players to

become ‘system integrators’?

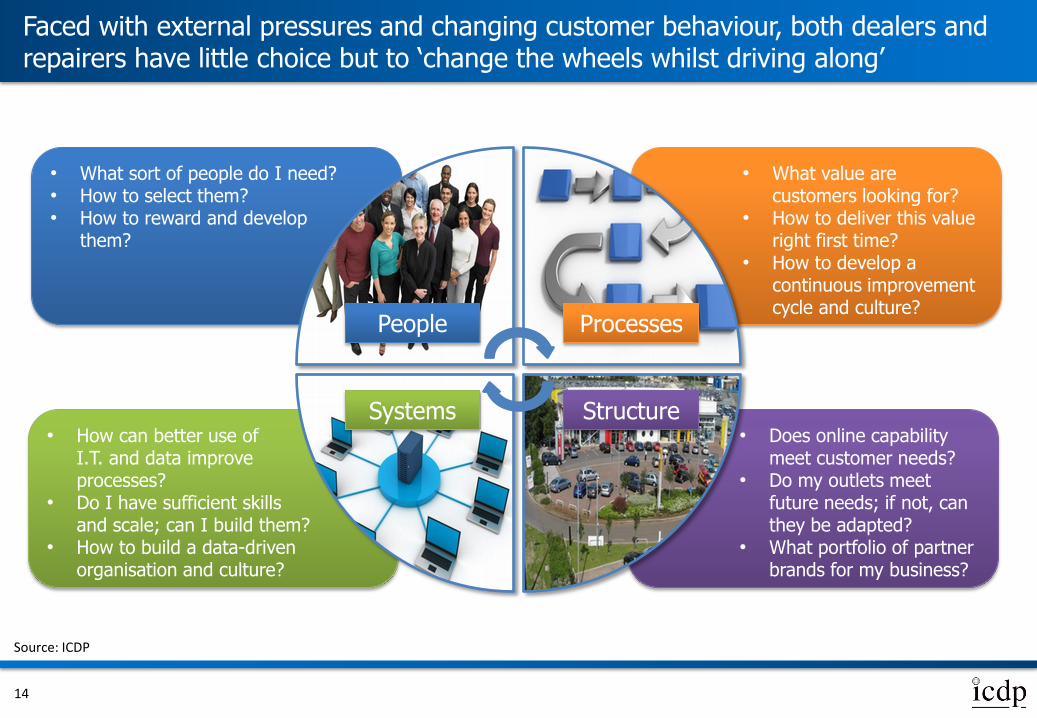

• What value are customers looking for?

• How to deliver this value right first time?

• How to develop a continuous improvement cycle and culture?

• Does online capability meet customer needs?

• Do my outlets meet future needs; if not, can they be adapted?

• What portfolio of partner brands for my business?

• What sort of people do I need? • How to select them? • How to reward and develop

them?

• How can better use of I.T. and data improve processes?

• Do I have sufficient skills and scale; can I build them?

• How to build a data-driven organisation and culture?

Faced with external pressures and changing customer behaviour, both dealers and repairers have little choice but to ‘change the wheels whilst driving along’

People Processes

Systems Structure

Source: ICDP

14

5, The Hen House, Oldwich Lane West, Chadwick End, Solihull B93 0BJ, UK

E-mail: [email protected]

Web: www.icdp.net

All requests to reproduce this material should be directed to the address above

Limited company registered in the UK, no. 2860398