Embed Size (px)

Citation preview

Chapter 1

Section 1.1

Personal Finance

Anything that involves money and you.Your allowanceThe money that you make at your jobThe money that you saveThe money that you spend

Personal Financial Planning

What is it?Is arranging to spend save and invest

money to live comfortably, have financial security and achieve goals.

Financial GoalsAre the things you want to accomplish.Going to college Buying a carSaving for your family

Write down on a sheet of paper at least 5 goals that you would like to accomplish financially in the next 20 years.

We will use these to direct ourselves through the rest of the discussion.

Steps to financial planning

1. Determine You current Financial Situation

2. Develop Your financial goals

3. Indentify Your Options

4. Evaluate your alternatives

5. Create and use your financial plan of action

6. Review and revise your plan

Determine your financial situation

Make a listHow much do you have in your savings,

checking, under your bed?How much money do you make a month

○ Job, gifts, allowance, interest incomeHow much do you spend a month on things

○ Lunch, Clothes, EntertainmentDebts

○ Who do you owe money to?

Mr . Prosser’s Current Financial Worth

Money Made Expenses

Teaching Salary - $90,000 per year

Coaching Salary - $5000 per year

Savings Account - $1000

Checking Accounts $3000

Interest per month - $100

Monthly Mortgage Payments $2000 per month

Car Payment $800 per month

Credit Card Payment $1000 per month

Rank Name Net Worth ($bil) Age Residence Source

1 William Gates III 57.0 52 Medina, WA Microsoft

2 Warren Buffett 50.0 78 Omaha, NE Berkshire Hathaway

3 Lawrence Ellison 27.0 64 Redwood City, CA Oracle

4 Jim Walton 23.4 60 Bentonville, AR Wal-Mart

5 S Robson Walton 23.3 64 Bentonville, AR Wal-Mart

6 Alice Walton 23.2 59 Fort Worth, TX Wal-Mart

6 Christy Walton & family

23.2 53 Jackson, WY Wal-Mart inheritance

8 Michael Bloomberg 20.0 66 New York, NY Bloomberg

9 Charles Koch 19.0 72 Wichita, KS manufacturing, energy

9 David Koch 19.0 68 New York, NY manufacturing, energy

11 Michael Dell 17.3 43 Austin, TX Dell

12 Paul Allen 16.0 55 Seattle, WA Microsoft, investments

13 Sergey Brin 15.9 35 Palo Alto, CA Google

14 Larry Page 15.8 35 San Francisco, CA Google

15 Sheldon Adelson 15.0 75 Las Vegas, NV casinos, hotels

15 Steven Ballmer 15.0 52 Hunts Point, WA Microsoft

15 Abigail Johnson 15.0 46 Boston, MA Fidelity

18 Jack Taylor & family 14.0 86 St Louis, MO Enterprise Rent-A-Car

19 Anne Cox Chambers 13.0 88 Atlanta, GA Cox Enterprises

20 Donald Bren 12.0 76 Newport Beach, CA real estate

Step 2 – Develop your Financial Plan

Think about your attitude toward money……Are you more likely to spend money right

now or save it?Would you rather go straight to work after

high school or are you wanting to go to college?

Your VALUES effect your financial decisions. (What do I mean by that?)

Values-

Are the beliefs and principles you consider important, correct and desirable. Different people value different things.Had friends go right to work after high

school, while others went to college. Both are successful and have families. They just believed that in order for them to be successful they had to travel their own path.

What else effects financial goals. Needs vs. Wants

Need – something you must have to survive. ○ Food, Water, Clothing (Does not that new

Versace purse either)Want – Something that you would like to

have but do not need.

You may need a new winter coat, but you may want the leather jacket……

Look back at your financial goals and determine which are needs and wants.

Lets list them on the board……

Step 3 – Identify your OptionsPretend that I gave you an extra $50.00

per week. What are your options?1. EXPAND YOUR CURRENT SITUATION -You could take

that extra $50 and put it into savings and even save more a month.

2. CHANGE YOUR CURRENT SITUATION - You could invest the money in the stock market to try to make more money.

3. START SOMETHING NEW - could pay off some debt the you may have acquired.

4. CONTINUE THE SAME COURSE OF ACTION – Chose not to do anything with the money.

Step 4 – Evaluate your alternatives. You need to look at your situation in life,

your present financial situation, and your personal values. For each situation that deals with money you need to consider the consequences and risks that come with each decision.

Step 4 – Evaluate your alternatives. What can help you make these decisions

Average Salary Financial Specialists

○ Accountants, bankers, financial planners Use the internet

○ Computer software can help you determine if you are getting in to deep into debt.Mortgage calculatorsIncome calculators

- http://www.disposableincome.net/ Books and magazines Financial Institutions Your education

Step 4 – Evaluate your alternatives. What are the consequences of your

choices…..Opportunity cost – a trade off, is what is

given up when making one choice instead of another. ○ Going to college instead of going right to work

and making money.

Step 4 – Evaluate your alternatives. What are the risks of making that decision. Though the risk may not be extremely dramatic there are

different types of risk to think about. Inflation risk – the cost of an item may increase next

year. Interest Rate Risk – may effect the cost of you borrowing

money Income Risk – you may loose your job, or may not get

that raise you hoped for. Personal Risk – The job you may do may be dangerous,

or the option of you driving a car to somewhere versus flying.

Liquidity Risk – How quickly can you convert this good into cash.

Step 5 – Create the plan of action. What are you going to do to achieve

your plan of action.Spend lessGet a second jobPay off debts

Step 6 – Review and Revise.

Look at your goals

Goals are set into three categoriesShort- Term – can be achieved in one yearIntermediate – 2 to 5 yearsLong-term – more than 5 years to achieve.

Go and categorize your goals on your sheet of paper.

Goals for different needs

Def – of need – something you need to survive.

Your financial goals are set on the types of things that you buy.Services – something that someone does

for you. Plumber, hair stylist provide services for you.

Goods – physical items that are produced and can be weighed or measured.

Types of goods Consumable goods – purchases that you make

often and use up quickly. Food, toothpaste etc. Thought the cost of these goods may not measure up to a cost of a car they do add up..

Durable Goods – are expensive items that you do not purchase often. Cars, appliances (refrigerators, stoves)

Intangible items – cannot be touched but are often important to our well-being and happiness. Happiness at your job, health, education, and free time,

and be very expensive.

S.M.A.R.T.

Specific ? Measurable? Attainable? Realistic? Timely?

Influences on Personal Financial Planning What types of things are going to

influence you personal finances in the future?Life SituationsPersonal SituationsEconomic Factors

Life Situations How long will you live? Going to College -

Starting a new career Getting married Having children Moving to a new city…

http://cgi.money.cnn.com/tools/costofliving/costofliving.html

Personal Situations

Choosing to move out of the house away from the parents.Average cost of rent in St. Louis $700 and

$800

Paying the bills that come with the move

Personal Situations

Choosing to move out of the house away from the parents.Average cost of rent in St. Louis $700 and

$800

Paying the bills that come with the move Do you want to be a millionaire?

Millionaire calculator

Economic Situations

EconomicsSomething you hear about everyday in the

news.The study of the decisions that go into

making, distributing, and using goods and services.

The Economy○ Is the actual “market” or ways in which we

make, distribute, and use goods and services.

Other Economic factors that effect personal decisions Supply vs. Demand

Supply – is the amount of goods and services you purchase

Demand – is the amount of goods and services people are willing to buy.

Three Final Economic Conditions that hit closer to home.1. Consumer Prices

2. Consumer Spending

3. Interest Rates

Consumer Prices

Most products increase in price over time.

This increase in price is called INFLATION.

During times of rapid inflation it takes more money to buy the same amount of good or service.

EX. A computer that cost $1000 a year ago may cost $1050 now.

Consumer Prices continued What causes inflation?

People have more money to spend on items without a increase in supply.

Remember the FED has something to do with this as well. When interest rates are low, people have a tendency to spend more money and inflation goes up…

When interest rates are high, people put money in the bank to save and interest rates go down.

2. Consumer Spending

You are a consumer and when you purchase and item. That company that produced the item makes money and hires more employees to make more products. This then increase our employment rate. More people work and spend more money. However the opposite can happen as well.

3. Interest Rates

Money has a price, that price is called interest…..

Interest – is the cost that people pay for to use other people money..

Here is how this all works….When you take grandmas birthday check and

deposit it into the bank, and the bank gives you an interest rate, they are paying you to let them use your money. The bank inturn takes your money and lends it to people who want to borrow money form the bank.

When the supply of money in the bank grows interest rates go down. People are saving more.

When consumers borrow more money, then interest rates go up.

Interest rates on loans also rise during inflation.

Section 1.2

Opportunity Cost and Strategies

Opportunity Cost

When you give up something to do something else.

Different types of Opportunity CostsPersonalFinancial

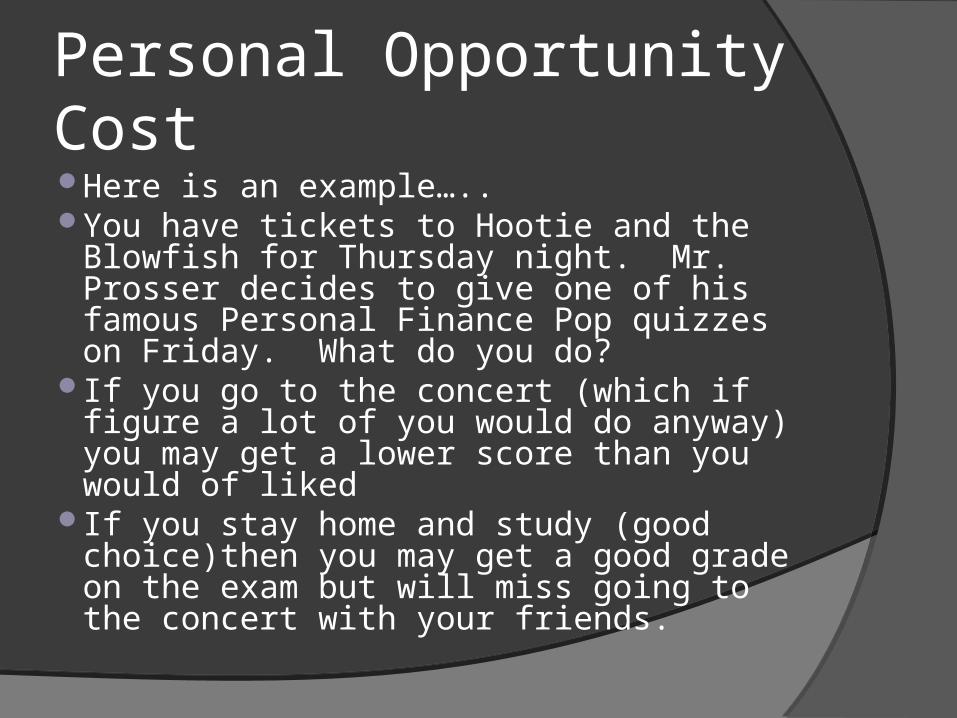

Personal Opportunity CostHere is an example…..You have tickets to Hootie and the Blowfish

for Thursday night. Mr. Prosser decides to give one of his famous Personal Finance Pop quizzes on Friday. What do you do?

If you go to the concert (which if figure a lot of you would do anyway) you may get a lower score than you would of liked

If you stay home and study (good choice)then you may get a good grade on the exam but will miss going to the concert with your friends.

Financial Opportunity Cost Here is an example.

You see the new set of shoes at the mall for $150. You decide to buy those. You could of used that money on the car insurance that is due next month or put it into the bank and save it……

Financial Opportunity Cost If you would of put the money into the

bank it could gain INTEREST. Definition of Interest?

Is the extra money earned from the bank using your money.

How do we calculate interest?○ Principal X Rate X Time = Interest

Interest

PrincipalIs the original amount you deposited into the

bank for a savings account.You put $2000 into the bank at the end of

one year how much money do you have if the interest is 3%.

2000 x 3% = $60So at the end of the year you will have

$2060$2000 + $60 = $2060

Simple Interest practice problems

Principal Rate Interest

200 2%

300 3%

500 4%

1000 6%

1200 7%

For now we are assuming that it is just for one yearLets look at Part 4 of the handout

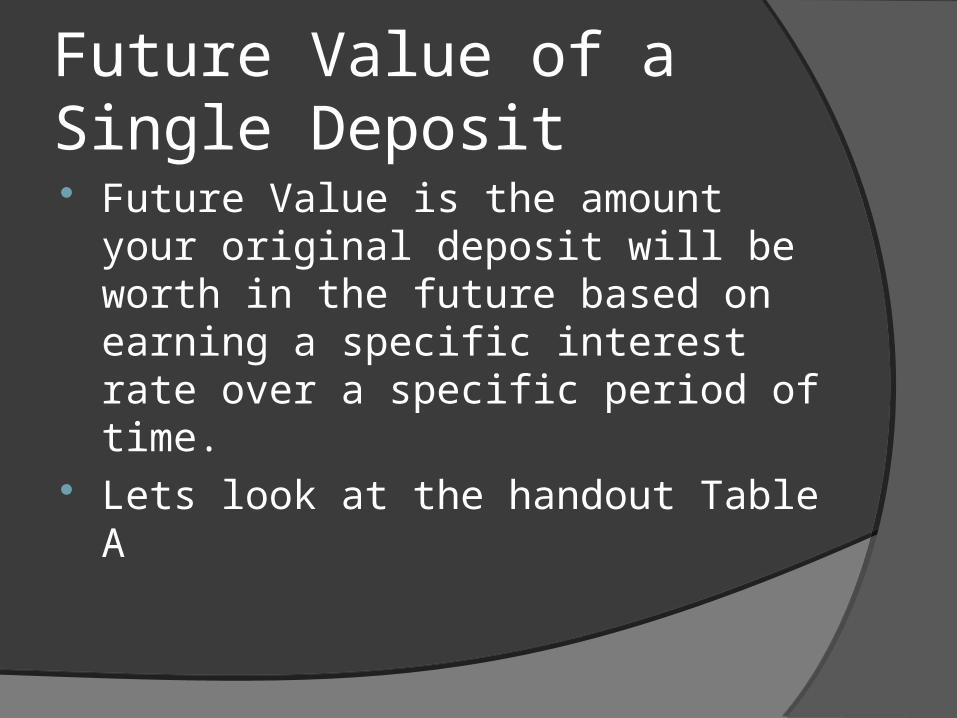

Future Value of a Single Deposit Future Value is the amount your original

deposit will be worth in the future based on earning a specific interest rate over a specific period of time.

Lets look at the handout Table A

Future Value of a Series of Deposits Sometimes instead of putting a large

amount in at the beginning of the year, you put smaller amounts throughout the year.

When you make a series of equal regular deposits is called an annuity.

Sample Problems for future value

Principal Years Rate Total

200 6 7&

400 8 5%

1000 5 8%

500 7 6%

Present Value of a Single Deposit Present value – If you want to have $1000 in 5 years

and the interest rate is 5%. How much will you need to deposit now to accumulate that $1000.

Remember that this is one lump sum and then you put it into an account and let it sit there.

Again using the table on page 23 will help us. Using the table and the information we have how

much do we need to deposit now. We want to have $1000 in 5 years with 5% interest. $1000 x .784 = $784 would need to be deposited

now.

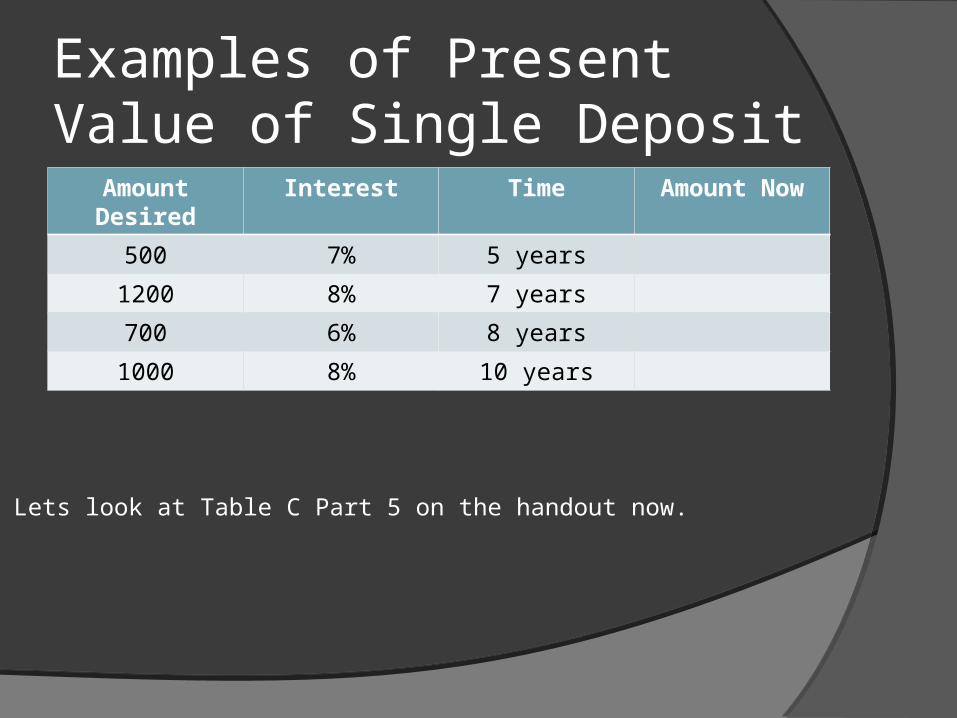

Examples of Present Value of Single Deposit

Amount Desired

Interest Time Amount Now

500 7% 5 years

1200 8% 7 years

700 6% 8 years

1000 8% 10 years

Lets look at Table C Part 5 on the handout now.

Present Value having yearly withdraws from your account. You can also use present value to calculate how much

you would need to deposit so you can take a specific amount of money out of your savings account for a certain number of years.

If you want to take $400 out of your account each year for nine years, and your money is earning interest at 8% a year. How much money would you need to deposit now.

$400 x 6.247 = $2498.80 This would be how much you would have to put into

the bank if you wish to deposit 400 per year. Many people use this to determine how much they will

have for retirement.

Present Value with yearly withdrawals example

Withdrawal amount per

year

Interest No. of Years Amount Deposited

200 9% 5

500 6% 9

1000 5% 7

600 8% 8

800 7% 6

Lets look at Part6 or Table D

What did it cost then to now??

2007 Cost Gallon of Milk $3.12 Gallon of Gas $2.56 Tube of Toothpaste $5.00 Lawnmower $235 Alarm Clock $25 Loaf of Bread $1.00 Stapler $19.95 Pair of Shoes $85 Car $22,000 $225,000 Home

1980’s CostGallon of Milk $1.23

Gallon of Gas 1.01

Tube of Toothpaste $1.98

Lawnmower $92.96

Alarm Clock $9.89

Loaf of Bread $.40

Stapler $7.89

Pair of Shoes $33.62

Car $8.702.87

Home $89000.67

http://data.bls.gov/cgi-bin/cpicalc.pl Back

![Subject cans [ all money that you win is not reality]](https://img.pdfslide.net/doc/110x75/568151ac550346895dbfdb72/subject-cans-all-money-that-you-win-is-not-reality.jpg)