Embed Size (px)

Citation preview

Chapter 10

Payroll Computations, Records, and Payment

Payroll Laws & Taxes

Employee vs. independent contractorFederal Employee Earnings &

Withholding Laws Fair Labor Standards Act of 1938 Social Security Tax Medicare Tax Federal Income Tax

State & Local Taxes

Employer’s Payroll Taxes & Insurance Costs Social Security Tax (FICA) Medicare Tax Federal Unemployment Tax (FUTA) State Unemployment Tax (SUTA) Workers’ Compensation Insurance

Calculating Earnings & Taxes

Computing Employee Total EarningsHourly rate basisSalary basisCommission basisPiece-rate basis

Hourly Employees

Need two pieces of data from weekly time sheets, time cards, etc. Number of hours worked Rate of Pay

Gross Pay Regular rate Overtime rate – 1½ times regular rate

Withholdings for Hourly Employees Required by Law

FICA (Social Security) 6.2% on the first $76,200

Medicare 1.45%

Federal income tax Use wage-bracket table method

• # of withholding allowances (W-4) • Total earnings during pay period

Withholdings Not Required by Law

Group life insuranceGroup medical insuranceCompany retirement plansBank or credit union savings plansLoan repaymentsSavings bonds, stocks, investment plansUnion dues

Determining Pay for Salaried Employees

Hours Worked Salaried workers who do not hold supervisory jobs

- covered by the Wage & Hour Law Salaried workers who hold supervisory or

managerial positions – are exempt from the Wage & Hour Law

Withholdings required by law Same procedures for salaried or hourly

employees.

Recording Payroll for Employees

Payroll RegisterAllowances Marital StatusCumulative EarningsNo. of hours workedRate or Salary

Recording Payroll for Employees

Payroll Register Continued Earnings

• Regular – Overtime – Gross - Cumulative Taxable Wages

• Social Security - Medicare – FUTA Deductions

• SS – Medicare – Income Tax - Other Distribution

• Net Amount – Check # - Type

Recording Payroll Information

Two separate journal entries: Record the payroll expense for the

employer Payment to the employees

• Can be written on the regular bank account• Individual payroll checks issued from a payroll

bank account

Individual Earnings Record

Individual Earnings record is created for each employee Also called a compensation record Shows all the payroll information for one

person through his employment history

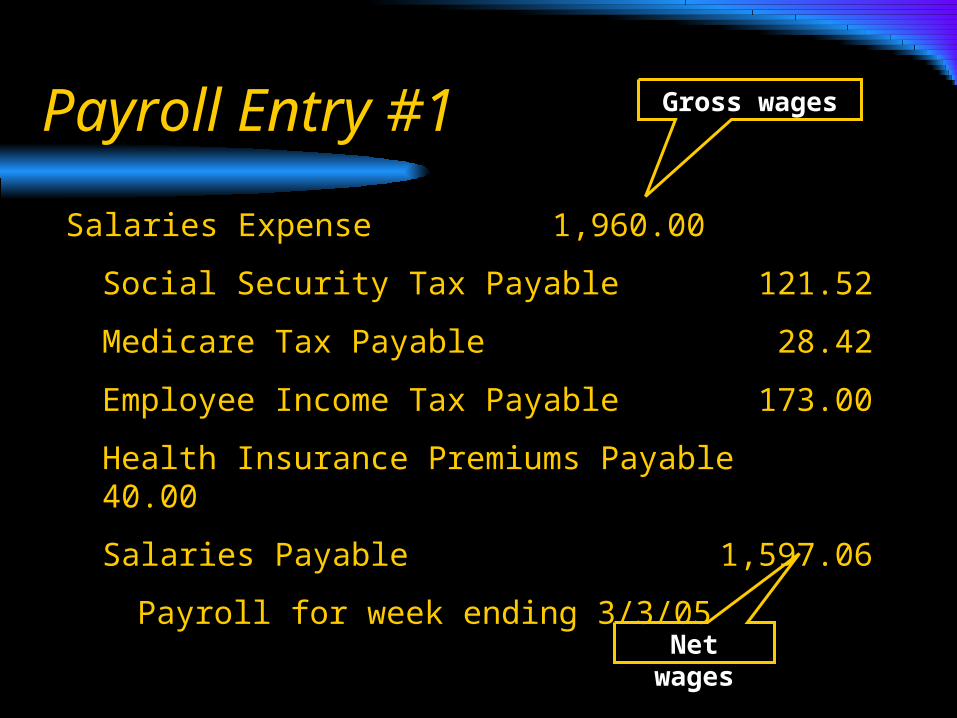

Payroll Entry #1

Salaries Expense 1,960.00

Social Security Tax Payable 121.52

Medicare Tax Payable 28.42

Employee Income Tax Payable 173.00

Health Insurance Premiums Payable 40.00

Salaries Payable 1,597.06

Payroll for week ending 3/3/05

Gross wages

Net wages

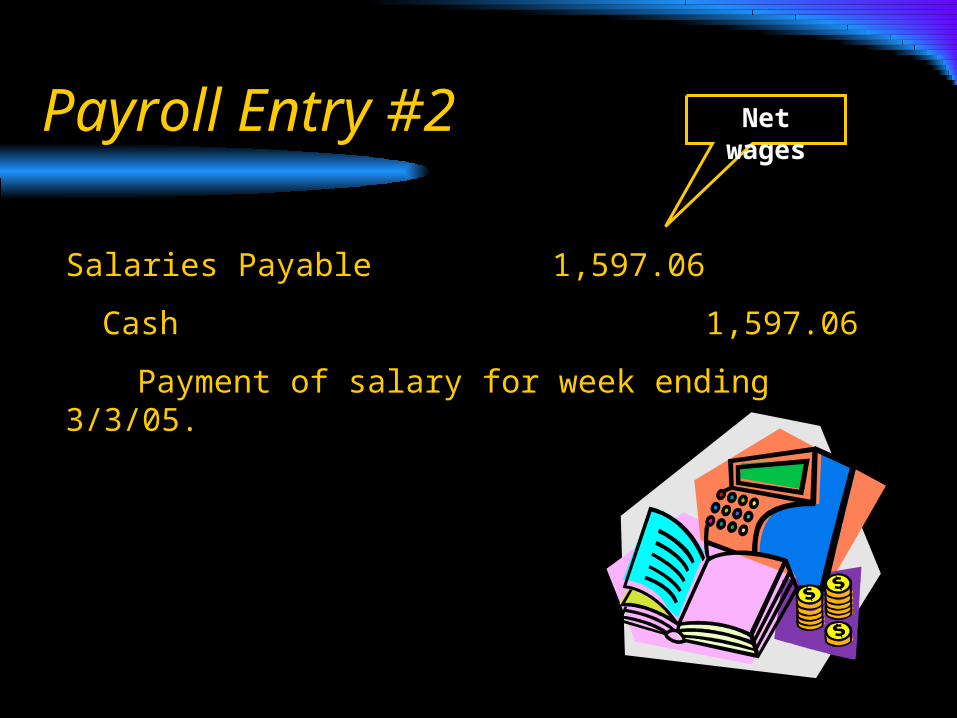

Payroll Entry #2

Salaries Payable 1,597.06

Cash 1,597.06

Payment of salary for week ending 3/3/05.

Net wages

Completing the Payroll

The two payroll journal entries below must be posted to the ledger accounts. To record the employer’s share of the

payroll, and To record the payment of payroll to the

employees

Learning Objectives Explain the major federal laws relating to employee

earnings and withholding Compute gross earnings of employees Determine employee deductions for social security tax Determine employee deductions for Medicare tax Determine employee deductions for income tax Enter gross earnings, deductions, and net pay in the

payroll register Journalize payroll transactions in the general journal Maintain an earnings record for each employee Define the accounting terms new to this chapter