Embed Size (px)

Citation preview

Chapter 10

Sovereign Risk

10-2

Overview • This chapter explores the risks FIs face when dealing

with foreign governments.• We compare and contrast credit and sovereign risk.• We examine the concept of debt repudiation and debt

rescheduling.• We learn about techniques for evaluating a country’s

risk profile and ratios that can estimate the financial health of an economy.

• We examine secondary markets for bonds issued by developing countries and the techniques available to address defaults.

Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Financial Institutions Management 2e, by Lange, Saunders, Anderson, Thomson and CornettSlides prepared by Maike Sundmacher

10-3

Introduction• Increased lending activities to less developed

countries (LDCs) in the 1970s resulted in large losses in the 1980s:– Debt repayment problems in 1980s: Poland and other

Eastern European countries.– Debt moratoria in 1982: Mexico and Brazil.

• Late 1980s / early 1990s, new large lending wave by US banks in form of debt and equity claims, followed by devaluation of Mexican peso.

• Emerging Asian markets faltered in 1997.• These examples highlight the importance of country

risk or sovereign risk assessment.

Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Financial Institutions Management 2e, by Lange, Saunders, Anderson, Thomson and CornettSlides prepared by Maike Sundmacher

10-4

Credit Risk versus Sovereign Risk• Credit risk is dependent on the ability and willingness

of the borrower to repay the loan.

• Governments can impose restrictions on debt repayments to outside creditors:– Loan may be forced into default even though borrower

had a strong credit rating when loan was originated.

– Legal remedies are very limited.

Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Financial Institutions Management 2e, by Lange, Saunders, Anderson, Thomson and CornettSlides prepared by Maike Sundmacher

10-5

Credit Risk versus Sovereign Risk• Sovereign risk is dependent on both:

– The willingness and the ability of the borrower to repay the loan,

– The probability that the Government of the country in which a foreign borrower operates will allow the repayment of foreign debt.

• Lending decisions to parties in foreign countries require two steps:1. Credit quality assessment of borrower,

2. Sovereign risk quality assessment of country.

Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Financial Institutions Management 2e, by Lange, Saunders, Anderson, Thomson and CornettSlides prepared by Maike Sundmacher

10-6

Debt Repudiation versus Debt Rescheduling

Debt Repudiation:• Outright cancellation of current and future debt

obligations by a borrower.• Examples:

– China (1949),– Cuba (1961),– North Korea (1964).

• 1996: World Bank, IMF and major governments around the world forgave the debt of the world’s poorest, most heavily indebted countries (HIPCs).

Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Financial Institutions Management 2e, by Lange, Saunders, Anderson, Thomson and CornettSlides prepared by Maike Sundmacher

10-7

Debt Repudiation versus Debt Rescheduling

Debt Rescheduling:• Changing the contractual terms of a loan, such as its

maturity and interest payments.• Most common form of sovereign risk event.• Example: debt moratoria.• Payment delays can refer to either:

– Principal repayment, or– Interest payments.

Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Financial Institutions Management 2e, by Lange, Saunders, Anderson, Thomson and CornettSlides prepared by Maike Sundmacher

10-8

Debt Repudiation versus Debt Rescheduling• Pre–Second World War: debt problems

predominantly met with debt repudiation.• Post–Second World War: debt problems

predominantly met with debt rescheduling.• Potential reasons:

– Post-war financing was mainly through bank loans rather than foreign bonds (major financing method pre-war).

– Rescheduling for loans is easier and cheaper due to lower number of FIs participating in negotiations,

– FI cohesiveness in loan renegotiations,

Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Financial Institutions Management 2e, by Lange, Saunders, Anderson, Thomson and CornettSlides prepared by Maike Sundmacher

10-9

Debt Repudiation versus Debt Rescheduling

• Potential reasons (continued):– Many loan contracts contain ‘cross-default

provisions’,– Public policy goals of some Governments aim to

avoid large FI failures (especially in developed countries),

– Perception of higher social cost on bank loan defaults compared to defaults on bonds.

– Specialness of banks argues for rescheduling, but there are incentives to default again if bailouts are automatic.

10-10

Country Risk EvaluationOutside Evaluation Models – The Euromoney Index:• Published in 1979.• Originally based on spread in Euromarket of the

required interest rate in a country’s debt over LIBOR.• More recently, replaced by index based on:

– Large number of economic and political factors,– Subjective weighting (relative importance).

Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Financial Institutions Management 2e, by Lange, Saunders, Anderson, Thomson and CornettSlides prepared by Maike Sundmacher

10-11

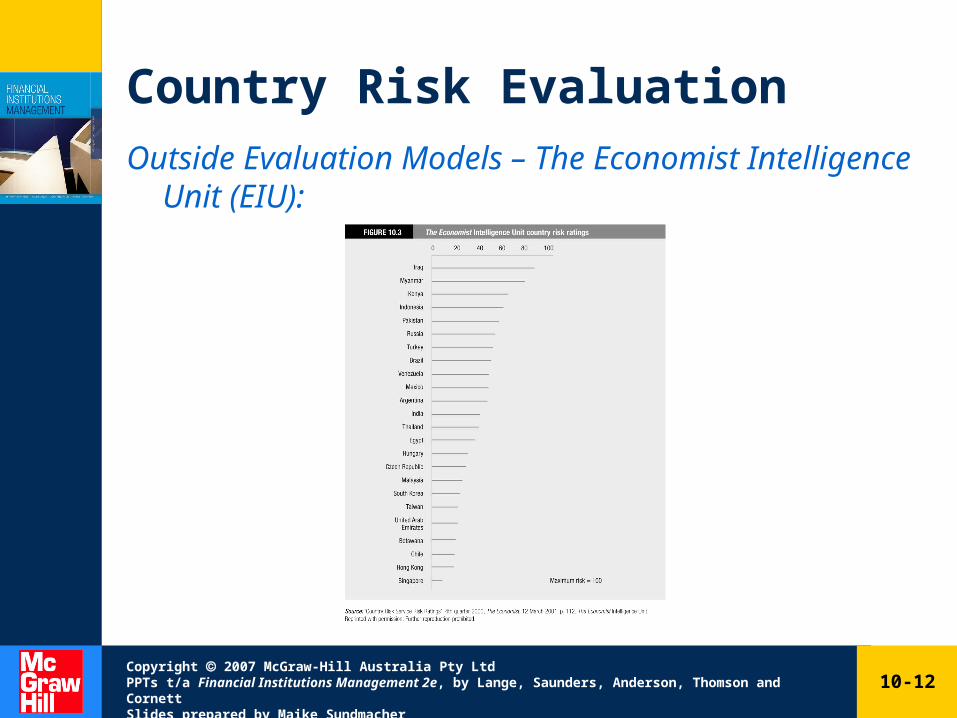

Country Risk EvaluationOutside Evaluation Models – The Economist

Intelligence Unit (EIU):• Rating through combination of economic and political

risk.• Maximum 100 point scale.• The higher the number, the worse the sovereign risk

rating.

• See: www.economist.com

Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Financial Institutions Management 2e, by Lange, Saunders, Anderson, Thomson and CornettSlides prepared by Maike Sundmacher

10-12

Country Risk EvaluationOutside Evaluation Models – The Economist

Intelligence Unit (EIU):

Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Financial Institutions Management 2e, by Lange, Saunders, Anderson, Thomson and CornettSlides prepared by Maike Sundmacher

10-13

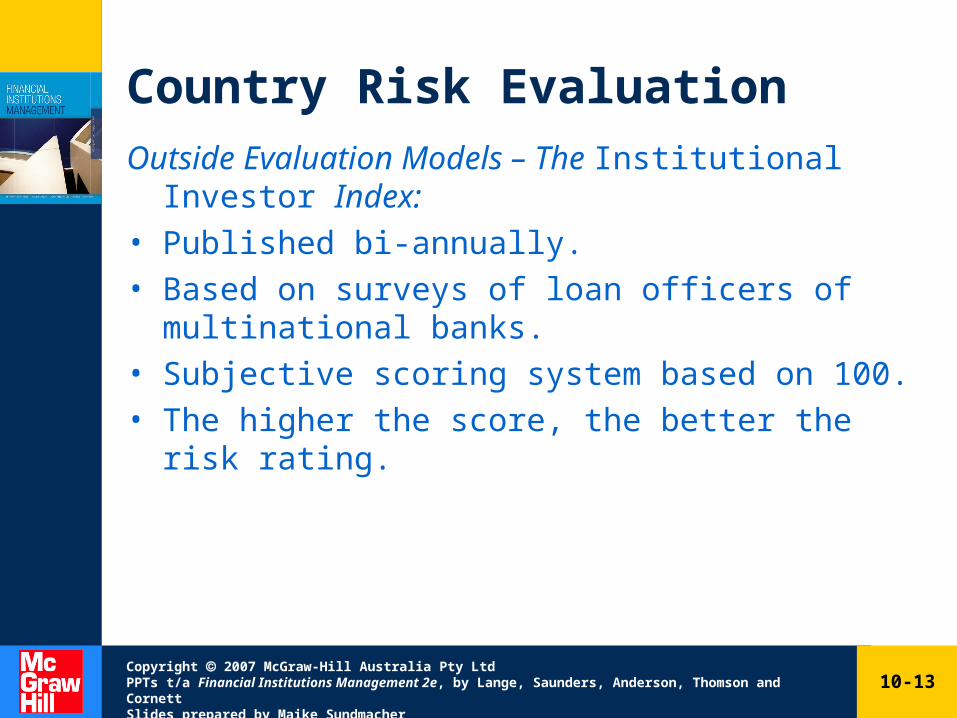

Country Risk EvaluationOutside Evaluation Models – The Institutional Investor

Index:• Published bi-annually.• Based on surveys of loan officers of multinational

banks.• Subjective scoring system based on 100.• The higher the score, the better the risk rating.

Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Financial Institutions Management 2e, by Lange, Saunders, Anderson, Thomson and CornettSlides prepared by Maike Sundmacher

10-14

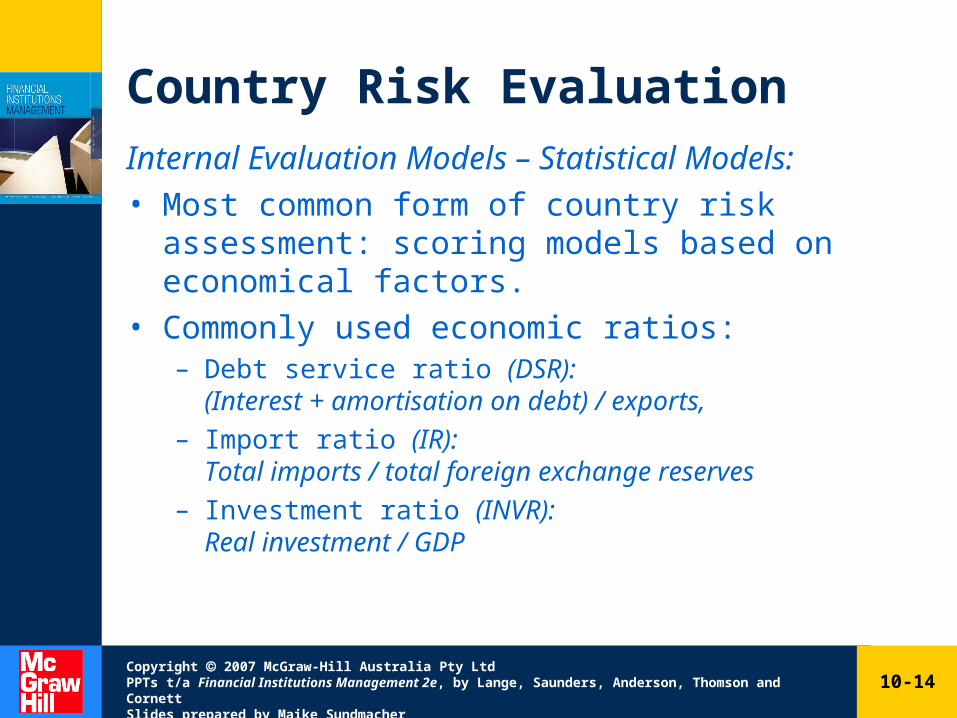

Country Risk EvaluationInternal Evaluation Models – Statistical Models:• Most common form of country risk assessment:

scoring models based on economical factors.• Commonly used economic ratios:

– Debt service ratio (DSR): (Interest + amortisation on debt) / exports,

– Import ratio (IR): Total imports / total foreign exchange reserves

– Investment ratio (INVR): Real investment / GDP

Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Financial Institutions Management 2e, by Lange, Saunders, Anderson, Thomson and CornettSlides prepared by Maike Sundmacher

10-15

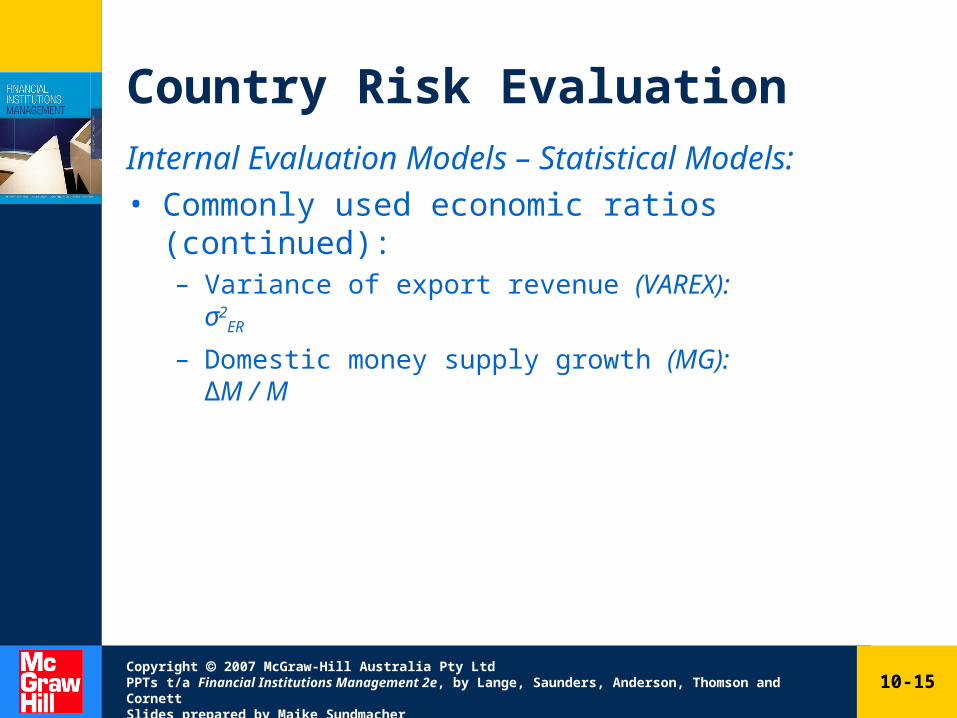

Country Risk EvaluationInternal Evaluation Models – Statistical Models:• Commonly used economic ratios (continued):

– Variance of export revenue (VAREX):σ2

ER

– Domestic money supply growth (MG):∆M / M

Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Financial Institutions Management 2e, by Lange, Saunders, Anderson, Thomson and CornettSlides prepared by Maike Sundmacher

10-16

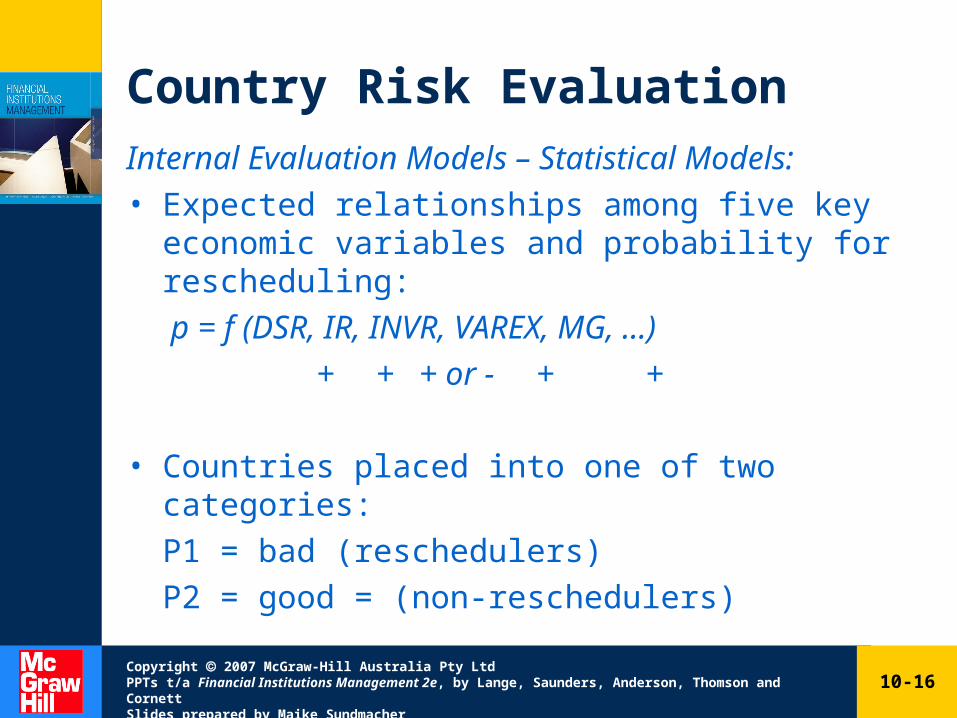

Country Risk EvaluationInternal Evaluation Models – Statistical Models:• Expected relationships among five key economic

variables and probability for rescheduling:

p = f (DSR, IR, INVR, VAREX, MG, …)

+ + + or - + +

• Countries placed into one of two categories:

P1 = bad (reschedulers)

P2 = good = (non-reschedulers)

Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Financial Institutions Management 2e, by Lange, Saunders, Anderson, Thomson and CornettSlides prepared by Maike Sundmacher

10-17

Country Risk EvaluationProblems with Statistical CRA Models:

• Measurements of key variables.

• Population groups– Finer distinction than reschedulers and non-reschedulers

may be required.

• Political risk factors:– Strikes, corruption, elections, revolution.

• Portfolio aspects: systematic versus unsystematic risk.

• Incentive aspects of rescheduling:– Cost and benefits for borrowers and lenders.– Stability: model likely to require frequent updating.

Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Financial Institutions Management 2e, by Lange, Saunders, Anderson, Thomson and CornettSlides prepared by Maike Sundmacher

10-18

Using Market Data to Measure Risk: The Secondary Market for LDC Debt

Market Structure:• Secondary market has enhanced liquidity of LDC

loans.• Sellers:

– Large FIs willing to accept write-downs of loans,– Small FIs wishing to disengage from LDC loan market,– FIs willing to swap LDC debt to rearrange portfolios.

• Buyers:– Wealthy investors, hedge funds, FIs and corporations:

speculation– FIs trying to rearrange LDC portfolios.

Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Financial Institutions Management 2e, by Lange, Saunders, Anderson, Thomson and CornettSlides prepared by Maike Sundmacher

10-19

Using Market Data to Measure Risk: The Secondary Market for LDC Debt

• Brady bond: issued by an LDC that is swapped for an outstanding loan by that LDC.

• Sovereign bonds.

• Performing loans.

• Non-performing loans.

Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Financial Institutions Management 2e, by Lange, Saunders, Anderson, Thomson and CornettSlides prepared by Maike Sundmacher

10-20

LDC Market Prices and Country Risk Analysis• Repayment problems are likely to be predicted by

combining LDC debt prices with key variables.

• Most significant variables affecting LDC loan sale prices (P) from 1985 to 1988:– Debt service ratios– Import ratio– Accumulated debt in arrears– Amount of loan loss provisions against LDC loans.

• Approach subject to same criticisms as traditional statistical models.

Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Financial Institutions Management 2e, by Lange, Saunders, Anderson, Thomson and CornettSlides prepared by Maike Sundmacher

10-21

Mechanisms for Dealing With Sovereign Risk Exposure

Debt-for-Equity Swaps:

Example: • Citibank sells $100 million Chilean loan to Merrill

Lynch for $91 million.• Merrill Lynch (market maker) sells to IBM at $93

million.• Chilean government allows IBM to convert the $100

million face value loan into pesos at a discounted rate to finance investments in Chile.

Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Financial Institutions Management 2e, by Lange, Saunders, Anderson, Thomson and CornettSlides prepared by Maike Sundmacher

10-22

Mechanisms for Dealing with Sovereign Risk Exposure

Multi-Year Restructuring of Loans (MYRAs):• Aspects of MYRAs:

– Restructuring fee charged by bank – Interest rate charged on new loan– Grace period– Maturity of loan– Option and guarantee features

• Concessionality: the amount a bank gives up in PV terms as a result of a MYRA.

Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Financial Institutions Management 2e, by Lange, Saunders, Anderson, Thomson and CornettSlides prepared by Maike Sundmacher

10-23

Mechanisms for Dealing With Sovereign Risk Exposure

Loan Sales:

• Benefits:– Removal of loans from balance sheet.– Sale at loss or reduced price indicates strength of balance

sheet.– Loss = tax write-off.

• Costs: – Loss.

Bond for Loan Swaps (Brady Bonds):

• Transform LDC loan into marketable liquid instrument.

• Usually senior to remaining loans of that country.

Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Financial Institutions Management 2e, by Lange, Saunders, Anderson, Thomson and CornettSlides prepared by Maike Sundmacher