Embed Size (px)

Citation preview

Chapter 11

Stockholders’ Equity

Stockholders’ Equity

Stockholders: Owners of a corporation Have a residual interest in assets after liabilities are

satisfied Stockholders’ equity:

Two major components Contributed capital Retained earnings

LO 1

Stockholders’ Equity

Contributed Capital: Amount a corporation receives from the sale of

stock (common or preferred) to the stockholders Additional Paid-In Capital : amount received at

issuance that exceeds the par value of the stock Retained earnings:

Amount of net income, over the life of the company not paid out as dividends

An important link between the income statement and the balance sheet

EXHIBIT 11.1—Advantages and Disadvantages of Stock versus Debt Financing

Stockholders’ Equity on the Balance Sheet

The basic accounting equation:

Two major components or subcategories:

Assets = Liabilities + Stockholders’ Equity

Components of the Stockholders’ Equity Section of the Balance Sheet

Number of Shares Par Value Additional Paid-In Capital Retained Earnings

Contributed Capital

Common stock Carries voting rights The common stockholders elect the corporation’s

officers • Establish its bylaws and governing rules

Preferred stock Flexible and tailored to a company’s needs Preference in dividends

Number of Shares

Authorized shares: the maximum number of shares a corporation may issue as indicated in the corporate charter

Issued shares: the number of shares sold or distributed to stockholders

Outstanding shares: the number of shares issued less the number of shares held as treasury stock

Par Value

An arbitrary amount that represents the legal capital of the firm

Stated on the face of the stock certificate Also called “stated value” Amount presented in the stock account

Additional Paid-In Capital & Retained Earnings

Additional paid-in capital: the amount received for the issuance of stock in excess of the par value of the stock

Retained earnings: net income that has been made by the corporation but not paid out as dividends Not necessarily available to stockholders May be used for purchase of assets, the retirement of

debt, or other financial needs

Exhibit 11.2—Retained Earnings Connects the Income Statement and the Balance Sheet

IFRS and Stockholders’ Equity Items that have characteristics of both debt and

equity Example: Convertible bond is similar to debt but

because it will become stock if converted, it also has the characteristics of equity

International accounting rules An item having both debt and equity component should

be separated into two parts—liability and stockholders’ equity

U.S. accounting standards Do not require to be recorded as a separate amount Recorded as either liability or stockholders’ equity

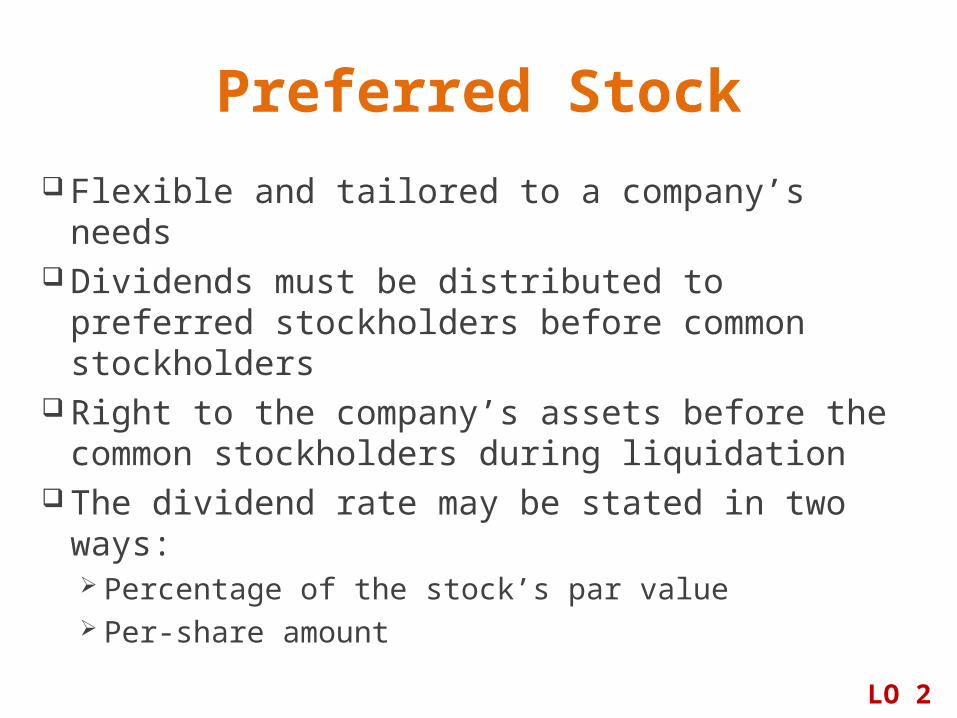

Preferred Stock

Flexible and tailored to a company’s needs Dividends must be distributed to preferred

stockholders before common stockholders Right to the company’s assets before the

common stockholders during liquidation The dividend rate may be stated in two ways:

Percentage of the stock’s par value Per-share amount

LO 2

Preferred Stock Additional Terms and Features

Convertible: allows preferred stock to be exchanged for common stock

Redeemable: allows stockholders to sell stock back to the company

Callable: allows the firm to eliminate a class of stock by paying the stockholders a specified amount

Preferred Stock Additional Terms and Features

Cumulative: the right to dividends in arrears before the current-year dividend is distributed

Participating: allows preferred stockholders to share on a percentage basis in the distribution of an abnormally large dividend

Issuance of Stock

Issued for cash or for noncash assets When issued for cash:

Par value reported in the stock account Amount in excess of par is reported in the Paid-In

Capital account When exchanged for noncash items:

Recorded at the fair market value of the stock or the assets received, whichever is most readily determined

LO 3

Example 11.1—Recording StockIssued for Cash

Assume that on July 1, a firm issued 1,000 shares of $10 par common stock for $15 per share

Example 11.2—Recording Stock for Noncash Consideration

Assume that on July 1, a firm issued 500 shares of $10 par preferred stock to acquire a building. The stock is not widely traded, and the current market value of the stock is not evident. The building has recently been appraised by an independent firm as having a market value of $12,000

Treasury Stock Represents the corporation’s own stock, previously issued to

shareholders, repurchased from stockholders and not retired, but held for various purposes

Repurchase is recorded as a debit to Treasury Stock, a contra-equity account

For an amount to be treated as treasury stock: It must be the corporation’s own stock It must have been issued to the stockholders at some point It must have been repurchased from the stockholders It must not be retired, but must be held for some purpose

LO 4

Example 11.3—Recording the Purchase of Treasury Stock

Assume that the Stockholders’ Equity section of Rezin Company’s balance sheet on December 31, 2014, appears as follows:

Example 11.3—Recording the Purchase of Treasury Stock (continued)

Assume that on February 1, 2015, Rezin buys 100 of its shares as treasury stock at $25 per share.

Stockholders’ Equity Section

The Stockholders’ Equity section of Rezin’s balance sheet on February 1, 2015, after the purchase of the treasury stock

Retirement of Stock

Repurchase of stock with no intention of reissuing To eliminate a particular class of stock or group of

stockholders The general principle for retirement of stock is the

same as for treasury stock transactions No income statement accounts are affected Effect is reflected in the Cash account and the

Stockholders’ Equity accounts

Cash Dividends

Declared only if a company has sufficient cash available and adequate retained earnings

Not an expense on the income statement Date of declaration: cash dividends are declared Payment date: cash dividends are paid Date of record: dividend is paid to the

stockholders who own the stock as of this date

LO 5

Dividend Payout Ratio

The annual dividend amount divided by the annual net income

Ratio for many firms is 50% or 60% and seldom exceeds 70%

Annual DividendAnnual Net IncomeDividend Payout Ratio =

Example 11.4—Recording the Declaration of a Dividend

Assume that on July 1, the board of directors of Grant Company declared a cash dividend of $7,000 to be paid on September 1.

Example 11.5—Computing Dividend Payments for Noncumulative Preferred Stock Assume that on December 31, 2014, Stricker Company has

outstanding 10,000 shares of $10 par, 8% preferred stock and 40,000 shares of $5 par common stock. Stricker was unable to declare a dividend in 2012 or 2013 but wants to declare a $70,000 dividend for 2014

Example 11.6—Computing Dividend Payments for Cumulative Preferred Stock If the terms of the stock agreement in Example 11.5

indicate that the preferred stock is cumulative, the preferred stockholders have a right to dividends in arrears before the current year’s dividend is distributed

Stock Dividends

The issuance of additional shares of stock to existing stockholders

Firms use stock dividends for several reasons Do not require the use of cash Reduce the market price of the stock• The lower price may make the stock more attractive

Do not represent taxable income to recipients

LO 6

Example 11.7—Recording a Small Stock Dividend

Assume that Shah Company’s Stockholders’ Equity category of the balance sheet appears as follows as of January 1, 2014:

Example 11.7—Recording a Small Stock Dividend (continued)

Assume that on January 2, 2014, Shah declares a 10% stock dividend to common stockholders to be distributed on April 1, 2014. Small stock dividends (usually those of 20% to 25%) normally are recorded at the market value of the stock as of the date of declaration. Assume that Shah’s common stock is selling at $40 per share on that date

Stockholders’ Equity Section

Example 11.8—Recording the Declaration of a Large Stock Dividend

Assume that instead of a 10% dividend, on January 2, 2014, Shah declares a 100% stock dividend to be distributed on April 1, 2014. The stock dividend results in 5,000 additional shares being issued and certainly meets the definition of a large stock dividend

Example 11.8—Recording the Declaration of a Large Stock Dividend (continued)

The effect when the stock is actually distributed is as follows:

The Stockholders’ Equity category of Shah’s balance sheet as of April 1 after the stock dividend is as follows:

Stock Splits

The creation of additional shares of stock with a reduction of the par value of the stock

LO 7

Example 11.9—Reporting a Stock Split Refer to the Shah Company in Examples 11-7 and 11-8. Assume that on

January 2, 2014,Shah issued a 2-for-1 stock split instead of a stock dividend. The split results in an additional 5,000 shares of stock outstanding but is not recorded in a formal accounting transaction. Therefore, the Stockholders’ Equity section of Shah Company immediately after the stock split on January 2, 2014, is as follows:

Statement of Stockholders’ Equity

Explains the reasons for the difference between the beginning and ending balances for all accounts in the Stockholders’ Equity category of the balance sheet

LO 8

Exhibit 11.3—Fun Fitness’s Statement of Stockholders’ Equity, 2014

Comprehensive Income

Total change in net assets from all sources except investments by or distributions to the owners

Important measure of a company’s profitability One-statement approach

Showed at the bottom of the income statement Two-statement approach

Statement of Comprehensive Income must be presented (indicated in Exhibit 11.4—next slide)

Exhibit 11.4—The Relationship between the Income Statement and the Statement of Comprehensive Income

Book Value Per Share

Rights of each share of stock to the net assets of the company

If preferred stock is present, stockholders’ equity must be adjusted to reflect its liquidation value

LO 9

Calculating Book Value When PreferredStock Is Present

Exhibit 11.5—Workout Wonders’ Stockholders’ Equity Section

$13,972 − $500 = $13,472 million common stockholders’ equity

$13,472 /1,679 = $8.02 Book Value per Share

Market Value per Share

The selling price of the stock as indicated by the most recent transactions

More meaningful measure of the value of the stock

Example: the listing for Nike Inc. stock on the Internet may indicate the following:

Exhibit 11.6—The Effect of Stockholders’ Equity Items on the Statement of Cash Flows

LO 10

Sole Proprietorships

Business owned by one person The owner have an unlimited liability

Not a separate entity for legal or tax purposes Assets and liabilities of the owner must be kept

separate from the business Owners’ equity is one account—the owner’s

capital account

LO 11

Example 11.10—Recording Investments in a Sole Proprietorship

Assume that on January 1, 2014, Peter Tom began a new business by investing $10,000 cash

Example 11.10—Recording Investments in a Sole Proprietorship (continued)

Assume that on July 1, 2014, Peter Tom took an auto valued at $6,000 from the business to use as his personal auto

Example 11.10—Recording Investments in a Sole Proprietorship (continued)

The Peter Tom, Drawing account is a contra-equity account. An increase in the account reduces the owner’s equity. At the end of the fiscal year, the drawing account should be closed to the capital account and the effect is as follows:

Example 11.10—Recording Investments in a Sole Proprietorship (continued)

Assume that all revenue and expense accounts of Peter Tom Company have been closed to the Income Summary account, resulting in a balance of $4,000, the net income for the year

Example 11.10—Recording Investments in a Sole Proprietorship (continued)

The Owner’s Equity section of the balance sheet

Partnerships More than one owner Separate capital account is maintained for each

partner, as well as separate drawing accounts Partnership agreement governs how income

(losses) will be distributed Unlimited liability Limited life Not taxed as a separate entity

Income is taxed on each owner’s tax return

Partnership Agreement

Specifies how much the owners will invest, what their salaries will be, and how profits will be shared

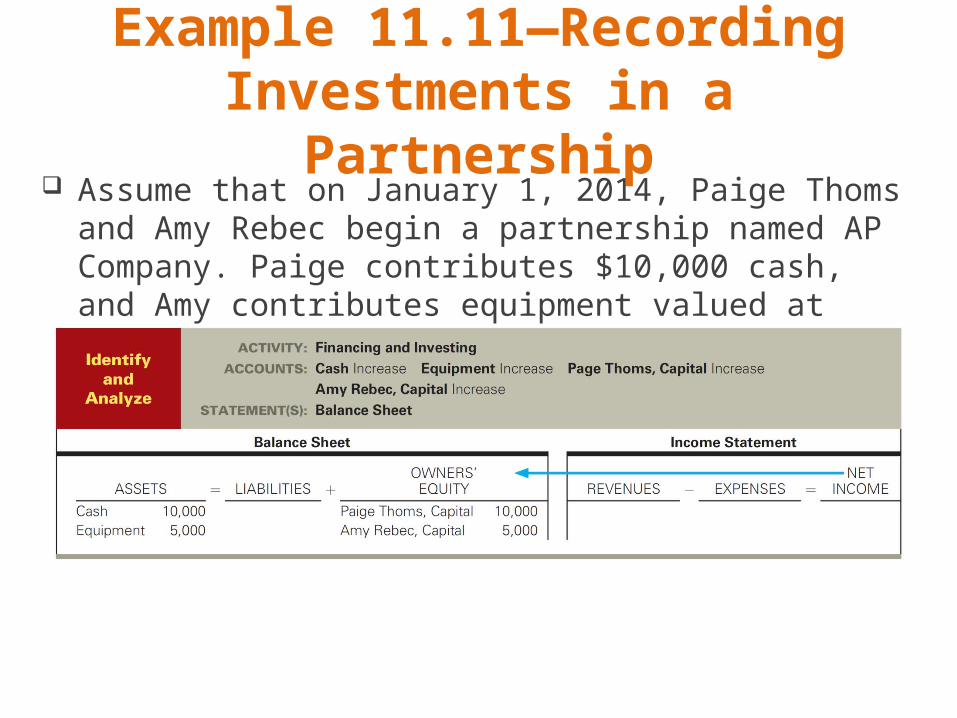

Example 11.11—Recording Investments in a Partnership

Assume that on January 1, 2014, Paige Thoms and Amy Rebec begin a partnership named AP Company. Paige contributes $10,000 cash, and Amy contributes equipment valued at $5,000

Example 11.11—Recording Investments in a Partnership (continued)

Assume that on April 1, 2014, each owner withdraws $2,000 of cash from AP Company

Distribution of Income Assume that AP Company has $30,000 of net income for the period

and has established an agreement that income should be allocated evenly between the two partners, Paige and Amy. Each capital account would be increased by $15,000

Distribution of Income (continued) Paige and Amy may specify that all income of AP Company should be

allocated in a 2-to-1 ratio, with Paige receiving the larger portion

Distribution of Income (continued) Assume that the partnership agreement of AP Company

specifies that Paige and Amy be allowed a salary of $6,000 and $4,000, respectively; that each partner receive 10% on her capital balance; and that any remaining income be allocated equally. Assume that AP Company has been in operation for several years and that the capital balances of the owners at the end of 2014, before the income distribution, are as follows:

Paige Thoms, Capital $40,000 Amy Rebec, Capital 50,000

Distribution of Income (continued) If AP Company calculated that its 2014 net income (before

partner salaries) was $30,000, income would be allocated between the partners as follows:

Distribution of Income (continued) Paige Thoms, Capital would be increased by $15,500, and Amy Rebec,

Capital, by $14,500. The effect of closing the Income Summary account to the capital accounts is as follows:

This indicates that the amounts of $15,500 and $14,500 were allocated to Paige and Amy, respectively. It does not indicate the amount actually paid to (or withdrawn by) the partners.

End of Chapter 11

![Total liabilities and stockholders' equity $ 226,322 $ 486,938 · united states securities and exchange commission washington, d.c. 20549-----form 10-q (mark one) [x] quarterly report](https://img.pdfslide.net/doc/110x75/5f7863602ef355421a42bc6c/total-liabilities-and-stockholders-equity-226322-486938-united-states-securities.jpg)