Embed Size (px)

Citation preview

CHAPTER 14

Alternative Minimum Tax

Forms

1040, p2 + Form 6251 - Taxes in addition to regular tax

Form, formula, lists6251 - filled in overall example

Rationale for AMT

no t/p with substantial economic income should be able to avoid significant tax

because of public perceptionBlue Book, TRA 1986, n.1. West “inherently unfair”

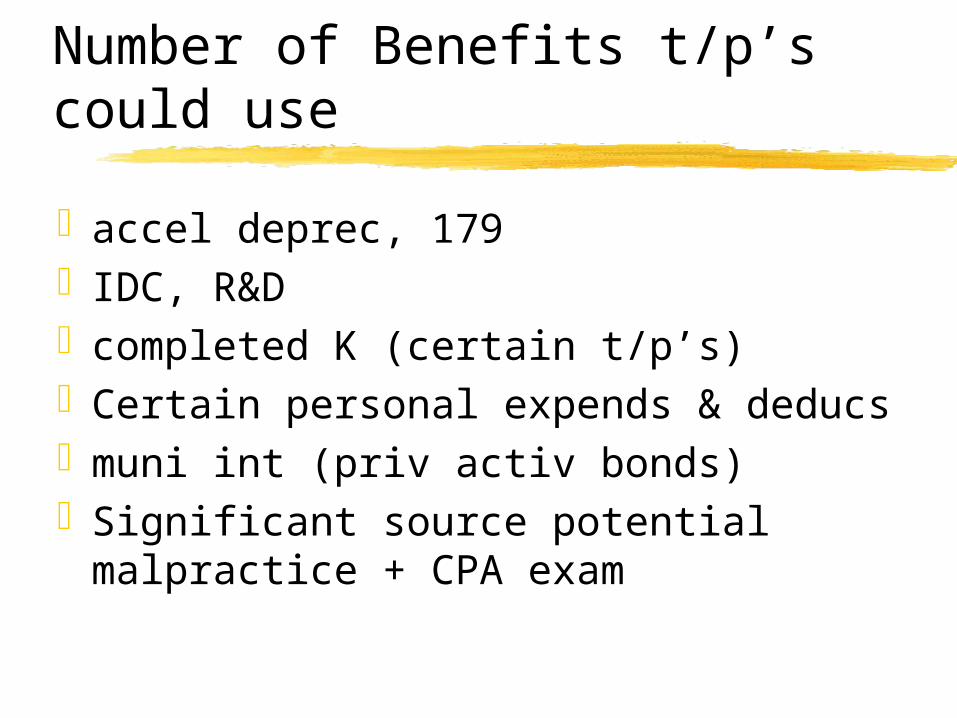

Number of Benefits t/p’s could use

accel deprec, 179 IDC, R&D completed K (certain t/p’s) Certain personal expends & deducs muni int (priv activ bonds)Significant source potential

malpractice + CPA exam

Formula (Figure 14-2)

Overview - TI is starting pointAdjustments - positive + negative

(often timing) adjust TI to get AMTI Preferences - add (positive only)

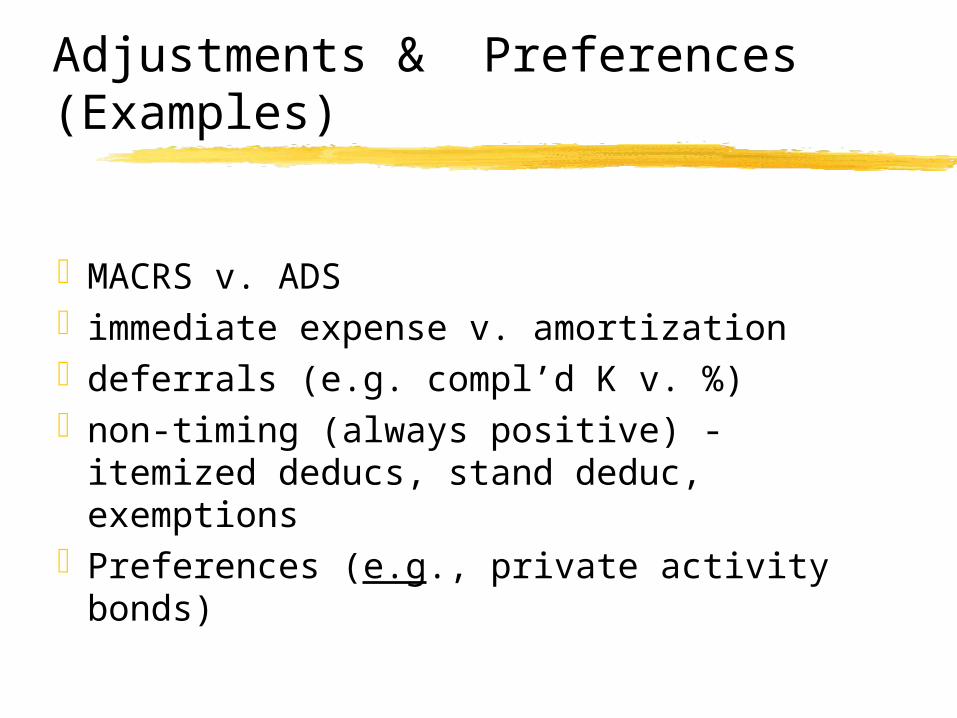

Adjustments & Preferences (Examples)

MACRS v. ADS immediate expense v. amortization deferrals (e.g. compl’d K v. %) non-timing (always positive) - itemized

deducs, stand deduc, exemptionsPreferences (e.g., private activity bonds)

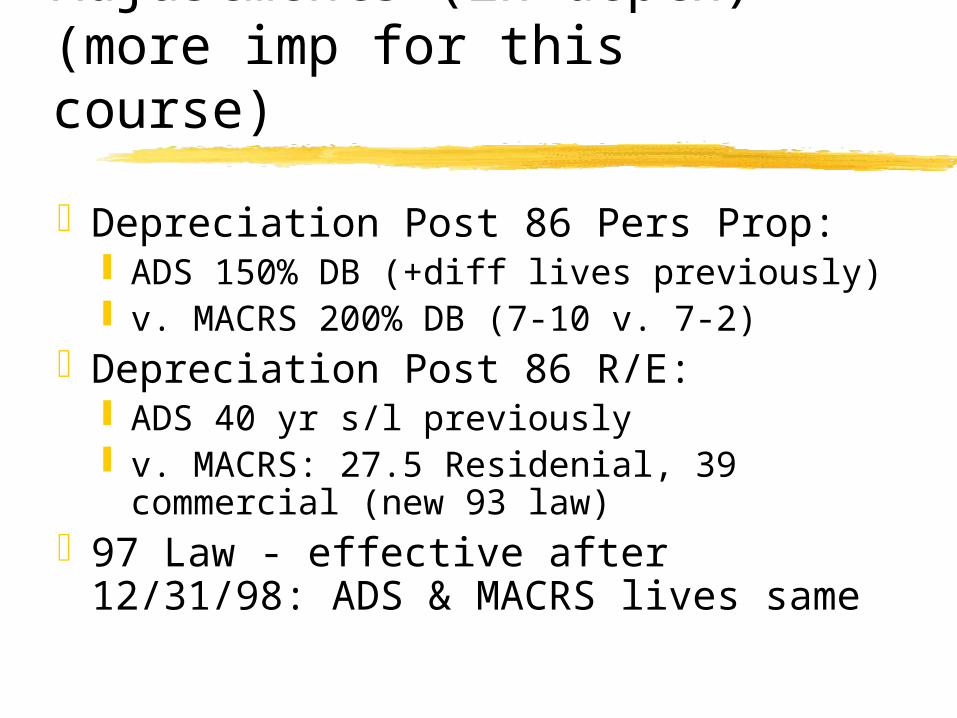

Adjustments (in depth) (more imp for this course)

Depreciation Post 86 Pers Prop: ADS 150% DB (+diff lives previously) v. MACRS 200% DB (7-10 v. 7-2)

Depreciation Post 86 R/E: ADS 40 yr s/l previously v. MACRS: 27.5 Residenial, 39

commercial (new 93 law) 97 Law - effective after 12/31/98:

ADS & MACRS lives same

PAL: AMTI v TI may result in different PAL

Adjustment for G or L AMTI G or L v. TI G

or L may differ bec of

basis differences e.g. deprecation

Alternative Tax NOL:

Reg tax NOL reduced by AMT adjustms & Prefs

AMT NOL CB & CF must be used v. AMTI

used up even if no AMT (ex 15)CB2 & CF20; elect to forego CB must

be made for both reg tax & AMTmax 90%

Itemized Deductions & Exemptions:

Taxes and miscellaneous itemized subject to 2% not allowed for AMT

+ if tax refund in inc, take out of AMTI

medical > 10% AGI Cut back of itemized for wealthy not

apply for AMT (neg adjustment)

Qualified housing int v. qualif’d resid int (AMT v. reg)

2 residences still but not home

equity int unless acquire or improve

Refi prior loan: no adjusm if Proceeds of prior loan were used to

acquire or improve Interest on prior = qualified housing int Amount of loan not increased If amount incr’s excess = adjusm

Invest int: if priv activ tax ex bond int is pref, increase invest int exp for AMT

home equity loan used to purchase investment = investment int for AMT

Standard deduction not allowedexemptions not allowed

Preferences (Some)

% depletion - preference to extent >AB

Excess IDC Charitable contribs of apprec’d prop:

FMV deduction for regular taxNew Law 93 - Charitable contrib of

appreciated property

Tangible pers prop after 6/30/92; other prop after 12/31/92 repealed preference

int on priv activ bonds - include for AMT deduc exps of private activity bonds

(but only as offset v. inc - not creat neg. preference)

Deprec - RE & leased pers prop before 87, pref = accel’d deprec minus S/L; RE after 92, no excess over S/L on pre 87 prop

50% exclus for certain small bus stk is amt pref (42% = preference - 97 Law)

ISO: spread (FMV exercise - FMV grant) - pref.

Exemption amounts - AMT

•New Law (93) JGTRRA (03 & 04)

MFJ 45,000 58,000

S 33,750 40,250

MFS 22,500 29,000

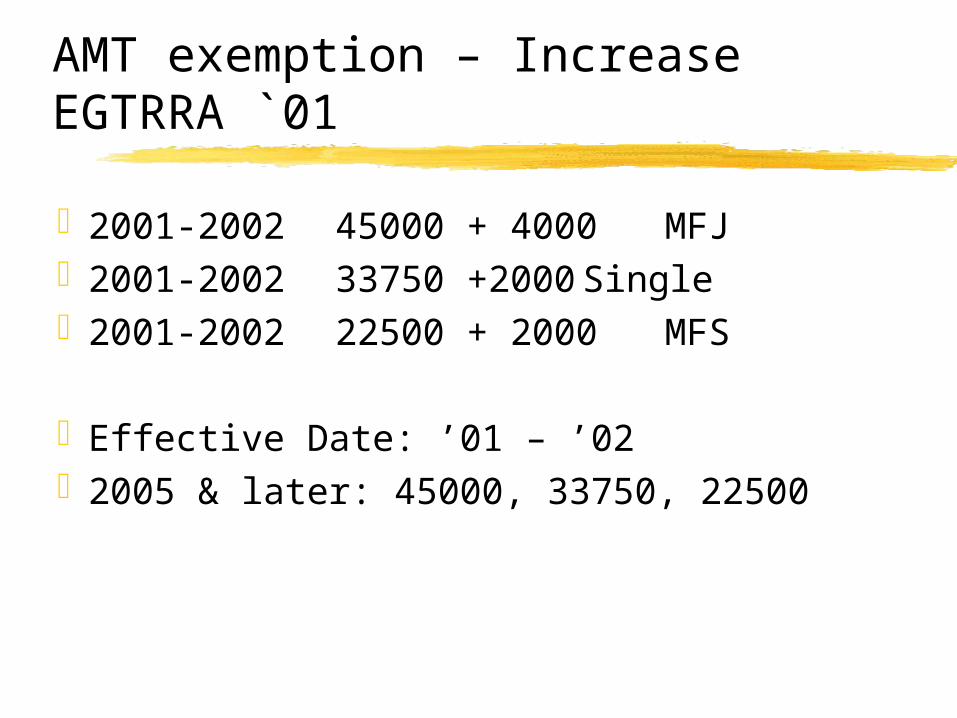

AMT exemption – IncreaseEGTRRA `01

2001-2002 45000 + 4000 MFJ2001-2002 33750 +2000

Single2001-2002 22500 + 2000 MFS

Effective Date: ’01 – ’022005 & later: 45000, 33750, 22500

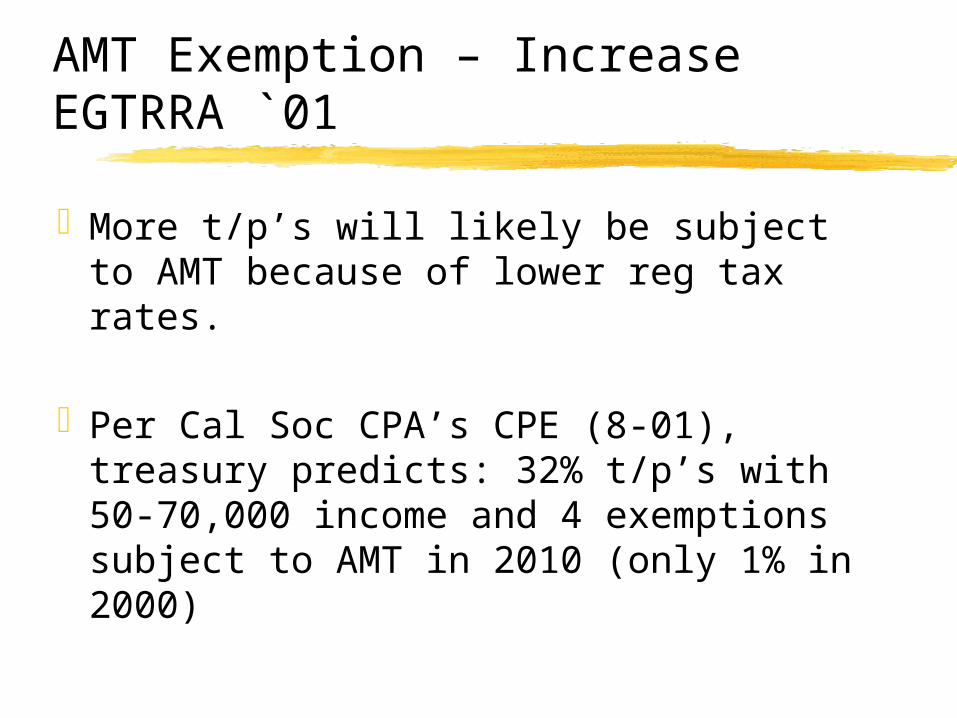

AMT Exemption – IncreaseEGTRRA `01

More t/p’s will likely be subject to AMT because of lower reg tax rates.

Per Cal Soc CPA’s CPE (8-01), treasury predicts: 32% t/p’s with 50-70,000 income and 4 exemptions subject to AMT in 2010 (only 1% in 2000)

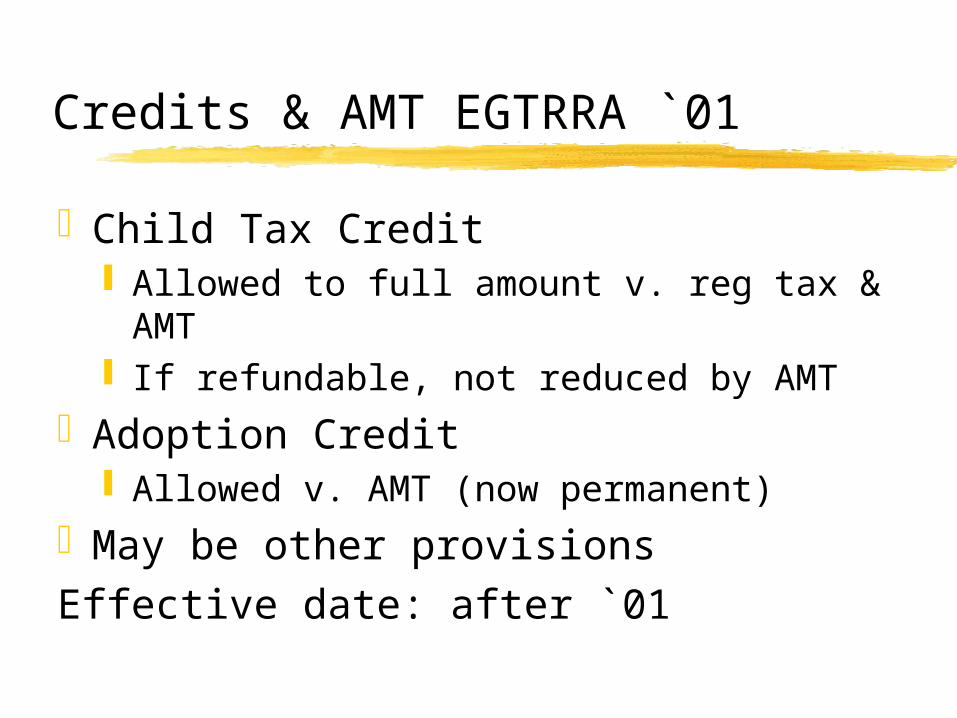

Credits & AMT EGTRRA `01

Child Tax Credit Allowed to full amount v. reg tax & AMT If refundable, not reduced by AMT

Adoption Credit Allowed v. AMT (now permanent)

May be other provisionsEffective date: after `01

Phaseout starts

MFJ 150,000

Single 112,500 Excess X 25%

MFS 75,000

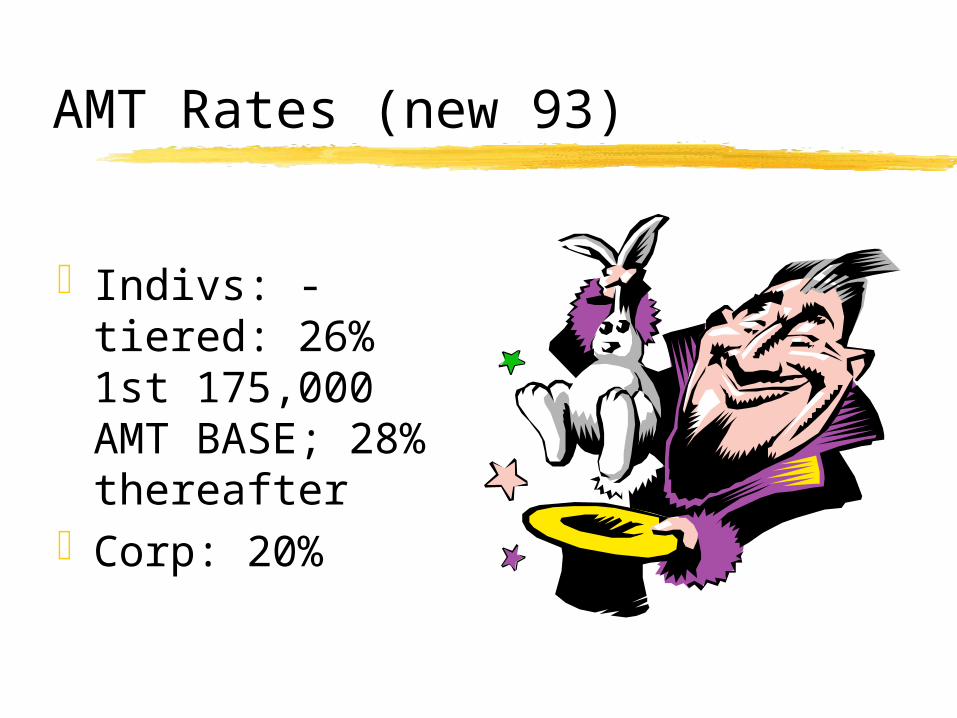

AMT Rates (new 93)

Indivs: - tiered: 26% 1st 175,000 AMT BASE; 28% thereafter

Corp: 20%

AMT Credit

Reg tax - may be reduced for prev yrs AMT attributed to timing differences

c/o indefinite Must recompute AMT (ex) - reflecting

only exclusion items & exemptions

Exclusion items: Stand deduc, exemptions, med deduc, itemized not allowed (misc 2%, taxes, int), excess % deplet, priv activ bonds tax ex interest

AMT - AMT (exclus items only) = credit (v. reg tax when reg > AMT, up to excess)

Corporate AMT

ACE Rat: old AMT (86): Large BI (book income) v. TI AMT - should make payment on BI; New AMT: old adjustment too much; influence on BI

ACE adjustment only for corps 75% X excess of ACE over AMTI b4 ACE (&

AMT NOL)Positive or negative - Neg limited to prior

positive

i.e. indirect requirement of conformity financial & tax Accounting

ACE starting point is AMTI b4 ACE & AMT NOL

Adjustments Exclusions - in E&P, not TI or AMTI

(eg tax exempt)

depreciation - ADS S/L

disallowing - not allowed E&P, not allowed ACE (e.g. DRD, NOL)

exceptions - ACE is not E&P & is not book inc

Other adjustments (as with E&P)

Special rules Fed Inc Tax -

deduc’d from E&P, not ACE

Corp Exemption

40000 — [25% x (AMTI-150000)]

Planning

private bonds - may be avoidwatch elections - circ exps, mining,

R&Davoid bunching - use AMT exemptionrate differential - If in REG tax v. AMT

e.g. gains, charitable deduction 1997 law: same CG rate as reg

Taxpayer Relief Act of 1997

(1) Chap 14, Chap 7

ADS – Recovery period are the same as MACRS for AMT

Method may still differ; (EG 150% DB v. 200% DB for personal property)

Effective for property placed in service after 12/31/98

(2) Chapter 14

AMT for small Corps – repealedSmall Corp: Ave Ann GR <5m; 3 yr

period beginning 12/31/94When (small Corp) lost; Ave ann GR

>7.5; for prec 3 yrs; lost prospectively only

Effective Date: Tax yrs beginning after 12/31/97

(3) Chapter 14

AMT Preference – 50% excl’d gain on certain small bus stk (1201); Pref now 42% (instead of 50%); Pref 28% (98 Law) holding period start after 00

Effective: tax yrs ending after 5/6/97

IRS Restructuring & Reform Act of 1998

Tax and Trade Relief Act of 1998

Chapter 14

Restructuring Act Small Business AMT Exemption

Clarification1) 7.5m GR Test – yrs after 12/31/93 only

considered2) All corps exempt corp AMT 1st yr of

existence regardless of inc level Effective: yrs beg after 12/31/97

Relief Act

Non refundable personal credits

Can offset reg tax in full

Not just excess of reg over tentative min

Credits = dep care, elderly & disab, adoption, child tax, int on mortgs, HOPE & lifetime lrng, DC homebuyer

1998 only originally

![Dnevni avaz [broj 6251, 14.1.2013]](https://img.pdfslide.net/doc/110x75/54525c29b1af9f5e028b4757/dnevni-avaz-broj-6251-1412013.jpg)