Embed Size (px)

Citation preview

Chapter 14

The Money Supply Process

© 2013 Pearson Education, Inc. All rights reserved. 14-2

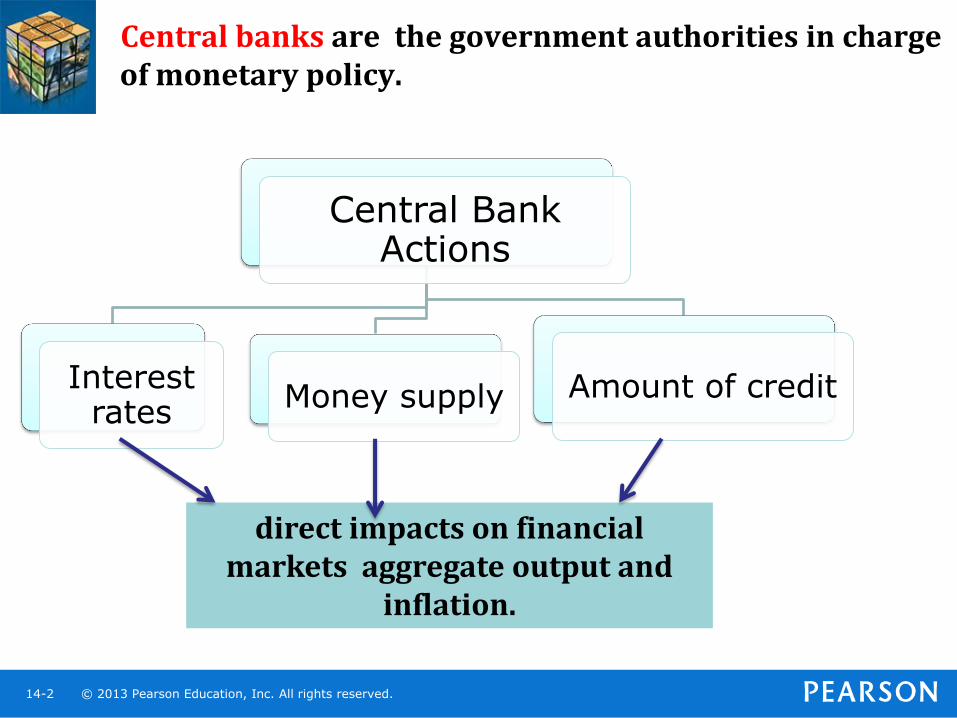

Central banks are the government authorities in charge of monetary policy.

Central Bank Actions

Interest rates

Money supply Amount of credit

direct impacts on financial markets aggregate output and

inflation.

© 2013 Pearson Education, Inc. All rights reserved. 14-3

To understand the role that central banks play in financial markets and the economy:

• How these organizations work?

• Who controls central banks and determines their actions?

Movements in the money supply affect interest rates and the overall health of the economy and thus affect us all.

• How the money supply is determined. Who controls it?

© 2013 Pearson Education, Inc. All rights reserved. 14-4

the money supply process: is the mechanism that determines the level of the money supply.

• deposits at banks are the largest component of the money supply.

• understanding how these deposits are created is the first step in understanding the money supply process

• how the banking system creates deposits, and describes the basic principles of the money supply?

© 2013 Pearson Education, Inc. All rights reserved. 14-5

Functions of the Federal Reserve Banks

• Clear checks

• Issue new currency

• Withdraw damaged currency from circulation

• Manage and make discount loans to banks.

• Evaluate proposed mergers and applications for banks to expand their activities

• Collect data on local business situations

• Use their staffs of professional economists to research topics related to the conduct of monetary policy

© 2013 Pearson Education, Inc. All rights reserved. 14-6

Four Players in the Money Supply Process

• Central bank (Federal Reserve System): the government agency that oversees the banking system and is responsible for the conduct of monetary policy

• Banks (depository institutions; financial intermediaries): the financial intermediaries that accept deposits from individuals and institutions and make loans

e.g., commercial banks, savings, savings banks, and credit unions.

© 2013 Pearson Education, Inc. All rights reserved. 14-7

Four Players in the Money Supply Process

• Depositors : individuals and institutions that hold deposits in banks

• Borrowers from banks

• individuals and institutions that borrow from the depository institutions and institutions that issue bonds that are purchased by the depository institutions.

the central bank is the most important player as its conduct of monetary policy involves actions that affect its balance sheet (holdings of assets and liabilities.

© 2013 Pearson Education, Inc. All rights reserved. 14-8

Conventional Monetary Policy Tools

• During normal times, Central banks use three tools of monetary policy to control the money supply and interest rates:

• discount lending

• open market operations

• reserve requirements

© 2013 Pearson Education, Inc. All rights reserved. 14-9

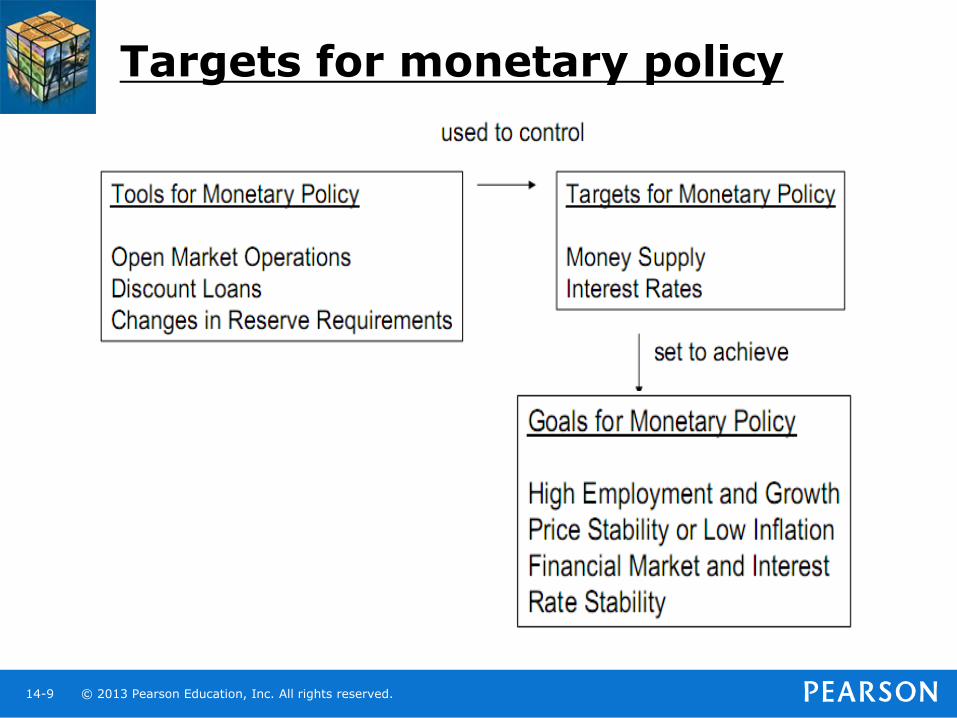

Targets for monetary policy

© 2013 Pearson Education, Inc. All rights reserved. 14-10

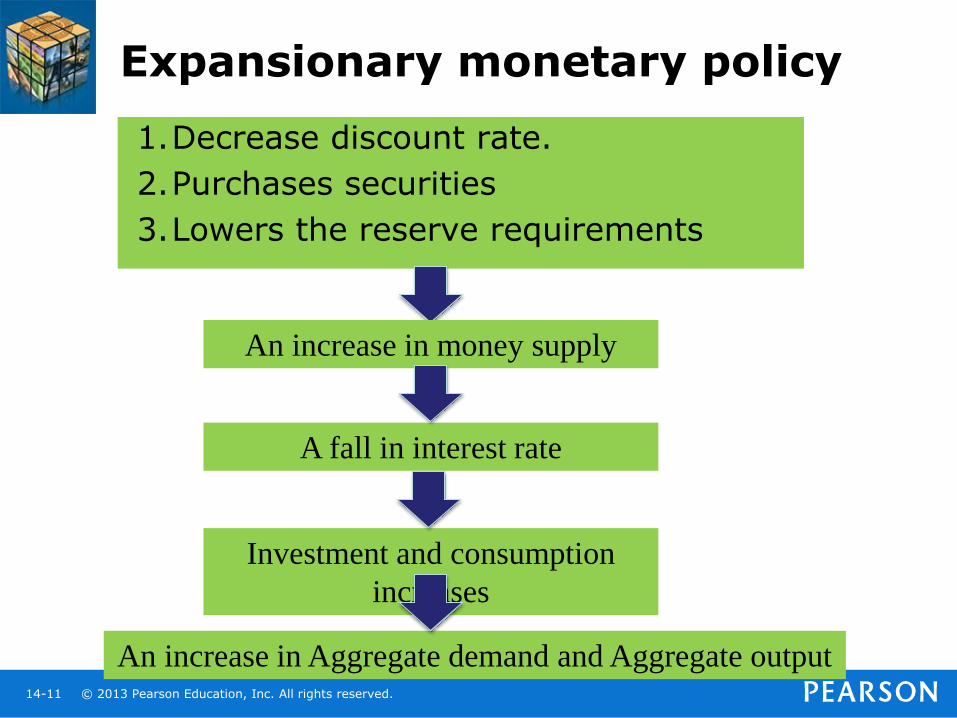

Expansionary monetary policy

• It is used to overcome recession or depression.

• When there is fall in consumer & business demand, the central bank

1. Decrease discount rate.

2. Purchases securities through open market operations.

3. Lowers the reserve requirements

These procedures lead to an upward shift in the AD.

© 2013 Pearson Education, Inc. All rights reserved. 14-11

Expansionary monetary policy

1.Decrease discount rate.

2.Purchases securities

3.Lowers the reserve requirements

An increase in money supply

A fall in interest rate

Investment and consumption

increases

An increase in Aggregate demand and Aggregate output

© 2013 Pearson Education, Inc. All rights reserved. 14-12

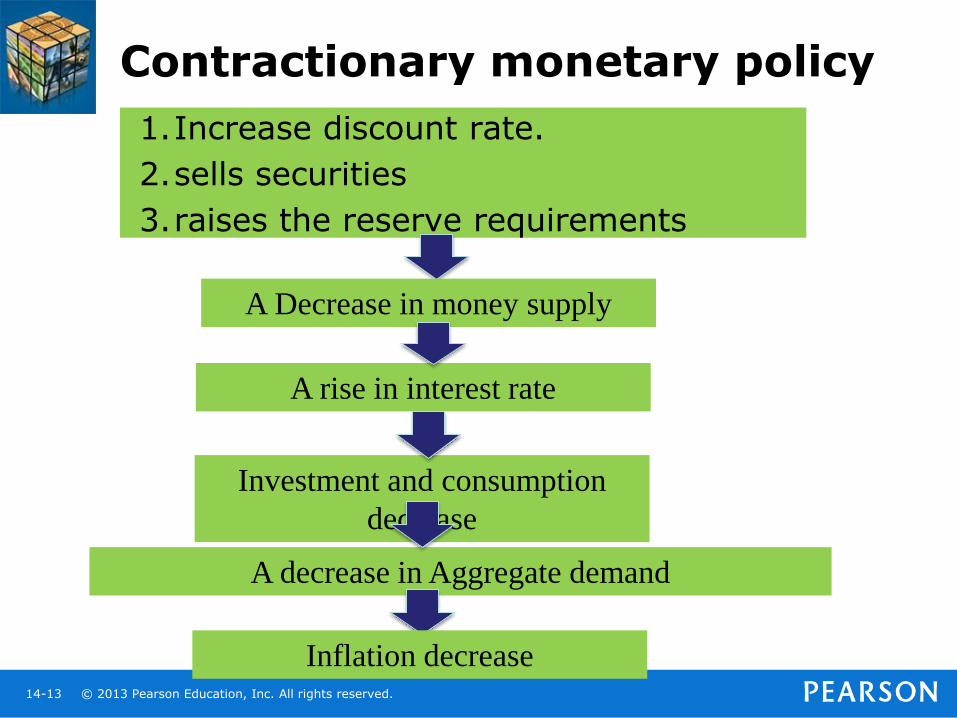

Contractionary monetary policy

• It is used to overcome inflation

• When there is an increase in inflation rate due to high aggregate demand, the central bank

1. Increase discount rate.

2. sells securities through open market operations.

3. Raises the reserve requirements

These procedures lead to an downward shift in the AD.

© 2013 Pearson Education, Inc. All rights reserved. 14-13

Contractionary monetary policy

1.Increase discount rate.

2.sells securities

3.raises the reserve requirements

A Decrease in money supply

A rise in interest rate

Investment and consumption

decrease

A decrease in Aggregate demand

Inflation decrease

© 2013 Pearson Education, Inc. All rights reserved. 14-14

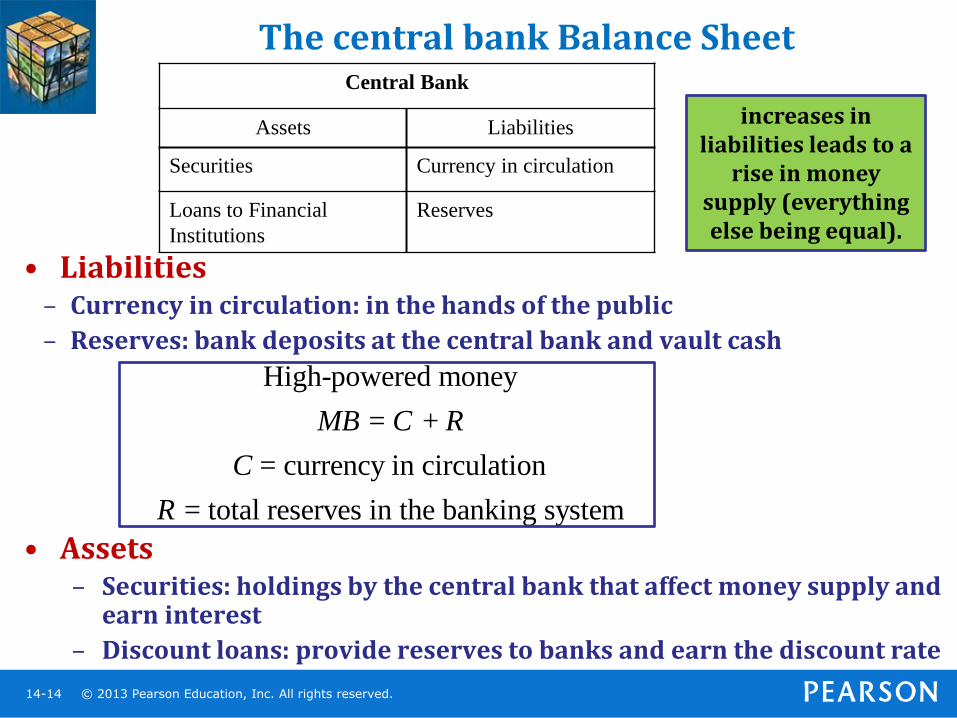

The central bank Balance Sheet

• Liabilities – Currency in circulation: in the hands of the public

– Reserves: bank deposits at the central bank and vault cash

• Assets – Securities: holdings by the central bank that affect money supply and

earn interest

– Discount loans: provide reserves to banks and earn the discount rate

Central Bank

Assets Liabilities

Securities Currency in circulation

Loans to Financial

Institutions

Reserves

increases in liabilities leads to a

rise in money supply (everything else being equal).

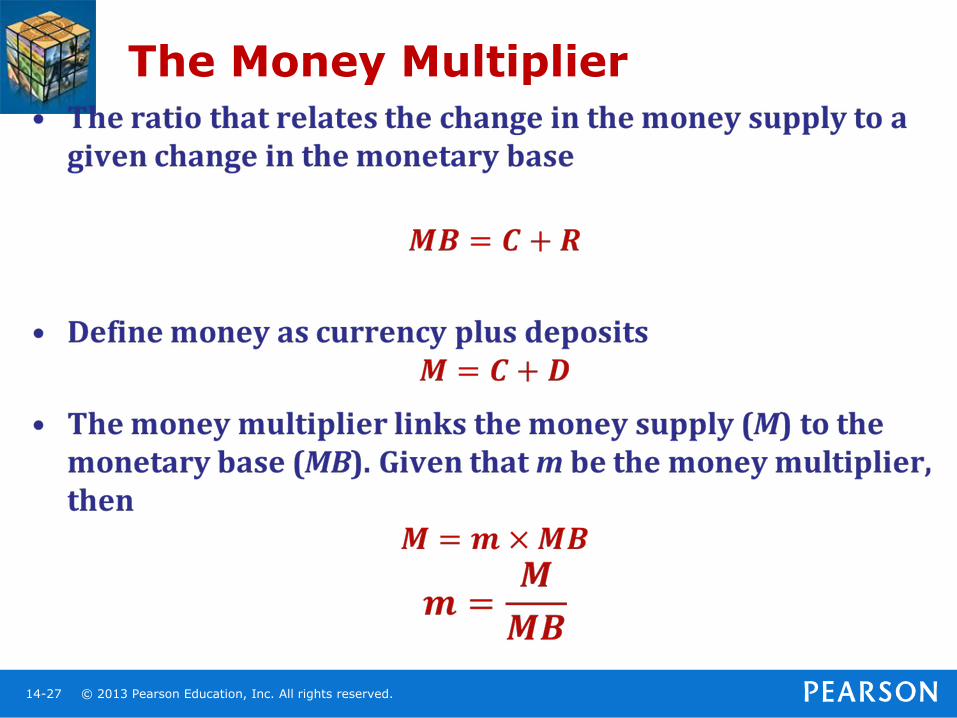

High-powered money

= +

= currency in circulation

= total reserves in the banking system

MB C R

C

R

© 2013 Pearson Education, Inc. All rights reserved. 14-15

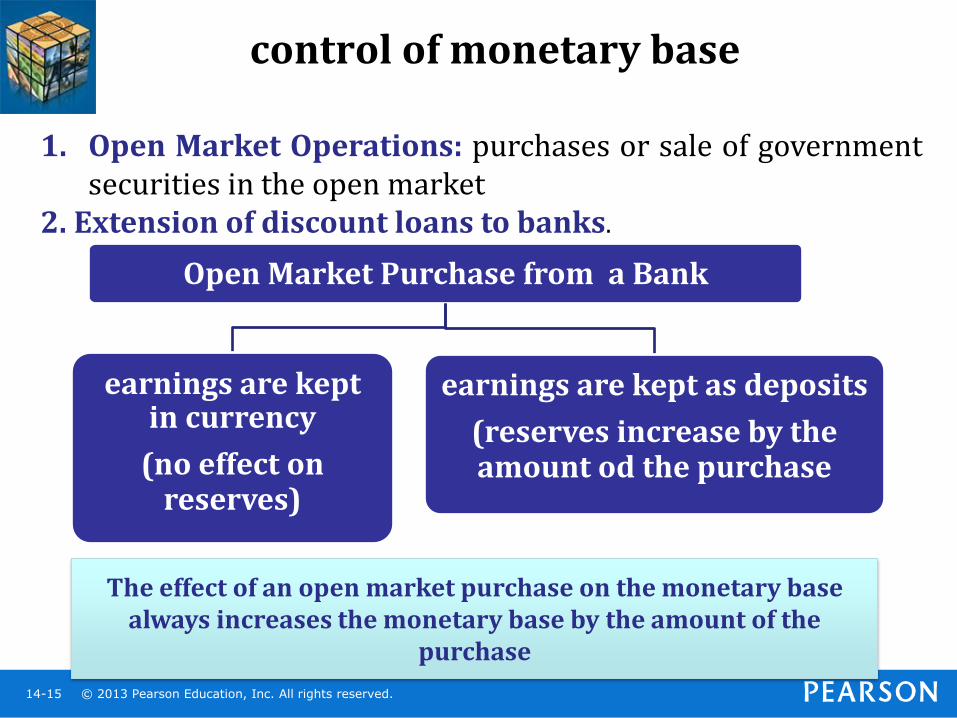

control of monetary base

1. Open Market Operations: purchases or sale of government securities in the open market

2. Extension of discount loans to banks.

Open Market Purchase from a Bank

earnings are kept in currency

(no effect on reserves)

earnings are kept as deposits

(reserves increase by the amount od the purchase

The effect of an open market purchase on the monetary base always increases the monetary base by the amount of the

purchase

© 2013 Pearson Education, Inc. All rights reserved. 14-16

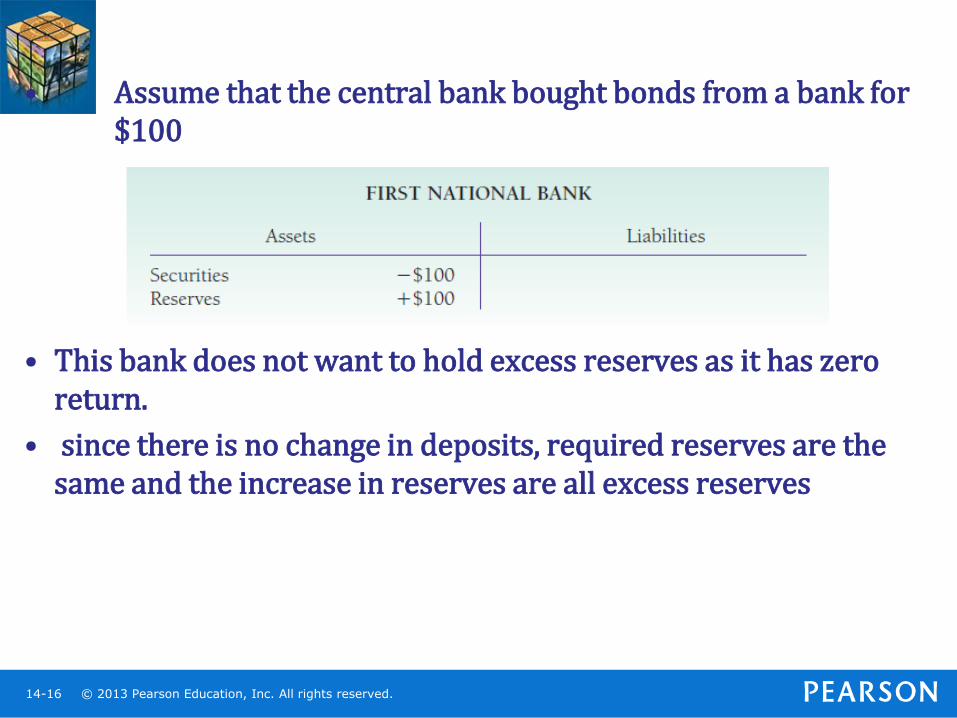

• Assume that the central bank bought bonds from a bank for $100

• This bank does not want to hold excess reserves as it has zero return.

• since there is no change in deposits, required reserves are the same and the increase in reserves are all excess reserves

© 2013 Pearson Education, Inc. All rights reserved. 14-17

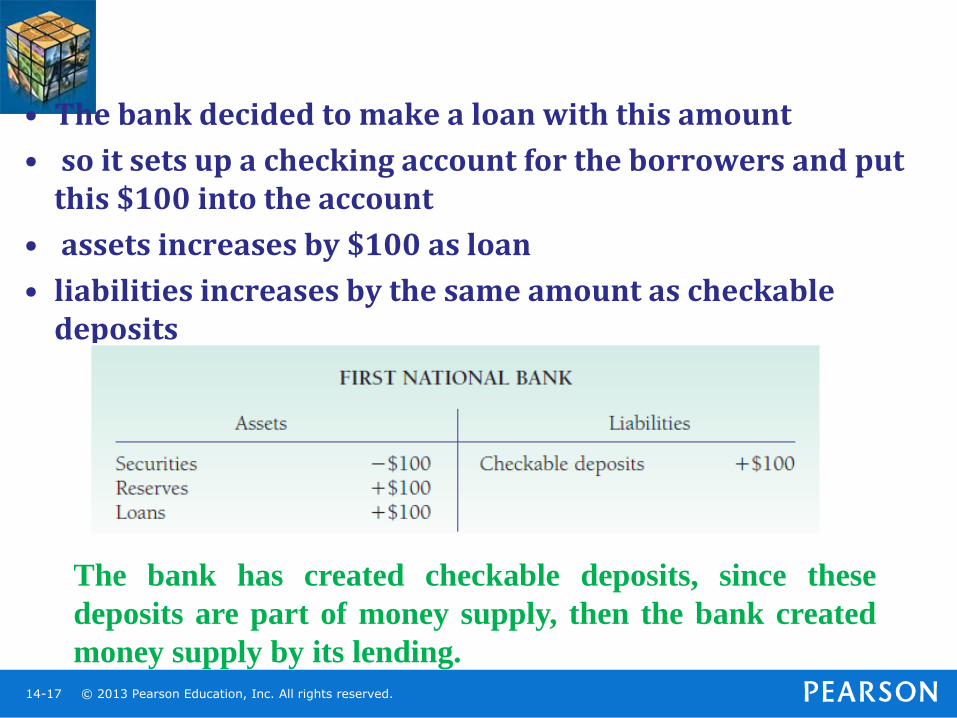

• The bank decided to make a loan with this amount

• so it sets up a checking account for the borrowers and put this $100 into the account

• assets increases by $100 as loan

• liabilities increases by the same amount as checkable deposits

The bank has created checkable deposits, since these

deposits are part of money supply, then the bank created

money supply by its lending.

© 2013 Pearson Education, Inc. All rights reserved. 14-18

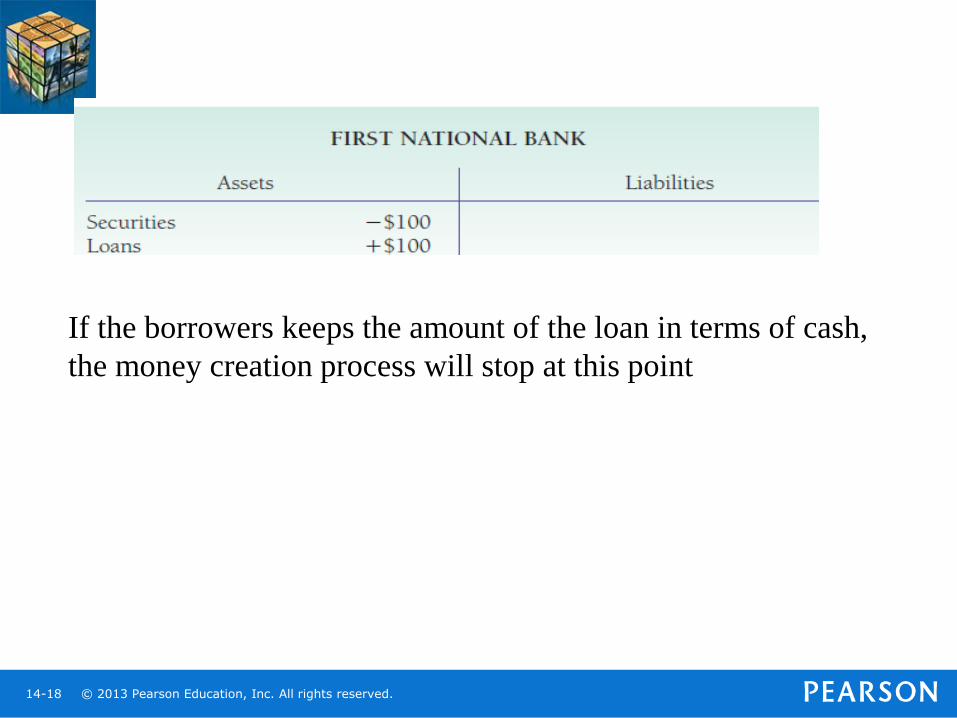

If the borrowers keeps the amount of the loan in terms of cash,

the money creation process will stop at this point

© 2013 Pearson Education, Inc. All rights reserved. 14-19

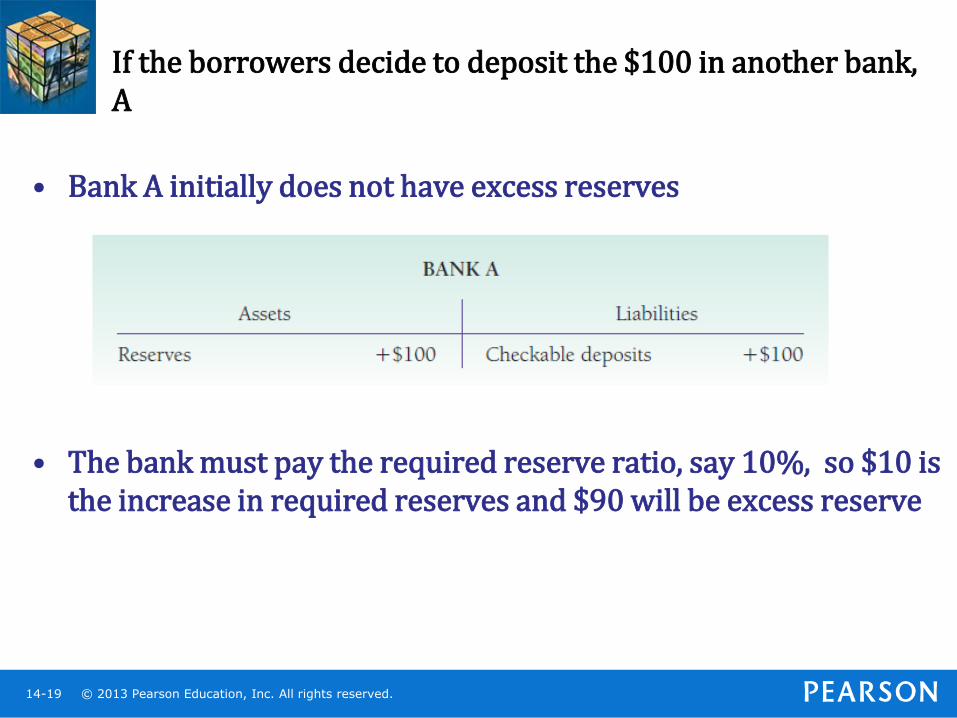

If the borrowers decide to deposit the $100 in another bank, A

• Bank A initially does not have excess reserves

• The bank must pay the required reserve ratio, say 10%, so $10 is the increase in required reserves and $90 will be excess reserve

© 2013 Pearson Education, Inc. All rights reserved. 14-20

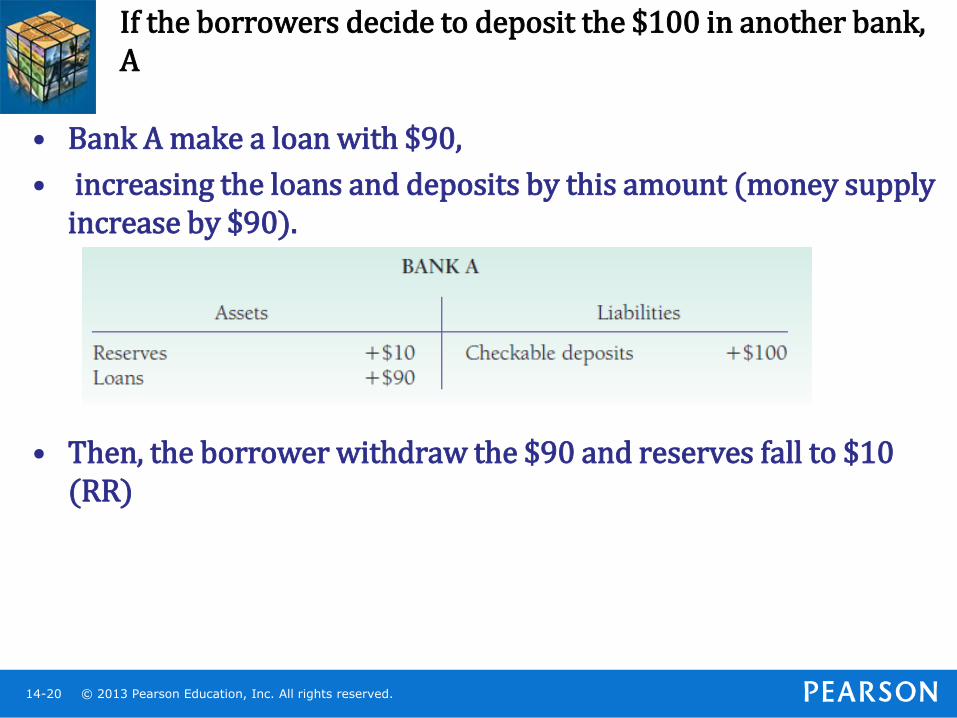

If the borrowers decide to deposit the $100 in another bank, A

• Bank A make a loan with $90,

• increasing the loans and deposits by this amount (money supply increase by $90).

• Then, the borrower withdraw the $90 and reserves fall to $10 (RR)

© 2013 Pearson Education, Inc. All rights reserved. 14-21

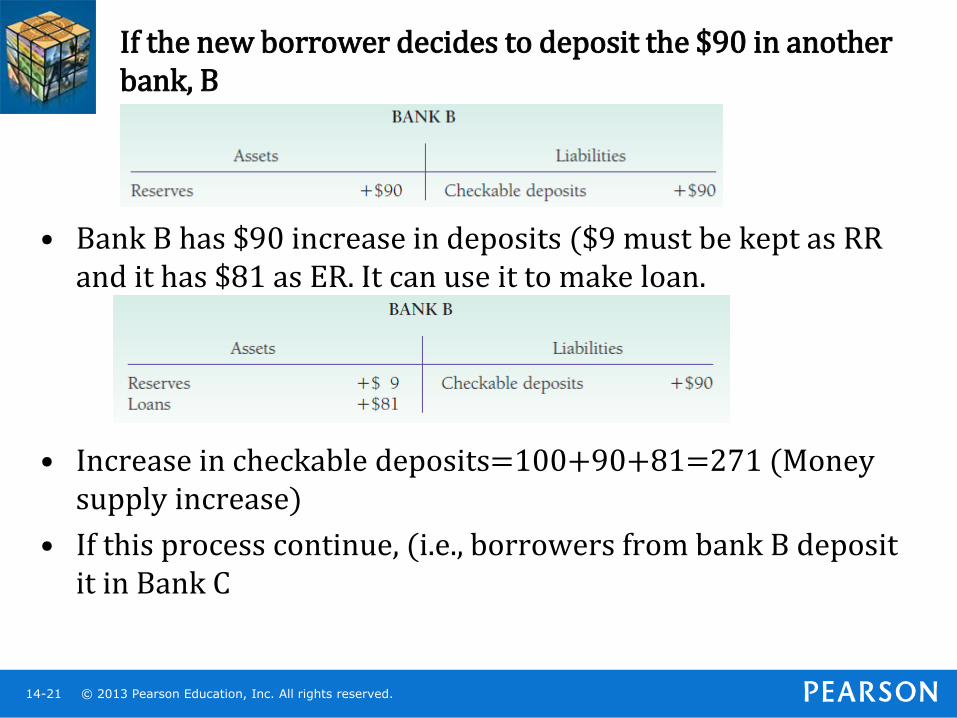

If the new borrower decides to deposit the $90 in another bank, B

• Bank B has $90 increase in deposits ($9 must be kept as RR and it has $81 as ER. It can use it to make loan.

• Increase in checkable deposits=100+90+81=271 (Money supply increase)

• If this process continue, (i.e., borrowers from bank B deposit it in Bank C

© 2013 Pearson Education, Inc. All rights reserved. 14-22

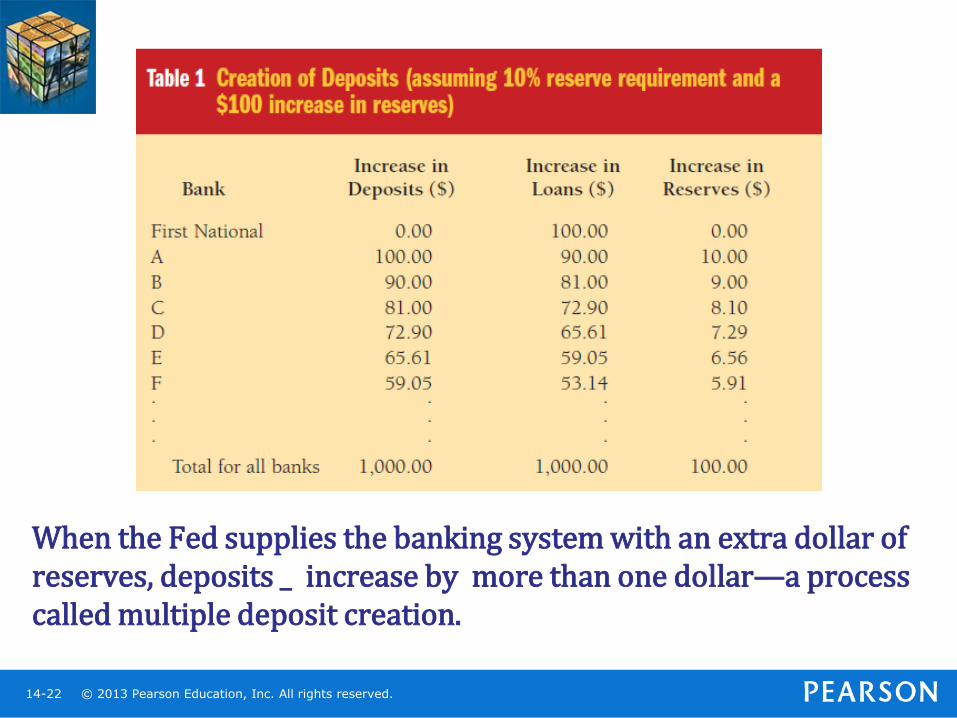

When the Fed supplies the banking system with an extra dollar of reserves, deposits _ increase by more than one dollar—a process called multiple deposit creation.

© 2013 Pearson Education, Inc. All rights reserved. 14-23

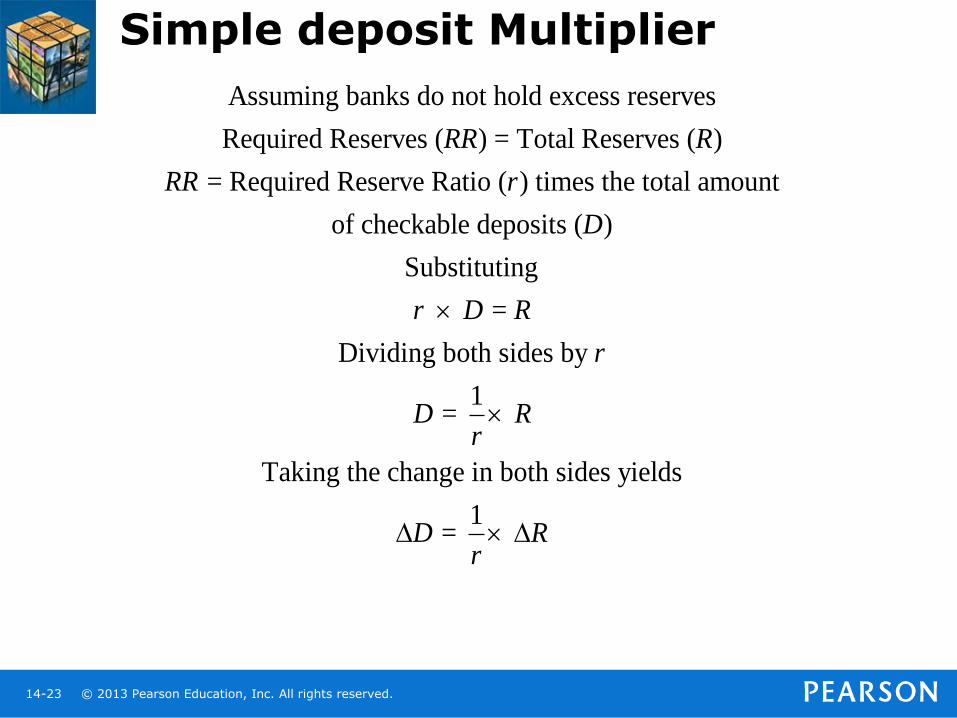

Simple deposit Multiplier

Assuming banks do not hold excess reserves

Required Reserves ( ) = Total Reserves ( )

= Required Reserve Ratio ( ) times the total amount

of checkable deposits ( )

Substituting

=

Dividing both s

RR R

RR r

D

r D R

ides by

1 =

Taking the change in both sides yields

1 =

r

D Rr

D Rr

© 2013 Pearson Education, Inc. All rights reserved. 14-24

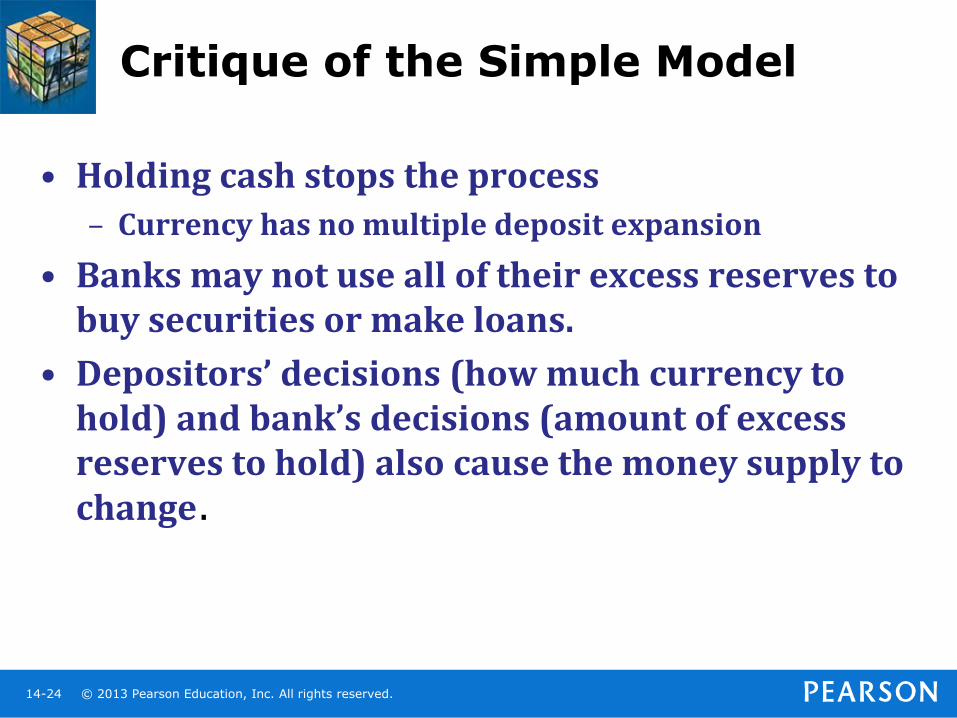

Critique of the Simple Model

• Holding cash stops the process

– Currency has no multiple deposit expansion

• Banks may not use all of their excess reserves to buy securities or make loans.

• Depositors’ decisions (how much currency to hold) and bank’s decisions (amount of excess reserves to hold) also cause the money supply to change.

© 2013 Pearson Education, Inc. All rights reserved. 14-25

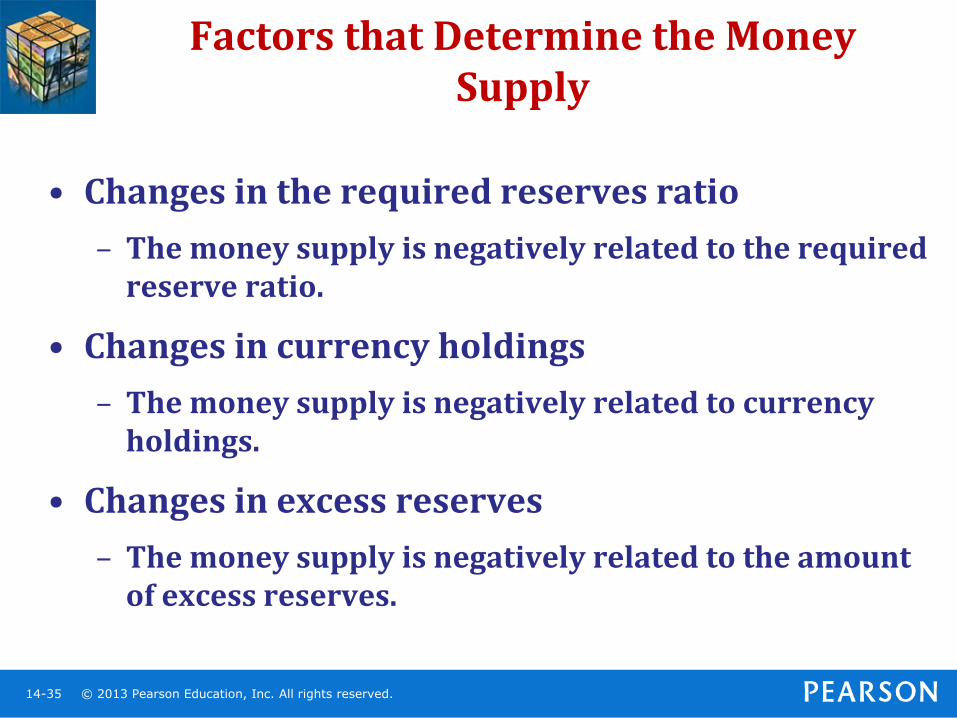

Factors that Determine the Money Supply

• Changes in the required reserves ratio

– The money supply is negatively related to the required reserve ratio.

• Changes in currency holdings

– The money supply is negatively related to currency holdings.

• Changes in excess reserves

– The money supply is negatively related to the amount of excess reserves.

© 2013 Pearson Education, Inc. All rights reserved. 14-26

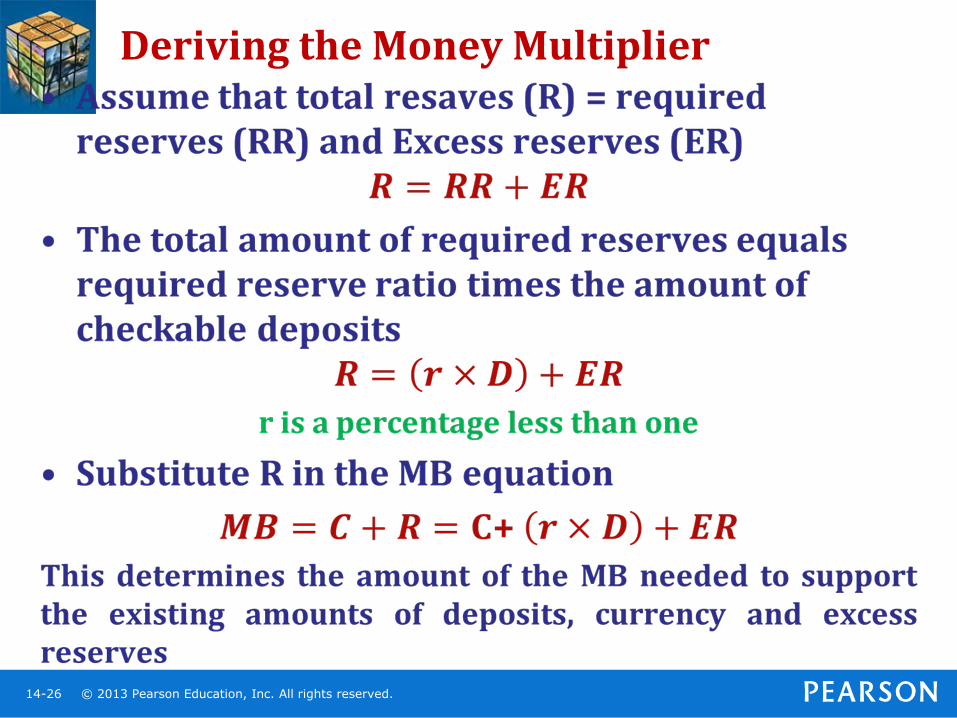

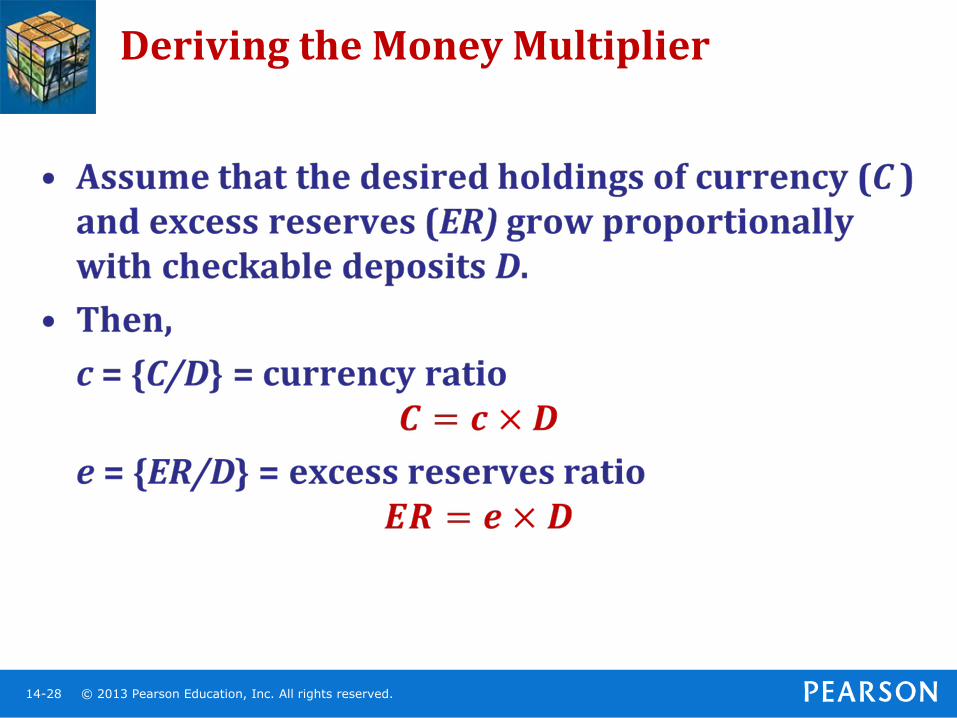

Deriving the Money Multiplier

© 2013 Pearson Education, Inc. All rights reserved. 14-27

The Money Multiplier

© 2013 Pearson Education, Inc. All rights reserved. 14-28

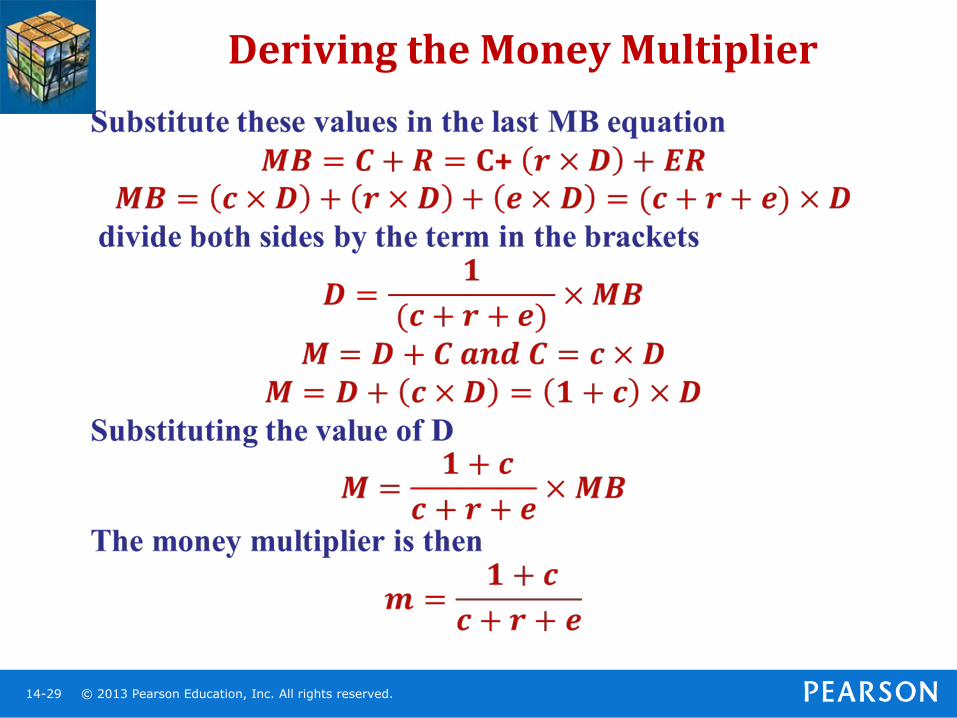

Deriving the Money Multiplier

© 2013 Pearson Education, Inc. All rights reserved. 14-29

Deriving the Money Multiplier

© 2013 Pearson Education, Inc. All rights reserved. 14-30

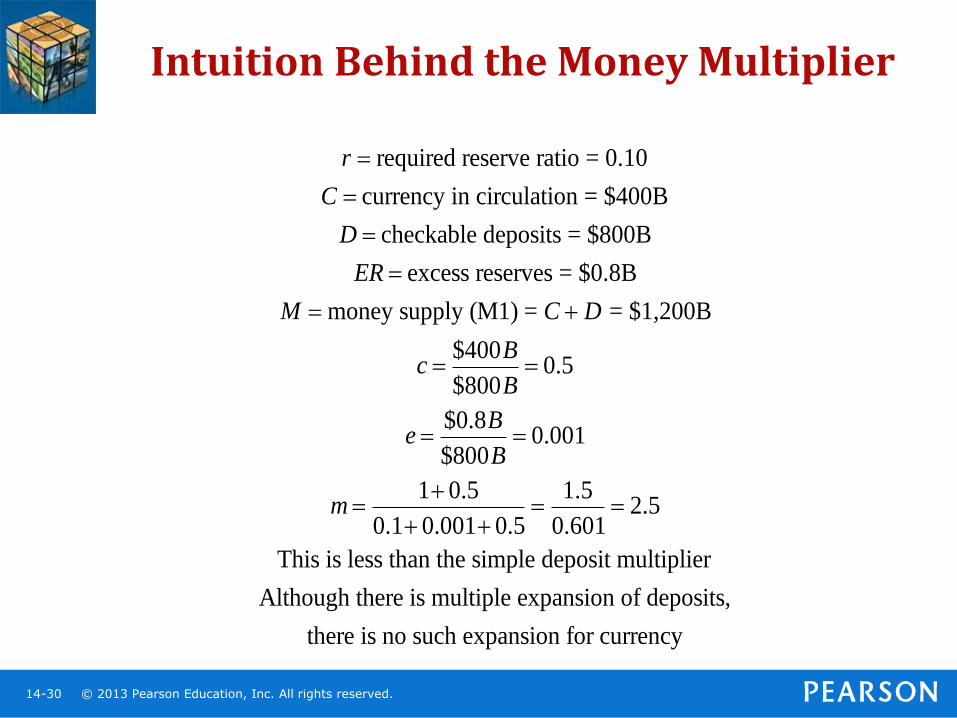

Intuition Behind the Money Multiplier

r required reserve ratio = 0.10

C currency in circulation = $400B

D checkable deposits = $800B

ER excess reserves = $0.8B

M money supply (M1) = C D = $1,200B

c $400B

$800B 0.5

e $0.8B

$800B 0.001

m 1 0.5

0.1 0.001 0.5

1.5

0.601 2.5

This is less than the simple deposit multiplier

Although there is multiple expansion of deposits,

there is no such expansion for currency

© 2013 Pearson Education, Inc. All rights reserved. 14-31

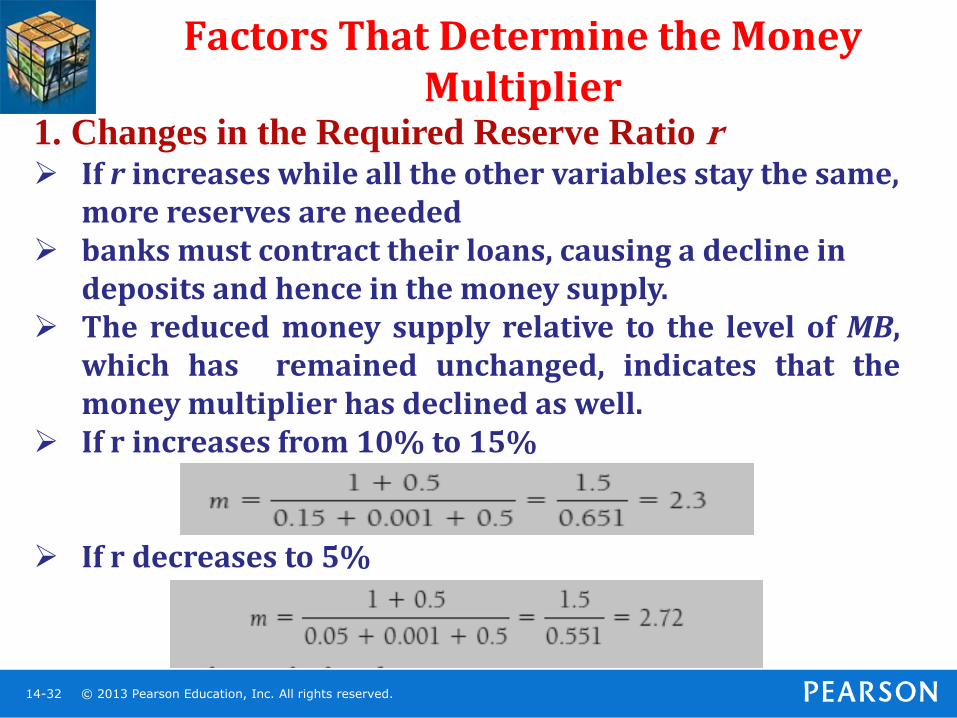

Factors That Determine the Money Multiplier

• Changes in the Required Reserve Ratio r

• Changes in the Currency Ratio c

• Changes in the Excess Reserves Ratio e

© 2013 Pearson Education, Inc. All rights reserved. 14-32

Factors That Determine the Money Multiplier

1. Changes in the Required Reserve Ratio r If r increases while all the other variables stay the same,

more reserves are needed banks must contract their loans, causing a decline in

deposits and hence in the money supply. The reduced money supply relative to the level of MB,

which has remained unchanged, indicates that the money multiplier has declined as well.

If r increases from 10% to 15%

If r decreases to 5%

© 2013 Pearson Education, Inc. All rights reserved. 14-33

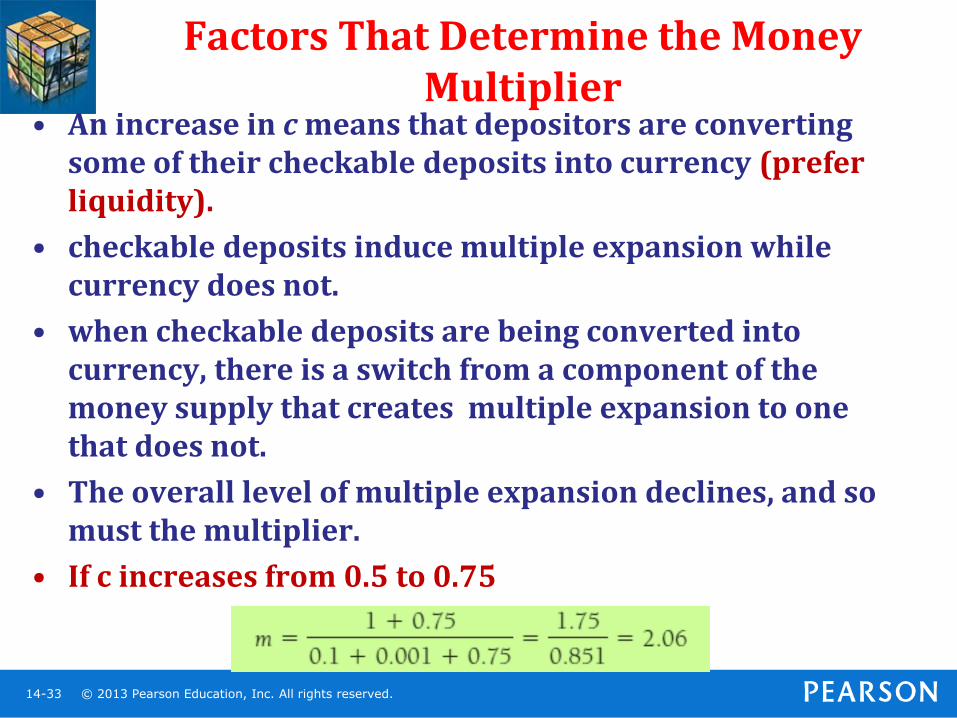

Factors That Determine the Money Multiplier

• An increase in c means that depositors are converting some of their checkable deposits into currency (prefer liquidity).

• checkable deposits induce multiple expansion while currency does not.

• when checkable deposits are being converted into currency, there is a switch from a component of the money supply that creates multiple expansion to one that does not.

• The overall level of multiple expansion declines, and so must the multiplier.

• If c increases from 0.5 to 0.75

© 2013 Pearson Education, Inc. All rights reserved. 14-34

Factors That Determine the Money Multiplier

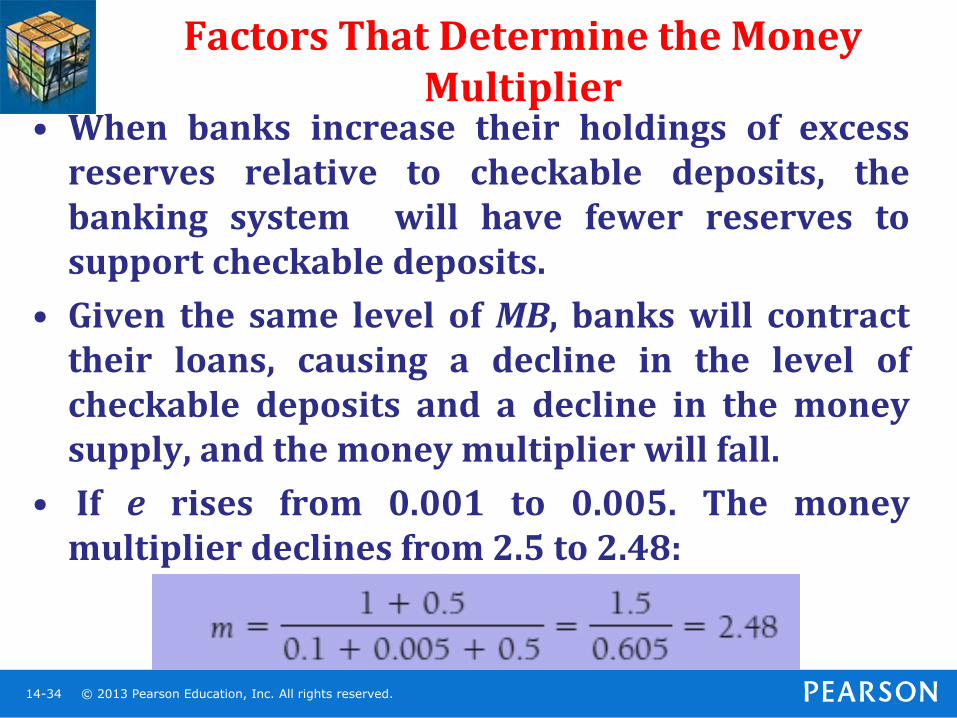

• When banks increase their holdings of excess reserves relative to checkable deposits, the banking system will have fewer reserves to support checkable deposits.

• Given the same level of MB, banks will contract their loans, causing a decline in the level of checkable deposits and a decline in the money supply, and the money multiplier will fall.

• If e rises from 0.001 to 0.005. The money multiplier declines from 2.5 to 2.48:

© 2013 Pearson Education, Inc. All rights reserved. 14-35

Factors that Determine the Money Supply

• Changes in the required reserves ratio

– The money supply is negatively related to the required reserve ratio.

• Changes in currency holdings

– The money supply is negatively related to currency holdings.

• Changes in excess reserves

– The money supply is negatively related to the amount of excess reserves.