Embed Size (px)

DESCRIPTION

finance

Citation preview

Retirement Planning

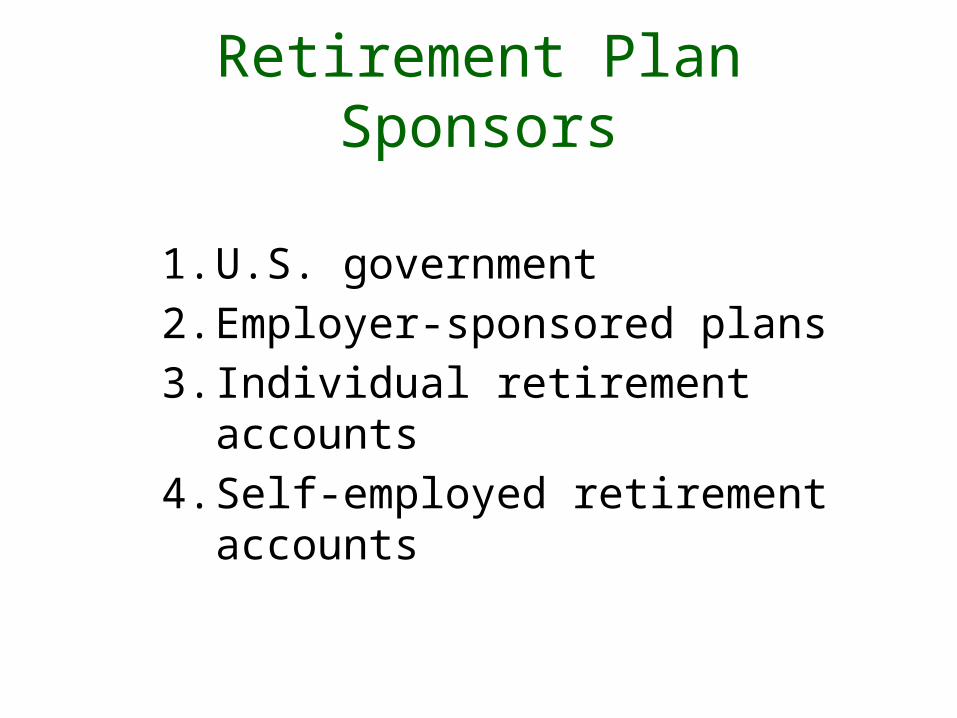

Retirement Plan Sponsors

1. U.S. government2. Employer-sponsored plans3. Individual retirement accounts4. Self-employed retirement accounts

Social Security

• Old-Age, Survivors, and Disability Insurance (OASDI) - Provides income to:– Covered individuals over age 65-67 (age 62 for

reduced benefits)– Surviving children or spouses of covered

individuals– Disability income to covered individuals and family

members

Average Monthly Social Security Retirement Benefit for an Individual

1990 1995 2000 2005 2006$0

$200

$400

$600

$800

$1,000

$1,200

603

720

844

1,0021,044

909947

9791,027 1,044

Current dollars Constant (2006) dollars

Ave

rage

Mon

thly

Ben

efit

Employer-Sponsored Retirement PlansDefined Benefit and Defined Contribution Plans in the U.S.

1990 to 2005

1990 1995 2000 20050

100

200

300

400

500

600

700

800

Num

ber o

f Pla

ns (T

hous

ands

)

Defined-benefit plans

Defined-contribution plans

Defined Benefit Plans

• Also called pension plans

• Promise a certain income on retirement

• Retirement income usually based on a multiple of last 3-5 years pay

• Employer responsible for investment risk

Defined Benefit PlansKey Items You Should Know About Your Plan

• Length of service needed until becoming vested in the plan

• Amount of contributions required by the employee

• How to compute the retirement benefit

• At what age can employee begin receiving benefits

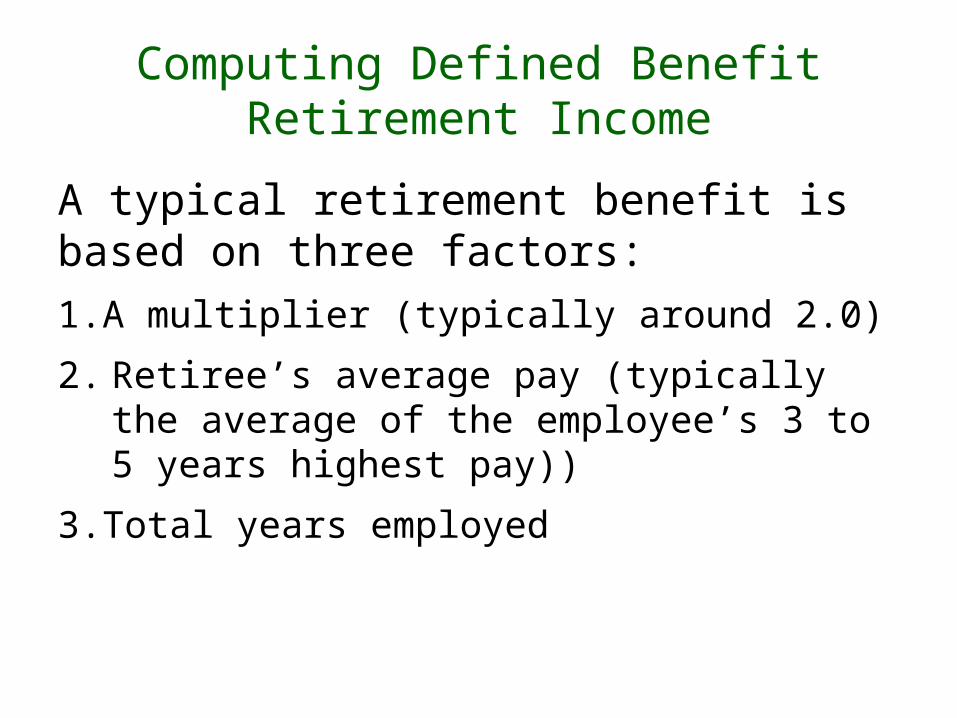

Computing Defined BenefitRetirement Income

A typical retirement benefit is based on three factors:1.A multiplier (typically around 2.0)

2. Retiree’s average pay (typically the average of the employee’s 3 to 5 years highest pay))

3.Total years employed

Example Defined Benefit Plan Terms

Retirement Benefit Formula:Annual retirement benefit = M x Years x Average Salarywhere: M = a multiplier such as 2.2

Years = years of employment with the employerAverage Salary = avg annual salary 5 highest paid years

Retirement Age and Benefits:100% of benefit at age 65 with a minimum of 10 years employment100% of benefit at any age with 35 years of employmentIf less than age 66 and age + years of employment >= 75 100% of benefit less 5% of benefit for each year less than 65

Vesting Schedule:Years

Employed Percent Vested2 20%3 40%4 60%5 80%6 100%

Employee Contributions:None

Defined Benefit PlanExample Benefit Calculation

Laura will have been working for Amalgamated Industries for 22 years at the end of this year when she plans to retire.

Amalgamated’s retirement plan pays an annual benefit of 2.1% times the employee’s average 5 years highest pay times the years of service. Laura’s last five years were her highest paid ones during which her average pay was $84,000.

Compute Laura’s monthly retirement income.

Annual retirement income = .021 x 84,000 x 22 = 38,808Monthly retirement income = 38,808/12 = 3,234

Defined Contribution Plans

• Employer and/or employee contribute to a retirement account

• Retirement benefit depends on the value of the account on retirement

• Beneficiaries, not employers, assume the investment risk of the account

Benefits of Defined Contribution Plans

• Tax break• Flexible investment options

Types of Defined Contribution Plans

• 401(k)• 403(b)• SEP• SIMPLE IRA• Profit-sharing plan• ESOP

Leaving a Job Before RetirementWhat Happens to Your Retirement Account?

1. Leave funds in the plan and draw benefits when you reach retirement age for the plan

2. Withdraw vested funds from plan and place them in another qualified plan

3. Transfer the plan to your new employer

Individual Retirement Accounts

• Traditional IRA– Contributions are tax deductible– Benefits are taxable

• Roth IRA– Contributions are not tax deductible– Benefits are tax-free

• Both plans allow account holder to begin withdrawing funds at age 59½

Retirement Accounts for Self-Employed Individuals

• Keogh plan• SEP

Financial Life Cycle

1. Education2. Employment3. Approaching retirement4. Retirement5. Estate planning

Start Saving for Retirement Early

20 25 30 35 40 45

$0

$500

$1,000

$1,500

$2,000

$2,500

$158$263

$442

$754

$1,317

$2,413

Monthly Savings Needed to have $1,000,000 by Age 60

Age When Starting to Save

Mo

nth

ly S

av

ing

s N

ee

de

d

Life Cycle Investing

Phase

Savings (Investment) Targets

Investment Horizon

RiskTaking Ability

Education Spend on education

Very long term High risk

Employment Save as much a possible

Very long term to long term

High risk

Approaching retirement

Continue saving

Intermediate term Balanced risk

Retirement Withdraw savings

Short term Low risk

Estate planning Bequests of savings

Short term Low risk

Implementing Life Cycle Investing

1. Select your own asset allocation2. Invest in life cycle mutual funds

a) Target-date life cycle fundsb) Target-risk life cycle funds

Estimating Retirement Fund Values

1. Constantly monitor account balances2. Perform scenario analyses