Embed Size (px)

Citation preview

Chapter 17

The Conduct of

Monetary Policy:

Strategy and

Tactics

(Lecture 2)

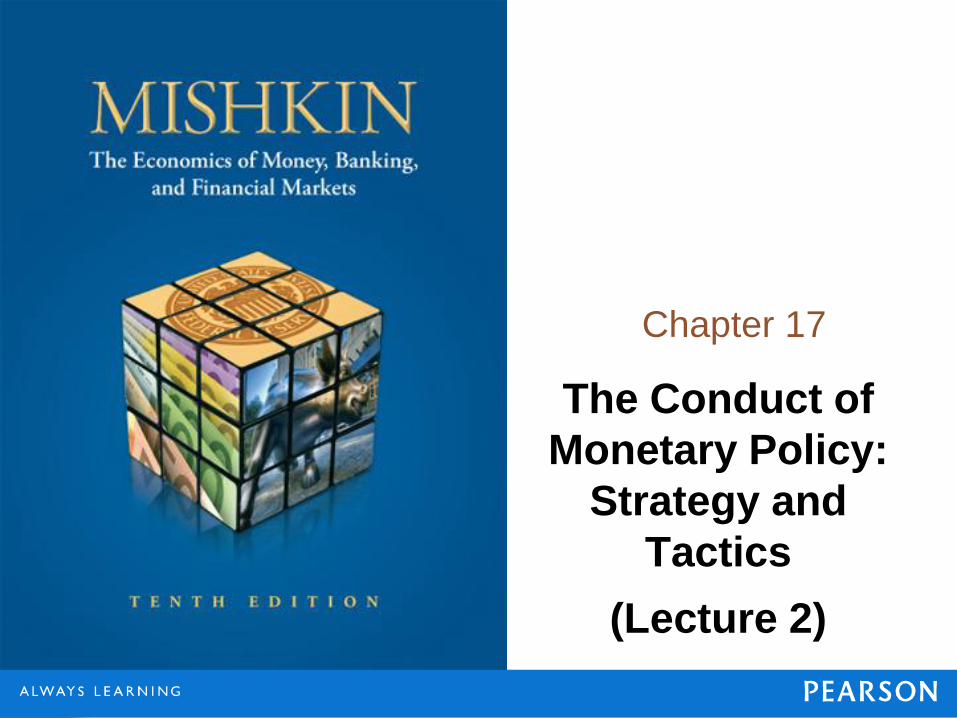

Lessons for Monetary Policy from the

Financial Crisis

• 1. Developments in the financial sector have a far greater impact on economic activity than was earlier realized

Importance of financial markets

• 2. The zero-lower-bound on interest rates can be a serious problem

Nonconventional tools to stimulate economy are less predictable

• 3. The cost of cleaning up after a financial crisis is very high

Economic growth is expected to be low for a decade after the crisis

• 4. Price and output stability do not ensure financial stability

Recent policy by the CBT

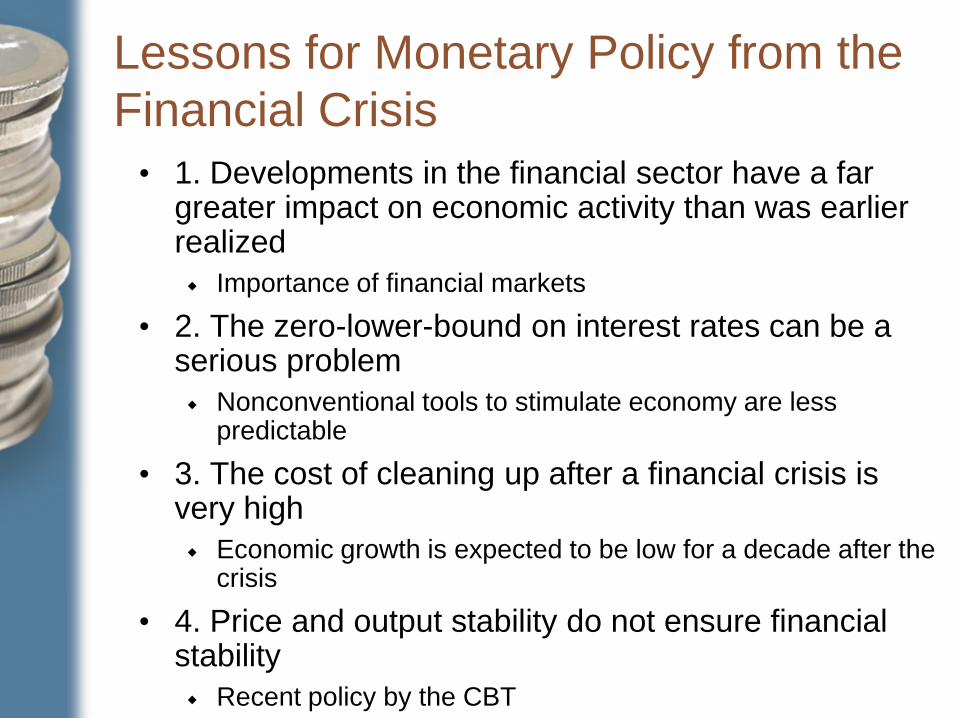

How should Central banks respond to

asset price bubbles?

Asset-price bubble: pronounced increase in asset prices that

depart from fundamental values, which eventually burst.

Alan Greeenspan (former chairman of the Fed): Central

Banks should not prick bubbles because:

• Bubbles are very difficult to identify. If CB knows, why wouldn’t market

participants know that prices are increasing beyond fundamentals

• Raising interest rates may or may not be effective in stopping such type

of buying behavior

• Monetary policy affects all markets broadly, not a specific market where

there is a bubble

• MP is a very powerful tool with strong consequences (unemployment,

decline in overall price level) that it may do more damage to the

economy while trying to prick the bubble

• It makes more sense to address the problem after the bubble bursts

• Types of asset-price bubbles

Credit-driven bubbles

• Most dangerous one for the economy

• Easy creditRise in asset valuesappreciation

of collateralmore lending for those assets

more demand for the assetsPrices go up

even more..

• Subprime financial crisis

Bubbles driven solely by irrational

exuberance

• Driven by expectations (e.g. Tech. Bubble of late

1990s

• Leaning against the bubble vs. cleaning the

bubble afterwards:

Recent crisis suggests that CBs should lean against credit-

driven bubbles rather than cleaning up afterwards

• Macropudential policy: regulatory policy to affect

what is happening in credit markets in the aggregate.

The idea is to curb excessive risk taking

Financial regulation and supervision to prevent excessive risk

taking

• Monetary policy: Central banks and other regulators

should not have a laissez-faire attitude and let credit-

driven bubbles proceed without any reaction.

Tactics: Choosing the Policy

Instrument

• Tools

Open market operation

Reserve requirements

Discount rate

• Policy instrument (operating instrument)

Reserve aggregates

Interest rates

May be linked to an intermediate target

• An intermediate target is a bridge between the policy instrument and the

ultimate goals of monetary policy

• An intermediate target is easier to measure relative to final goals

16-7

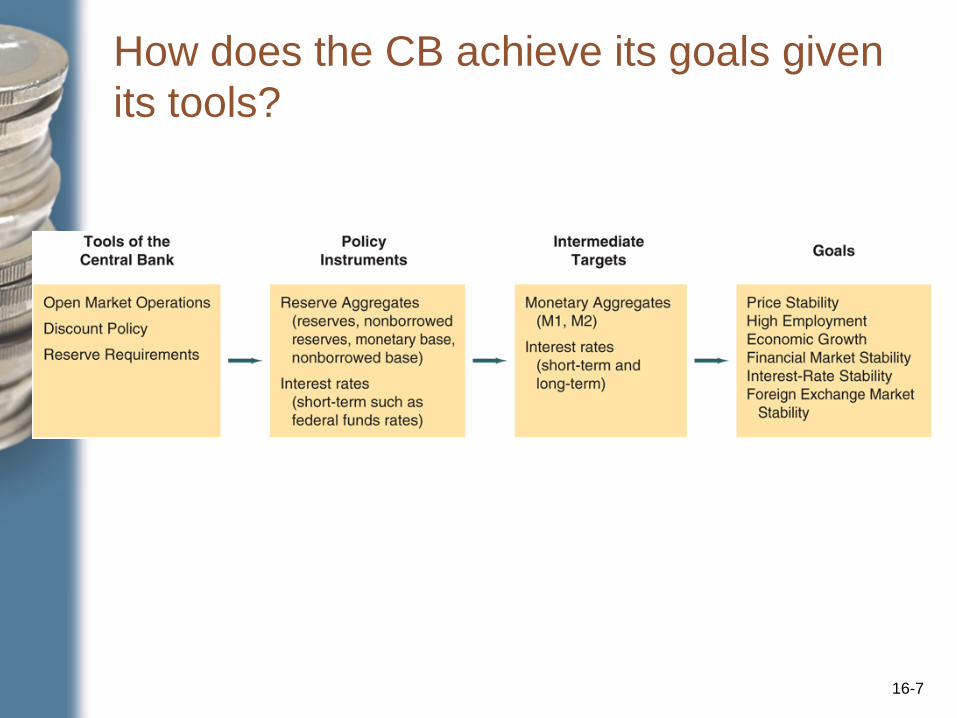

How does the CB achieve its goals given

its tools?

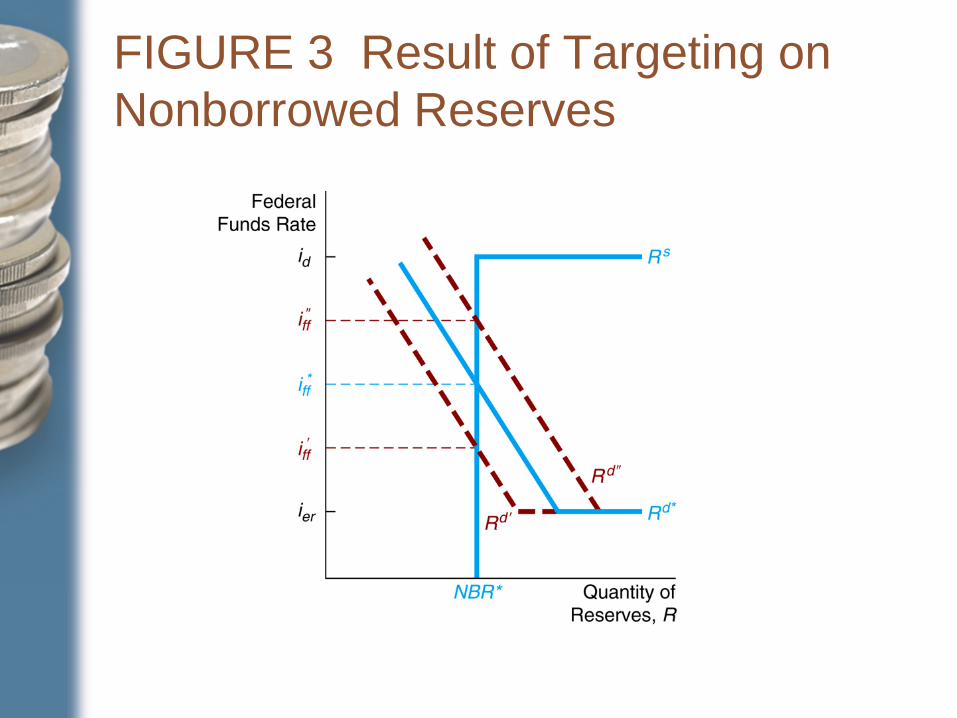

FIGURE 3 Result of Targeting on

Nonborrowed Reserves

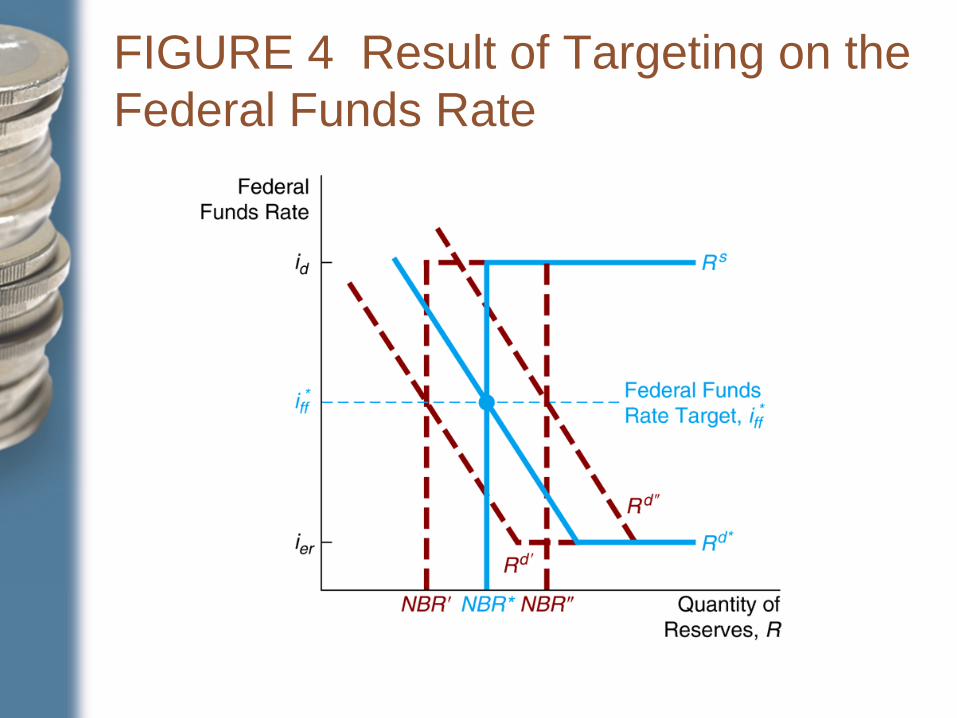

FIGURE 4 Result of Targeting on the

Federal Funds Rate

16-10

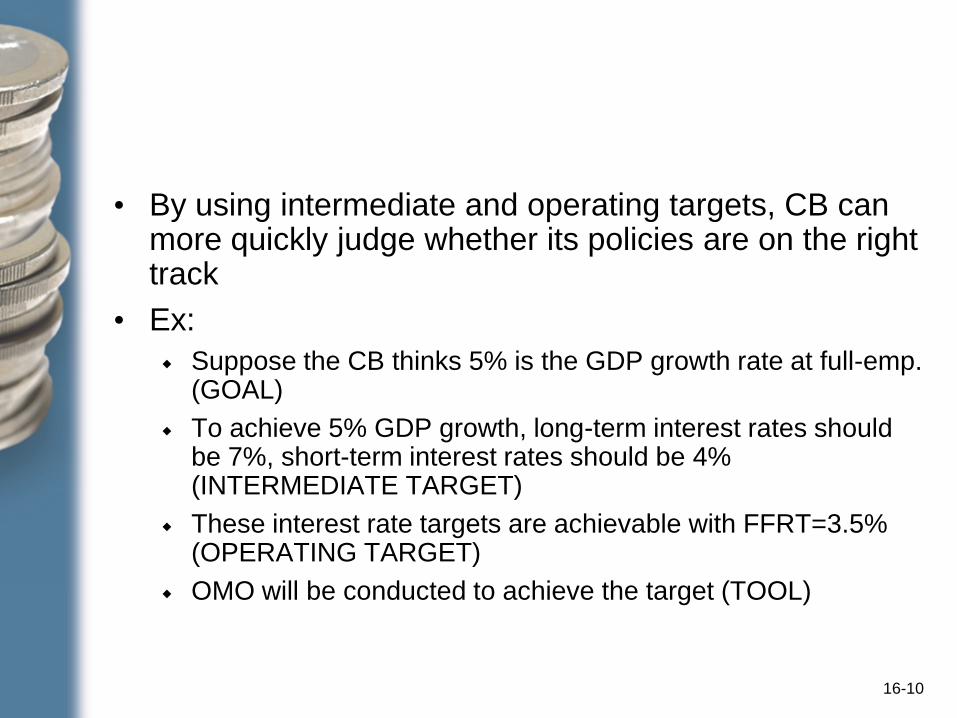

• By using intermediate and operating targets, CB can more quickly judge whether its policies are on the right track

• Ex:

Suppose the CB thinks 5% is the GDP growth rate at full-emp. (GOAL)

To achieve 5% GDP growth, long-term interest rates should be 7%, short-term interest rates should be 4% (INTERMEDIATE TARGET)

These interest rate targets are achievable with FFRT=3.5% (OPERATING TARGET)

OMO will be conducted to achieve the target (TOOL)

16-11

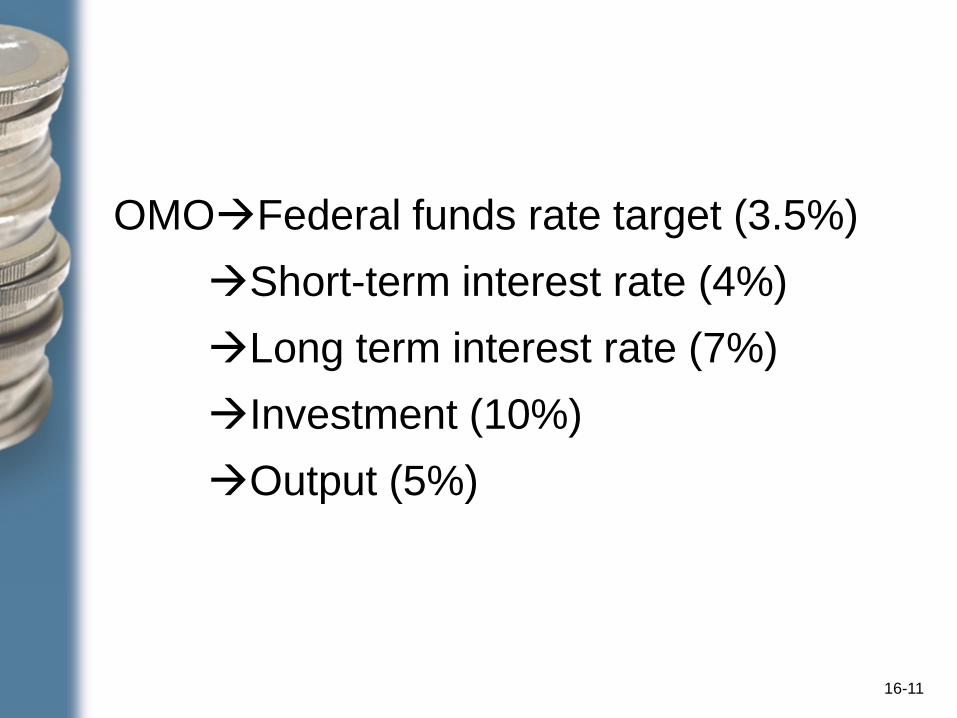

OMOFederal funds rate target (3.5%)

Short-term interest rate (4%)

Long term interest rate (7%)

Investment (10%)

Output (5%)

16-12

• Periodically, CB will check the growth

rates/levels of its intermediate targets and re-

adjust its operating target to achieve the

desirable level in its intermediate target

• Difficulty: In real life, it is hard to measure the

exact impact of your operating target on your

intermediate target or the precise link between

the intermediate target and the policy goals.

16-13

Criteria for

Choosing the Policy Instrument

• Observability and Measurability

The policy instrument must be easily

measured to be informative about where

MP stands

Nominal interest rates are measured faster

than monetary aggregates, however, real

interest rates are more difficult to measure

It is hard to choose between interest rates

vs. monetary aggregates based on this

criteria

16-14

• Controllability

The CB should have effective control over

the instrument.

CB has direct control on overnight nominal

interest rates and imperfect control over

money (which is determined by public

behavior)

CB’s control over longer term interest rates

is harder due to inflation expectations

It is hard to choose between interest rates

vs. monetary aggregates based on this

criteria

16-15

• Predictable effect on Goals

The control over intermediate target should imply indirect control over policy goals.

• Question: The Fed has switched from a monetary aggregates targeting to interest rate targeting. Why?

• Answer: The link between monetary aggregates and macroeconomic variables (output growth) weakened (Chapter 19)

End of chapter questions

• All but 8, 12, 16, 22, 23, 25

16-16