Embed Size (px)

DESCRIPTION

CHAPTER 18 H ost-Country Regulation: Corporate Law, Taxation, and Currency Risk. Host- Country Corporate Law Affecting Foreign Investment. Host country corporate law can impact the “bottom line”: - PowerPoint PPT Presentation

Citation preview

Copyright © 2009 South-Western Legal Studies in Business,

a part of South-Western Cengage Learning.

CHAPTER 18 CHAPTER 18 HHost-Country Regulation: Corporate ost-Country Regulation: Corporate Law, Taxation, and Currency RiskLaw, Taxation, and Currency Risk

2Copyright © 2009 South-Western Legal Studies in Business,

a part of South-Western Cengage Learning.

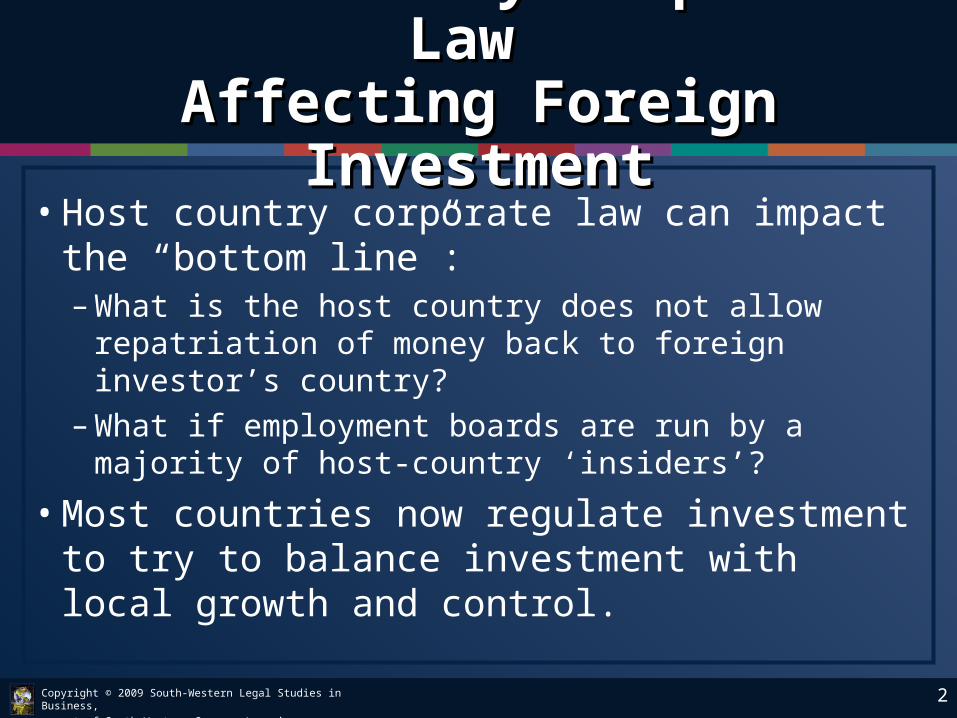

Host- Country Corporate Law Host- Country Corporate Law Affecting Foreign InvestmentAffecting Foreign Investment

• Host country corporate law can impact the “bottom line”:– What is the host country does not allow repatriation of

money back to foreign investor’s country?– What if employment boards are run by a majority of

host-country ‘insiders’?

• Most countries now regulate investment to try to balance investment with local growth and control.

3Copyright © 2009 South-Western Legal Studies in Business,

a part of South-Western Cengage Learning.

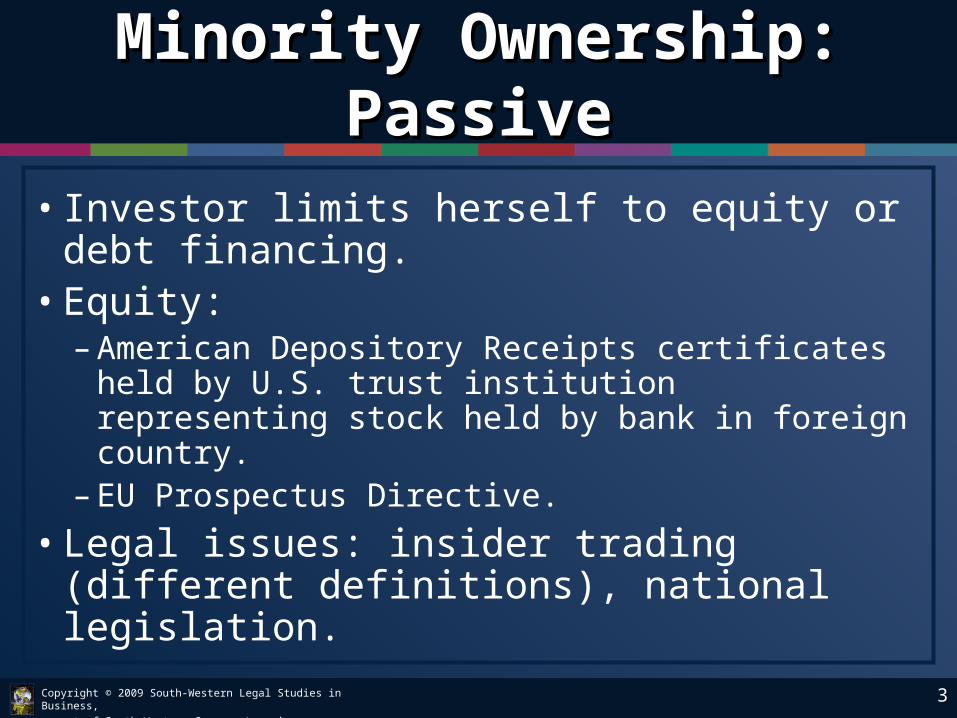

Minority Ownership: PassiveMinority Ownership: Passive

• Investor limits herself to equity or debt financing.• Equity:

– American Depository Receipts certificates held by U.S. trust institution representing stock held by bank in foreign country.

– EU Prospectus Directive.• Legal issues: insider trading (different

definitions), national legislation.

4Copyright © 2009 South-Western Legal Studies in Business,

a part of South-Western Cengage Learning.

Minority Ownership: ActiveMinority Ownership: Active

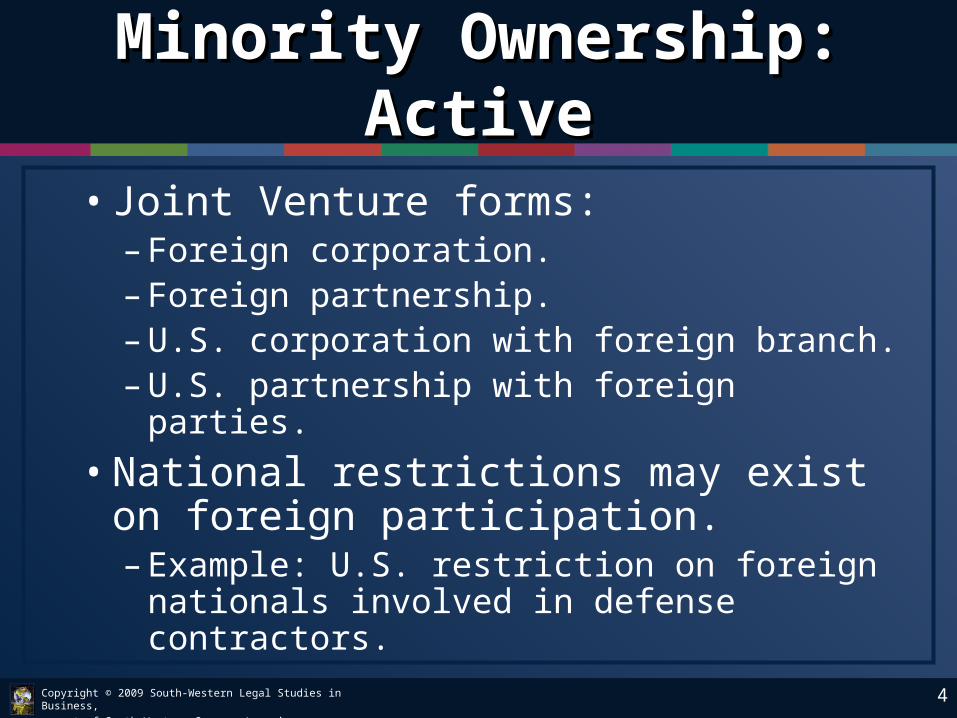

• Joint Venture forms:– Foreign corporation.– Foreign partnership. – U.S. corporation with foreign branch.– U.S. partnership with foreign parties.

• National restrictions may exist on foreign participation.– Example: U.S. restriction on foreign nationals

involved in defense contractors.

5Copyright © 2009 South-Western Legal Studies in Business,

a part of South-Western Cengage Learning.

Majority Ownership and SubsidiariesMajority Ownership and Subsidiaries

• Reason: Foreign company can exercise greater control, but some countries either forbid 100% foreign ownership or impose high taxes.

• Option: create a foreign branch subsidiary.

6Copyright © 2009 South-Western Legal Studies in Business,

a part of South-Western Cengage Learning.

What Is the Difference Between a What Is the Difference Between a Subsidiary and a Branch?Subsidiary and a Branch?

• Control.• Tax.• Liability.• When might you consider a branch first?

7Copyright © 2009 South-Western Legal Studies in Business,

a part of South-Western Cengage Learning.

Tax Issues: Tax Issues: Bank of America v. U.S.Bank of America v. U.S.

• Foreign tax credits - in the U.S. you get credit on U.S. income tax on foreign taxes paid. See the Bank of America Nat’l Trust & Savings Assn. v. United States case. Holding: BOA petition dismissed tax credits appeal.

8Copyright © 2009 South-Western Legal Studies in Business,

a part of South-Western Cengage Learning.

Tax Issues: E-CommerceTax Issues: E-Commerce

• Should the internet be a “tax free” zone?• Great variation among regions:

– All EU purchases subject to a VAT tax, from 15-25%.– EU treats downloadable music as a “service.”

• Transfer pricing - to prevent tax evasion require intercompany transactions at arms length prices.

9Copyright © 2009 South-Western Legal Studies in Business,

a part of South-Western Cengage Learning.

Tax IssuesTax Issues

• Foreign sales corporation - legal mechanism to reduce taxes. See the Compaq Computer case.

• U.S. Enforcement of Foreign Tax Laws. – David B. Pasquantino v. United States: Supreme

Court held that Department of Justice has the power to prosecute Americans for the evasion of foreign tax laws.

10Copyright © 2009 South-Western Legal Studies in Business,

a part of South-Western Cengage Learning.

Foreign Control IssuesForeign Control Issues

• Virtually every country prohibits foreign entities in sensitive sectors.

• US outlaws foreign investment in “national security” fields such as telecommunications, air transportation, and military procurement.

• Mexico has now changed its laws to allow up to 100% foreign investment.

• Investor reaction to limits has always been negative.

11Copyright © 2009 South-Western Legal Studies in Business,

a part of South-Western Cengage Learning.

Controlling Currency RiskControlling Currency Risk

• Inconvertibility: make agreement with government regarding currency exchange results & import substitution rights.

• Minimizing Fluctuation Risks: Currency Swaps.• Arrangements with the Soft-Currency Country.• Payment and Price Adjustment Approaches.

12Copyright © 2009 South-Western Legal Studies in Business,

a part of South-Western Cengage Learning.

Controlling Currency RiskControlling Currency Risk

• Structuring of Hard-Currency Obligations and Revenues.

• Countertrade.– Counterpurchase.– Barter.– Offsets.– Buy-Back.

• Consortia or parallel exchange.

![biuletyn_2013_v3 [ost.]](https://img.pdfslide.net/doc/110x75/55cf8d225503462b139255a6/biuletyn2013v3-ost.jpg)