Embed Size (px)

Citation preview

Chapter 24. The open economy with fixed exchange rates

ECON320Prof Mike Kennedy

Fixed exchange rates as a policy regime

• From the previous chapter we know that the choice of an exchange rate regime has no effect on the long run equilibrium of an economy

• But that choice has important implications for how an open economy will adjust in the short run

• It also determines whether monetary or fiscal policy is a useful tool for stabilization

• This chapter will examine the implications for adjustment when a country adopts a fixed exchange rate

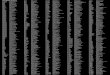

• Canada, like many other countries, has had experience with both fixed and flexible exchange rates

Canada has had experience with fixed exchange rates

0.60

0.70

0.80

0.90

1.00

1.10

-0.25

-0.0500000000000002

0.15

0.35

0.55

0.75

0.95

1.15Recession CanadaForeign exchange rate (an increase is an appreciation)

Fixed exchange rate period

The impotence of monetary policy under fixed exchange rates

• With perfect capital mobility we have

• With fixed exchange rates, the currency is not expected to change so we have

• This equality of nominal interest rates is enforced by the central bank’s commitment to keep the nominal exchange rate pegged to that of the foreign country

The case for adopting a fixed exchange rate

• Facilitates trade by reducing (eliminating) exchange rate risks– While short-term exchange rate risks can be covered in the forward

markets, long-term one typically cannot be

• Flexible exchange rates often overshoot their equilibrium values, sometimes for extended periods of time– The concern here is about excessive exchange rate changes which can

have serious effects on a country’s competitive position

• Provides a nominal anchor to help bring down inflation (e.g., the UK and other high-inflation European countries)– In effect, a country can “import credibility” by pegging to a country

which has a better record on keeping inflation low

Euro area inflation rates fell as countries moved to adopt a common currency

y-1980

y-1981

y-1982

y-1983

y-1984

y-1985

y-1986

y-1987

y-1988

y-1989

y-1990

y-1991

y-1992

y-1993

y-1994

y-1995

y-1996

y-1997

y-1998

y-1999

y-2000

y-2001

y-2002

y-2003

y-2004

y-2005

y-2006

y-2007

y-2008

y-2009

y-2010

y-2011

y-2012

y-2013

y-2014

y-2015

y-2016

y-2017

y-2018

y-2019

-5

0

5

10

15

20

25

30

35

Belgium Denmark France Germany

Greece Ireland Italy Luxembourg

Netherlands Portugal Spain

Another measure of inflation convergence

y-1980

y-1981

y-1982

y-1983

y-1984

y-1985

y-1986

y-1987

y-1988

y-1989

y-1990

y-1991

y-1992

y-1993

y-1994

y-1995

y-1996

y-1997

y-1998

y-1999

y-2000

y-2001

y-2002

y-2003

y-2004

y-2005

y-2006

y-2007

y-2008

y-2009

y-2010

y-2011

y-2012

y-2013

y-2014

y-2015

y-2016

y-2017

y-2018

y-2019

-15

-10

-5

0

5

10

15

20

25

30

plus/minus 2 Std Deviations

Mean of inflation in euro area

Inflation, exchange-rate dynamics and the AD curve• When the nominal exchange rate is fixed it follows that the real

exchange rate changes only with relative inflation rates

• The real exchange rate is constant only when

• The above is a condition for long-run equilibriumThe AD-AS curves• With fixed exchange rates the AD curve in Slide 15, Chapter 23

becomes

• Note that– The ∆e is no longer present because it does not change– The second term includes only foreign monetary policy variables

• The AS curve is

Expectations formation under credibly fixed exchange rates

• To complete the model, we need to specify how inflation expectations are formed

• Assume that there are two groups in the economy– Group 1: Backward looking so that πe = π-1

– Group 2: Rational and realise that πe = πf

• If group 2 is a fraction φ of the total then

• We start by assuming that φ = 1, called weakly rational expectations, so that

• The above says that the authorities have implicitly adopted the foreign inflation rate as their target – in this case monetary policy is determined in the foreign country

The complete AD-AS model The AD curve

The SRAS

The real exchange rate

• The AD curve is downward sloping in relation to inflation since a rise in domestic inflation reduces the competitive position of domestic goods thereby reducing y

• The variable z represents real shocks, which now include changes in foreign as well as domestic variables

From a short run to the long-run equilibrium

• Assume that the economy’s is initially in recession shown as A1 in the following slide

• The recession has driven π lower which will improve the economy’s competitive position – exports are now cheaper, imports more expensive

• This improvement in competitiveness drives the economy back to its long-run equilibrium position

• If π ≠ πf then er ≠ er-1 and the economy will enter the next period with a

new predetermined real exchange rate not equal to er

• In the figure, the new exchange rate is shown in brackets after each AD curve

• Note that the SRAS does not shift since we assume that πe is firmly anchored on πf

• In equilibrium the domestic inflation rate is equal to foreign inflation rate and er will equal 0, its long run value (remember ln(Er =1) = 0)

• Note that adjustment is endogenous with fixed exchange rates – there is no Taylor driving short-term interest rates as in a closed economy

The adjustment to long-run equilibrium under fixed exchange rates

Stability and adjustment speeds• As in chapter 18 we start with• The three equations of the model are now

• Inserting SRAS into AD and solving for

• The strategy is to plug the above plus the SRAS for into the third equation and solve for (see next slide)

Finding whether or not the model is stable

• Performing the required substitutions we get

• We can see from the above that 0 < β < 1 so the economy will converge to an equilibrium where

Finding whether or not the model is stable con’t

• The speed of adjustment will depend on the size of β1

– The larger is β1, that faster the adjustment speed

• The coefficient β1 in turn measures the responsiveness of the economy to the real exchange rate and is defined as

• This key coefficient depends on the Marshall-Lerner condition being not only satisfied but large enough to offset the term

• Based on the values noted in the text, β around 0.82, which implies a half life of 3½ years

Unsystematic fiscal policy: A temporary increase in government spending

• The figure shows the effect of unsystematic temporary change in fiscal policy

• The increase in g in period 1 shifts the AD curve to AD1 and raises inflation to π1

• In period 2 the fiscal stimulus is removed but with inflation now higher than πf the real exchange rate has risen worsening the countries competitive position and pushing the AD curve to AD2, which is below the original equilibrium position A0

• With output below potential inflation now moves back toward πf and the real exchange rate returns to its equilibrium level

• Note again that the SRAS does not change since we have assumed that inflation expectations remain firmly anchored at the foreign rate of inflation

A temporary fiscal expansion

Systematic fiscal policy• Imagine we have the following reaction function (fiscal policy is

assumed to react to the business cycle – it is counter-cyclical)

• Inserting the above into the original AD curve we get a new AD

• The AD curve with active fiscal policy (a > 0) now has a steeper slope • The figure in the next slide shows the short-run effect of a negative

demand shock under both regimes• The shock shifts the AD curve down by an amount but depending on

the slope of the AD curve the effect on output and inflation are different

• When fiscal policy is active, output and inflation fall by less

Negative demand shocks with passive versus counter-cyclical fiscal policy

Systematic fiscal policy with an unfavourable supply shock

• The figure next slide shows the effect of an unfavourable supply shock

• Again with active fiscal policy the drop in output is less compared with the case of passive fiscal policy but now inflation is higher

• In the case of supply shocks, the government faces a trade off• Using the same procedure as above, we see that now the speed of

adjustment back to equilibrium is slower when fiscal policy is active

• At the same time the initial displacement from equilibrium from long-run equilibrium is less under active fiscal policy

• Governments may be willing to accept a reduction in the speed of adjustment if it means a smaller deviation from long-run equilibrium

Negative supply shocks with passive versus counter-cyclical fiscal policy

Exchange rate policy

• Governments can also change the parity rate• Here we examine an unanticipated devaluation• If the devaluation is unanticipated and the government credibly

commits to the new fixed rate then • Using this the AD curves becomes

• The AD curve shifts up in period 1 because of the improved competitive position (see figure next slide)

• The higher inflation rate will now cause the AD curve to shift back towards A0 – the devaluation is neutral in the long run

The effects of an unanticipated devaluation

Exchange rate policy: The long run when the devaluation was unanticipated

• To see this remember that in long-run equilibrium we get

• Inserting these conditions into the AD curve we can solve for the long-run equilibrium exchange rate

• This equation shows that the nominal exchange rate plays no role in the determination of the real long-run exchange rate

An unanticipated devaluation

• In the figure next we see how an unanticipated devaluation can be used to shorten the length of a recession

• In the case the output gap in reduced by moving the short run equilibrium from A0 to A0’

Speeding up the adjustment with an unanticipated devaluation

An anticipated devaluation

• As often as not, devaluations are anticipated, at least partially• To examine the process we need to go in three stages• We start in short run equilibrium in period 0 and assume that the

devaluation is to take place in period 2• Stage 1: The anticipation effect of devaluation

– The equation shows the rate of devaluation expected to occur in period 2 compared with what actually occurs

where ϕ is an estimate of the devaluation – Because of arbitrage the domestic nominal interest rate in period 1 must be

– Expectations of inflation, which itself will be raised by the devaluation, are formed before the devaluation (referred to by the superscript eb) are given by

where θ2 represents the extent to which inflation is expected to rise due to the anticipated devaluation

An anticipated devaluation• Stage 1: continued• The domestic real interest rate depends on the expected rate of price

between periods 1 and 2

• The equation says that the domestic real interest rate will rise above the foreign real interest rate provided that the devaluation is at least partially anticipated so that ϕ >0

• In the absence of shocks, equilibrium in the goods market is given by

• From the definition of the real exchange rate we have

• The AD curve now becomes

An anticipated devaluation

• Stage 1: continued• Reproducing the AD curve for comparison

• In period 0, with no expectations of a devaluation then

• Expectation of a devaluation shifts the AD curve in period 0 downward by

(see next slide)• The expectations pushes the domestic real interest rate above

the foreign rate which pushes the economy into recession• Since the devaluation does not occur until period 2, the SRAS

is unaffected – that is, expected inflation has not changed

The anticipation effect of a devaluation

An anticipated devaluation

• Stage 2: The implementation of an anticipated devaluation• We assume that the devaluation takes place prior to price-

and wage-setting behaviour and investment decisions • Once the magnitude of the devaluation is known, decisions

will be based on the expected inflation rate which is

• In period 2 the SRAS is , which when subbed into the above yields

• The SRAS now has an additional term (θ2∆e2) which shows the amount by which the SRAS shifts up

An anticipated devaluation

• Stage 2: The implementation continued• Next we need to determine what happens to AD• The AD curve for period 2 is

• The real exchange rate for period 2 is now

• Assuming that the implementation of the new exchange rate is credible (it is expected to stay constant) then i2 = if

• But the devaluation will affect inflation in period 3

• Subbing in these last two equation into the first we get AD2

An anticipated devaluation• Stage 2: The implementation continued• The AD curve in period 0 is

• The new AD curve (last equation previous slide) is

• The comparison shows that AD2 has shifted to a point above the original equilibrium (see figure final slide)– The temporary drop in π in period 1 coupled with the period 2

devaluation has improved competitiveness ( )– The domestic real interest rate falls because expected inflation has

risen as measured by

• While the SRAS will shift the devaluation effect is sufficiently strong to insure that output rises

An anticipated devaluation

• The basic insight of the above complex analysis– An expected devaluation may create a boom-bust scenario– Initially output falls as fears of a devaluation cause capital to flow out of

the country and domestic interest rates rises– When the devaluation occurs, the economy’s competitiveness improves

and real interest rates fall

Stage 3: Long-term adjustment to an anticipated devaluation• After the devaluation occurs π > πf and competitiveness starts to

worsen• The AD curve will shift back, pushing inflation and output back

towards equilibrium• In the end, the devaluation has no effect on the long-run values

of output and inflation

The implementation effects of a devaluation which is partly anticipated