Embed Size (px)

Citation preview

Chapter 26:Learning Objectives

The Bank for International Settlements: History & Operations

The International Monetary Fund & World Bank: History and Operations

European Institutions: EBRD, EMS & EMU

The Workings of the EMS Target Zone

Why did International Financial Institutions Emerge?

Began as a way of reducing the dangers associated with “beggar thy neighbour” policies

Also, institutions were needed to coordinate post-war recovery and management of reparations

The growth of international trade and capital movements also necessitated some international institutions

Bank for International Settlements

Originally formed to deal with Germans reparations after WW I

Became a forum for central bankers to discuss common issues

Members include industrialized as well as other central banks representatives (25+ countries and growing)

Managed by a Board which includes members from central banks and member countries Treasuries

BIS cont’d

Activities include: Buying/selling of gold lending to member countries issuance and marketing of securities negotiate international financial agreements (e.g.,

BIS capital standards; CHAPTER 10) forum for discussion of international monetary

issues

International Monetary Fund

Outcome of post-war plans by the US and UK mainly

Major goal was to improve financial coordination and avoid problems with the gold standard, namely deflation and lack of independence in monetary policy

Member countries have voting rights roughly a function of the volume of trade in the world

Created at Bretton Woods, NH, where the founders agreed to an “adjustable peg” system of exchange rates

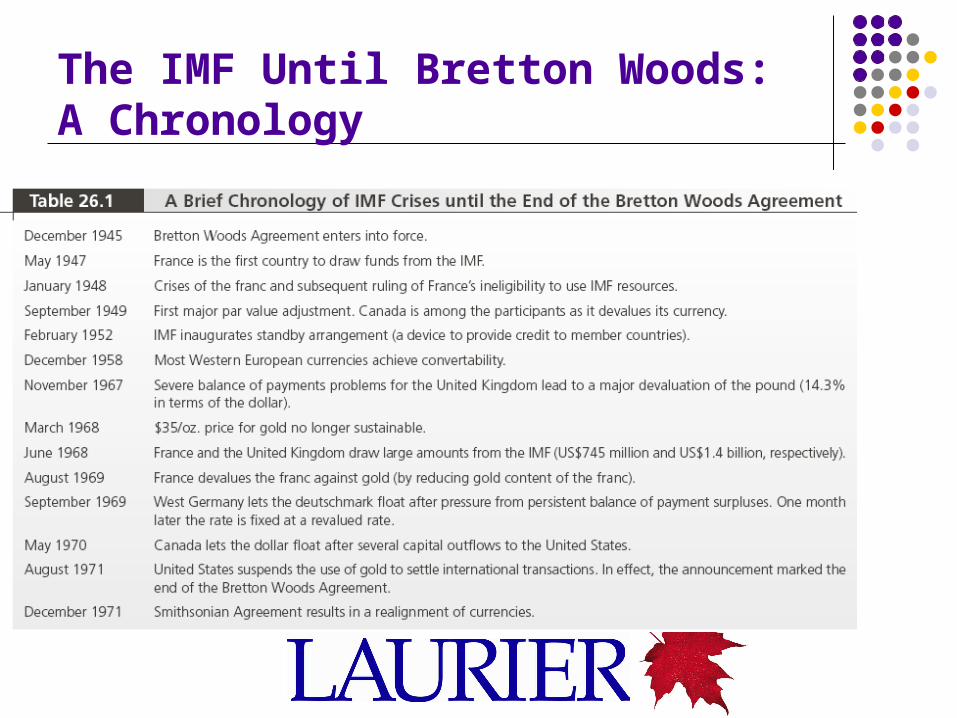

The IMF Until Bretton Woods: A Chronology

IMF cont’d

The BW system permitted a +/- 1% fluctuation in exchange rates around the “par” rate

Devaluations permitted only if “chronic” BOP difficulties arose

The US $ and UK £, along with gold, were the “reserve” currencies at first

The “par” exchange rate was vis-à-vis the US $ and members could convert into gold @ $35/oz.

IMF cont’d

BW was flawed because the system assumed the US would not inflate and that it would run a BOP deficit in perpetuity

Germany, in particular, eventually had to revalue its currency continuously until it was no longer willing to do so

The IMF is no stranger to controversy especially because of its “conditionality” programs

Nixon took the US of the gold standard effectively ending BW

The Future of the IMF

Most countries are adopting flexible exchange rates and full capital mobility, putting in question IMF’s mission

International expectations for the IMF to ensure financial stability has increased, especially since the 1994-95 Mexican crisis and the Asian crisis of 1997-98

Should the IMF become an international lender of last resort? An international credit rating agency?

World Bank

Created at the same time as the IMF to facilitate reconstruction and development through access to liquidity

Borrows on the open market and makes different types of loans to developing countries

Coordination with sister institution - the IMF - to monitor and assist in meeting conditionality requirements

The European Monetary System

Organized with the ending of BW in 1972 Originally called the “snake” and consisted

essentially of the Benelux, Germany, and France In 1979 renamed the EMS or ERM Member countries grew as the EC grew and

eventually led to the Maastricht Treaty of Monetary Union in 1991

The EMS has essentially the same flaws as BW but is currently far more flexible (i.e., wider bands, more realignments)

Real Effective Exchange Rates in 5 EMS Countries

80

90

100

110

120

130

140

80 82 84 86 88 90 92 94 96 98

FRANCE GERMANY ITALY NETHERLANDS UK

Rea

l effe

ctiv

e ex

chan

ge r

ate

(199

5=10

0)

The Target Zone Model: Hypothetical Illustration

Exchange rate

TIME< realignment

Target Zone

Actual exchange rate

Central parity

Franc/Deutschmark Exchange Rates

2.0

2.4

2.8

3.2

3.6

4.0

80 81 82 83 84 85 86 87 88 89 90 91 92

Exp

ecte

d R

ate

of D

epre

ciat

ion

(%) Upper limit

of target zone V

^Lower limit oftarget zone < Realignment

Exp Rate of Dep'n 3 months ahead V

The EMS cont’d

With Maastricht comes EMU or European Monetary Union

In 1998, the members of EMU were announced (11 countries)

EMU participants were thought to have satisfied the “convergence” requirements (inflation, interest rates, govt debt)

The “Euro” was launched in 1999 while the European Central Bank was launched in 1998

Conversion rates to the Euro

European Central Bank

Considered perhaps the most independent central bank in the world

Its principal objective is price stability defined as inflation in “Euroland” < 2%

To achieve its objective the ECB also monitors money growth and the exchange rate (two of the three “pillars” of monetary policy)

The creation of the ECB has raised interest in currency unions, especially in Canada

Currency Unions

What are the ideal determinants of a currency area? What is an optimum currency area? Labour mobility: allow movement to regions with

greater labour demand Capital mobility: funds should be able to seek out

highest available return for given risk Openness and regional interdependence: close trading

relationship reduces need for separate currency Industrial and portfolio diversification: eases impact of

shocks Wage and price flexibility: replaces the primary

function of the exchange rate

Point Counterpoint: Should Canada drop its currency?

POINT: Lower transactions costs Connection between

fundamentals and exchange rate unclear

Facilitates trade between countries

More price competition Encourages labor

mobility

COUNTERPOINT: Transactions costs

savings small BOC equation suggests

that exchange rate is an important shock absorber

Canada’s monetary policy pretty good

Since NAFTA scope for price competition is small

Summary

This chapter surveys international financial institutions

The principal institutions are: BIS, IMF, World Bank The history of exchange rate arrangements since

WW II is dominated by Bretton Woods and the EMS The 1990s see the ratification of the Maastricht

Treaty of European Monetary Union The new ECB is created in 1998 with the Euro to be

introduced in 1999 EMU has rekindled interest in currency unions