Embed Size (px)

Citation preview

Chapter 28

Inflation: Causes and Consequences

Copyright © 2005 Pearson Addison-Wesley. All rights reserved. 28-2

Figure 28.1 Consumer Price Level in the U.S., 1939-2002

Copyright © 2005 Pearson Addison-Wesley. All rights reserved. 28-3

Causes of Short-Term Price Level Fluctuations

• Nominal aggregate demand could rise due to a nominal money supply increase.

• Nominal aggregate demand could rise due to a short-run increase in velocity.

• A fall in the growth rate of aggregate supply could occur.

Copyright © 2005 Pearson Addison-Wesley. All rights reserved. 28-4

Figure 28.2 Price Level Effects of an Increase in the Money Supply

Copyright © 2005 Pearson Addison-Wesley. All rights reserved. 28-5

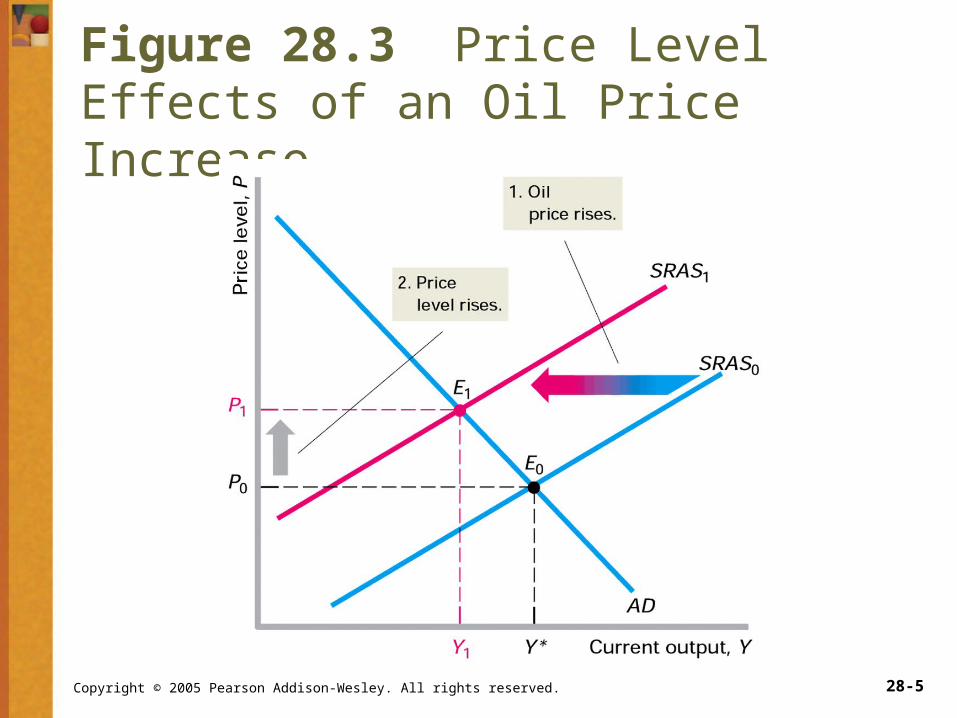

Figure 28.3 Price Level Effects of an Oil Price Increase

Copyright © 2005 Pearson Addison-Wesley. All rights reserved. 28-6

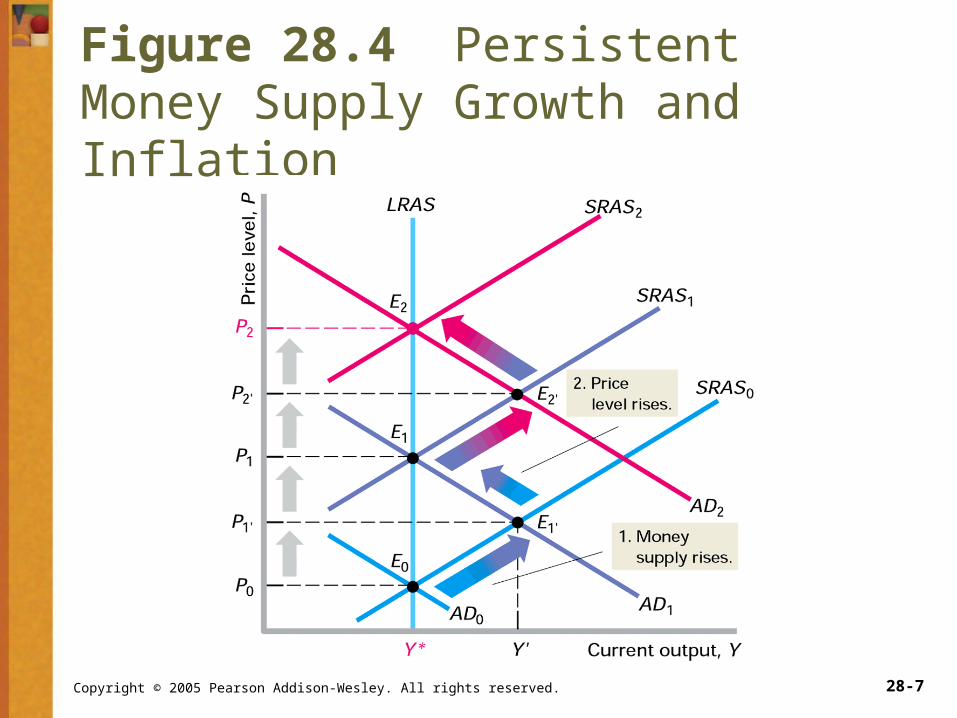

Sustained Changes in the Price Level: Inflation

• Sustained rates of change in the price level constitute inflation.

• Inflation arises when aggregate demand grows faster than aggregate supply.

• One-time shocks cannot by themselves produce inflation.

• Sustained money supply growth causes inflation but does not affect real output.

Copyright © 2005 Pearson Addison-Wesley. All rights reserved. 28-7

Figure 28.4 Persistent Money Supply Growth and Inflation

Copyright © 2005 Pearson Addison-Wesley. All rights reserved. 28-8

Costs of Expected Inflation

• Inflation is a tax on real money balances if they pay less than the market interest rate.

• If tax brackets are not indexed for inflation, then the problem of bracket creep occurs.

• Expected inflation can also distort financial decisions.

• Menu costs, or the costs of changing prices, are another cost.

Copyright © 2005 Pearson Addison-Wesley. All rights reserved. 28-9

Costs of Unexpected Inflation

• Because some contracts are set in nominal terms, wealth redistribution can occur.

• Inflation uncertainty causes distortion of information provided by prices.

• When inflation fluctuates significantly, relative prices may change.

• An extreme case of uncertain inflation occurs in a hyperinflation.

Copyright © 2005 Pearson Addison-Wesley. All rights reserved. 28-10

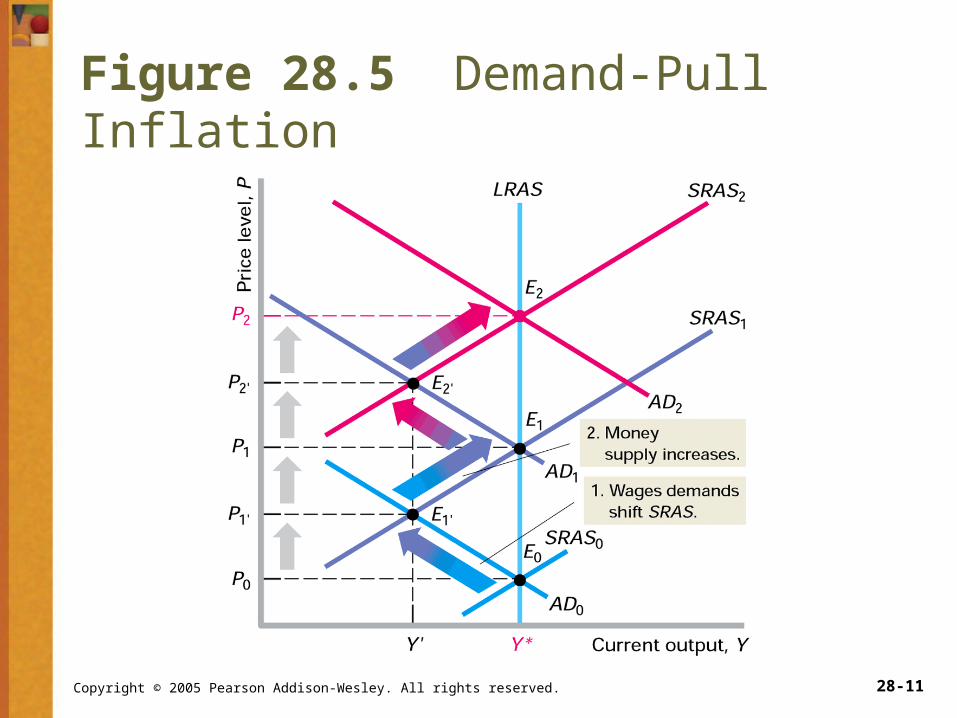

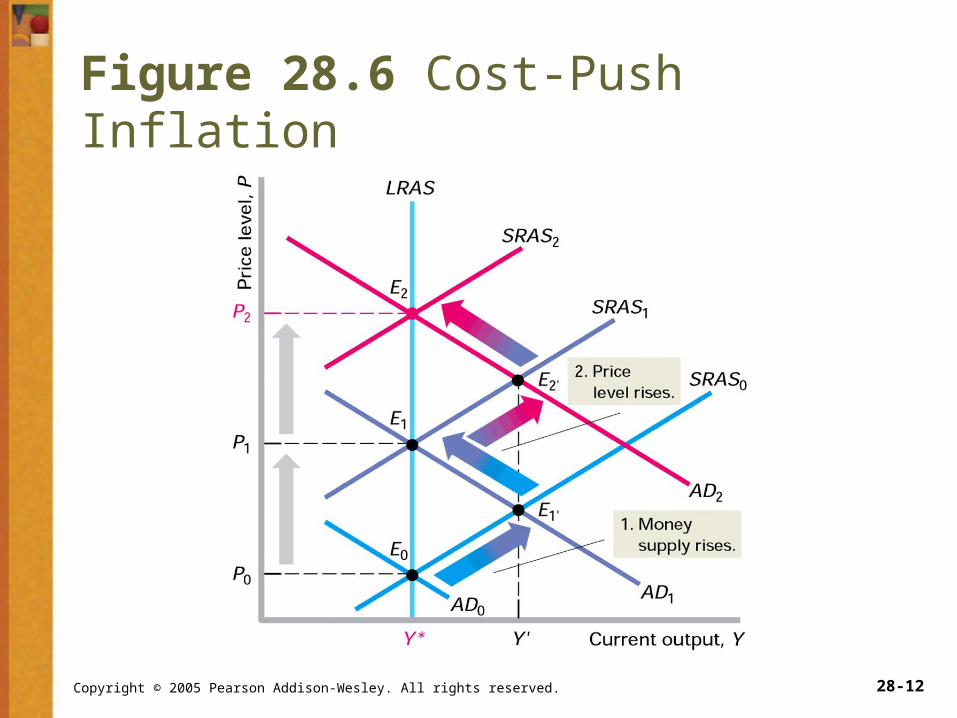

Inflation and Monetary Policy

• Cost-push inflation results from workers’ pressure for higher wages.

• Demand-pull inflation results from attempts to decrease the unemployment rate too low.

Copyright © 2005 Pearson Addison-Wesley. All rights reserved. 28-11

Figure 28.5 Demand-Pull Inflation

Copyright © 2005 Pearson Addison-Wesley. All rights reserved. 28-12

Figure 28.6 Cost-Push Inflation

Copyright © 2005 Pearson Addison-Wesley. All rights reserved. 28-13

Costs of Reducing Inflation

• Disinflation refers to a decline in long-run inflation.

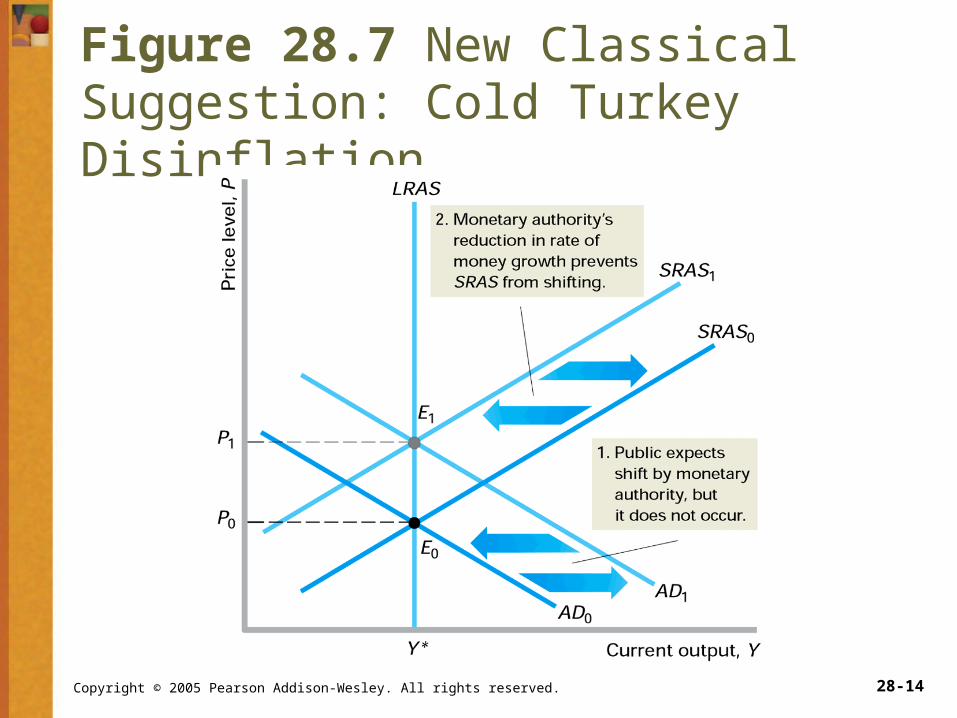

• The new classical view argues for an immediate reduction in money growth.

• New Keynesians advocate slow and steady reduction in money growth.

Copyright © 2005 Pearson Addison-Wesley. All rights reserved. 28-14

Figure 28.7 New Classical Suggestion: Cold Turkey Disinflation

Copyright © 2005 Pearson Addison-Wesley. All rights reserved. 28-15

Figure 28.8 New Keynesian Suggestion: Gradual Disinflation

Copyright © 2005 Pearson Addison-Wesley. All rights reserved. 28-16

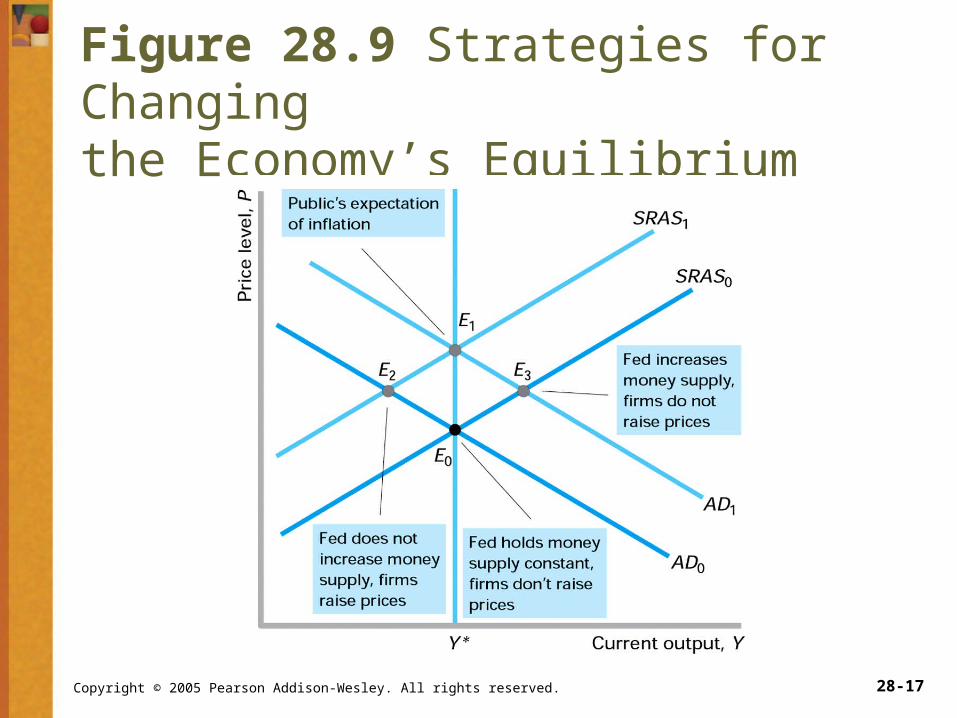

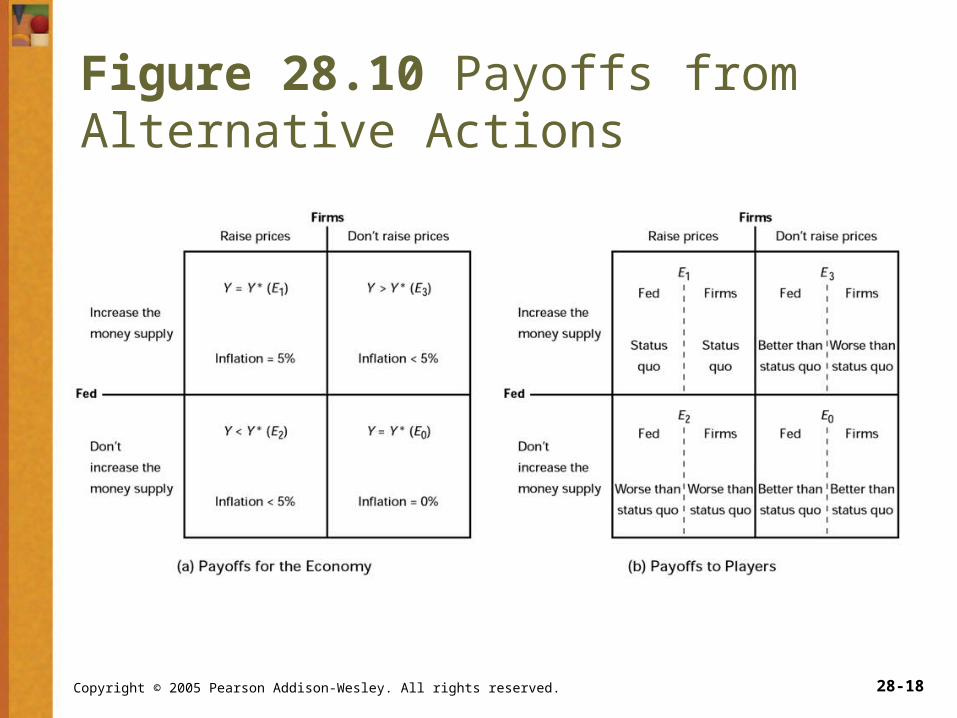

Central Bank Credibility

• A crucial factor in disinflationary policy is central bank credibility.

• Appointing a “tough” central banker is likely to increase central bank credibility.

• Some economists argue that the central bank should adopt a rules strategy.

• Other economists support a discretion strategy.

Copyright © 2005 Pearson Addison-Wesley. All rights reserved. 28-17

Figure 28.9 Strategies for Changing the Economy’s Equilibrium

Copyright © 2005 Pearson Addison-Wesley. All rights reserved. 28-18

Figure 28.10 Payoffs from Alternative Actions