Embed Size (px)

Citation preview

Chapter 3Process Costing

Job-Order v. Process Costing

Job-Order Costing

• Many jobs are worked on during each period, with each job having different production requirements.

• Costs are accumulated by job.

• The job cost sheet is the key document for accumulating costs.

• Units costs are computed by job on a job cost sheet.

Process Costing

• A homogeneous product is produced on a continuous basis or for long periods of time.

• Costs are accumulated by department.

• The departmental production report is the key document showing the accumulation and disposition of costs.

• Unit costs are computed by department on production reports.

Problem InformationMixing Packaging

Unit Information: Beginning Work in Process:

(Mixing) 10,000(Packaging) 15,000

Started into Production 70,000 N/A Transferred In N/A ?

Ending Work in Process:(Mixing 100% material, 50% conversion) 20,000

(Packaging 100% material, 40% conversion) 5,000

Problem Information (Continued)

Mixing PackagingCost information: Beginning Work in Process: Direct materials $18,000 $10,500 Transferred in N/A $92,250 Conversion $31,200 $13,500

Costs Added Currently: Direct materials $142,000 $49,500 Transferred in N/A ? Conversion $248,800 $83,700

Calculation of Equivalent Units

Beginning Work-in-Process Inventory:

Physical Units X = XXX100%

Started and Completed in Current Period:

Physical Units X 100% = XXX

Ending Work-in-Process Inventory:

Physical Units X Percent of work completed in the current period = XXX

XXXEquivalent Units of Production

Equivalent Units Illustration - Mixing

Beginning WIP:

10,000 x 100% = 10,000

Started & Completed:

50,000 x 100% = 50,000

Ending WIP:

20,000 x 100% = 20,000

Equivalent Units 80,000

Materials Conversion CostsBeginning WIP:

10,000 x 100% = 10,000

Started & Completed:

50,000 x 100% = 50,000

Ending WIP:

20,000 x 50% = 10,000

70,000

Equivalent Units Illustration –Mixing (alternative approach)

Units Completed:

60,000 x 100% = 60,000

Ending WIP:

20,000 x 100% = 20,000

Equivalent Units 80,000

Materials Conversion Costs

Units Completed:

60,000 x 100% = 60,000

Ending WIP:

20,000 x 50% = 10,000

70,000

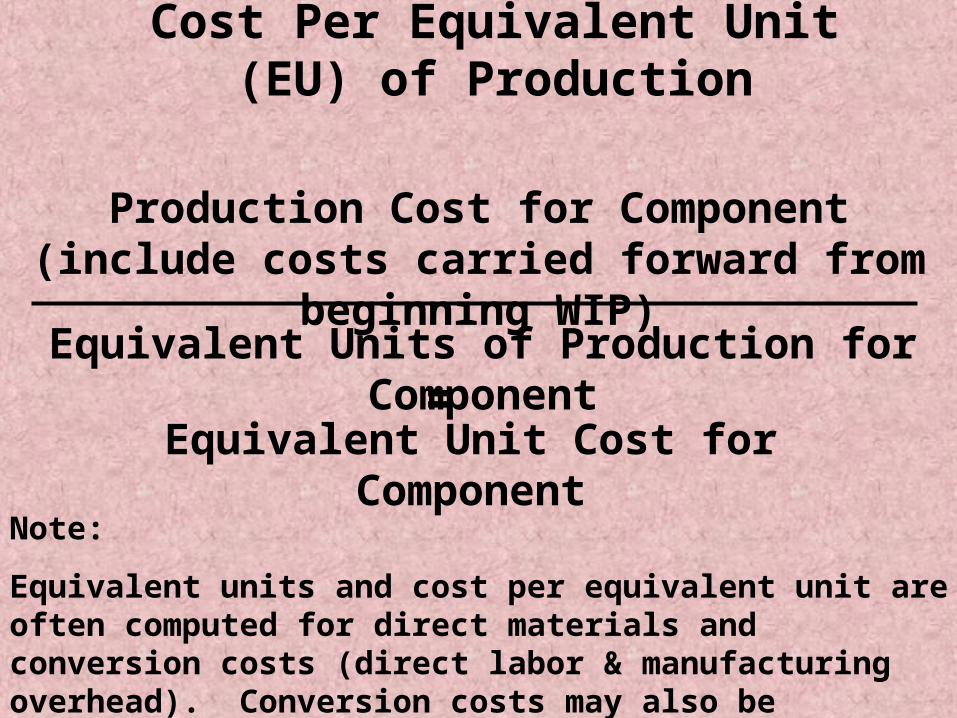

Cost Per Equivalent Unit (EU) of Production

Production Cost for Component (include costs carried forward from beginning WIP)

Equivalent Units of Production for Component=

Equivalent Unit Cost for Component

Note:

Equivalent units and cost per equivalent unit are often computed for direct materials and conversion costs (direct labor & manufacturing overhead). Conversion costs may also be calculated separately.

Cost Per Equivalent Unit Illustration - Mixing

Materials

$18,000 + $142,000

80,000 EU= $2.00

Conversion

$31,200 + $248,800

70,000 EU

$4.00=

Total Equivalent Unit Cost:

Materials $2.00

Conversion 4.00

$6.00Total EU Cost

See Direct Material, DL, & MOH Journal Entries on Page 84

Costs Accounted For

Transferred Out:

Transferred Out EU x Cost Per EU = XXX

Cost in Ending Work-in-Process Inventory:

Ending WIP EU x Cost Per EU = XXX

XXX

Note:

Total cost is computed for direct materials and conversion costs (direct labor & manufacturing overhead). Conversion costs may also be calculated separately.

Costs Accounted For Illustration - Mixing

Transferred Out:

60,000 EU x $6.00

Cost in Ending Work-in-Process Inventory:

$440,000

360,000

Materials: 20,000 EU x $2.00 $40,000Conversion: 10,000 EU x $4.00 40,000 80,000

Total Cost

See Transferred In Journal Entry on Page 84

Equivalent Units Illustration - Packaging

Beginning WIP:

15,000 x 100% = 15,000

Started & Completed:

55,000 x 100% = 55,000

Ending WIP:

5,000 x 100% = 5,000

Equivalent Units 75,000

Materials Conversion CostsBeginning WIP:

15,000 x 100% = 15,000

Started & Completed:

55,000 x 100% = 55,000

Ending WIP:

5,000 x 40% = 2,000

72,000

Equivalent Units Illustration – Packaging (alternative approach)

Units Completed (includes 60,000 transferred in from Mixing):

70,000 x 100% = 70,000

Ending WIP:

5,000 x 100% = 5,000

Equivalent Units 75,000

Materials and Transferred In Conversion Costs

Units Completed (includes 60,000 transferred in from Mixing):70,000 x 100% = 70,000

Ending WIP:

5,000 x 40% = 2,000

72,000

Cost Per Equivalent Unit Illustration - Packaging

Materials

$10,500 + $49,500

75,000 EU= $0.80

Conversion

$13,500 + $83,700

72,000 EU

$1.35=

Total Equivalent Unit Cost:

Materials $0.80

Conversion 1.35

$8.18Total EU Cost

Transferred In

$92,250 + $360,000

75,000 EU$6.03=

Transferred In 6.03

Costs Accounted For Illustration - Packaging

Transferred Out:

70,000 EU x $8.18

Cost in Ending Work-in-Process Inventory:

$609,450

572,600

Materials: 5,000 EU x $6.83 $34,150Conversion: 2,000 EU x $1.35 2,700 36,850

Total Cost

Production Report Format

Quantity Schedule and Equivalent Units

Units to be accounted for:Beginning work in processStarted into production

Units accounted for: (compute equivalent units) Transferred out (from beginning WIP & started & completed)Ending work in process

Total and Unit Cost

Costs to account for:Beginning work in processStarted into production

Cost ReconciliationCosts accounted for:Transferred out (from beginning WIP & started & completed)Ending work in process