Embed Size (px)

Citation preview

Chapter 4 and 5

International Classification of Financial Reporting International Harmonization of accounting

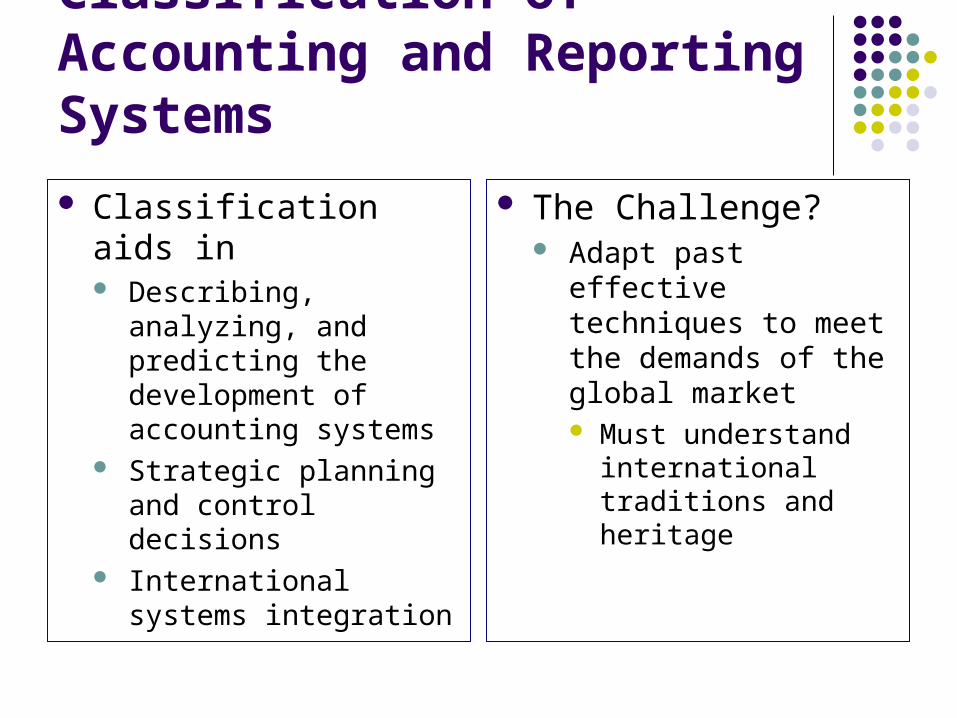

Classification of Accounting and Reporting Systems

Classification aids in Describing, analyzing,

and predicting the development of accounting systems

Strategic planning and control decisions

International systems integration

The Challenge? Adapt past effective

techniques to meet the demands of the global market Must understand

international traditions and heritage

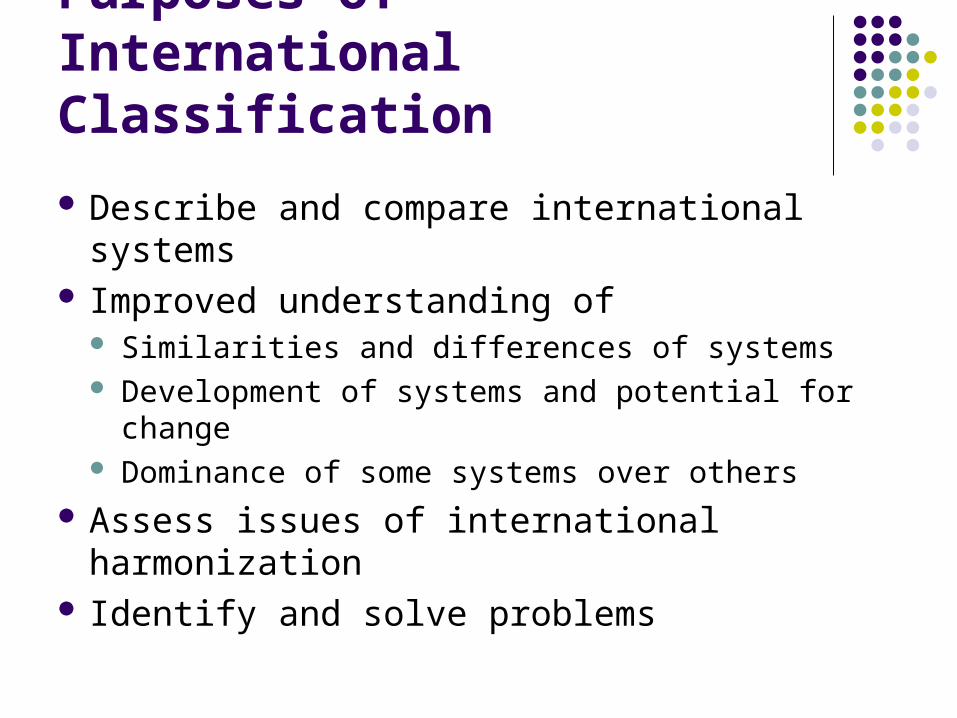

Purposes of International Classification

Describe and compare international systems Improved understanding of

Similarities and differences of systems Development of systems and potential for change Dominance of some systems over others

Assess issues of international harmonization Identify and solve problems

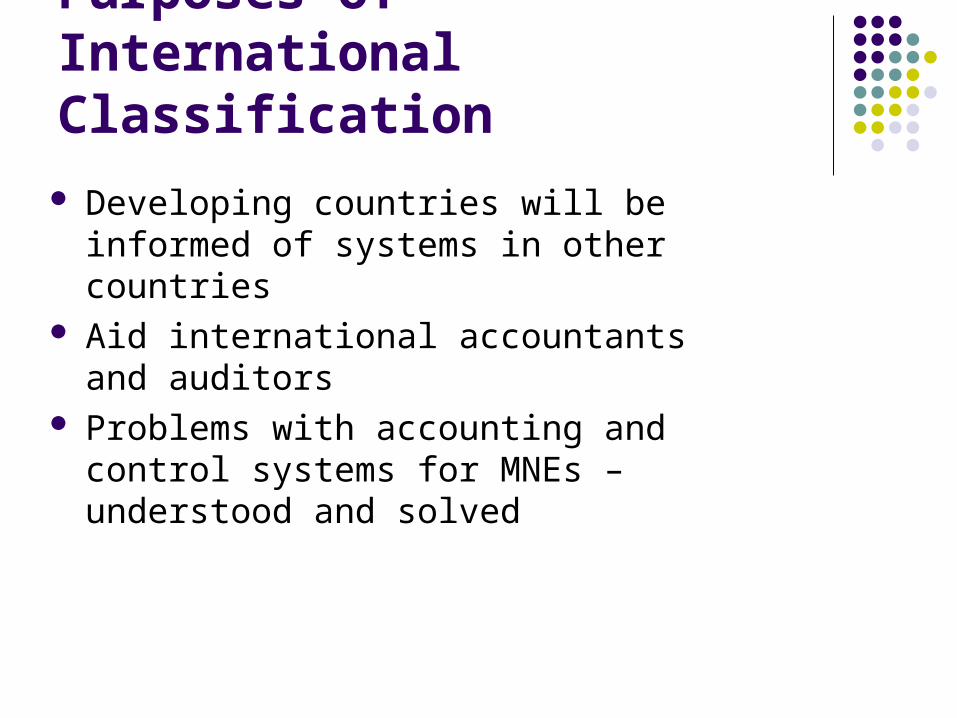

Purposes of International Classification

Developing countries will be informed of systems in other countries

Aid international accountants and auditors Problems with accounting and control

systems for MNEs – understood and solved

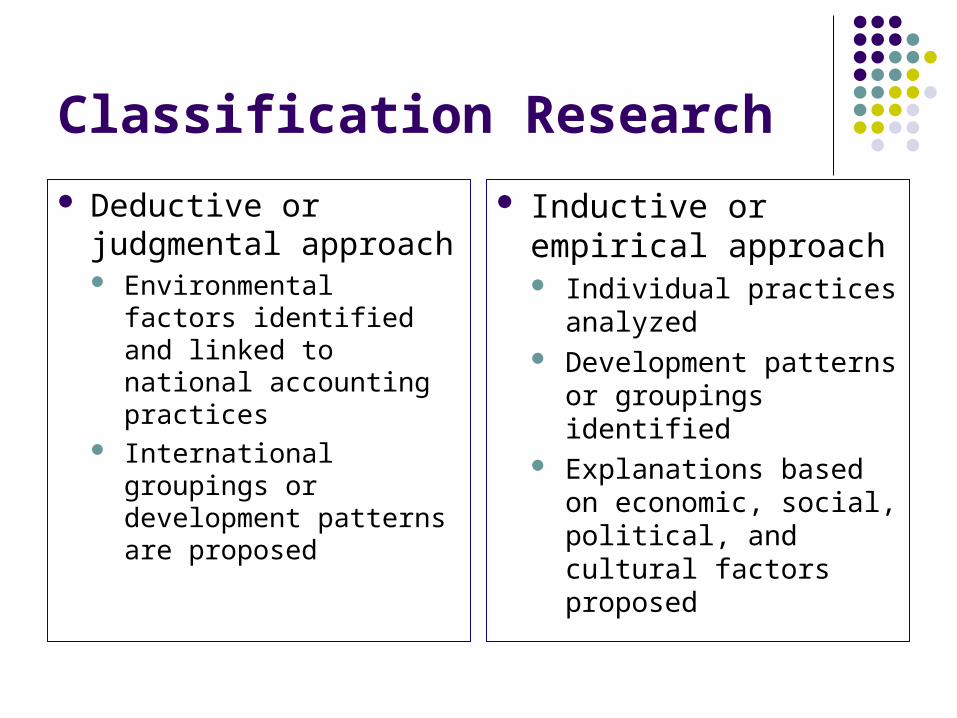

Classification Research

Deductive or judgmental approach Environmental factors

identified and linked to national accounting practices

International groupings or development patterns are proposed

Inductive or empirical approach Individual practices

analyzed Development patterns or

groupings identified Explanations based on

economic, social, political, and cultural factors proposed

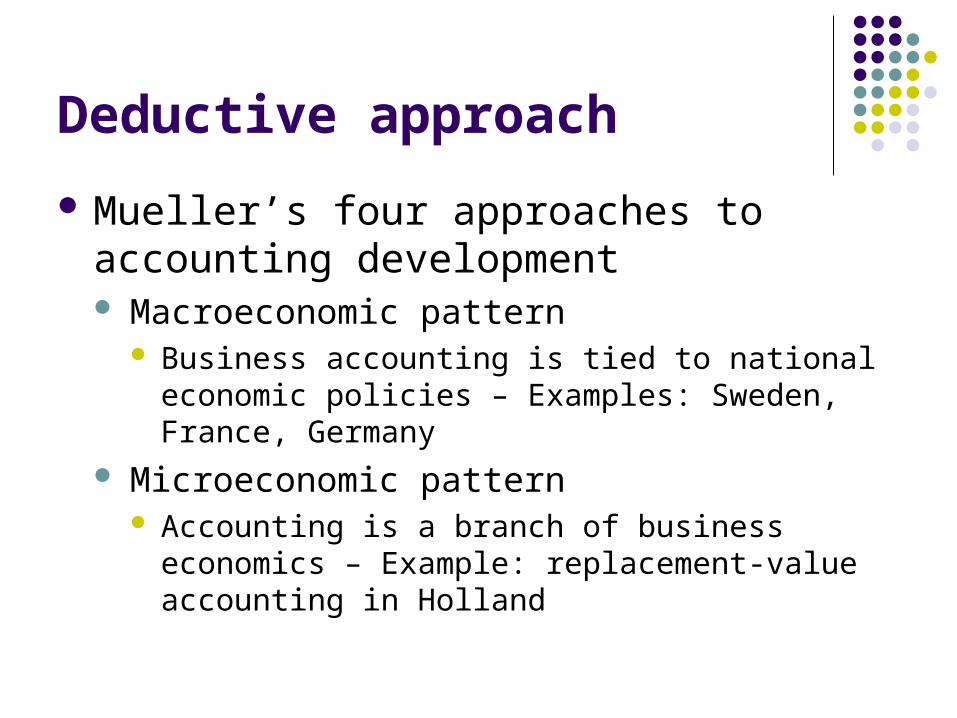

Deductive approach

Mueller’s four approaches to accounting development Macroeconomic pattern

Business accounting is tied to national economic policies – Examples: Sweden, France, Germany

Microeconomic pattern Accounting is a branch of business economics –

Example: replacement-value accounting in Holland

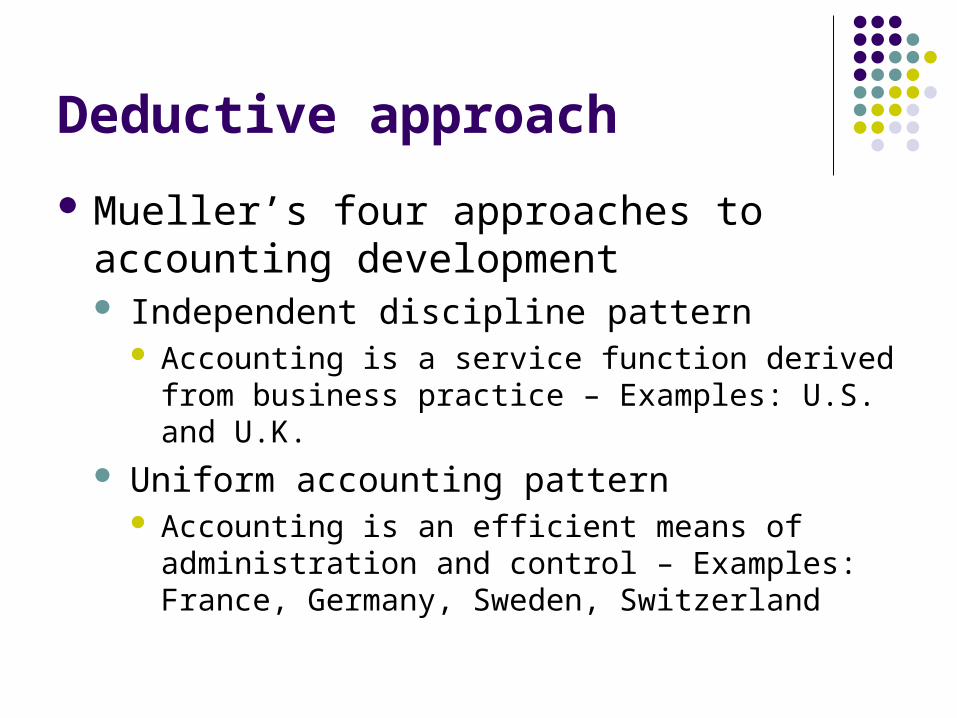

Deductive approach

Mueller’s four approaches to accounting development Independent discipline pattern

Accounting is a service function derived from business practice – Examples: U.S. and U.K.

Uniform accounting pattern Accounting is an efficient means of administration and

control – Examples: France, Germany, Sweden, Switzerland

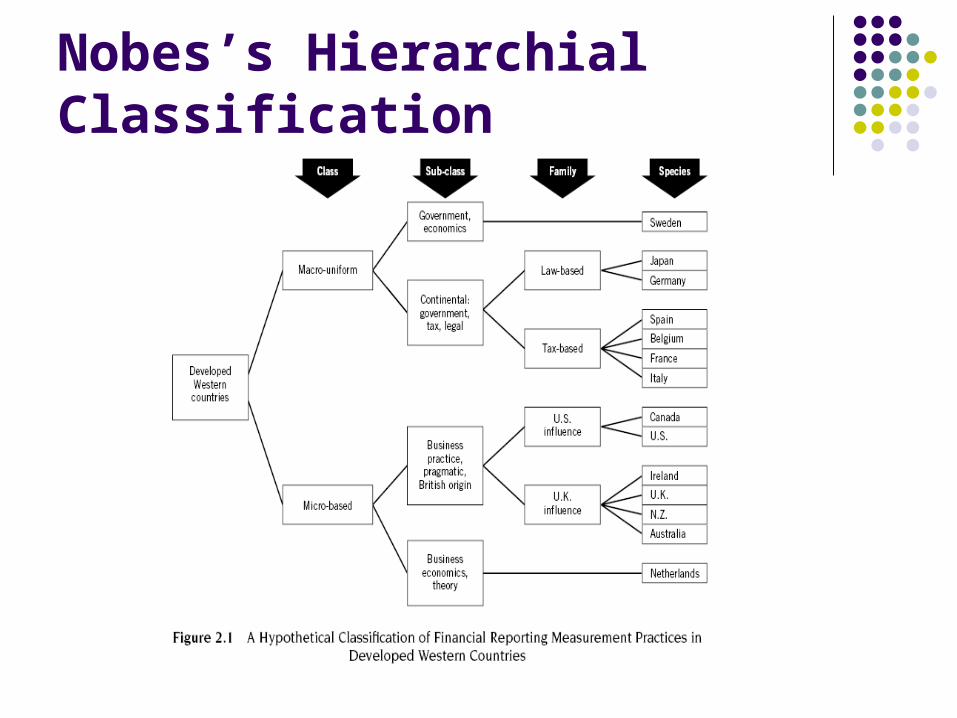

Nobes’s Hierarchial Classification

Inductive Approach

Nair and Frank (1980) findings 1973 data

Four measurement groups British Commonwealth Latin America Continental European U.S.

Seven disclosure groups Could not be plausibly described No explanation offered for difference in groupings

Inductive Approach

Nair and Frank (1980) findings Differences between measurement and

disclosure groups Hypotheses not supported

Cultural and economic variables associated with disclosure practices

Trading variables associated with measurement practices

Overall – little attention given to influence of culture

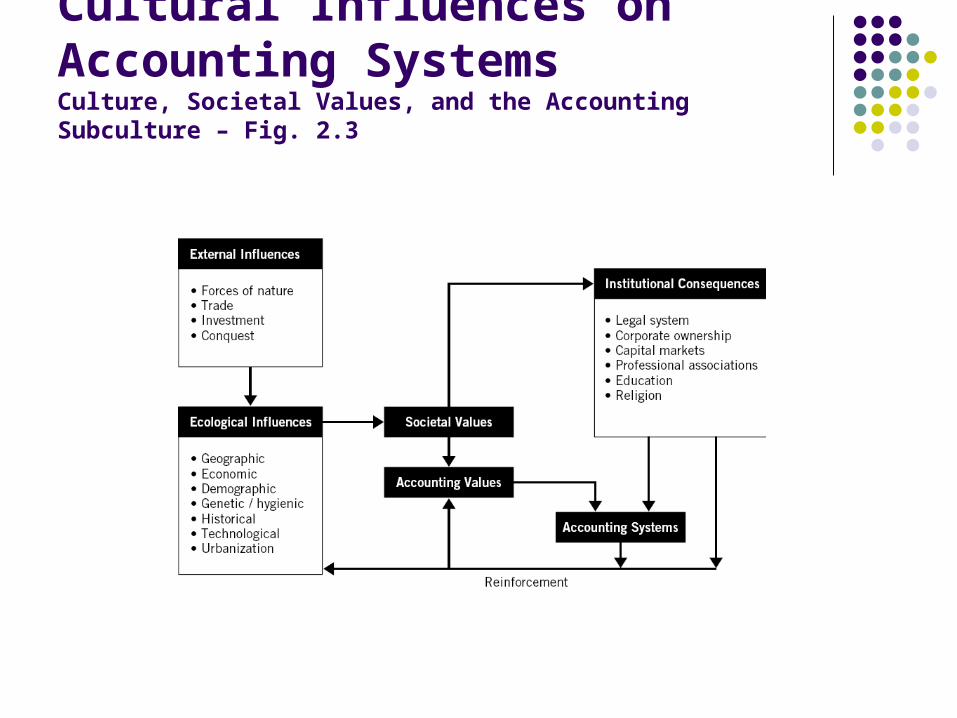

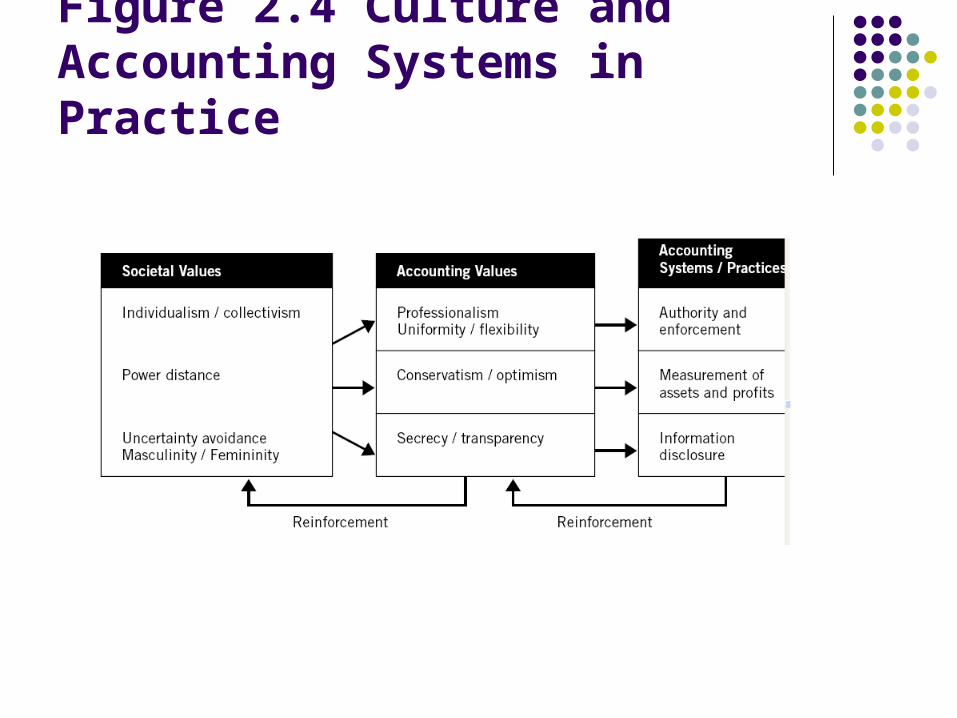

Cultural Influences on Accounting Systems Culture, Societal Values, and the Accounting Subculture – Fig. 2.3

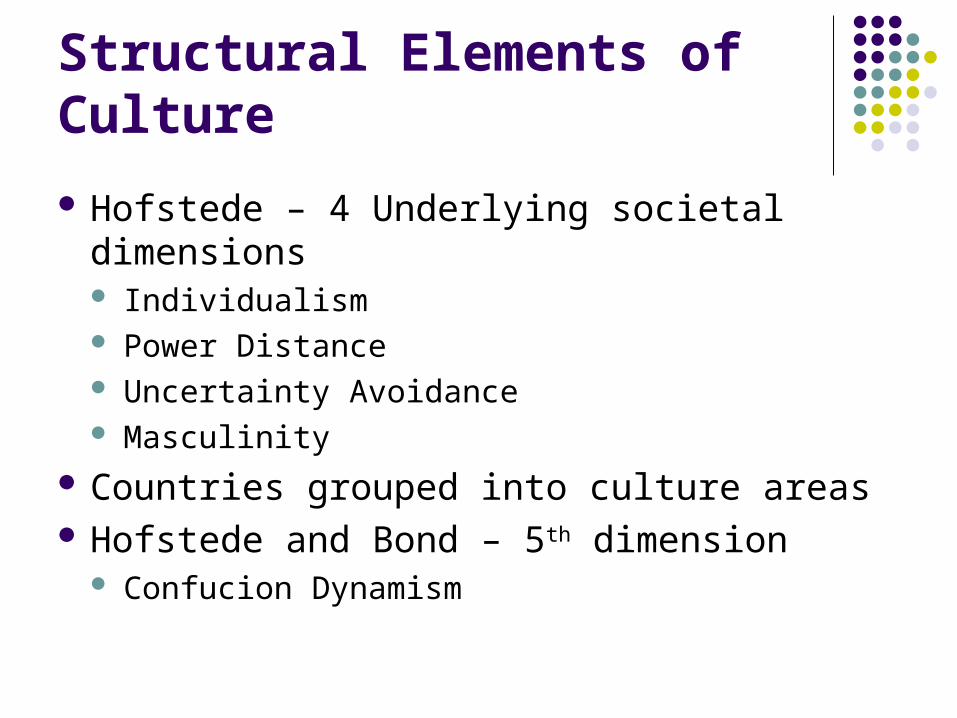

Structural Elements of Culture

Hofstede – 4 Underlying societal dimensions Individualism Power Distance Uncertainty Avoidance Masculinity

Countries grouped into culture areas Hofstede and Bond – 5th dimension

Confucion Dynamism

Hofstede’s Societal Dimensions

Individualism versus Collectivism People’s self-concept: “I” or “we”

Large versus Small Power Distance How a society handles inequalities among people

Strong versus Weak Uncertainty Avoidance Control the future or just let it happen

Masculinity versus Femininity The way a society allocates social roles to gender

Confucian Dynamism Short-term or long-term orientation

Accounting Values – Gray

Professionalism versus statutory control Uniformity versus flexibility Conservatism versus optimism Secrecy versus transparency

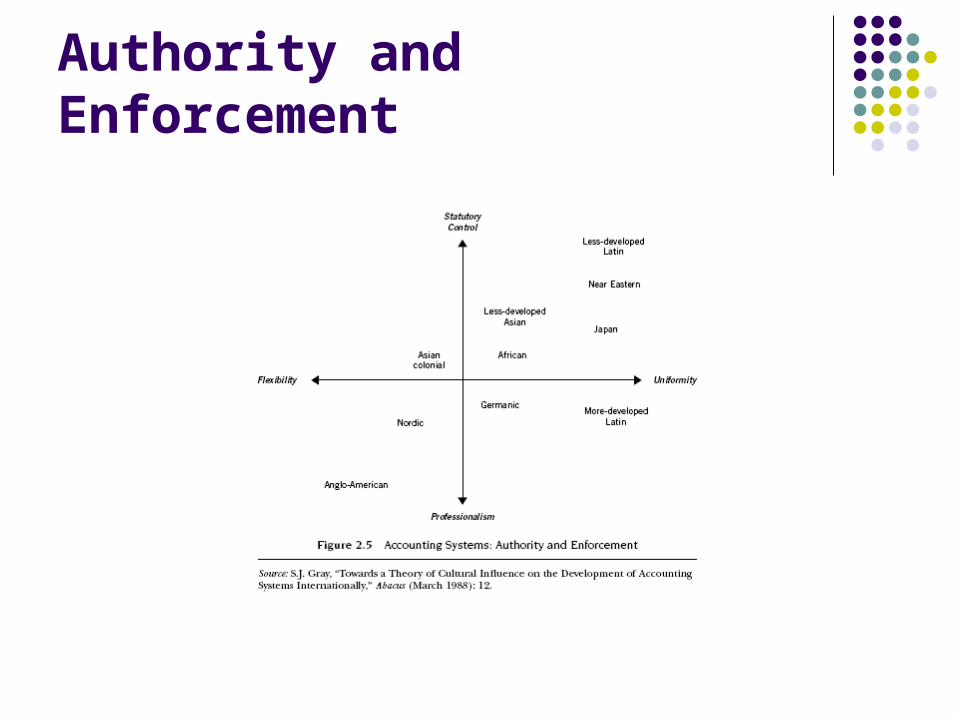

Professionalism versus Statutory Control Accountants are perceived to have independent

attitudes throughout the world Public regulation or self regulation

U.K. – rely on judgment of accountant France and Germany – implement detailed legal

requirements Link to societal value dimensions – Professionalism

Individualism Weak uncertainty avoidance Small power distance Masculinity Short-term orientation

Uniformity versus Flexibility Uniform accounting plan and imposition of tax rules

for measurement purposes France and Spain

Facilitate national planning Pursue macroeconomic goals

Intertemporal consistency and some degree of intercompany comparability b/c of flexibility U.S. and U.K.

Link to societal value dimensions – Uniformity Strong uncertainty avoidance Collectivism Large power distance

Figure 2.4 Culture and Accounting Systems in Practice

Authority and Enforcement

Conservatism versus Optimism

Conservatism seen as a fundamental value Strongly conservative

Japan, France, Germany, Switzerland Less conservative

U.S., U.K., the Netherlands

Link to societal value dimensions – Conservatism Strong uncertainty avoidance Long-term orientation Collectivism Femininity

Secrecy versus Transparency Stems from management and accountants Closely related to conservatism

Secrecy relates to disclosure Conservatism relates to measurement

Secrecy High – Japan, France, Germany, Switzerland Low – U.S. and U.K.

Link to societal value dimensions – Secrecy Strong uncertainty avoidance High power distance Collectivism Femininity

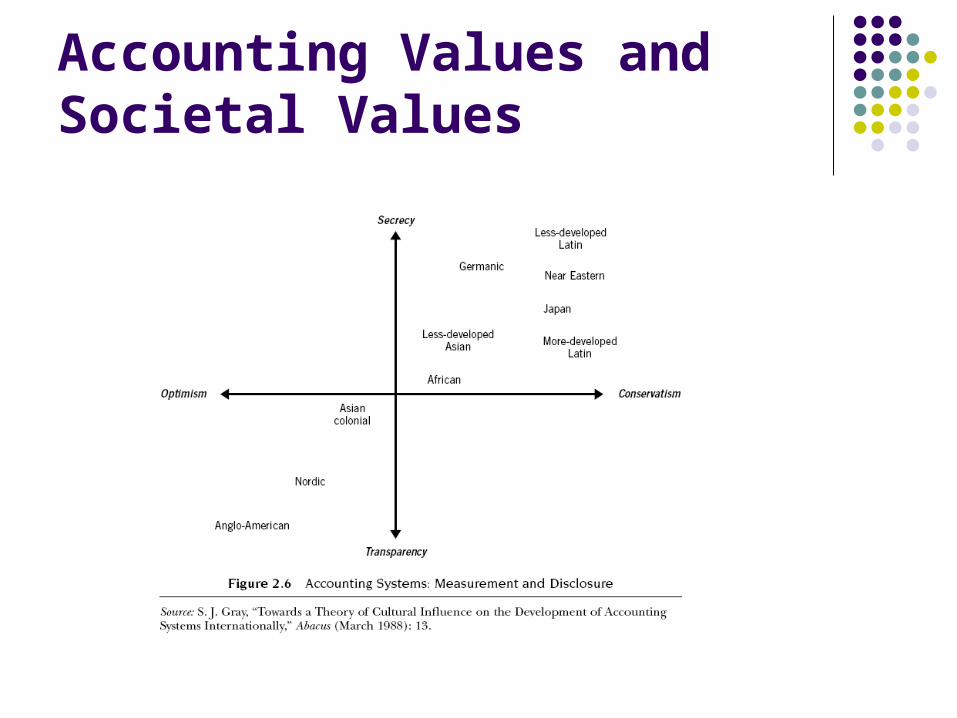

Accounting Values and Societal Values

Accounting Values and International Classification

Accounting values most relevant to professional or statutory authority and enforcement Professionalism and Uniformity

Both concerned with regulation and degree of enforcement or conformity

Accounting values most relevant to measurement and disclosure Conservatism and secrecy

Country groupings Optimistic and transparent Conservative and secretive

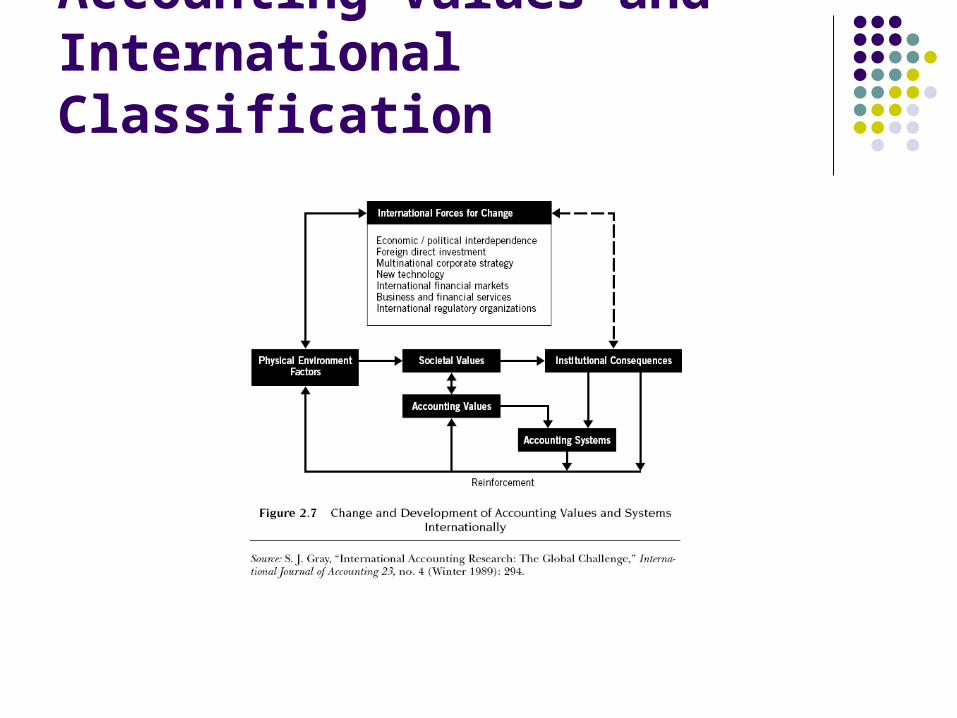

Accounting Values and International Classification

International Pressures for Accounting Change

Growing international interdependencies Harmonization of the regulatory framework

internationally Centrally planned economies embraces

market-oriented approach Former U.S.S.R., Eastern Europe, China

New opportunities for international investment, joint ventures, and alliances

Economic Groupings and International Organizations

European Union Promotes economic integration/harmonization

UN World Bank International Monetary Fund UN conference on Trade and Development World Trade Organisation

OECD Foster international economic and social development in

industrialized countries “Code of Conduct” for MNEs

Impact of MNEs and Globalization

Cultural and social Employment and consumption patterns

Significantly influenced Pressure for more accountability Environmental impact

Impact of MNEs and Globalization

OECD, EU, IOSCO work for harmonization and internationalization of securities markets

IASB and the International Federation of Accountants (IFAC) Professional organizations involved in

harmonization

![International Harmonization of Standards[1]. Detailed Report [Power Apparatus](https://img.pdfslide.net/doc/110x75/577cd9711a28ab9e78a38367/international-harmonization-of-standards1-detailed-report-power-apparatus.jpg)