Embed Size (px)

Citation preview

171

Chapter-5

Investor Grievances Redressal Mechanism and

Protection for Retail Investors

5.1 Introduction Investor grievance redressal mechanism and protection of retail investors go hand in

hand with one another. If there is a transparent, time bound, easier and simpler

grievance redressal mechanism for retail investors, their protection will be

automatically ensured and they will be able to park their investments in the capital

markets, and thus would contribute towards development of economy by channelizing

their savings into investments and facilitating capital formation in the economy.

Nayak (2010) is of the view that the system must offer adequate checks and balances

in which the entrepreneurial effort is backed by investors' confidence so as to easily

capitalize on it. This has, however, failed to happen at least to the extent expected and

desired. In succeeding paras, grievances of retail investors, their redressal at

Securities & Exchange Board of India (SEBI), Ministry of Corporate Affairs (MCA),

Stock Exchanges and listed companies have been studied and critically examined. An

effort has also been made to study the existing Grievance Redressal Mechanism at

few foreign Stock Exchanges of repute. These stock exchanges include New York

Stock Exchange, Singapore Stock Exchange, Australian Stock Exchange, Toronto

Stock Exchange and Taiwan Stock Exchange. The study of these stock exchanges has

been done so that international practices on this subject are also examined and

analyzed at the global level, so as to propose the most suited model for Indian

Securities Market.

5.1.1 Grievances of Retail Investors

Despite the various measures and steps taken by Securities and Exchange Board of

India, Ministry of Corporate Affairs, Ministry of Finance and Stock Exchanges, the

retail investors feel disappointed, dejected and sometimes feel excluded from the

172

system. Various laws, acts, rules and regulations have been framed to protect the

interest of the retail investors, but their grievances still remain. On paper, Indian laws

are at par with the world standard. Despite this retail investors are not coming to the

mainstream. These laws need to be effective so as to provide the redressal mechanism

in a timely and effective manner.

The redressal mechanism of the grievances of retail investors is not yet satisfactory

and much remains to be done on this account by the Government, market regulator

SEBI as well as from other market intermediaries. While comparing the grievances

redressal mechanism in India and overseas market, Deena Mehta, Managing Director,

Asit C Mehta Investment Intermediates, and one of the three trading member-

directors on the board of the Bombay Stock Exchange, in her report states that the

biggest difference between Indian markets and overseas markets is speedy disposal of

cases and harsh and immediate punishment to wrongdoers (Dalal, 2011). This is

harming the Retail Investors and Indian Capital Market.

During the last two decades, especially after 1991, many scams like Harshad Mehta

scam, plantation companies scam, Ketan Parekh scam, Unit Trust of India (UTI)

fiasco, vanishing companies, Satyam scam and various other malpractices like insider

trading, bucket trading (commonly called dabba trading in India), unauthorized

trading in the accounts of investors, churning to increase brokerage, induced volatility

to make arbitrage opportunities for larger players at cost of the retail players etc.,

apart from incurring of heavy losses for them in securities market has shaken the

confidence of retail investors.

According to Somaya (2005) as per one estimate, 50,000 crore of savings of

retired people, pensioners, salaried persons were either looted or locked up in these

scams but no concrete action has been taken to recover this huge amount of money

from the perpetrators of these scams, besides the retail investors continuously lose due

to these malpractices. The retail investors have a lot of grievances against the market

regulator and other various intermediaries. The grievances of the investors can be

against any of the following agencies/ intermediaries, namely:

1. Securities & Exchange Board of India,

173

2. Stock Exchanges,

3. Depositories and Depository Participants,

4. Stock Brokers and sub-brokers,

5. Merchant Bankers,

6. Registrars and Transfer Agents,

7. Listed Companies, and

8. Other Stock Market Intermediaries.

The various studies and the data show that investors are far from happy and their

grievances are piling. At time, most of the grievances go unnoticed by the regulatory

authorities as the investors find it difficult to approach the right authority for lodging

their complaints. Their grievances are either not redressed in time, or partially

redressed at most times. What is required is to have a relook at the redressal

mechanism and sincere efforts to be made to recover the lost money of grieved

investors and given back to them. Table 5.1 depicts the various types of

grievances/complaints of the investors.

Table 5.1: Various Types of Investors’ Grievances

S. No. Nature of Grievance

1. Delay in transfer of shares

2. Non-receipt of shares/dividends/rights/bonus shares

3. Delay/ Non-receipts in issue of duplicate shares

4. Delay/ Non-receipt of annual reports

5. Delay/ Non-receipt of redemption amount of debentures

6. Delay/ Non-receipt of interest on debentures

7. Delay/ Non-credit of shares in the account by the broker

8. Delay/ Non-payment of sale proceeds by the broker etc.

9. Manipulation in the accounts statements

10. Unauthorized trades and unauthorized movements of shares

and funds from the clients’ accounts.

11. Dabba Trading/ churning etc. in clients’ accounts

12. Delay/ Non-updating of clients’ information in records

SEBI website: www.http://investor.sebi.gov.in.investorcomplaint.form.)

174

The present study articulates the various grievances of the investors in securities

market so as to have a meaningful redressal of their grievances. SEBI, the market

regulator has classified various types of grievances of retail investors in securities

market.

5.1.2 Grievance Redressal Mechanism

5.1.2.1 Preamble Different regulators bodies and Self Regulatory Organisations (SROs), like SEBI,

Stock Exchanges, Reserve Bank of India (RBI), Ministry of Corporate Affairs (MCA)

and Ministry of Finance (MoF) have different grievance redressal mechanism for the

retail investors in India. Stock Exchanges on paper too have a powerful grievance

redressal system for retail investors and have different entities with their specific roles

assigned. Other stock market intermediaries at the direction of SEBI have set up their

own grievances redressal mechanism. The main redressal mechanism is with the stock

exchanges that directly interact with the investors on day-to-day basis.

Companies listed with Stock Exchanges also have set up their own grievance

redressal mechanism for their shareholders, which is made effective through the

provisions of the Company Law, 1956, and the listing agreement executed with the

Stock Exchanges.

5.1.2.2 Classification of Complaints and with whom to Lodge

In order to have early resolution of complaints and to have clarity in the minds of the

investors, market regulator SEBI has clear cut defined mechanism specifying therein

the nature of the complaint and whom to lodge so that the investors are not harassed,

and at the same time to facilitate a quick resolution of the complaint. One can also

approach according to the nature of one’s complaint to various agencies for its

redressal. Depending upon their grievances, the investors can approach the concerned

authority for redressal of their grievances.

Table no. 5.2 depicts the nature of complaints and to whom the same are to be lodged

for their speedy redressal.

175

Table 5.2: Classification of Complaints and with whom to Lodge these Complaints

S. No. With whom to File Nature of Complaint

1. The Stock Exchanges at their Investor Service Centre

• Complaints related to securities traded/listed with the Exchanges

• Complaints regarding the trades effected in the Exchange with respect to the companies listed on it or by the members of the Exchange

• Complaints against listed companies with Stock Exchanges

• 2. Department of

Corporate Affairs/ concerned Registrar of Companies (ROC)

• Complaints against unlisted companies • Complaints regarding non-receipt of annual

report, AGM Notice, etc. • Complaints relating to fixed deposits in

manufacturing companies 3. The Reserve Bank of

India • Fixed deposits in banks and NBFCs

4. The concerned company/ ROC

• Forfeiture of shares, etc.

5.2 Grievance Redressal Mechanism with SEBI SEBI has been mandated to protect the interest of the investors in securities market of

the country. SEBI Act, 1992 clearly specifies that SEBI has been formed for the

development, regulation of securities market and to protect the interest of the

investors. That is why the protection of the investors’ interest has always been the

priority of SEBI. An investor would like to trade in securities market only if he knows

how to invest, if he has full knowledge of the market, if the market is safe and there

are no miscreants, and more importantly there is a strong mechanism to redress his

grievances, if any.

SEBI has established a comprehensive and robust investor grievance redressal

mechanism and has also directed the Stock Exchanges to do the same at their level.

Investor assistance and education division of SEBI located at Mumbai takes up the

complaints from the investors. Office of Investor Assistance and Education (OIAE)

acts the single window interface, interacting with investors seeking assistance of

SEBI. SEBI has also put in dedicated helpline telephone numbers with dedicated

176

personnel operating the helpline (SEBI website www.http://sebi.gov.in, Complaints

and Assistance – Contact Details of Division Chiefs).

SEBI has put in dedicated grievance cell for grievances against listed companies,

against stockbrokers, against Depository Participants and other market intermediaries.

Each complaint received by SEBI is acknowledged and reference no. is sent to the

complainant. Each complaint is taken up with the company, and if the complaint is

not resolved within a reasonable time, this division carries out periodical follow up

with the concerned company. The officials of SEBI regularly hold meetings with

company officials to impress upon their obligations to redress the grievances of

investors. But the question arises whether these measures are effective enough to

provide speedy redressal of the grievances.

SEBI has a comprehensive mechanism to facilitate redressal of investor grievance

against intermediaries and listed entities. Whenever a retail investor has any grievance

against broker, sub-broker, or listed entities, the complaint can be filed with Stock

Exchange or SEBI. Stock Exchanges are having the jurisdiction over above-said

entities to resolve, conciliate the complaints of the investors. Investors can also send

the complaints to SEBI directly. Recently, SEBI has realized 30 crore of disgorged

money of unlawful gains from IPO irregularities and distributed to the aggrieved

investors. Is this action of SEBI enough? The question remains to be answered.

5.2.1 Classification of Investors’ Complaints In order to have clarity in the minds of the investors and easy & early redressal of

investors’ complaints, SEBI has classified various types of complaints in different

eleven categories from type I to type XI. The classification aims to identify the

various complaints such as refund order/ allotment advice, non-receipt of dividend/

debentures and their proceeds, complaints against collective investment schemes,

mutual funds, etc. against stock exchanges, DPs, and various other intermediaries.

This classification has been done in order to bring the clarity in the minds of investors

and for the speedy resolution of their complaints, to provide smooth and sound

mechanism for the redressal of their complaints.

177

The detailed classification is with regard to the nature of the complaints like non-

receipt of refund orders/ allotment advices, non-receipt of dividend from the listed

companies, non-receipt of share certificates lodged for transfer with listed entities,

non-receipt of debenture proceeds or redemption amount, complaints against

Collective Investment Vehicles, complaints against brokers, etc. Table 5.3 classifies

various types of complaints, which can be lodged with market regulator SEBI, and

other various intermediaries.

Table 5.3: Types of Complaints

S. No. Type Nature of Complaints

1. Type-I Refund Order/ Allotment Advice

2. Type-II Non-receipt of dividend

3. Type-III Non-receipt of share certificates after transfer

4. Type-IV Debentures

5. Type-V Non-receipt of letter of offer for rights

6. Type-VI Collective Investment Schemes

7. Type-VII Mutual Funds/ Venture Capital Funds/ Foreign Venture Capital Investors/ Foreign Institutional Investors/ Portfolio Managers, Custodians

8. Type-VIII Brokers/ Securities Lending Intermediaries/ Merchant Bankers/ Registrars and Transfer Agents/ Debenture Trustees/ Bankers to Issue/ Underwriters/ Credit Rating Agencies/ Depository Participants

9. Type-IX Securities Exchanges/ Clearing and Settlement Organizations/ Depositories

10. Type-X Derivatives Trading

11. Type-XI Corporate Governance/ Corporate Restructuring/ Substantial Acquisition and Takeovers/ Buyback/ Delisting/ Compliance with Listing Conditions

Source: SEBI Annual Report, 2004-05, www.http://sebi.gov.in.

SEBI has further specified that in order to have timely corrective actions, investors

are advised to address their grievances pertaining to above-said grievances directly to

Office of Investor Assistance and Education (OIAE) Division, SEBI Office, Mumbai

office or at its regional offices. As on date SEBI has the following regional offices

where the investors can lodge their grievances:

178

1. Northern Region : New Delhi

2. Eastern Region : Kolkata

3. Western Region : Ahmadabad

4. Southern Region : Chennai

5.2.2 Complaints not dealt by SEBI Investors are advised to know which types of the complaints are dealt and which

types of complaints are not dealt by SEBI. This would result in avoidance of wastage

of time of the investors as well as enable them for speedy redressal of their

grievances. Following types of complaints are not dealt by SEBI:

1. Complaints against unlisted/ delisted/ wound up/ liquidated/ sick companies.

2. Complaints those are sub-judice (relating to cases which are under

consideration of any court of law, quasi-judicial proceedings, etc.)

3. Complaints falling under the purview of other regulatory bodies e.g. Reserve

Bank of India, Insurance Regulatory Development Authority, Pension Fund

Regulatory and Development Authority of India (PFDRA), Competition

Commission of India (CCI), Forward Market Commission (FMC), etc.

5.2.3 SEBI Complaint Redressal System (SCORES) Faced with the piling of unaddressed investors’ grievances, SEBI, the market

regulator has put in place a web-based centralized system for speedy redressal of

these grievances. The present grievance system lacked a centralized database and the

resolutions of the grievances usually got delayed. By reducing the time gap between

the receipt and redressal of a complaint, the new system of SEBI is expected to help

in proper storage of investors’ grievances and their timely handling.

The new system is code named SCORES, i.e., SEBI Complaints Redressal System

(www.http://sebi.giv.in Circular No. CIR/OIAE/2/2011. June 3, 2011). The system

facilitates the investors for lodging the complaints pertaining to any of the regional

SEBI offices from anywhere across the country. All the grievances of the investors

are now in the electronic mode and linked to the central server. Besides this, the

179

investors are able to access the status of their complaints, including action taken, if

any, on their grievances. The salient features of the system are as under:

1. Centralized grievances tracking system for the entire SEBI,

2. Grievances pertaining to any of regional SEBI office can be lodged from

anywhere across the country,

3. All grievances and Action Taken Report to be in electronic mode, and

4. Action taken and the current status of the grievance can be accessed online by

the investors.

5.2.4 Status of Investor Grievance Received and Redressed Although the market regulator SEBI is making continuous efforts to redress the

pending complaints and have put in computerized system for early disposal of the

complaints, yet the number of unresolved investors’ complaints as on March 2011

stood at 150711 which includes 28,653 pending grievances cases where action is yet

to be initiated (SEBI, Annual Report 2010-11). Although as per SEBI, this number is

smaller, but if comparison is made with the unresolved complaints for the

corresponding previous years’ figures, the position is not. Table 5.4 gives a detailed

status of grievances received, redressed and pending during the last five years with

SEBI.

Table 5.4: Status of Investor Grievances Received and Redressed

Year

Grievances Received Grievances Redressed Pending Grievances Cumulative

Year-wise

Cumulative Year-wise

Cumulative Action Initiated

Pending

2006-07 26,473 25,62,047 17,899 23,95,895 1,66,152

2007-08 54,933 26,16,980 31,676 24,27,571 1,33,354 56,055

2008-09 57,580 26,74,560

75,989 25,03,560

1,21,887

49,113

2009-10 32,335 27,06,895 42,742

25,46,302 1,22,713 37,880

2010-11 56,670 27,63,565 66,542 26,12,854 1,22,058 28,653

Source: Compiled from SEBI Annual Reports for the period 2006-07 to 2010-11

180

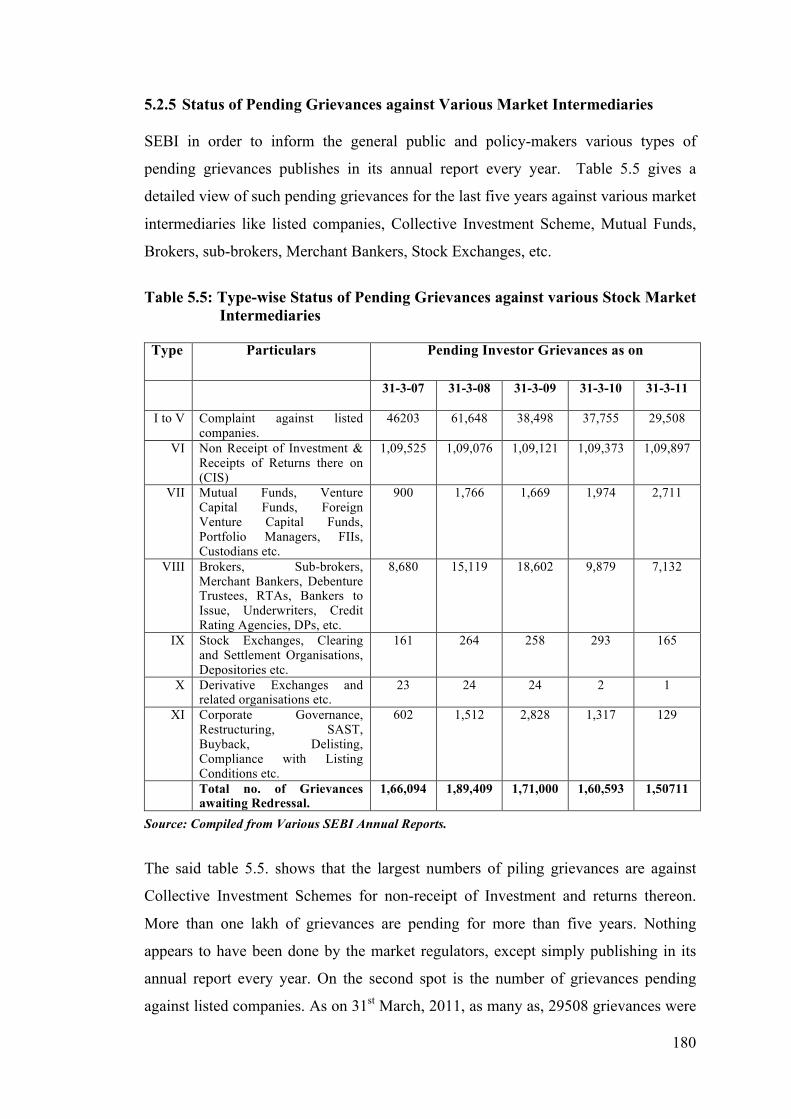

5.2.5 Status of Pending Grievances against Various Market Intermediaries SEBI in order to inform the general public and policy-makers various types of

pending grievances publishes in its annual report every year. Table 5.5 gives a

detailed view of such pending grievances for the last five years against various market

intermediaries like listed companies, Collective Investment Scheme, Mutual Funds,

Brokers, sub-brokers, Merchant Bankers, Stock Exchanges, etc.

Table 5.5: Type-wise Status of Pending Grievances against various Stock Market

Intermediaries Type Particulars Pending Investor Grievances as on

31-3-07 31-3-08 31-3-09 31-3-10 31-3-11

I to V Complaint against listed companies.

46203 61,648 38,498 37,755

29,508

VI Non Receipt of Investment & Receipts of Returns there on (CIS)

1,09,525 1,09,076 1,09,121 1,09,373 1,09,897

VII Mutual Funds, Venture Capital Funds, Foreign Venture Capital Funds, Portfolio Managers, FIIs, Custodians etc.

900 1,766

1,669

1,974

2,711

VIII

Brokers, Sub-brokers, Merchant Bankers, Debenture Trustees, RTAs, Bankers to Issue, Underwriters, Credit Rating Agencies, DPs, etc.

8,680 15,119

18,602

9,879

7,132

IX

Stock Exchanges, Clearing and Settlement Organisations, Depositories etc.

161 264

258

293

165

X Derivative Exchanges and related organisations etc.

23 24 24 2 1

XI Corporate Governance, Restructuring, SAST, Buyback, Delisting, Compliance with Listing Conditions etc.

602 1,512 2,828

1,317

129

Total no. of Grievances awaiting Redressal.

1,66,094 1,89,409 1,71,000 1,60,593 1,50711

Source: Compiled from Various SEBI Annual Reports.

The said table 5.5. shows that the largest numbers of piling grievances are against

Collective Investment Schemes for non-receipt of Investment and returns thereon.

More than one lakh of grievances are pending for more than five years. Nothing

appears to have been done by the market regulators, except simply publishing in its

annual report every year. On the second spot is the number of grievances pending

against listed companies. As on 31st March, 2011, as many as, 29508 grievances were

181

pending against the listed companies. Also, as many as, 7132 complaints of Type VIII

were pending with the market regulator. It is pertinent to note that despite the best

efforts of SEBI, the number of complaints has not come down considerably. This is a

serious issue and needs to be addressed at all levels. As per the following table, as on

31 March 2011, as many as 1,50,711 complaints are pending against various capital

market intermediaries. Out of these huge pending complaints, action against only

28,653 complaints has been initiated.

5.2.6 Enforcement against Listed Companies The details of enforcement actions against listed companies are presented in table 5.6.

Table 5.6: Enforcement Actions against Listed Companies for Failure to

Redress the Investors Grievances ( in Lakh)

S. No. Name of the company Penalty Imposed/ Action Initiated

1. Enkay Texofood Industries Ltd. 30,00,000 2. Jayant Vitamins Ltd. 17,00,000 3. Nexus Software Ltd. 10,00,000 4. Steelco Gujarat Ltd. 5,00,000 5. Pankaj Agro Protinex Ltd. 2,00,000 6. Motorol Enterprise Ltd. 25,00,000 7. Kleidscope Films Ltd. (Formerly known

as Gujrat Investment Castings Ltd.) 17,00,000

8. Akar Laminations Ltd. Directors Restrained 9. Bhuvan Tripura Industries Ltd. Directors Restrained 10. Chicago Software Industries Ltd. Directors Restrained 11. Dr. Softtech Industries Ltd. Directors Restrained 12. Hindustan Industrial Chemicals Ltd. Directors Restrained 13. Indo-American Credit Corporation Ltd. Directors Restrained 14. Indo-American Optics Ltd. Directors Restrained 15. Ishwar Medical Services Ltd. Directors Restrained 16. Kanel Oil & Export Industries Ltd. Directors Restrained 17. Kolar Information Technologies Directors Restrained 18. Neon Resin & Industries Limited Directors Restrained 19. Panjawani Packaging Ltd. Directors Restrained 20. Prakash Fortan Softech Ltd. Directors Restrained 21. Rane Computers Consultancy Ltd. Directors Restrained 22. Steelco Gujarat Ltd. Directors Restrained 23. Topline Shoes Ltd. Directors Restrained Source: Compiled from Various SEBI Annual Reports,

182

In order to initiate action against the defaulting companies and for speedy resolution

of the investors’ grievances, SEBI has identified top 100 companies in terms of

number of unresolved grievances and is vigorously following up for the resolution.

Adjudication proceedings have been initiated against twenty-three companies, which

failed to redress the investors’ grievances. As per the Table SEBI has levied penalty

against top seven defaulting companies, and the directors of sixteen defaulting

companies have been restrained from accessing the capital markets for a certain

period.

5.2.7 Regulatory Action against Suspended Companies It has been observed that number of unresolved cases against the suspended

companies are continuously piling. SEBI has also initiated action against the

suspended companies by initiating the following actions:

1. The members of board of directors of the suspended companies shall disclose

the details of their directorship in the offer document, if any, of the companies

whose shares have been/ were suspended from trading by stock exchanges,

when they were director of such suspended company for more than three

months, in the five year period preceding the date of filing of the offer

document.

2. Stock Exchanges have been advised to display on their respective websites, the

names of the companies suspended as on date along with the name of directors.

3. Stock Exchanges have been advised to submit report to SEBI in respect of each

suspended company along with the names of directors and the compliance

officer.

4. Directing the Stock Exchanges to allow the resumption of trading only after

resolution of all investors’ complaints to their satisfaction.

5.2.8 Action taken against Insider Trading and Market Manipulation SEBI has been initiating action against the various stock market intermediaries

including listed companies with regard to violations of insider trading and market

manipulation. Sabarinathan (2010), is of the view that Indian Securities Market is still

183

subject to several manipulative practices and lot of instances of insider trading do

happen. Although, SEBI has initiated action against the violators, yet from the data

published by SEBI shows much more is still desired to done to make the capital

market a safe place for market players.

Table no. 5.7 highlights SEBI’s record of action initiated against insider trading,

market manipulation and takeover, and action completed against these manipulations

for the last five years. The data given during the year indicates number of fresh cases

taken up during the year. This does not include the number of pending cases as on 1st

April. During the year 2005-06, 6 more complaints were received against insider

trading and proceedings against 8 were completed during the year. Similarly, SEBI

undertook 140 cases of market manipulation during the year 2005-06, but could

complete only 63.

Table 5.7: Record of Action against Insider Trading and Market Manipulation

Year Insider Trading Market Manipulation Takeovers Miscellaneous

Taken

up*

Completed Taken up*

Completed Taken up*

Completed Taken up*

Completed

05-06 6 8 140 63 4 3 15 7

06-07 18 10 95 81 2 3 5 8

07-08 7 28 12 118 2 2 4 21

08-09 14 12 54 63 3 1 5 7

09-10 10 10 46 53 2 5 13 6

Source: SEBI, Handbook of Statistics on the Indian Securities Market 2010, *The figures indicate numbers taken-up during the year in addition to pending as

on beginning of the year.

5.3 Grievance Redressal Mechanism with Ministry of Company Affairs (MCA)

5.3.1 Introduction Ministry of Corporate Affairs (MCA) acknowledges that there is a strong need for the

effective and efficient mechanism for redressal of the investor grievances. The Motto

of the Ministry is “Empowering Business, Protecting Investors.” It is the

184

responsibility of the Government to establish accountable, responsive and user-

friendly effective and efficient mechanism to that effect. Ministry of Company

Affairs deals with the Grievance Redressal Mechanism for investors in securities

market, which includes investor complaint form to be submitted to the Ministry. The

complaint pertaining to debentures or bonds, Fixed deposits (non-receipt of amount,

Miscellaneous non-receipt of shares/ funds and pertaining to non-receipt of share

certificate, Conversion, Splitting, Consolidation, Duplicate or submission of

indemnity bond, Transfer, Endorsement, Dividend warrants, Bonus, etc. may be

lodged with MCA.

5.3.2 Structure of Grievance Redressal Mechanism The grievances of the investors are received at various designated places. There are

mainly two nodal agencies that handle the grievances. These are:

1. Department of Administrative Reforms and Public Grievances

2. Directorate of Public Grievances, Cabinet Secretariat

5.3.3 Procedure of Handling the Grievances

The Department of Administrative Reforms and Public Grievances primarily

undertakes initiatives in the fields of administrative reforms and public in a hassle-

free manner, and eliminates the causes of grievance. The grievances received by the

Department are forwarded to the concerned Ministries/ Departments/ State

Governments/ UTs, which are dealing with the substantive function linked with the

grievance for redressal under intimation to the complainant.

On the basis of the grievances received, Department identifies the areas in which the

problems arise in a regular manner. These problem areas are then subjected to studies

and remedial measures are suggested to the concerned Department/ Organization.

5.3.4 Public Grievance Redressal Mechanism in Central Government Ministries/

Departments/ Organizations

1. The Public Grievance Redressal Mechanism functions in Government of India

on a decentralized basis. The Central Government Ministries/ Departments,

185

their attached and subordinate offices and the autonomous bodies dealing with

substantive functions deal directly with the mechanism.

2. The functioning of Public Grievance Redressal Machineries in various

Ministries/ Departments/ Organizations is regularly reviewed by a Standing

Committee of Secretaries.

3. With a view to ensure prompt and effective redressal to the grievances, a

number of instructions have been issued by Department of AR&PG from time

to time for quicker disposal of the complaints (Department of Administrative

Reforms and Public Grievances, Government of India, 2010).

5.3.5 On Line Registration of Grievances

The objective of the Ministry is to make ‘Public Grievance Redressal and Monitoring

System’ (PGRAMS) software, operational with every Director of Grievances. This

shall enable the Director of Grievances to immediately place the details of grievances

received in a database (efficient ‘dak’ management) as well as record the fact whether

he intends to monitor its progress, identify the section/division where it is being sent,

etc., generate the time taken in dealing with the grievance, enable review of pending

grievances in the organization or across the organizations, generate

acknowledgements to complainants, conduct analysis etc. The system should also

have the facility of on-line registration of grievances by the citizens and access to

information on the status of his/her grievances.

5.4 Grievance Redressal Mechanism at Stock Exchanges

5.4.1 Introduction Various Stock Exchanges of the country at the directions of SEBI have established

grievances redressal mechanism for the speedy and orderly redressal of the grievances

of the investors and have set up various mechanisms for the redressal of the

grievances (www.http://bseindia.com).

Table no. 5.8 depicts the various mechanisms that have been set by the Stock

Exchanges:

186

Table No. 5.8 : Grievance Redressal Mechanism of Stock Exchanges

S. No. Grievance Redressal Mechanism

1. Investor Service Cell & Investor Service Committee/

Investor Grievance Cell & Committee

2. Arbitration & Conciliation Mechanism

3. Investor Protection Fund

4. Listing Agreement Mechanism

Source: http://www:bseindia.com , http://www:nseindia.com

5.4.2 Investor Service Cell and Investor Service Committee Stock Exchanges as per the direction of SEBI have constituted Investor Service Cell

and Investor Service Committee to provide a host of services to the investors. The

activities of this cell and committee are to provide educational services like bulletin,

literature of the capital market, conducting seminars, encourage research papers etc.

The main objective of the cell/committee is to provide education and related

assistance to investors. The cell also continuously educate the investors about their

rights, responsibilities and various Dos & Don’ts related to stock market activities.

The most important job of the investor grievance cell/committee is redressal of the

grievances of the investors against both brokers and listed companies. Whenever any

complaint/ grievance is received, the investor service cell immediately records the

complaints and takes up with the concerned entity against whom the complaint/

grievances is lodged. The cell continuously follows up with both the investor and the

entity against which the grievance is lodged. It provides all the logistic support to the

investor in its bid to successfully resolve the grievance.

5.4.3 Investor Grievance Cell and Arbitration Committee Stock Exchanges have conciliation and arbitration mechanism to resolve the

grievances/ complaints of investors. If the complaint is not resolved at the level of

investor service cell, the matter is taken up with investor services committee of stock

exchange. If the complaint is still unresolved, the complainant is advised to approach

the arbitration mechanism of the Exchange. Stock Exchanges are having requisite

187

arbitration mechanism through the constitution of Arbitration Committees for

effective resolution of the investors’ complaints. One can go in appeal against the

appeal of the arbitration committee to the court of law within 90 days of the order of

the committee under section 34 of Arbitration and Conciliation Act, 1996. The

exchange arbitration mechanism is a quasi-judicial mechanism with a penal of

arbitrators, consisting of retired Judges and other professionals such as solicitors,

chartered accountants, company secretaries and other having expert domain of capital

market.

The stockbroker is the first point of contact in case of investor grievance. The byelaws

of the exchanges provide that investor should bring his dispute to the notice of broker

within six months of transactions. If it is not resolved, the investors can approach

Investor Grievance Cell of the stock exchange for the resolution of their complaints.

5.4.4 Arbitration and Conciliation Mechanism The bye-laws of the recognised Stock Exchanges provide for redressal mechanism for

disputes, between members or between members and non-members, through

conciliation and arbitration (the term "non-member" shall include a client (investor)

of the member), arising out of or in relation to any bargains, dealings, transactions or

contracts made subject to the Rules, Bye-laws, Circulars, Orders and Regulations of

the Exchange as well as instructions/ guidelines/ directions/ rules/ regulations issued

by Securities & Exchange Board of India/ Central Government from time to time or

with reference to anything incidental thereto.

5.4.4.1 SEBI Circular SEBI in consultations with Stock Exchanges has streamlined the arbitration

mechanism at stock exchanges arising out of claims, complaints, and differences

arising between investors and brokers and between broker members of exchange. The

said mechanism has been laid down vide SEBI circular no. CIR/MRD/DSA/24/2010

dated August 11, 2010. The SEBI circular provides for the detailed procedure and

carries the following contents:

1. Maintenance of Panel of Arbitrator

188

2. Code of Conduct for Arbitrators

3. Arbitration Procedures

4. Appellate Arbitration

5. Arbitration Fees

6. Place of Arbitration

7. Implementation of Arbitration Award

8. Records and Arbitration.

5.4.4.2 Arbitration Panel SEBI has laid down criterion for formation of arbitration panel. The arbitration

mechanism is as under:

1. Stock Exchanges shall maintain a panel of arbitrators having numbers of

arbitrators commensurate to the number of disputes;

2. Stock Exchanges shall have a set of fair and transparent criteria for inclusion of

names of arbitrators. While deciding the panel of arbitrators stock exchanges

shall look into their background like age, qualification of subject matter,

unblemished track record, etc.; and

3. Stock Exchanges shall enforce proper code of conduct.

5.4.4.3 Arbitration Procedure The limitation period for filing an arbitration reference has been prescribed as

provided in The Limitation Act, 1963. The arbitration claim or the counter claim up to

25 lakh is dealt with by a sole arbitrator, and for the amount above 25 lakh, the

same is to be dealt by a panel of three arbitrators. The stock exchange is to ensure that

the process of appointment of arbitrator(s) is completed within 30 days from the date

of receipt of application for arbitration. The arbitration reference has to be concluded

by way of arbitral award within four months from the date of appointment of

arbitrator(s).

5.4.4.4 Appellate Arbitration The aggrieved party by an arbitral award may appeal to the appellate panel of

arbitrations of the Stock Exchange against such award. The appeal before the

189

arbitrators is required to be filed within one month of the award, and the appellate

panel shall consist of three arbitrators who shall be different from the one who passed

the arbitral award. Stock Exchanges are supposed to appoint the appellate tribunal

within one month of the reference, and the panel has to dispose of the appeal within

three months of their appointment by way of appellate arbitral award.

“The conciliator(s) are guided by the Rules, Regulations, Bye-laws, Circulars, orders

of Exchange as well as the instructions, guidelines, directions, rules, regulations

issued by Securities and Exchange Board of India/ Central Government from time to

time. They are also supposed to follow the principles of objectivity, fairness and

natural justice while looking at the cases. They shall only attempt to reach a

settlement between the parties in relation to the dispute.”

5.4.5 Investor Protection and Education Fund SEBI (2003) through the Model Bye-laws has advised the stock exchanges to

establish and maintain an Investors' Protection Fund to protect the interests of

investors against the possible defaults or the expulsion of the trading members.

Objective of the said fund, is to compensate the investors a genuine and bona-fide

claim made by any client, who has either not received the securities bought from a

trading member for which the payment has been made by such client to the trading

member or has not received the payment for the securities sold and delivered to the

trading member or has not received any amount or securities which is/are legitimately

due to such client from the trading member, who is either declared a defaulter or

expelled by the Exchange.

5.4.5.1 Corpus and Composition of the Fund

SEBI has further advised the stock exchanges that every trading member of the

Exchange shall contribute such amount, as may be determined by the relevant

authority from time to time, to constitute the corpus of the Investors’ Protection Fund.

The relevant authority shall have the power to call for such additional contributions,

as may be required from time to time to make up for any shortfall in the corpus of the

Investors’ Protection Fund. The Exchange shall also credit to the Investors’ Protection

Fund such amount out of the listing fees collected by it in each financial year, as may

190

be prescribed by SEBI or as may be specified in the relevant Regulations from time to

time. The Exchange may also augment the Investors' Protection Fund from such other

sources, as it may deem fit.

5.4.5.2 Ceiling for Corpus The Exchange or SEBI may from time to time determine the ceiling amount up to

which the contribution from the trading members and contribution from the listing

fees shall be collected and credited to the Investors’ Protection Fund. While

determining the ceiling amount, the Relevant Authority may be guided by factors,

which may, inter alia, include highest amount of compensation disbursed from the

Investors’ Protection Fund in a financial year during the preceding five financial

years, amount of interest accrued to the Fund in the previous financial year and the

number of times the size of the corpus is a multiple of the highest aggregate amount

of compensation disbursed from the Investors’ Protection Fund in any particular

financial year. The relevant authority may, subject to taking prior approval of SEBI

with proper justification, decide to reduce, and/or not to call for, any further

contribution from the trading members and/or from listing fees.

5.4.5.3 Management of the Fund The Investors’ Protection Fund shall be held in trust and shall vest in the Exchange or

any other entity or authority, as may be specified by the relevant authority from time

to time. The Investors’ Protection Fund shall be managed by the Trustees appointed

under the Trust Deed created and executed and in accordance with the provisions

contained in the Trust Deed and the Rules, Byelaws and Regulations of the Exchange.

5.4.5.4 Utilization of the Fund Once the claim is lodged with the stock exchange for payment under the fund rules

and guidelines, the Trustees of the fund shall refer matter to the Committee for

Settlement of Claims Against Defaulters, which may scrutinize and vet each of the

claims placed before it for consideration after due screening by the officials of the

Exchange and also by an Independent Chartered Accountant, if need be, for satisfying

that each claim meets the requirements, as may be stipulated by the Committee for

Settlement of Claims against Defaulters from time to time.

191

5.4.5.5 Claims Entertained only if executed on the Trading System of Exchange (ATS) While considering a claim under the said rules, Committee for Settlement of Claims

against defaulters may direct payment of such claim, which, in the opinion of the

Committee, the investor has made the claim which has the direct relevance to such

transactions executed on the system of the Exchange.

5.5 Grievance Redressal Mechanism with Listed Companies vis-a-vis

Listing Agreement of Stock Exchanges Under section 21 of securities Contract (Regulation) Act, 1956, all the recognised

Stock Exchanges on the direction of SEBI have prescribed a listing agreement. Every

company, which intends to list its share with the recognised stock exchange is

required to execute listing agreement with it. The listing agreement contains 53

exhaustive clauses with the ultimate objective of protecting the interest of investors.

The listing agreement through its various clauses ensures the Redressal of their

Grievances also. A listing agreement is legal document, which is executed between a

company and a Stock Exchange when the securities of a company are listed on it. It is

binding on a company to comply with post-listing requirements of the listing

agreement. Any violation of provisions of listing agreement attracts strong penal

action from the Exchange which includes suspension in the trading of scrips of a non-

compliant company, fines, penalties and even delisting the company from stock

exchange.

5.5.1 Listing Agreement and Investor Protection The objective of entire listing agreement is to ensure the investor protection by

ensuring timely dissemination of important information to shareholders, publication

of financial results, adherence to the highest standards of corporate governance and

host of various other requirements which the listed company is required to implement

in an effective manner. Table 5.9 provides the summary of some of the clauses of the

Listing Agreement that directly relate to investor protection and grievance redressal

mechanism.

192

Table 5.9: Listing Agreement and Grievance Redressal Mechanism Clause No. and Contents

Rationale behind the Clause

3, 12, and 21 Timely handling of share certificates

As per these clauses, a company is required to execute share transfers within one month of lodgment. As most of the complaints are relating to share transfers, these clauses have been important legal provisions in the hands of investors.

12(a) Transfer of shares

This clause also strengthens an investor towards his request for transfer of shares. Subsection 12(a) of the Listing agreement stipulates that a company shall not refuse the transfer of shares when proper documents are lodged for transfer and there are no material defects in the documents except minor difference in signature of the transferor(s).

15 and 16 Book Closure

As per clause 15 & 16 of the Listing agreement, a listed company is required to give advance notice of Book Closure and record date to the Exchange. The same notice is disseminated on the website of the Exchange through trading terminals across the country. This instrument works for the protection of investors.

19 Price sensitive information

The objective of this clause is to inform the shareholders about these events so that undue fluctuations in the prices are avoided and investors are able to take informed decisions pursuant to such information.

20- Prior intimation to SE regarding board meetings

The objective of this clause is also to inform the shareholders as early as possible about the price sensitive information arising out of board decisions about these events so that undue fluctuations in the prices are avoided and investors can take well informed decisions in a timely manner.

30- To notify the exchange any material development

The objective of this clause is also to inform the shareholders of any material development at the earliest, so that the information reaches to all the investors at quickest possible time so that they are able to take informed decisions in a timely manner.

31(1) and 32 Copies of Annual Report

It is clearly evident that a listed company is required to supply a copy of annual report as per this clause and an investor specially a retail investor comes to know about state of affairs in a company.

35 & 36 Price sensitive information to Exchange.

These clauses empower the investors about any price sensitive information/ information having material impact on the operations of the company. These protect their interests by informing them and ensuring adequate disclosures from the company.

193

40- Minimum level of public shareholding

The rationale behind this clause is to have at all times the at least minimum number of shareholders in the company so as to have enough liquidity and public float in the scrips of the company.

41- Un-audited Financial results

This clause empowers the retail investors about vital financial information of a company at frequent levels which is also disseminated on the website of the Exchange where the securities of a company are listed.

49- Corporate Governance clause

This clause is the most important provision in the listing agreement which safeguards the interests of investors through following provisions: a. Role of Investors Services Committee, b. Role of Audit Committee, c. Independence of Board of Directors, and d. Other important disclosure provisions of this clause. This provision acts as a tool of investor protection. Independent directors and Audit Committee are expected to work for the interests of shareholders or investors. It ensures the accuracy and authenticity of Annual Accounts. Management Discussion and Analysis as part in the Annual Report of a listed company which discloses vital information about the opportunities, threats facing a company in a given business environment, risk and concerns, material developments in Human Resources and Industrial Relations, etc. Two provisions regarding shareholders and investors’ grievances committee are also very important and deal with information to be placed to investors about directors, their resumes, expertise etc. and constitution of a shareholders’ grievances committee for redressal of shareholders’ complaints like transfer of shares, non-receipt of balance-sheet, non-receipt of declared dividends etc. This institution of committee is a useful weapon in the hands of an investor to lodge his complaint if it is not resolved by the official/ Registrar & Transfer Agent of the company.

52- Corporate Filing and Dissemination System(CFDS)

SEBI has required all the listed companies to upload the corporate electronic filings in the exchange system in a standard format so that the investors get the latest information of the company without any hassles.

194

5.6 Regulatory Framework for Investor Grievances Redressal System and Protection for Retail Investors

A comprehensive policy framework exists for redressal of complaints of retail

investors in Indian securities market. Various acts, rules, regulations and circulars

have been brought into force by various regulatory authorities from time to time on

procedure for redressal of investor complaints. Following is the detailed description

of policy framework for resolution of investor complaints in India:

5.6.1 SEBI (Disclosure and Investor Protection) Guidelines, 2000 SEBI (Disclosure and Investor Protection) Guidelines were notified by SEBI in 2000

to regulate the primary market in India. The guidelines through its various provisions

stipulated the regulatory framework for companies proposing to issue securities,

promoters’ contribution and lock in requirements; contents of offer document, bonus

& preferential issues, etc. Various provisions of the aforesaid guidelines were in

force since 19.01.2000, but of late these guidelines have been repealed with ICDR.

These guidelines ensured that adequate disclosures are made by the companies

proposing to issue securities in the market and cast responsibilities upon various

market intermediaries and define their entry standards. These guidelines were

originally issued by SEBI in June, 1992 under section 11 of the SEBI Act, 1992 and

fresh DIP Guidelines were issued in 2000 and came into effect from 27.01.2000.

5.6.2 SEBI (Issue of Capital and Disclosures Requirement) Regulations, 2009 (ICDR)

SEBI, vide powers conferred by section 30 through a Gazette of India notification

(2009), prescribed SEBI (Issue of Capital and Disclosures Requirements)

Regulations, 2009, which shall be applicable to the followings:

1. a public issue,

2. a right issue value the aggregate value of specified securities offered is

fifty lakh rupees or more,

3. a preferential issue,

4. an issue of bonus shares by a listed issuer,

5. a qualified institution placement by a listed issuer,

195

6. an issue of Indian Depository receipt.

These regulations are divided into eleven chapters and twenty schedules. The chapter

inter alia deals with the disclosures’ requirements and cast responsibility upon the

issues of the securities with the ultimate objective of protection of interests of the

investors. These guidelines contain the provisions relating to common conditions for

the public issues, right issues and bonus issues, eligibility of requirements, pricing in

public issues, promoter’s contributions, pricing in public issues, promoters

contribution, its lock-in period (restriction on transferability), minimum offer to

public, disclosures and the manner of such disclosures, preferential issues, qualified

institutional placements, provisions relation to the issue of Indian Depository

Receipts, responsibilities of company management, merchant bankers and various

other intermediaries associated with issue process etc.

The schedules cover the inter-se responsibilities of the company and intermediaries,

formats for the issue of due diligence certificates and agreement between lead

merchant banker and issuer company, mandatory collection centers, and fees to be

paid along with the offer document, Manner of Submission of Soft copy of Draft

Offer Document and Offer Document to the SEBI etc. The schedules further specify

nature of up-dating/ changes in the offer document, disclosures in offer document,

abridged prospectus & abridged prospectus, formats or report to be submitted by

monitoring agency, facilities or services included in the term Infrastructure Sector,

book building process, format of report for Green Shoe Option, formats for

advertising for Public Issues, illustration explaining minimum application size,

illustration explaining procedure of allocation, formats post issue reports, format of

underwriting development statement, disclosures in placement document, disclosures

in prospectus & abridged prospectus for issue of Indian Depository Receipts, and

amendment in other regulations etc.

5.7 Grievance Redressal Mechanism at few leading Foreign Stock

Exchanges International stock exchanges have a strong system of grievances resolution and these

exchanges too have online filing of complaints. These exchanges use arbitration as

quick dispute resolution method as it involves lesser amount of time and justice is

196

delivered in a shortest possible time. Given below is the mechanism of complaint

resolution at few international stock exchanges like New York Stock Exchange,

Singapore Stock Exchange, Australian Stock Exchange, Taiwan Stock Exchange,

Toronto Stock Exchange and IOSCO wherein the system of investor grievances

redressal mechanism has been explained.

5.7.1 Grievance Redressal Mechanism of New York Stock Exchange (NYSE) The New York Stock Exchange has a well-defined system for the redressal of the

investors’ grievances. NYSE welcomes information from investors and others who

believe that a broker has violated securities rules and regulations. Following sorts of

complaints can be lodged with NYSE on-line system:

1. Order execution,

2. Insider trading,

3. Market manipulation on NYSE,

4. Unfair sale practices,

5. Improper business conduct by brokers or their representatives,

6. Banks and Saving Institutions,

7. Insurance Companies, and

8. Transfer Agents (www.http://usequities.nyx.com/regulation/complaints-

and-inquiries/before-proceeding).

The Grievance Redressal Mechanism of New York Stock Exchange deals with

dispute resolution mechanism to resolve disputes between investors and brokers. It

includes Arbitration, which enables a dispute to be resolved quickly and fairly by

impartial arbitrators, who are knowledgeable and trained in the art of resolving

disputes relating to transactions in securities. The investors are first advised to contact

the broker and if it fails to resolve, the investors may lodge the complaint with NYSE.

In order to quickly resolve their grievances, the investors are advised to submit their

complaints with following details:

1. Name of security and stock symbol

2. Date of the trade

197

3. Specific order information

4. Order type e.g. buy, sell. Limit price or market order, etc.

5. Order size

6. Order identification code, branch code and sequence number

7. Specific nature of complaint or enquiry.

The investor can also go for arbitration mechanism, and if he chooses arbitration to

resolve the dispute, he waives the right to pursue the matter in court. Arbitration is

final and binding. It further mentions that an individual investor with a complaint or

inquiry about an NYSE brokerage firm or individual broker may file online

complaints with NYSE.

5.7.2 NASD and SIPC

5.7.2.1 Role of NASD

NASD-DR,

and the New York Stock Exchange are the leading providers of

arbitration services for the securities industry in US. They have adopted detailed

procedures for conducting the arbitrations they sponsor. The Securities Exchange

Commission (SEC) of US, as part of its oversight of the SROs, reviews the procedural

fairness of SRO arbitration rules through its review and approval of proposed SRO

rule changes. The SEC also inspects the SRO arbitration programmes on a regular

basis. The SROs’ arbitration rules require arbitrators to disclose potential conflicts

and give parties the ability to strike or challenge arbitrators based on those disclosures

(Perino, 2002). Although the NASD does about 90% of securities arbitrations in US,

it further regulates the market through computerised audit trail system called RADAR

(Research and Data Analysis Repository) surveillance mechanism (NASD Corporate

Profile). There are three primary components of the arbitration process:

1. Obtaining and updating arbitrator background information;

2. Arbitrators’ disclosure obligations and conflict training; and

3. Selecting the arbitration panel.

198

5.7.2.2 The Securities Investor Protection Corporation (SIPC) Securities Investor Protection Corporation (SIPC) is a government mandated, non-

profit organization at United States. Its objective is to protect the investors in certain

securities related losses to investors from the brokers default. However, it does not

protect the investors against losses in the securities markets, identity theft, or other

3rd-party fraud.

Although, it is not a US government agency, but SIPC was established in 1970 by an

Act of Congress through adoption of the Securities Investors Protection Act. SIPC

serves two primary roles in the event when a broker fails. First, SIPC acts to organize

the distribution of cash and securities to investors from the broker concerned. Second,

if the broker is not in a position to pay the requisite amount or the securities, SIPC

provides insurance coverage up to $500,000 of the customer's net equity balance,

including up to $250,000 in cash.

It protects the investors against the non-payment of funds and most types of

securities, such as notes, stocks, bonds, and certificates of deposit. Other items, such

as commodity or futures contracts, are not covered which are registered with the

Securities and Exchange Commission (www.http://sipc.org).

5.7.3 Grievances Resolution Mechanism of Singapore Stock Exchange (SGX) If anyone has a complaint against a Singapore Stock Exchange (SGX), its Member

such as securities or futures broker or a person registered with SGX such as a trading

representative (typically a remeiser, dealer or futures trader) and one has information

concerning an instance of market misconduct? –he can make the lodge the complaint

in the specified format to the authorities for the redressal of his grievances. The

grievance redressal mechanism at SGX is given below:

5.7.3.1 Lodging a Complaint against Stock or Futures Broker If the complaint is regarding a commercial dispute between the complainant and his

broker or trading representative for unsatisfactory service by the broker or trading

representative or it relates to technical problems with a broker's trading system,

investor is first advised to lodge a complaint promptly with his broker. If the investor

199

fails to receive a satisfactory response after follow-ups with the broker, he may lodge

a complaint with SGX. If the matter is purely commercial, the SGX does not

intervene in the dispute. But if it involves a breach of SGX rules, the Exchange does

consider an investigation of that matter.

5.7.3.2 Lodging a Complaint with Singapore Exchange Where a matter is relating to alleged improper conduct by a broker/ trading

representative, who had allegedly executed trades in the account of an investor

without his approval, investor may lodge the complaint with Singapore Stock

Exchange (SGX). When filing a complaint, the investors are advised to include the

following information in their complaint:

1. Name, address and contact numbers of the complainant,

2. The name of the brokerage firm and the individuals at the firm with whom

the complainant dealt, and

3. A description of the alleged improper conduct; the date when the improper

conduct took place and the details of the transactions involved.

The focus of investigation is regulatory in nature. If SGX is of the view that a breach

has occurred, it may commence disciplinary proceedings against the broker/trading

representative. However, its investigations do not necessarily result in compensation

to the complainant by the broker or the withdrawal of civil proceedings to recover

amounts owned. SGX pay compensation to the aggrieved investors from the Fidelity

Fund (a fund created for this purpose) up to a maximum amount of $ 50,000, and the

present corpus of the fund is $ 53 million.

5.7.4 Grievance Redressal Mechanism at Australian Stock Exchange Australian Stock Exchange (ASX) is committed to addressing complaints and

enquiries from the investors in a timely manner. ASX believes that timely resolution

of the grievances of investors results in fair, orderly and transparent markets and at

the same time it ensures that market participants at all times are complying to their

obligations under the ASX rules. ASX has specified that it would be able to assist in

the following matters:

200

1. Matters where a stock broker may have breached the ASX operating Rules,

2. Matters where listed companies may have breached the ASX Listing Rules,

3. Matters related to the Clearing House Electronic Sub-Register System

(CHESS Depository) Holding Statements, and

4. Matters related to the operations of the clearing and settlement facilities,

including activities of ASX.

The ASX rules further advise investors how to contact and where to contact, if they

have any grievances against the market participants. For the following types of

grievance, the investors are advised to contact Australian Securities and Investments

Commission (ASIC):

1. Breach of ASIC Market Integrity Rules including potential stock market

manipulations, client order instructions, client order priority, provision for

confirmation/ contract notes,

2. Breach of Corporations Act including provision of advise and quality of

advise, potential insider trading, stock price manipulation, short selling,

margin lending, false and misleading information, stock lending and

borrowing, directors’ duties, prospectus requirements and other disclosure

obligations.

The investors are advised to complete the ASX complaint form and send to the ASX

Customer Service Centre along with all the supporting documents. ASX confirms that

the acknowledgement is given within two business days of receipt of the complaint

and final response within 21 business days to the complainant. ASX rules further state

that it would refer the complaint to ASIC if the substance of the complaint relates to

the matter within the ASIC’s jurisdiction.

5.7.5 Grievance Redressal Mechanism of Taiwan Securities Market Taiwan has one of the most advanced trading and clearing system in the world. It is

the only country, which has T+1 trading mechanism. Even India, which boasts of one

of the most vibrant settlement system in the world, has T+2 system. Taiwan

201

acknowledges it of utmost importance to enhance investor protection by ensuring

their rights and benefits. Its investor protection and grievance redressal mechanism

includes strong surveillance mechanism of stock exchange, the level of corporate

governance and self-regulation by the various enterprises. Taiwan enacted the

Investor Protection Law in 2003 with the following objectives:

1. To establish a protection centre and build up a protection fund for investor

protection,

2. To compensate the investors out of the funds in case of breach by the

intermediaries,

3. To handle the complaints and to act as a mediation settlement to settle the

grievances and to pass irrevocable judgment, and

4. To put its efficient action and effective arbitration mechanism in place

(www.http://oecd.org/finance/financialmarkets/18468447.pdf).

In order to strengthen investor protection and promote the sound development of the

securities and futures markets in Taiwan, the Securities and Futures Investors

Protection Center was set up in 2003. In addition to consultation and mediation, the

Center also handles investors’ complaints, files class-action lawsuits on behalf of

investors, and derivative suits on behalf of companies. This Center also manages an

investor compensation fund. It also provides consummations with regard to various

issues concerning investors’ rights in securities market. Where an individual is

involved in a dispute related to the trading of securities or futures, the person may opt

for arbitration mechanism or go for civil lawsuit. The Center has a arbitration or

mediation committee to provide mediation for civil disputes involving securities and

futures investors. Any individuals who are involved in a dispute may apply for

mediation with the Center.

In order to protect investor rights, the centre may file lawsuits or submit cases for

arbitration on behalf of twenty or more securities or futures investors affected by the

same incident. This helps speedy resolution of complaints from investors. In order to

strengthen corporate governance mechanisms and protect investors from securities

fraud schemes, the Center may advise company management to file a lawsuit against

the director(s) accused of wrongdoing or vice versa in the event that they may have

202

performed actions or duties that are, or were, materially injurious to the company or

are in violation of laws whenever conducting business. If the supervisors or directors

fail to act upon the advise within thirty days after receiving the advise made by the

Center, then the Center may file the lawsuit on behalf of the company. In case, the

insiders as defined under Article 157 of the "Securities and Exchange Act" and

Article 11 of the "Securities and Exchange Law Enforcement Rules", make any

profits from buying and selling the securities of the company within six months of the

transaction, they are bound to deposit the profits earned.

As required by the Securities Investor and Futures Trader Protection Act, the Center

has set up a protection fund to protect the rights of securities investors and futures

traders. The compensation is paid from the fund, in case, the brokerage firms become

insolvent are can not pay to the investors. Like wise in order to protect the investors

as global level, the Center signed the Memorandum of Understanding with the

Securities Investors Protection Corporation (SIPC) of the U.S. and Canadian Investors

Protection Fund of Canada in June 2006 and March 2009 respectively. These

memorandums, provide a sound mechanism for the investor protection. This was

done not only to safeguard the rights of investors in cross-border transactions, but also

to offer an sound platform for information exchange and cooperation.

(http://www.twse.com.tw/en/about/company/guide.php, and www.sfipc.org.tw.)

Thus, Taiwan has one of the most effective and robust corpus of the Investor

Protection Fund. As on March 2010, it has a huge corpus of NT$ 1.031 billion and it

aims to have NT$ 5 billion. The rules of the investor protection provide a detailed

mechanism to settle the grievances of the investors. The maximum compensation

amount to each investor or trader is NT$ 1 million, and maximum compensation

amount to be paid to total investors or traders of each security from the fund is NT$

100 million. Apart from this, there is a provision for legal suits in the case of insider

trading, effective arbitration mechanism and irrevocable judgment against the erring

market intermediaries.

203

5.7.6 Investor Protection in Canada- Toronto Stock Exchange The Canadian securities legal system is structured and evolved in such a way that

investors’ protections are fairly consistent between common law and civil law

provinces. Toronto Stock Exchange is seventh largest stock exchange in the world in

terms market capitalization with US $ 1912 billions as on December 31, 2011

(http://en.wikipedia.org/wiki/List_of_stock_exchanges, 2011) which is around 4.4%

of the world’s market capitalization, and it has fairly large numbers of players in the

market. Toronto Stock Exchange (TSX) is the largest stock exchange in Canada with

about 4000 listed companies. As regards investor protection, Canadian system has

managed to maintain level of profitability, liquidity and financial stability during the

credit and financial crisis. Although, the system is effective, it is complex in nature

because of multiple regulators managing each province.

Canada regulation are unique as it employs regulators only at the provincial and

territorial level. As a result, the securities regulation landscape is divided into thirteen

jurisdictions. It increase noncompliance and impose unnecessary costs on investors

and market participants. There is thus overlapping of functions and may cause delay

in redressal of investors’ grievances (Puri, 2012). Consequently, the Canadian

Securities Administrators (“CSA”) undertakes coordination efforts across provinces

and territories, and aligns policy goals across jurisdictions with regard to law

enforcement and redressal of investors grievances.

All over the world, there is debate over the single regulator for banking, insurance and

capital market in a country, yet Canada continues to have as many as thirteen

provincial and territorial regulators, each with its own securities act, fees and

regulations. This causes the increase in cost and other operation difficulties. This

system has inherent weakness in the form of inefficient allocation of resources, co-

ordination problems, high cost involved, time delays, and the most important non-

proper priorities for the investor protection. The civil law jurisdiction as prevalent in

Canada provides weaker legal protection than common laws jurisdictions. There are

separate investor protection laws in Canada Business Corporation Act (CBCA) and

Qualifications and Curriculum Authority (QCA) and there are multiple corporate laws

statutes with each province and the federal government having their own statutes. As

204

a whole, there are lesser investors’ complaints and it remained unscathed from the

2007-2009 financial crisis. Despite complex regulatory system, Canada has

maintained safe and sound capital market environment. Halpern and Puri (2007) are

of the view that amidst the economic turbulence that the world has experienced since

2008, Canada is perceived to have a safe and stable regulatory system and a

conservative banking industry. As quoted by them, Washington Post writes that,

“While the United States reels from the global financial crisis, with credit markets

still frozen and stock prices careening from highs crease Canada’s competitiveness

and maintain investor protection.

5.7.7 IOSCO and Investor Protection The objectives od IOSCO is to promote the financial stability across the globe by

joining the regulations of all the countries at a common platform by applying the

consistent standards across all world’s financial markets with an ultimate objective to

enable to enable effective enforcement across jurisdictions. Diplock (2010) states that

the regulators across the globe through the mechanism of IOSCO membership, aim do

the followings:

1. to cooperate in promoting high standards in securities regulations in order to

maintain just, efficient and sound market;

2. to cooperate in promoting high standards of regulation in order to maintain just,

efficient and sound markets;

3. to cooperate in promoting high standards of regulation in order to maintain just,

efficient and sound markets;

4. to exchange information on their respective experiences in order to promote

development of their domestic markets;

5. to exchange information on their respective experiences in order to promote

development of their domestic markets;

6. to unite their efforts to establish standards and effective surveillance of

international securities transactions; and

7. to assist each other in promoting the integrity of markets by rigorous application

of standards and their effective enforcement.

Likewise, Okubo (2011), states that IOSCO cooperates, supports and coordinates

205

with other members of organization other committees and their members, in order to

enhance the effectiveness and value of self regulation in promoting efficiency,

transparency and integrity of markets; contribute to regulatory policy development

and implementation through the expertise and input provided by its members and

related parties; identify potential investor protection and market integrity issues and

proactively address emerging trends; effectively address the wide range of issues in

securities markets for the benefit of the regulatory community and investors globally;

and share experiences as SROs with other members and interested parties through

seminars and training programs.

International Organisation Securities Commission (IOSCO) has made a system for the

investor protection where it receives alerts and warnings from its members about

firms which are not authorized to provide investment services in the jurisdiction

which issued the alert or warning. Some of the alerts or warnings are about

unauthorized firms using names similar to those of authorized firms or about

unauthorized firms falsely claiming to be associated with authorized firms. The alerts

and warnings are provided in the specified formats and the investors can download

the details of the warning by clicking the download button. These warnings are

provided by IOSCO members on a voluntary basis. The contents of the alerts and

warnings are the responsibility of the IOSCO member which issues them.

By clicking on these the investors are directed to the text of the alert or warning on

the IOSCO member's web page. Investors are advised to look at the IOSCO member's

web page to get all the relevant information. Only alerts posted during the previous

and current months are visible, but the investors can reach to all alerts which are

searchable.

5.8 Summary From the above, it is evident, that in India, there is multiplicity of agencies involved

in the redressal of investor complaints with specific tasks assigned to them. Some of

the key areas have overlapping of various activities, and because of this, there is lack

of clarity. This causes confusion not in only in the minds of intermediaries, but also

confuses the investors. For a retail investor who has not adequate resources, expertise

206

and knowledge and skills, it is a very complex and cumbersome process for him to

have redressal of his complaints in a timely and effective manner. He wastes a

considerable time and energy in approaching the authorities and mechanism as stated

above. Some-times, when he gets the justice, it is too late, and the very purpose of

filing his complaint is defeated. If he gets his shares back say after one year, the

market price of the shares may have gone down to a considerable extent causing him

the great loss. Similarly, if he gets his money after a long gap, he looses opportunities

in the market. In nutshell he is so frustrated with lengthy grievance redressal system,

he decides to say goodbye to the investing in securities market altogether.

Hence, there is need for devising a simpler, cost- effective and time bound grievance

redressal mechanism for retail investors, which will go a long way in protecting the

interests of investors. This would make Indian securities market deeper and broader,

and more and more money would come to securities market.

207

References