Embed Size (px)

Citation preview

CHAPTER 5CHAPTER 5 Learning About Learning About Return and Risk Return and Risk from the from the Historical RecordHistorical Record

5-2

Factors Influencing Rates

• Supply

– Households

• Demand

– Businesses

• Government’s Net Supply and/or Demand

– Federal Reserve Actions

5-3

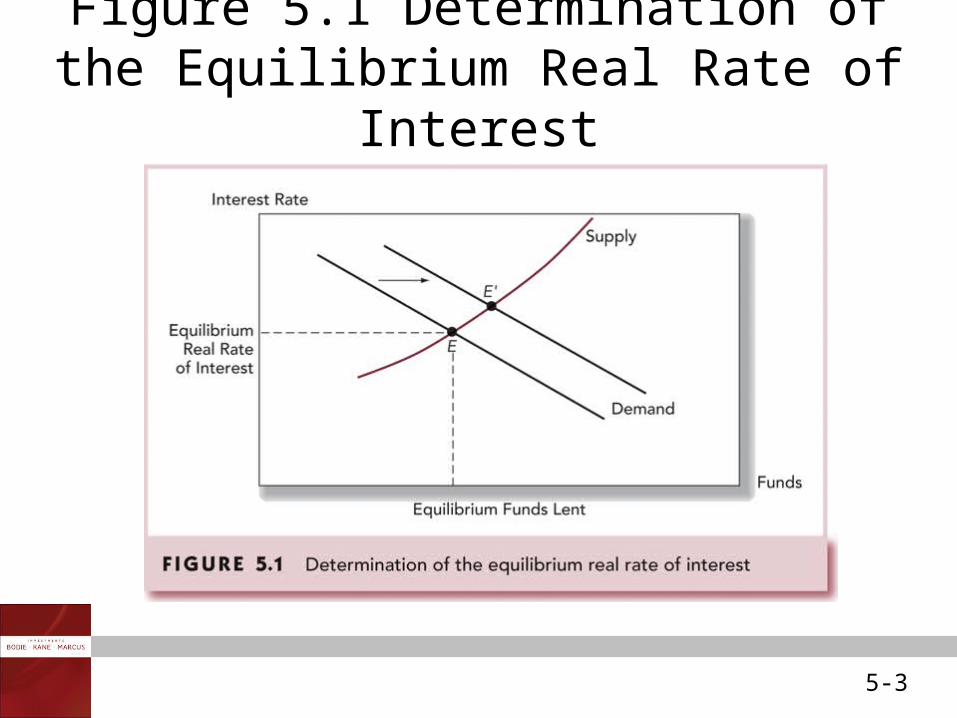

Figure 5.1 Determination of the Equilibrium Real Rate of Interest

5-4

Equilibrium Nominal Rate of Interest

• As the inflation rate increases, investors will demand higher nominal rates of return

• If E(i) denotes current expectations of inflation, then we get the Fisher Equation:

( )R r E i

5-5

Taxes and the Real Rate of Interest

• Tax liabilities are based on nominal income

– Given a tax rate (t), nominal interest rate (R), after-tax interest rate is R(1-t)

– Real after-tax rate is:

(1 ) ( )(1 ) (1 )R t i r i t i r t it

5-6

Comparing Rates of Return for Different Holding Periods

100( ) 1

( )fr T P T

Zero Coupon Bond

5-7

Formula for EARs and APRs

1

{ } 11 ( )

1(1 )T

TfEAR r T

EARAPRT

5-8

Bills and Inflation, 1926-2005

• Entire post-1926 history of annual rates:

– www.mhhe.com/bkm

• Average real rate of return on T-bills for the entire period was 0.72 percent

• Real rates are larger in late periods

5-9

Table 5.2 History of T-bill Rates, Inflation and Real Rates for Generations, 1926-2005

5-10

Figure 5.2 Interest Rates and Inflation, 1926-2005

5-11

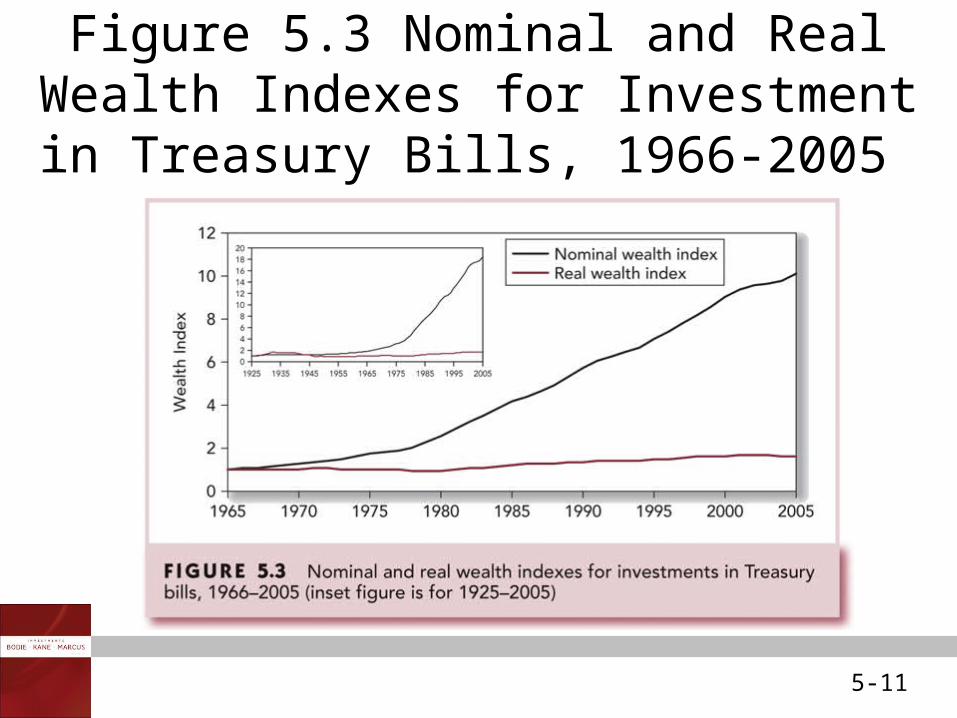

Figure 5.3 Nominal and Real Wealth Indexes for Investment in Treasury Bills,

1966-2005

5-12

Risk and Risk Premiums

P

DPPHPR0

101

HPR = Holding Period Return

P0 = Beginning price

P1 = Ending price

D1 = Dividend during period one

Rates of Return: Single Period

5-13

Ending Price = 48

Beginning Price = 40

Dividend = 2

HPR = (48 - 40 + 2 )/ (40) = 25%

Rates of Return: Single Period Example

5-14

Expected returns

p(s) = probability of a stater(s) = return if a state occurss = state

Expected Return and Standard Deviation

( ) ( ) ( )s

E r p s r s

5-15

State Prob. of State r in State 1 .1 -.052 .2 .053 .4 .154 .2 .255 .1 .35

E(r) = (.1)(-.05) + (.2)(.05)… + (.1)(.35)E(r) = .15

Scenario Returns: Example

5-16

Standard deviation = [variance]1/2

Variance:

Var =[(.1)(-.05-.15)2+(.2)(.05- .15)2…+ .1(.35-.15)2]Var= .01199S.D.= [ .01199] 1/2 = .1095

Using Our Example:

Variance or Dispersion of Returns

22 ( ) ( ) ( )s

p s r s E r

5-17

Time Series Analysis of Past Rates of Return

n

s

n

ssr

nsrsprE

11)(

1)()()(

Expected Returns and the Arithmetic Average

5-18

Geometric Average Return

1 2(1 )(1 ) (1 )nnr r rx xTV

TV = Terminal Value of the Investment

1/1 TVg n

g= geometric average rate of return

5-19

Variance and Standard Deviation Formulas

• Variance = expected value of squared deviations

• When eliminating the bias, Variance and Standard Deviation become:

22

1

1( )

n

s

r s rn

2

1

1( )

1

n

j

r s rn

5-20

The Reward-to-Volatility (Sharpe) Ratio

Sharpe Ratio for Portfolios =Risk PremiumSD of Excess Return

5-21

Figure 5.4 The Normal Distribution

5-22

Figure 5.6 Frequency Distributions of Rates of Return for 1926-2005

5-23

Table 5.3 History of Rates of Returns of Asset Classes for Generations, 1926- 2005

5-24

Table 5.4 History of Excess Returns of Asset Classes for Generations, 1926- 2005

5-25

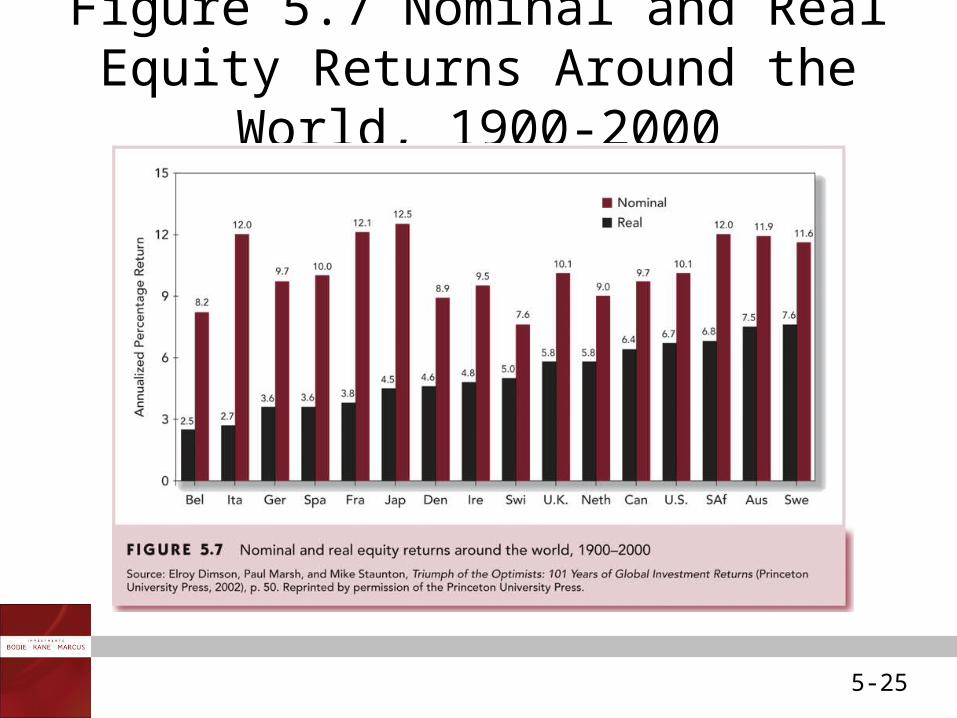

Figure 5.7 Nominal and Real Equity Returns Around the World, 1900-2000

5-26

Figure 5.8 Standard Deviations of Real Equity and Bond Returns Around the World, 1900-2000