Embed Size (px)

Citation preview

7.1 | P a g e

Principles of Real Estate Chapter 7-Brokerage And Agency

This chapter will underline the responsibilities agents, brokers, sellers, buyers and third-party agents have to each other. It will also explore the different regulations each party must follow.

Overview

This chapter will underline the responsibilities agents, brokers,

sellers, buyers and third-party agents have to each other. It will

also explore the different regulations each party must follow.

7.2 | P a g e

Objectives

At the end of this chapter, the student will be able to:

Recognize, define and provide examples of the principal's obligations to an agent

Describe the obligations of a listing agreement, and list and define each type of listing

Identify the ways in which a listing agreement can be terminated

List and describe the three buyer agency agreements, and provide an explanation of a buyer agency

Define antitrust Recognize the purpose of antitrust laws List actions violating antitrust laws Provide the fines for violating antitrust laws

Agency

An agency is created when one person, called the principal, delegates to another person -- called the agent -- the right to act on the principal's behalf in dealing with third parties.

The principal in an agency relationship can be either a natural person or a legal person, such as a corporation. Likewise, an agent can either be a natural person or a corporation such as a real estate brokerage company.

The people and firms with whom the principal and agent negotiate are called third parties. You will also hear these third parties referred to as the broker's customers and the principal referred to as the broker's client.

Levels of Agency

There are three levels of agency:

Universal agency General Agency Special Agency

7.3 | P a g e

Universal Agency

A universal agency is one in which the principal gives the agent legal power to transact matters of all types on the principal's behalf.

An example is an unlimited power of attorney.

Universal agencies are rarely encountered in practice, and courts generally frown on them because they are so broad.

General Agency

A general agency is one in which the agent is given the power to bind the principal in a particular trade or business. For example, a salesperson is a general agent of his or her employing broker. Another example is that of a property manager for a property owner.

Special Agency

A special agency is one in which the principal empowers the agent to perform a particular act or transaction.

One example is a real estate listing. When a salesperson lists a property for his firm, the agency relationship created between the seller and broker is

a special agency.

Creating an Agency

Agencies can be created in a few different ways:

Written agreement Ostensible agency Agency by ratification Agency coupled with an interest Dual agency

7.4 | P a g e

Written Agreement

A written agreement is the preferred method of creating an agency because it provides a document to evidence the existence of the agency relationship.

Ostensible Agency

An ostensible agency is created when a principal gives a third party reason to believe that another person is his agent even though that person is unaware of the appointment. If the third party accepts this as true, the principal may well be bound by the acts of his agent. For example, you give your house key to a plumber with instructions that when he has finished unstopping the water lines he is to lock the house and give the key to your next-door neighbor. Even though you do not call and expressly appoint your neighbor as your agent to receive your key, once the plumber gives the key to your neighbor, your neighbor becomes your agent with regard to that key. Since you told the plumber to leave the key there, he has every reason to believe that you appointed your neighbor as your agent to receive the key.

Agency by Ratification

An agency by ratification is one established after the fact.

For example, if an agent secures a contract on behalf of a principal and the principal subsequently ratifies or agrees to it, a court may hold that an agency was created at the time the initial negotiations started.

Agency Coupled with an Interest

An agency coupled with an interest is said to exist when an agent holds an interest in the property he is representing.For example, a broker is a part-owner in a property he has listed for sale.

Dual Agency

A dual agency is created when there are two principals in the same transaction. A dual agency requires that the agent have written permission from each principal to perform in that capacity.

Dual agency is not allowed in all states.

7.5 | P a g e

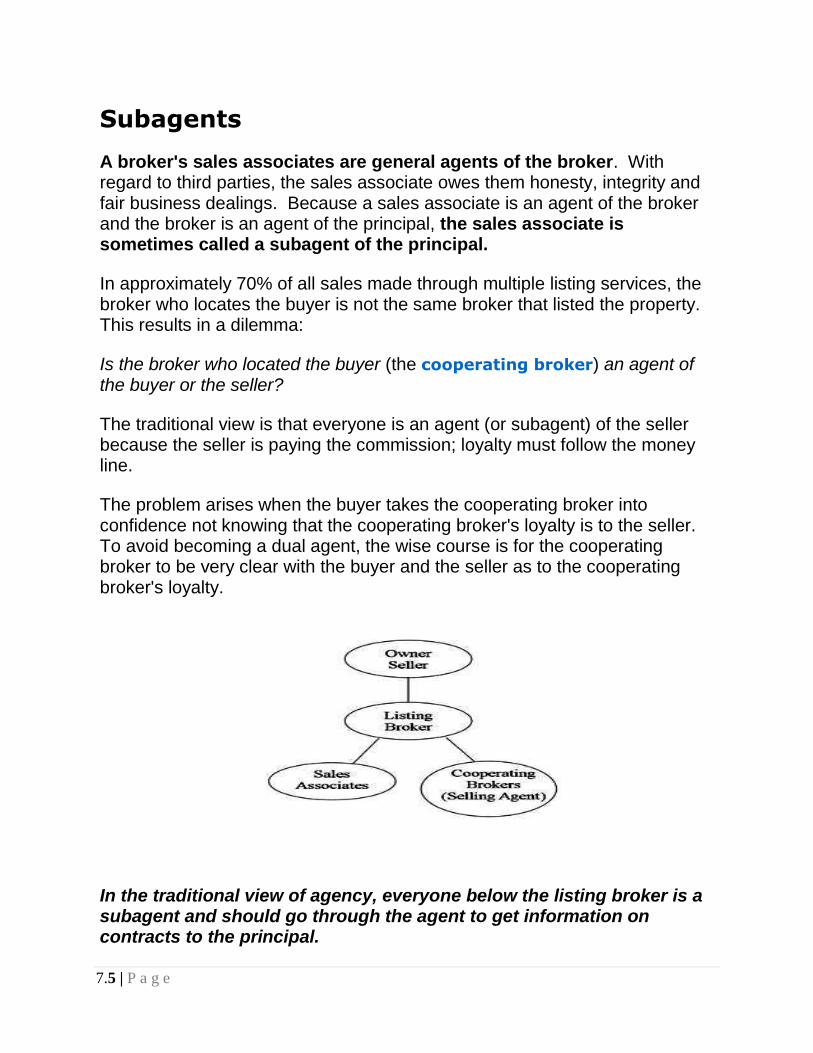

Subagents

A broker's sales associates are general agents of the broker. With regard to third parties, the sales associate owes them honesty, integrity and fair business dealings. Because a sales associate is an agent of the broker and the broker is an agent of the principal, the sales associate is sometimes called a subagent of the principal.

In approximately 70% of all sales made through multiple listing services, the broker who locates the buyer is not the same broker that listed the property. This results in a dilemma:

Is the broker who located the buyer (the cooperating broker) an agent of the buyer or the seller?

The traditional view is that everyone is an agent (or subagent) of the seller because the seller is paying the commission; loyalty must follow the money line.

The problem arises when the buyer takes the cooperating broker into confidence not knowing that the cooperating broker's loyalty is to the seller. To avoid becoming a dual agent, the wise course is for the cooperating broker to be very clear with the buyer and the seller as to the cooperating broker's loyalty.

In the traditional view of agency, everyone below the listing broker is a subagent and should go through the agent to get information on contracts to the principal.

7.6 | P a g e

Termination of Agency

An agency is terminated by the operation of law upon the death or incapacity of either party (except that an agency coupled with an interest is not terminated by the death of the principal), by the destruction or condemnation of the property, upon the bankruptcy of either party, or foreclosure of the principal.

An agency is rarely terminated by operation of law, however, and is most often terminated in one of the following ways:

By the purpose of the agency being completed By expiration of the term of the agency By mutual agreement By revocation. An agency may be revoked by either party at any time,

except that an agency coupled with an interest may not be revoked by the principal.

Fiduciary Obligations

The broker, as an agent, owes his or her principal certain duties. These duties are clear and specific. They are not simply moral or ethical; they are the law -- the law of agency. An agent has a fiduciary relationship with his or her principal; that is, a relationship of trust and confidence between employer and employee.

This confidential relationship carries with it certain duties that the broker must perform. The duties can be remembered by the word "POLAND:"

Personal performance (must have authorization for sub-agency) Obedience Loyalty Accountability Notice Due or reasonable care

7.7 | P a g e

Care

The broker, as an agent, must exercise a reasonable degree of care while transacting business entrusted to him by the principal. Remember, the broker is liable to the principal for any loss resulting from negligence or carelessness.

Obedience

The broker is at all times obligated to act in good faith and in conformity with his or her principal's instructions and authority. Again, a broker is liable for any losses incurred by the principal due to any acts the broker performs that are not within the scope of authority granted to him or her. The broker is not, however, required to obey unlawful or unethical instructions. The broker may disobey a principal or perform acts beyond his or her authority in an emergency situation as long as the broker's actions are in the principal's best interests.

The broker is obligated to present all offers to the seller. He/she is not authorized to decide which offers will or will not be seen by the principal. In addition, the broker, or salesperson, may not offer the property for sale for any price not authorized by the seller in writing.

Accounting

The broker must be able to report the status of all funds entrusted to him or her by the principal. Most states' real estate license laws require brokers to give accurate copies of all documents to all parties affected by them and to keep copies of such documents on file for a specified period of time. In addition, the license laws generally require the broker to promptly deposit all funds entrusted to him or her in a special trust, or escrow account; the laws make it illegal for the broker to commingle such money with personal funds. The broker may, however, use his or her own funds to open an escrow account.

Once funds have been placed in an escrow account they may only be removed under one of the following conditions:

Upon completion of the transaction With written consent of all the parties With a court order directing the disposition of the funds

7.8 | P a g e

Loyalty

Loyalty is a must -- the broker owes his or her employer the utmost in loyalty. An agent must always place a principal's interests above those of the other people with whom he or she is dealing. Thus, an agent cannot disclose such information as the principal's financial condition, the fact that the principal (if the seller) will accept a price lower than the listing price for his or her real estate, or any similar confidential

facts that might harm the principal's bargaining position.

All states forbid brokers or salespeople to buy property listed with them for their own accounts, or for accounts in which they have a personal interest, without first notifying the principal of such interest and receiving his or her consent. Likewise, by law neither brokers nor salespeople may sell property in which they have a personal interest without informing the purchaser of that interest.

Notice

There is the duty of notice of full disclosure. It is the broker's duty to keep the principal fully informed at all times of all facts or information the broker obtains that could affect the principal's business or decisions.

In certain instances, the broker may be held liable for damages for failure to disclose such information.

Agent Responsibilities to Third Parties

In dealing with a buyer, a broker, as an agent of the seller, must exercise extreme caution and be aware of the laws and ethical considerations that affect this relationship.

For example, brokers must be careful about the statements they or their staff members make about a parcel of real estate.

Statements of opinion are permissible as long as they are offered as opinions and without any intention to deceive. Making such statements when selling real estate is called puffing. Puffing is not

7.9 | P a g e

illegal, but is strongly discouraged. Statements of facts must be accurate. Brokers and salespeople must

be alert to ensure that none of their statements can in any way be interpreted as involving fraud. Fraud is the intentional misrepresentation of a material fact that harms or takes advantage of another person. In addition to false statements about a property, the concept of fraud covers intentional concealment or nondisclosure of important facts. If a contract to purchase real estate is obtained as a result of fraudulent statements made by a broker or his or her salespeople, the contract may be disaffirmed or renounced by the purchaser.

Brokers and salespeople should be aware that the courts have ruled that a seller is responsible for revealing to a buyer any hidden or latent defects in a building. A latent defect is one that is known to the seller but not to the buyer and that is not discoverable by ordinary inspection. As an agent of the seller, a broker is likewise responsible for disclosing known latent defects.

Advertising a property for sale "as is" does not relieve the seller and broker of this responsibility.

Principal's Obligations to Agent

A principal (typically the seller) has certain obligations to the agent.

First of all, the property owner must cooperate with the broker in the performance of their agreement.

It is not uncommon for the broker to pay expenses not related to the sale itself, such as minor repairs or lawn care, especially if the owner lives out of town. In these cases, the broker is entitled to a reimbursement from the owner. Obviously, good business practice dictates that the broker obtains written authorization before making such expenditures. Better still, the broker should arrange, whenever possible, for the owner to make payment directly to the person providing the service.

The principal is obligated for compensation when the agent performs. The amount of compensation an owner is obligated to pay

7.10 | P a g e

the broker is not set by the real estate board or by the local association of REALTORS®; it must always be negotiated between the owner and broker. If the owner feels the broker's fee is too high, he can list his property with someone who charges less or he can sell it himself. The broker must decide what fee he can accept that will make his time and effort in finding a buyer worthwhile.

Under no circumstances can brokers decide among themselves to set commission rates. Any attempt to agree on standard commission rates is considered price fixing.

An agent is entitled to indemnification and is to be held blameless for actions of the principal, such as a misrepresentation by the principal that was passed on in good faith to a buyer.

Listing Agreements

A listing agreement is really an employment contract that creates a special agency and whereby the property owner is hiring a broker to find a buyer who is ready, willing, and able. A buyer indicates he or she is ready and willing upon entering into a purchase agreement, and is able, upon being financially capable, which is usually evidenced by being approved for a loan.

When a broker has produced a ready, willing, and able buyer, he or she is said to be the procuring cause of the sale and is entitled to the commission.

A listing agreement does not authorize the broker to enter into a contract to sell the property, only to find a buyer. Neither does the listing agreement obligate the seller to sell.

There are a few types of listings in use:

Open Listing Exclusive Agency Listing Exclusive Right to Sell Listing Net Listing

7.11 | P a g e

Open Listing

Open listings may be either written or oral. They are also called general listings. An owner can give an open listing to as many brokers as he wishes, and at the same time, avoid paying a commission if he sells the property himself. The only way a broker holding an open listing is assured of earning a commission is if he finds a buyer who is ready, willing, and able to meet the seller's price and terms. Few brokers are willing to devote a lot of time and money attempting to sell a property on which they have this type of employment agreement with the seller.

An open listing need not contain a definite termination date. In such a case, the listing terminates after a reasonable period of time. In Virginia, 90 days is considered a reasonable period of time.

Note that oral listings, while not specifically illegal, are unenforceable under many state statutes of fraud.

Exclusive Agency Listing

Under an exclusive agency listing agreement, the seller authorizes only one broker to represent him in finding a buyer for his property. Even though this arrangement protects the broker from unwanted competition, the owner reserves the right to sell the property himself without being obligated to pay the broker a commission.

An exclusive agency listing must be a written agreement based on mutual consideration. In other words, the owner promises to pay the broker a commission if the property is sold by anyone other than himself. In return, the broker promises that he will use his best efforts in actively seeking a buyer. Because of these mutual promises, an exclusive agency listing is a bilateral contract. The agency relationship ends when the property is sold, or on the expiration date which must be stated in the agreement.

All exclusive listings must have definite termination dates.

7.12 | P a g e

Exclusive Right to Sell Listing

The most widely used type of listing agreement is the exclusive right to sell listing. It provides the broker with the most protection because he is assured of earning his commission regardless of who sells the property during the listing period.

While the owner does not reserve the right to sell his own property without being obligated to pay a commission, this type of employment contract can be to his advantage; the broker simply has more incentive. He promises to spend his best efforts in marketing the property because the seller promises to pay him a commission if it is sold, no matter who sells it. This mutual consideration makes an exclusive right to sell listing a bilateral contract. Also, it must be in writing and have a definite date of expiration.

The agency relationship will end on the expiration date if the property has not already sold.

Generally, most exclusive right to sell listings have a provision which extends the broker's protection period for three to four months after the listing expires. This provision, sometimes called a safety clause, only protects the broker in the event the seller sells to one of the prospects with whom he had negotiated during the listing term. The safety clause is sometimes called a protection clause.

Net Listing

A net listing is a listing agreement whereby the broker is authorized to sell the property for any price he can, while the seller agrees to accept a set amount.

A net listing agreement can be an open listing, exclusive agency listing, or an exclusive right-to-sell listing. With a net listing, ethical questions often arise. For instance, as an agent for the seller, does the broker not have the responsibility for getting him the highest possible price for his property? If the broker earns an unusually high rate of commission, was he not obligated to tell the seller what his home was actually worth? Because net listings allow the potential for unethical practice, they are prohibited in most states.

7.13 | P a g e

Multiple Listing Service (MLS)

A multiple listing service (MLS) is an organization made up of brokers who wish to exchange listing information. Its purpose is to give each listed property the widest market exposure possible, thereby increasing its chances of selling. A multiple listing is usually any exclusive right-to-sell listing that is submitted to MLS members. The seller lists his home with only one broker who assumes the primary responsibilities as his agent. The listing broker in turn, allows each member broker of the MLS to assist in making the sale. In this capacity, the selling broker is a subagent of the seller, and a subagency exists between the listing brokers and other brokers in the MLS.

Both the listing broker (agent) and the selling broker (subagent) share in the commission after a fee is paid to the MLS for the cost of operation.

Terminating Listing Agreements

Thankfully, most listing agreements are terminated through full performance, or accomplishing the purpose intended: finding a buyer.

If a buyer is not found, an exclusive listing will expire at midnight on the last day of its term.

Because a listing is basically an agency contract, it may be terminated by revocation prior to its expiration date. If it is revoked without just cause, the broker may recover damages. Even though it was revoked, the seller may still be responsible for the commission if it was revoked for the purpose of avoiding a commission and the property is sold during the remaining term of the listing.

A listing may also be terminated by:

Mutual agreement Death or incapacity of either party (does not terminate a purchase

agreement) Destruction or condemnation of the property Bankruptcy Foreclosure Abandonment by the broker.

7.14 | P a g e

Buyer Agency Agreements

In an exclusive buyer agency agreement the buyer is legally responsible to compensate the agent if the buyer purchases a property of the type described in the contract regardless of whether the agent located the property.

In an exclusive-agency buyer agency agreement the buyer is not obligated to pay the broker if the buyer locates a property on his own.

An open buyer agency agreement permits the buyer to enter into agreement with an unlimited number of brokers. The buyer is obligated to compensate only the broker who locates a property that the buyer purchases.

In any agency relationship, the source of compensation is not the factor that determines the agency relationship. Compensation of the agent is always negotiable

Choosing Helpers

If you, as an agent, hire someone to look into a question, make certain you hire someone who is professionally qualified.

In the following case the broker listed a house and in due course found a buyer for it:

The sale was contingent on getting an inspection and approval of the plumbing, furnace, air conditioning, and roof. The buyer asked the broker for someone who could do this, and the broker hired someone used occasionally to make minor inspections. The inspection was made, the items reported to be in good order and the closing took place.

Upon moving in, the buyer found the house lacked water pressure because the pipes were corroded. This was confirmed by the city water department. The buyer had the pipes replaced and sent the broker the bill for $2,200. The broker felt no liability and did not pay. The buyer then sued the broker.

7.15 | P a g e

At the trial, the buyer introduced evidence that the broker had assured the buyer that the broker would have a man check the plumbing and other items. At the trial, the man who made the inspection stated he inspected the house but did not check the water pressure. The court found the broker negligent: The broker should have known to hire a competent plumber, not a handyman.

In deciding for the buyer, the judge expressed the opinion that a real estate agent, like a doctor or lawyer, holds himself/herself out to be an expert in his/her field.

Anti-Trust Laws-Sherman Anti-Trust Act

The real estate industry is subject to federal and state antitrust laws.

Generally, these laws prohibit monopolies and contracts, combinations, and conspiracies that unreasonably restrain trade.

The most frequent of the antitrust violations that can occur in the real estate business are price fixing and allocation of customers or markets.

Illegal price fixing occurs when brokers conspire to set prices for the services they perform (sales commissions, management rates) rather than let those prices be established through competition in the open market.

Allocation of customers or markets involves an agreement between brokers to divide their markets and refrain from competing for each other's business. Allocations may take place on a geographic basis, with brokers agreeing to specific territories within which they will operate exclusively.

The division may also take place along other lines; for example, two brokers may agree that one will handle only residential properties under $100,000 in value, while another will handle residential properties over $100,000 in value.

Violation of the anti-trust act is punishable by a maximum $100,000 fine and three years in prison. For corporations, the fine may be up to $1 million.

7.16 | P a g e

Civil Rights Act of 1866

The efforts of the federal government to guarantee equal housing opportunities to all U.S. citizens began over 100 years ago with the passage of the Civil Rights Act of 1866. This law, an outgrowth of the Fourteenth Amendment, prohibits any type of discrimination based on race.

The act states, in part:

"All citizens of the United States shall have the same right in every state and territory as is enjoyed by white citizens thereof to inherit, purchase, lease, sell, hold, and convey real and personal property."

Fair Housing Act of 1968

In 1968, two major events occurred that greatly encouraged the progress of fair housing. The first of these was the passage of the federal Fair Housing Act, which is contained in Title VIII of the Civil Rights Act of 1968.

This law provides that it is unlawful to discriminate on the basis of race, color, religion, sex, or national origin when selling or leasing residential property. It covers dwellings and apartments, as well as vacant land acquired for the construction of residential buildings.

The Fair Housing Act also requires that each brokerage office display an Equal Housing Opportunity poster in a conspicuous place.

Exemptions to the Federal Fair Housing Act of 1968 are also provided. They include:

The sale or rental of a single-family home when the home is owned by an individual who does not own more than three such homes at one time and when the following conditions exist:

o A broker, salesperson, or agent is not used and o Discriminatory advertising is not used. o If the owner is not living in the dwelling at the time of the

transaction or was not the most recent occupant, only one such sale by an individual is exempt from the law within any 24-month period.

The rental of rooms or units in an owner-occupied one-to-four-family dwelling, and the owner lives in one of the units.

7.17 | P a g e

Dwelling units owned by religious organizations may be restricted to people of the same religion if membership in the organization is not restricted on the basis of race, color, or national origin. The dwelling must be non-commercial.

A private club that is not open to the public may restrict the rental or occupancy of lodgings that it owns to its members, as long as the lodgings are not operated commercially.

While the 1968 federal law exempts individual homeowners and certain groups, the 1866 law prohibits all racial discrimination without exception. So, despite any exemptions in the 1968 law, an aggrieved person may seek a remedy for racial discrimination under the 1866 law against any homeowner, regardless of whether the owner employed a real estate broker and/or advertised the property.

A 1972 amendment to the federal Fair Housing Act of 1968 instituted the use of the equal housing opportunity poster. This poster, which can be obtained from HUD, features the equal housing opportunity slogan, an equal housing statement pledging adherence to the Fair Housing Act, support of affirmative marketing and advertising programs, and the equal housing opportunity logo. When HUD investigates a broker for discriminatory practices, it considers failure to display the poster evidence of discrimination.

Fair Housing: Blockbusting, Steering and Redlining

Blockbusting and steering are undesirable housing practices frequently discussed in connection with fair housing.

It is a common misconception that blockbusting is the purchase of a home in a homogeneous neighborhood by a member of a minority group. In fact, blockbusting, called panic selling, means inducing homeowners to sell by making representations regarding the entry or prospective entry of minorities into the neighborhood. The blockbuster frightens homeowners into selling, and makes a profit by buying the homes cheaply and selling them at considerably higher prices to minority individuals.

Steering is the channeling of homeseekers to particular areas, either to maintain the homogeneity of an area or to change the

7.18 | P a g e

character of an area in order to create a speculative situation. This practice makes certain homes unavailable to homeseekers on the basis of race, national origin, gender, religion, familial status or handicap.

The practice of refusing to make mortgage loans due to the age of the neighborhood or its ethnic composition without regard to the economic qualifications of the applicant is known as redlining. This practice, which often contributes to the deterioration of older, transitional neighborhoods, is frequently based on racial grounds rather than on any real objections to the applicant. It is important to note that a lending institution that refuses a loan solely on sound economic grounds cannot be accused of redlining.

The Federal Fair Housing Act is administered by the Office of Equal Opportunity under the direction of the Secretary of the Department of Housing and Urban Development. Any aggrieved person may file a complaint with the secretary or his or her delegate within 360 days after a discriminatory action occurs. Complaints may be reported to: Fair Housing, Department of Housing and Urban Development, Washington DC 20410, or to Fair Housing c/o the nearest HUD regional office.

The penalty for a first violation is $10,000. A second violation within five years would carry a fine of $25,000, while a third violation within seven years could result in a fine of $50,000.

The Department of Justice may itself initiate a suit in which case the penalty would be $50,000 and $100,000 for repeat violations.

Fair Housing Amendments of 1988

The Fair Housing Amendments Act of 1988 came into effect on March 12, 1989. Its purpose is to expand the scope of federal regulations to protect handicapped individuals and familial status of individuals.

The amendments define handicap consistently with existing federal and state laws. A handicapped person is one who has a physical or mental impairment which substantially limits one or more major life activities.

The law requires that covered multi-family dwellings be accessible and designed to be adaptable for handicapped residents. The adaptable design requirements did not affect pre-existing structures or any ready for occupancy within 30 months of enactment of the 1988 amendments. With

7.19 | P a g e

respect to all multi-family housing available for occupancy after this transition period, however, the design requirements are imposed.

Covered multi-family dwellings are defined to mean:

Buildings of four or more units with elevators Buildings of four or more ground-floor units in other, non-elevator

buildings.

The bill does not require the installation of elevators or the renovation of existing units. It does require that:

Doors and hallways be wide enough to accommodate wheelchairs Switches and other environmental controls be in convenient locations Most rooms and spaces be on an accessible route Kitchen and bathrooms permit a wheelchair to maneuver in them Disabled individuals be allowed to easily make additional

accommodations if needed -- such as installing grab-bars in the bathroom -- without major renovation or structural change. The law required developers to incorporate these adaptations into the design of new buildings.

The principles of adaptable design require that the public and common-use portions of multi-family dwellings be readily accessible to and usable by handicapped individuals. Hallways, lounges, lobbies, passageways among and between buildings, and other common areas and facilities must not contain barriers to entrance and use by those with handicaps. There is no requirement that all entrances be made accessible to handicapped individuals for the same purpose for which it is used by others. Amenities, such as laundry rooms or public bathrooms need not be installed, but if such amenities are provided, they must be readily accessible to and usable by those with handicaps.

The amendments also made it illegal to deny permission to tenants with disabilities to make reasonable modifications of existing premises, at their own expense, if the modifications are necessary for their full enjoyment of the premises. Examples of such modifications might be:

Installation of a lever doorknob or grab-bars in the bathroom Individuals who have a hearing disability could install a flashing light in

order to indicate that someone is ringing the doorbell

7.20 | P a g e

A person in a wheelchair may need to install fold-back hinges in order to be able to go through a door, or may need to build a ramp to enter the unit.

In requiring that landlords allow reasonable modifications by handicapped individuals, the law imposes the costs of both installing the modification as well as returning the premises to their original condition upon the individual requesting permission to make the modification. Reasonable accommodations in rules, policies, practices, or services must also be allowed if necessary to give a person with handicaps equal opportunity to use and enjoy a dwelling.

The law specifically states that it shall not be considered handicap discrimination to deny a dwelling to an individual whose tenancy would constitute a direct threat to the health or safety of other individuals.

The amendments also make clear that current illegal users of or addicts to controlled substances, as defined by the Controlled Substances Act, are not considered to be handicapped under the Fair Housing Act. However, individuals who have a record of drug use or addiction, but who do not currently use illegal drugs would continue to be protected if they fell under the definition of handicap.

Discrimination against families with children under age 18 is prohibited under the 1988 Amendments. This protection extends to expectant parents as well as those in the process of adopting a child.

The restrictions on familial status discrimination permit an exemption for communities intended for older people. Housing for older people is defined by Arent, Fox, Kintner, Plotkin & Kahn.

Arent, Fox, Kintner, Plotkin and Kahn

Arent, Fox, Kintner, Plotkin & Kahn defines housing intended for older people through two tests:

The first test is a simple standard: The community must be provided for the elderly by state or federal agencies or be intended for and occupied solely by people 62 years of age or older. This limitation would not exclude temporary visitors or necessary resident employees such as medical staff or maintenance personnel.

7.21 | P a g e

The second test requires that the community be intended to provide housing for those 55 or older, eighty percent of the units must be occupied by at least one person 55 or older, and there must be policies, procedures, and significant facilities and services specifically designed to meet the physical or social needs of the older residents. Those amenities include items such as dining facilities, social programs, health care, education, counseling, and transportation. The requirement for facilities and services would not be met by providing minor amenities, such as putting a couch in a laundry room and labeling it a recreation center, or installing a ramp at the front entrance. A grandfather provision of the amendments ensures that an elderly housing community will not be found out of compliance with these requirements because of tenants under the age of 55 who lived there before enactment of the law.

In addition to the procedures for a hearing before an administrative law judge or civil litigation filed by the attorney general, the 1988 amendments also permit enforcement by a civil action filed by an aggrieved person on his own behalf. The statute of limitations for such actions is extended from 180 days to one year. This time period does not include any time during which administrative proceedings may be pending. The law requires the cessation of the administrative proceedings at the commencement of a civil trial in district court. While an aggrieved person is not required to exhaust administrative remedies before a civil action, if an administrative hearing has commenced, the charging party may not commence a civil action.

In Review

An agency is created when one person delegates to another person the right to act on his or her behalf in dealing with third parties.

The three levels of agency are: universal, special and general

Agencies can be created through written agreement, by ratification, by coupling it with an interest, and through creating a dual agency

Agencies may be terminated by being completed, by expiration, by mutual agreement, or by revocation.

Among other things, a broker owes his or her principal personal

7.22 | P a g e

performance, obedience, loyalty, accountability, notice and due or reasonable care

Principals owe brokers cooperation, compensation and indemnification Listing agreements include: open listing, exclusive agency listing,

exclusive right to sell listing, and net listing The real estate industry is subject to federal and state antitrust and fair

housing laws.