Embed Size (px)

Citation preview

Chapter 8 Performance Management

and Evaluation

Fall 2007

Crosson

Use only with permission of Susan Crosson

Learning Objectives:

Management Responsibility, Accountability, and PerformanceResponsibility centers and performance measuresEnd-to-end accountability with the balanced scorecardLinking executive compensation and performance

Use only with permission of Susan Crosson

Responsibility, Accountability, and Performance

Responsibility accounting:An information system that classifies data according to areas of responsibility and reports each area’s activities by including only the revenues, cost, and resource categories that the assigned manager can control.Organizational chart: Line and staff relationships Responsibility centers-5 kinds

Use only with permission of Susan Crosson

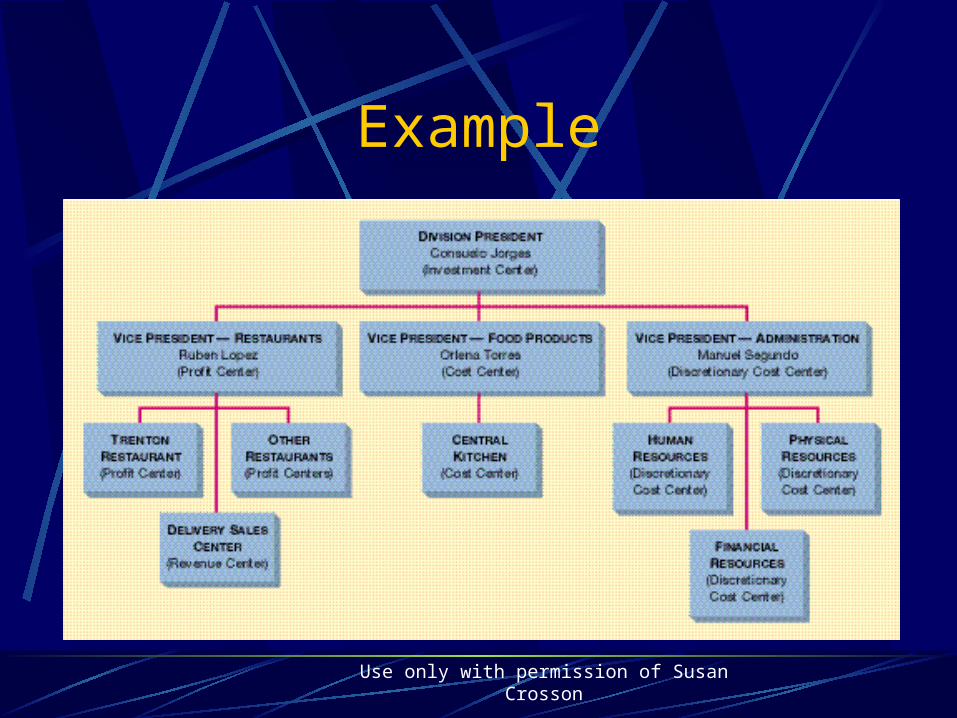

Example

Use only with permission of Susan Crosson

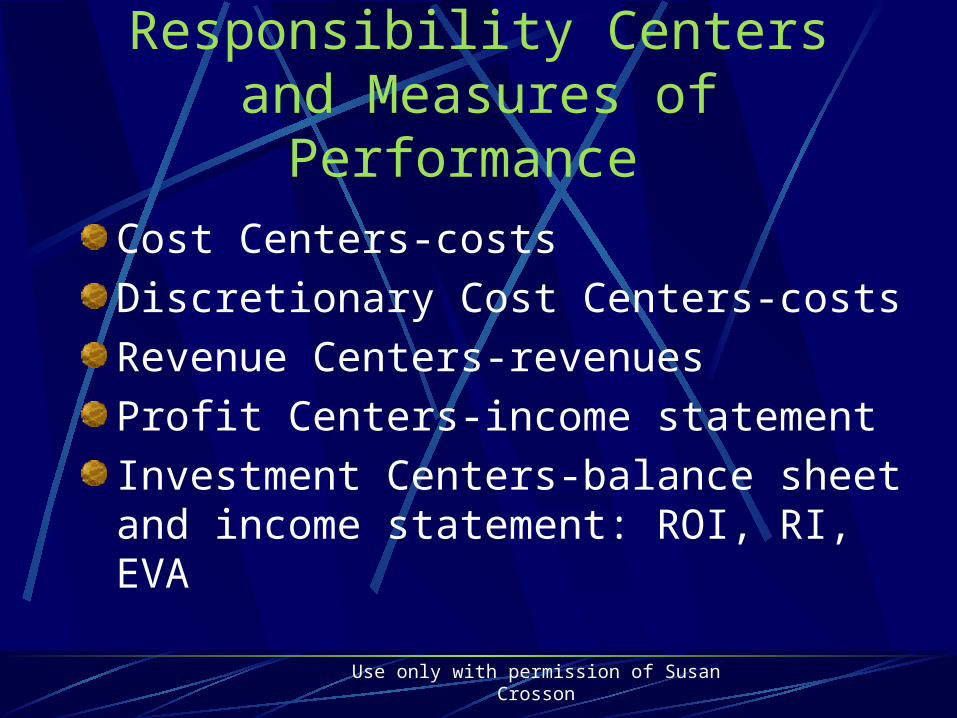

Responsibility Centers and Measures of Performance

Cost Centers-costs

Discretionary Cost Centers-costs

Revenue Centers-revenues

Profit Centers-income statement

Investment Centers-balance sheet and income statement: ROI, RI, EVA

Use only with permission of Susan Crosson

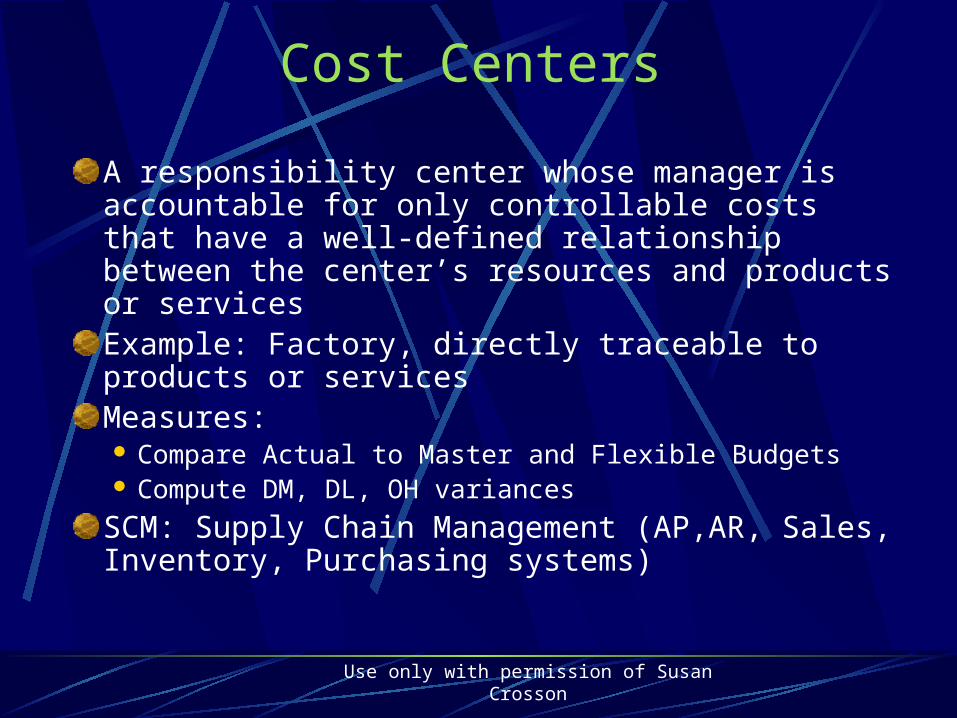

Cost Centers

A responsibility center whose manager is accountable for only controllable costs that have a well-defined relationship between the center’s resources and products or servicesExample: Factory, directly traceable to products or servicesMeasures: Compare Actual to Master and Flexible Budgets Compute DM, DL, OH variances

SCM: Supply Chain Management (AP,AR, Sales, Inventory, Purchasing systems)

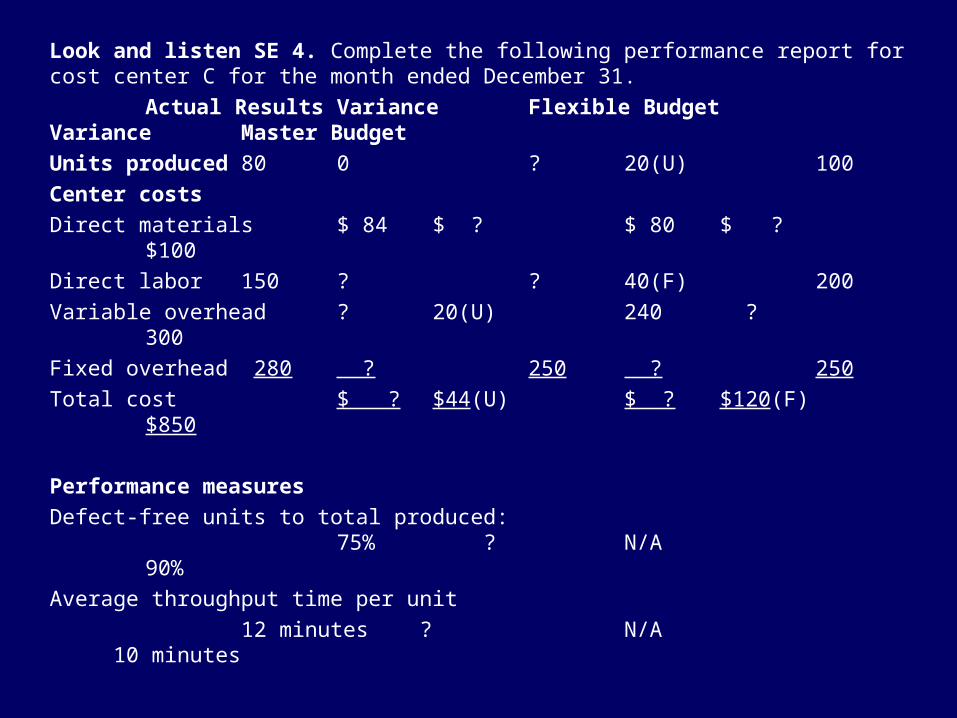

Look and listen SE 4. Complete the following performance report for cost center C for the month ended December 31.

Actual Results Variance Flexible Budget Variance Master Budget

Units produced 80 0 ? 20(U) 100

Center costs

Direct materials $ 84 $ ? $ 80 $ ? $100

Direct labor 150 ? ? 40(F) 200

Variable overhead ? 20(U) 240 ? 300

Fixed overhead 280 ? 250 ? 250

Total cost $ ? $44(U) $ ? $120(F) $850

Performance measures

Defect-free units to total produced:75% ? N/A 90%

Average throughput time per unit

12 minutes ? N/A 10 minutes

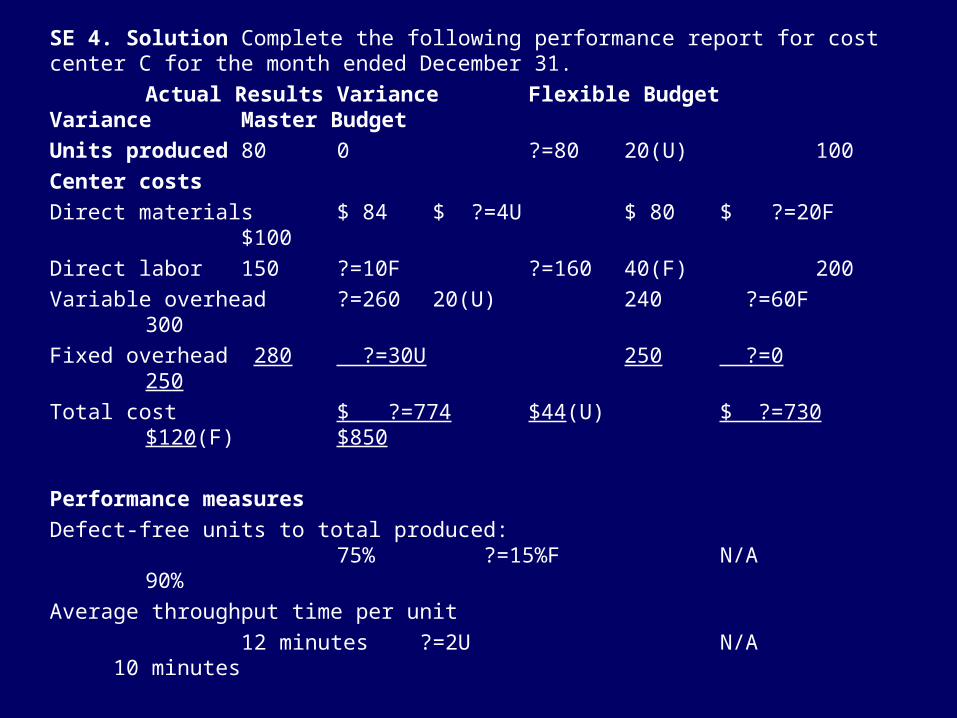

SE 4. Solution Complete the following performance report for cost center C for the month ended December 31.

Actual Results Variance Flexible Budget Variance Master Budget

Units produced 80 0 ?=80 20(U) 100

Center costs

Direct materials $ 84 $ ?=4U $ 80 $ ?=20F $100

Direct labor 150 ?=10F ?=160 40(F) 200

Variable overhead ?=260 20(U) 240 ?=60F 300

Fixed overhead 280 ?=30U 250 ?=0 250

Total cost $ ?=774 $44(U) $ ?=730 $120(F) $850

Performance measures

Defect-free units to total produced:75% ?=15%F N/A 90%

Average throughput time per unit

12 minutes ?=2U N/A 10 minutes

Use only with permission of Susan Crosson

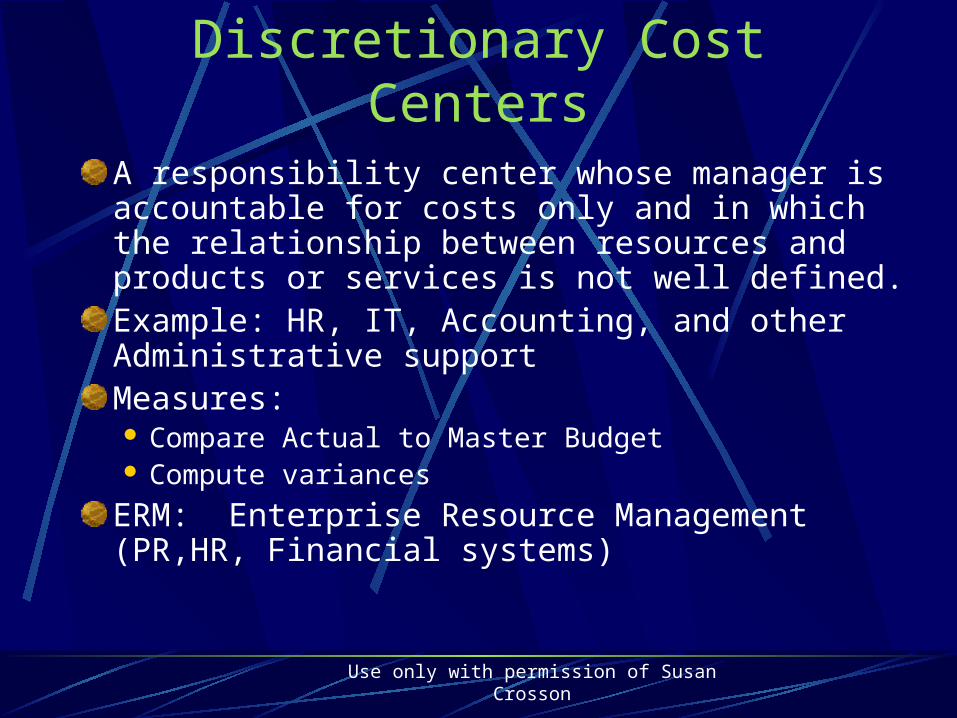

Discretionary Cost Centers

A responsibility center whose manager is accountable for costs only and in which the relationship between resources and products or services is not well defined.Example: HR, IT, Accounting, and other Administrative supportMeasures: Compare Actual to Master Budget Compute variances

ERM: Enterprise Resource Management (PR,HR, Financial systems)

Use only with permission of Susan Crosson

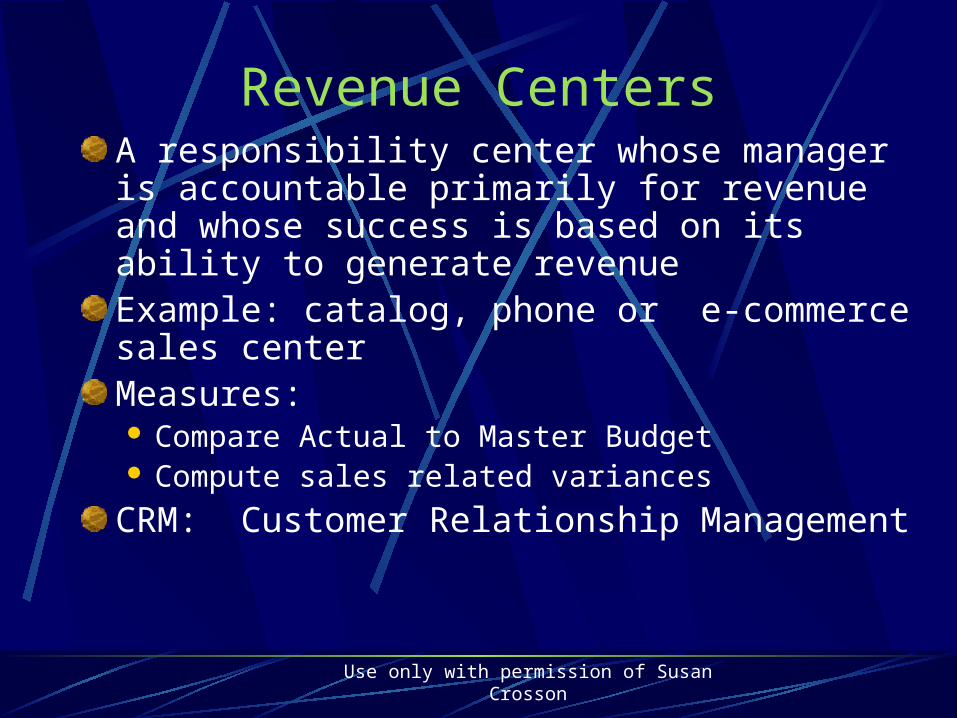

Revenue CentersA responsibility center whose manager is accountable primarily for revenue and whose success is based on its ability to generate revenueExample: catalog, phone or e-commerce sales center Measures: Compare Actual to Master Budget Compute sales related variances

CRM: Customer Relationship Management

Use only with permission of Susan Crosson

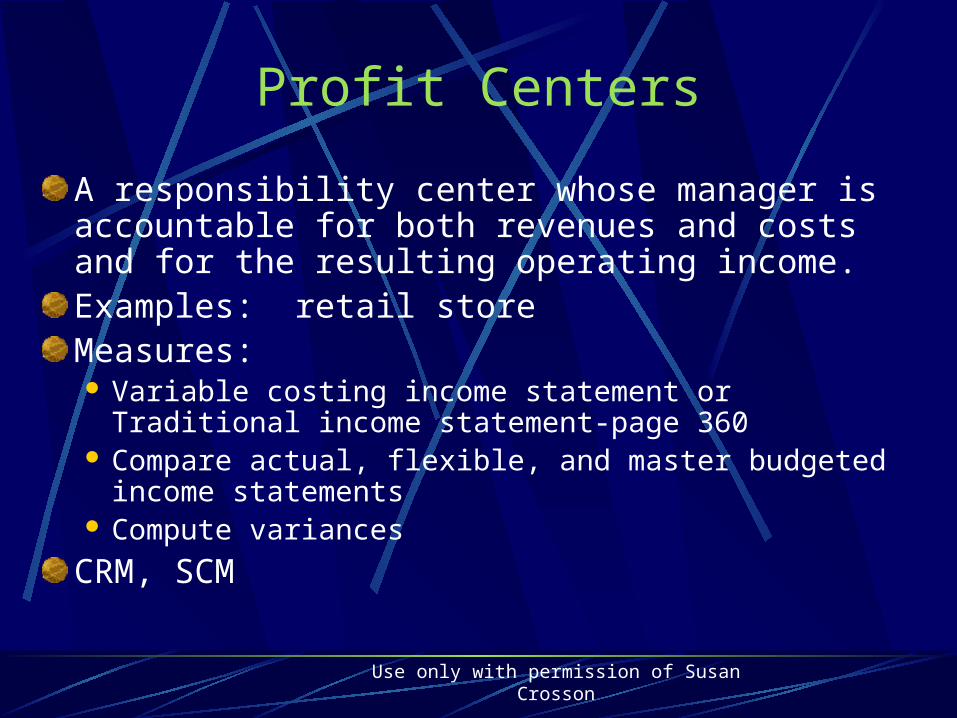

Profit Centers

A responsibility center whose manager is accountable for both revenues and costs and for the resulting operating income.Examples: retail store Measures: Variable costing income statement or Traditional income

statement-page 360 Compare actual, flexible, and master budgeted income

statements Compute variances

CRM, SCM

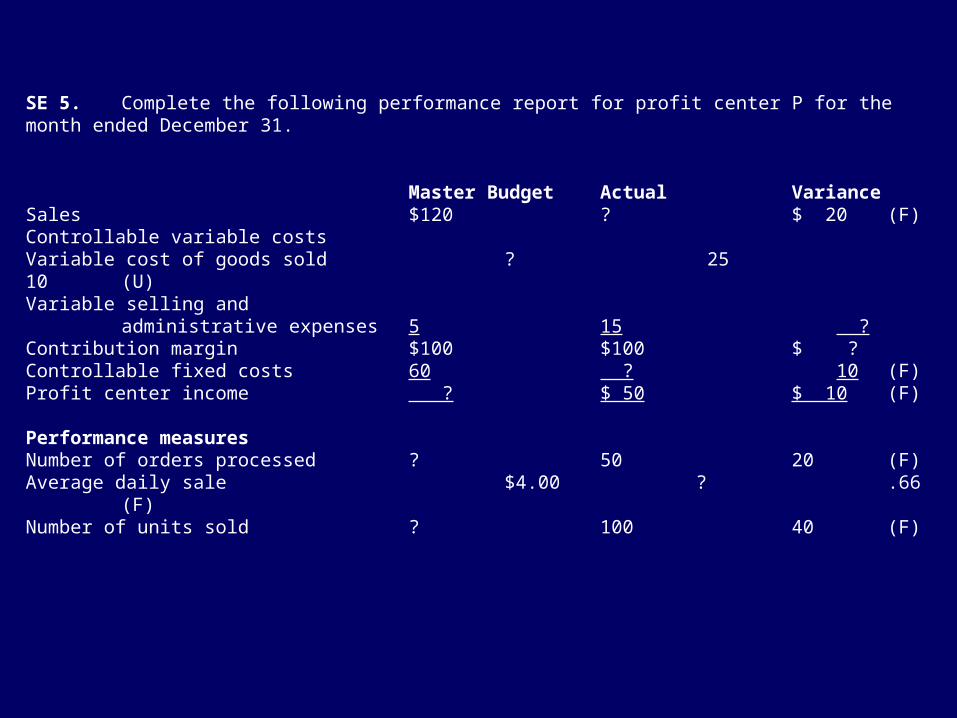

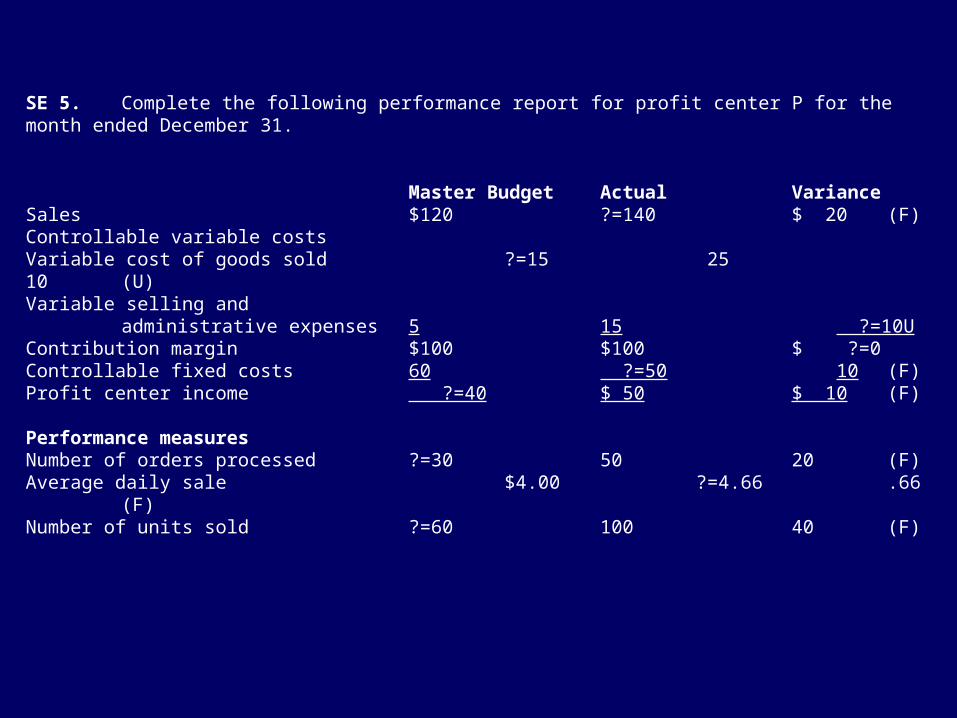

SE 5. Complete the following performance report for profit center P for the month ended December 31.

Master Budget Actual VarianceSales $120 ? $ 20 (F)Controllable variable costsVariable cost of goods sold ? 25 10 (U)Variable selling and

administrative expenses 5 15 ?Contribution margin $100 $100 $ ?Controllable fixed costs 60 ? 10 (F)Profit center income ? $ 50 $ 10 (F) Performance measuresNumber of orders processed ? 50 20 (F)Average daily sale $4.00 ? .66 (F)Number of units sold ? 100 40 (F)

SE 5. Complete the following performance report for profit center P for the month ended December 31.

Master Budget Actual VarianceSales $120 ?=140 $ 20 (F)Controllable variable costsVariable cost of goods sold ?=15 25 10 (U)Variable selling and

administrative expenses 5 15 ?=10UContribution margin $100 $100 $ ?=0Controllable fixed costs 60 ?=50 10 (F)Profit center income ?=40 $ 50 $ 10 (F) Performance measuresNumber of orders processed ?=30 50 20 (F)Average daily sale $4.00 ?=4.66 .66 (F)Number of units sold ?=60 100 40 (F)

Use only with permission of Susan Crosson

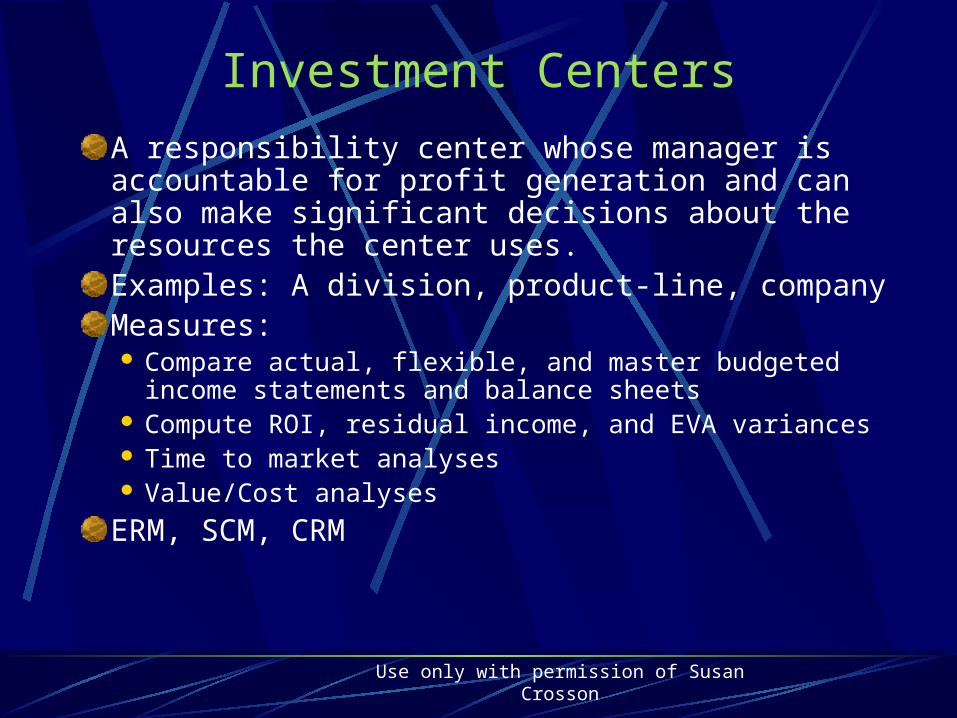

Investment Centers

A responsibility center whose manager is accountable for profit generation and can also make significant decisions about the resources the center uses.Examples: A division, product-line, companyMeasures: Compare actual, flexible, and master budgeted income

statements and balance sheets Compute ROI, residual income, and EVA variances Time to market analyses Value/Cost analyses

ERM, SCM, CRM

Use only with permission of Susan Crosson

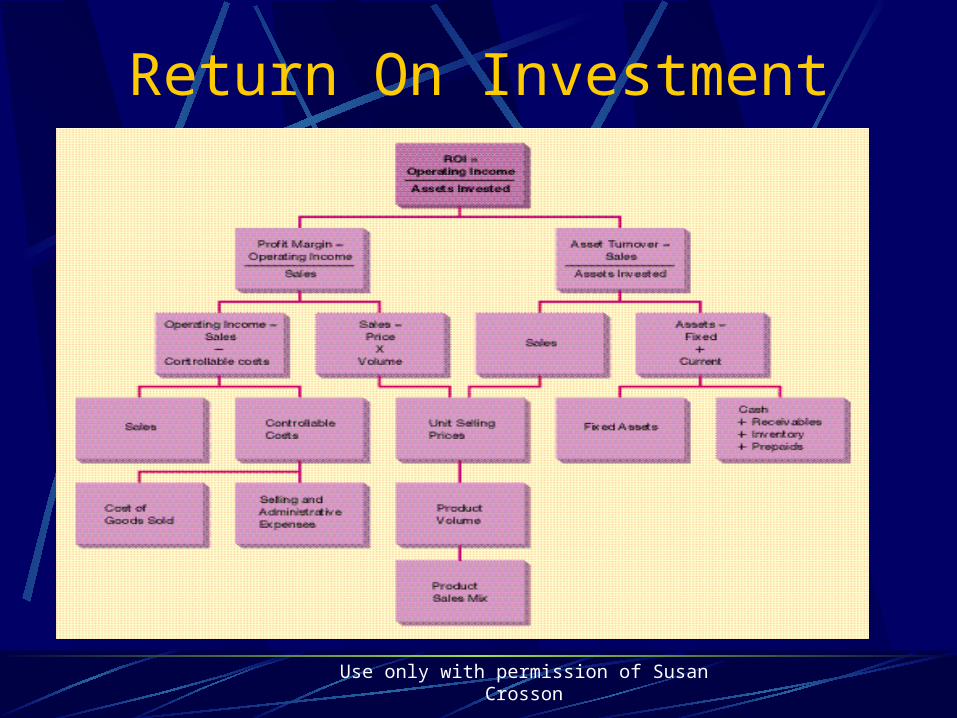

Return On Investment

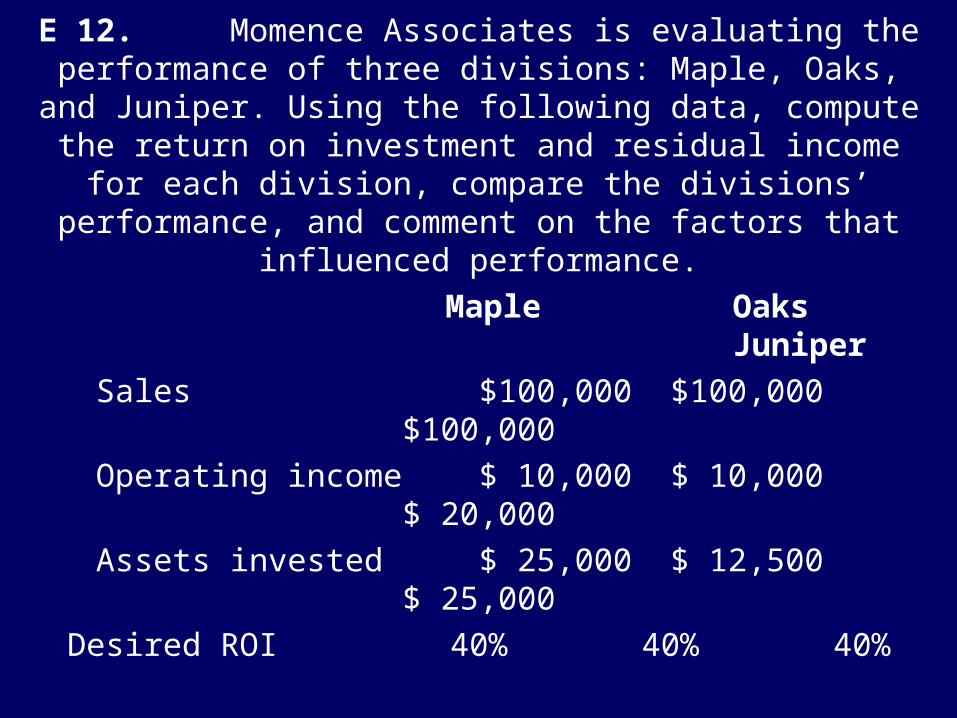

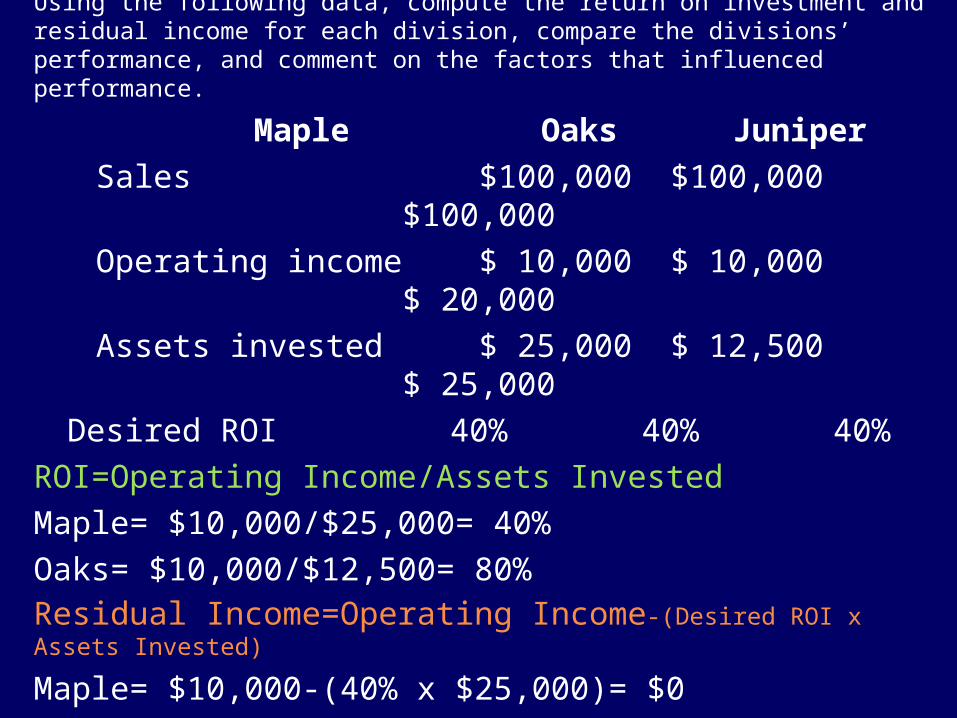

E 12. Momence Associates is evaluating the performance of three divisions: Maple, Oaks, and Juniper. Using the following data, compute the return on investment and residual income for each division, compare the divisions’ performance, and

comment on the factors that influenced performance.

Maple Oaks Juniper

Sales $100,000 $100,000 $100,000

Operating income $ 10,000 $ 10,000 $ 20,000

Assets invested $ 25,000 $ 12,500 $ 25,000

Desired ROI 40% 40% 40%

E 12. Solution Momence Associates is evaluating the performance of three divisions: Maple, Oaks, and Juniper. Using the following data, compute the return on investment and residual income for each division, compare the divisions’ performance, and comment on the factors that influenced performance.

Maple Oaks Juniper

Sales $100,000 $100,000 $100,000

Operating income $ 10,000 $ 10,000 $ 20,000

Assets invested $ 25,000 $ 12,500 $ 25,000

Desired ROI 40% 40% 40%

ROI=Operating Income/Assets Invested

Maple= $10,000/$25,000= 40%

Oaks= $10,000/$12,500= 80% Residual Income=Operating Income-(Desired ROI x Assets Invested)

Maple= $10,000-(40% x $25,000)= $0

Oaks= $10,000-(40% x $12,500)= $5,000

Use only with permission of Susan Crosson

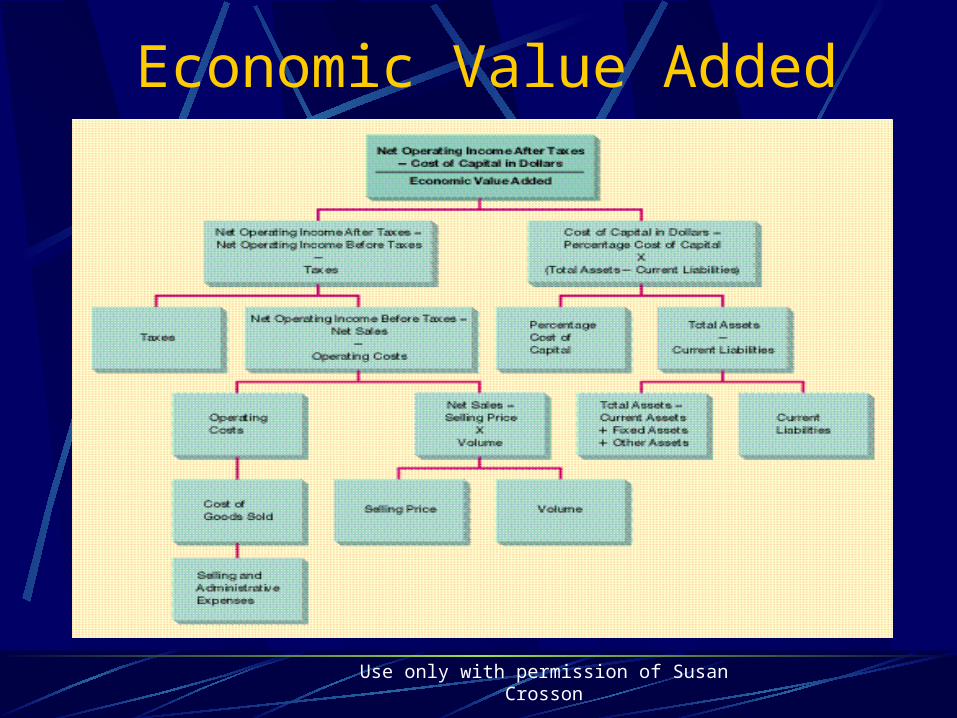

Economic Value Added

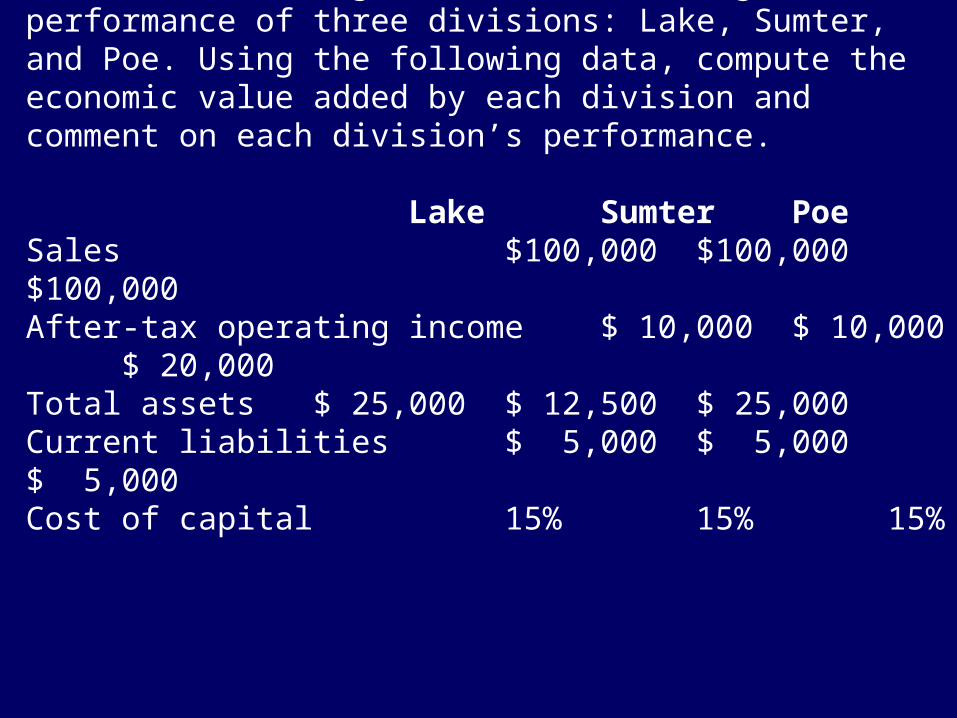

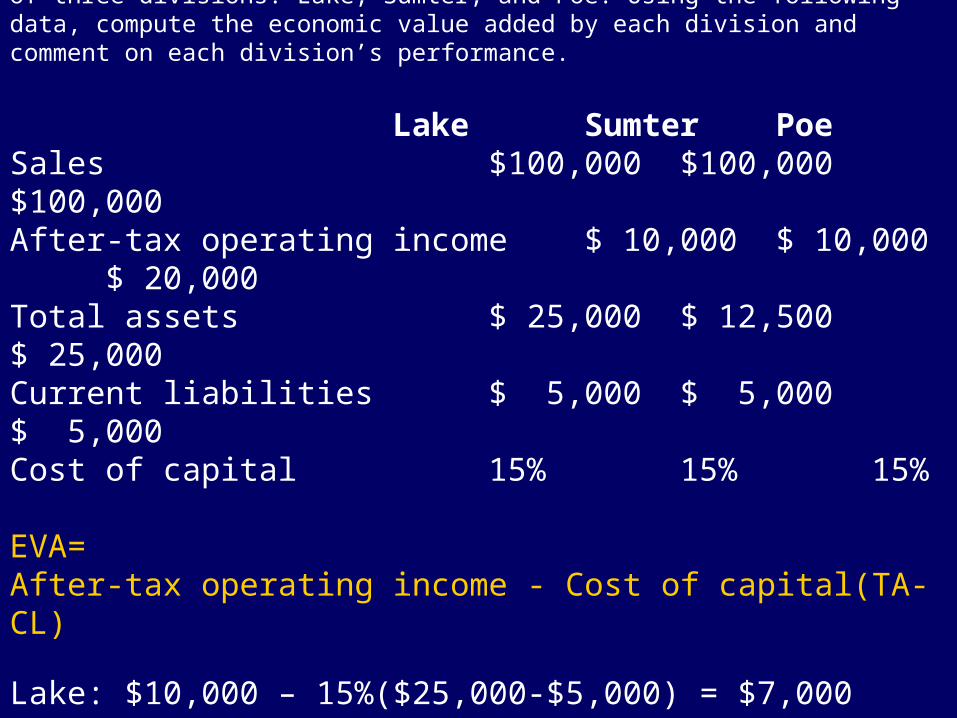

E 13. Leesburg, LLP, is evaluating the performance of three divisions: Lake, Sumter, and Poe. Using the following data, compute the economic value added by each division and comment on each division’s performance.

Lake Sumter PoeSales $100,000 $100,000 $100,000After-tax operating income $ 10,000 $ 10,000 $ 20,000Total assets $ 25,000 $ 12,500 $ 25,000Current liabilities $ 5,000 $ 5,000 $ 5,000Cost of capital 15% 15% 15%

E 13. Solution Leesburg, LLP, is evaluating the performance of three divisions: Lake, Sumter, and Poe. Using the following data, compute the economic value added by each division and comment on each division’s performance.

Lake Sumter PoeSales $100,000 $100,000 $100,000After-tax operating income $ 10,000 $ 10,000 $ 20,000Total assets $ 25,000 $ 12,500 $ 25,000Current liabilities $ 5,000 $ 5,000 $ 5,000Cost of capital 15% 15% 15%

EVA= After-tax operating income - Cost of capital(TA-CL)

Lake: $10,000 – 15%($25,000-$5,000) = $7,000Sumter: $10,000 – 15%($12,500-$5,000) = $8,875

Use only with permission of Susan Crosson

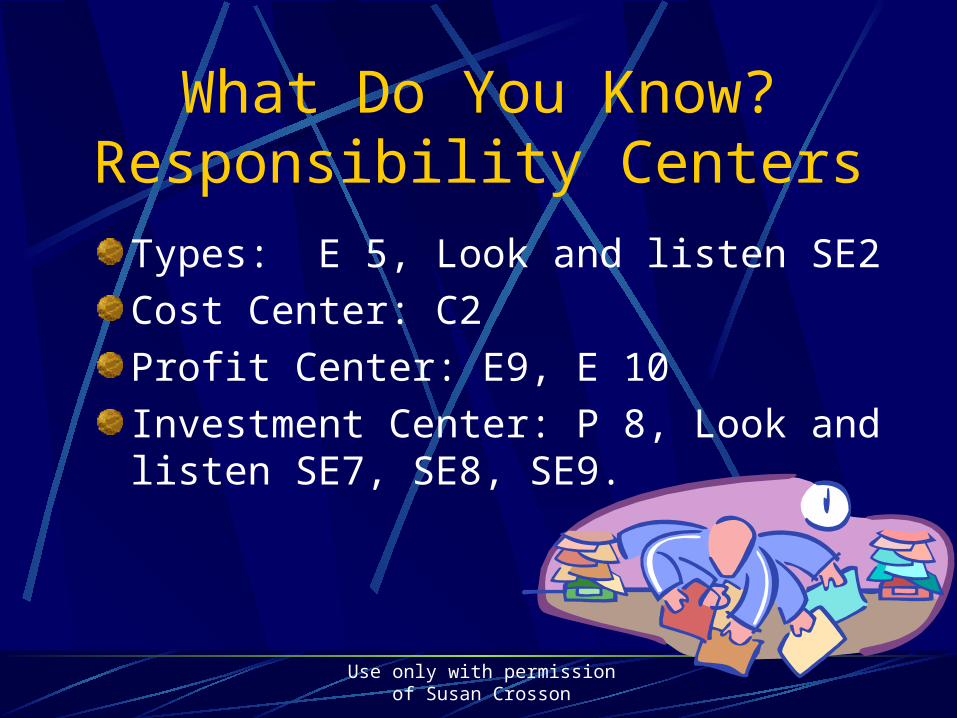

What Do You Know?Responsibility Centers

Types: E 5, Look and listen SE2

Cost Center: C2

Profit Center: E9, E 10

Investment Center: P 8, Look and listen SE7, SE8, SE9.

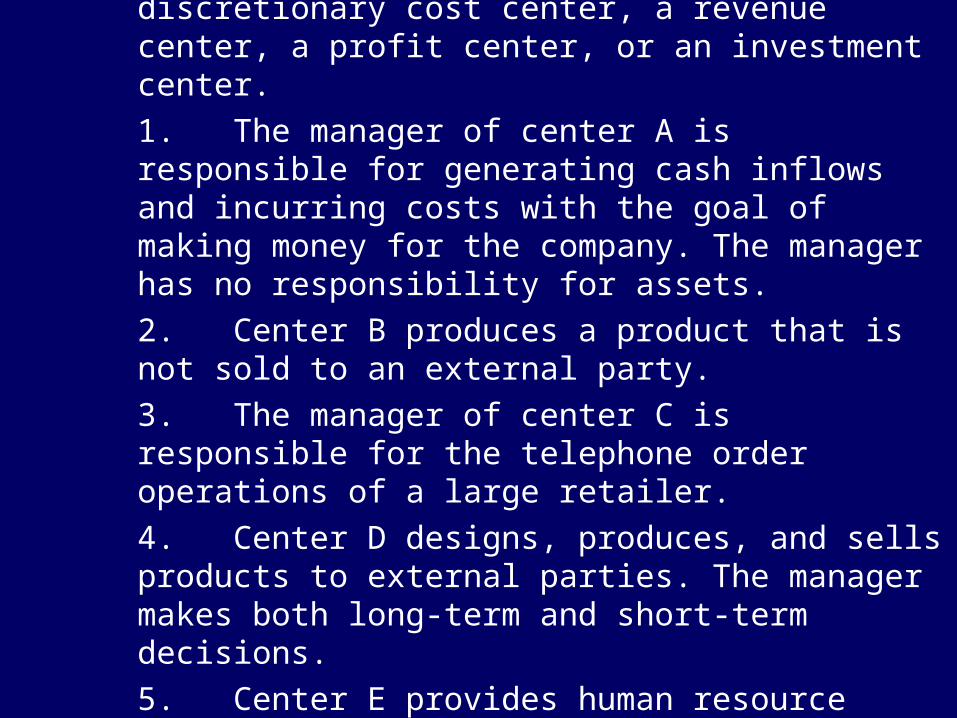

Look and listen SE 2. Identify each of the following as a cost center, a discretionary cost center, a revenue center, a profit center, or an investment center.

1. The manager of center A is responsible for generating cash inflows and incurring costs with the goal of making money for the company. The manager has no responsibility for assets.

2. Center B produces a product that is not sold to an external party.

3. The manager of center C is responsible for the telephone order operations of a large retailer.

4. Center D designs, produces, and sells products to external parties. The manager makes both long-term and short-term decisions.

5. Center E provides human resource support for the other centers in the company.

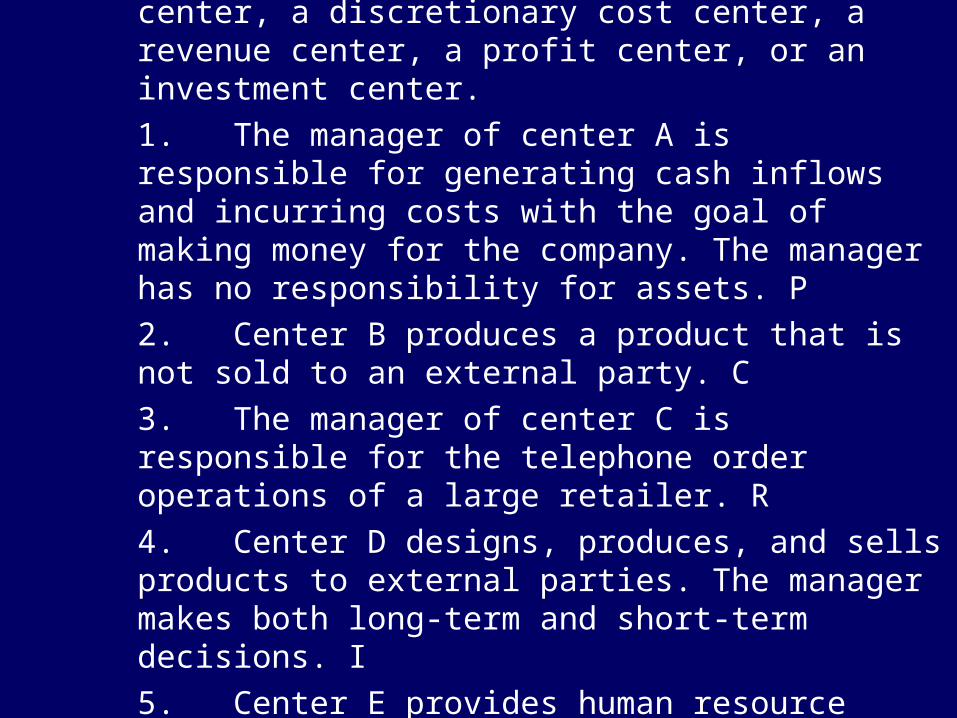

SE 2.Solution

Identify each of the following as a cost center, a discretionary cost center, a revenue center, a profit center, or an investment center.

1. The manager of center A is responsible for generating cash inflows and incurring costs with the goal of making money for the company. The manager has no responsibility for assets. P

2. Center B produces a product that is not sold to an external party. C

3. The manager of center C is responsible for the telephone order operations of a large retailer. R

4. Center D designs, produces, and sells products to external parties. The manager makes both long-term and short-term decisions. I

5. Center E provides human resource support for the other centers in the company. DC

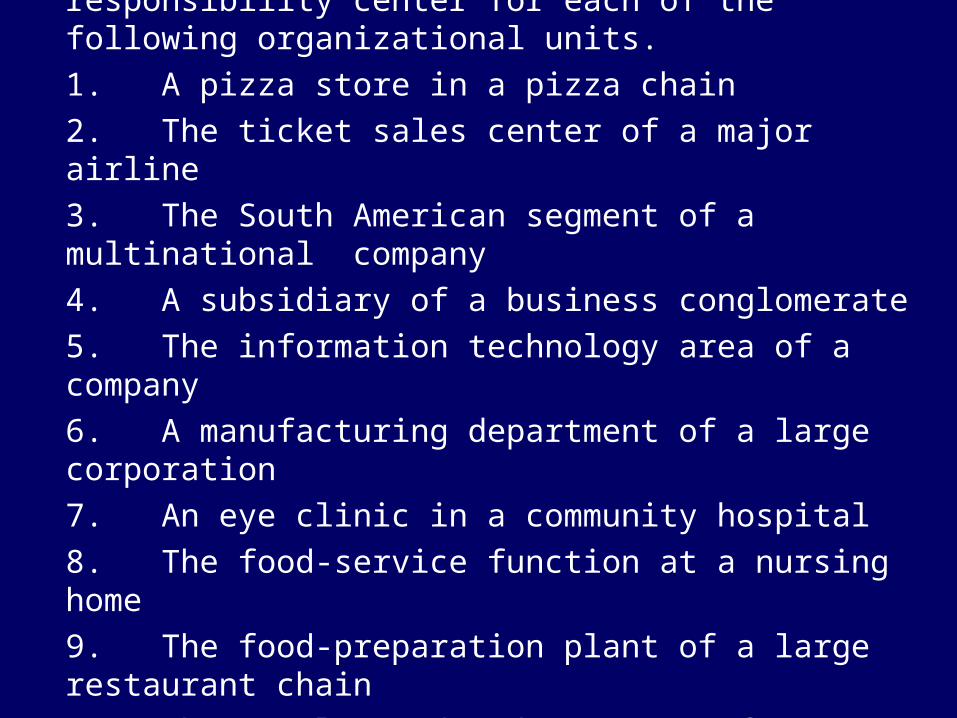

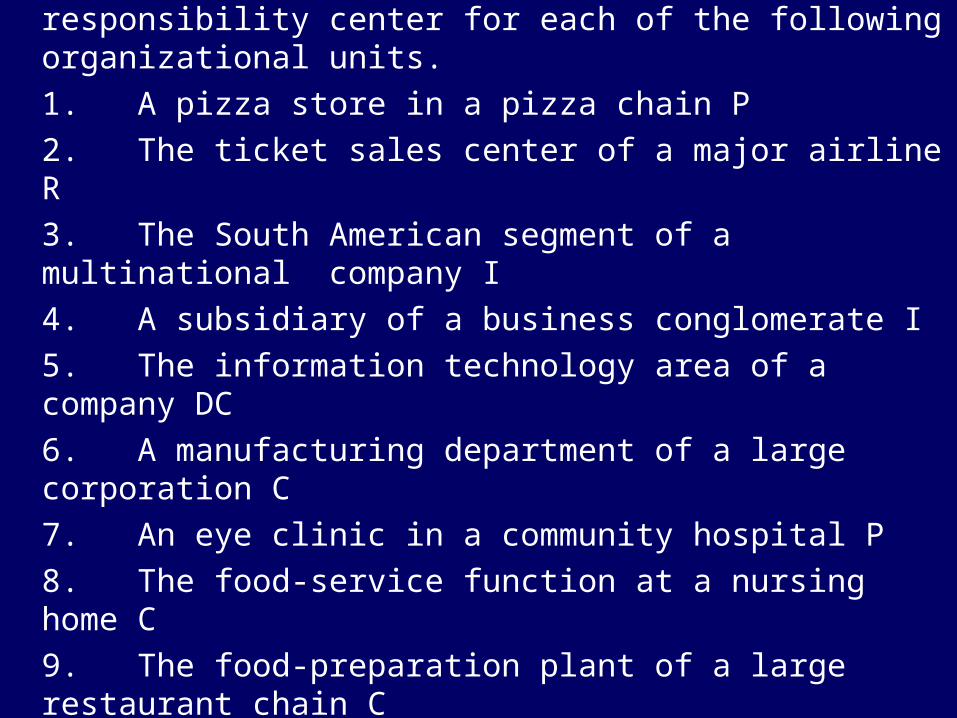

E 5. Identify the most appropriate type of responsibility center for each of the following organizational units.

1. A pizza store in a pizza chain

2. The ticket sales center of a major airline

3. The South American segment of a multinational company

4. A subsidiary of a business conglomerate

5. The information technology area of a company

6. A manufacturing department of a large corporation

7. An eye clinic in a community hospital

8. The food-service function at a nursing home

9. The food-preparation plant of a large restaurant chain

10. The catalog order department of a retailer

E 5.Solution

Identify the most appropriate type of responsibility center for each of the following organizational units.

1. A pizza store in a pizza chain P

2. The ticket sales center of a major airline R

3. The South American segment of a multinational company I

4. A subsidiary of a business conglomerate I

5. The information technology area of a company DC

6. A manufacturing department of a large corporation C

7. An eye clinic in a community hospital P

8. The food-service function at a nursing home C

9. The food-preparation plant of a large restaurant chain C

10. The catalog order department of a retailer R

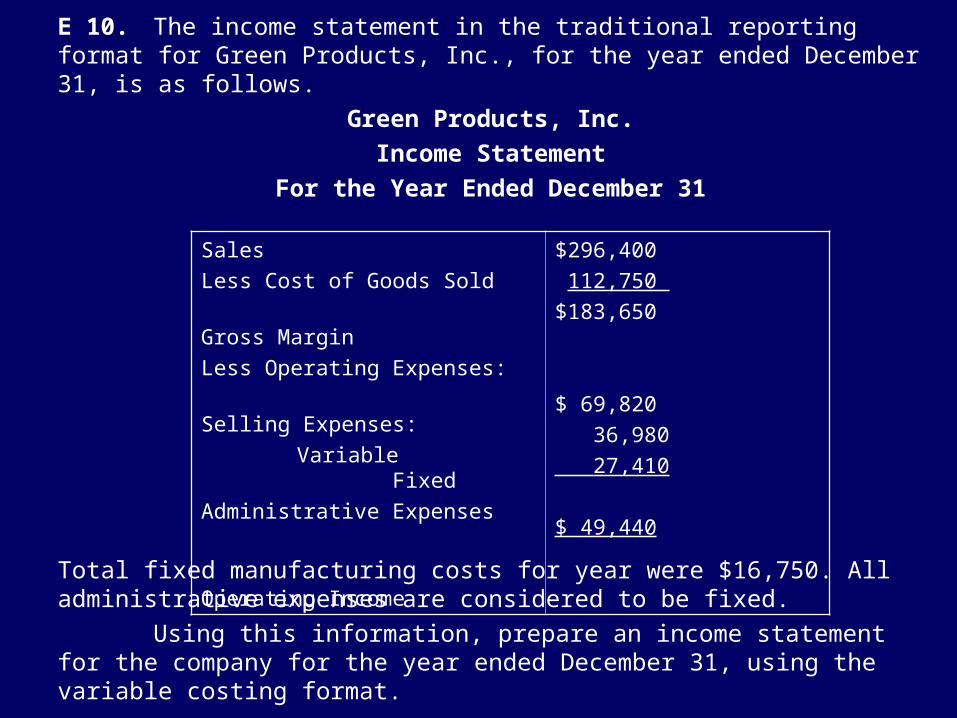

E 10. The income statement in the traditional reporting format for Green Products, Inc., for the year ended December 31, is as follows.

Green Products, Inc.

Income Statement

For the Year Ended December 31

Total fixed manufacturing costs for year were $16,750. All administrative expenses are considered to be fixed.

Using this information, prepare an income statement for the company for the year ended December 31, using the variable costing format.

Sales

Less Cost of Goods Sold

Gross Margin

Less Operating Expenses:

Selling Expenses:

VariableFixed

Administrative Expenses

Operating Income

$296,400

112,750

$183,650

$ 69,820

36,980

27,410

$ 49,440

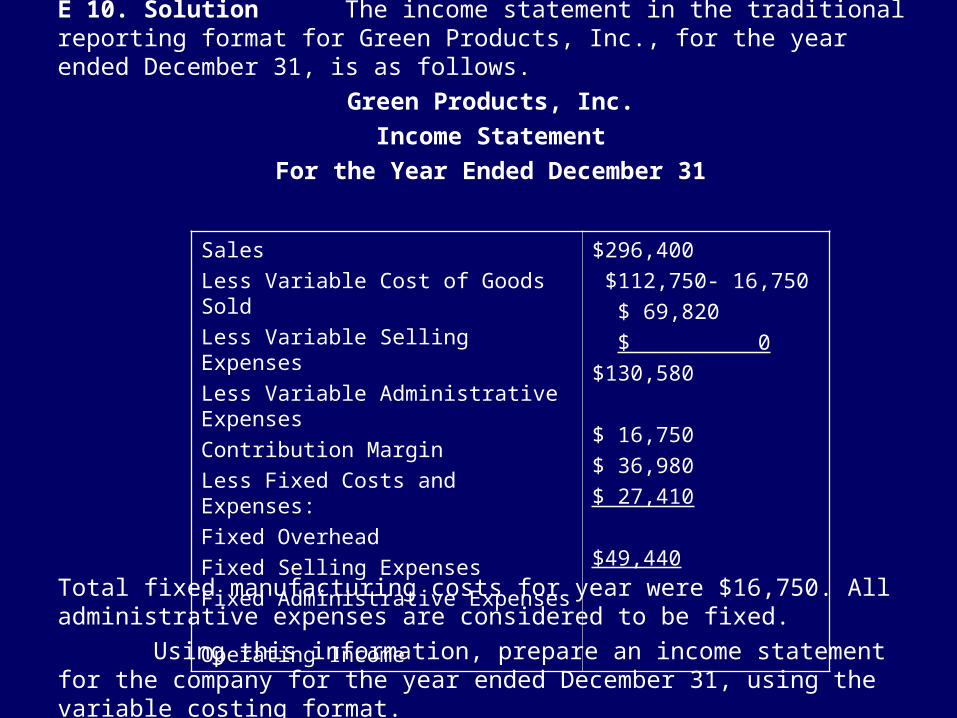

E 10. Solution The income statement in the traditional reporting format for Green Products, Inc., for the year ended December 31, is as follows.

Green Products, Inc.

Income Statement

For the Year Ended December 31

Total fixed manufacturing costs for year were $16,750. All administrative expenses are considered to be fixed.

Using this information, prepare an income statement for the company for the year ended December 31, using the variable costing format.

Sales

Less Variable Cost of Goods Sold

Less Variable Selling Expenses

Less Variable Administrative Expenses

Contribution Margin

Less Fixed Costs and Expenses:

Fixed Overhead

Fixed Selling Expenses

Fixed Administrative Expenses

Operating Income

$296,400

$112,750- 16,750

$ 69,820

$ 0

$130,580

$ 16,750

$ 36,980

$ 27,410

$49,440

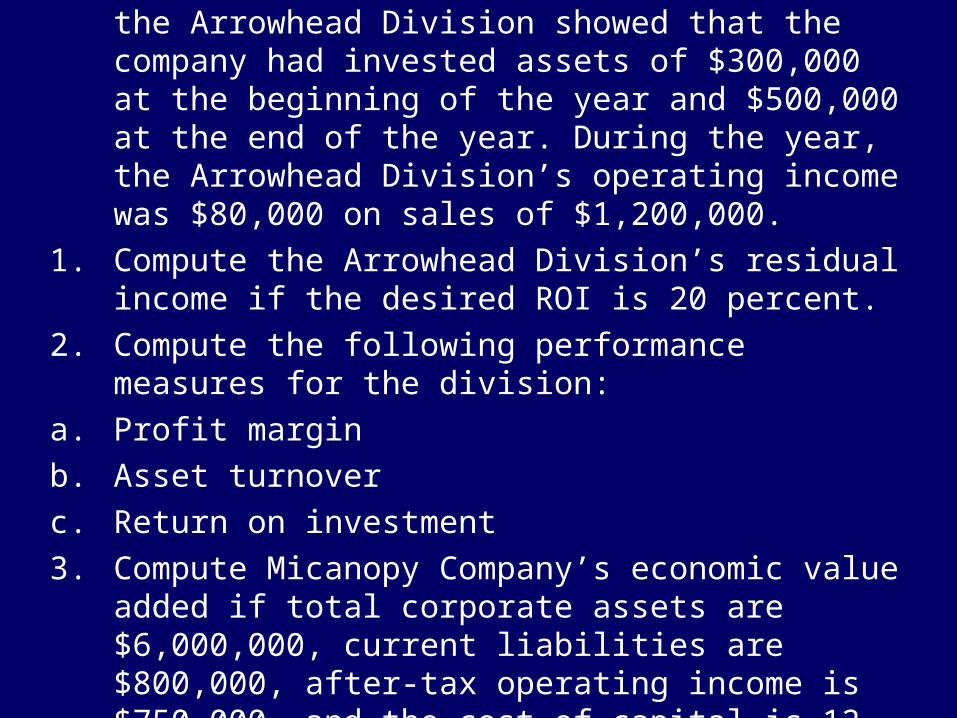

P 8. Micanopy Company makes replicas of Indian artifacts. The balance sheet for the Arrowhead Division showed that the company had invested assets of $300,000 at the beginning of the year and $500,000 at the end of the year. During the year, the Arrowhead Division’s operating income was $80,000 on sales of $1,200,000.

1. Compute the Arrowhead Division’s residual income if the desired ROI is 20 percent.

2. Compute the following performance measures for the division:

a. Profit margin

b. Asset turnover

c. Return on investment

3. Compute Micanopy Company’s economic value added if total corporate assets are $6,000,000, current liabilities are $800,000, after-tax operating income is $750,000, and the cost of capital is 12 percent.

Use only with permission of Susan Crosson

Balanced Scorecard

End-to-end AccountabilityOne type of a Manager’s DashboardKey Performance Objectives, Measures and Targets Linked

Use only with permission of Susan Crosson

The Balanced Scorecard

Developed by Robert S. Kaplan and David P. Norton

A framework that links the perspectives of an organization’s four basic stakeholder groups with the organization’s mission and vision, performance measures, strategic plan, and resources.

Use only with permission of Susan Crosson

Classic Balanced Scorecard Perspectives

Financial

(investors)

Learning and growth (employees)

Internal business processes

CustomersTo succeed, an organization must add value for all groups in both the short and long term……

Use only with permission of Susan Crosson

Other Balanced Scorecard Perspectives

Community GovernmentFinancial (investors)Learning and growth (employees)Internal business processesCustomers

To succeed, an organization must add value for all groups in both the short and long term……

Balanced Scorecard Framework

Ideally, everyone in the organization should be able to see how their actions contribute to the achievement of organizational goals from multiple perspectives…..•Lead indicators•Lag indicators

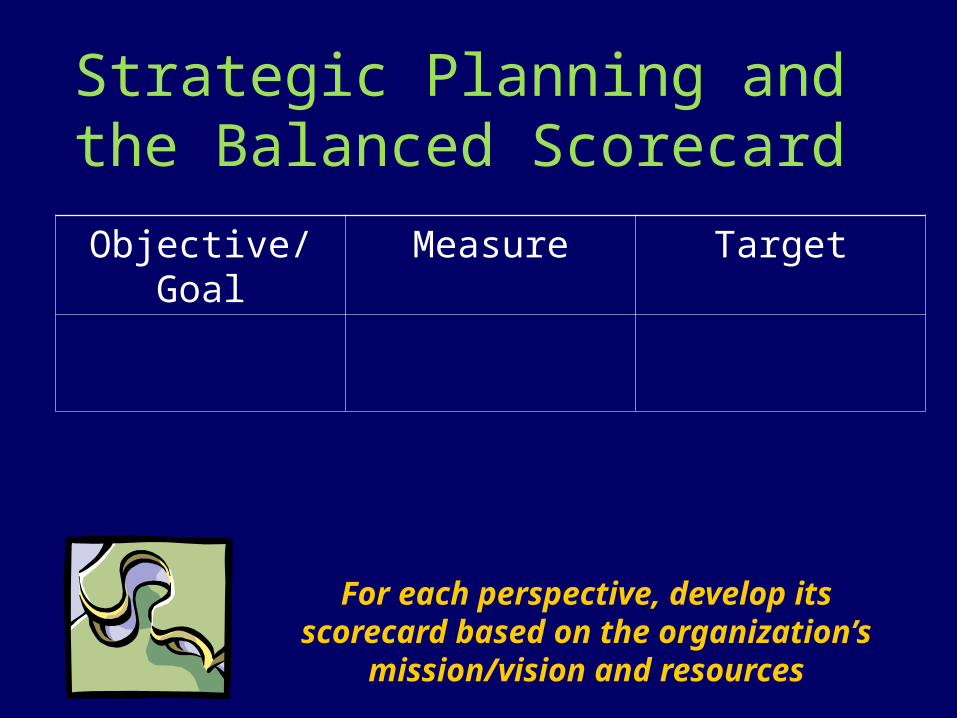

Strategic Planning and the Balanced Scorecard

For each perspective, develop its scorecard based on the organization’s

mission/vision and resources

Objective/Goal Measure Target

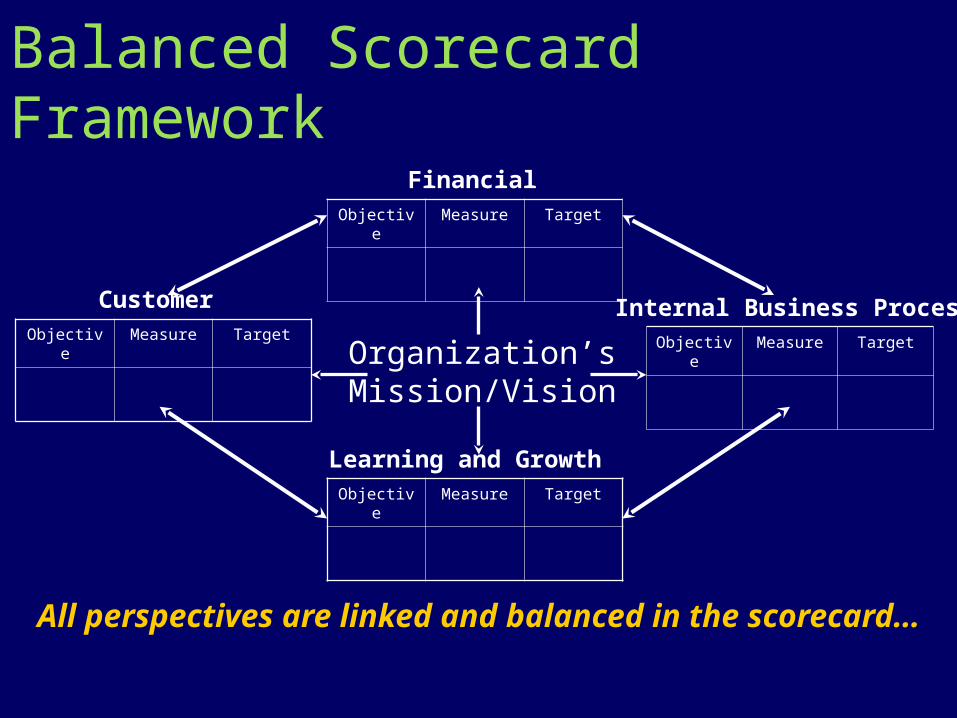

Balanced Scorecard Framework

All perspectives are linked and balanced in the scorecard…

Objective Measure Target

Objective Measure TargetObjective Measure Target

Objective Measure Target

Organization’sMission/Vision

Financial

Customer Internal Business Process

Learning and Growth

Use only with permission of Susan Crosson

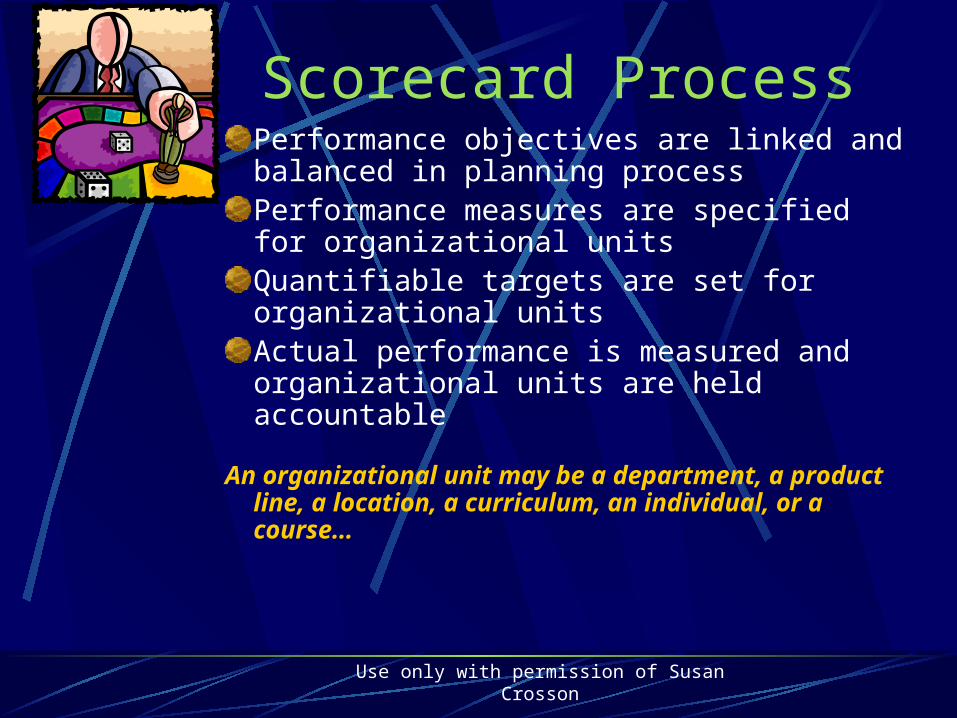

Scorecard ProcessPerformance objectives are linked and balanced in planning processPerformance measures are specified for organizational unitsQuantifiable targets are set for organizational units Actual performance is measured and organizational units are held accountable

An organizational unit may be a department, a product line, a location, a curriculum, an individual, or a course…

Use only with permission of Susan Crosson

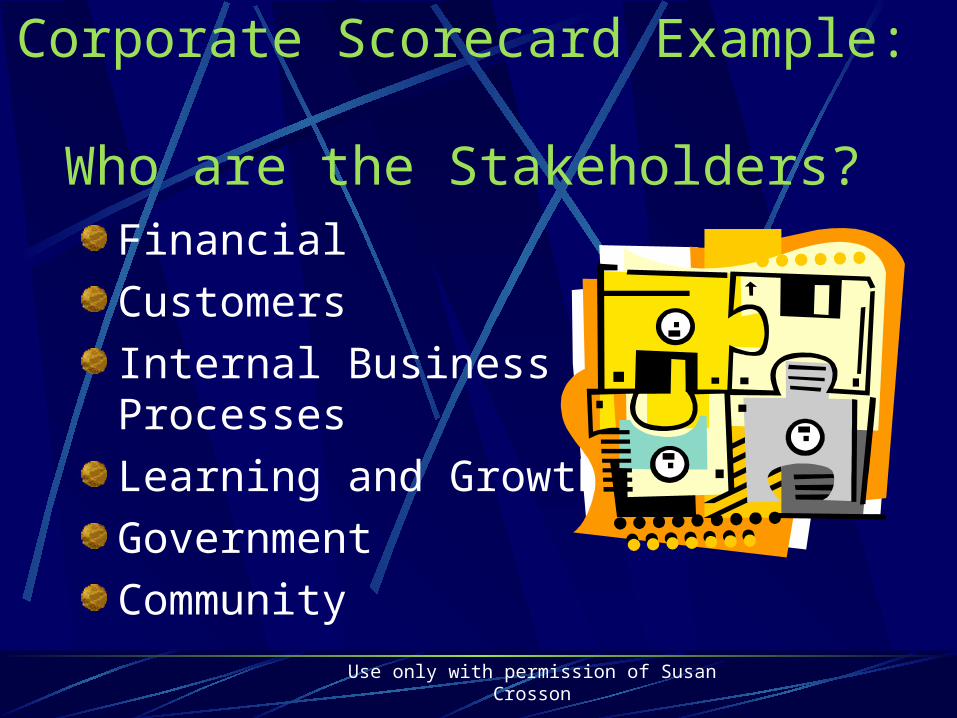

Corporate Scorecard Example: Who are the Stakeholders?

Financial

Customers

Internal Business Processes

Learning and Growth

Government

Community

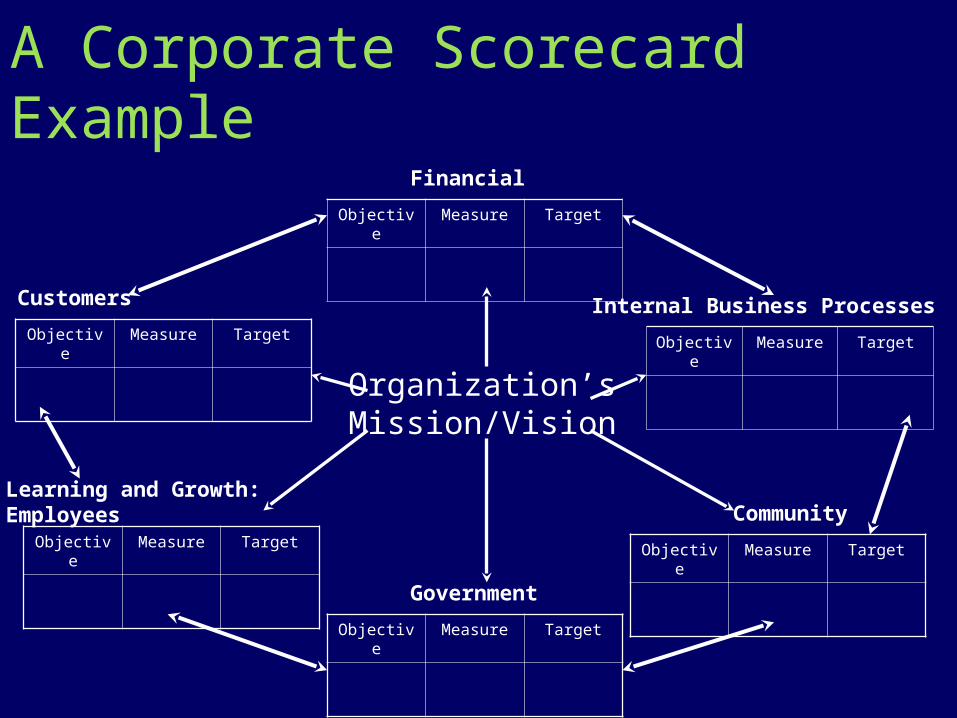

A Corporate Scorecard Example

Objective Measure Target

Objective Measure TargetObjective Measure Target

Objective Measure Target

Organization’sMission/Vision

Financial

Customers Internal Business Processes

Learning and Growth: Employees

Government

Community

Objective Measure Target

Objective Measure Target

Use only with permission of Susan Crosson

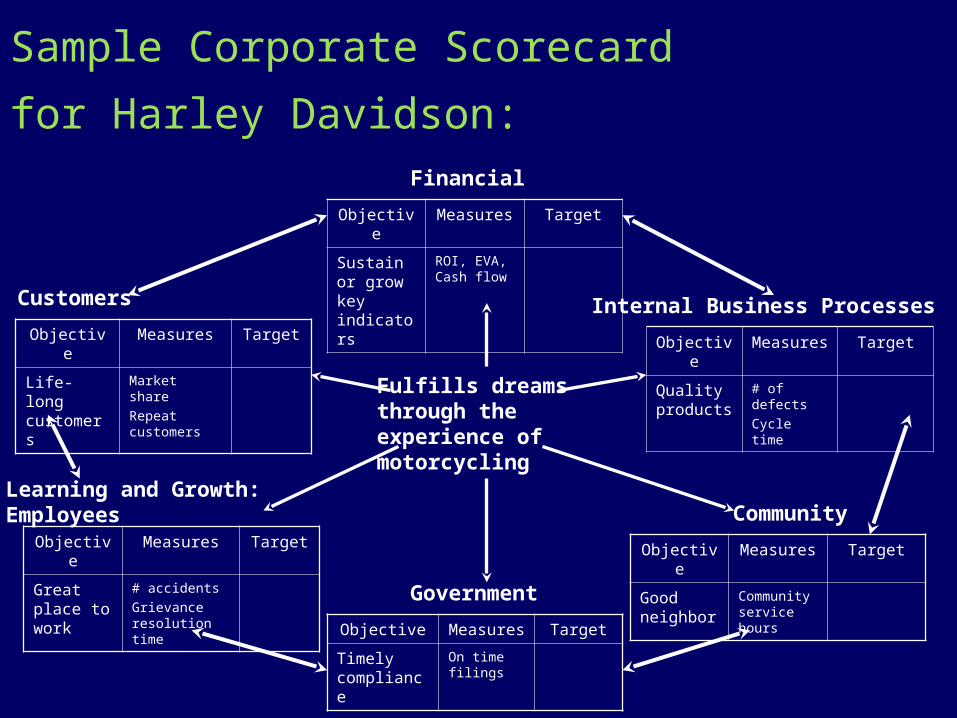

Harley Davidson’s

““Fulfills dreams through the Fulfills dreams through the experience of motorcycling”experience of motorcycling”

Corporate Mission/Vision

Sample Corporate Scorecard

for Harley Davidson:

Objective Measures Target

Sustain or grow key indicators

ROI, EVA, Cash flow

Objective Measures Target

Quality products

# of defects

Cycle time

Objective Measures Target

Life-long customers

Market share

Repeat customers

Objective Measures Target

Great place to work

# accidents

Grievance resolution time

Fulfills dreams through the experience of motorcycling

Financial

Customers Internal Business Processes

Learning and Growth: Employees

Government

Community

Objective Measures Target

Good neighbor

Community service hours

Objective Measures Target

Timely compliance

On time filings

Use only with permission of Susan Crosson

What Do You Know?Balanced Scorecard

E 15

Scorecard for

Review Problem

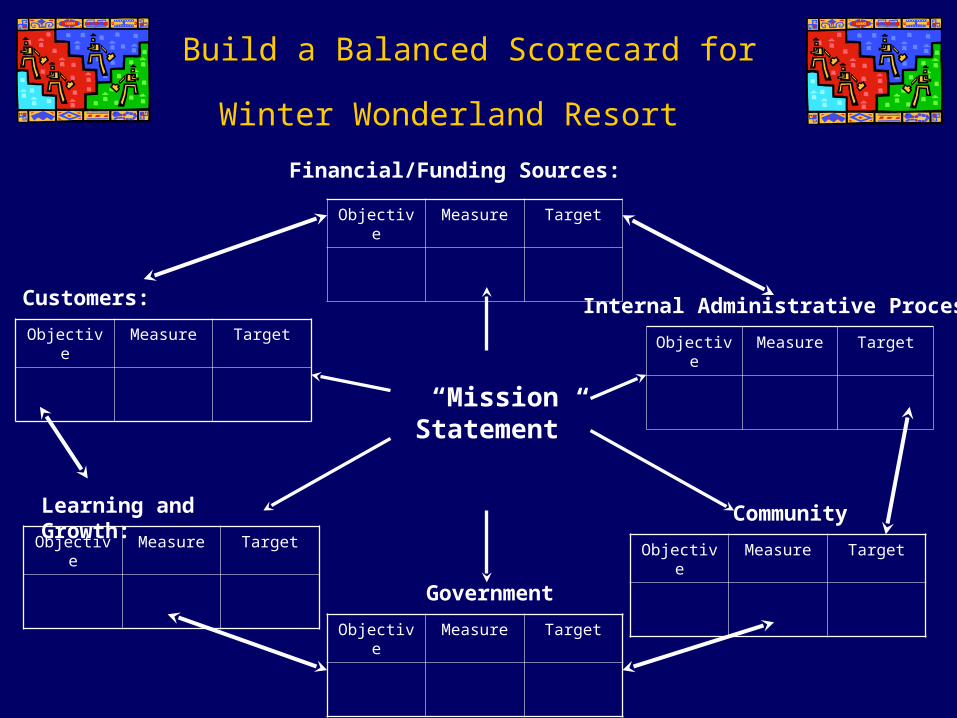

Build a Balanced Scorecard for Winter

Wonderland Resort

Objective Measure Target

Objective Measure TargetObjective Measure Target

Objective Measure Target

Financial/Funding Sources:

Customers: Internal Administrative Processes

Learning and Growth:

Government

Community

Objective Measure Target

Objective Measure Target

“Mission Statement”

Use only with permission of Susan Crosson

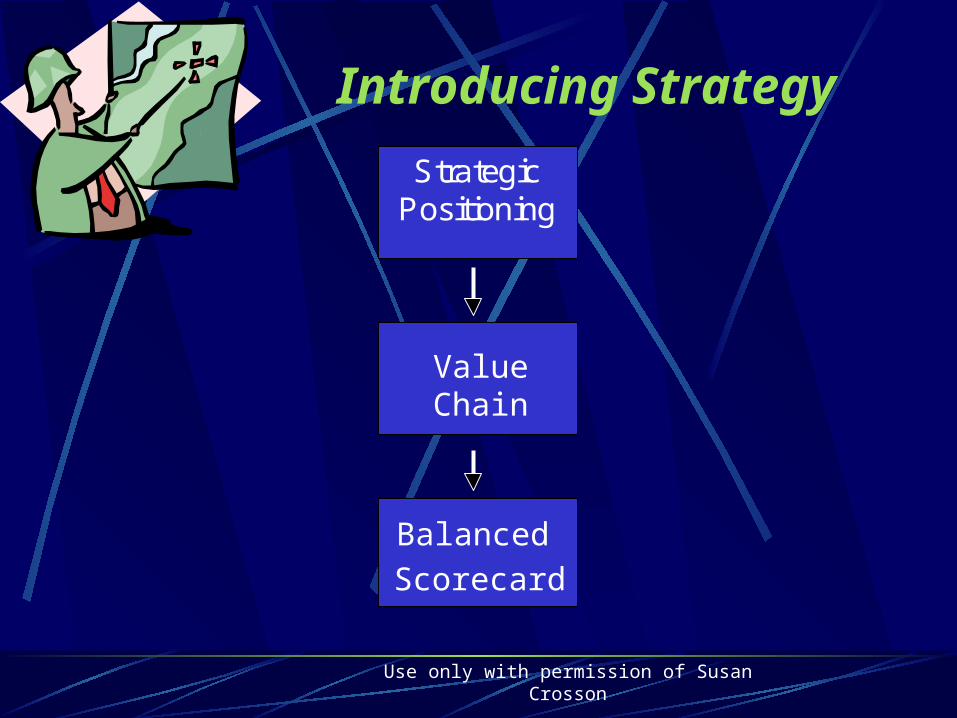

Introducing Strategy

ValueChain

Balanced

Scorecard

StrategicPositioning

Use only with permission of Susan Crosson

Strategic Positioning

Michael Porter…

• Cost Leadership

• Differentiation

• (Focus)

Use only with permission of Susan Crosson

UpstreamManufacturing/OperationsDownstream

Value Chain AnalysisA Detailed Look at Strategy…

Use only with permission of Susan Crosson

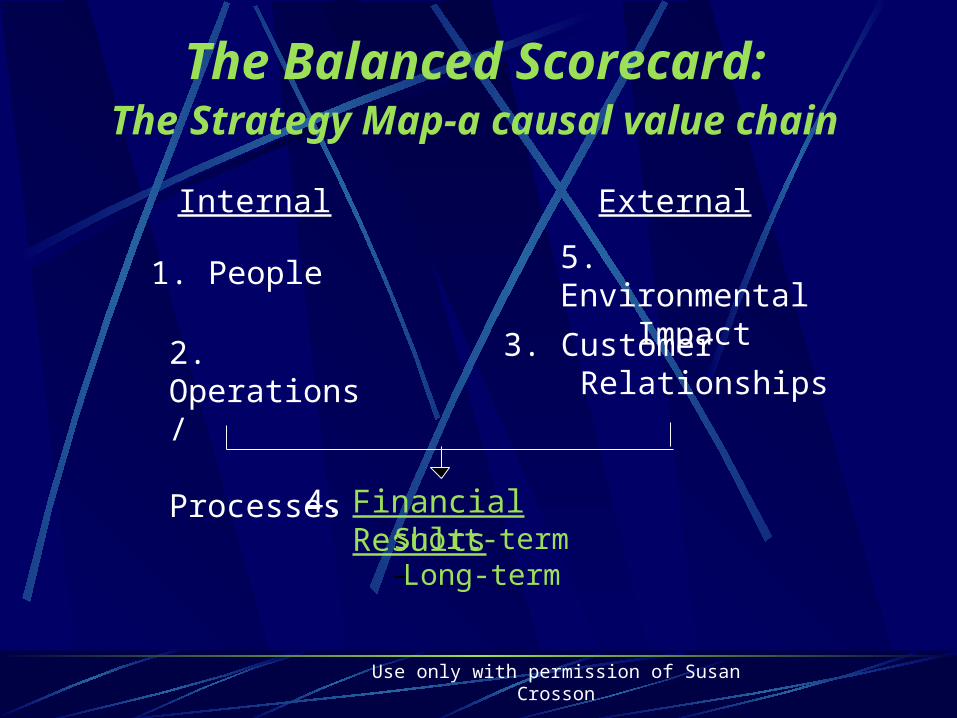

The Balanced Scorecard:The Strategy Map-a causal value

chainInternal External

2. Operations/ Processes

1. People

3. Customer Relationships

5. Environmental Impact

4. Financial Results– Short-term– Long-term

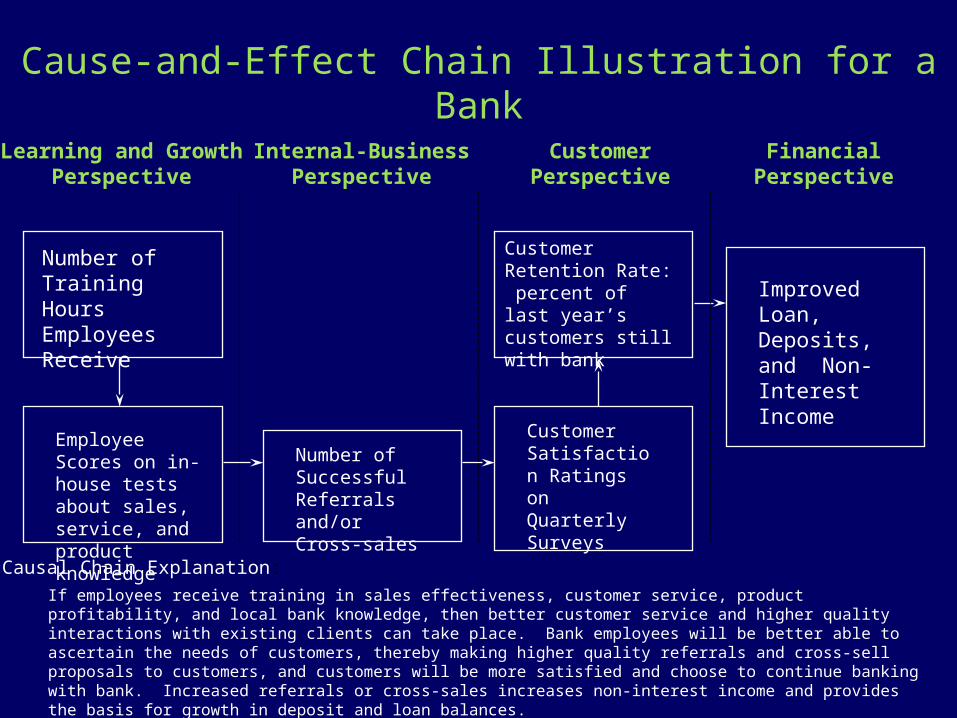

Cause-and-Effect Chain Illustration for a Bank

Learning and GrowthPerspective

Internal-BusinessPerspective

CustomerPerspective

FinancialPerspective

Number of Training Hours Employees Receive

Employee Scores on in-house tests about sales, service, and product knowledge

Number of Successful Referrals and/or Cross-sales

Customer Satisfaction Ratings on Quarterly Surveys

Customer Retention Rate: percent of last year’s customers still with bank

Improved Loan, Deposits, and Non-Interest Income

If employees receive training in sales effectiveness, customer service, product profitability, and local bank knowledge, then better customer service and higher quality interactions with existing clients can take place. Bank employees will be better able to ascertain the needs of customers, thereby making higher quality referrals and cross-sell proposals to customers, and customers will be more satisfied and choose to continue banking with bank. Increased referrals or cross-sales increases non-interest income and provides the basis for growth in deposit and loan balances.

Causal Chain Explanation:

Use only with permission of Susan Crosson

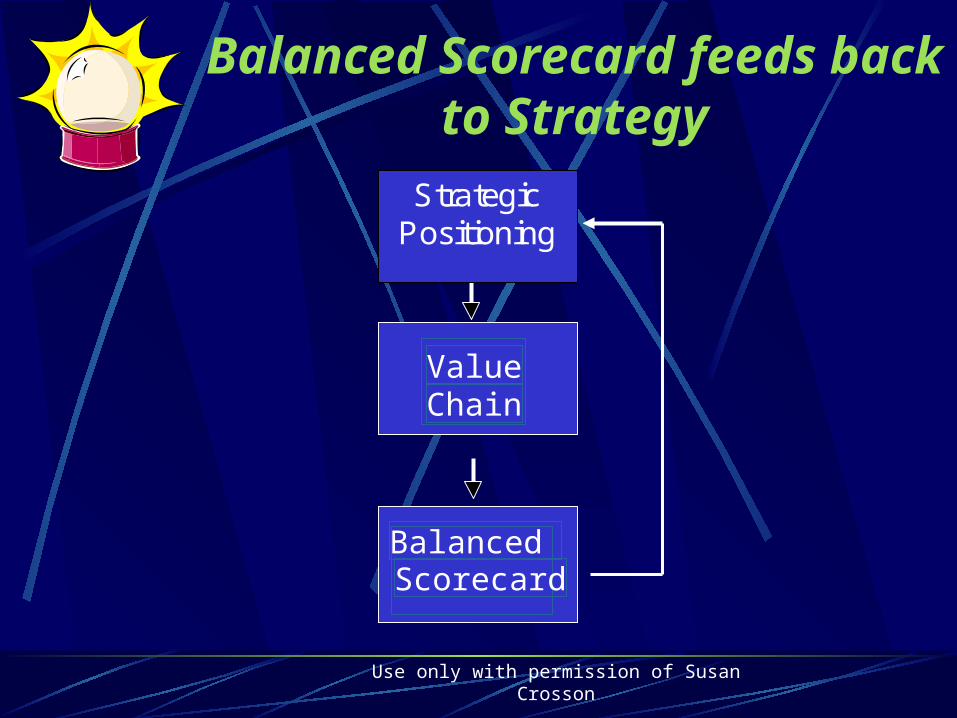

Balanced Scorecard feeds back to Strategy

ValueChain

Balanced Scorecard

StrategicPositioning

Use only with permission of Susan Crosson

Linking executive compensation and performance

Performance-based payProfit sharing Cash bonusStock options, ESOPsRestricted stock

You get what you measure

Use only with permission of Susan Crosson

Homework

P 3