Embed Size (px)

Citation preview

183chAPTeR 9. Markets

DavidN.Wear,JeffreyPrestemon,RobertHuggett, andDouglasCarter1

key FiNDiNGS

•AlthoughtimberproductionintheSouthmorethandoubledfromthe1960stothelate1990s,outputlevelshavedeclinedoverthelast10years,signalingstructuralchangesintimbermarkets.

• Forsoftwoodproducts,productiondeclinesaremostclearlyrelatedtodemandissues.Demandforsoftwoodsolidwoodproductsisstronglylinkedtohousingmarkets,andasharpdeclineinconstructionbeginningin2007reducedtimberdemand,ashortrunadjustment.DemandforpulpwoodinpapermanufacturinghasdeclinedastheproductioncapacityhasdroppedintheSouth,alongrunadjustment.

•Asdemanddeclined,investmentsinsoftwoodproductioncontinuedtoexpand,leadingtosupplygrowthforallsoftwoods,butespeciallyforsoftwoodpulpwood.Thenetresultwasasubstantialreductioninsoftwoodpulpwoodprices.

• Incontrasttosoftwoodproducts,hardwoodpulpwoodoutputdeclinedanditspriceincreasedinthe2000s,indicatingacontractionofsupply,especiallyintheCoastalPlainwherepaperproductionisconcentrated.

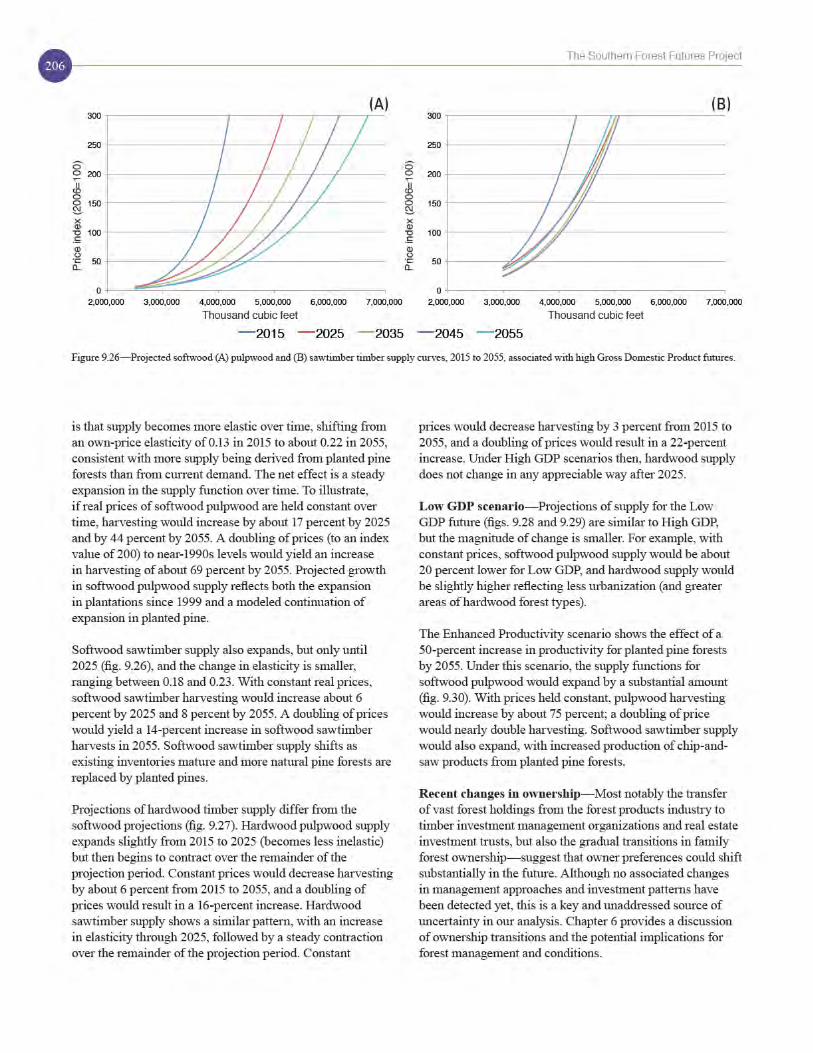

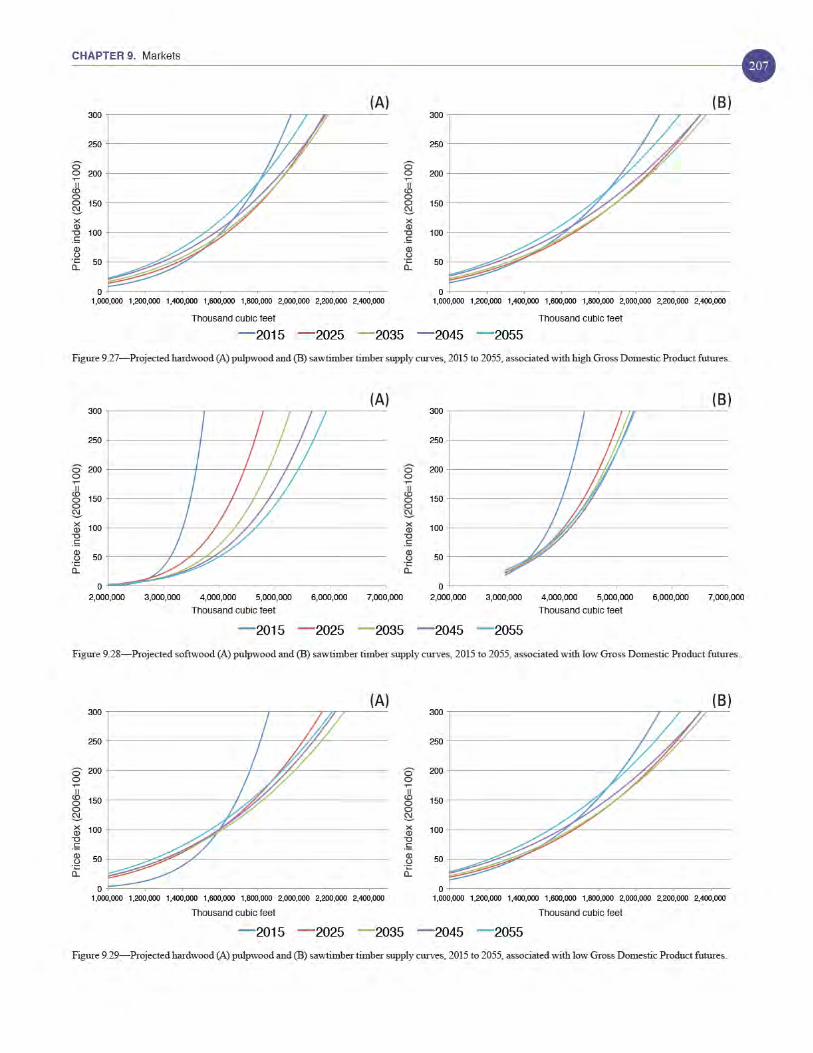

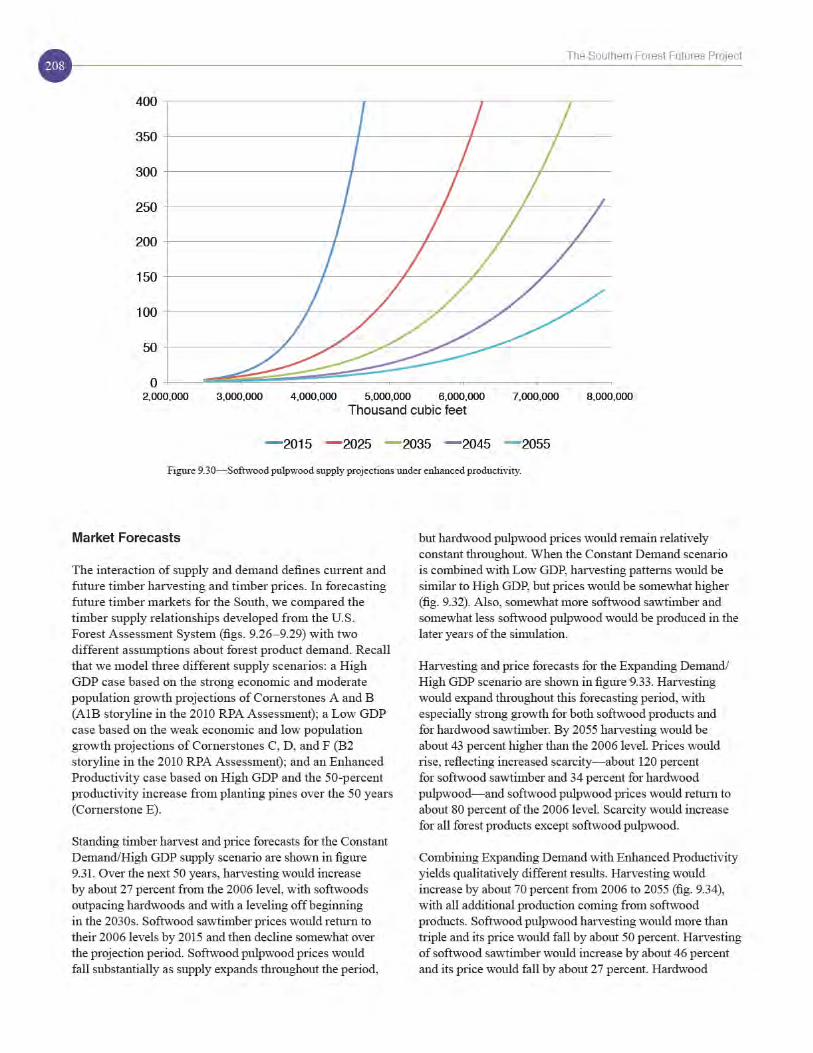

• Severalforecastsoftimbermarketsshowexpandingsuppliesofsoftwoodtimber,especiallysoftwoodpulpwood,asnewplantationsmatureandadditionalplantationsaccumulateacrosstheSouth.Acrossallforecasts,softwoodpulpwoodsupplyexpandsthroughthenext40years,whilesoftwoodsawtimbersupplygrowsoverthenextdecadeandthenstabilizes.

• Forecastsofhardwoodsuppliesindicateagradualcontractionasurbanizationshrinksinventories.

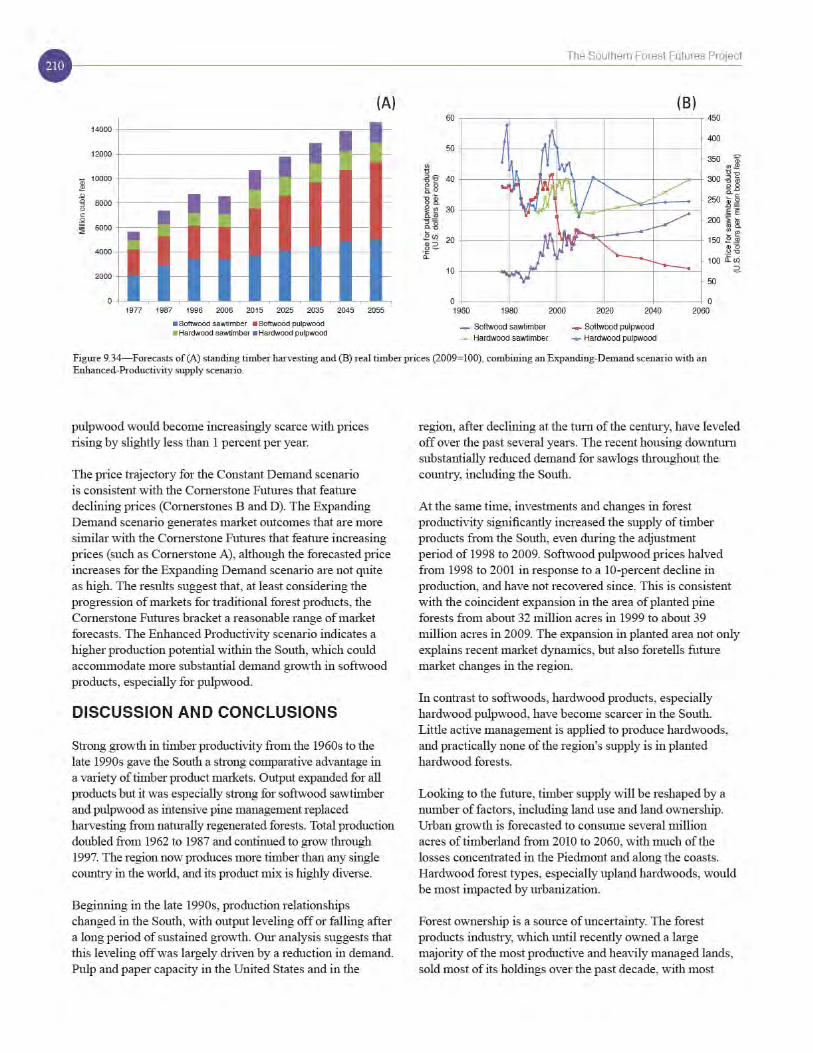

• Iftimberproductdemandreturnstoandstaysatthe2006levels,totaltimberproductionisforecastedtoexpandbyabout25percentoverthenext50years,withlittleimpactonthepriceofsoftwoodsawtimberandhardwoodpulpwood.Softwoodpulpwoodpriceswoulddeclinebyabout50percent.

1DavidN.WearistheProjectLeader,CenterforIntegratedForestScience,SouthernResearchStation,U.S.DepartmentofAgricultureForestService,Raleigh,NC27695;JeffreyPrestemonisaResearchForesterattheForestEconomicsandPolicyResearchWorkUnit,SouthernResearchStation,U.S.DepartmentofAgricultureForestService,ResearchTrianglePark,NC27709;RobertHuggettisaResearchAssistantProfessor,DepartmentofForestryandEnvironmentalResources,NorthCarolinaStateUniversity,Raleigh,NC27695;DouglasCarterisaProfessor,SchoolofForestResourcesandConservation,UniversityofFlorida,Gainesville,FL32611.

• Ifdemandgrowthreturnsto1980sand1990slevels,totaltimberproductioncouldexpandbyabout40percentoverthenext50years,withthegreatestgainsinsoftwoodpulpwoodoutput.Softwoodpulpwoodpricesstabilizeat2006levelswhilesoftwoodsawtimberandhardwoodpulpwoodpriceswouldincreaseatanaverageannualrateofslightlylessthan1percent.

•Growthindemand,coupledwithgainsintheproductivityofplantedpineforests,wouldlikelyexpandtotaltimberproductionbyabout70percent,withtheproductionofsoftwoodpulpwoodmorethantripling.Thepriceofsoftwoodsawtimberwouldstabilize,thepriceofsoftwoodpulpwoodwouldfallatlessthan1percentperyear,andthepriceofhardwoodpulpwoodwouldincreasebylessthan1percentperyear.

• ForecastsindicatethattheSouth’stimbersupplycouldexpandifmoderateratesoffutureforestinvestmentsareaddedtoinvestmentsinforestsmadeoverthepast20years.Forecastsfor2055showthatannualproductionofsoftwoodpulpwoodcouldincreasebeyond2006levelsbyanadditional2.4billionto3.7billioncubicfeet(36.6millionto57.9milliongreentons)withoutsubstantialpriceeffects.

•TimberproductionhasthepotentialtoexpandsubstantiallyintheSouth,butfuturemarketsarelikelytobelimitedbydemandlevels.Bioenergyisapotentialbuthighlyuncertainsourceofdemand.Recoveryofhousing-relateddemandforwoodproductsremainsakeyuncertaintyintheshortrun.

•Withoutanexpansionintimberdemand,privateforestownerswouldbeexpectedtoeventuallyexperienceastrongshiftawayfromforestmanagementasinvestmentreturnsdiminishtothepointwherecontinuedinvestmentscannotbejustified.

iNTRoDucTioN

TimberproductionfromtheSouthgrewsubstantiallyandsteadilyfrom1950tothelate1990s.Althoughproductionhasdeclinedfrom1997/1998peaklevels,theregionstillprovidesamajorityofthetimberproductsproducedintheUnitedStates(Smithandothers2009).Rapidgrowthinproductionfrom1970to1998didnot,however,depletestandinginventoriesofbiomassbecausehighgrowthratesandinvestmentsinagricultural-styleforestryincreased

Chapter 9. markets

184The Southern Forest Futures Project

forestproductivity—plantedpineforestsnowrepresent19percentofsouthernforestland.Recentharvestdeclinesraisequestionsaboutthefutureoftimbermarkets,andrecentpolicydiscourseabouttheuseofwoodtoproduceenergyonlargescalessuggestspotentialforuncertaintyandstructuralchangesinthesemarkets.

Theobjectivesofthischapteraretoexaminethehistoryofchangeinforestproductsmarketsandtoconsiderpotentialfutures.Weusehistoricalrecordsofharvestquantitiesandtimberpricestotestgeneralhypothesesaboutchangesinsupplyanddemand.Supplyforecastsandtrendsinproductdemandarethenusedtoanalyzemarketpotentialandtoconstructalternativeforecastsofharvestsandtimberprices.Throughouttheseanalyses,thechapteraddressesthefollowingspecificquestions:

•Howhavemarketsforforestproductschanged,especiallyinthepastdecade?

•Whataretheimplicationsofthesechangesforthefutureoftimbermarkets?

•Howistimbersupplyprojectedtochange?•Whatfactorsinfluencethefutureofforestproductdemandandwhataretheimplicationsfortimbermarkets?

•Howmightmarketsdevelopinresponsetoalternativescenariosforfuturesupplyanddemand?

influences on Timber Supply

Timbersupplydefineshowlandownersdelivertimbertomarketinresponsetotimberpricesand,inthelongerrun,toavarietyofothersignals.Severalfactorsmakeitdifficulttoanalyzethetimbersupplysituation,includingthelongproductionperiodinvolvedingrowingtrees,themultiplebenefitsthatlandownerscanderivefromstandingforests,andconstantchangesinthelandbasefromwhichtimberisproduced.Itiscommontothinkofsupplyassimplytherelationshipbetweenharvestsandpricesbuttheseotherfactorsneedtobeaccountedfor,especiallywhenconsideringlongrunsupplydynamics.

Suppliesoftimberareultimatelydeterminedbytheintersectionofthebiologicalproductioncapacityofforestsandthepreferencesofforestlandowners.Thischapterdescribesalternativeproductionpossibilitiesbyevaluatingalternativeassumptionsaboutproductivity.Italsoconsidersarangeofproducerbehaviorbyconsideringalternativeprojectionsofforestinvestments(plantationreplacementandestablishment),basedonthehistoricalbehaviorofprivateforestlandowners.

influences on Timber Demand

Demandisaneconomicconceptthatrelatestheconsumptionofacommoditytoitsprice.Economictheoryindicates

thatlessofacommodityisconsumedatahigherpriceandthatchartingallthepossibleprice-consumptioncombinationsdefinesademandcurve.Thiscurve,however,canberepositionedbasedonmanyfactorsotherthanthecommodity’sprice—suchasincome,pricesofsubstitutesforthecommodity,andchangingtastes.Inthischapter,weexaminedemandfortimberproductsbyanalyzingthevariousfactorsthatcouldalterdemandrelationships.Welookcloselyatsubstitutionpossibilities,productioncapacity,andinternationaltradeasindicatorsofchangesindomesticdemandfortimberproducts.

Perhapsthemostimportantuncertaintyaboutthefutureoftimberdemandisthedevelopmentofnewmarketsforfiberintheproductionofbioenergy.Asarenewableresource,forestbiomassmayplayanimportantroleinmeetinggoalsestablishedthroughrenewableportfoliostandards,andcellulosicfeedstocksforliquidfuelshavebeentargetedin2008FarmBillandotherpoliciesaimedatincreasingtheuseofrenewableenergy.Demandsforwoodforco-firingincoalfiredelectricityplantsandforproductionoffuelpelletshavealreadyemerged,althoughbiofuelproductiononalargescalewouldrequiretechnologicaladvances.Chapter10addressespotentialbioenergyfuturesindetail.

Scope of Analysis

Chapter10examineshowdemandforwoodintheproductionofbioenergycoulddevelopinthefuture,andwerefertothatchapterinexaminingafullrangeofmarketfutures.Whileevaluatingmarketfutures,wedonotattempttoforecastthebusinesscycle,inparticular,therecoveryfromthe2007recessionandthereturntohistoricaltrendsinproductdemand.Rather,ourfocusisonlongruntrendsand,ultimately,theimplicationsforforestsustainabilityandthecapacitytoadapttochangingdemandforfiberinthecomingyearsanddecades.

meThoDS

Theanalysisofhistoricalchangesintimbermarketspresentedherestartsbyupdatingthedatafromareport(Wearandothers2007)thatexaminedbasicprice-andharvest-quantityindicatorsandinterpretedpatternsofchangetoprovidegeneralinsightsintomarketdirectionandtrendsindemandandsupply.Asetofexplanatoryfactorsthathaveaffectedthedemandfortimberproducts—includingdomesticconditions,technologychanges,andinternationaltrade—placesdemandtrendsincontext.Ananalysisoftimbersupplyfundamentalsfocusesonlanduse,forestinvestment,andtimberlandownershipandtheireffectsonthefutureprovisionoftimberfromprivatelands.

Weuseempiricalmodelsoftimbersupplyanddemandtoexplorealternativefuturesfortimbermarkets.Futuretimber

185chAPTeR 9. Markets

supplyrelationshipsarederivedfromsimulationrunsoftheU.S.ForestAssessmentSystem’sForestDynamicsModeldescribedinchapters4and5.ThemodelsimulateschangeintheSouthonallplotsoftheForestInventoryandAnalysis(FIA)ProgramoftheForestService,U.S.DepartmentofAgriculture,includingharvestchoicesmadeinresponsetothefuturemarketconditionsdescribedbythepriceprojectionsofthesixCornerstoneFutures(chapter2):

•CornerstoneAdescribesafutureofveryrapideconomicandtechnologicalgrowth,combinedwithincreasingtimberprices.

•CornerstoneBisalsobasedonrapideconomicandtechnologicalgrowthbutcombinedwithdecreasingtimberprices.

•CornerstoneCisbasedonmoderatelevelsofeconomicdevelopmentandlessrapidbutmorediversetechnologicalchange,combinedwithincreasingtimberprices.

•CornerstoneDisalsobasedonmoderatelevelsofeconomicdevelopmentandlessrapidtechnologicalchange,butcombinedwithdecreasingtimberprices.

•CornerstoneEisbasedonCornerstoneAbutallowsforanincreasedrateofplantingfollowingtheharvestofnaturallyregeneratedforests.

•CornerstoneFisbasedonCornerstoneDbutwithadecreasedrateofforestplantingfollowingharvests.

HarvestchoicemodelsarebasedonempiricalmodelsofhistoricalharvestinglinkedtoFIAplotsintheSouth.Themodelsaresensitivetochangingforestproductivityandpricesthataffectnetrevenuesfromharvest/noharvestalternatives.UsingtheCornerstoneFutures,simulationsofharvestsforarangeofpricesaresummedacrossallplotstodefinethetimbersupplyfunction(definedastherelationshipbetweenaggregatetimberharvestquantitiesandtheirrespectivetimberpriceswithinaforecastperiod).Pricesforsoftwoodsawtimber,othersoftwoods,hardwoodsawtimber,andotherhardwoodsenterthecalculations(Polyakovandothers2010),andasetofempiricalsupplyfunctionsarederivedforthesefourproductclasses.

Supply Scenarios

WeusedamodifiedversionofthemethodoutlinedbyPolyakovandothers(2010)toconstructaggregatesupplies.ForasetofrelatedCornerstoneFutures—forexample,CornerstonesA,B,andE,thatsharethesamepopulationandeconomicgrowthfuturesbutapplydifferentpriceprojections—weusethesimulationstogeneratemultiplesupplyrealizations,specifically,abootstrappingapproach(employingrandomsamplingwithreplacement)ofsimulationsforeachStateineachtimeperiodthatgenerates1000observationsofsupply.Theserealizationsprovidethedataforregressionequationswheretheharvestquantityforeachproductismodeledasthefunctionofitsprice,

andcumulativeresultsforallproductsprovideestimatesofsupplymodelsineachperiod.Wesetuptheequationssothatthecoefficientonpriceistheown-priceelasticityofsupply(theratioofproportionalchangeinharvesttotheproportionalchangeinprice),andsothatsupplyforeachperiodreflectsforecastsoflandusechangeandresponsestoclimate,disturbances,andforestsuccession.

TheU.S.ForestAssessmentSystemmodelsthesupplyoftotalremovalsfrominventory,butourquestionstargetspecificproductmarkets.Estimatedquantitiesofproductsobtainedfromnumbersofremovalsderivefromutilizationcoefficientsthattranslatesawtimber-sizedremovalsandotherremovalsintowhatwelabelsawlogsandpulpwood.Sawlogsareusedintheproductionoflumberandveneerforpanels.Pulpwoodisdefinedasmaterialdeliveredforuseinthepapermanufacturingandinotherindustrialprocesses—especiallyforfuelwoodandforthemanufactureoforientedstrandboard.Thetimberproductoutputdatabase(Johnsonandothers2010)providesestimatesoftheseconversionfactors,whichweadjustedtoreflectthedifferencebetweenchip-and-sawsawlogsfromplantationsandsawtimberproductsfromnaturallyregeneratedforests.

Basic supply scenarios—WeconstructedtwosupplyscenariosfromtheCornerstoneFutures,onelabeled“HighGDP”toreflectthestrongeconomicandmoderatepopulationgrowthprojectionsofCornerstonesA,B,andE;andtheotherlabeled“LowGDP”toreflecttheweakeconomicandlowpopulationgrowthprojectionsofCornerstonesC,D,andF.

TheseforecastsofchangesinforestsarecontingentonprojectionsoftimberharvestsacrossprivateandpublicforestedplotsintheFIAinventoryusingmarket-drivenharvestprobabilitymodels(Polyakovandothers2010).HarvestpredictionsaredrivenbythepriceprojectionsthatarepartoftheassumptionsthatstructureeachoftheCornerstoneFutures.Weusetheseprojectionsofharveststoestimatesupplyfunctionsforthetwofundamentaleconomicstorylinestheyembody.Associatedforestconditionforecastsandlanduseforecastsaredescribedinchapters5and4,respectively.

Effects of productivity increases—TheimputationapproachadoptedfortheU.S.ForestAssessmentSystemthatundergirdsoursupplyprojectionsusescurrentobservedforestproductivitytoconstructforecasts.Thisisappropriateforshortrunsupplyforecasts,butrecentresearchindicatesthattheproductivityofpineplantationscouldexpandoverthenextseveralyears(McKeandandothers2003).Treeimprovementprogramshaveyieldedgenotypeswithlargegainsinproductivityandnewlyplantedforestsareexpectedtohaveevenlargerproductivitygains(withadditionalcrossingofsuperior

186The Southern Forest Futures Project

parents).Tissueculturepropagationalongwithotheradvancedgenetictechniquesmayincreaseoutputperacrebyevengreateramounts.Therateofdeploymentofimprovedplantingstockandtheproportionofestablishedplantationsreceivingintensivemanagementthroughouttheirrotationisunclearandcompoundstheuncertaintyofanyattempttoforecastproductivitygrowth.

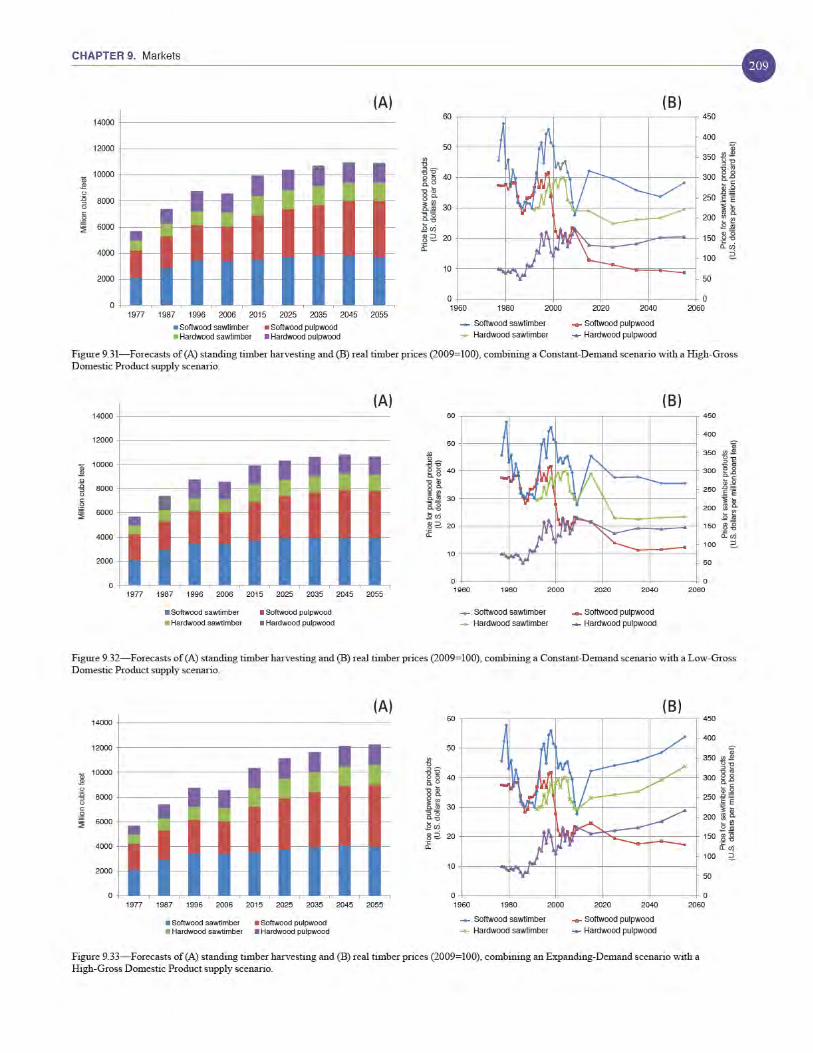

Toexaminethepotentialcontributionsofthisenhancedproductivity,weadoptedastraightforwardsimulationapproachusinganadditiveformulathatincreasesproductivityby10percenteachdecade,sothatbythe2050saverageproductivityofplantedpineforestsis50percenthigherthanthecurrentlevel.Althoughweexpectincreasedproductivitytoeventuallyalterplantingdecisions,andthereforeskewsomeofthedecisionmodelsthatundergirdouranalysis,webelievethatthissimulationapproachprovidesafirstapproximationoflongrunproductionpotential.

Demand Scenarios

Weexaminetwodifferentdemandscenarios.Thefirst—labeledConstantDemand—holdsthedemandrelationshipsfortimberproductsin2006constantoverthe50-yearprojectionperiod.Thisisconsistentwithdemandstabilityforbothpaperandsolid-woodproductsandwouldbeconsistentwithsomesubstitutionwithinproductlines.Ineffect,itisconsistentwithmoderate(longrunaverage)housingdemandandthestabilityobservedinpulpandpapermarketsinthelate2000s.Demandwasmodeledusingaconstantelasticityequationbyintersectingtheharvest-priceobservationfor2006andapplyingexogenouslydeterminedown-priceelasticity,always-0.5,aswasconsistentwiththeliterature.Notethatconstantdemanddoesnotimplyconstantharvests.Ratheritholdsthedemandrelationshipbetweenpriceandharvestconstant,sopricesandharvestscanvaryovertimeinresponsetosupplyshifts.

Theseconddemandscenario—labeledExpandingDemand—examinesareturntodemandgrowthintheSouth.Underthisscenario,productdemandisassumedtoreturnto1996levelsby2015andthenexpand10percentperdecadethroughtheendoftheprojectionperiod.Thisisroughlyconsistentwithdemandgrowthinthe1980sand1990s.

Wedidnotconstructthesedemandscenariostoaddresschangesinworldtradeofforestproductsexplicitly,butinsteadassumedthattheycapturerangeofmarketrealizationsthatisusefulforourprojections,i.e.,theyshouldprovideusefulinsightsintothepotentialrangeofmarketresponsesoverthenext50years.

market Forecasts

Formarketforecastsdefinedbypermutationsofthesupplyanddemandscenarios,wereportforecastedharvestsandpricesforeverydecade.Inventoryandremovalsareconstructedonadecadalbasis,withinventoryreflectingtheconditionsattheendoftheperiodandremovalsreflectingtheaverageremovalsoverthepreviousdecade—forexample,the2030inventoryreflectsremovalsoccurringovertheyears2021–30.Allpricesareinreal2009dollarsandharvestforecastsare,afterapplyingconversionfactors,comparabletothehistoricaltimberproductoutputdataandreportedinsummaryreports(Johnsonandothers2010)forthe2010ResourcesPlanningAct(RPA)Assessment.

Data Sources

HistoricalharvestquantitydataarederivedfromthetimberproductoutputsystemoftheForestService,U.S.DepartmentofAgriculture.ReportsofroundwoodoutputbyregionhavebeendevelopedfortheRPANationalInventoryDatabasefortheyears1952,1962,1977,1981,1996,2001,and2006(Smithandothers2001,2004,2009).ComparableannualdataforsoftwoodandhardwoodpulpwoodharvestshavebeencompiledfortheSouth(JohnsonandSteppleton2005).WealsoconstructedanannualseriesofsoftwoodsawlogproductionbyinterpolatingbetweentheRPAreportingyearsbasedontheproductionofsoftwoodlumberintheSouthasreportedbytheSouthernForestProductsAssociation.

ToexaminepricetrendsweconstructedregionalpriceindicesbasedonpricesreportedbyTimber-MartSouthforallsubregionsoftheSouth.Weconstructedpriceindicesbyproductclassbasedonpricesreportedforintra-StateareasbyTimberMart-South,witheachindexrepresentinganaverageweightedbytheinventoryvolumesofitsassociatedgeographicarea.Throughoutthispaperwereportpricesinrealterms,adjustedforinflationusingtheConsumerPriceIndexpricedeflator,with2009asthevaluebasis.Indicesoftimberpriceswerealsousedtoalloweasiercomparisonsamongproducttypes.Whenindiceswereused,wedefined1977asthebaseyear(theindexissetequalto1in1977)andappliedtheindexingtotherealpricesdescribedabove.

TradedataweretakenlargelyfromthedatabasecompiledbyDaniels(2008),whichsummarizesextensiverecordsonimportsandexportsfromtheU.S.DepartmentofCommercethrough2005.Othersecondarysourcesweretappedtoprovidedataonexports/importsofselectedproductsbeyond2005,woodproductscapacity,andvariouspriceindices.

187chAPTeR 9. Markets

ReSulTS

WestartthissectionbyexamininghowtimbermarketshavechangedintheSouthsincedetailedrecordshavebeenkept(withemphasisonthemostrecentchanges)usingtimberharvestsandpricesassummaryindicatorsofdevelopmentovertime.Webeginbyexamininghowharvestquantitiesandpriceshavechanged,andwherepossible,deconstructingthosechangesintoimpliedshiftsinsupplyanddemandtoaddcontext.

historical Timber markets

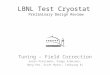

Southernforestsyieldawidevarietyofhardwoodandsoftwoodtimberproducts.Softwoodproductsconstituted71percentofharvestoutputin2006,thelatestyearforwhichcomprehensivetimberproductoutputdataareavailable(fig.9.1).Forty-twopercentoftotalharvestwasforsawlogsand38percentwasforpulpwoodproducts.Softwoodsawlogscomprisedthelargestproductclass(31percent),followedbysoftwoodpulpwood(26percent)andhardwoodpulpwood(12percent);thethreerepresentedroughly69percentofharvests,continuingatrendthatbeganinthe1970s(fig.9.1).

Timberharvestsfromsouthernforeststrendedstronglyupwardduringthelasthalfofthe20thcentury(fig.9.1).From1962to1996,annualharvestingmorethandoubledfromabout4toalmost10billioncubicfeet,witharelativelyconstantproductmix.Productionrangedfrom39to44percentfrompulpwoodand64to71percentfromallsoftwoods,withnoconsistenttrends.

Growthinharvestsforallproductswassteadyfromoneyeartothenextwithonlyafewexceptions(fig.9.2),themostnotablebeingadipinoutputduringabriefrecessioninthemid-1970s.Growthinharvestswasatitsstrongestfrom1982through1998,withoutputexpandingatacompoundrateof3.3percentperyear.Afterthislongperiodofstronggrowth,totalharvestquantityfellbyapproximately23percentfrom1997to2008,returningtotalharvestquantityto1987levels.Thisrepresentsthelargestandlongestdownturninharvestingoverthehistoricalperiod(1952to2008).

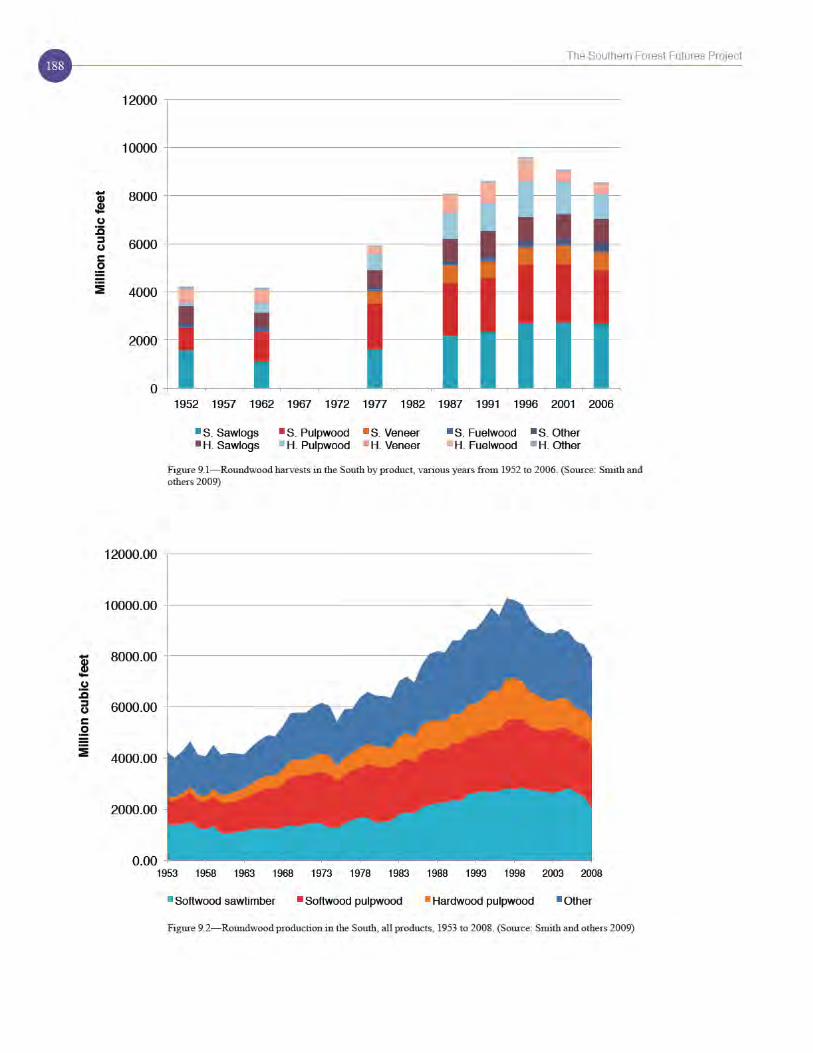

Trendsinthethreelargestproductclasses(fig.9.3)showthattheharvestdeclinewasledbyreductionsinhardwoodpulpwood(alossof42percent),followedby27percentforsoftwoodsawtimberand7percentforpulpwood.Mostofthedeclineinsoftwoodsawtimberproductionoccurredsince2005(fig.9.3).Wewereunabletoconstructanannualtimeseriesofhardwoodsawlogproduction(thefourthlargestproductclass)usingacomparabletechnique,buttheperiodicdata(fig.9.1)suggestthathardwoodsawtimberharvestswererelativelystableatleastthrough2006,with

incompletedatasuggestingsubstantialdeclinesbeginningin2007inassociationwiththehousing-relatedrecessionthatbeganthatyear.

Timberpricesareanindicatorofthescarcityoftimberasaninputtoproduction,andtheyreflecttheinteractionofsupplyanddemand:ifstumpagepricesincrease,thentimberbecomesrelativelyscarcer.Conversely,fallingstumpagepricesindicatethattimberisbecomingmoreabundantrelativetodemandforitsuse.Pricesforvariouswoodproductsdemonstratedavarietyoftrendsfrom1977to2009,theperiodforwhichwehavecomprehensivedata,indicatingthatscarcityorabundanceoftheseresourcesisacomplexandevolvingstory.

From1977tothelate1980s,timberpriceswereflat-to-decliningforallhardwoodandsoftwoodproducts(fig.9.4).Comparedto1977,softwoodsawtimberpricesdeclinedveryslightlythrough1991,softwoodpulpwoodpriceswereessentiallyflatthrough1989,andhardwoodpulpwoodpriceswereflatthrough1988.Harvestinggrewatmoderaterates(fig.9.3),withnoindicationsofincreasingscarcitythroughthelate1980s.

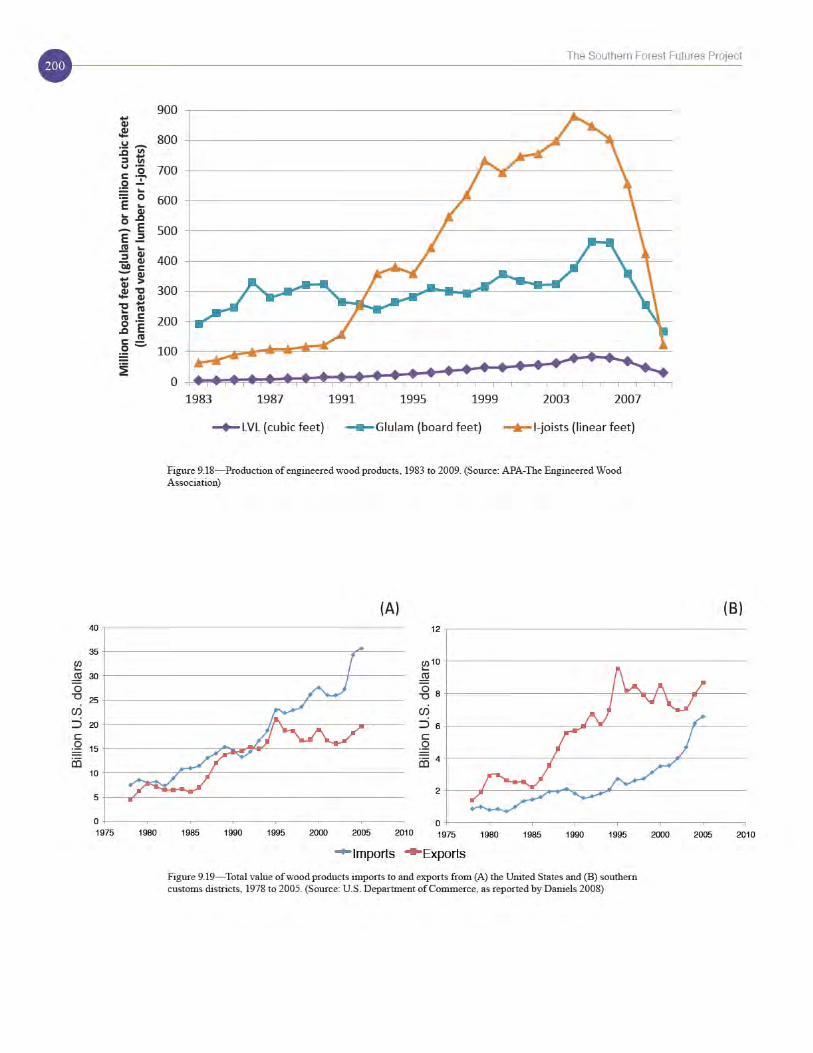

Pricepatternsbeganchangingbetween1989and1992(fig.9.4).Real-dollarpricesturnedupwardforallfourproductsandincreasedthrough1997or1998,whenproductionpeaked.From1988to1998,hardwoodpulpwoodpricesincreasedatanaverageannualrateof12percent,followedbysoftwoodpulpwoodat5percentandsoftwoodsawtimberat8percent.Hardwoodsawtimberpricesincreasedby6percentfrom1992to1998.Thesepricedataindicateincreasingscarcityforalltimberproductsoverthedecade.

From1998to2009,hardwoodpulpwoodandsawtimberpricesstabilized,andsoftwoodsawtimberpricesdeclinedfromtheirnear-peak1998level(onlyexceededin1979)andfrom2005to2009reachedtheirlowestlevelofthehistoricalperiod.Softwoodpulpwoodpriceshave,however,followedadecidedlydifferentpattern.From1998to2001,pricesforthisproductfelltoabouthalfoftheir1998value,theirlowestlevelofthehistoricalperiod,andhaveremainedatthislevelthrough2009.

Changesinharvestquantitiesandtimberpricessince1998suggestthattimbermarketshavebeenandcontinuetobedynamic.Softwoodproductpriceshavedeclinedfromtheirpeaklevels,buthardwoodproductpriceshaveremainedrelativelyconstant.Thesepricechanges,combinedwithharvestpatterns,suggestthatreturnsavailabletomosttimberlandownersarenowsubstantiallylowerthantheywereinthepeakyearsofthe1990s.Forsoftwoodpulpwood,thesepatternssuggestacontractioninpulpwooddemandcoupledwithstable-to-expandingsupplyofstandingpulpwood-sizedtimber.Incontrast,hardwoodpulpwood

190The Southern Forest Futures Project

seemstohavebecomesomewhatscarcer;softwoodpulpwoodpriceswereabouttwiceashighashardwoodpulpwoodpricesintheearly1990s,butthetwoproductsarenowroughlyequalinprice(fig.9.4).

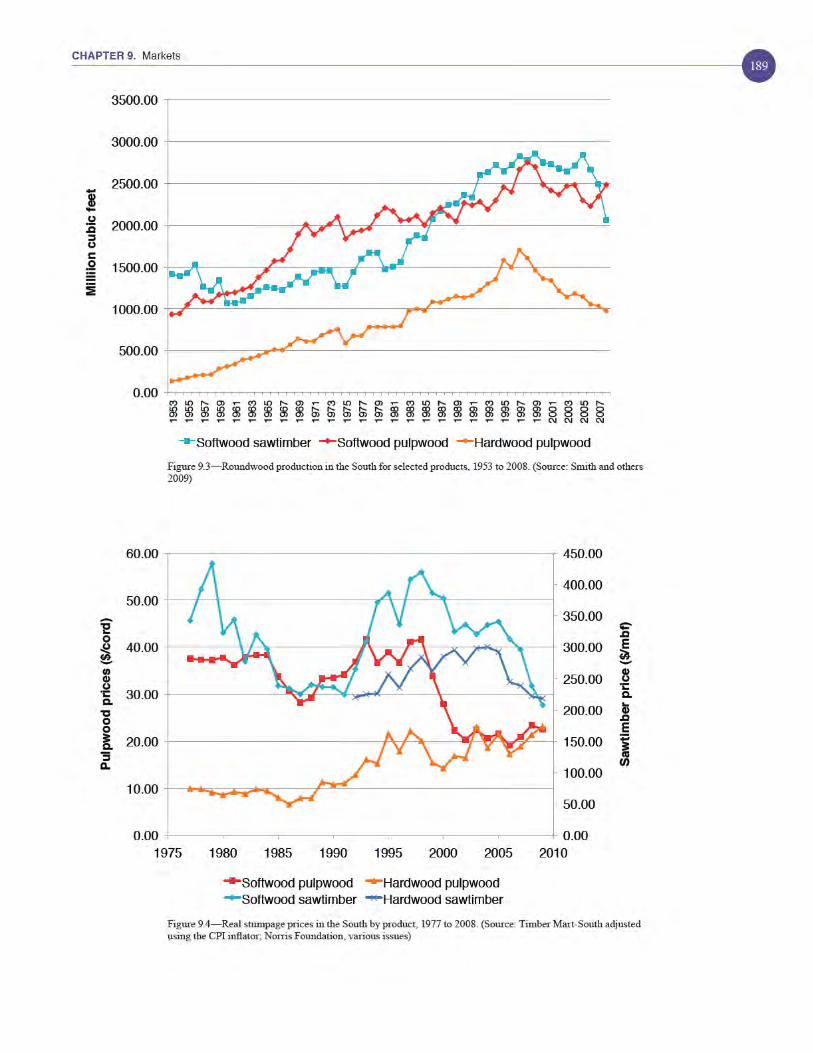

LookingjointlyatpriceandharvestchangesforthethreelargestproductclassesintheSouth(fig.9.5),wecandefinethreedistinctperiodsofdevelopmentfrom1977to2008.

Moderate growth phase (1977 to 1986)—Duringthisperiod,harvestsofallproductsincreasedatamoderateratewhiletimberpricesstayedconstantorevendeclinedforallthreeofthemajorproducts.Thesetrendsareconsistentwithexpansionofbothsupplyanddemandfortheproducts—thatis,forestinvestmentsgeneratedadditionalwoodsupplyandkeptpricesfromincreasingwithoutput.

Rapid growth phase (1986 to 1998)—Duringthisperiod,harvestsofhardwoodpulpwood,softwoodpulpwood,andsoftwoodsawtimbercontinuedtoincreasebutatfasterratesthantheearlierperiod.Pricesfortheseproductsalsoincreased,andatahigherratethanforharvests.Thispatternisconsistentwithastrongexpansionintimberdemandbutdoesnotprovideconclusiveevidenceofchangeintimbersupply.Itisconsistent,however,withdemandexpandingfasterthansupply.Incontrast,productionwasstablebutpriceincreasedforhardwoodsawtimber,signalingatighteningofhardwoodsawlogsupply.

Adjustment phase (1998 to 2009)—Followingtheproductionpeakson1997through1998,fundamentalchangesinoutputandpricetrendssuggestimportantchangesintimbermarkets.Forhardwoodpulpwood,pricesinitiallyfellandthenincreasedagainfrom2001to2009,andharvestsdeclinedsteadilythroughouttheperiod,fallingbyabout60percent.Fallingoutputwithincreasingpricesindicatesacontractioninsupplyforhardwoodpulpwoodovertheperiod,irrespectiveofdemandchanges.Forsoftwoodpulpwood,harvestsfellabout7percentfrom1997to2000,andthenstabilized,butpricesfellbyabout50percentbetween1998and2001andhaveremainedatthislevelthrough2009.Decreasingpriceswithastableoutputisconsistentwithastrongexpansioninthesupplyofsoftwoodpulpwood.Forsoftwoodsawtimber,simultaneousdeclinesinharvestandpricesindicatethatmarketsweredominatedbyacontractionofdemandfrom2005to2009,coincidentwithstrongdeclinesinthedemandforU.S.housingconstruction.

Demand Trends for Pulp and Paper Products

Forseveraldecades,theUnitedStateshasproducedmorewoodpulpthananyothernation.In2006,hardwoodandsoftwoodpulpwoodmadeup36percentofthetimberconsumedintheSouth.Theregion’spapermillsareconcentratedinthefewareaswhereplentifulwateris

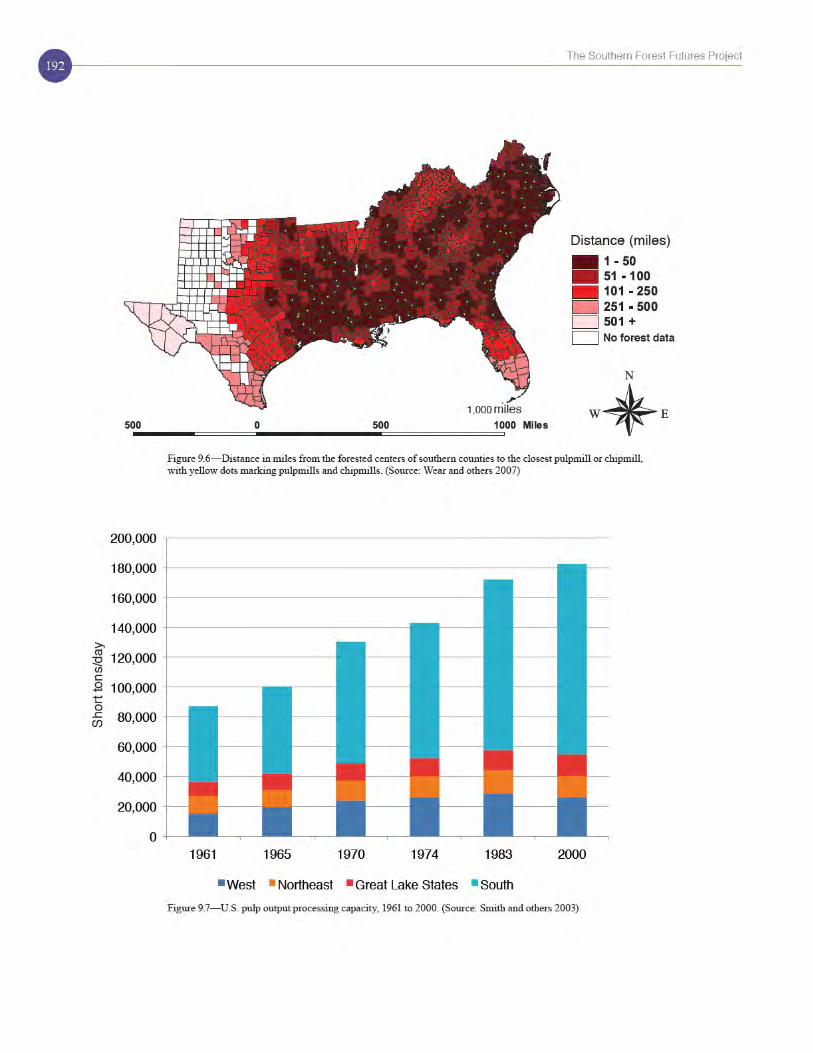

available.TheseareasincludesoutheasternGeorgia,northeasternFlorida,andsouthernAlabamaandMississippi.ConcentrationofpaperproductioncapacityorganizesthedemandforpulpwoodwithintheSouth:demandforpulpwoodisstrongestinthevicinityofmillsandweakenswithdistancefromthemillgate(fig.9.6).Althoughsatellitechipmillsdistributedthedemandforpulpwoodoverawiderareainthe1990s,pulpwoodmarketsarestillmuchmoreconcentratedgeographicallythanaremarketsforsolidwood.

Therawmaterialforproductionofpaperproductscomesfrompulpwood-gradetrees,fromwoodproductmanufacturingresiduals,andincreasinglyfromrecycledfiber.Ince(2000)showsthatrecycledmaterialcomprised37.9percentofU.S.paperproductsin1998,upfrom23.9percentin1985.Thishasresultedinadropinthedemandforvirginwoodfiber.TheamountofrecycledmaterialusedinU.S.papermanufacturingmayhavereachedamaximum,especiallygivenstrongexportdemandforrecoveredpaper.Soitislikelythatexpandinguseofrecycledmaterialmitigateddemandandpriceincreasesduringtherapidgrowthphase(1986to1998),butthatchangesindemandforrecycledmaterialhavenotbeenamajorinfluenceintheadjustmentphase(since1998).

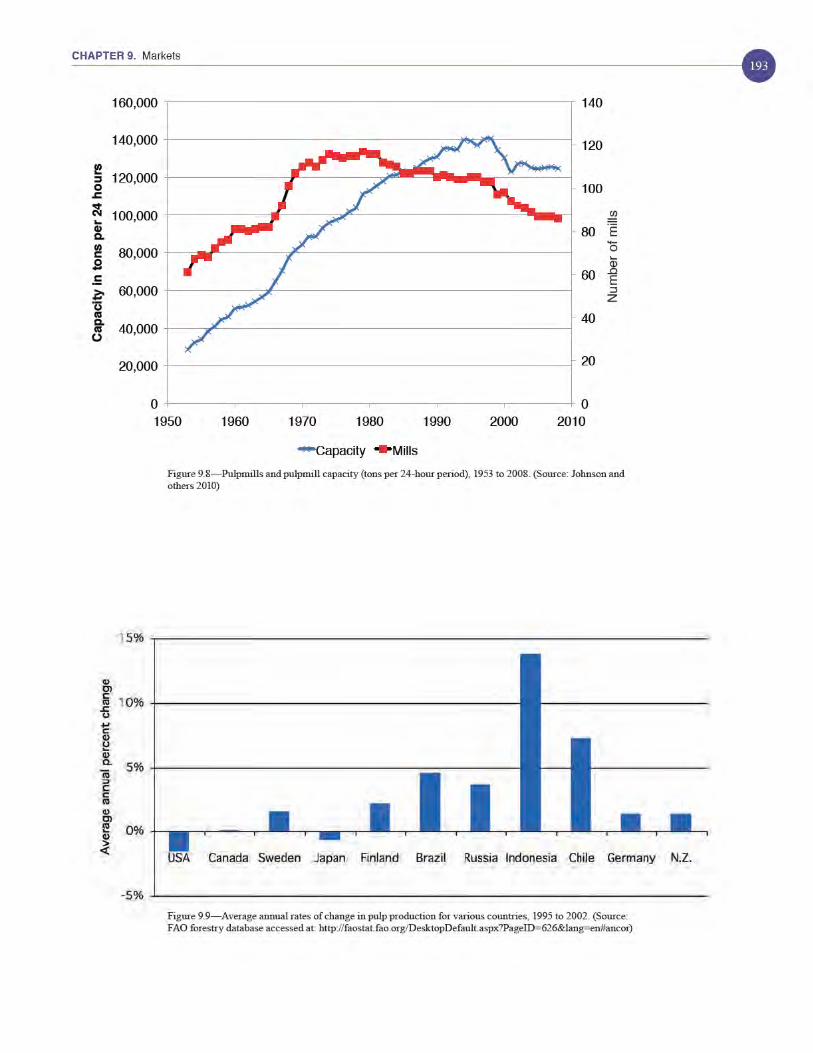

Pulpingcapacitywithintheregiondefinestheupperlimitforpulpwooddemand,atleastintheshortrun.Becauseexpandingcapacitythroughconstructionrequiresalargecommitmentofcapital(typicallyinthe$2billionrange),trendsincapacityprovideastrongindicatorofcurrentandanticipateddemandforpulpwood.Through1998,bothU.S.andsouthernpulpmillcapacitytrendedupward(fig.9.7).Sincethen,U.S.capacityhasdecreasedonlyslightly,whileSoutherncapacitydecreasedby16percentbeforestabilizingin2003(fig.9.8).Therateofdecreaseinsoutherncapacitywasmuchlowerthandecreasesinthenumberofpapermills,reflectinganincreasedconcentrationofproductioninremainingplants.

AccompanyingthesedeclinesindomesticcapacitywasanexpansionincapacitybyothercountriessuchaSweden,Finland,Chile,andBrazil(fig.9.9).AlthoughtheUnitedStatesandtheSouthcontinuetoleadinpulpwoodproduction,theirshareofworldwidecapacityhasdeclinedsince1991.By2003,pulpcapacityintheSouthhadreturnedtoits1985level(wellshortofthe1998level),whereitremainedthrough2008.

Newpulpmillcapacityandpulpproductionisfeedingincreasedworldwide(andespeciallyAsian)demandforpaperproducts.Withlevel-to-decliningcapacityintheUnitedStates,itisclearthatthenewcapacityisbeingdevelopedelsewhere.Thesechangesarelikelyexplainedbyshiftsincomparativeadvantageresultingfromseveralfactors,includinglaborcosts,rawmaterialscosts,andproximityto

194The Southern Forest Futures Project

finalproductmarkets,whichcontrolstransportationcosts.OthercontributingfactorsincludetheshrinkageofU.S.manufacturing,whichrequirespaperforpackaging,andthedemandforpulpwoodinproductslikeorientedstrandboard.

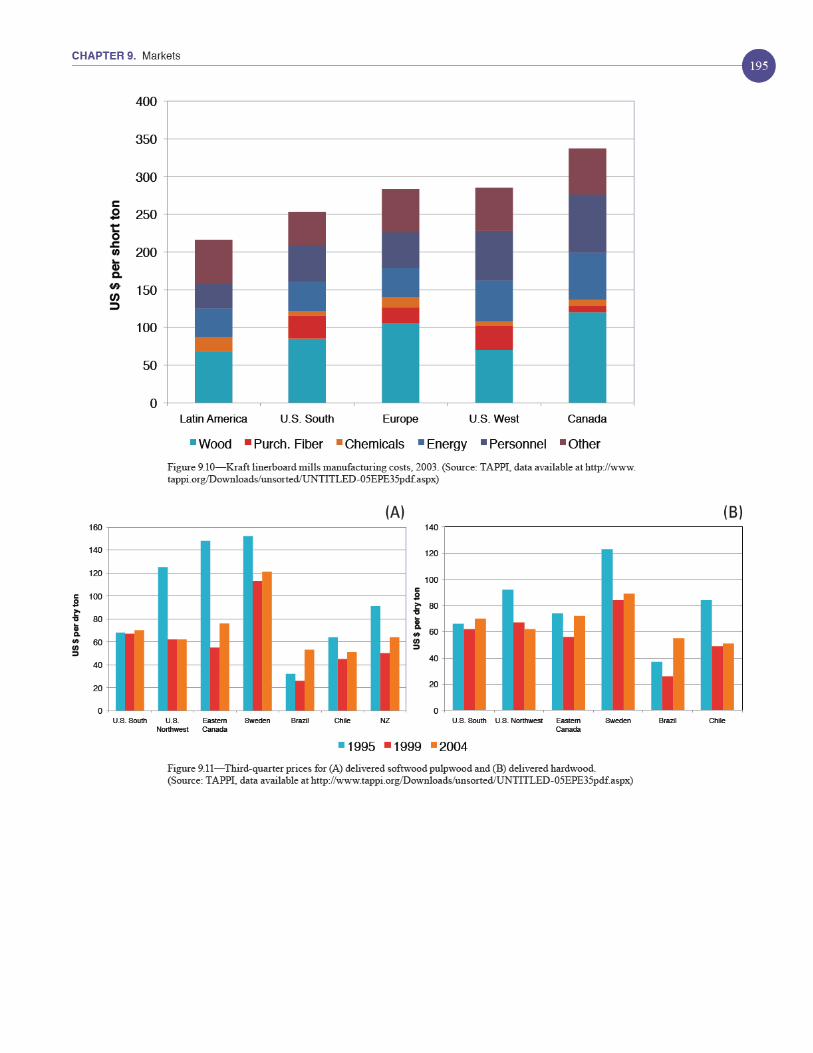

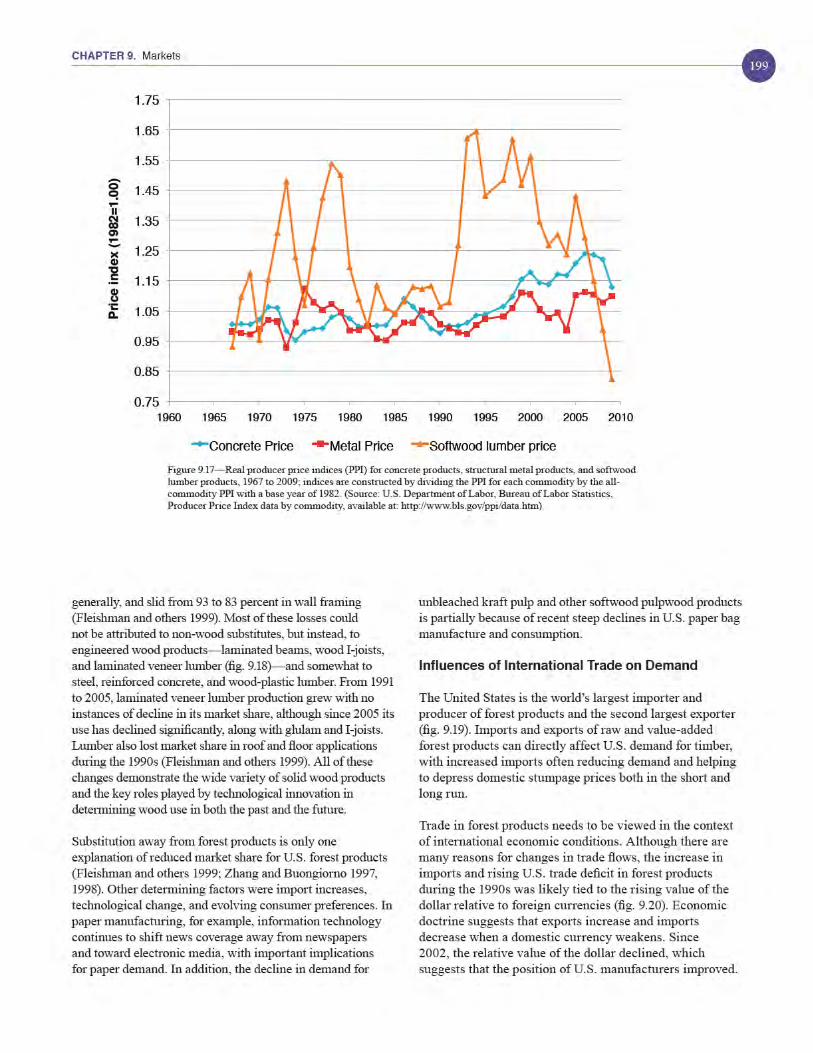

Manufacturingcostsforkraftlinerboard(fig.9.10)provideanexampleofdifferencesincomparativeadvantageamongregionsandcountries.TheSouthiscompetitiveinthismarketcomparedtotheWesternUnitedStates,Canada,andEurope,butitscoststructurelagsbehindLatinAmericancountries(primarilyBrazilandChile),mainlybecausefiberandlaborcostsaresignificantlylowerinlessindustrializedcountries.TheSouthretainscomparativeadvantagebecauseofitsproximitytoU.S.demandcenters(therebyloweringtransportationcosts),butlaborandwoodcostdifferentialsmakeLatinAmericanproducersviablecompetitors.

In1995,1999,and2004,bothBrazilianandChileanproducerscoulddeliversoftwoodandhardwood(mostlyEucalyptus)pulpwoodtomillsatsubstantiallylowercostthanproducersintheSouth(fig.9.11).In2004,deliveredsouthernsoftwoodpulpwoodwas24percenthigherthaninBrazil(21percentforhardwoodpulpwood)and27percenthigherthaninChile(27percentforhardwoodpulpwood).Pricedifferentialsarenotstatichowever,andpricesinBrazilandChilehaverisensince1999.Thecomparativeadvantageheldbythesenationswoulddecreaseifthistrendweretocontinue.

Demand Trends for Solid Wood Products

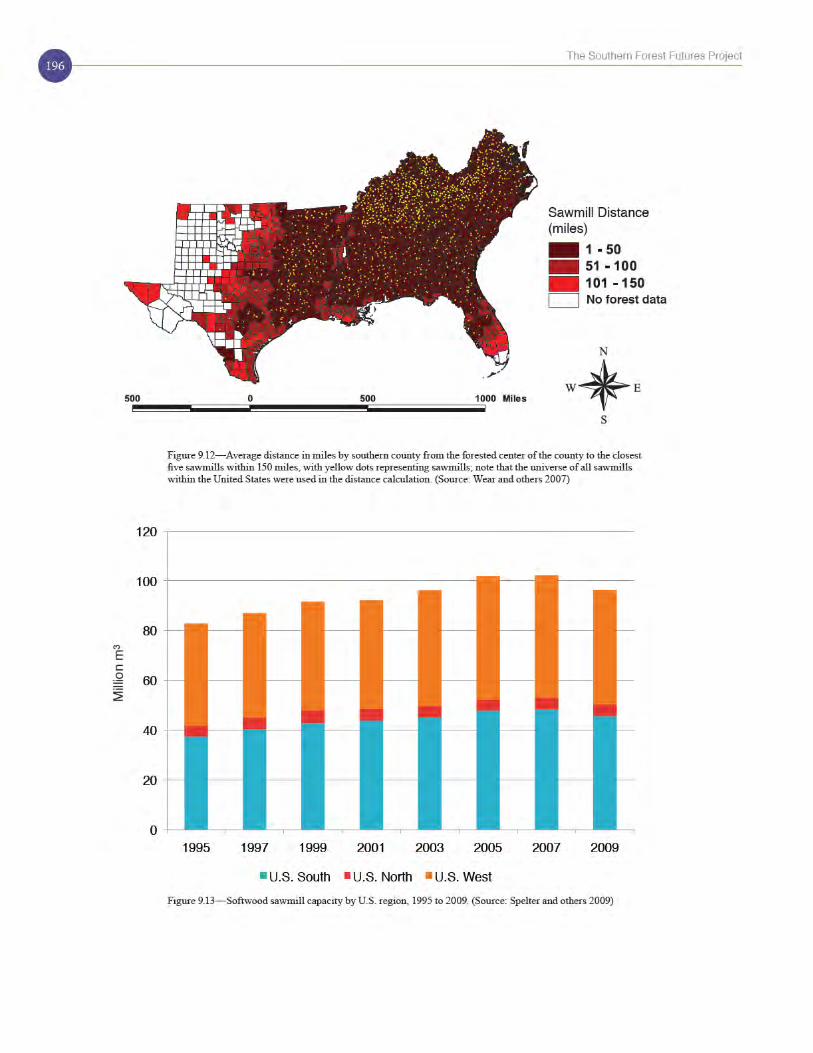

ThelargemajorityofthesolidwoodproducedintheSouthgoesintolumberandpanelproducts,comprisingabout52percentin2006.Theregion’slumbermills,unlikeitspulpandpapermills,arewidelydispersed(fig.9.12).Southernsoftwoodsawmillcapacitygrewsteadilyfrom1995to2005andthendeclinedslightlythrough2009(Spelterandothers2009),mirroringastrongdeclineinlumberproductionassociatedwiththedeclineinU.S.housingconstruction(fig.9.13).ComparabledataarenotavailableforhardwoodlumbercapacityintheSouth.

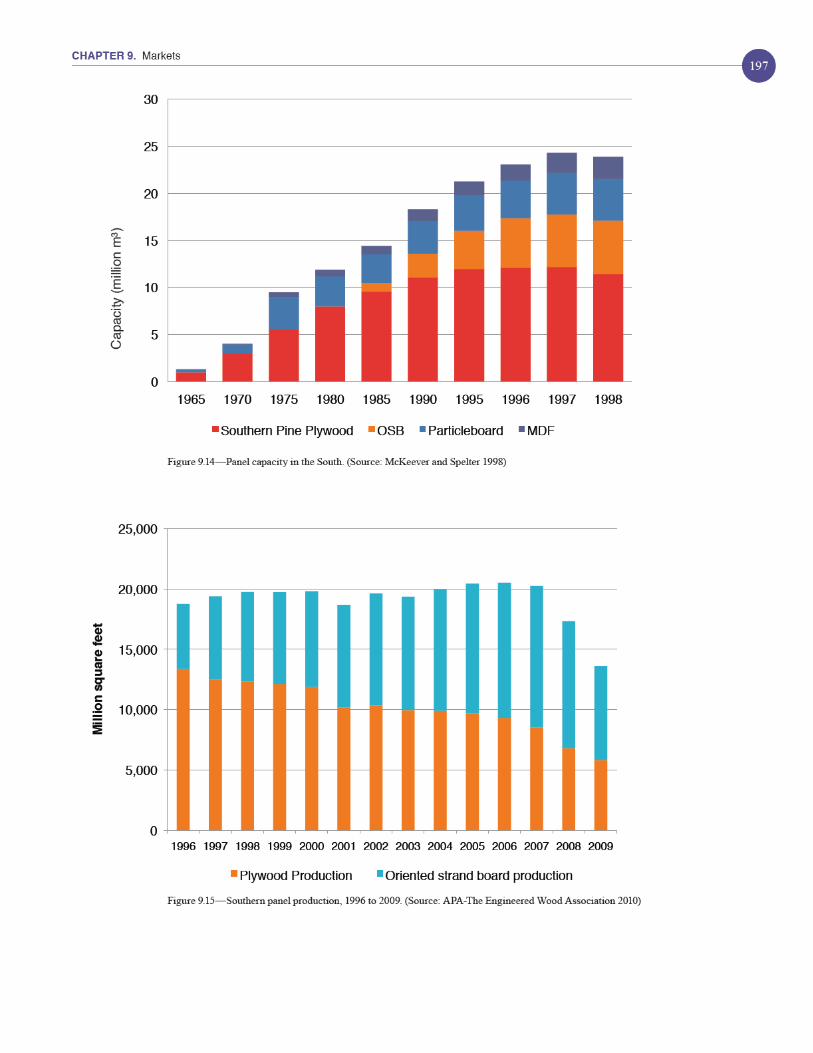

McKeeverandSpelter(1998)reportthatsouthernpanelcapacityexpandedsignificantlyinthe1990s(fig.9.14).From1998to2009,orientedstrandboardcapacitynearlydoubled(APA-TheEngineeredWoodAssociation2010)from7,900to13,840squarefeet(3/8-inchbasis),representing81percentoftotalU.S.capacity.Incontrast,southernpineplywood,whichdominatedpanelproductionthroughthe1970s,peakedinthe1990sandhassincedeclined(APA-TheEngineeredWoodAssociation2010).Atthe1996peak,plywoodcapacitywas14,530millionsquarefeet(3/8-inchbasis)butfellto9,190squarefeetby2009(APA-TheEngineeredWoodAssociation2010).Capacityformediumdensityfiberboardproductiongrewstronglythroughthe1990s.

Morerecentdataindicatethatalthoughsouthernpanelproductionremainedstablefrom1996to2007andfellprecipitouslyin2008/2009becauseofthe2007recessionandhousingmarketcollapse,orientedstrandboardasashareofproductionhascontinuedtogrow(fig.9.15).Expandingorientedstrandboardcapacitycoupledwithdecliningplywoodcapacitysuggestsincreasingdemandforlessexpensive,small-diametertimber,especiallywhencomparedtotheveneerlogsusedinplywoodproduction.

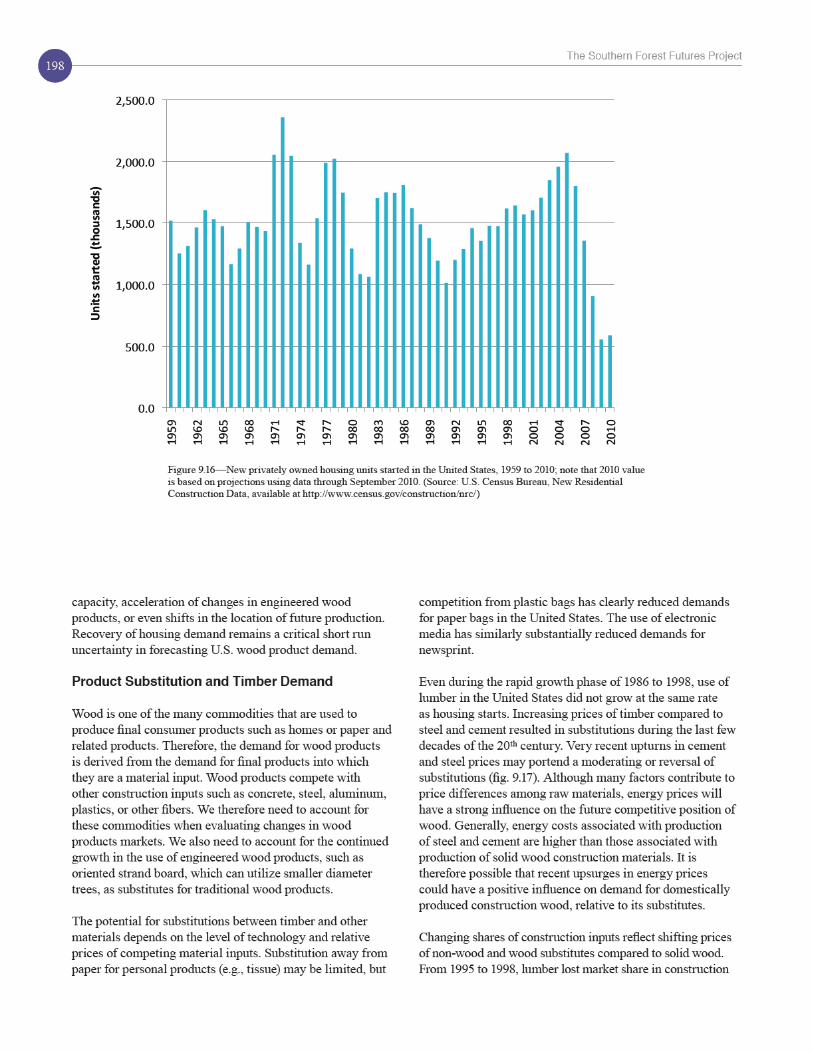

Unlikethedemandforpaperproducts,whichismostclearlylinkedtogenerallevelsofeconomicactivity,notablymanufacturingactivity,demandforsolidwoodproductsisstronglylinkedtotheconstructionindustry.Housingstartsinparticularprovideastrongcorrelatetotheconsumptionofsolidwoodproducts,andrecenteconomicdevelopmentsareastrongreminderthatthehousingmarketiscyclical.Peaksinhousingstartsintheearly1970s,inthelate1970s,inthemid-1980s,andin2006haveallbeensucceededbyrapiddeclinesofatleast30percent(fig.9.16),withthesecyclescenteringonabaselevelofabout1.5millionunitsperyear.Withinthiscontext,themostrecentdeclineandcontinuingstagnationofhousingmarketsisunprecedented.Afterexceeding2millionunitsin2005,housingstartsfellto554,000unitsin2009and(asprojected)619,000unitsin2010(fig.9.16),comparedtolowsthathadnotdippedbelow1millionfrom1959to2007.

TheCongressionalBudgetOfficehasconstructedalternativeforecastsofconstructionactivityrecoveryfromthecurrenthousingtroughthatincorporateexistinghousingstocks,populationgrowth,householdformation,depreciation,andemployment.Theforecastspredictedthathousingstartscouldreturntobetween1.2and1.5millionunitsby2012(CongressionalBudgetOffice2008),atrendthatlongertermforecastspredictedwouldcontinue.Fromtheperspectiveofalongrunanalysis,thisforecastedstabilitysuggestsrecoveryandsubsequentstabilityindemandforsolidwoodproductsusedinconstruction.Inaddition,theexpansionintheoverallnumberandageofexistingresidencesmaybringincreasedupkeepandrepairs,stimulatingagradualexpansionindemandforwood.

MorerecentdataindicatethattherecoveryofconstructionactivityprojectedbytheCongressionalBudgetOfficehasyettoberealized.InMarch2011,theU.S.CensusBureau(2011)estimatednewprivatehousingstartsataseasonallyadjusted479,000units,considerablylowerthanthehousingstartsrecordedin2009and2010.Thetime-pathofarecoveryinhousinginfluencesthefutureofsolidwoodproductsdemand.Withasustainedsuppressionofhousingdemand,solidwoodprocessingwouldlikelyshrink,eventuallyresultinginstructuralchangesinthesemarkets.Althoughnecessarilydifficulttopredict,theimplicationsofsustainedsuppressionmightincludesustaineddeclinesinproduction

203chAPTeR 9. Markets

definesaceilingfordomestichardwoodstumpagepricesincertainareasoftheSouth.

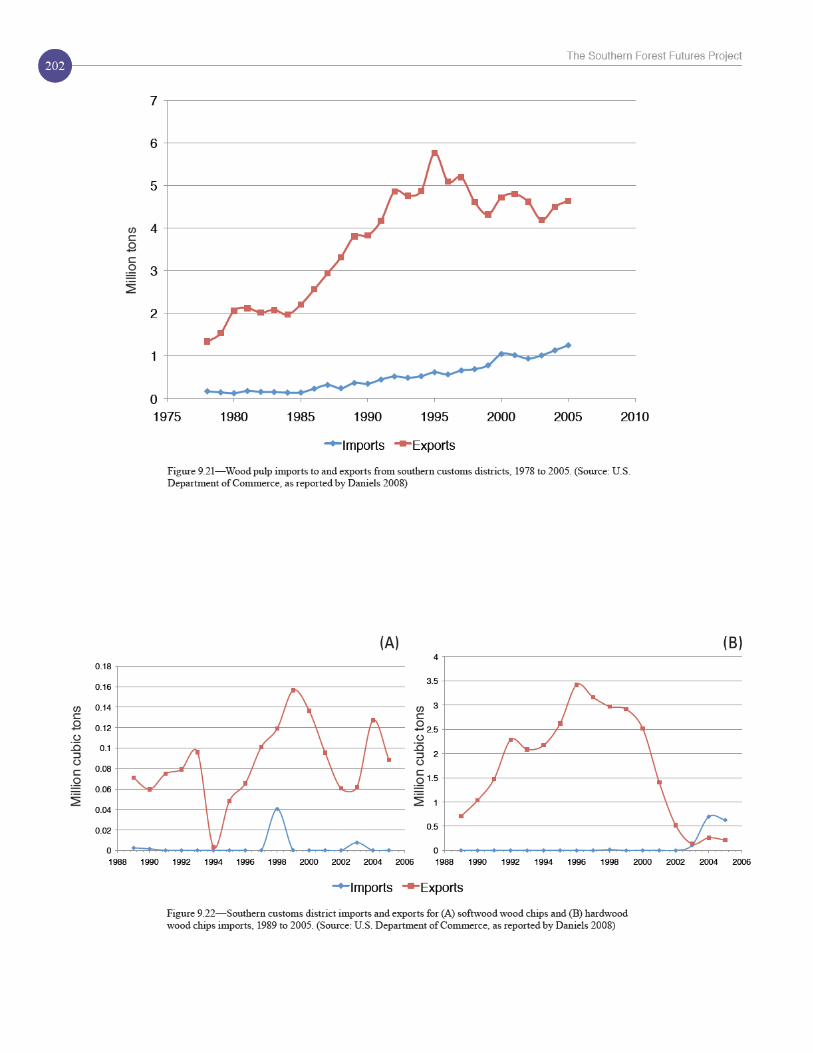

Fromthebeginningofthedataseries(1989)to2002,theUnitedStateshashadalargetradesurplusinwoodchips(fig.9.22)—withexportsfarexceedingimports.Since1999,however,thetradesurplushasfallensteadily,fromaround3milliontonsinthemid-1990stolessthan0.1milliontonsin2003.From1991to2002,nearlyallofthewoodchipsexportedfromU.S.southernportswereshippedtoJapan.

By2002,chipexportsfromsouthernportsessentiallyceased.In2003,thereductioninsouthernchipexports—primarilyhardwoodchips—toJapanwasequivalentto5percentoftotalsouthernpulpwoodproductionandnearly16percentofsouthernhardwoodpulpwoodproduction.WithmostofthetradeinwoodchipsmovingthroughMobile,wemightexpecttheeconomicimpactsofreduceddemandtobestrongestinAlabamaandtodeclineinanoutwardradiatingpattern.

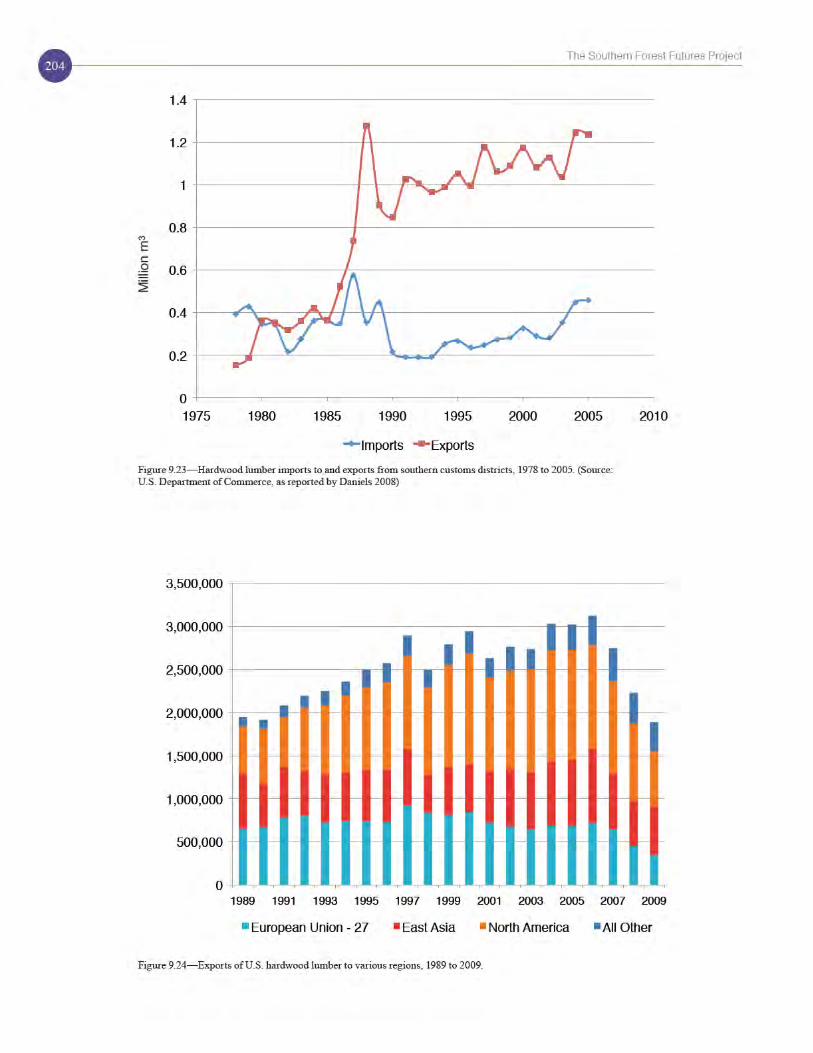

Lumber—Sincethelate1980s,theUnitedStateshasbeenalargenetimporterofsoftwoodlumber,primarilyfromCanada(fig.9.23).LumberimportsfromSouthAmerica,althoughrelativelysmallfrom1989to2004,havebeenrisingsteadily.AlthoughtheUnitedStatesexportssomelumber,thebalanceoftradefavorsimports,andthetradedeficitisgrowing.

ImportsoflumberfromCanadahaveanimportantinfluenceonallU.S.timbermarkets,buttheeffectsonsouthernmarketsarelikelytobeindirect.LumberfromWesternCanadamoredirectlysubstitutesforlumberofspeciesthatgrowintheWesternUnitedStates(Nagubadiandothers2004),andimportsaregenerallynotdirectlysubstitutableforthetreatedlumberproducedintheSouth.

In2004,theUnitedStatesledallothertemperatecountriesinproducing(60percent)andconsuming(52percent)hardwoodlumber,withabout8percentofdomesticproductionexported.Hardwoodlumberisamuchmoreheterogeneouscommoditythansoftwoodlumber,soitsproductionandtradeservesawidevarietyofenduses—fromflooringtofurnituretoshippingpallets—andaggregatedataprovideonlyaverygeneraldescriptionoftrends.Notethatabout10percentofU.S.hardwoodexportsarefromthePacificNorthwest(especiallyredalder)comparedtoabout90percentfromtheEasternUnitedStates.

ExportsofhardwoodlumberfromtheSouthincreasedfromabout0.4millionm3in1989tojustover1.2millionm3in2004(fig.9.23)—mostlytootherNorthAmericancountries,followedbyEastAsiaandthe27countriesoftheEuropeanUnion(seefig.9.24),andwithabout10percentgoingtoallothercountriescombined.Thedistributionofexports

amongthesedestinationshaschangedsomewhatsince1989,withshipmentstoEuropedecliningandshipmentstootherCanadaandMexicoincreasingsubstantially(fig.9.24).ShipmentstoEastAsiahavebeenessentiallyconstantinaggregate,withachangingmixofindividualcountrydestinationsandlargeincreasesinshipmentstoChinaoffsetbydecreasesinshipmentstootherAsiancountries.The2007recessionledtoastrongdeclineintotalhardwoodexportswiththedistributionamongdestinationsremainingrelativelyconstant(fig.9.24).

Southernexportsofsoftwoodlumberhavebeenrelativelysmallandhavedeclinedoverthelastdecade(fig.9.25),fallingtoaboutathirdof1992levelsin2004andnowrepresentingonly1to2percentoftotalproduction.

Panels—Tradeinpanelproductsisweightedtowardimports,withabout15percentofplywoodconsumptionand38percentoforientedstrandboardconsumptionimportedfromCanadaandothercountriesin1999(Spelter2001).Particleboard,waferboard,andorientedstrandboardimportsfromCanadagrewstronglythroughthemid-2000s,increasingfrom$1.53billionin1999to$3.16billionin2004,beforedecreasingsubstantiallyattheendofthedecade(APA-TheEngineeredWoodAssociation2010)U.S.exportsofpanelscannotbeconsiderednegligible,althoughtheyaresubstantiallylowerthanimports.Forexample,in2009,plywoodexportswere482millionsquarefeet(3/8-inchbasis)comparedto616millionsquarefeetforimports.Orientedstrandboardtradehasbeensignificantlymoreimbalanced,tiltedtowardimports(APA-TheEngineeredWoodAssociation2010).

Orientedstrandboardmarketsexpandedthroughthemid-2000s.NorthAmericawilllikelycontinuetodominateWorldproductioninthiscommodityclass,butthetradebalancewithinNorthAmerica—especiallybetweenCanadaandtheUnitedStates—couldchangewithmarketexpansion.Inaddition,adeclineindemandforsouthernpulpwoodcouldofferacompetitivemill-sitingadvantagetoU.S.manufacturers.

Overall,weseenodramaticchangeininternationalmarketsthatwouldstronglyaffectsoutherntimberdemandintheshortrun.Atthenationallevel,thevalueofwoodproductsimportsexceedsexportssothewoodproductsbalanceoftradeisnegative.Forsouthernports,thewoodproductsbalanceoftradeispositive,butasmallshareoftotalproduction.

Timber Supply Trends

Overall,changesduringtheadjustmentphase(1997to2009)indicatesomeimportantchangesinsupply.Anexpandedsupplyofsoftwoodpulpwoodtimbercoupledwith

211chAPTeR 9. Markets

forestsstillinproductionbutwithaverydifferentsetofowners.Forecastsoftheimpactsofthisownershipchangeoninvestmentcanonlybespeculativeatthispoint,butwillplayanimportantpartindeterminingfuturesupply.

Forecastsofsupplyindicateasubstantialexpansioninsoftwoodsupplyoverthenextdecadeasnewpineplantationsmature.Thisportendscontinuedlowpricesforsoftwoodproducts,especiallysoftwoodpulpwood.Beyond2020,supplydependsonamuchlowerrateofexpansioninforestplantations—generallytherateofplantingharvestedforestsisassumedtobeabouthalfofwhatitwasinthe1990s.Evenattheseloweredlevels,thesupplyoftimberwouldgrowandthepriceofproductswouldgenerallydeclineifdemanddoesnotgrowoverthenextdecades.Whilesupplygrowthcouldalsobeaffectedbypolicychangesaffectingfuturemanagementoptions—e.g.,potentialrestrictionsontheuseofherbicidesforsitepreparation—ouranalysisfocusesonafuturewithnosubstantialchangesinpolicyenvironment.Policychangescouldleadtodifferentoutcomes.

GrowthinharvestingcanbesupportedbytheforestlandoftheSouth.Areturnto1990sdemandlevelswouldresultinapricestabilizationforsoftwoodpulpwoodpricesandanincreaseoflessthan1percentperyearforsoftwoodsawtimberandhardwoodpulpwood,aswellasanincreaseintotaloutputofabout40percentfrom2006to2055.If,inaddition,productivityinpineplantationsgrowsby50percent,thenoutputcouldincreaseevenmoresubstantially—upto70percentforsoftwoodpulpwood.

Demandisperhapsthemostcrucialuncertaintyinthisanalysis.Currentdemandissuppressedbytheunprecedentedfallinhousingconstructionin2008,andbylongrunphenomena,suchasthedeclineinpaperproductioncapacityintheSouthinlinewithbroadereconomy-wideshiftsthatareimpactingthetimberproductsindustryandglobalcapacityshifts.Recoveryfromthe2007recessionwillstronglyaffectthecourseoffuturedemand,butpolicydevelopmentsmayalsoplayarole.IncentivesforusingrenewablebiomassinvariousbioenergyoperationscouldprovideapotentiallylargenewdemandfortimberproductsintheSouth(chapter10).

Whatisclearfromouranalysisisthat,absentrenewedgrowthindemandfortraditionalsouthernforestproducts,productiongrowthcouldbesustainedinsupportofnewmarketswithoutsubstantialincreasesontimberprices,althoughregionalstabilitycouldcoincidewithimportantscarcitiesinlocaltimbermarkets,forexampleifsomeindividualStatesdeveloptheirownRenewablePortfolioStandards.Thequestionthatremainsis,“Howmuch?”Withoutproductivitygains,thelargestprojectionsofdemandforwood-basedbioenergyproducts(understrongeconomicandmoderatepopulationgrowthprojections

ofCornerstonesAandB,andtheA1Bstorylineinthe2010RPAAssessment)outlinedbytheU.S.DepartmentofEnergyanddescribedinchapter10wouldleadtolargepriceincreases(asmuchas400percentby2055).Withthe50-percentproductivitygrowthforplantations,thisdemandcouldmorereadilybeaccommodatedwithoutstrongpriceincreases,evenwithexistingindustriesconsumingtheircurrentlevelsoftimberproducts.UndertheExpandingDemandscenarioandholdingpulpwoodconsumptionforexistingindustriesat2006levels,anadditional2.4billioncubicfeetor36.6milliongreentonsperyearofsoftwoodpulpwoodharvestingareforecastedfor2055.CombiningEnhancedProductivitytotheabovescenariowouldincreasesoftwoodpulpwoodharvestingto3.7billioncubicfeetor57.9milliongreentonsperyear.

Insummary,theSouthhasthecapacitytoexpandproductionwellintothiscentury,butdemandforforestproductsseemstobealimitingfactor.Timbersupplyhascontinuedtogrowwhiledemandhasslackenedoverthepastdecade,inducingdisinvestmentinpulpandpapermanufacturingandslowerinvestmentinotherwoodproductsbytheforestproductsindustry.Giventhisreality,thefutureoftimbermarketswilllargelybedeterminedbydemandgrowththatwouldemergeprimarilyfromtherequirementsofforestfiberinputstosupplybio-basedenergy.

kNoWleDGe AND iNFoRmATioN GAPS

Ourmarketmodelsarebased,totheextentpossible,onempiricalmodelsofbiologicalchangesandmanagementbehavior.Oneareawhereempiricalmodelshavenotprovedsufficientisinforestinvestments.Betterinformationonhowvariousownerandinvestorgroupsadjusttheirmanagementplans,particularlybyexpandingtreeplantinginresponsetomarketsignals,couldreducetheuncertaintyofmarketprojections.Bettermodelsofthedemandforfinalwoodproductsandtimberinputstotheirproductioncouldalsoimprovemarketprojections.

Changeintheownershipofforestsisanotherkeysourceofuncertainty.Giventheinformationathand,weassumethatthemanagementobjectivesandmanagementmodelsoftimberinvestmentmanagementorganizationsaresimilartothoseoftheverticallyintegratedforestproductscompaniesthattheyhavereplacedoverthepast10years(chapter6).Littleisknownaboutthebroaderimplicationsofthesechangesinownershipandassociatedchangesinmanagementstrategiesforthelandthathasbeentransferred.Forexample,theproductivityofplantedforestsderivesfromothertreatments,includingfertilization,weedcontrol,andthinningwhichhavenotbeenmodeledhere.Wehaveassumedthatmanagementstrategieshavenotbeengreatlyimpactedbythesechanges,butthisremainsanuntestedhypothesis.

212The Southern Forest Futures Project

Pastattemptstomodelsoutherntimbermarketshavebeensuccessfulbecauseofthedominanceofprivateowners.Ourmodelsindicatethatforestharvestingcanbemodeledasafunctionofmarketsignalsandisthereforepredictable.However,animportantuncertaintymaywellbethedevelopmentofnewdemandsforbioenergyandbiofuelsthataredriven,notbymarkets,butbynewStateandFederalpolicies,whichareunknowableatthispoint.Inaddition,thespatialscopeofourmodelsaddressestheregion’stimbermarketsasoneentity,giventhecurrentdistributionofproductiondemandsandforestmanagementtypes.However,policiesattheStatelevel,especiallyStateRenewablePortfolioStandards,maycreatelocaldemandsthatcouldresultinlocalscarcitiesandaspatialrealignmentofproduction;thesewecannotaddresswithourmodels.

AckNoWleDGmeNTS

ThankstoShanLiu,SouthernResearchStation,U.S.DepartmentofAgricultureForestService;RuhongLi,DepartmentofForestryandManagement,UniversityofWisconsin,Madison;andRobertC.Abt,DepartmentofForestryandEnvironmentalResources,NorthCarolinaStateUniversity.

liTeRATuRe ciTeD

APA-theEngineeredWoodAssociation.2010.Structuralpaneland engineeredwoodyearbook.APAEconomicsReportE176.Tacoma,WA:AmericanPlywoodAssociation.80p.

CongressionalBudgetOffice.2008.Theoutlookforhousingstarts,2009to2012.BackgroundPaper.U.S.Congress,CongressionalBudgetOffice.23p.http://www.cbo.gov/ftpdocs/98xx/doc9885/11-17-HousingStarts.pdf.[Dateaccessed:October28,2010].

Daniels,J.M.2008.UnitedStatestradeinwoodproducts,1978–2005.Gen.Tech.Rep.PNW-GTR-738.Portland,OR:U.S.DepartmentofAgricultureForestService,PacificNorthwestResearchStation.124p.

Fleishman,S.J.;Eastin,I.L.;Shook,S.R.1999.Materialsubstitutiontrendsinresidentialconstruction,1995vs.1998.CenterforInternationalTradeinForestProductsWorkingPaperNumber73.Seattle:UniversityofWashington.76p.

Ince,P.2000.IndustrialwoodproductivityintheUnitedStates,1900-1998.Res.NoteFPL-RN-0272.Madison,WI:U.S.DepartmentofAgricultureForestService,ForestProductsLaboratory.14p.

Johnson,T.G.;Steppleton,C.D.2005.Southernpulpwoodproduction,2003.Resour.Bull.SRS-101.Asheville,NC:U.S.DepartmentofAgricultureForestService,SouthernResearchStation.38p.

Johnson,T.G.;Steppleton,C.D.;Bentley,J.W.2010.Southernpulpwoodproduction,2008.Resour.Bull.SRS–165.Asheville,NC:U.S.DepartmentofAgricultureForestService,SouthernResearchStation.42p.

McKeand,S.;Mullin,T.;Byram,T.;White,T.2003.Deploymentof geneticallyimprovedloblollyandslashpinesintheSouth.JournalofForestry.101(3):32-37.

McKeever,T.;Spelter,H.1998.Wood-basedpanelplantlocationsandtimberavailabilityinselectedU.S.States.Gen.Tech.Rep.FPL-GTR-103.Madison,WI:U.S.DepartmentofAgricultureForestService,ForestProductsLaboratory.53p.

Nagubadi,R.;Zhang,D.;Prestemon,J.;Wear,D.N.2004.SoftwoodlumberproductsintheUnitedStates:substitutes,complements,orunrelated?ForestScience.50(4):416-426.

NorrisFoundation.1977–present.TimberMart-SouthStateTimberPriceReports.CenterforForestBusiness,WarnellSchoolofForestryandNaturalResources,UniversityofGeorgia,Athens,GA.

Poylakov,M.;Wear,D.N.;Huggett,R.2010.Harvestchoiceandtimbersupplymodelsforforestforecasting.ForestScience.56(4):344-355.

Smith,B.R.;Rice,R.W.;Ince,P.J.2003.PulpcapacityintheUnitedStates,2000.Gen.Tech.Rep.FPL–GTR–139.Madison,WI:U.S.DepartmentofAgricultureForestService,ForestProductsLaboratory.23p.

Smith,W.B.;Miles,P.D.;Perry,C.H.;Pugh,S.A.2009.ForestresourcesoftheUnitedStates,2007.Gen.Tech.Rep.WO-78.Washington,DC:U.S.DepartmentofAgricultureForestService.336p.

Smith,W.B.;Miles,P.D.;Vissage,J.S.;Pugh,S.A.2004.ForestresourcesoftheUnitedStates,2002.Gen.Tech.Rep.NC-241.St.Paul,MN:U.S.DepartmentofAgricultureForestService,NorthCentralResearchStation.137p.

Smith,W.B.;Vissage,J.S.;Darr,D.R.;Sheffield,R.M.2001.ForestresourcesoftheUnitedStates,1997.Gen.Tech.Rep.NC-219.St.Paul,MN:U.S.DepartmentofAgricultureForestService,NorthCentralResearchStation.190p.

Spelter,H.2001.Wood-basedpanels—supply,tradeandconsumption.In:ECE/FAOForestProductsAnnualMarketReview1999-2000:113-130.Chapter10.

Spelter,H.;McKeever,D.;Toth,D.2009.Profile2009:softwoodsawmillsintheUnitedStatesandCanada.Res.Pap.FPL-RP-659.Madison,WI:U.S.DepartmentofAgricultureForestService,ForestProductsLaboratory.55p.

U.S.CensusBureau.2011.Pressrelease:newresidentialconstructioninFebruary2011.March16,2011.http://www.census.gov/const/www/newresconstindex.html.[Dateaccessed:April5,2011].

Uusivuori,J.;Buongiorno,J.1991.PassthroughofexchangeratesonpricesofforestproductexportsfromtheUnitedStatestoEuropeandJapan.ForestScience.37(3):931-948.

Wear,D.N.;Carter,D.R.;Prestemon,J.2007.TheU.S.South’stimbersectorin2005:aprospectiveanalysisofrecentchange.Gen.Tech.Rep.SRS-99.Asheville,NC:U.S.DepartmentofAgricultureForestService,SouthernResearchStation.29p.

Zhang,Y.;Buongiorno,J.1998.Paperorplastic?TheUnitedStates’demandforpaperandpaperboardpackaging.ScandinavianJournalofForestResearch.13:54-65.

Zhang,Y.;Buongiorno,J.1997.CommunicationmediaanddemandforprintingandpublishingpapersintheUnitedStates.ForestScience.43(3):362-377.