Embed Size (px)

Citation preview

149

Chapter 9

Rental Activities

Teaching Suggestions

Many students will find the vacation home rules to be the most difficult concept covered in the chapter. Tohelp them in understanding these rules, it might be useful for them to realize that these rules only affect dwellingunits that the taxpayer rents out part of the year and personally uses during other parts of the year. Once it hasbeen determined that the vacation rules may apply, it is necessary to determine whether the rental income istaxable. If the property was rented less than 15 days during the year, then the rental income is not taxable to thetaxpayer. If the property is rented more than 14 days during the year, then the rental income is taxable and thetaxpayer must allocate expenses between personal and rental use. This allocation is based on the ratio of thenumber of rental days to total days used during the year. Finally, students need to determine whether rentalexpenses are limited to rental income. This occurs if the dwelling unit meets the definition of a “residence,� whichis property that the taxpayer personally uses for the greater of (i) 14 days or (ii) 10% of the days rented during theyear.

Solutions to Questions and Problems1. ¶901.01.

Taxpayer Amount Description

A $6,000 The taxpayer recognizes $6,000 as rental income. Both cash-method and accrual-method taxpayers recognize rent received in advance at the time of receipt. Asecurity deposit is not treated as income until the tenant forfeits it (for example,used as a final payment of rent).

B 3,600 The taxpayer reports 10 months’ rent at $300 per month, plus $600 of improvementspaid by the tenant.

C 0 If a personal residence is rented for less than 15 days during the year, none of therent received is included in gross income.

2. ¶901.02.

Taxpayer Amount Description

A $1,0251 Expenses on property rented to a friend at $100 per month and to an unrelated partyat $275 per month.

B 02 Expenses on personal dwelling rented 12 days.

1 When property is rented to a friend for less than fair rental value, the days count as personal days. Thus,the property qualifies as a residence. The taxpayer can deduct expenses only to the extent of the rentalincome.

2 If a dwelling is rented for less than 15 days during a taxable year, the rental income is not taxable and norental expenses are deductible (other than interest and taxes on Schedule A).

Chapter 9

150 Essentials of Federal Income Taxation

3. ¶901.03.

a.

Depreciation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $4,000

Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2,000

Interest . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1,600

Utilities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1,200

Total . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $8,800

Rental portion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . × 50 %

$4,400

Repairs . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 500

Deductible rental expenses . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $4,900

b. Quinn deducts one-half of the taxes and interest as itemized deductions.

Taxes (1/2 × $2,000) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $1,000

Interest (1/2 × $1,600) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 800

Deductible on Schedule A . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $1,800

4. Being a cash-method taxpayer, Scott recognizes December’s rent in 2007 when she collects it. ¶901.

Rental income (11 months × $500) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $5,500

Less Expenses:

Utilities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $3,600

Depreciation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3,000

Insurance . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 600

Total . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $7,200

Rental portion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . × 50 %

$3,600

Maintenance and repairs . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 400 (4,000)

Net rental income . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $1,500

5. a.

Occupant Personal RentalDays Days

Danielle Haywood 13

Haywood’s sorority sister, who paid no rent 5

Haywood’s brother, who paid fair rental 21

Couple who won a charity auction (paid $2,000) 7

Unrelated persons, who paid rent of $5,000 50

46 50

Chapter 9 ©2007 CCH. All Rights Reserved.

151Textbook Solutions

b.

Rental income ($2,100 + $5,000) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $7,100

Less: Rental expenses

Mortgage interest ($6,700 × 50/96) . . . . . . . . . . . . . . . . . . . . . . . . . . . $3,490

Real estate taxes ($3,300 × 50/96) . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1,719 (5,209)

$1,891

Utilities and repairs ($2,540 × 50/96) . . . . . . . . . . . . . . . . . . . . . . . . . (1,323)

$ 568

Depreciation ($6,650 × 50/96) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ( 568)

Net rental income . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 0

Of the $3,464 rental portion of depreciate expense ($6,650 × 50/96), only $568 is deductible in 2007.The rest ($2,896) is carried over and added to 2008 depreciation expense. ¶902.02.

6. a. The cabin will be treated as a residence because the 16 days it was used for personal purposes exceedsthe greater of (1) 14 days or (2) 10% of the 92 days the cabin was rented at fair rental.

Allocation Ratio Summary of Days Used: Days

June-September . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 122

Not rented . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . (14 )

Personal use . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . (16 )

Days rented at fair rental . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 92

b. For purposes of allocating expenses, a day that the unit is rented at a fair rental price is treated as a dayof rental use. ¶902.02.

Personal use: 16/108 (Total days used = 122 − 14 = 108)

Rental use: 92/108

7. a. The personal use portion of real estate taxes can be taken as an itemized deduction regardless ofwhether or not the rental property is treated as a residence. However, the personal use portion ofmortgage interest can be deducted as an itemized deduction only if the rental property is treated as aresidence and the taxpayer selects it as the second residence.

b. If treated as a residence, deductible rental expenses from that property cannot exceed rental incomefrom that rental property.

8. See filled-in Schedule E for Barone. Barone carries over $120 of depreciation expense to 2008 ($4,000 ×90/150 = $2,400 − $2,280). ¶903.01.

Rental income . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $6,000

Less: (1) Interest and taxes (90/150 × $4,500) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . (2,700)

$3,300

(2) Utilities and maintenance (90/150 × $1,700) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . (1,020)

$2,280

(3) Depreciation (90/150 × $4,000), but limited to $2,280 . . . . . . . . . . . . . . . . . . . . . . . . . (2,280)

Net rental income . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 0

Chapter 9

152 Essentials of Federal Income Taxation

Filled-in Schedule E for Barone.

Chapter 9 ©2007 CCH. All Rights Reserved.

153Textbook Solutions

9.

a. The at-risk rules limit losses that can be deducted for certain activities to the taxpayer’s cashcontribution and investment in other property contributed to the activity, plus amounts borrowed foruse in the activity when the taxpayer is personally liable for payment. ¶905.

b. Generally, any activity that is carried on as a trade or business or for the production of income issubject to at-risk loss limitations. ¶905.

10. a. Most rental activities and other trade or business activities in which the taxpayer does not materiallyparticipate throughout the year are considered to be passive activities. ¶906.01.

b. It is material participation if the taxpayer is involved in the operation of the activity on a regular,continuous, and substantial basis. It is active participation (for rental activities only) as long as thetaxpayer participates in a significant and bona fide sense such as making management decisions orarranging for others to provide service.

The material participation test applies when determining whether a business activity is active or passivein nature. The active participation test is used to determine whether an owner of a rental real estateactivity qualifies for the special $25,000 rental loss deduction. The active participation test is much lessstringent than is the material participation test. ¶906.01.

c. These types of income are called portfolio income. Generally, such income may not be used to offsetpassive losses. ¶906.01.

11. a. The taxpayer works more than 500 hours in an activity that does not involve rental real estate. Thus,the material participation requirement has been met. ¶907.01.

b. The activity is a passive activity because the taxpayer’s hours working in a real estate trade or businessdo not exceed 750. However, 650 hours of participation could warrant active participation for purposesof the $25,000 special deduction. ¶907.01.

c. The taxpayer does not work more than 500 hours in the activity, therefore, he is not considered to be amaterial participant under the 500 hour rule. The taxpayer’s hours exceed 100, so if 150 hours is at leastas much as the participation of any other individual, including employees, then the taxpayer’sparticipation will be deemed to be material. If this is not the case, then perhaps one of the otherrequirements described in IRS Publication will apply. ¶906.01.

d. A husband and wife can pool their hours for activities that do not involve rental real estate. Thus, thecouple’s 550 hours exceed 500 hours. Therefore, the material participation requirement has been met.¶906.01.

e. A couple cannot pool their hours when the activity involves rental real estate. Since neither spouse’sparticipation exceed 750 hours, the material participation requirement for rental real estate has notbeen met. However, their participation could warrant active participation for purposes of the $25,000active participation special deduction. ¶907.01.

f. Although the wife’s hours exceed 750, her participation in real estate businesses is not more than 50%of the personal services she provides during the year. However, their participation might be activeparticipation for purposes of the $25,000 active participation special deduction. ¶907.01.

12. a. Of the $15,000 passive loss, $6,000 can be used to offset the $6,000 of passive income. ¶908.01.

b.

Activity Gross Income Deductions Income (Loss) Carryover Loss

A $12,000 $ 8,000 $ 4,000 0

B 20,000 32,000 (12,000 ) $(7,200 )1

C 3,000 6,000 (3,000 ) (1,800 )2

D 14,000 12,000 2,000 0

Totals $49,000 $58,000 $(9,000 ) $(9,000 )

Chapter 9

154 Essentials of Federal Income Taxation

1 $12,000/$15,000 × $9,000 = $7,200 (The ratio of $12,000/$15,000 represents the loss from Activity B inrelation to the combined loss from Activities B and C).

2 $3,000/$15,000 × $9,000 = $1,800.

The carryover loss allocated to each passive activity generating losses in order to determine how muchpassive loss can be recovered in subsequent periods when a passive activity is sold or otherwisedisposed of. ¶908.01.

13.

Activity a. b.

2 $(11,143)1 $ (2,357)3

3 (14,857)2 (3,143)4

1 $26,000 × ($13,500/($13,500 + $18,000)).2 $26,000 × ($18,000/($13,500 + $18,000)).3 $13,500 − $11,143 = $2,357.4 $18,000 − $14,857 = $3,143.

14. The Matthewses may deduct $10,000 of the loss on their tax return. The remaining $12,000 ($22,000 −$10,000) must be carried forward. ¶907.02.

AGI before loss consideration . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $130,000

Less: Amount not subject to phase-out . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . (100,000)

Amount subject to phase-out . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 30,000

Phase-out percentage . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . × 50 %

Reduction in allowable deduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 15,000

Maximum rental real estate deduction allowable . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 25,000

Less: Reduction in allowable deduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . (15,000)

Current year deduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 10,000

15. a. Southworth’s net loss from passive activities equals $31,000 [($10,000) + ($30,000) + $9,000]. Since thepassive activities all involve rental real estate in which Southworth actively participates, he is entitled todeduct up to $25,000 of the net loss against active and portfolio income. Southworth can deduct $25,000of this loss on his return since his AGI is less than $100,000.

b. The suspended loss is $6,000 ($31,000 − $25,000). Of this amount, $1,500 is allocated to Activity X[($10,000/$40,000) × $6,000]; $4,500 is allocated to Activity Y [($30,000/$40,000) × $6,000]. ¶907.02.

16. The loss carry forwards are added to the current year income (loss). This results in a $10,000 loss, a$40,000 loss and $20,000 income, for activities X, Y, and Z, respectively. Jefferson deducts $20,000 of thistotal $50,000 [$10,000 from X + $40,000 from Y] passive loss against activity Z’s $20,000 passive income.This leaves Jefferson with a $30,000 loss carryover to 2008. The carryover will be allocated $6,000 toActivity X [($10,000/$50,000) × $30,000] and $24,000 to Activity Y [($40,000/$50,000) × $30,000]. ¶908.01.

17. a. See Schedule E and Form 8582 for Tomey. ¶903.01.

Depreciation on the condo: $135,000/27.5 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $4,909

Depreciation on the furnishings: $18,500 × 11.52% . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2,131

Total depreciation expense (Schedule E, line 20) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $7,040

Chapter 9 ©2007 CCH. All Rights Reserved.

155Textbook Solutions

Filled-in Schedule E for Tomey.

Chapter 9

156 Essentials of Federal Income Taxation

Filled-in Form 8582 for Tomey.

Chapter 9 ©2007 CCH. All Rights Reserved.

157Textbook Solutions

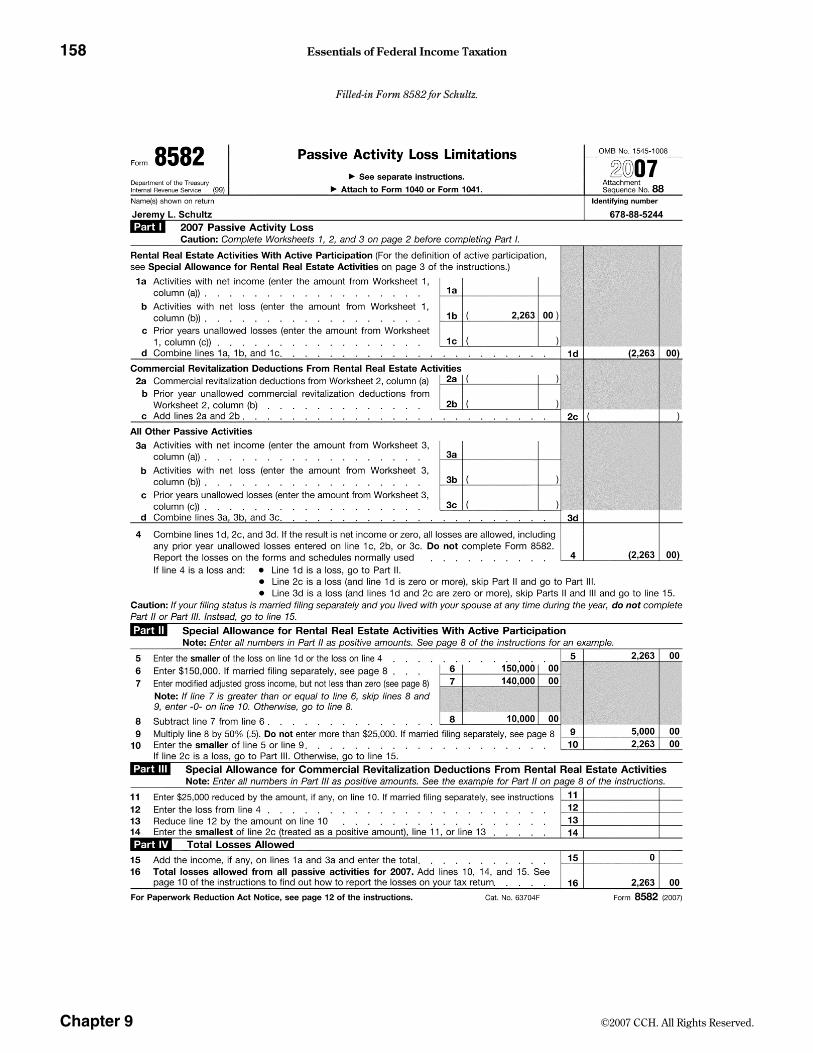

b. See filled-in Schedule E and Form 8582 for Schultz. ¶910.02.Filled-in Schedule E for Schultz.

Chapter 9

158 Essentials of Federal Income Taxation

Filled-in Form 8582 for Schultz.

Chapter 9 ©2007 CCH. All Rights Reserved.

159Textbook Solutions

18. According to Publication 925, a taxpayer materially participated in a trade or business activity for a tax yearif the taxpayer satisfies any of the following seven tests.

(1) The taxpayer participated in the activity for more than 500 hours.

(2) The taxpayer’s participation was substantially all the participation in the activity of all individuals forthe tax year, including the participation of individuals who did not own any interest in the activity.

(3) The taxpayer participated in the activity for more than 100 hours during the tax year, and the taxpayerparticipated at least as much as any other individual (including individuals who did not own anyinterest in the activity) for the year.

(4) The activity is a significant participation activity, and the taxpayer participated in all significantparticipation activities for more than 500 hours. A significant participation activity is any trade orbusiness activity in which the taxpayer participated for more than 100 hours during the year and inwhich the taxpayer did not materially participate under any of the material participation tests, otherthan this test.

(5) The taxpayer materially participated in the activity for any 5 (whether or not consecutive) of the 10immediately preceding tax years.

(6) The activity is a personal service activity in which the taxpayer materially participated for any 3(whether or not consecutive) preceding tax years. An activity is a personal service activity if itinvolves the performance of personal services in the fields of health (including veterinary services),law, engineering, architecture, accounting, actuarial science, performing arts, consulting, or any othertrade or business in which capital is not a material income-producing factor.

(7) Based on all the facts and circumstances, the taxpayer participated in the activity on a regular,continuous, and substantial basis.

However, for purposes of test (7), taxpayers did not materially participate in the activity if they participatedin the activity for 100 hours or less during the year. Participation in managing the activity does not count indetermining whether the taxpayer materially participated under this test if:

(1) Any person other than the taxpayer received compensation for managing the activity, or

(2) Any individual spent more hours during the tax year managing the activity than the taxpayer did(regardless of whether the individual was compensated for the management services).

19. a. Gross income ($200,000) less deductions ($260,000) results in a $60,000 passive loss. The partnershipwill pass half of the loss ($30,000) through to each of the partners who will report it as a passive loss ontheir personal tax returns. As such, it is deductible from other passive income that the partners mayhave. If passive income is insufficient to absorb the loss, the loss carries forward as a suspended loss.In addition, to deduct this loss, the partner must be “at-risk� for the amount of the loss.

b. S corporations treat the loss in a manner similar to the partnership described in “a� above.

c. Normally, the passive loss limitations do not apply to corporations. However, this is a closely-heldcorporation, and the passive loss rules apply. Thus, the corporation can only deduct the $60,000 passiveloss against passive income. Any remaining loss stays in the corporation and carries forward to offsetfuture passive incomes. The loss is not passed through to the shareholders.

20. See filled-in Form 1040 and Schedule E for Jetson. ¶903.01.

The personal use portion of property taxes ($850) and mortgage interest ($550) are itemizeddeductions. However, these amounts do not exceed the $5,000 standard deduction for a singletaxpayer. Amounts from Schedule E are obtained as follows:

Line 3: $2,100 (6 × $350) + $2,000 (5 × $400) = $4,100

Line 7: $80 (1/2 × $160) + $420 = $500

Line 9: 1/2 × $376 = $188

Line 12: 1/2 × $1,100 = $550

Line 14: (1/2 × $300) + $70 = $220

Line 16: 1/2 × $1,700 = $850

Chapter 9

160 Essentials of Federal Income Taxation

Line 17: 1/2 × ($440 + $800) = $620

Line 20: 1/2 × ($41,250 ÷ 27.5) = $750

Filled-in Form 1040, page 1 for Jetson.

Chapter 9 ©2007 CCH. All Rights Reserved.

161Textbook Solutions

Filled-in Form 1040, page 2 for Jetson.

Chapter 9

162 Essentials of Federal Income Taxation

Filled-in Schedule E for Jetson.

Chapter 9 ©2007 CCH. All Rights Reserved.

![[PPT]CFIN - Mid-State Technical Collegeinstructor.mstc.edu/instructor/khansen/Finance/integrated... · Web viewChapter 2 – Integrative Problems Analysis of Financial Statements](https://img.pdfslide.net/doc/110x75/5ae783197f8b9aee078e4ffd/pptcfin-mid-state-technical-viewchapter-2-integrative-problems-analysis.jpg)