Embed Size (px)

Citation preview

152

CHAPTER - 4

ANALYSIS OF PERFORMANCE OF SELECTED FMCG COMPANIES

The performance of the FMCG Companies can be evaluated in three ways, they are:

(1) Solvency:

This is the measure of the firm‘s ability to pay its debts as they come due and still be

financially capable of carrying on normal operations.

(2) Profitability:

This is the measure of the firm‘s ability to earn a net income. Generally historical

evidence is used as the criterion is used as the firm‘s success in this area.

(3) Future potential:

The evaluation of a firm‘s future potential required reference to several factors some of

this cannot measure quantitatively.

So the evaluation of a firm will collectively included above since they are mutually

interdependent and cannot be entirely separated for appraised purpose.

For the purpose of the study, financial performance analysis is made.

(1) Financial performance analysis:

The classification of financial analysis can be made either on the basis of material used

for the some or according to modus operation of the analysis.

(A) According to material used:

(1) External analysis:

―Analysis of financial statements conducted by those who do not have access to books of

accounts or carried out on the basis of published information is known as external

analysis‖(Sharma R. 2006, P-461).

This is affected by those who do not have access to the detailed accounting record of the

company. This group comprising investors, credit agencies, government and the public

153

depends almost entirely on published financial statement. With the recent changes in the

government regulations required business concern to make available detailed information

to the public through audited concerns to make available detailed information to the

public through audited accounts, the position of the external analyst has been

considerably improved.

(2) Internal analysis:

―Analysis conducted by those who have access to book of accounts is known as internal

analysis‖ (Sharma R., 2006, p. 461). It is based on detailed information available within

enterprise, which is not available to the outsiders.

This is affected by those who have access to the books of accounts and other information

relating to the business concern. Any financial analysis is conducted with reference of a

whole unit. Executives and employees of the business units as well as government

agencies, which have statutory control and jurisdiction over such units, conduct this type

of analysis meant for managerial purpose.

Table 4.1 Difference between internal and external analysis

Point of

Difference

Internal Analysis External Analysis

By whom? It is conducted by the persons

within the business firms e.g.

accounting and finance department

It is conducted by the outsiders e.g.

financial analysts, share market

researchers

Base It is conducted on the basis of

books of accounts as access of

them is possible.

It is conducted on the basis of

published information as access of

the books of accounts is not possible.

Reliability As it is based on the books of

accounts, it is more reliable as

compares to external analysis.

As it is based on published

information, it is not conducted in

depth and hence it has less reliability.

154

(B) According to modus operandi of analysis:

(A) Horizontal or Dynamic Analysis:

―Analysis which involves comparisons and establishing relationship among related items

based on financial statements of an enterprise for a number of years or financial statement

of various enterprises for the same year is known as horizontal analysis.‖(Sharma R.,

2006, P-461). As the data of more than one year are used in such a type of analysis, it is

possible to generate the trend of each item of financial statements. As the data of various

years are used in horizontal analysis, it is known as dynamic analysis. (Sehgal Ashok &

Deepak, Advanced Accounting- 2, Corporate Accounting, Taxmann‘s Taxmann Allied

Services (p) Ltd. P-407).When financial statement for a certain number of years is

analyzed the analysis is called a horizontal analysis. It is also known as ‗Dynamic

analyses. This is based on the data spread over a period of years rather than on one date

or period of time as a whole.

(B) Vertical Analysis:

―Analysis of financial data based on relationship among various items in a single period

of financial statements is called vertical analysis.‖ (Sharma R., 2006, P-461). Normally,

common-size statements may be considered as a tool of vertical analysis. As the facts and

figures of financial statements of given period of time are used in vertical analysis, it is

also known as static analysis. This refers to analysis of ratio developed for one date or for

one accounting period. This is also known as ‗static analyses. But vertical analysis does

not facilitate a proper analysis and interpretation of figures in perspective and also

comparison over a period of years. As such this type of analysis is not resorted to by the

financial analysis. In short, financial analysis done on the basis of only one year is known

as vertical analysis.

(C) Trend Analysis:

The financial statements for a series of years may be analyzed to determine the trend of

the data contained there in. The trend percentages are also referred to as „trend ratios‟.

This method of analysis is adopted to determine the direction upward or downward. This

155

involves the computation of the percentage relationship that each item in the statement

bears to the corresponding items contained in that of the base year. For this purpose the

earliest year involved in comparison or any intervening year may be considered as the

base year. The trend percentages emphasize changes in the financial data from year to

year and facilitate horizontal comparison and study of the data. These trend ratios can be

considered as index number showing relative change in the financial data over a period of

years.

Table 4.2: Different between horizontal and vertical analysis

Point of

Difference

Horizontal Analysis Vertical Analysis

Requirement To conduct horizontal analysis,

financial statements of two or more

periods are required.

To conduct vertical analysis,

financial statements of one year

are needed.

Items Under such analysis, items of more

than one year are taken into account.

Under such analysis, items of one

year taken into account.

Reach It involves of comparison of items

given in the financial statements.

It creates a base for the purpose of

conducting comparison of the

items given in the financial

statements.

Utility It is a significant tool for inter-firm

comparison or series analysis.

It is a significant tool for intra-firm

comparison or cross-section

analysis.

Tool Comparative financial statements

analysis is an important tool of this

type.

Common-size statements may be

considered as a tool of horizontal

analysis.

Synonyms It is also known as dynamic

analysis.

It is also known as static analysis.

156

RATIO ANALYSIS

4.1 INTRODUCTION

To evaluate the financial condition and performance of a firm, the financial analyst yields

certain yardstick frequently used as a ratio, or index, relating two pieces of financial data

to each other. Analysis and interpretation of various ratios should give experienced,

skilled analyst a better understanding of the financial conditions and performance of the

firm than they would obtain from analysis of financial data alone.

4.2 WHAT IS RATIO?

Ratio analysis is a powerful tool of financial analysis.

A Ratio is defined as—―The indicated quotient of two mathematical expressions and as

the relationship between two or more things‖. In financial analysis a ratio is used as

benchmark for evaluating the financial position and performance of a firm. Ratios help to

summarize large quantities of financial data and to make qualitative judgments about the

firm‘s financial performance.

The financial statements are prepared and presented annually are of little use for guidance

of prospective investors, creditors and even management. If relationships between

various related items in the financial statement are established, they can provide useful

clues to gauge accurately the financial health and ability of business to make profit.

This relationship between two related items of financial statement is known as ―Ratio‖.

Ratio can be expressed in three different ways such as-

Percentage- for example, the Return on Investment is 30%.

Rates- for example, Price Earning Ratio is 5 times.

Proportion- for example, Debt-Equity Ratio is 1:2

157

Standards of Comparison

The ratio analysis involves comparison for a useful interpretation of the financial

statement. A single ratio itself does not indicate favourable condition. It should be

compared with some standards. The standards may consist of:

Past ratio: Ratios calculated from the past financial statement of the same firm

Competitors‟ ratio: Ratio of some selected firms especially the most successful

competitor, at the same point in time.

Industry ratios: Ratios of the industry to which the firm belongs.

Projected ratios: Ratios developed using the projected financial statement of the

same firm.

4.3 TYPES OF RATIO ANALYSIS

The ratio analysis involves comparison for useful interpretations of the financial

statements a single ratio in itself does not indicate favorable or unfavorable condition. It

should be compared with some standard. Standards of comparison may consist of:

4.3.1 Time Series Analysis

The easiest way to evaluate the performance of a firm is to compare its current ratios with

the past ratios. Such analysis is known as the time series (or trend) analysis. It gives an

indication of the direction of change and reflects whether the firm‘s financial

performance has improved, deteriorated or remained constant over time. The analyst

should not simply determine change, but more importantly, he should understand why

ratios have changed. The change, for example, may be affected by changes in the

accounting policies without a material change in the firm‘s performance.

4.3.2 Pro-forma Analysis

Sometimes future ratios are used as the standard of comparison. Future ratios can be

developed from the projected financial statements. The comparison of current or past

158

ratios with future ratios shows the firm‘s relative strengths and weaknesses in the past

and future. If the future ratios indicate weak financial position, corrective actions should

be initiated.

4.3.3 Cross-Sectional Analysis

Another way of comparison is to compare ratios of one firm with some selected firms in

the same industry at the same point in time. This kind of comparison is known as the

cross-sectional analysis. In most cases, it is more useful to compare the firm‘s ratio with

ratio of few carefully selected competitors, who have similar operations. This kind of a

comparison indicates the relative financial position and performance of the firm. A firm

can easily resort to such a comparison, as it is not difficult to get the published financial

statements of the similar firms.

4.3.4 Industry Analysis

To determine the financial condition and performance of a firm, its ratios may be

compared with average ratios of the industry analysis, helps to ascertain the financial

standing and capability of the some point of time to determine the position of company in

the industry.

4.4 TYPES OF RATIOS:

Several ratios, calculate from the accounting data can be grouped into various classes

according to financial activity or function to be evaluated. The ratios can be classified for

the purpose of exposition. Into four broad groups, viz,

Liquidity Ratio: Measure the firms ability to meet current obligations;

Leverage ratios: Show the proportions of debt and equity in financing the firm‘s

acts;

Profitability Ratio: Measure overall performance and effectiveness of the firm;

Activity Ratios; Reflect the firm‘s efficiency in utilizing its assets.

159

The present study is based on the profitability ratios which would give a clear idea how

ratios are interrelated with the designing of the firm‘s impact of the industrial policy.

However, the other ratios also directly or indirectly affect to the financial performance of

the FMCG companies.

Accounting ratios are relationship expressed in mathematical terms between figures

which are connected with each other in some manner. Obviously, no purpose will be

served by comparing two sets of figures which are not at all connected with each other.

Moreover, absolute figure are also unfit for comparison.

4.5 CLASSIFICATION OF RATIOS

Ratio can be classified into different categories depending upon the basis of

classification.

The traditional classification has been on the basis of the financial statement to which the

determinants of a ratio belong. On this basis the ratios could be classified as:

1. Profitability ratios,

2. Turnover ratio, and

3. Financial ratio.

4.6 MEANING OF PROFITABILITY RATIOS

Profitability is an indication of the efficiency with which the operations of the business

are carried on. Poor operational performance may indicate poor sales and hence poor

profits. A lower profitability may arise due to the lack of control over the expenses.

Bankers, financial institutions and other creditors look at the profitability ratios as an

indicator whether or not the firm earns sub stability more than it pays interest for the use

of borrowed funds and whether the ultimate repayment of their debts appears reasonably

certain. Owners are interested to know the profitability as it indicates the return which

they can get on their investments.

160

Profit is the difference between revenues and expanses over a period of time. Profit is the

ultimate output of a company and it will have no future if it fails to make sufficient

profits. Therefore, the financial manager should continuously evaluate the efficiency of

the company in terms of profit. The Profitability Ratios are calculated to measure the

operating efficiency of the company.

Generally, two major types of profitability ratios calculated

Profitability in relation to sales

Profitability in relation to the investment

The profit is commonly measured by Profit after Tax (PAT) which is the result of the

impact of all factors on the firm‘s earnings. Taxes are not controllable by management.

To separate the influence of taxes Profit before Tax (PBT) may be computed. If the

firm‘s profit has to be examined from the point of view of all the investors the

appropriate measure of profit is operating profit. Operating profit is Earnings before

Interest and Tax (EBIT). This measure of earnings shows earnings arising directly from

the commercial operations of the business without the effect of financing.

Comparative study of Ratios of the selected companies

The study includes the following companies of the FMCG Industry, they are:

1. Britannia, Mumbai.

2. Nirma Limited., Ahmedabad.

3. Dabur India Limited, New Delhi.

4. Colgate- Palmolive (India) Limited, Mumbai

5. Godrej Consumer Product Limited, Mumbai.

6. Procter & Gamble Hygine and Health care Limited, Mumbai.

7. Hindustan Lever/ Unilever Ltd, Mumbai.

161

For the Analysis of performance of selected FMCG companies the following ratios

are used:

1. Net Profit Ratio 9. Stock Turnover Ratio

2. Return on Investment Ratio 10. Debtors Turnover Ratio

3. Return on Capital Employed Ratio 11. Working Capital Turnover Ratio

4. Return on Shareholders Fund 12.Inventory to Working Capital Rat

5. Operating Profit Ratio 13. Sales to Fixed Assets Ratio

6. Debt-Equity Ratio 14. Total Assets Turnover Ratio

7. Current Ratio 15. Fixed Assets to Long term Funds Ratio

8. Quick Ratio

These ratios and their trends are used to evaluate performance of selected FMCG

companies. So, these ratios are serving the purpose.

1. NET PROFIT RATIO

The profit margin measures the relationship between profit and sales. The Net Profit

Ratio determines this relationship. This ratio is also known as ―Net Margin‖. It is arrived

at by dividing the Earning after Tax with Sales.

Net Profit Ratio = EAT x 100

Sales

It is indicative of ―Management‘s ability to operate the business with sufficient success

not only to recover from revenues of the period, the cost of merchandises or services, the

expenses of operating the business (including depreciation) and the cost of borrowed

funds, but also to leave a margin of reasonable compensation to the owners for providing

their capital at risk.

162

Table 4.3: Net profit Ratio (in %)

Years Britannia Nirma Dabur Colgate Godrej P&G HUL

1999-00 N.A. N.A. 7.80 4.75 N.A. 15.79 12.35

2000-01 N.A. N.A. 7.30 5.31 N.A. 18.45 14.96

2001-02 N.A. 8.14 6.49 6.01 8.16 18.81 17.78

2002-03 N.A. 9.02 7.75 8.39 10.16 15.53 17.48

2003-04 8.08 12.12 9.88 10.36 11.86 15.97 12.06

2004-05 9.21 13.24 11.67 10.56 14.26 18.19 12.73

2005-06 8.05 10.76 13.80 11.30 17.44 23.38 15.33

2006-07 4.64 4.30 15.75 11.56 16.59 16.24 14.04

2007-08 7.30 8.67 15.20 14.92 16.13 20.14 13.31

Average 7.45 9.46 10.62 9.24 13.51 18.05 14.44

CV (%) 23.01 31.18 33.82 36.63 26.15 14.20 14.65

Source: Computed from the annual reports of the companies.

Graph 4.1: Net Profit Ratio (in %)

7.46

9.4710.63

9.24

13.52

18.06

14.45

0.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00

16.00

18.00

20.00

Britannia Nirma Dabur Colgate Godrej P&G HLL/HUL

FMCGs

Table 4.3 represents the NP ratios, average ratios and CV value of selected companies for

the period understudy. The NP ratio highest was 23.38 per cent for P&G in 2005-06 and

lowest was 4.3 per cent for Nirma in 2006-07 among the selected units during the period

of the study. The average NP ratio highest was 18.05 per cent for P&G and lowest was

7.45 per cent for Britannia during the study period. The CV value of the NP ratios highest

was 36.63% for Colgate followed by Dabur 33.82%, Nirma 31.18%, Godrej 26.15%,

163

Britannia 23.01%, HUL 14.65% and P&G 14.20% during the period understudy. Thus, it

reveals that the profitability of P&G and HUL was remained consistant during the period

understudy.

2. RETURN ON INVESTMENT RATIO (ROI)

Efficiency or productivity measures the output of a system in relation to its input; the

greater the volume of output produced from a given level of input the more efficient the

system. A business invests in assets to generate sales and profits. The more sales and

profit a business can generate from a given level of investment in assets the more

productive it is. The term investment may refer to total assets or net assets.

The conventional approach of calculating return on investment is to divide PAT by

investment. Investment represents the pool of fund supplied by shareholders and lenders,

while PAT represents Residue income of shareholders.

Return on Investment = Earnings after tax X 100

Total Assets

In general terms, the higher the ROI ratio the better; it suggests the business in utilizing

its assets productively. This is very short sighted approach, as not replacing existing

assets or not purchasing new assets when necessary may be more damaging in the longer

term.

Table 4.4: Return on Investment (ROI) (in %)

Years Britannia Nirma Dabur Colgate Godrej P&G HUL

1999-00 N.A. N.A. 16.35 19.87 N.A. 63.87 152.92

2000-01 N.A. N.A. 19.79 30.61 N.A. 83.80 114.96

2001-02 N.A. 9.00 18.16 41.19 51.79 86.19 127.72

2002-03 N.A. 8.83 25.29 83.50 73.10 49.31 120.64

2003-04 40.78 9.14 72.77 91.45 96.97 36.37 77.60

2004-05 45.08 10.06 104.84 625.22 154.43 42.83 216.77

2005-06 40.68 9.82 101.65 271.36 473.89 50.44 296.45

2006-07 33.63 4.18 109.63 280.01 159.78 101.92 651.28

2007-08 50.16 8.70 91.27 304.08 137.55 59.88 809.92

Average 7.45 9.46 10.63 9.24 13.51 18.05 14.45

CV (%) 14.53 23.26 66.74 102.13 87.05 34.81 92.35

Source: Computed from annual reports of the companies

164

Graph 4.2: Return on Investment (ROI) (in %)

42.06

8.53

62.19

194.14

163.93

63.85

285.36

0.00

50.00

100.00

150.00

200.00

250.00

300.00

Britannia Nirma Dabur Colgate Godrej P&G HLL/HUL

FMCGs

Table 4.4 represents the Return on Investment, average ratios and CV value of selected

companies for the period understudy.The Return on Investment highest was 809.92 per

cent for HUL in 2007-08 and lowest was 8.70 per cent for Nirma in 2007-08 among the

selected units during the period of the study. The average Return on Investment ratio

highest was 18.05 per cent for P&G and lowest was 7.45 per cent for Britannia during the

study period. The CV value of the ROI ratios highest was 102.13% for Colgate followed

by HUL 92.35%, Godrej 87.05%, Dabur 66.74%, P&G 34.81%, Nirma 23.26%,

Britannia 14.53% during the period understudy. Thus, it reveals that the Return on

Investment of P&G and Nirma was remained consistant during the period understudy.

3. RETURN ON CAPITAL EMPLOYED

The fund employed in the net assets is known as capital Employed. Rate of return on

capital employed is one of the means which provides a basis for testing of profitability

related to the source of long term funds. There are number of sources through which a

firm can acquire its total assets. Thus, the capital employed is the tool of measuring the

profitability of the examined units. This ratio is yardstick for measuring the profitability

of the firm.

165

Return on Capital Employed = Earning After Tax X 100

Capital Employed

Capital Employed = Owner‟s fund + Secured Loan + Unsecured Loan.

Table 4.5: Return on Capital Employed (in %)

Years Britannia Nirma Dabur Colgate Godrej P&G HUL

1999-00 N.A. N.A. 13.35 16.87 N.A. 36.97 50.39

2000-01 N.A. N.A. 15.26 24.79 N.A. 44.98 52.48

2001-02 N.A. 9.15 12.30 24.69 53.64 35.35 47.61

2002-03 N.A. 8.85 18.20 30.28 78.71 29.53 46.10

2003-04 24.22 10.66 35.85 43.79 87.41 37.00 33.60

2004-05 31.88 11.61 37.05 44.65 134.63 54.80 59.60

2005-06 26.14 10.07 38.97 49.96 137.70 51.00 66.36

2006-07 17.37 3.96 56.53 56.24 57.03 30.85 126.03

2007-08 22.16 7.58 55.29 138.84 50.35 37.44 108.48

Average 24.35 8.84 31.42 47.79 85.64 39.77 65.63

CV (%) 21.87 28.47 55.54 76.59 43.30 21.85 47.15

Source: Computed from the annual reports of the companies.

Graph 4.3: Return on Capital Employed (in %)

24.35

8.84

31.42

47.79

85.64

39.77

65.63

0.00

10.00

20.00

30.00

40.00

50.00

60.00

70.00

80.00

90.00

Britannia Nirma Dabur Colgate Godrej P&G HLL/HUL

FMCGs

166

Table 4.5 represents the Return on Capital Employed, average ratios and CV value of

selected companies for the period understudy.The Return on Capital Employed highest

was 138.84 per cent for Colgate in 2007-08 and lowest was 3.96 per cent for Nirma in

2006-07 among the selected units during the period of the study. The average Return on

Capital Employed ratio highest was 85.64 per cent for Godrej and lowest was 8.84 per

cent for Nirma during the study period. The CV value of the Return on Capital Employed

ratios highest was 76.59% for Colgate followed by Dabur 55.54%, HUL 47.15%, Godrej

43.30%, Nirma 28.47%, Britannia 21.87% and P&G 21.85% during the period

understudy. Thus, it reveals that the Return on Capital Employed of P&G and Dabur was

remained consistant during the period understudy.

4. RETURN ON SHAREHOLDER‟S FUNDS

This Ratio expresses the net profit in terms of the equity shareholders funds. This ratio is

an important yardstick of performance for equity shareholders since it indicates the return

on the funds employed by them. However, this measure is based on the historical net

worth and will be high for old plants and for new plants.

The factor which motivates shareholders to invest in a company is the expectation of an

adequate rate of return on their funds and periodically, they will want to assess the rate of

return earned in order to continue with their investment. There are various factors of

measuring the return including the earning yield and dividend yield which are examined

at later stage. This ratio is useful in measuring the rate of return as a percentage of the

book value of shareholders equity.

Return on Shareholder‟s Fund = Net Profit after Interest and Tax X 100

Shareholders Funds

167

Table 4.6: Return on Shareholder‟s Funds (in %)

Years Britannia Nirma Dabur Colgate Godrej P&G HUL

1999-00 N.A. N.A. 25.40 17.25 N.A. 38.06 52.65

2000-01 N.A. N.A. 23.52 26.14 N.A. 44.98 53.93

2001-02 N.A. 14.85 18.86 28.18 78.95 35.35 48.37

2002-03 N.A. 15.32 23.24 32.24 117.59 29.53 82.84

2003-04 27.56 15.09 42.22 44.21 153.06 37.00 57.21

2004-05 33.55 15.18 43.78 45.36 172.63 55.22 61.07

2005-06 26.66 11.79 42.22 50.76 158.50 51.17 68.13

2006-07 17.50 4.49 62.52 57.10 119.16 30.85 133.78

2007-08 25.27 8.89 59.96 142.85 98.42 37.91 130.68

Average 26.10 12.23 37.97 49.34 128.33 40.01 76.52

CV (%) 22.05 34.13 42.72 75.68 26.65 21.89 43.36

Source: Computed from the annual reports of the companies.

Graph 4.4: Return on Shareholder‟s Fund (in %)

26.1112.23

37.97

49.34

128.33

40.01

76.52

0.00

20.00

40.00

60.00

80.00

100.00

120.00

140.00

Britannia Nirma Dabur Colgate Godrej P&G HLL/HUL

FMCGs

Table 4.6 represents the Return on Shareholder‘s Fund, average ratios and CV value of

selected companies for the period understudy.The Return on Shareholder‘s Fund highest

was 172.63 per cent for Godrej in 2004-05 and lowest was 4.49 per cent for Nirma in

2006-07 among the selected units during the period of the study. The average Return on

Shareholder‘s Fund ratio highest was 128.33 per cent for Godrej and lowest was 12.23

per cent for Nirma during the study period. The CV value of the Return on Shareholder‘s

168

Fund ratios highest was 75.68% for Colgate followed by HUL 43.36%, Dabur 42.72%,

Nirma 34.13%, Godrej 26.65%, Britannia 22.05% and P&G 21.89% during the period

understudy. Thus, it reveals that the Return on Investment of P&G and Dabur was

remained consistant during the period understudy.

5. OPERATING PROFIT RATIO

Operating profit ratio is the ratio between operating profit and sales.

Operating profit is the net profit earned from the business for which the concern is

started. It is the excess of net sales over the operating cost. It is the net profit plus non-

operating expenses minus non-operating incomes.

Operating Profit Ratio = Operating profit X 100

Net sales

The operating profit ratio also indicates the operating efficiency or inefficiency of a

business.

The standard operation profit ratio is 10%, so, on operating profit ratio of 10% or more is

an indication of the operating efficiency of the business. An operating profit ratio of less

than 10% is an indication of the operating inefficiency of the business.

Table 4.7: Operating profit ratio (Operating profit margin ratio) (in %)

Years Britannia Nirma Dabur Colgate Godrej P&G HUL

1999-00 N.A. N.A. 7.78 8.25 N.A. 17.18 15.70

2000-01 N.A. N.A. 7.30 8.99 N.A. 21.70 17.71

2001-02 N.A. 18.06 6.49 9.88 12.30 24.81 22.07

2002-03 N.A. 18.84 7.75 13.29 13.29 21.14 22.14

2003-04 13.64 26.17 9.88 14.54 14.01 22.03 15.16

2004-05 15.25 23.71 13.01 76.48 15.54 24.47 14.51

2005-06 11.43 22.30 15.65 15.43 18.97 31.17 15.38

2006-07 5.63 15.20 17.76 14.55 16.87 26.31 15.92

2007-08 9.41 14.42 17.53 81.52 18.43 27.67 14.95

Average 11.07 19.81 11.46 26.99 15.63 24.05 17.06

CV (%) 33.96 22.21 40.02 109.76 16.46 17.07 17.57

Source: Computed from the annual reports of the companies.

169

Graph 4.5: Operating Profit Ratio (in %)

10.75

19.81

11.46

26.99

15.63

24.05

17.06

0.00

5.00

10.00

15.00

20.00

25.00

30.00

Britannia Nirma Dabur Colgate Godrej P&G HLL/HUL

FMCGs

Table 4.7 represents the Operating Profit Ratio, average ratios and CV value of selected

companies for the period understudy.The Operating Profit Ratio highest was 81.52 per

cent for Colgate in 2007-08 and lowest was 5.63 per cent for Britannia in 2006-07 among

the selected units during the period of the study. The average Operating Profit Ratio

highest was 26.99 per cent for Colgate and lowest was 11.07 per cent for Britannia during

the study period. The CV value of the Operating Profit Ratio highest was 109.76 for

Colgate followed by Dabur 40.02%, Britannia 33.96%, Nirma 22.21%, HUL 17.57%,

P&G 17.57% and Godrej 17.07% during the period understudy. Thus, it reveals that the

Operating Profit Ratio of Godrej and HUL was remained consistant during the period

understudy.

170

6. DEBT- EQUITY RATIO

Debt-equity ratio is the ratio which expresses the relationship between debt and equity.

Debt, generally, refers to long-term liabilities.

Debt / Shareholders‟ Equity

Equity, for the purpose of this ratio, means owners, or proprietors, funds. Owners, fund

comprises capital, all accumulated reserves and profits. Of course, if there are losses and

fictitious assets, they should be adjusted in, i.e., deducted from, the owners, funds.

The standard or ideal debt equity ratio is 2:1. As such, if the debt is less than two times

the equity, the logical conclusion is that the financial structure of the concern is sound,

and so, the stake or risk of the long-term creditors is relatively less. On the other hand, if

the debt is more than two times the equity, the conclusion is that the financial structure of

the undertaking is weak, and so, the stake of the long-term creditors is relatively more.

Table 4.8: Debt- Equity Ratio

Years Britannia Nirma Dabur Colgate Godrej P&G HUL

1999-00 N.A. N.A. 0.90 0.02 N.A. N.A. 0.04

2000-01 N.A. N.A. 0.54 0.05 N.A. N.A. 0.03

2001-02 N.A. 0.62 0.53 0.14 0.47 N.A. 0.02

2002-03 N.A. 0.73 0.28 0.06 0.49 N.A. 0.80

2003-04 0.14 0.42 0.18 0.01 0.75 N.A. 0.70

2004-05 0.05 0.31 0.18 0.02 0.28 N.A. 0.02

2005-06 0.02 0.17 0.08 0.02 0.15 N.A. 0.03

2006-07 0.01 0.13 0.11 0.02 1.09 N.A. 0.06

2007-08 0.14 0.17 0.08 0.03 0.95 N.A. 0.20

Average 0.07 0.36 0.32 0.04 0.59 N.A 0.21

CV (%) 88.61 64.92 87.63 98.39 57.98 N.A 147.61

Source: Computed from the annual reports of the companies.

Note: Here we can‟t get long term liabilities of P&G. Hence we have not obtained

this ratio for said FMCG.

171

Graph 4.6: Debt- Equity Ratios

0.07

0.36

0.32

0.04

0.60

0.01

0.21

0

0.1

0.2

0.3

0.4

0.5

0.6

Britania Nirma Dabur Colget Godrej P&G HLL

FMCGs

Table 4.8 represents the Debt-Equity Ratios, average ratios and CV value of selected

companies for the period understudy.The Debt-Equity Ratios highest was 1.09 per cent

for Godrej in 2006-07 and lowest was 0.01 per cent for Britannia in 2006-07 among the

selected units during the period of the study. The average Debt-Equity Ratios highest was

0.59 per cent for Godrej and lowest was 0.04 per cent for Colgate during the study

period. The CV value of the Debt-Equity Ratios highest was 147.61% for HUL followed

by Colgate 98.39%, Britannia 88.61%, Dabur 87.63%, Nirma 64.92% and Godrej

57.98% during the period understudy. Thus, it reveals that the Debt-Equity Ratios of

Colgate and HUL was remained consistant during the period understudy.

172

7. CURRENT RATIO

Current ratio is the ratio which expresses the relationship between current assets and

current liabilities.

Current Assets / Current Liabilities

Current assets refer to all those asset which change their form and substance and which

are ultimately converted into cash during the normal operating cycle of business i.e., the

normal course of the business, which is normally, 12 months.

Current liabilities refer to all short-term obligations or liabilities which are enquired to be

repaid within a period of one year out of short-term.

The actual current ratio, ascertained with the help of the relevant financial figures, has to

be compared with the standard or ideal current ratio of 2:1. If the current ratio is less than

the standard current ratio of 2:1, the logical conclusion is that the concern does not enjoy

sufficient liquidity, and there is shortage of working capital. If the actual is more than 2:1,

it can reasonably be taken as a sign of the liquidity or the short-term solvency of the

concern.

Table 4.9: Current Ratio

Years Britannia Nirma Dabur Colgate Godrej P&G HUL

1999-00 N.A. N.A. 3.90 1.36 N.A. 0.87 0.90

2000-01 N.A. N.A. 2.66 1.04 N.A. 0.88 1.09

2001-02 N.A. 2.54 2.33 1.00 0.84 0.88 1.07

2002-03 N.A. 4.35 2.08 0.80 0.82 1.45 1.07

2003-04 1.08 6.56 1.01 1.14 0.69 2.16 1.05

2004-05 0.94 11.83 0.79 0.71 0.66 2.87 0.75

2005-06 1.08 8.73 0.93 0.61 0.70 3.87 0.76

2006-07 1.23 3.64 0.97 0.65 0.69 0.93 0.68

2007-08 1.64 4.73 1.17 0.67 0.81 1.74 1.14

Average 1.19 6.05 1.76 0.89 0.74 1.74 0.95

CV (%) 22.58 53.78 60.20 29.38 10.14 60.88 18.54

Source: Computed from the annual reports of the companies.

173

Graph 4.7: Current Ratio

1.19

6.05

1.76

0.89

0.74

1.74

0.95

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

Britannia Nirma Dabur Colgate Godrej P&G HLL/HUL

FMCGs

Table 4.9 represents the Current Ratio, average ratios and CV value of selected

companies for the period understudy.The Current Ratio highest was 11.83 per cent for

Nirma in 2004-05 and lowest was 0.61 per cent for Colgate in 2005-06 among the

selected units during the period of the study. The average Current Ratio highest was 6.05

per cent for Nirma and lowest was 0.74 per cent for Godrej during the study period. The

CV value of the Current Ratio highest was 60.88% for P&G followed by Dabur 60.20%,

Nirma 53.78%, Colgate 29.38%, Britannia (22.58%, HUL 18.54%, and Godrej 10.14%

during the period understudy. Thus, it reveals that the Current Ratio of Godrej and HUL

was remained consistant during the period understudy.

174

8. QUICK RATIO

Quick ratio is the ratio which expresses the relationship between quick or liquid assets

and quick or liquid liabilities.

Quick assets refer to those current assets which can be converted into cash quickly, i.e.,

within a very short period without much loss. They include all current assets excepts

inventories or stocks and prepaid expenses.

Quick liabilities refer to all those liabilities which should necessarily be paid within a

short period of one year. They include all current liabilities expect bank overdraft and

cash credit.

Quick Ratio = Quick Assets

Quick Liabilities

The actual quick ratio has to be compared with the standard or ideal quick ratio of 1:1. If

the actual quick ratio is equal to or more than the standard ratio of 1:1, the conclusion can

be that the concern is liquid, and so, it can pay off its short-term liabilities out of its

quickly realizable assets without any difficulty. On the other hand, if the actual quick

ratio is less than the standard quick ratio of 1:1, the conclusion can be that the concern is

not liquid.

Table 4.10: Quick Test Ratio

Years Britannia Nirma Dabur Colgate Godrej P&G HUL

1999-00 N.A. N.A. 2.20 0.85 N.A. 0.56 0.37

2000-01 N.A. N.A. 1.43 0.62 N.A. 0.60 0.58

2001-02 N.A. 1.00 1.10 0.70 0.43 0.64 0.55

2002-03 N.A. 1.70 0.96 0.58 0.36 1.19 0.52

2003-04 N.A. 3.88 0.33 0.83 0.25 1.87 0.48

2004-05 0.29 8.30 0.25 0.37 0.11 2.38 0.30

2005-06 0.53 5.37 0.34 0.35 0.13 3.48 0.27

2006-07 0.33 1.38 0.40 0.40 0.15 0.56 0.17

2007-08 0.42 1.48 0.53 0.45 0.13 1.38 0.55

Average 0.39 3.30 0.84 0.57 0.22 1.41 0.42

CV (%) 27.16 82.46 78.13 33.68 57.25 71.88 35.12

Source: Computed from the annual reports of the companies.

175

Graph 4.8: Quick Test Ratio

0.39

3.30

0.84

0.57

0.22

1.41

0.42

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

Britannia Nirma Dabur Colgate Godrej P&G HLL/HUL

FMCGs

Table 4.10 represents the Quick Ratio, average ratios and CV value of selected

companies for the period understudy.The Quick Ratio highest was 8.30 per cent for

Nirma in 2004-05 and lowest was 0.11 per cent for Godrej in 2004-05 among the selected

units during the period of the study. The average Quick Ratio highest was 3.30 per cent

for Nirma and lowest was 0.22 per cent for Godrej during the study period. The CV value

of the Quick Ratio highest was 82.46% for Nirma followed by Dabur 78.13%, P&G

71.88%, Godrej 57.25%, HUL 35.12%, Colgate 33.68% and Britannia 27.16% during the

period understudy. Thus, it reveals that the Quick Ratio of Colgate and Dabur was

remained consistant during the period understudy.

176

9. STOCK TURNOVER RATIO

This is also called as Inventory Turnover or Stock velocity. This ratio is calculated to

consider the adequacy of the quantum of capital and its justification for investing in stock

or inventory. Inventory Turnover is the number of times obtained by dividing cost of

sales by average stock. The logic behind establishing the relationship between Average

Stock and cost of sales seems to be that stock should be compared with cost of sales

because the stock is at cost price.

Stock Turnover Ratio = Cost of Goods Sold

Average Stock

Stock turnover is used to measure the efficiency of sales. If a concern is able to effect

higher volume of sales with lower quantum of stock, then it can be concluded that

marketing efficiency of the concern is very sound and high. Concerns having too high

stock turnover ratio may be operating with low margin of profit. However, too high stock

turnover may be a symptom of over-trading.

If the stock turnover is low or of smaller magnitude then it may be assumed to indicate (i)

that there is slump in the business, (ii) that there is over investment in stock, (iii) that the

closing stock has been increased just to take the advantage of expected rise in selling

price or to meet the estimated rise in future sales, (iv) that stock has been valued

incorrectly or improperly, (v) that items of stock have been included in an unbalanced

manner or in disproportionate manner.

Table – 4.11: Stock Turnover Ratio (in times)

Years Britannia Nirma Dabur Colgate Godrej P&G HUL

1999-00 N.A. N.A. N.A. N.A. N.A. N.A. N.A.

2000-01 N.A. N.A. 8.23 14.64 N.A. 10.62 9.06

2001-02 N.A. 8.34 7.81 14.55 16.78 11.27 7.90

2002-03 N.A. 8.84 7.31 16.72 15.51 12.41 7.59

2003-04 12.03 6.85 7.91 18.12 12.64 14.15 6.93

2004-05 12.60 6.86 10.59 15.76 9.81 13.80 7.92

2005-06 11.38 7.30 11.24 16.36 8.56 14.34 8.44

177

2006-07 11.58 6.39 11.73 17.91 7.77 18.53 7.84

2007-08 10.14 4.73 11.62 19.92 6.51 16.76 9.03

Average 11.55 7.04 9.55 16.75 11.08 13.98 8.09

CV (%) 7.93 19.07 19.96 10.99 35.78 19.06 8.95

Source: Computed from the annual reports of the companies.

Graph 4.9: Stock Turnover Ratio (in times)

11.55

7.05

9.56

16.75

11.08

13.99

8.09

0.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00

16.00

18.00

Britannia Nirma Dabur Colgate Godrej P&G HLL/HUL

FMCGs

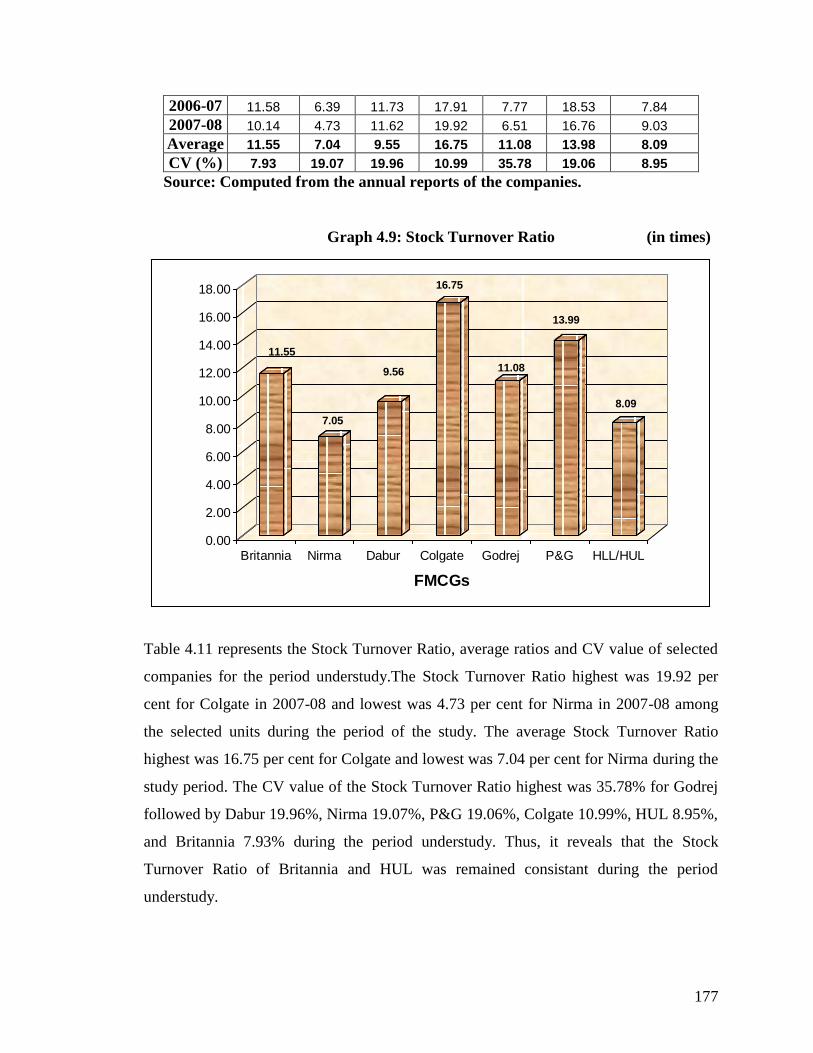

Table 4.11 represents the Stock Turnover Ratio, average ratios and CV value of selected

companies for the period understudy.The Stock Turnover Ratio highest was 19.92 per

cent for Colgate in 2007-08 and lowest was 4.73 per cent for Nirma in 2007-08 among

the selected units during the period of the study. The average Stock Turnover Ratio

highest was 16.75 per cent for Colgate and lowest was 7.04 per cent for Nirma during the

study period. The CV value of the Stock Turnover Ratio highest was 35.78% for Godrej

followed by Dabur 19.96%, Nirma 19.07%, P&G 19.06%, Colgate 10.99%, HUL 8.95%,

and Britannia 7.93% during the period understudy. Thus, it reveals that the Stock

Turnover Ratio of Britannia and HUL was remained consistant during the period

understudy.

178

10. DEBTORS‟ TURNOVER RATIO

Receivables or debtors constitute an important item of current assets. That means the

quality of debtors determines the liquidity of the firm to a great extent. To judge the

quality of the debtors‘ the receivables turnover ratio, debtors‘ turnover ratio or debtors‘

velocity is used.

Debtors‘ turnover ratios are the ratio which indicates the relationship between debtors

and sales. It is the ratio which indicates the number of times the debts are collected in a

year.

Debtors‟ Turnover Ratio= Net annual credit sales

Average debtors (i.e., average debtors and

bills receivables)

Or

Debt Collection Period Ratio = Number of days in a year, (i.e., 365days or 360 days)

Debtor‟ Turnover

The collection period, as calculate above, is compared with the credit period allowed, and

conclusions are drawn. If the actual period of credit allowed is more than the normal

period of credit or the ideal period of credit, viz., 30 days, the indication is that credit

collection is not efficient. On the other hand, if the actual period of credit allowed is less

than the normal period of credit or the ideal period of credit, the indication is that credit

collection is efficient.

Table – 4.12: Debtor‟s turnover ratio (in times)

Years Britannia Nirma Dabur Colgate Godrej P&G HUL

1999-00 N.A. N.A. 8.82 24.96 N.A. 22.93 40.09

2000-01 N.A. N.A. 9.05 19.90 N.A. 15.16 27.68

2001-02 N.A. 14.05 9.83 20.36 23.55 12.45 23.74

2002-03 N.A. 15.00 15.53 28.69 30.03 9.62 21.12

2003-04 73.90 11.46 25.13 41.71 59.33 12.45 19.62

2004-05 35.80 10.37 33.29 90.03 103.17 26.22 22.97

2005-06 87.20 9.87 31.16 154.09 84.81 50.98 27.39

2006-07 81.00 11.29 19.83 149.68 72.44 39.52 27.99

2007-08 56.50 12.25 19.06 58.79 75.26 38.32 50.51

Average 66.88 12.04 19.08 65.36 64.08 25.29 29.01

CV (%) 31.14 15.63 48.65 82.51 44.94 57.91 34.58

Source: Computed from the annual reports of the companies.

179

Graph 4.10: Debtor‟s Turnover Ratio (in times)

66.88

12.04

19.08

65.3664.08

25.30

29.01

0.00

10.00

20.00

30.00

40.00

50.00

60.00

70.00

Britannia Nirma Dabur Colgate Godrej P&G HLL/HUL

FMCGs

Table 4.12 represents the Debtor‘s Turnover Ratio, average ratios and CV value of

selected companies for the period understudy.The Debtor‘s Turnover Ratio highest was

154.09 per cent for Colgate in 2005-06 and lowest was 8.82 per cent for Dabur in 1999-

00 among the selected units during the period of the study. The average Debtor‘s

Turnover Ratio highest was 66.88 per cent for Britannia and lowest was 12.04 per cent

for Nirma during the study period. The CV value of the Debtor‘s Turnover Ratio highest

was 82.51% for Colgate followed by P&G 57.91%, Dabur 48.65%, Godrej 44.94%, HUL

34.58%, Britannia 31.14%)and Nirma 15.63% during the period understudy. Thus, it

reveals that the Debtor‘s Turnover Ratio of Colgate and HUL was remained consistant

during the period understudy.

180

11. WORKING CAPITAL TURNOVER RATIO

Working capital turnover ratio is the ratio between working capital and turnover.

Working capital is the excess of current assets over current liabilities.

Turnover means net sales, i.e., total sales less sales returns.

Working Capital Turnover Ratio = Net Sales

Working Capital

This ratio indicates the efficient or inefficient utilization of the working capital of an

enterprise. There is no standard or ideal working capital turnover ratio. Though there is

no standard working capital turnover ratio, one can say that a higher working capital

turnover ratio indicates the efficiency and a lower working capital turnover ratio indicates

the inefficiency of the management in the utilization of working capital.

Table 4.13: Working Capital Turnover Ratio (in times)

Years Britannia Nirma Dabur Colgate Godrej P&G HUL

1999-00 N.A. N.A. 3.43 13.57 N.A. 10.32 28.40

2000-01 N.A. N.A. 4.96 313.44 N.A. 8.47 146.21

2001-02 N.A. 5.16 4.45 20.42 29.02 3.66 41.51

2002-03 N.A. 4.23 6.36 35.80 22.16 2.96 27.49

2003-04 126.30 35.08 67.94 28.34 18.33 3.59 24.25

2004-05 40.76 32.95 18.06 17.07 16.10 4.95 8.16

2005-06 52.60 2.36 59.69 24.53 16.38 3.33 8.94

2006-07 37.70 2.56 39.69 20.92 28.46 3.50 7.48

2007-08 12.62 2.41 69.86 11.72 73.60 3.04 7.32

Average 53.99 12.11 30.49 53.98 29.15 4.87 33.31

CV (%) 70.56 51.23 88.82 196.91 113.04 71.93 104.28

Source: Computed from the annual reports of the companies.

181

Graph 4.11: Working Capital Turnover Ratio (in times)

54.00

3.34

30.49

53.98

29.15

4.87

36.56

0

10

20

30

40

50

60

Britania Nirma Dabur Colget Godrej P&G HLL

FMCGs

Table 4.13 represents the Working Capital Turnover Ratio, average ratios and CV value

of selected companies for the period understudy.The Working Capital Turnover Ratio

highest was 313.44 per cent for Colgate in 2000-01 and lowest was 2.36 per cent for

Nirma in 2005-06 among the selected units during the period of the study. The average

Working Capital Turnover Ratio highest was 53.99 per cent for Britannia and lowest was

4.87 per cent for P&G during the study period. The CV value of the Working Capital

Turnover Ratio highest was 196.91% for Colgate followed by Godrej 113.04%, HUL

104.28%, Dabur 88.82%, P&G 71.93%, Britannia 70.56% and Nirma 51.23% during the

period understudy. Thus, it reveals that the Working Capital Turnover Ratio of P&G and

Nirma was remained consistant during the period understudy.

182

12. INVENTORY TO WORKING CAPITAL RATIO

Inventory to working capital ratio is the ratio of inventory to working capital.

Inventory or stock refers to closing stocks of raw materials, work-in-progress and

finished goods.

Working capital is the excess of current assets over current liabilities.

Inventory to working capital ratio= Inventory x100

Working capital

As per the standard or ideal inventory to working capital ratio, the inventories should not

absorb more than 75% of the working capital. As such a low inventory to working capital

ratio( i.e., a ratio of less than 75%) indicates under stocking, and so, a high liquid

position, while a high inventory to working capital ratio(i.e., a ratio over 75%) indicates

overstocking, and so, a low liquid position.

Table 4.14: Inventory to Working Capital Ratio (in %)

Years Britannia Nirma Dabur Colgate Godrej P&G HUL

1999-00 N.A. N.A. 47.46 92.54 N.A. 97.86 316.60

2000-01 N.A. N.A. 59.18 2302.21 N.A. 74.32 1652.45

2001-02 N.A. 61.88 60.68 128.59 172.89 29.84 533.19

2002-03 N.A. 48.05 92.15 180.59 156.98 25.20 377.60

2003-04 1072.50 13.81 659.88 167.76 164.90 27.59 359.26

2004-05 344.59 12.50 182.22 118.53 196.91 39.68 97.53

2005-06 568.42 32.37 503.79 149.79 208.07 15.82 114.36

2006-07 368.43 48.95 390.23 121.28 418.77 19.84 106.55

2007-08 147.24 57.75 674.50 57.08 1322.16 21.63 1383.04

Average 500.24 39.33 296.67 368.71 377.24 39.08 548.95

CV (%) 18.75 10.45 19.53 32.48 23.34 34.97 18.16

Source: Computed from the annual reports of the companies.

183

Graph 4.12: Inventory to Working Capital Ratio (in %)

500.23

39.33

296.68

368.71 377.24

39.09

548.95

0.00

100.00

200.00

300.00

400.00

500.00

600.00

Britannia Nirma Dabur Colgate Godrej P&G HLL/HUL

FMCGs

Table 4.14 represents the Inventory to Working Capital Ratio, average ratios and CV

value of selected companies for the period understudy.The Inventory to Working Capital

Ratio highest was 2302.21 per cent for Colgate in 2000-01 and lowest was 12.50 per cent

for Nirma in 2004-05 among the selected units during the period of the study. The

average Inventory to Working Capital Ratio highest was 548.95 per cent for HUL and

lowest was 39.08 per cent for P&G during the study period. The CV value of the

Inventory to Working Capital Ratio highest was 34.97% for P&G followed by Colgate

32.48%, Godrej 23.34%, Dabur 19.53%, Britannia 18.75%, HUL 18.16%, and Nirma

10.45% during the period understudy. Thus, it reveals that the Inventory to Working

Capital Ratio of P&G and Nirma was remained consistant during the period understudy.

13. SALES TO FIXED ASSETS RATIO (FIXED ASSETS TURNOVER RATIO)

Fixed Assets Turnover ratio is the ratio between fixed assets and turnover.

Sales to Fixed Assets Ratio = Net Sales

Fixed Assets

184

This ratio indicates as to what extent the fixed assets of a concern have contributed to

sales. In other words, it indicates as to what extent the fixed assets have been utilized.

The standard fixed assets turnover ratio is 5 times. So, fixed assets turnover ratio of 5

times or more indicates better utilization of fixed assets.

In this context, it may be noted that a very high fixed assets turnover ratio means under-

trading, which is not good for the business.

Table 4.15: Sales to Fixed Assets Ratio

(In times)

Years Britannia Nirma Dabur Colgate Godrej P&G HUL

1999-00 N.A. N.A. 4.16 5.24 N.A. 3.48 9.88

2000-01 N.A. N.A. 4.80 6.03 N.A. 3.88 9.07

2001-02 N.A. 1.27 4.76 6.84 5.52 3.84 8.19

2002-03 N.A. 1.14 6.02 6.77 6.00 5.90 7.83

2003-04 11.54 1.00 7.41 11.61 5.42 7.20 6.98

2004-05 16.84 1.14 6.62 13.45 5.99 8.66 7.98

2005-06 12.93 1.28 6.89 7.61 9.50 9.13 8.64

2006-07 11.68 1.24 6.70 8.26 5.38 5.88 9.01

2007-08 10.86 1.39 7.08 8.11 5.94 5.30 12.60

Average 12.77 1.21 6.05 8.21 6.25 5.92 8.91

CV (%) 9.34 9.20 28.22 36.71 36.39 17.18 50.51

Source: Computed from the annual reports of the companies.

Graph 4.13: Sales to Fixed Assets Ratio (in times)

12.77

1.21

6.05

8.21

6.25 5.92

8.91

0.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00

Britannia Nirma Dabur Colgate Godrej P&G HLL/HUL

FMCGs

185

Table 4.15 represents the Sales to Fixed Assets Ratio, average ratios and CV value of

selected companies for the period understudy.The Sales to Fixed Assets Ratio highest

was 16.84 per cent for Britannia in 2004-05 and lowest was 1.00 per cent for Nirma in

2003-04 among the selected units during the period of the study. The average Sales to

Fixed Assets Ratio highest was 12.77 per cent for Britannia and lowest was 1.21 per cent

for Nirma during the study period. The CV value of the Sales to Fixed Assets Ratio

highest was 50.51% for HUL followed by Colgate 36.71%, Godrej 36.39%, Dabur

28.22%, P&G 17.18%, Britannia 9.34%, and Nirma 9.20% during the period understudy.

Thus, it reveals that the Sales to Fixed Assets Ratio of Godrej and Nirma were remained

consistant during the period understudy.

14. TOTAL ASSETS TURNOVER RATIO

Total assets turnover ratio is the ratio between total assets and sales.

Total Assets turnover ratio = Net sales

Total Assets

This ratio indicates the efficiency or inefficiency in the use of total resources or assets of

a concern. It is a measure of the overall performance of the business.

The standard or idle total assets turnover ratio is that the sales should be at least two

times the value of the assets. A total assets turnover ratio more indicates that the assets of

the concern have been utilized effectively.

In this context, it may be noted that a very high total assets turnover ratio indicates over-

trading.

Table 4.16: Total Assets Turnover Ratio (in times)

Years Britannia Nirma Dabur Colgate Godrej P&G HUL

1999-00 N.A. N.A. 1.71 3.55 N.A. 2.34 4.08

2000-01 N.A. N.A. 2.09 4.67 N.A. 2.44 3.51

2001-02 N.A. 1.12 1.89 4.11 6.57 1.88 2.68

2002-03 N.A. 0.98 2.35 3.61 7.75 1.90 2.64

2003-04 3.00 0.88 3.63 4.23 7.37 2.32 2.79

2004-05 3.46 0.88 3.18 4.23 9.44 3.01 4.68

186

2005-06 3.25 0.94 2.82 4.42 7.89 2.18 4.33

2006-07 3.74 0.92 3.59 4.86 3.44 1.90 8.98

2007-08 3.04 0.88 3.64 9.31 3.12 1.86 8.15

Average 3.29 0.94 2.76 4.77 6.51 2.20 4.65

CV (%) 16.42 26.24 16.12 30.27 28.84 44.89 45.15

Source: Computed from annual reports of the companies

Graph 4.14: Total Assets Turnover Ratio (in times)

3.30

0.94

2.77

4.78

6.51

2.20

4.65

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

Britannia Nirma Dabur Colgate Godrej P&G HLL/HUL

FMCGs

Table 4.16 represents the Total Assets Turnover Ratio, average ratios and CV value of

selected companies for the period understudy.The Total Assets Turnover Ratio highest

was 9.44 per cent for Godrej in 2005-06 and lowest was 0.88 per cent for Nirma in 2007-

08 among the selected units during the period of the study. The average Total Assets

Turnover Ratio highest was 6.51 per cent for Godrej and lowest was 0.94 per cent for

Nirma during the study period. The CV value of the Total Assets Turnover Ratio highest

was 45.15% for HUL followed by P&G 44.89%, Colgate 30.27%, Godrej 28.84%, Nirma

26.24%, Britannia 16.42% and Dabur 16.12% during the period understudy. Thus, it

reveals that the Total Assets Turnover Ratio Britannia and Nirma were remained

consistant during the period understudy.

187

15. FIXED ASSETS TO LONG TERM FUNDS RATIO

The fixed assets are shown as a proportion to long term funds as follow:

Fixed Assets to Long Term Funds Ratio = Fixed Assets

Long-Term Funds

This ratio indicates the proportion of long term funds deployed in fixed assets. Fixed

assets represent the gross fixed assets minus depreciation provided on this till the date of

calculation. Long term funds include share capital, reserve and surplus and long term

loans. The higher the ratio indicates the safer the funds available in case of liquidation. It

also indicates the proportion of long-term funds that is invested in working capital.

Table 4.17: Fixed Assets to Long-term funds Ratio

Years Britannia Nirma Dabur Colgate Godrej P&G HUL

1999-00 N.A. N.A. 2.43 1.48 N.A. 1.49 2.42

2000-01 N.A. N.A. 2.30 1.29 N.A. 1.59 2.59

2001-02 N.A. 1.13 2.51 1.67 0.84 2.04 3.06

2002-03 N.A. 1.16 2.57 1.88 0.77 3.10 2.97

2003-04 3.85 1.14 2.04 2.75 0.74 3.11 2.50

2004-05 4.86 1.30 2.08 3.18 0.63 2.88 1.71

2005-06 3.99 1.37 2.44 1.72 1.20 4.18 2.00

2006-07 3.12 1.35 1.87 1.70 1.56 3.10 1.00

2007-08 3.58 1.58 1.95 0.87 1.90 2.85 1.55

Average 3.88 1.29 2.24 1.84 1.09 2.70 2.2

CV (%) 16.51 12.63 11.67 38.77 44.07 31.66 31.19

Source: Computed from annual reports of the companies

188

Graph 4.15: Fixed Assets to Long-term funds Ratio

3.88

1.10

2.24

1.84

1.09

2.70

2.28

0

0.5

1

1.5

2

2.5

3

3.5

4

Britania Nirma Dabur Colget Godrej P&G HLL

FMCGs

Table 4.17 represents the Fixed Assets to Long-term funds Ratio, average ratios and CV

value of selected companies for the period understudy.The Fixed Assets to Long-term

funds Ratio highest was 4.86 per cent for Britannia in 2004-05 and lowest was 0.63 per

cent for Godrej in 2004-05 among the selected units during the period of the study. The

average Fixed Assets to Long-term funds Ratio highest was 3.88 per cent for Britannia

and lowest was 1.09 per cent for Godrej during the study period. The CV value of the

Fixed Assets to Long-term funds Ratio highest was 44.07% for Godrej followed by

Colgate 38.77%, P&G 31.66%, HUL 31.19%, Britannia 16.51%, Nirma 12.63% and

Dabur 11.67% during the period understudy. Thus, it reveals that the Fixed Assets to

Long-term funds Ratio of Britannia and Nirma was remained consistant during the period

understudy.