Embed Size (px)

Citation preview

CHAPTER FIVE

Time Value of Money

J.D. Han

Learning ObjectivesLearning Objectives

1. Explain what is meant by the time value of money.

2. Define Present Value versus Future Value

3. Define discounting versus compounding.

4. Explain the difference between the nominal and the effective rate of interest.

5.1 Introduction5.1 Introduction

Time value of money -$1 received today is worth more than $1 received

tomorrow, or vice versa

- Present Value of $1 tomorrow is less than $1: $1 discounted by interest rate

- Future Value of $1 today is more than $1: $1 compounded by interest rate

*Simple versus Compound *Simple versus Compound Interest RateInterest Rate

Investing $1000 at 3% per year for 4 years

According to Simple Interest:4 years later The total future cash flow isF = $1000x (1 + 0.8x4)=$1,320

According to Compound Interest: F = $ 1,000 (1+0.08)(1+0.08)(1.08)(1.08) =$1,000(1.08)4 =$1,360.49

5.2 Compound and 5.2 Compound and Discounting VariablesDiscounting Variables

P = current cash flowF = future cash flowPV = present value of a future cash flow(s)FV = future value of a cash flow(s)

i = the stated (or nominal) interest rate per period r = the effective rate of return per periodn = # of periods under consideration

A = the amount of annuity

Compounding and DiscountingCompounding and DiscountingCompounding :For now i = r with an annual compounding

and annual payment

Fn = P(1 + r)n

OR

FV = PV(1 + r)n

The equations represent the compounding relationship that is the basis for determining equivalent future and present values of cash flows

DiscountingDiscounting

PV = FV

(1 + r)n

Discounting – the process of converting future values of cash flows into their present value equivalents

AnnuitiesAnnuities

Annuity – series of payments over a specific period that are of the same amount and are paid at the same interval where one discount rate is applied to all cash flows

Examples of annuities: interest payments on debt and mortgages

Future Value of an AnnuityFuture Value of an Annuity

1) Numerical Illustration: i= 10%; annuity of 4 years

Year

1 2 3 4

$1000 ------------------------------ 1,331

$1000--------------------- 1,210

$1000----------->1,100

$1,000

Total FV = 4,641

2) Formula

FV = A(1+r)n-1+A(1+r)n-2 + …..+A(1+r)+ A

r

nrAFV

1)1(

Present Value of an AnnuityPresent Value of an Annuity

Year

1 2 3 4 5

1000 1000 1000 1000

909

826

751

683

Total PV = $3,169

2) Formula

PV = A/(1+r)+A/(1+r)2 + …..+A/(1+r)n

rr

APVn)1(

111

*Annuity Due*Annuity DueAnnuity due - payments are made at the

beginning of each period (Example: leasing arrangements)

PV = A + A/(1+r)+A/(1+r)2 +…..+A/(1+r)n-1

Formula: multiply the future or present value annuities factors by (1 +r)

)()(

rr

rAPV

n

1

1

111

** Relationship between FV and PV Formulas

FV = A(1+r)n-1+ A(1+r)n-2…..+A/(1+r) + A

PV = A/(1+r)+A/(1+r)2 + …..+A/(1+r)n

FV = PV/(1+r)n

PerpetuitiesPerpetuities

Exist when an annuity is to be paid in perpetuity

Present value of PerpetuityExample: Equities

r

APV

5.3 Effective Interest Rate: 5.3 Effective Interest Rate: Varying Compound PeriodsVarying Compound Periods

Quoted or Nominal interest rate : iperiod interest rate x # of periods in a year

i annua = i sub-period times # of sub-periods in a year

im = i / m

One Complication which creates One Complication which creates the gap between r and the gap between r and i:i:

The effective annual interest rate is not simply liner times of the effective sub-annual interest rate; It is a compounded one:m=1, 2, 4, 12, or 365 times compounding by lender(bank)

Effective Annual interest rate: r actual interest rate earned/payable after adjusting the

nominal/quoted interest rate for the number of compounding periods

(1+rannual) = (1+ i/m)m

Second ComplicationsSecond Complications

The frequency of interest payments by borrower

(1+Effective Annual Interest Rate) =(1 + Effective Semi-annual Interest Rate)2 =(1 + Effective Quarterly Interest Rate)4

=(1 + Effective Monthly Interest Rate)12

= (1 + Effective Daily Interest Rate)365

= ( 1 + r f ) r

Formulas: Effective Interest RatesFormulas: Effective Interest Rates

Effective annual rate formulam = # of compounding by lender per year

Effective period rate formula

f= # of payments by borrower in a year; 1, 2, 4, or 12

11

m

m

iannualr

11

f

m

m

ieffectiver

*Numerical Examples*Numerical ExamplesSavings at (the ‘quoted’ annual interest rate of) 12% ‘compounded

quarterly;

Effective Quaterly interest rate = 12%/ 4 = 3%;

Effective annual interest rate rannual:

rannual = (1+0.03)4 -1= 0,1255 or 12.55%;

Effective montly interest rate rmonthly :

(1+ rmonthly)12 = 1.1255%

rmonthly = (1.1255)1/12-1 = 0.009901or 0.9901%

5.4 Amortization of Term Loans5.4 Amortization of Term Loans

Common computational problems with term loans or mortgages include:

1. What effective interest rate is being charged?

2. Given the effective interest rate, what amount of regular payments have to be made over a given time period, or what is the duration over which payments have to take place given the amount?

3. Given a set of repayments over time, what portion• represents interest on principle?• represents repayment of principle?

Repayment Schedules for Repayment Schedules for Term Loan and MortgagesTerm Loan and Mortgages

Most loans are not repaid on an annual basis

Loans can have monthly, bi-monthly or weekly repayment schedules

In Canada, interest on mortgages is compounded semi-annually posing a problem in calculating the effective period interest rate

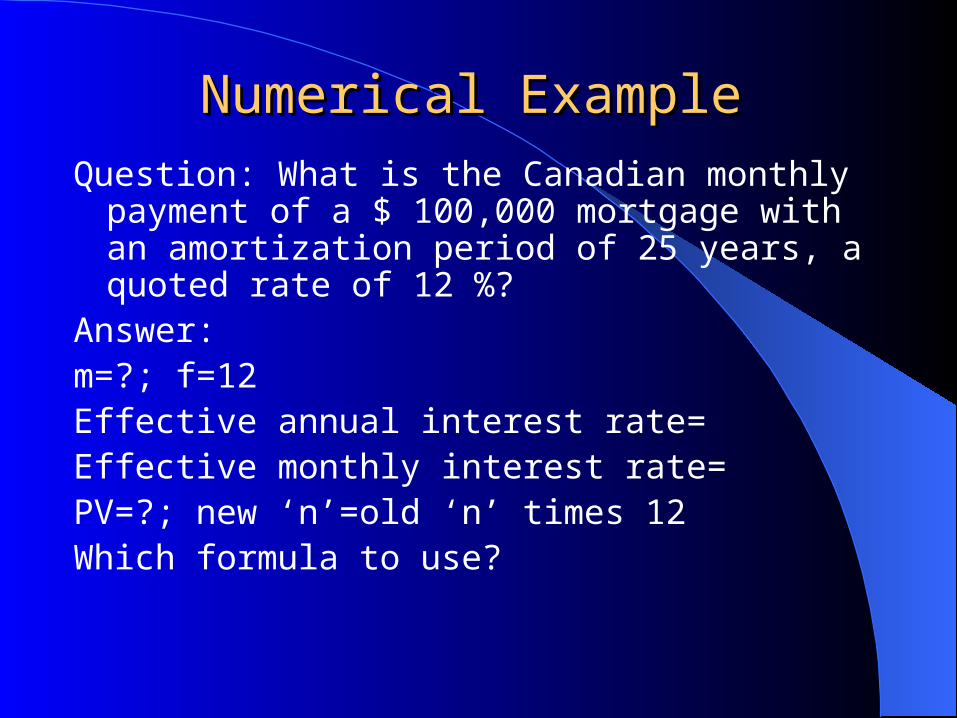

Numerical ExampleNumerical Example

Question: What is the Canadian monthly payment of a $ 100,000 mortgage with an amortization period of 25 years, a quoted rate of 12 %?

Answer:m=?; f=12Effective annual interest rate=Effective monthly interest rate=PV=?; new ‘n’=old ‘n’ times 12Which formula to use?

Numerical ExampleNumerical Example

Answer:

m=2; f=12

Effective annual interest rate= (1+0.12/2)2-1

Effective monthly interest rate= [(1+0.12/2)2]1/12-1

PV=100,000; n = 300

00975000975011

11000100

11

11

300

.).(

,

)(

A

rr

APVn