Embed Size (px)

Citation preview

CHAPTER II

METHIOPOLOGY

2.1 STATEMENT OF PROBLEM

"Institutional Farm Credit Recovery Issues in Tiruchirapalli District

1990-91 to 1994-95 - A Multidimensional Analysis."

2.2 AN OVERVIEW OF INSTITUTIONAL FARM CREDIT

India has been and will remain in the future, a predominantly

agricultural country. India is a country of .villages. About 75% of people

live in rural areas. Agriculture in its broad connotation accounts for

approximately 50% of its gross national product (GNP). Much emphasis is

on for economic development to revitalise the rural sector which constitutes

the backbone of the Indian economy accounting for over a third of Gross

Domestic Product (GDP).

Agriculture has been die traditional primary occupation of die

peasantry in Tamilnadu. Most of the people living in rural areas are engaged

agricultural activities by way of raising crops suitable to die area based on its

resources like soil, irrigation, backward and forward linkages - for their

income generation. In addition to agricultural activities as their main

occupation, subsidiary occupations like dairying, poultry, sheep/goat rearing

etc. are undertaken in which mostly womenfolk are involved.

With the advent of the Green Revolution (late 1960s) in India with the

main objective of producing more agricultural produce to meet the needs of a

growing population, an improved package of high yielding/hybrid seeds,

inorganic manures (chemical fertilizers), pest and disease control measures,

use of farm machinery, etc. was introduced. This innovative approach

attracted cultivators to invest more to meet the cost of inputs for getting high

productivity. Another consequence, beneficial both to the farmer and also

the society in general is the commercialisation of agriculture that

mechanisation promotes. The farmer produces more than before and much

more than he needs for self consumption. This leads to an increase in

income. However, the cost of high yielding/ hybrid seeds, fertilizers, plant

protection chemicals, tractors for ploughing, plant protection chemicals and

chemical fertilizers could not be met without additional money being

ploughed in. Here comes the importance of credit support from outside

agencies - both non-institutional and institutional sources.

2.2.1 SIGNIFICANCE OF INSTITUTIONAL FARM CREDIT

The institutional credit system has shown the way for comprehensive

development comprising agricultural productivity, creation of better

employment opportunities in rural areas, improving farm systems and

development of other agricultural sub systems such as livestock farming,

fisheries, farm forestry, social forestry, sericulture, horticulture and support

activities. A basic requirement for making credit an effective instrument

for a dynamic agriculture is to change the agrarian scenario so that farming

and other related activities become a profitable proposition. The basic-

objective of the rural credit system is to provide adequate and timely credit

for agriculture and related activities to enable rural people to exploit

opportunities for development. Banking is one of the institutions involved in

the process of development. In India, till the introduction of social control

over Banks (Nationalization - 1969), financing of agriculture did not take

place. It is worth mentioning that during the pre-nationalization period

(1951-1968) the share of agricultural credit to total credit remained at 2%

only.

2.2.2 RECOVERY OF FARM CREDIT .

In a credit delivery system, repayment of loans play a vital role in

recycling of funds to assist more and more number of farmers as well

implement more schemes for agricultural development as a whole. Timely

credit and timely repayment/recovery are important in financing of

production oriented schemes. Proper repayment of loans encourages further

lendings failing which it demotivates die bankers who tend to avoid further

lendings in view of accountability on the part of the lender (Bank Official).

Mounting overdues in farm credit disbursements causes serious concern

amongst planners, bankers, National Bank for Agriculture and Rural

Development (NABARD), Reserve Bank of India and even public

representatives including such as Hon'ble Minister of Finance, Government

of India. Low recovery performance is not only restricting the benefits to

beneficiaries in terms of low cost capital but also jeopardizing the interest of

the lenders who go to the level of blacklisting some of the villages having

recalcitrant borrowers. This is highly detrimental to developmental activities

as well as to financial institutions. The then Finance Minister Chidambaram

P. said that "we need to revitalize and restore the rural credit system, die

system just cannot be sustained if loan recovery rates are under 60 per cent".

(The Hindu, Chennai, June, 1996) This is very much pertinent when loan

disbursements are increasing every year with increased demand due to

technological innovations, HITECH agricultural projects, more area brought

under irrigation through major, medium and minor irrigation projects,

increased need for poultry products, sheep/goat flesh for consumption, etc.

The tendency for mounting of overdues will also increase simultaneously.

Non-repayment by die borrowers under farm credit is a great burden for

them and it creates a barrier between die borrowers and die lending

institutions. This will ultimately drive poor people into the hands of local

money lenders who will in turn exploit them financially. From the data

available region-wise in India, district-wise in Tamilnadu and bank-wise in

Tiruchirapalli, it can be seen diat a high amount is overdue every year which

is increasing (State level bankers' committee meeting notes. Indian Overseas

Bank-Chennai).

2.3. SCOPE OF THE STUDY

The present research focuses only on institutional farm credit

recovery issues in Tiruchirapalli district for a period of 5 years, i.e. 1990-91

to 1994-95 and is a multi dimensional analysis of socio-economic and

political dimensions.

While a bank's finance helps the borrower to generate sufficient

income for repayment, the willingness to repay die loans plays an important

act in recovery of loans. The willingness' is controlled by certain socio

economic and extra-ordinary factors. The recovery process revolves around

2 basic questions.

Can the borrowers repay ?

Will the borrowers repay ?

The reasons for default may be broadly categorised as follows:

• Diversion of borrowed bank money

• Loss of investments

• Negative attitude towards prompt repayment

2.3.1 CAN THE BORROWERS REPAY ?

This involves the use of borrowed funds properly and generation of

adequate surplus or incremental income to meet the repayment commitments.

The activities should perform well and marketing aspects be fulfilled in

time. In case of sugarcane crop cultivation under tie-up arrangement, prompt

repayment is not forthcoming due to delayed cuttings and delayed cane

proceeds due to the reasons in-built in die sugar industry. This can be taken

as a default committed by the borrower. So also in die case of paddy

cultivation die default due to late marketing for want of better and stable

market price because of huge arrivals after die harvests. Is it to be taken as

wilful default of die borrower concerned?

2.3.2 WILL THE BORROWERS REPAY ?

This is the crux of the recovery problem. This reveals the basic-

attitude of the borrowers towards repayment of loans obtained for generation

of income from raising of crops or creation of assets like milch animals

(dairying) for production of agricultural commodities and milk respectively

and for marketing of produce ultimately.

Even though tlie borrowers have got adequate surplus to repay, they

are not prepared to fulfil their repayment obligations, due to obvious reasons

like diversion of funds for some other productive and unproductive purposes.

Prompt repayment depends mainly on the integrity and honesty of the

borrowers.

The magnitude of tlie problem of recovery is serious in this case and

tlie lender has to waste time and energy on proceeding with recovery efforts

by legal means which is normally protracting leading to loss of time, money

and manpower. This also creates a virtual block on liberal lendings for

agricultural purposes by tlie banker. Sometimes, even a few cases of default

in a village will lead to blacklisting tlie entire village affecting genuine

people in getting financial assistance with or without subsidy.

The Agricultural and Rural Debt Relief Scheme - 1990 by the central

government provided relief to the overdue borrowers with a view that the

borrowers get out of the default list subjected to effective recovery efforts

and in order to assist them for further needs. Though tlie Government

introduced the scheme with a huge financial outlay from the exchequer, the

ill effect in die minds of the prompt repayers for not having enjoyed the

benefit has been generated simultaneously.

The problem of overdues due to the complimentary effect of

borrowers and lenders deserves exploratory research to enlist the factors

responsible for regular repayment and reasons for default widi a view to

suggest suitable measures for improving the situation for the benefit of both

the lender and borrower.

2.4. RESEARCH DESIGN

The research work attempts to understand the nature of prompuiess

and defaultness in repayment of farm credit granted for productivity purposes

to different banks for short term and term leadings. Short term lendings are

provided for raising of crops not exceeding a period of IS months and term

lendings for creation of productivity assets to generate income during a

certain period of time. The research work has been undertaken by contacting

both the lender and borrower so as to find out the reasons for promptness and

defaultness in repayment by the borrowers as well as recovery efforts by the

bankers. The nature of the study may also contribute to assess the actual

position of the beneficiaries in respect of their credit received and repaid as

well as help in assessing the opinion of the lenders who are involved in the

selection of borrowers and conducting follow up measures for recovery of

bank dues. The study also aims to find out the socio, economic and political

tactors with regard to the repayment of credit particulars in an area having

irrigation potential, good soil condition, availability of other inlrastructural

facilities like marketing, supply of agricultural inputs, transport, road, etc.

With a view to conduct this research properly, purposive and random

sampling techniques had been adopted at different stages.

2.5. PILOT STUDY

A detailed discussion with the Lead Bank, National Bank for

Agriculture and Rural Development (NABARD), the Block Development

Office, District Central Co-operative Bank, Land Development Banks and

other commercial bank officials was made to assess die necessity for this

research study. Ultimately, the aim has been to find out the reasons for

defaultness mainly in an area where the facilities for providing farm credit,

production efforts, etc. are conducive. The secondary data collected at the

state level, district level and block level from the State Level Bankers

Committee (SLBC - Indian Overseas Bank, Chennai), District Consultative

Committee (DCC - Indian Overseas Bank, Tiruchirapalli), District

Collectorate ( Agriculture Section), Block Development Office have paved

the way for conducting the research at Lalgudi Block of Tiruchirapalli

District. The choice of the topic on farm credit recovery wa:̂ discussed in a

Block Level Bankers' Committee Meeting held and got endorsed for conduct

of research based on its urgent need.

2.6 SELECTION OF TIRUCHIRAPALLI DISTRICT AS UNIVERSE

OF THE STUDY

According to SLBC, Chennai (1994), as on 30.9.1994. it was reported

that Tiruchirapalli District stood first in granting of farm credit to the tune of

Rs.226.36 crores (6.8%) to 301400 (9.86%) borrowers among 23 districts of

the state (State level bankers' committee notes - IOB, Chennai). The overdue

position of the district has been at 30.20% (5 years average June 1991 to

June 1994) and the amount of average overdue recorded was Rs.34.67 crores

as against the average demand raised of Rs. 114.94 crores which can be

considered a serious one. (District Consultative Committee Meeting notes -

I.O.B. Tiruchirapalli). It warrants further research to find out the actual

reasons for the borrowers and bankers and to suggest measures for its

improvement. Secondly, Tiruchirapalli district was selected for research

study based on the working place of the research scholar who is placed at the

State Bank of India, Zonal Office, Tiruchirapalli. Further, the rapport

maintained by the researcher as an agricultural banker in the district from

1990 to June 1997 has been very helpful in collecting the data required at die

district and block level as well as banks and branches level of commercial

banks, co-operative banks and land development banks. It is heartening to

note the support extended by the bankers in scrutinising their loan ledger

records which is not normally exposed to any outsider. There are 34

commercial banks, and 3 co-operative banks and 1 state financial institution

having a net work of 389 branches in the district of which 186 are rural

branches (47.81%).

61

2.7. SELECTION OF BLOCK - LALGUDI

Timchirapalli district (undivided) has got 32 development blocks. The

district has been recently (1997) trifurcated viz. Timchirapalli, Karur and

Perambalur for administrative conveniences. The district has got both

irrigated and unirrigated areas for raising of crops. Under normal

agricultural banking, tine farm credit goes mainly to irrigated crops like

paddy, sugarcane, banana, gingelly, etc. Timchirapalli district being blessed

witli the Mettur Canal Project of the Cauvery river has a larger area covered

by paddy crop with two crops sequence. Secondly, with the commissioning

of M/s Kothari, Cauvery and EID Parry Sugars Private Ltd. Mills and

Perambalur Sugar Mill, the area under sugarcane crop has been on the

increase. Being the "Banana District "of India, there is good scope for

extending crop loans for these crops.

As per the Lead Bank Annual Credit Plan (Lead bank office - IOB -

Timchirapalli), the credit target for FARM' CREDIT (Agricultural Loans).

the highest credit absorbing block is Lalgudi Block (Rs.9.55 crores - 1994-

95) which has got 100% of its cultivated area under irrigation. Lalgudi is 23

kms. away from Timchirapalli. This block has got different crops under

cultivation mainly paddy, sugarcane, banana, gingelly, all which attracts a

larger amount of farm credit as short term loan (crop loans). The scale of

finance per acre, i.e. crop loan amount for sugarcane and banana has been

the highest which ultimately shows larger credit disburses every year.

Paddy being a short duration crop (4-5 months), it is being rotated as Paddy

after Paddy in Kuruvai and Thaladi (Late Samba) seasons with the help of

Mettur Canal Project water coupled with ground water resource by way of

borewells. Lalgudi Block being a paddy growing area, scope for rearing

milch animals has been bright with adequate production of paddy straw for

feeding of animals besides availability of green grass. Granting of milch

animal loans under subsidy scheme (Integrated Rural Development

Programme) and Bank Scheme without subsidy has been in vogue in this

block due to reasons of the existence of agricultural labour, marginal and

small farmers in larger numbers. Commercial dairies have been initiated by

some progressive farmers in the block for production of milk. With the

availability of good soil types, irrigation through canal and ground water,

proximity of the town to Tiruchirapalli, the credit flow has been on die

increase which may subject it to the increased problem loan recovery as

credit disbursals increase.

In Lalgudi Block there are 53 revenue villages, 43 panchayats and 2

town panchayats. (FIG.2). According to the 1991 census, the total

population was recorded as 132462 of which male were 66342, females

66120, SC - 28951, ST - 122. The literate people among the male and female

are 46148 and 33056 respectively. Among the population, labour force

occupies 23383, 13004 and 8740 with agricultural labourers, cultivators and

non- agricultural labourers respectively. Net area sown was 15431 hectares

and gross cropped area was 18687 hectares. The area under paddy,

sugarcane, banana, groundnut were 12229, 1757, 71721, 518 hectares

respectively. The nonnal rainfall of tlie block is 1015 mm which is above

tlie district level of 842 mm. Regarding tlie banlcing network, tliere are 10

commercial banks, 1 district central co-operative bank, 1 primary land

development bank and 18 primary agricultural co-operative banks.

2.8. SELECTION OF BANKS

Lalgudi block with its high resources for agricultural production and

tlie presence of tlie Sugar Mill M/s Kothari Sugars Pvt. Ltd. at Kattur, has

seen remarkable improvement in agricultural activities. With these

favourable factors for banking activities, commercial banks like State Bank

of India, nationalized banks, private bank, primary agricultural co-operative

banks and primary land development banks are in operation in tlie entire

block area. With tlie introduction of Service Area Approach by tlie Reserve

Bank of India (1989), the villages have been allocated to each designated

bank branch based on proximity, contiguity and earlier financial connections

for tlie commercial banks. The primary agricultural co-operative banks have

been allowed to continue their operations in their own jurisdiction. Hence.

in a village, both a commercial bank branch and a primary agricultural co

operative bank are operating to assist the needy people for productive

purposes.

It was decided to identify a commercial banks, primary agricultural

co-operative bank and primary land development banks as three units which

are extending short term (crop loans) and term loans for Land Development,

minor irrigation, farm mechanization, dairy, etc. These loans are for all

categories of fanners, viz. agricultural labourers, marginal/small farmers and

big fanners and are for agricultural development. They are extended mostly

for priority sector 1 endings, viz. small scale industries, small business finance

and agriculture. As there are 3 different commercial banks, viz. State Bank

of India, nationalized banks, (Indian Bank, Indian Overseas Bank, Bank of

Baroda) and private bank (Lakshmi Vilas Bank), a single bank has to be

selected for the purpose of selection of universe. It was proposed to select a

bank based on the average quantum of farm credit extended from 1990-91 to

1994-95. Accordingly, based on the data collected from all the banks, it was

decided to select State Bank of India which has extended die largest farm

credit in the block among die commercial banks group.

2.8.1 SELECTION OF BANK BRANCH

It was proposed to list out the farm credit disbursals excluding Jewel

Loans with the 5 years average loan amount outstanding in the bank books

for all die branches under State Bank of India, Primary Agricultural Co

operative Banks, to select the first ranking bank branch. Accordingly, based

on the data listed, Kattur Agricultural Development Branch (ADB) of State

Bank of India, and Primary Agricultural Co-operative Bank, Anbil were

selected for the purpose of selection of respondents. As diere is only one

unit - Primary Land Development Bank at Lalgudi catering to the financial

needs of Lalgudi Taluk which includes Lalgudi Block, the same was

selected.

2.8.2 SELECTION OF ACTIVITIES (SCHEMES) - CROP LOAN &

DAIRY LOAN

Crop loan for raising of paddy, sugarcane, banana, gingelly, etc. is

the major activity under farm credit extended by the selected bank branches.

It is a form of short term credit. Besides, instalment credit for creation of

milch animal under dairying is an activity provided with credit by the banks

and has been selected for study. Primary Agricultural Co-operative Bank,

Anbil has distributed crop loans and dairy loans. Suite Bank of India, Kattur

Agricultural Development Branch has disbursed credit for crop loans as a

major activity. Primary Land Development Bank, Lalgudi has disbursed

credit for Dairying.

2.9. THE UNIVERSE

A list of crop loan borrowers who have received crop loan during

1994-95 (1.4.1994 to 31.3.1995) was prepared from the loan disbursed

records of the branches of State Bank of India, Kattur A.D.B. and Primary

Agricultural Co-operative Bank, Anbil. A list of dairy loan borrowers who

have received loans during 1990-91 from Primary Agricultural Co-operative

Bank, Anbil and during 1991-92 from Primary Land Development Bank.

Lalgudi was prepared as the universe of the research. The crop loan is due

for payment from 6-8 months for paddy, 12-14 months for sugarcane, 12

months for banana, 6 months for gingelly crops. For dairy loans, Primary

Agricultural Co-operative Bank, Anbil has fixed a repayment of 3 years and

Primary Land Development Bank, Lalgudi has fixed 5 years as repayment

period. Annual instalments were fixed for Dairy Loans. The study has got

the reference period from 1990-91 to 1994-95 (5 years), hence die list of

borrowers has been prepared during a year within this period for the purpose

of selection of respondents to collect empirical data.

2.10 SELECTION OF RESPONDENTS

From die universe list prepared, 25 % of respondents under sampling

method were selected for Personal interview purpose based on Lottery

Method for crop loans. For dairy loans census method was selected. In total

30% of the universe was selected as respondents. Before fixing the

respondents under crop loans the list of universe was stratified according to

crop-wise borrowers. Under dairy loans, as the universe was limited, it was

decided to adopt census. The details of sampling is as follows:

TABLE 2.1

SELECTION OF RESPONDENTS

No

i.

11.

111.

Bank Branch

Crop Loans Primary Agricultural Co-op. Bank. Anbil a) Paddy h) Sugarcane c) Banana d) Gingelly Sub Total State Bank of India. Kattur A.D.B. a) Paddy b) Sugarcane c) Banana Sub Total Total Dairy Loans P.A.C.B.. Anbil P.L.D..B. Laliiudi Sub Total Grand Total

Universe

229 143

3 20

395

70 294 21

385 780

35 23 58

846

Respondents

56 49

1 6

112

16 59

5 80

192

35 23 58

250

Percen-tage

24 34 33 30 28

23 20 24 21 25

100 100 100

30%

The universe under reference is the total number of borrowers listed

out during 1994-95 in case of crop loans received from Kattur ADB (State

Bank of India) and PACB, Anbil and Dairy Loans received during 1990-91

(PACE. Anbil 1991-92 )Primary Land Development Bank, Lalgudi). From

the above universe (total borrowers) 25 % of the borrowers were selected as

the respondents by random sampling method in case of crop loans and 100%'

under Dairv Loans.

The selected sample borrowers (respondents) were given numbers as

follows:

I.

II.

III.

P.A.C.B. Anbil

P.L.D.B. Lalgudi -

S.B.L Kattur A.D.B

- Crop Loan

(112/395)

Dairy Loans

(35/35)

Dairy Loans

(23/23)

- Crop Loans

(80/385)

Paddy

Sugarcane

Banana

Gingelly

•

Paddy

Sugarcane

1-C-P1 toP56

1-C-S1 toS49

1-C-B1

1-C-G1 toG6

1-D-l to 35

2-D-l to 23

3-C-P1 to P16

3-C-S1 to S59

Banana 3-C-B1 to B5

The respondents represent the whole block and are spread in the

following villages.

TABLE 2.2

LIST OF VILLAGES SELECTED

1. Neikuppai 2. Kamarajapuram Cly. ?-. Muthurajapuram 4. Dhamianatliapurain 5. Arivur 0. Mettupatti 7. NaL'ar 8. Mankkal 9. Kurichi lO.Siruinayaiiiuidi 1 l.Kotliamangalam l2.K.atiur

13.Pervalanallur 14.Poovalur 15. Vdayuthanpettai 16.Pathukattu 17.Konnakudi lS.Thinniyani 19.Sekaraiyur 20. Aiantrudi Mahajauaiii 21.Keda Anbil 22.Kalaihiiveiulram 23.Kuinarapalayani 24.T.Kalvikudi

25.Mullal 26.Tliiruniauaniedu 27.Pachanipettu 28.Komakudi 29.Semb;iiai 30. Vtnavakapuram 31. Mangamnialpuram 32. Venkaiajalapurani 33. Sangamanrajapuraiii 34.Anbil Padut'ai 35.Siruthaiyur 36.LaliJudi

2.10.1 SELECTION OF BANKERS

In order to know the bankers' view on recovery of farm credit which

they have been personally involved right from the selection of borrowers,

activity, disbursements, guidance, follow up and finally recovery of farm

credit. Almost all the bankers (19) operating in the block were selected as

respondents. The branch managers, field officers, secretaries and field

supervisors were requested to answer a questionnaire which was explained to

them personally by the researcher. The questionnaire was designed based

on experience of the researcher in the field of agricultural banking since 1978

and discussion with senior officers of the bank working in various banks

including lead bank office, regional/zonal offices and local head office. The

aim is to examine the farm credit officers' knowledge on bank policies and

priorities, credit management, follow up of farm credit, difficulties

experienced during recovery visits, factors influencing prompt recovery,

obstacles in prompt recovery, recovery efforts by die bankers, opinion on

good and poor recovery factors, and suggestions for better recovery

performance.

2.11. TOOLS OF DATA COLLECTION

The primary data have been collected by means of the survey method.

This metliod involved personal contact with die help of a interview schedule

specially designed for the purpose in the case of sample borrowers and a

questionnaire for die sample bankers. After careful discussion with die

research supervisor, external expert and bankers involved in farm credit

disbursals and recovery, an interview schedule for the borrowers was

designed with the following details, viz. personal particulars, economic

status, cropping pattern, banking transaction, quantum of liability (non-

institutional source), investments made during the reference period, income

from farming and other sources, pattern of expenses, source of information

for banking transaction, experience in availing bank loan, training undergone

for conducting the activity, intervening influence, suggestions to ensure

prompt repayment, attitude towards repayment etc.

2.12. PRE-TESTING

The borrower's interview schedule and bankers questionnaire

were pre-tested with persons outside the sample (respondents) for its

relevance and effectiveness and accordingly the schedule and questionnaire

were finalised.

2.13. DATA COLLECTION

As most of the borrowers/respondents are illiterate, low level of

literacy interviewing by face to face method was used with the aid of an

interview schedule for collecting the necessary data/particulars. The

borrowers may have needed help in explaining the questions for clarity to

answer properly. It was a herculean task for the researcher to meet all die

250 borrowers at their door step in remote villages but the local bank

officials/staff were very helpful in identifying and introducing the borrowers

to the researcher even at the early and late hours of the day. The interview

took place mostly in the early morning and late evening, people are available

at home after their day's work in the field. The discussion with each

borrower has taken not less than 30 minutes -and at times exceeded more than

a hour depending upon die borrowers' capacity to understand and recollect

the past details especially income and expenses. The borrowers' were frank

and open in furnishing the details. The researcher had to travel by a two

wheeler to remote villages due to inadequate bus transport.

2.14. CONSTRUCTION OF ATTITUDE SCALE TOWARDS

REPAYMENT

By way of contribution to this research work, a new attitude scale was

constructed based on judges (experts) opinion initially on a 5-Point

continuum range. Out of 65 judges, 40 responded from all over India.

Finally 10 statements (5 negative and 5 positive") were selected for

administering with borrowers for analysis on their most favourable.

favourable and less favourable attitude towards repayment of institutional

credit.

Attitude is defined as the degree of positive or negative affect

associated with some psychological object (Thurstone 1946). Attitude is a

tendency to accept or reject an individual or group of people or ideas or

institution. According to Thurstone, by it means any symbol, phrase,

slogan, person, institution, ideal or idea towards which people can differ with

respect to positive or negative affect. Right from 1920, psychologists,

politicalscientists, sociologists and educationists have been using continuously

scales for measuring attitudes.

Rogers and Shoemaker (1971) explained attitude as a relatively

enduring organization of individual's belief about an object that pre-disposes

his action.

To measure attitudes there are different methods. According to Krech

and Crutchfield (1948) "Of all methods of measurement of beliefs and

attitudes, by for the most prominent, the most widely used and the most

carefully designed and tested is the attitude or opinion scale "

Attitude scale can be constructed through paired comparison, Equal

Appearing Methods and by Summated Rating Method. In this study, equal

appearing interval technique is used to construct attitude scale to measure the

attitude of the borrowers who have received crop loans for raising various

crops like paddy, sugarcane, banana and gingelly and term loan for purchase

of dairy animals towards repayment of the loan amount due to the bank

within the prescribed repayment period.

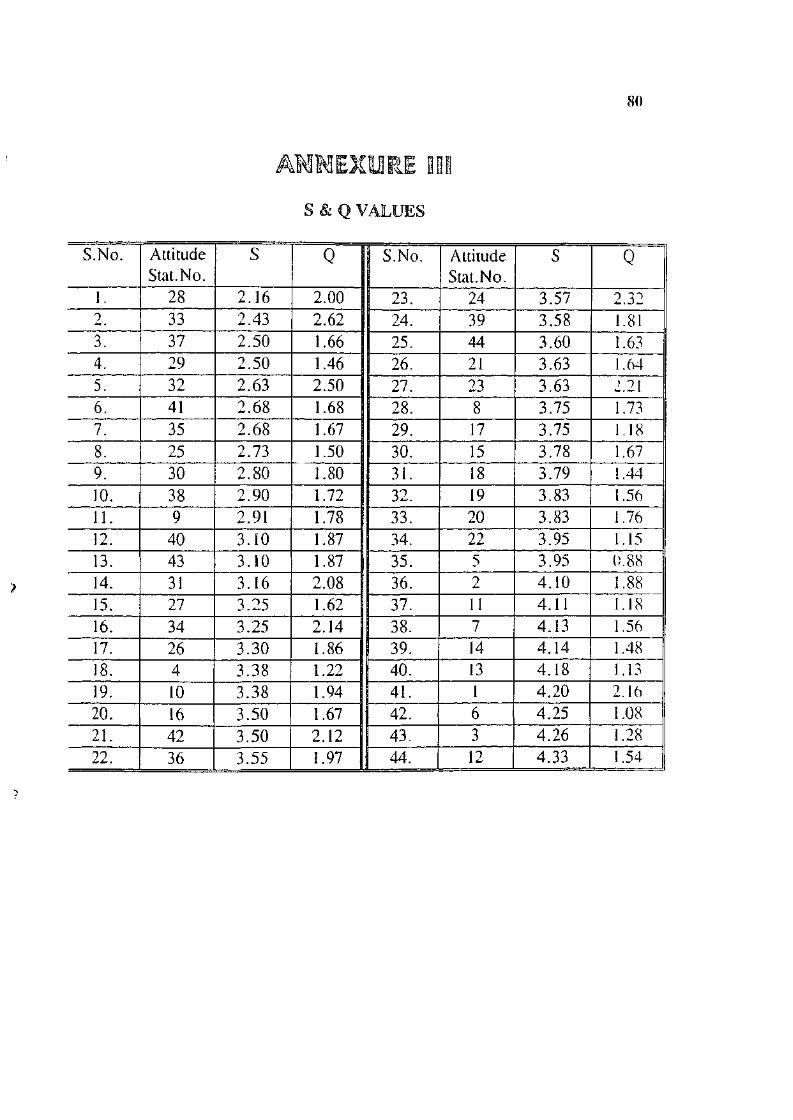

79 statements relating to the psychological object to be measured

namely repayment of farm credit were collected from all possible sources

based on the field experience of die researcher, other bankers' experience,

borrowers' versions and home related literature. Then they were edited on

the criteria suggested by Edwards (1969) and finally forty four statements

were selected (Annexure I).

As suggested by Webb (1959), all die forty four statements were then

administered for judgement on a five point continuum ranging from most

unfavourables to most favourables (Annexure II). This list was sent to 65

judges selected for the study comprising of the agricultural extension and

rural sociologists and agricultural economists of Tamilnadu, Kerala,

Karnataka, Andhra Pradesh, New Delhi, Gujarat, Maharashtra, Punjab. Of

the 65 judges 40 responded the statements after duly recording their

judgements. The responses of 40 judges were considered for calculation of

the scale and "Q"values of the attitude statements (Annexure III).

For the selection of final attitude statement to constitute a scale, the

following criteria were used

a) The statement selected should represent the universe of

opinions or content with regard to repayment of institutional

farm credit.

b) The scale values should have equal appearing interval, i.e.

distributed uniformly along the continuum.

c) The statement should have smaller uQ"values as far as

possible.

d) These should be equal number of statements with favourable

and unfavourable attitudes as far as possible.

Based on these criteria 10 attitude statements were finally selected.

The scale values of these statements ranged from 2.50 to 4.33 with

approximate interval of 0.18. The "Q" value ranged from 1.46 to 1.54

(Annexure IV).

In this study, reliability of the scale was determined by "Split-Half

Method. The 10 statements were divided into two halves by odd-even

method. The two parts were administered separately to 30 borrowers (non-

sample). Thus, single borrower had two scores based on each half. The

correlation co-efficient between the two sets of scores was 0.85 and the

values were found to be highly significant.' Thus the scale constructed to

measure the attitude towards repayment of institutional farm credit was a

reliable one.

A scale possesses validity when it actually measures what it claims to

measure (Goode and Halt 1958). it was necessary to establish whether the

scale developed was valid. In this study, content validity has been

established.

Content validity is a kind of validity by assumption. The main criteria

is how well the contents of the scale sample matches the subject matter which

is important for the variable under study. This was ensured by pursuing

relevant literature, discussion with social scientists, rural bankers and

members of doctoral committee for collection and selection of statements for

the construction of the scale.

The 10 attitude statements selected finally were arranged randomly in

the data collection tools in order to avoid biased responses which might

contribute to low reliability and detraction from validity of the scale. In the

final format, there were 5 columns representing a Five point continuum

(Likert Scale) of agreement or disagreement to the statements. The five

points on the continuum were strongly agree, agree, neutral (undecided),

disagree and strongly disagree with respective weights 5,4,3,2 and 1 for

favourable statements and 1,2,3,4 and 5 for unfavourable statements.

This format of attitude scale was administered to the respondents.

They were asked to respond to each statement in terms of their own degree

of agreement or disagreement by making a tick mark in the appropriate

column during the interview. The total score for an individual was obtained

by adding the weights of all 1 to 10 statements. Categorisation was done

based on cumulative frequency method as less favourable, favourable and

more favourable.

2.15. LIMITATIONS OF THE STUDY

It is essential to mention that the field study is limited to three

branches only. One from Commercial Banks, the second from Primary

Agricultural Co-operative Bank and tliird from Primary Land Development

Bank. State Bank of India, Kattur Agricultural Development Branch, a

specialised branch for Agricultural Banking and the Primary Land

Development Bank branch are situated at Lalgudi Centre and operate through

Lalgudi Block. But the State Bank of India, Kattur Agricultural

Development Branch is operating in 13 villages only under Service Area

Approach concept introduced during 1989.

![[Introduction] - WordPress.com · · 2012-06-25Chapter - Introduction Discrete Structures Samujjwal Bhandari 2 Introduction Discrete Mathematics deals with discrete objects. Discrete](https://img.pdfslide.net/doc/110x75/5b18f6f47f8b9a32258c36c3/introduction-2012-06-25chapter-introduction-discrete-structures-samujjwal.jpg)