Embed Size (px)

Citation preview

The financial crises that erupted in east Asia in thesecond half of 1997 are the latest in a series of

such episodes that have been experienced byeconomies in various regions of the world in recentyears. In the 1990s, currency crises have occurred inEurope (the 1992–93 crises in the European MonetarySystem’s exchange rate mechanism, ERM), LatinAmerica (the 1994–95 “tequila crisis”), as well as ineast Asia (the 1997–98 crises in Indonesia, Korea,Malaysia, the Philippines, and Thailand). These criseshave been costly in varying degrees—and particularlyso where banking sector problems have been in-volved—both in lost output and in the fiscal and quasi-fiscal outlays to shore up fragile financial sectors.Also, they have involved significant internationalspillovers and in a number of cases have required in-ternational financial assistance to limit their severityand costs and to contain their contagious spread andspillovers to other countries.

Financial crises are not unique to current financialsystems, of course; history is replete with bankingand exchange rate crises.77 In this century, for in-stance, there were the numerous financial crises ofthe interwar period; the sterling and French franccrises of the 1960s; the breakdown of the BrettonWoods system in the early 1970s; and the debt crisisof the 1980s. Earlier periods, too, were peppered withfinancial crises, especially banking crises—two no-table examples were the Barings Crisis of 1890,which bears striking parallels to the Mexican crisis of1994–95,78 and the U. S. exchange rate crisis of1894–96, which has been seen as a speculative attackon the United States’ adherence to the gold standardand as an early example of the effectiveness of offi-cial borrowing of international reserves to stem a cur-

rency crisis.79 Indeed, it was largely in response tovarious crises that modern institutions and practicessuch as the lender-of-last-resort function of centralbanks, deposit insurance, prudential and regulatorystandards, and international financial arrangements—especially the IMF itself—were established andevolved.

Not only are financial crises not a recent phenome-non, but many of the same forces have often been atwork in different crises. Financial innovations and theincreased integration of global financial markets in thepast two decades or so, however, do appear to have in-troduced some new elements and concerns, so that de-spite some similarities, crises in recent years have dif-fered from those in the more distant past in importantrespects. In particular, the spillover effects and thecontagious spread of crises seem to have become bothmore pronounced and far reaching.

This chapter analyzes financial crises in thepost–Bretton Woods period, with a view to drawinglessons about their causes, their macroeconomic char-acteristics, and early warning signals of vulnerabilityto them. The analysis considers the experience of bothdeveloping and industrial countries; for the developingcountries, the focus is on emerging market econ-omies—that is, on economies that have been signifi-cant recipients of private capital flows and thus are po-tentially susceptible to shifts in market sentiment.

Types of Crises

A number of broad types of economic or financialcrisis can be distinguished. A currency crisis may besaid to occur when a speculative attack on the ex-change value of a currency results in a devaluation (orsharp depreciation) of the currency, or forces the au-thorities to defend the currency by expending largevolumes of international reserves or by sharply raisinginterest rates. A banking crisis refers to a situation inwhich actual or potential bank runs or failures inducebanks to suspend the internal convertibility of their li-abilities or which compels the government to inter-

74

IVFinancial Crises: Characteristics and Indicators of Vulnerability

77See, for instance, Michael D. Bordo and Anna J. Schwartz,“Why Clashes Between Internal and External Stability Goals End inCurrency Crises, 1797–1994,” Open Economies Review, Vol. 7(Suppl. 1, 1996), pp. 537–68; and Charles P. Kindleberger, Manias,Panics, and Crashes: A History of Financial Crises (New York:Basic Books, 1978); and Annex VI, International Capital Markets:Developments, Prospects, and Key Policy Issues (Washington: IMF,November 1997), pp. 234–51.

78See Barry Eichengreen, “The Baring Crisis in a MexicanMirror,” CIDER Working Paper C97–084 (Berkeley, California:Center for International and Development Economics Research,University of California, February 1997).

79See Vittorio Grilli, “Managing Exchange Rate Crises: Evidencefrom the 1890s,” Journal of International Money and Finance,Vol. 9 (September 1990), pp. 258–75.

©1998 International Monetary Fund

vene to prevent this by extending assistance on a largescale.80 A banking crisis may be so extensive as to as-sume systemic proportions. Systemic financial crisesare potentially severe disruptions of financial marketsthat, by impairing markets’ ability to function effec-tively, can have large adverse effects on the real econ-omy. A systemic financial crisis may involve a cur-rency crisis, but a currency crisis does not necessarilyinvolve serious disruption of the domestic paymentssystem and thus may not amount to a systemic finan-cial crisis. Finally, a foreign debt crisis is a situation inwhich a country cannot service its foreign debt,whether sovereign or private.

Crises of all types have often had common origins:the buildup of unsustainable economic imbalances andmisalignments in asset prices or exchange rates, oftenin a context of financial sector distortions and struc-tural rigidities. A crisis may be triggered by a suddenloss of confidence in the currency or banking system,prompted by such developments as a sudden correc-tion in asset prices, or by disruption to credit or exter-nal financing flows that expose underlying economicand financial weaknesses. Crises may involve sharpdeclines in asset prices, and failures of financial insti-tutions and nonfinancial corporations.81 Of course, notall corrections of imbalances involve a crisis. Whetherthey do or not depends, apart from the magnitude ofthe imbalances themselves, on the credibility of poli-cies to correct the imbalances and achieve a “soft land-ing,” and on the robustness of the country’s financialsystem. These factors together determine the econ-omy’s vulnerability to crises. Crises may then be con-sidered to be the consequence of financial or economicdisturbances when economies suffer from a high de-gree of vulnerability.

At times elements of currency, banking, and debtcrises may be present simultaneously, as in the recenteast Asian crisis and in the 1994–95 Mexican crisis.The 1992–93 ERM crises were essentially currencycrises, although the Nordic countries that experiencedcurrency crises also had domestic banking crises ataround the same time. Furthermore, what may start outas one type of crisis may develop into others as well.Banking crises have often preceded currency crises,especially in developing countries—for instance, inTurkey and Venezuela in the mid-1990s. Bankingproblems have preceded debt crises, too, as in Argen-tina and Chile in 1981–82. The converse has also oc-curred, as in Colombia, Mexico, Peru, and Uruguay,where the withdrawal of external financing in 1982precipitated banking crises. More recently, what beganas currency crises in some east Asian countries metas-tasized into banking and debt crises, as illustratedmost clearly by Indonesia. That one type of crisis pre-cedes another does not necessarily imply causality,however. Banking sector difficulties may not alwaysbe apparent, especially in poorly supervised and inad-equately regulated systems, or in circumstances wherelending booms and asset price inflation may maskbanking problems until a correction in asset prices ex-poses the fragility of the financial system. The same istrue for problems linked to corporate sector indebted-ness. In these situations, the fragility of the bankingsystem or the corporate sector may be fully revealedonly after a run on the currency has undermined con-fidence more generally and precipitated speculativeshifts that expose and exacerbate banking and debtproblems.82 This has clearly been a feature of the re-cent east Asian crisis.

Identifying Crises

What has been the incidence of currency and bank-ing crises in emerging market economies and in indus-trial countries in the past two decades or so? Has therebeen any tendency for one type of crisis to becomemore or less prevalent? And what have been the costsof financial crises? To answer these questions, opera-tional criteria to identify currency and banking crisesare needed. The measurement and dating of both ex-change market and banking crises pose various diffi-culties. In this chapter, following procedures adoptedin the economic literature, episodes of significant for-eign exchange market pressures are identified anddated using statistical criteria. This approach, whilecapturing the more serious currency crises, also picksup episodes where there were significant but less than

Identifying Crises

75

80This definition follows Michael D. Bordo, “Financial Crises,Banking Crises, Stock Market Crashes, and the Money Supply:Some International Evidence, 1870–1933,” in Forrest Capie andGeoffrey Wood, eds., Financial Crises and the World BankingSystem (New York: St. Martin’s, 1985); Gerard Caprio, Jr., andDaniela Klingebiel, “Banking Insolvency: Bad Luck, Bad Policy, orBad Banking,” in World Bank, Annual World Bank Conference onDevelopment Economics 1996 (Washington, 1997); and BarryEichengreen and Andrew K. Rose, “Staying Afloat When the WindShifts: External Factors and Emerging-Market Banking Crises,”NBER Working Paper 6370 (Cambridge, Massachusetts: NationalBureau of Economic Research, January 1998).

81Not all financial disturbances that produce falling asset pricesand wealth losses to particular economic sectors or agents—such asthose associated with a collapse of land prices following a boom, orthe bursting of bubbles in various asset markets—are to be viewedas true financial crises. Financial disturbances that do not impingeon the payments mechanism and do not have potentially damagingconsequences for economic activity have been characterized as“pseudo-financial crises”—see Anna J. Schwartz, “Real andPseudo-Financial Crises,” in Capie and Wood, Financial Crises andthe World Banking System; and Frederic S. Mishkin, “PreventingFinancial Crises: An International Perspective,” NBER WorkingPaper 4636 (Cambridge, Massachusetts: National Bureau ofEconomic Research, June 1994).

82For more in-depth discussions of related banking sector issues,see Carl-Johan Lindgren, Gillian Garcia, and Matthew I. Saal, BankSoundness and Macroeconomic Policy (Washington: IMF, 1996).

IV FINANCIAL CRISES: CHARACTERISTICS AND INDICATORS OF VULNERABILITY

critical foreign exchange market pressures, and itmakes the results sensitive to the statistical criteriaused. This must be borne in mind in interpreting the re-sults and drawing inferences of general applicability.

A currency crisis could be identified simply as asubstantial nominal currency devaluation.83 This crite-rion, however, would exclude instances where a cur-rency came under severe pressure but the authoritiessuccessfully defended it by intervening heavily in theforeign exchange market, or by raising interest ratessharply, or by other means. An alternative approach isto construct an index of speculative pressure that takesinto account not only exchange rate changes, but alsomovements in international reserves or interest ratesthat absorb pressure and thus moderate the exchangerate changes.84 Crises identified by using such anindex would therefore include not only those occa-sions in which the currency depreciated significantly,but also occasions where actions by the authoritiesaverted a large devaluation or the abandonment of anexchange rate peg.

Banking crises are more difficult to identify empiri-cally, partly because of the nature of the problem andpartly because of the lack of relevant data. Althoughdata on bank deposits are readily available for mostcountries, and thus could be used to identify crises as-sociated with runs on banks, most major banking prob-lems in recent years have not originated on the liabili-ties side of banks’ balance sheets. Thus, among theindustrial countries, neither the banking crises inFinland, Norway, and Sweden in the late 1980s andearly 1990s, nor the earlier banking problems in sev-eral other countries, such as in Spain in the early 1980s,nor the more recent banking problems in Japan wereassociated with runs on deposits. Among the develop-ing countries, large withdrawals of deposits and runson banks have been more frequent—for instance, thebanking crises in the 1980s and 1990s in Argentina, thePhilippines, Thailand, Turkey, Uruguay, and Venezuelawere associated with bank runs. A failure to roll overinterbank deposits, as in Korea recently, can have re-sults similar to those of a run on banks. Instances of

large deposit withdrawals, however, as in the recent fi-nancial crisis in Indonesia, have tended to follow thedisclosure of difficulties on the assets side or wide-spread uncertainty about whether the currency wouldmaintain its value. In general, runs on banks are the re-sult rather than the cause of banking problems.

Banking crises generally stem from the assets sideof banks’ balance sheets—from a protracted deterio-ration in asset quality. This suggests that variablessuch as the share of nonperforming loans in banks’portfolios, large fluctuations in real estate and stockprices, and indicators of business failures could beused to identify crisis episodes. The difficulty is thatdata for such variables are not readily available formany developing countries or are incomplete (as withdata on nonperforming loans in many countries). Incases where central banks have detailed informationon nonperforming loans, it is usually laxity in theanalysis of, and in follow-up action in response to, thedata that allows the situation to deteriorate to thepoint of crisis.

Given these limitations, banking crises have usuallybeen dated by researchers on the basis of a combina-tion of events—such as the forced closure, merger, orgovernment takeover of financial institutions, runs onbanks, or the extension of government assistance toone or more financial institutions—or in-depth assess-ments of financial conditions, as in many case studies.

For the analysis that follows, currency and bankingcrises were identified for a group of over 50 countriesfor the period 1975–97.85 An index of foreign exchangemarket pressure was constructed as a weighted averageof (detrended) monthly exchange rate changes andreserve changes. Occasions when values of the indexexceeded a specified threshold were classified ascrises.86 Banking crises were compiled from previous

76

83Jeffrey A. Frankel and Andrew K. Rose, “Currency Crashes inEmerging Markets: Empirical Indicators,” NBER Working Paper5437 (Cambridge, Massachusetts: National Bureau of EconomicResearch, January 1996), define a “currency crash” as a nominaldepreciation of the currency of at least 25 percent in a year, alongwith a 10 percent increase from the previous year in the rate of de-preciation. The latter condition is included so as to omit from cur-rency crashes the large trend depreciations of high-inflationcountries.

84See, for example, Barry Eichengreen, Andrew K. Rose, andCharles Wyplosz, “Contagious Currency Crises: First Tests,”Scandinavian Journal of Economics, Vol. 98 (No. 4, 1996), pp. 463–84, in which a weighted average of changes in the exchangerate, foreign reserves, and interest rates relative to Germany (the ref-erence country) is used to examine currency crises in industrialcountries. Crises are identified as extreme values of the speculativepressure index.

85The group included 22 industrial countries and 31 developingcountries. The developing country group consisted mainly of coun-tries commonly referred to as emerging market countries. Germanyand the United States were excluded from the currency crisis sam-ple (but included in the banking crisis sample) because they werethe reference countries for the European and the non-Europeancountries, respectively. Hong Kong SAR also was excluded in thecurrency crisis sample because of the lack of monthly data.Currency crises were analyzed using monthly data, while bankingcrises were analyzed using annual data.

86The weights were chosen so as to equalize the variance of thetwo components, thus avoiding the possibility of one of the twocomponents dominating the index. Interest rates were not includedin the index, owing to the paucity of comparable, market-deter-mined interest rate data for many developing countries over thesample period. The threshold was set to 1.5 times the pooled stan-dard deviation of the calculated index plus the pooled mean of theindex. Weights and thresholds were calculated separately for peri-ods with low and high inflation, where the latter were defined as12-month inflation rates greater than 80 percent. For any one coun-try, crises identified within 18 months of a previous crisis wereconsidered as part of the earlier crisis and excluded. For informa-tion about a similar index, see Eichengreen, Rose, and Wyplosz,“Contagious Currency Crises.”

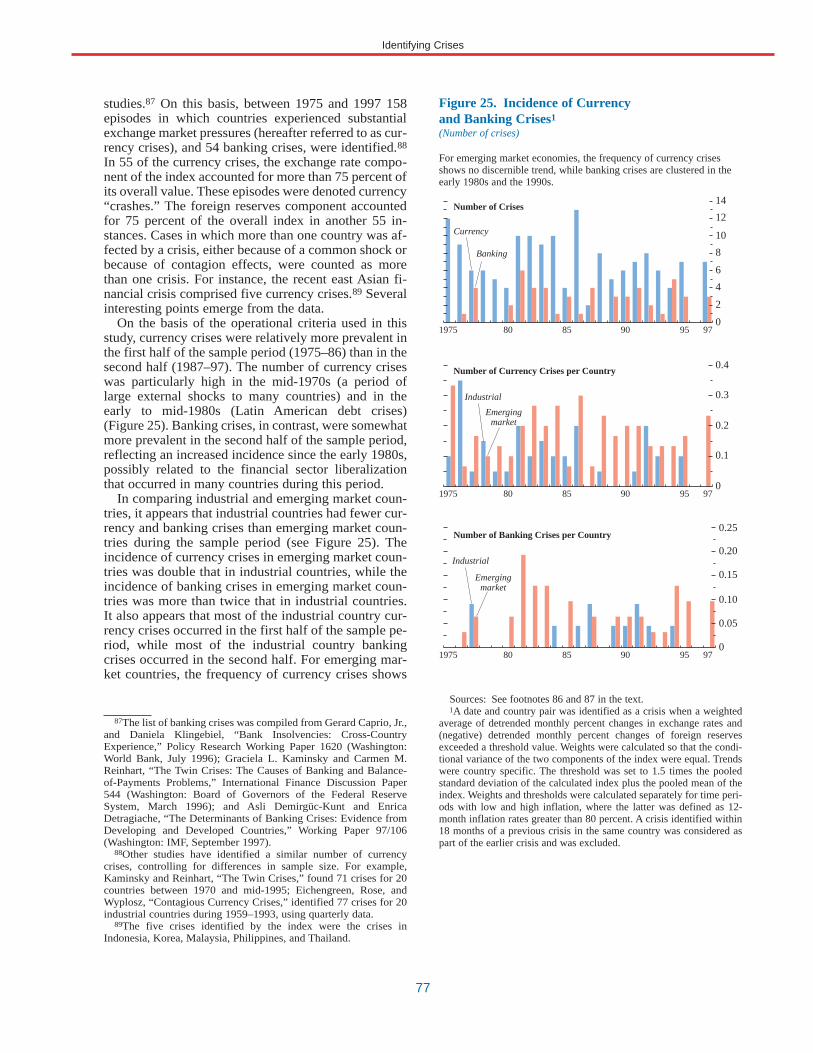

studies.87 On this basis, between 1975 and 1997 158episodes in which countries experienced substantialexchange market pressures (hereafter referred to as cur-rency crises), and 54 banking crises, were identified.88

In 55 of the currency crises, the exchange rate compo-nent of the index accounted for more than 75 percent ofits overall value. These episodes were denoted currency“crashes.” The foreign reserves component accountedfor 75 percent of the overall index in another 55 in-stances. Cases in which more than one country was af-fected by a crisis, either because of a common shock orbecause of contagion effects, were counted as morethan one crisis. For instance, the recent east Asian fi-nancial crisis comprised five currency crises.89 Severalinteresting points emerge from the data.

On the basis of the operational criteria used in thisstudy, currency crises were relatively more prevalent inthe first half of the sample period (1975–86) than in thesecond half (1987–97). The number of currency criseswas particularly high in the mid-1970s (a period oflarge external shocks to many countries) and in theearly to mid-1980s (Latin American debt crises)(Figure 25). Banking crises, in contrast, were somewhatmore prevalent in the second half of the sample period,reflecting an increased incidence since the early 1980s,possibly related to the financial sector liberalizationthat occurred in many countries during this period.

In comparing industrial and emerging market coun-tries, it appears that industrial countries had fewer cur-rency and banking crises than emerging market coun-tries during the sample period (see Figure 25). Theincidence of currency crises in emerging market coun-tries was double that in industrial countries, while theincidence of banking crises in emerging market coun-tries was more than twice that in industrial countries.It also appears that most of the industrial country cur-rency crises occurred in the first half of the sample pe-riod, while most of the industrial country bankingcrises occurred in the second half. For emerging mar-ket countries, the frequency of currency crises shows

Identifying Crises

77

87The list of banking crises was compiled from Gerard Caprio, Jr.,and Daniela Klingebiel, “Bank Insolvencies: Cross-CountryExperience,” Policy Research Working Paper 1620 (Washington:World Bank, July 1996); Graciela L. Kaminsky and Carmen M.Reinhart, “The Twin Crises: The Causes of Banking and Balance-of-Payments Problems,” International Finance Discussion Paper544 (Washington: Board of Governors of the Federal ReserveSystem, March 1996); and Asli Demirgüc-Kunt and EnricaDetragiache, “The Determinants of Banking Crises: Evidence fromDeveloping and Developed Countries,” Working Paper 97/106(Washington: IMF, September 1997).

88Other studies have identified a similar number of currencycrises, controlling for differences in sample size. For example,Kaminsky and Reinhart, “The Twin Crises,” found 71 crises for 20countries between 1970 and mid-1995; Eichengreen, Rose, andWyplosz, “Contagious Currency Crises,” identified 77 crises for 20industrial countries during 1959–1993, using quarterly data.

89The five crises identified by the index were the crises inIndonesia, Korea, Malaysia, Philippines, and Thailand.

Figure 25. Incidence of Currencyand Banking Crises1

(Number of crises)

Sources: See footnotes 86 and 87 in the text.1A date and country pair was identified as a crisis when a weighted

average of detrended monthly percent changes in exchange rates and(negative) detrended monthly percent changes of foreign reservesexceeded a threshold value. Weights were calculated so that the condi-tional variance of the two components of the index were equal. Trendswere country specific. The threshold was set to 1.5 times the pooledstandard deviation of the calculated index plus the pooled mean of theindex. Weights and thresholds were calculated separately for time peri-ods with low and high inflation, where the latter was defined as 12-month inflation rates greater than 80 percent. A crisis identified within18 months of a previous crisis in the same country was considered aspart of the earlier crisis and was excluded.

Number of Crises

Number of Currency Crises per Country

Number of Banking Crises per Country

1975 80 85 90 95 97

1975 80 85 90 95 97

1975 80 85 90 95 97

Currency

Banking

14

12

10

8

6

4

2

0

0.4

0.25

0.20

0.15

0.10

0.05

0

0.3

0.2

0.1

0

Emergingmarket

Industrial

Emergingmarket

Industrial

For emerging market economies, the frequency of currency crisesshows no discernible trend, while banking crises are clustered in theearly 1980s and the 1990s.

IV FINANCIAL CRISES: CHARACTERISTICS AND INDICATORS OF VULNERABILITY

no marked trend, while banking crises are clustered inthe early 1980s and the 1990s.

Given that the two types of crises may have com-mon origins, or that one type of crisis may induce theother, it is not surprising that countries appear to havebanking and currency crises at around the same time.In these instances, banking crises preceded currencycrises more often than the other way around. With thetiming of crises identified on an annual basis, bankingcrises led currency crises by one year on 13 occasions,and by two years on 10 other occasions. The criseswere contemporaneous in 12 instances.90 Currencycrises preceded banking crises by one year only seventimes and by two years another four times. This evi-dence, while suggestive, should be interpreted withcaution in view of the difficulties in dating the begin-ning of banking crises.91

Financial crises can be very costly, both in the fiscaland quasi-fiscal costs of restructuring the financialsector and, more broadly, in the effect on economic ac-tivity of the inability of financial markets to functioneffectively (Table 14).92 Resolution costs for bankingcrises have in some cases reached over 40 percent ofGDP (for example, in Chile and Argentina in the early1980s), while nonperforming loans have exceeded 30percent of total loans (for example, in Malaysia during1988 and for state banks in Sri Lanka during the early1990s).93 In general, the resolution costs of bankingcrises have been higher in emerging market countriesthan in industrial countries: except for Spain, resolu-tion costs in industrial countries have been held tounder 10 percent of GDP, whereas in several emergingmarket countries, particularly in Latin America, reso-lution costs have been much larger (Box 6).94

In addition to their fiscal and quasi-fiscal costs,banking and currency crises may also lead to misallo-cation and underutilization of resources, and thus tolosses of real output. In some instances, however,crises may not lead to output losses, such as when acrisis simply brings about a needed correction of amisaligned exchange rate. To provide a rough assess-ment of the costs in terms of lost output, GDP growthafter a crisis was compared with trend GDP growth.The cost in lost output was then estimated by addingup the differences between trend growth and actualgrowth in the years following the crisis until the timewhen annual output growth returned to its trend. Forapproximately 40 percent of the currency crises and 20percent of the banking crises, there were no significant

78

Table 14. Selected Crises: Costs of RestructuringFinancial Sectors and Nonperforming Loans

Fiscal and NonperformingCountry Years Quasi-Fiscal Costs1 Loans2

Argentina 1980–82 13–55 91985 . . . 30

Brazil 1994–96 4–10 9

Chile 1981–85 19–41 16

Colombia 1982–87 5–6 25

Finland 1991–93 8–10 9

Indonesia 1994 2 . . .

Japan3 1990s 3 10

Malaysia 1985–88 5 33

Mexico 1994–95 12–15 11

Norway 1988–92 4 9

Philippines 1981–87 3–4 . . .

Spain 1977–85 15–17 . . .

Sri Lanka 1989–93 9 35

Sweden 1991–93 4–5 11

Thailand 1983–87 1 15

Turkey 1982–85 3 . . .

United States 1984–91 5–7 4

Uruguay 1981–84 31 . . .

Venezuela 1980–83 . . . 151994–95 17 . . .

Sources: See footnote 92 in the text.1Estimated in percent of annual GDP during the restructuring pe-

riod. Where a range is shown, the lower estimate includes only costsof funds, credit, and bonds injected directly into the banking system,while the higher estimate includes other fiscal costs, such as ex-change rate subsidies.

2Estimated at peak of nonperforming loans in percent of totalloans. Measure is dependent on country definition of nonperformingloans.

3Cost estimates through 1995 only. Official estimates of the costs,which take into account the costs of settling housing loan corpora-tions (“Jusen”), and of nonperforming loans are 0.14 percent and 3percent, respectively.

90Currency and banking crises seem to have become more con-temporaneous since the late 1980s: 10 of the 12 instances in whichbanking and currency crises occurred in the same year have takenplace since 1989.

91It should be noted that others have found evidence that bankingcrises are statistically significant in helping to predict currencycrises, but not conversely—see Kaminsky and Reinhart, “The TwinCrises.”

92The costs of banking crises were compiled from Caprio andKlingebiel, “Bank Insolvencies: Cross-Country Experience”; ClaudiaDziobek and Ceyla Pazarbasioglu, “Lessons from Systemic BankRestructuring: A Survey of 24 Countries,” Working Paper 97/161(Washington: IMF, December 1997); Liliana Rojas-Suarez andSteven R. Weisbrod, “Banking Crises in Latin America: Experiencesand Issues,” in Banking Crises in Latin America, Ricardo Hausmannand Liliana Rojas-Suarez, eds., (Washington: Inter-AmericanDevelopment Bank, 1996); and Bank for International Settlements,66th Annual Report (Basle, Switzerland: BIS, June 1996).

93The data on nonperforming loans should be regarded as indica-tive only of broad orders of magnitude. Comparisons across coun-tries are difficult because of differences in the classification of loansas nonperforming. Often nonperforming loans are underreported,particularly at the beginning of a crisis.

94However, since any resolution of a banking crisis generally in-volves some elements of net resource transfers among differentgroups in an economy, the fiscal costs associated with restructuringoperations are likely to overstate the true welfare cost.

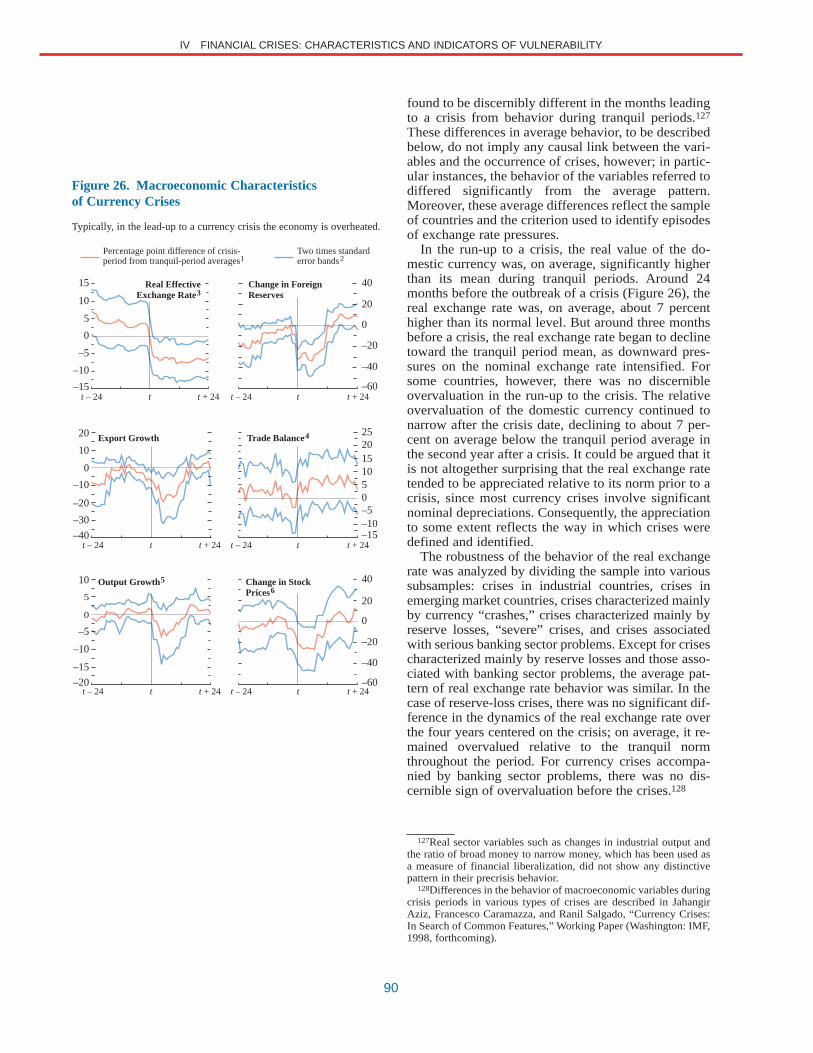

output losses estimated using this technique.95 For thecurrency crises, on average, output growth returned totrend in a little over one and one-half years, and thecumulative loss in output growth per crisis was 4!/4percentage points (relative to trend) (Table 15).96 For“severe” currency crises, the recovery time and cumu-lative loss of output growth per currency crisis in-creases to two and one-quarter years and 8!/4 percent-age points, respectively.97

Banking crises, not surprisingly, were more pro-longed and more costly than currency crises: on aver-age it took three years for output growth to return totrend, and the average cumulative loss in outputgrowth was 11!/2 percentage points.98 Although this

may seem intuitively convincing, some caution is inorder: the criteria used to identify banking crises maytend to select occasions when financial sector prob-lems were severe, whereas the statistical criteria usedto identify currency crises are independent of suchjudgments. When banking crises occurred within ayear of currency crises, the losses were substantiallylarger, amounting to 14!/2 percent, on average. It is in-teresting to note that for both currency and bankingcrises the average recovery time was shorter in emerg-ing market countries than in industrial countries, butthe cumulative output loss was on average larger. Thedifferences in recovery time and cumulative outputlosses may result, in part, from the higher mean andvariance of output growth in emerging market coun-tries compared with industrial countries.99 These re-sults are for the group of countries and time periodused in the analysis in this chapter; results will obvi-ously differ from case to case.

Origins of Currency and Banking Crises

The factors that underlie the emergence of imbal-ances and that render an economy vulnerable to finan-

Origins of Currency and Banking Crises

79

Table 15. Costs of Crises in Lost Output Relative to Trend

Cumulative LossAverage Cumulative Loss Crises with of Output per Crisis

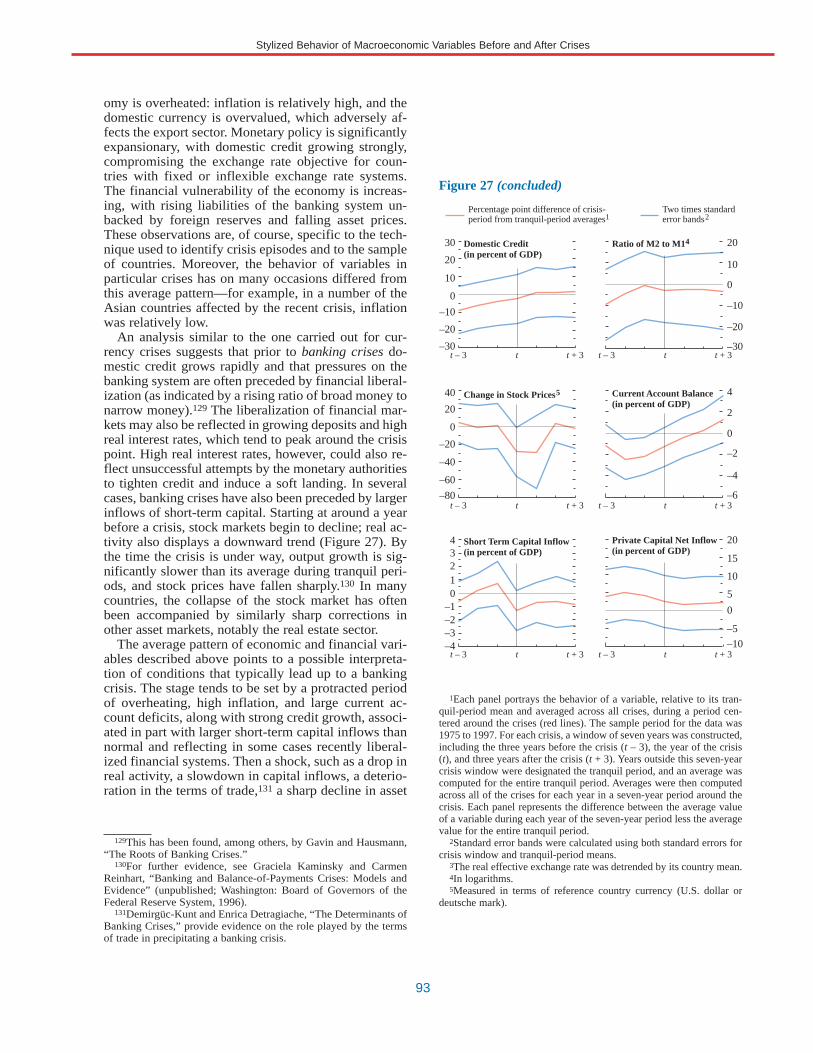

Number of Recovery Time1 of Output per Crisis2 Output Losses3 with Output Loss4

Crises (in years) (in percentage points) (in percent) (in percentage points)

Currency crises 158 1.6 4.3 61 7.1Industrial 42 1.9 3.1 55 5.6Emerging market 116 1.5 4.8 64 7.6

Currency crashes 5 55 2.0 7.1 71 10.1Industrial 13 2.1 5.0 62 8.0Emerging market 42 1.9 7.9 74 10.7

Banking crises 54 3.1 11.6 82 14.2Industrial 12 4.1 10.2 67 15.2Emerging market 42 2.8 12.1 86 14.0

Currency and banking crises 6 32 3.2 14.4 78 18.5Industrial 6 5.8 17.6 100 17.6Emerging market 26 2.6 13.6 73 18.8

1Average amount of time until GDP growth returned to trend. Because GDP growth data are available for all countries only on an annualbasis, by construction the minimum recovery time was one year.

2Calculated by summing the differences between trend growth and output growth after the crisis began until the time when annual outputgrowth returned to its trend and by averaging over all crises.

3Percent of crises in which output was lower than trend after the crisis began.4Calculated by summing the differences between trend growth and output growth after the crisis began until the time when annual output

growth returned to its trend and by averaging over all crises that had output losses.5Currency “crashes” are identified by crises where the currency component of the exchange market pressure index accounts for 75 percent

or more of the index when the index signals a crisis.6Identified when a banking crisis occurred within a year of a currency crisis.

95This may be because in some cases it takes several years for theconsequences of financial sector weaknesses to materialize.

96This cost estimate may be biased downward because instanceswhere output growth did not return to trend over the sample periodwere excluded from the calculation.

97“Severe” currency crises are identified by increasing the thresh-old for the exchange market pressure index to three times the pooledstandard deviation plus the pooled mean.

98This should be viewed only as indicative of the macroeconomiccosts associated with banking crises and not as suggesting that thebanking crises caused these output losses. Recessions may give riseto banking crises, which then amplify the recessions. Furthermorethe magnitude of output losses for different countries may dependon their specific cyclical positions before the crisis. It is, in princi-ple, possible to derive output losses correcting for each country’scyclical position, but, since the cyclical positions of the 50 countriesin the sample have not been closely synchronized, the effect of thecorrection on average losses will be limited.

99The mean and standard deviation of output growth were 4.5 per-cent and 3.7 percent, respectively, for emerging market countries;they were 2.7 percent and 2.3 percent, respectively, for industrialcountries.

IV FINANCIAL CRISES: CHARACTERISTICS AND INDICATORS OF VULNERABILITY

cial disturbances may be grouped under the follow-ing (not mutually exclusive) headings: unsustainablemacroeconomic policies, weaknesses in financial struc-ture, global financial conditions, exchange rate mis-alignments, and political instability. In addition, thereis a natural tendency for economic activity to fluctuate,giving rise to shifts in market sentiment that can con-

tribute to stresses in the financial system. These factorsmake up the conditions under which crises occur andshould be distinguished from the proximate causes (ortriggers) of crises, which are usually events or newsthat lead economic agents to reassess their positions.

Macroeconomic instability has been an importantunderlying factor in many financial crises. In many

80

The resolution of widespread banking problems willusually require the adoption of a carefully designed fi-nancial sector restructuring strategy to restore confidencein the banking system and set it on a path that will returnit to soundness and profitability. Typically, the strategywill entail the recapitalization and restructuring of a num-ber of banks and the establishment for three key groups—bank owners and managers, creditors (including deposi-tors), and bank supervisors—of the incentives and abilityto monitor bank operations properly and ensure prudentbank management. Developing appropriate incentives forthe three groups is especially critical to prevent recur-rences of banking crises.1

When banking difficulties first emerge, bank ownersand managers, and public authorities, are often temptedto conceal their extent. The motivation of bank ownersand managers will tend to be to retain their stake in, andcontrol of, the bank. The primary concern of the authori-ties will be to maintain public confidence in the bankingsystem, particularly given its vital economic role in fi-nancial intermediation and operation of the paymentssystem. Furthermore, it is not always obvious at the out-set whether banking difficulties are permanent or transi-tory. Large adverse macroeconomic shocks (such as achange in the terms of trade or a rise in interest rates) maytemporarily affect even well-run banks. The effects of aloss of confidence in the banking system in the face ofsuch shocks are difficult to predict and may be enormousand irreversible.

As a result, bank owners, bank managers, and publicauthorities may attempt to defer disclosing losses in thebanking system. Banks, in order to conceal nonperform-ing loans and maintain the illusion of solvency, may ex-tend new credits to bankrupt customers, sometimes evenwith the encouragement of the authorities, so that thesecustomers can continue to service their outstanding debts.A delay in assessing losses, however, can ultimately leadto even larger losses as more funds are lent to businessesthat may never return to profitability. In addition, bank

managers may be tempted to “gamble” by paying above-market interest rates to attract deposits and then on-lend-ing these funds for high-risk, high-return projects, sincethey do not expect to bear the full consequences of theirbehavior (for example, because of limited liability, ex-plicit or implicit deposit insurance, or expected govern-ment bailouts).

Studies of banking crises have shown, however, thatcountries that are quickest to diagnose the underlyingproblems, assess losses, and take measures to ensuremacroeconomic stability and restructure their bankingsectors are generally the most successful in recoveringfrom the crises.2 These measures involve correction ofthe policy weaknesses that may have contributed to thecrisis. Several countries, such as Argentina, Chile, andthe Philippines in the early 1980s, attempted to hidebanking system losses by providing excessive financialsupport, often through the central bank. This policy even-tually put pressure on the central bank to adopt an ac-commodative monetary policy stance and led to mone-tary expansion and high inflation. In other instances,excessively tight policies (resulting, for example, in a“credit crunch”) or inappropriate exchange rate regimeshave exacerbated crises.

The measures needed to resolve problems in the bank-ing system, however, are typically structural or micro-economic. The most urgent requirements are often to re-structure bank balance sheets to address problem loans,and to restore financial viability and confidence in thebanks. Countries have taken alternative approaches tothis process, although in most cases some temporary gov-ernment financial support of distressed banks has beenunavoidable, since the magnitude of the losses could notbe covered by the private sector in a timely manner. Inseveral countries, the central bank has taken the lead byassuming extensive responsibilities, including financialsupport and bank and asset (nonperforming loan) man-agement. In other countries, the central bank has playeda much more limited role, simply providing short-term

Box 6. Resolving Banking Sector Problems

1The issues involved in restructuring strategies are complexand cannot be examined fully in a few pages. This box toucheson only some of the issues. For a more extensive discussion, seeCarl-Johan Lindgren, Gillian Garcia, and Matthew I. Saal, BankSoundness and Macroeconomic Policy (Washington: IMF,1996); and Charles Enoch and John H. Green, eds., BankingSoundness and Monetary Policy: Issues and Experiences in theGlobal Economy (Washington: IMF, 1997).

2For example, Claudia Dziobek and Ceyla Pazarbasioglu,“Lessons from Systemic Bank Restructuring: A Survey of 24Countries,” Working Paper 97/161 (Washington: IMF, Decem-ber 1997), found that countries that made substantial progress inrestructuring their banking sectors began to take measures, onaverage, in less than 10 months after banking problems sur-faced, while countries that made slow progress waited over 40months.

cases, overly expansionary monetary and fiscal poli-cies have spurred lending booms, excessive debt accu-mulation, and overinvestment in real assets, whichhave driven up equity and real estate prices to un-sustainable levels. The eventual tightening of policiesto contain inflation and promote the adjustment ofexternal positions, and the inevitable correction of

asset prices, has then led to a slowdown in economicactivity, debt-servicing difficulties, declining collat-eral values and net worth, and rising levels of nonper-forming loans that threaten banks’ solvency. Macro-economic factors, especially lending booms, havebeen found to play an important role in creating finan-cial sector vulnerability in many Latin American coun-

Origins of Currency and Banking Crises

81

liquidity. Sweden, for instance, placed strict limits oncentral bank financing when systemic banking problemsarose.3 Experience suggests that, generally, the smallerthe role of the central bank, the more progress the coun-try makes in bank restructuring, mainly because directcentral bank involvement can create conflicts with mon-etary policy objectives.4

Countries in which the central bank did not take a directrole in recapitalizing banks often used an independentagency to lead the restructuring efforts. These agenciesimplemented firm exit policies, closed or merged insol-vent banks, facilitated loss-sharing between the state, thebanks, and the public, and helped solvent banks to sellbonds or equity in exchange for nonperforming loans.These agencies can be established to manage a particularcrisis (for example, the Resolution Trust Corporation inthe United States), or to manage bank restructuring caseson an ongoing basis (a role the Federal Deposit InsuranceCorporation plays in the United States).

Failing to actively manage the nonperforming assets ofall banks, as well as the remaining assets of failed banks,increases the total cost of restructuring. It also creates aninequitable distribution of losses by rewarding defaultersand by impairing incentives for debt repayment in the fu-ture. Liquidation may be necessary in some cases, butloan or debt restructuring may be the least costly alter-native under certain conditions. Mass liquidation, inparticular, could result in asset price deflation, exacerbat-ing a country’s macroeconomic difficulties. Loan workoutunits, decentralized or centralized, which are activelymanaged to maximize returns and maintain asset values,can contribute to the recovery of bank restructuring costsand send the appropriate signals to delinquent borrowers.5

In instances where difficulties were concentrated instate-owned banks, the problem banks were sometimes

privatized. The design of privatization programs is veryimportant in these situations. Poorly designed programscan contain the seeds of subsequent banking crises. Insome such cases, preferences were given to certain bid-ders, banks assets were overpriced, and weak legislationallowed nonbank conglomerates to acquire large portionsof the financial system.

Once recapitalization has commenced, the operationalperformance of banks must be improved by creating theappropriate incentives for bank owners, bank managers,supervisors, and the market to monitor banks and ensureprudent corporate governance and bank profitability onan ongoing basis. In particular, shortcomings in thesupervisory, regulatory, legal, and accounting frame-works and in excessive and distorted taxation schemesmust be addressed. In Chile, for example, where restruc-turing made significant progress after the crises in the1980s, managers were dismissed, shareholders borelosses, and fraud was prosecuted where it existed. More-over, accounting rules and supervision were broughtup to international standards, and banks were barredfrom lending to borrowers in default and are now re-quired to be rated by private credit agencies at leasttwice a year.6 In Malaysia, a credit bureau was estab-lished so that banks can have better access to informa-tion about potential borrowers. New Zealand’s market-oriented approach, which may not be readily applicablein every country, focuses on disclosure and incentives. Inaddition to their income and balance sheet statements,banks are required to disclose other information on aquarterly basis, including asset quality and provisioning,risk management systems, loan concentration, and creditratings. Abbreviated disclosure statements must beposted in all banks, and full disclosure statements mustbe available on demand. Bank managers, moreover,must attest that the statements contain no misleading in-formation and can be subject to criminal penalties andunlimited liability.73Central bank or other government funding may also be un-

avoidable when a systemic crisis leads to the imminent risk ofruns on otherwise solvent banks. In this instance, a temporaryblanket guarantee on bank liabilities may be required to stabi-lize bank funding (particularly, the deposit base).

4See Dziobek and Pazarbasioglu, “Lessons from SystemicBank Restructuring,” for more details. The study also found,however, that in transition countries the central bank may needto take the lead in financial sector restructuring, given thescarcity of banking expertise in the public sector.

5In Sweden, the net fiscal cost of bank restructuring has beendiminishing over time mainly because of the success in loan re-covery by the asset management companies.

6See Box 7 for a discussion of the core principles that are crit-ical for effective banking regulation and supervision.

7For more details, see Gerard Caprio, Jr., and DanielaKlingebiel, “Bank Insolvency: Bad Luck, Bad Policy, or BadBanking?” Annual World Bank Conference on DevelopmentEconomics (Washington: World Bank, 1996) and GerardCaprio, Jr., “Safe and Sound Banking in Developing Countries:We’re Not in Kansas Anymore,” Policy Research WorkingPaper 1739 (Washington: World Bank, March 1997).

IV FINANCIAL CRISES: CHARACTERISTICS AND INDICATORS OF VULNERABILITY

tries100 and in other emerging market economies aswell.101 Macroeconomic instability has been an im-portant underlying factor also in most of the bankingcrises experienced by industrial countries in the post-war period.

In addition to domestic macroeconomic conditions,external conditions have also played a role in financialcrises, especially in emerging market economies.102

Most notable have been sudden, large shifts in theterms of trade and in world interest rates. An unantic-ipated drop in export prices, for instance, can impairthe capacity of domestic firms to service their debtsand can result in a deterioration in the quality ofbanks’ loan portfolios. Movements in interest rates inthe major industrial countries have become increas-ingly important to emerging market economies world-wide, reflecting the increasing integration of worldcapital markets and the globalization of investment.103

Sustained declines in world interest rates have inducedsurges in capital flows to emerging market countries,as international investors have sought higher yieldsand as the creditworthiness of externally indebtedcountries has benefited from lower rates. An abruptrise in industrial country interest rates, however, cancurb the flow of foreign financing to emerging mar-kets, raising the cost to domestic banks (and firms) offunding themselves offshore and increasing adverseselection and moral hazard problems and the fragilityof the financial system.104 Some recent empirical re-

search has found that the incidence of banking crisesin emerging market economies is systemically relatedto changes in global financial conditions.105

The composition of capital inflows has been consid-ered an important factor in a number of currency crisesin emerging market countries. In both the recent crisisin Thailand and in the 1994–95 Mexican crisis, the re-liance on short-term borrowing to finance large cur-rent account deficits was a crucial ingredient precipi-tating the crises.106 Foreign direct investment, incontrast to debt-creating inflows, is often regarded asproviding a safer and more stable way to finance de-velopment because it refers to ownership and controlof plant, equipment, and infrastructure and thereforefunds the growth-creating capacity of an economy,whereas short-term foreign borrowing is more likelyto be used to finance consumption.107 Furthermore, inthe event of a crisis, while investors can divest them-selves of domestic securities and banks can refuse toroll over loans, owners of physical capital cannot findbuyers so easily. In practice, however, questions maybe raised about the reliability of data that distinguishdirect investment from other capital flows, and someresearch has shown that net foreign direct investmentflows are in fact quite volatile.108

Changes in recent decades in the maturity structureand composition of portfolio investment flows, and ininterest rate arrangements, have altered the vulner-ability of countries to shocks. In the high-inflationenvironment of the 1970s, international transactionsshifted toward shorter maturities and variable interestrates. Thus, the debt crisis of 1982 was worsened be-cause much of the external debt of the Latin Americancountries affected by the crisis was tied to short-termrates. More recently, the syndicated bank loans of the1980s were replaced by equity and bond investmentsas the preferred vehicles of international lending. Thishas been viewed by some as having made suddenwithdrawals of capital more difficult, since duringcrises foreign investors may not only incur foreign ex-change losses but also face falling domestic assetprices. The crises in Mexico and east Asia, however,have clearly demonstrated the dangers of high levelsof short-term, foreign-currency-denominated debt,whether sovereign or private.

82

100See Michael Gavin and Ricardo Hausmann, “The Roots ofBanking Crises: The Macroeconomic Context,” in Hausmann andRojas-Suarez, Banking Crises in Latin America; and Jeffrey Sachs,Aaron Tornell, and Andrés Velasco “Financial Crises in EmergingMarkets: The Lessons from 1995,” Brookings Papers on EconomicActivity: 1 (1996), pp. 147–98.

101See Kaminsky and Reinhart, “The Twin Crises.” Eichengreenand Rose, “Staying Afloat When the Wind Shifts,” however, foundthat, while there is some evidence that unstable domestic macroeco-nomic policies play a role in the onset of banking crises in emergingmarket countries, there is little evidence of an independent role fordomestic credit booms.

102See Annex VI, International Capital Markets (November1997).

103The sensitivity of capital flows to developing countries tochanges in world interest rates has been emphasized by GuillermoA. Calvo, Leonardo Leiderman, and Carmen M. Reinhart, “CapitalInflows and Real Exchange Rate Appreciation in Latin America:The Role of External Factors,” Staff Papers, IMF, Vol. 40 (March1993), pp. 108–51, and “Inflows of Capital to Developing Countriesin the 1990s,” Journal of Economic Perspectives, Vol. 10 (Spring1996), pp. 123–39; and Mark P. Taylor and Lucio Sarno, “CapitalFlows to Developing Countries: Long- and Short-Term Determi-nants,” World Bank Economic Review, Vol. 11 (September 1997),pp. 451–70. For a further assessment of the role played by world in-terest rate movements, see International Capital Markets (Nov-ember 1997), pp. 243–45.

104The links between increases in interest rates, adverse selectionand moral hazard problems, and financial crises have been de-scribed in Frederic S. Mishkin, “Understanding Financial Crises: ADeveloping Country Perspective,” NBER Working Paper 5600(Cambridge, Massachusetts: National Bureau of EconomicResearch, June 1996).

105See Eichengreen and Rose, “Staying Afloat When the WindShifts.”

106For additional details see Box 1, “Overconsumption VersusOverinvestment: The Crises in Mexico and Thailand Compared,” inthe December 1997 World Economic Outlook: Interim Assessment,pp. 10–11.

107Even if short-term capital inflows finance investment, a liquid-ity crisis can occur if sovereign and corporate asset-liability man-agement is poor.

108See Michael P. Dooley, Eduardo Fernandez-Arias, andKenneth M. Kletzer, “Recent Private Capital Flows to DevelopingCountries: Is the Debt Crisis History?” NBER Working Paper 4792(Cambridge, Massachusetts: National Bureau of EconomicResearch, July 1994).

Another lesson of recent crises is that currency mis-matches in private sector balance sheets (of either fi-nancial institutions or corporations) may be more of aproblem in countries with inflexible exchange rates,since an exchange rate peg may encourage borrowersto ignore exchange rate risk. In sum, experience sug-gests that countries with high levels of short-termdebt, variable-rate debt, foreign-currency-denomi-nated debt, or foreign debt intermediated through do-mestic financial institutions are likely to be particu-larly vulnerable to internal or external shocks and thussusceptible to financial crises.

Financial sector distortions, in conjunction withmacroeconomic volatility, form another group of fac-tors behind many banking crises. Often these distor-tions arise in times of rapid financial liberalization andinnovation in countries with weak supervisory andregulatory policies or where the government inter-venes directly in the allocation or pricing of credit.Insufficiently stringent regulatory regimes in more lib-eralized financial environments have created moralhazard by encouraging financial institutions with lowcapital ratios to assume imprudent risks. They havealso tended to increase the mistakes financial institu-tions make in evaluating and monitoring risks in themore competitive environments arising from deregu-lation or the privatization of state-owned banks.109 Insome cases, connected lending, politically motivatedlending, and fraud further worsen the quality of assetportfolios. And deficiencies in accounting, disclosure,and legal frameworks add to the problem by allowingfinancial institutions to disguise the extent of their dif-ficulties (Box 7). To all this must be added the fre-quent failure of governments to take prompt correctiveaction when problems emerge, with the consequencethat losses become larger and more difficult tomanage.

Currency Crises and Contagion

Macroeconomic imbalances have often been at theroot of foreign exchange market crises. Experienceclearly demonstrates that unsustainably large currentaccount deficits can bring about sudden reversals incapital inflows and sharp changes in exchange rates(Box 8). Most often, crises have arisen when large ex-ternal imbalances have developed in inflexible ex-

change rate systems that have allowed the currency tobecome significantly overvalued. A remarkable fea-ture of recent currency crises, however, has been theextent to which instability in foreign exchange mar-kets has been transmitted across countries. An attackon one currency has spilled over or spread conta-giously to the currencies of other countries with ap-parently sound fundamentals.

It is useful to distinguish three sets of reasons whycurrency crises tend to be clustered in time.110 One isthat crises may stem from a common cause—for in-stance, major economic shifts in industrial countriesthat trigger crises in emerging markets—in what hasbeen referred to as “monsoonal effects.”111 The sharpincrease in U.S. interest rates in the early 1980s wasan important factor in the Latin American debt crisis.Similarly, the large appreciation of the dollar, espe-cially vis-à-vis the yen, between mid-1995 and 1997contributed to the weakening of the external sector inseveral southeast Asian countries. But while externalevents may contribute to or precipitate a crisis, acountry’s vulnerability to a crisis depends on domes-tic economic conditions and policies, such as over-borrowing for unproductive uses, a fragile financialsector, or an inflexible exchange rate system. A sec-ond reason why crises may be clustered is that a cri-sis in one country may affect the macroeconomic fun-damentals in another country, either because of tradeand capital market linkages (for example, a devalua-tion in one country adversely affects the internationalcompetitiveness of other countries) or because of in-terdependences in creditors’ portfolios (for example,illiquidity in one market forces financial intermedi-aries to liquidate assets in other markets).112 Such“spillovers” resulting from interdependences havebeen cited as contributing in important ways to thespread of the east Asian crisis. A third reason for clus-tering is that a crisis in one country may lead creditorsto reevaluate the fundamentals of other countries,even if these have not objectively changed, or maylead creditors to reduce the riskiness of their portfo-lios and “flee to quality.” It is this effect, specifically,that is sometimes referred to as contagion (or “pure”contagion);113 it may be associated with “herding” byinvestors, resulting from bandwagon effects driven byasymmetric information or from the incentives facedby fund managers.

Currency Crises and Contagion

83

109Despite the trend toward greater financial market openness, inmany emerging market economies government involvementremains large. As a consequence, banks often make decisions thatare not based on purely commercial criteria, thus increasing the risk-iness of banks’ assets. Moreover, because of their limited experienceunder repressed or regulated financial systems of operating on acommercial basis, banks are rendered more vulnerable to the com-petitive pressures that emerge when the sector is deregulated.

110See Paul R. Masson, “Contagion: Monsoonal Effects, Spill-overs, and Jumps Between Multiple Equilibria” (unpublished;Washington: IMF, 1998).

111Paul R. Masson and Michael Mussa, “The Role of the IMF:Financing and Its Interactions with Adjustment and Surveillance,”Pamphlet Series, No. 50 (Washington: IMF, 1995).

112Ilan Goldfajn and Rodrigo O. Valdés, “Capital Flows and theTwin Crises: The Role of Liquidity,” Working Paper 97/87(Washington: IMF, July 1997).

113This arises only if financial markets exhibit multiple equilibriaand self-fulfilling speculative attacks.

IV FINANCIAL CRISES: CHARACTERISTICS AND INDICATORS OF VULNERABILITY

The scope for speculative pressures to spread acrosscountries has been of increased concern to policymak-ers since the 1992–93 ERM crises and especially sincethe 1994–95 Mexican crisis and the recent east Asiancrisis. During the ERM crises, the French franc, the

Irish pound, and the Swedish krona experienced spec-ulative pressures when the Italian lira, the pound ster-ling, and the Finnish markka were floated. Similarpressures were experienced by Norway when theSwedish krona’s peg to the European currency unit

84

Effective prudential regulation and supervision ofbanks are essential to the financial stability and efficientfunctioning of any economy because the banking systemplays a central role in the payments system and in the mo-bilization and distribution of saving. The task of suchregulation and supervision is to ensure that banks operatein a prudent manner and that they hold capital and re-serves sufficient to support the risks that arise in theirbusiness. Strong and effective banking regulations andsupervision provide a public good that is needed to com-plement market forces for prudent banking to be ensuredin any country.

Weaknesses in the banking system of a country canthreaten financial stability, both in that country and inter-nationally. Thus, ways to strengthen financial systemshave attracted growing international concern. Several of-ficial bodies, including the Basle Committee on BankingSupervision,1 the Bank for International Settlements(BIS), the IMF, and the World Bank, have recently beenexamining ways to do so.2

The Basle Committee on Banking Supervision hasformulated 25 basic principles (The Basle Core Prin-ciples) that need to be in place for a supervisory systemto be effective. These principles can be summarized asfollows.3

Preconditions for Effective Banking Supervision

1. To be effective, a system of banking supervisionshould have clear responsibilities and objectives for eachagency involved in the supervision of banking organiza-tions. Each such agency should possess operational in-dependence and adequate resources. A suitable legalframework for banking supervision is also necessary, in-cluding provisions relating to authorization of banking

organizations and their ongoing supervision; powers toaddress compliance with laws as well as safety andsoundness concerns; and legal protection for supervi-sors. Arrangements for sharing information among su-pervisors, and protecting its confidentiality, should alsobe in place.

Licensing and Structure

2. The permissible activities of institutions that are li-censed and subject to supervision as banks should beclearly defined, and the use of the word “bank” in namesmust be controlled as far as possible.

3. The licensing authority must have the right to setcriteria and reject applications for establishments that donot meet the standards set. The licensing process, at aminimum, should consist of an assessment of the bankingorganization’s ownership structure, directors, and seniormanagement; its operating plan and internal controls; andits projected financial condition, including its capitalbase. Where the proposed owner or parent organization isa foreign bank, the prior consent of its home country su-pervisor should be obtained.

4. Banking supervisors must have the authority to re-view and reject any proposals to transfer significant own-ership or controlling interests in existing banks to otherparties.

5. Banking supervisors must have the authority to es-tablish criteria for reviewing major acquisitions or in-vestments by a bank and to ensure that corporate affilia-tions or structures do not expose the bank to undue risksor hinder effective supervision.

Prudential Regulations and Requirements

6. Banking supervisors must set prudent and appropri-ate minimum capital adequacy requirements for allbanks. Such requirements should reflect the risks that thebanks undertake and must define the components of cap-ital, bearing in mind their ability to absorb losses. At leastfor internationally active banks, these requirementsshould not be less than those established in the BasleCapital Accord and its amendments.

7. An essential part of any supervisory system is theevaluation of a bank’s policies, practices, and proceduresrelated to the granting of loans and making of invest-ments and the ongoing management of the loan and in-vestment portfolios.

8. Banking supervisors must be satisfied that banksestablish and adhere to adequate policies, practices, andprocedures for evaluating the quality of assets andthe adequacy of loan-loss provisions and loan-lossreserves.

Box 7. Effective Banking Prudential Regulations and Requirements

1The Basle Committee on Banking Supervision was estab-lished by the central bank Governors of the Group of Ten coun-tries in 1975 and consists of senior representatives of bankingsupervisory authorities and central banks from Belgium,Canada, France, Germany, Italy, Japan, Luxembourg, theNetherlands, Sweden, Switzerland, the United Kingdom, andthe United States.

2For details see David Folkerts-Landau and Carl-JohanLindgren, Toward a Framework for Financial Stability (Wash-ington: IMF, January 1998).

3A comprehensive summary of these principles is providedin Folkerts-Landau and Lindgren, Toward a Frameworkfor Financial Stability. See also Basle Committee on Bank-ing Supervision, Core Principles for Effective BankingSupervision (Basle, Switzerland: Bank for InternationalSettlements, 1996).

(ECU) was abandoned, and by the Portuguese escudowhen the Spanish peseta was devalued. The deprecia-tion of the Mexican peso in December 1994 led tospeculative pressures on other emerging market cur-rencies, especially those of Argentina and Brazil, and

to a lesser extent the Philippines. Finally, the crisis inThailand in mid-1997 quickly spread with great forceand persistence to Indonesia, Malaysia, the Philippines,and, somewhat later, to Korea and, more briefly, toHong Kong SAR, Singapore, and Taiwan Province of

Currency Crises and Contagion

85

9. Banking supervisors must be satisfied that bankshave management information systems that enable man-agement to identify concentrations within the portfolio,and supervisors must set prudential limits to restrictbank exposures to single borrowers or groups of relatedborrowers.

10. To prevent abuses arising from connected lending,banking supervisors must have in place requirements thatbanks lend to related companies and individuals on anarm’s-length basis, that such extensions of credit are ef-fectively monitored, and that other appropriate steps aretaken to control or mitigate the risks.

11. Banking supervisors must be satisfied that bankshave adequate policies and procedures for identifying,monitoring, and controlling country risk and transfer riskin their international lending and investment activities,and for maintaining appropriate reserves against suchrisks.

12. Banking supervisors must be satisfied that bankshave in place systems that accurately measure, monitor,and adequately control market risks; supervisors shouldhave powers to impose specific limits or a specific capitalcharge (or both) on market risk exposures, if warranted.

13. Banking supervisors must be satisfied that bankshave in place a comprehensive risk management process(including appropriate board and senior managementoversight) to identify, measure, monitor, and control allother material risks and, where appropriate, to hold capi-tal against these risks.

14. Banking supervisors must determine that bankshave in place internal controls that are adequate for thenature and scale of their business. These should includeclear arrangements for delegating authority and responsi-bility; separation of the functions that involve commit-ting the bank, paying away its funds, and accounting forits assets and liabilities; reconciliation of these processes;safeguarding its assets; and appropriate independent in-ternal or external audit and compliance functions to testadherence to these controls as well as applicable laws andregulations.

15. Banking supervisors must determine that bankshave adequate policies, practices, and procedures inplace, including strict “know-your-customer” rules, thatpromote high ethical and professional standards in the fi-nancial sector and prevent the bank being used, inten-tionally or unintentionally, by criminal elements.

Methods of Ongoing Banking Supervision

16. An effective banking supervisory system shouldconsist of some form of both on-site and off-site super-vision.

17. Banking supervisors must have regular contactwith bank management and thorough understanding ofthe institution’s operations.

18. Banking supervisors must have a means of collect-ing, reviewing, and analyzing prudential reports and statis-tical returns from banks on a solo and consolidated basis.

19. Banking supervisors must have a means of inde-pendent validation of supervisory information eitherthrough on-site examinations or use of external auditors.

20. An essential element of banking supervision is theability of the supervisors to supervise the banking groupon a consolidated basis.

Information Requirements

21. Banking supervisors must be satisfied that eachbank maintains adequate records drawn up in accordancewith consistent accounting policies and practices thatenable the supervisor to obtain a true and fair view ofthe financial condition of the bank and the profitabil-ity of its business, and that the bank publishes on aregular basis financial statements that fairly reflect itscondition.

Formal Powers of Supervisors

22. Banking supervisors must have at their disposaladequate supervisory measures to bring about timely cor-rective action when banks fail to meet prudential require-ments (such as minimum capital adequacy ratios), whenthere are regulatory violations, or where depositors arethreatened in any other way. In extreme circumstances,this should include the ability to revoke the banking li-cense or recommend its revocation.

Cross-Border Banking

23. Banking supervisors must practice global consoli-dated supervision over their internationally active bank-ing organizations, adequately monitoring and applyingappropriate prudential norms to all aspects of the busi-ness conducted by these banking organizations world-wide, primarily at their foreign branches, joint ventures,and subsidiaries.

24. A key component of consolidated supervision isestablishing contact and information exchange with thevarious other supervisors involved, primarily host-coun-try supervisory authorities.

25. Banking supervisors must require the local opera-tions of foreign banks to be conducted to the same highstandards as are required of domestic institutions andmust have powers to share information needed by thehome-country supervisors of those banks for the purposeof carrying out consolidated supervision.

IV FINANCIAL CRISES: CHARACTERISTICS AND INDICATORS OF VULNERABILITY

China within the region, as well as to a number ofemerging market economies in other regions.

Empirical evidence on the ERM crises suggests thatspillover and contagion effects did play a role.Countries that came under speculative attack had quitedifferent macroeconomic fundamentals, and only insome cases could the attacks be explained by weak-nesses in this area. Rather, the beliefs of investors

about the incentives facing monetary authorities toease policy so as to promote economic recovery seemto have played an important role.114

86

In evaluating the macroeconomic and external implica-tions of persistent current account deficits, three questionsare often posed. Is the debtor country solvent? Are currentaccount imbalances sustainable? Is the current accountdeficit excessive? This box discusses the notion of currentaccount sustainability, its relation to solvency, and the twomain approaches that have been used to make this notionoperational.1 The question of whether the current accountdeficit is “excessive” is not discussed in detail.2

A first approach to current account sustainability re-lies on projecting into the future the current policystance or private sector behavior; sustainability is en-sured if the resulting path of the trade balance is consis-tent with intertemporal solvency. If an unchanged policystance is eventually going to lead to a “drastic” shift toreverse the trade balance position (such as a sudden pol-icy tightening, causing a large recession) or lead to a bal-ance of payments crisis (such as an exchange rate col-lapse that raises the probability of default on externalobligations), the current account position is assumed tobe unsustainable. The drastic change in policy or crisissituation can be triggered by a domestic or an externalshock that causes a shift in domestic and foreign in-vestors’ confidence and a reversal of international capi-

tal flows.3 A second approach to external sustainability,which is linked to the extensive literature on balance ofpayments and currency crises, relies instead on a com-posite set of macroeconomic, financial, and external in-dicators to evaluate the risk of external crises.4

Until recently, analyses of external sustainability basedon the first approach relied on the standard condition re-lating the dynamics of debt accumulation to the trade bal-ance, the economy’s growth rate, the real interest rate onthe debt, and the real exchange rate. Given the change inthe composition of capital flows during the 1990s, how-ever, this approach provides only a partial picture of thedynamics of external liabilities because it ignores theevolution of the net equity position of the country and itsimpact on future investment income outflows. It is there-fore necessary to extend the approach so as to account forthe impact of non-debt-creating flows, such as foreign di-rect investment and portfolio equity investment, on acountry’s stock of external liabilities. This raises impor-tant measurement problems, as well as interesting ques-tions regarding risk sharing between the domestic econ-omy and foreign investors.

Clearly, for an economy to remain solvent, the ratio ofexternal liabilities to output or to exports cannot growwithout bound. Therefore, the long-run net resource trans-

Box 8. The Current Account and External Sustainability

1For further discussion, see Gian Maria Milesi-Ferretti andAssaf Razin, Current Account Sustainability, Princeton Studiesin International Finance, No. 81 (Princeton, New Jersey:Princeton University, October 1996).

2To answer this question, a benchmark is needed that givesinformation on the “appropriate” level of current account im-balances. This benchmark can be based on a model that speci-fies the behavior of consumption, investment, and output, withpublic and private sectors obeying their intertemporal budgetconstraints. Actual imbalances can then be compared with thepredicted ones to judge whether they have been excessive.Intertemporal models of current account determination usingdata from industrial and developing countries have been esti-mated by, among others, Atish Ghosh and Jonathan Ostry, “TheCurrent Account in Developing Countries: A Perspective fromthe Consumption-Smoothing Approach,” World Bank EconomicReview, Vol. 9 (No. 2, May 1995), pp. 305–33; LeonardoLeiderman and Assaf Razin, “Determinants of ExternalImbalances: The Role of Taxes, Government Spending, andProductivity,” Journal of the Japanese and InternationalEconomies, Vol. 5 (December 1991), pp. 421–50; and ReuvenGlick and Kenneth S. Rogoff, “Global Versus Country-SpecificProductivity Shocks and the Current Account,” Journal ofMonetary Economics, Vol. 35 (February 1995), pp. 159–92.

3For an analysis of sharp reductions in current accountdeficits and their consequences for economic activity, see GianMaria Milesi-Ferretti and Assaf Razin, “Sharp Reductions inCurrent Account Deficits: An Empirical Analysis,” WorkingPaper 97/168 (Washington: IMF, December 1997); and GianMaria Milesi-Ferretti and Assaf Razin, “Current AccountReversals and Currency Crises,” paper presented at the NBERconference on Currency Crises, Cambridge, Massachusetts,February 6–7, 1998.

4See, for example, Rudiger Dornbusch, Ilan Goldfajn, andRodrigo Valdes, “Currency Crises and Collapses,” BrookingsPapers on Economic Activity: 2 (1995), pp. 219–93; MorrisGoldstein, “Presumptive Indicators/Early Warning Signals ofVulnerability to Financial Crises in Emerging Market Eco-nomies” (unpublished; Washington: Institute for InternationalEconomics, January 1996); Graciela Kaminsky, Saul Lizondo,and Carmen M. Reinhart, “Leading Indicators of CurrencyCrises,” Working Paper 97/79 (Washington: IMF, July 1997);Gian Maria Milesi-Ferretti and Assaf Razin, “Current AccountSustainability: Selected East Asian and Latin AmericanExperiences,” Working Paper 96/110 (Washington: IMF, October1996); and Jeffrey Sachs, Aaron Tornell, and Andrés Velasco,“Financial Crises in Emerging Markets: Lessons from 1995,”Brookings Papers on Economic Activity: 1 (1996), pp. 147–98.

114See Barry Eichengreen, Andrew K. Rose, and CharlesWyplosz, “Speculative Attacks on Pegged Exchange Rates: AnEmpirical Explanation with Special Reference to the European

Spillover and contagion effects also appear to haveplayed a role in the 1994–95 Mexican crisis. Evidenceof increased cross-country correlation in movements

of equity and Brady bond returns among emergingmarkets in Latin America in the wake of the crisis, to-gether with the heterogeneity of macroeconomic fun-damentals, has been interpreted as indicating eitherherding behavior by investors or the effect of in-vestors selling off equities in several emerging mar-kets in order to raise cash to meet expected increasesin redemptions in other markets (that is, interdepen-

Currency Crises and Contagion

87

Monetary System,” in Matthew Canzoneri, Wilfred Ethier, andVittorio Grilli, eds., The New Transatlantic Economy (New Yorkand Cambridge: Cambridge University Press, 1996). See also theJanuary 1993 World Economic Outlook: Interim Assessment.

fer (trade surplus) that an indebted country must undertakein order to keep the ratio of external liabilities to GDPconstant has often been used as a simple measure of sol-vency. This measure, however, has serious shortcomings.First, although it provides a long-run condition for the sta-bility of the ratio of external liabilities to GDP, there canbe no presumption of whether that ratio is “optimal” or ap-propriate. Second, in developing countries, protracted cur-rent account imbalances can characterize these countries’transition toward higher levels of output, implying thatsteady-state conditions may not be the appropriate bench-mark to evaluate the sustainability of current account im-balances. In other words, there can be no presumption thatin the short and medium run a fast-growing economy witha low level of external liabilities should aim at stabilizingthe ratio of external liabilities to GDP or to exports at itscurrent level. Third, this calculation is based on the pre-sumption that the country will not face future “liquidityconstraints” because foreign investors would be willing tocontinue lending on current terms. In a world of high cap-ital mobility and rapid response of capital flows to“news,” this assumption may be inappropriate. For exam-ple, these simple solvency tests would clearly have failedto signal problems ahead for most fast-growing Asianeconomies, including Indonesia and Korea.

For these reasons, some authors are strongly critical ofsustainability analyses that focus exclusively on solvencyconditions and flow variables, such as the current ac-count, and argue that external crises can occur because ofstock imbalances and capital market factors, and not justbecause of the current account position.5 This suggeststhe need to monitor a more comprehensive set of capitalaccount and financial indicators, in addition to the currentaccount, so as to correctly evaluate external sustainabil-ity. The approach based on indicators can be comple-mentary to the study of the dynamics of external liabili-ties; a more general set of macroeconomic, financial, andexternal variables can provide useful information on acountry’s vulnerability to external shocks and changes inforeign investors’ sentiment.