Embed Size (px)

Citation preview

CHAPTER THREE

FINANCIAL REPORTING PROCESS

PRINCIPLE – Revenue Recognition

Revenue is recognized when it is earned not paid

Expenses are recognized when it happens

Accrual vs Cash Basis

All individuals are on a cash basis. Record the revenue and expense when it is paid in cash.

Small business may also use cash basis.Accrual – “It is a cruel thing not to pay”.Record when it happens not when it paid. Corporations report on an accrual basis

PRINCIPLE - Matching

To get a true net income expenses should match the revenue earned in the same period of time.

Most important at the end of the year. If you receive the revenue in December 2012 but don’t pay your employees until January 2013—the revenue is in December 2012 but the expense for that revenue is in January 2013.

Tool to match revenue and expenses

Adjusting entries One account must be a balance sheet

account, the other must be an income statement account

NO CASH in adjusting entries

repayments – covers more than one month Rent, supplies, insurance, depreciation

Types of adjusting entries

PrepaymentsAccrued Expenses and revenue

Prepayments

covers more than one monthRent, supplies, insurance, depreciation

Rent – Original Entry Prepaid Rent Cash

Adjusting Entry to record Rent for the current month Rent Expense – income statement account Prepaid Rent – Balance Sheet account

Page 137 Be3-7

Supplies

Original Entry Supplies Cash

Record what was used during the month Supplies Expense – income statement Supplies - balance sheet

Page 137 BE 3-6

Insurance

Original Entry for 6 months of insurance Prepaid Insurance Cash

Record insurance used up for the month Insurance Expense – Income Statement Prepaid Insurance – Balance Sheet

Page 143 BE 3-8

Depreciation

Original Entry Plant Asset N/P

Adjusting Entry Depreciation Expense – income statement Accumulated Depreciation - Balance Sheet

DON”T TOUCH THE ASSET!!! Don’t change the cost of the asset put it in a contra asset account – accumulated depreciation

Pg 143 BE 3-9

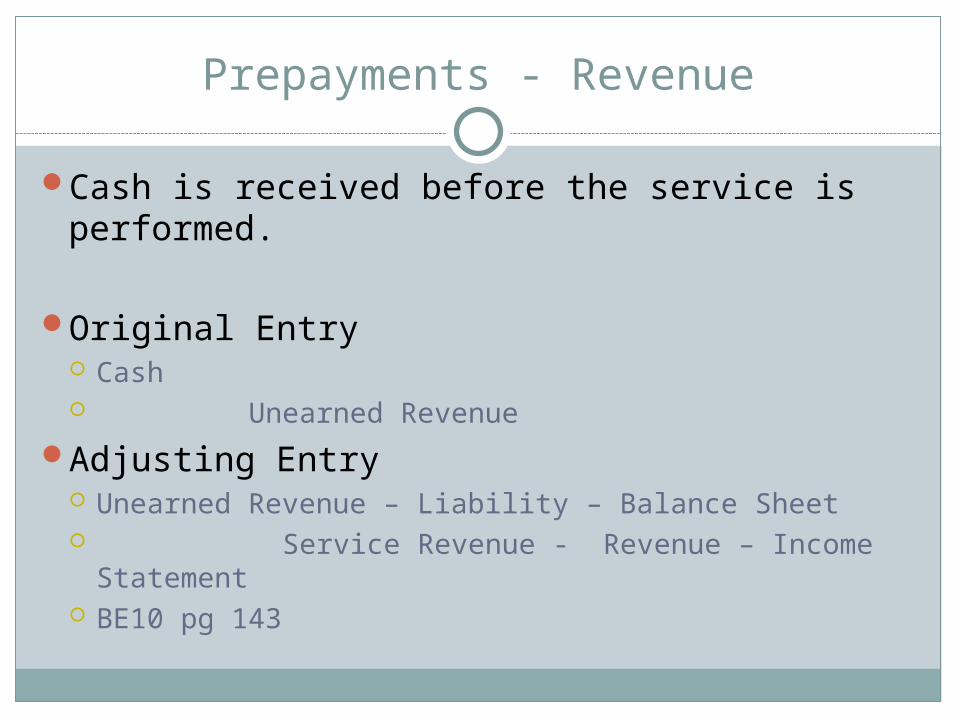

Prepayments - Revenue

Cash is received before the service is performed.

Original Entry Cash Unearned Revenue

Adjusting Entry Unearned Revenue – Liability – Balance Sheet Service Revenue - Revenue – Income Statement BE10 pg 143

Accruals

Cash is received after the expense has incurred or the revenue has been earned.

Accrued Expenses Accrued Wages, Utilities, Interest Expense

Accrued Revenue Interest Receivable, A/R (I disagree with this one.

Should be other than A/R like fees receivable or service receivable)

Unpaid (Accrued)Wages

Need to record the expense in the same month as the revenue

No original Entry since it was not paidAdjusting Entry

Wages Expense – Income Statement Wages Payable – Balance Sheet

BE11 pg 143

Interest Expense

Owe interest on a note but will not pay it until the note comes due.

Interest Expense Interest Payable - has not been paid

Accrued Revenue

Need to record the revenue but will not be paid for it until a later date.

Note receivable has interest accumulating until the due date, must record the interest when it is earned not paid

Interest receivable Interest Receivable – Balance Sheet Interest Income – Income Statement BE 13 pg144

Service Revenue performed in advance

Contractor: BuilderPerformed the work but can’t be paid until the

project is 75% complete. The project at end of year is 70% complete. Have expenses during this time so must record the revenue to match it.

Can’t record an invoice so shouldn’t put it in A/R – won’t reconcile with A/R master account. Fees Receivable Service Revenue

Exercises

E8 pg 147E10 pg 147

Accounting Cycle so far

General Journal – Daily TransactionsPost to General LedgerTrial BalanceGeneral Journal – Adjusting EntriesPost to General LedgerAdjusted Trial BalanceFinancial Statements: IN, SE, BS

Closing Entries

Assets, Liabilities, Stockholders Equity = Permanent Accounts. Always open, never close

Revenue and Expenses= Net Income By the Year so you must close at the end of

each year.To close means to make zero by transfering it

somewhere.Do the opposite of the normal balance. Close to Retained Earnings Entries are recorded on General Journal –

Closing Entries

RED

Close revenue to Retained Earnings (R) Service Revenue Consulting Revenue Retained Earnings

Close expenses to Retained Earnings (E) Rent Expense Salary Expense Utitlity Expense Retained Earnings

Close Dividends to Retained Earnings Retained Earnings (reduces retained earnings) Dividends Example : page 132 Illustration 3-15

Post entries to General LedgerPost Closing Trial Balance

Will only have A, L , SE No revenue and expenses

BE 3-19 and BE 3-20 pg 145

Last part of accounting cycle

After Financial Statements at end of year

Record closing entries to General JournalPost to General LedgerPrepare Post Closing Trial Balance

![[PPT]Revenue Recognition (ppt) - WordPress.com · Web viewProper revenue recognition revolves around three terms: Revenue are realized when-A company exchanged goods and services](https://img.pdfslide.net/doc/110x75/5adeed427f8b9ac0428b817d/pptrevenue-recognition-ppt-viewproper-revenue-recognition-revolves-around.jpg)