Embed Size (px)

Citation preview

CHAPTER TWELVE

CONVERTIBLE SECURITIES

© 2001 South-Western College Publishing

2

Outline

Convertible Bonds Characteristics Pricing of Convertible Bonds Why Companies Issue Convertible Bonds Unusual Features

Convertible Preferred Stock Background on Preferred Stock The Conversion Feature

3

Outline

Warrants Characteristics Pricing of Warrants Warrants and Leverage

Accounting Implications: An Optional Technical Note Dilution of Earnings Common Stock Equivalents and

Other Potentially Dilutive Securities Computation of PEPS and FDEPS

4

Convertible Bonds: Characteristics

Convertible bonds give their owner the right to exchange the bonds for a set quantity of some other asset. This other asset is normally shares of stock in the same company.

The number of shares the bondholder receives per $1,000 par value when converting the bond is called the conversion ratio.

5

Convertible Bonds: Characteristics

conversionvalue

conversionratio

currentstock price= X

conversion price =par value

conversion ratio

premium overconversion value = -

marketprice

conversionvalue

6

Pricing of Convertible Bonds

Over time, a convertible bond will increasingly act like a share of stock or like a non-convertible bond.

A bond whose conversion price is substantially above the current market price of the associated common stock is a busted convertible.

A convertible in a company whose stock has appreciated is an example of a common stock equivalent.

Metamorphosis of a Convertible Bondst

ock

pri

ce

7

time

conversion price

commonstock

equivalent

rising stock price

Acts like a Stock

bustedconvertible

declining or slow rising stock price

Acts like a Bond

newconvertible

bond

8

Pricing of Convertible Bonds

Convertible bonds should never sell for less than their conversion value.

With a busted convertible, the conversionfeature has little value.

Convertible bonds provide for upside potential while reducing downside risk.

9

Pricing of Convertible Bonds

The premium payback period is the time required for the enhanced income from the bond (relative to the equivalent number of stock shares) to offset the premium over the conversion value.

The premium payback period is sometimescalled the break-even time.

10

Calculating Premium Payback Period

ratio conversion

valuemarket price conversionmarket

ratio conversion

share per dividendsratio conversion -interest bondprice stock - price conversionmarket

Premium payback period =

11

Why Companies Issue Convertible Bonds

Convertible bonds can usually be offered at a

lower interest rate than would otherwise be required.

All convertible bonds are callable. If called, a convertible bond must be (1)sold, (2)redeemed, or (3)converted.

Corporations like to issue convertible bonds because of the likelihood that they will never have to repay the debt.

12

Convertible Bonds: Unusual Features

Interest payments: A few convertible bonds do not pay interest twice a year, but monthly or quarterly, for example.

Underlying asset: Many convertible bonds are convertible into the securities of another company. Some are convertible into cash.

LYONs: Many companies issue zero coupon bonds, or liquid yield option notes (LYONs). A number of these are convertible into the company’s common stock.

13

Convertible Preferred Stock

Preferred stock is attractive to corporations

because of the tax-exempt nature of most dividend income.

From an investment perspective, preferred stock is a fixed income security.

Preferred stock is identified by its annual dividend.

The fundamentals of conversion are the same as those for convertible bonds.

14

Warrants: Characteristics

A warrant is a nondividend-paying security giving its owner the right to buy a certain number of shares at a set price directly from the issuing company.

Warrants have no voting rights. Outside the United States, warrants are often

issued in conjunction with a new debt issue, thus enabling a lower interest rate than would otherwise be required on the issue.

Warrants can be detachable or non-detachable.

15

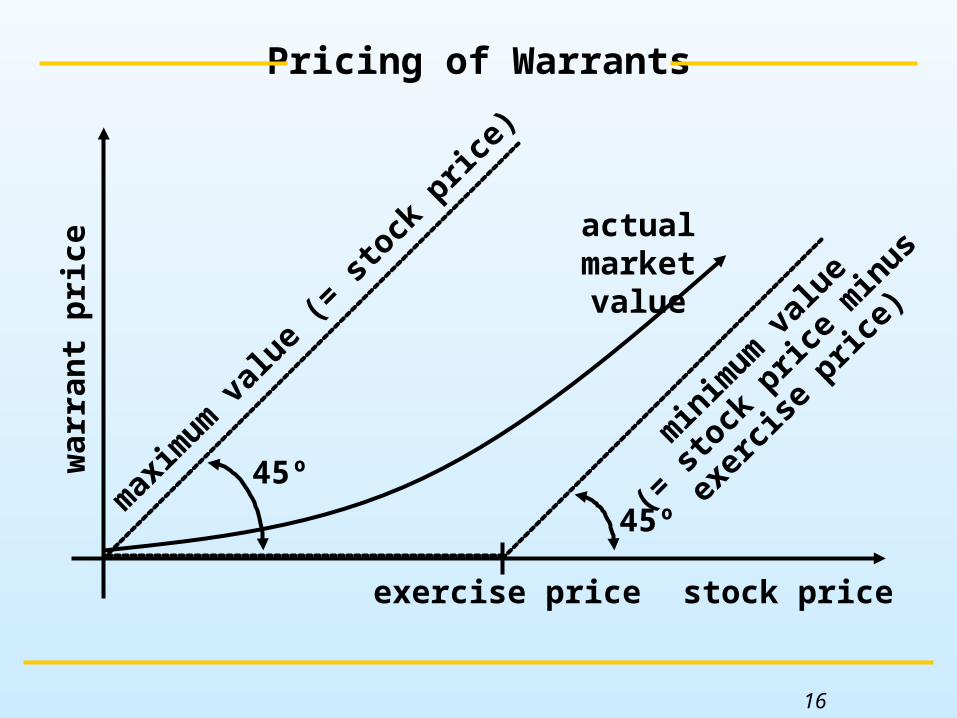

The exercise price is the price at which an investor holding warrants may buy the underlying shares.

When the stock price rises above theexercise price, the warrant is in-the-money, and has intrinsic value.

If the stock price is below the exercise price, the warrant is out-of-the-money.

Speculators buy warrants because of theleverage they provide.

Pricing of Warrants

Pricing of Warrants

16

war

ran

t p

rice

stock price

actual marketvalue

45ºmax

imum

val

ue (=

sto

ck p

rice)

exercise price

45º

min

imum

val

ue

(= s

tock

pric

e m

inus

exer

cise

pric

e)

17

When common stock equivalents are present,

accountants must determine both primary and fully diluted earnings per share.

Primary earnings per share (PEPS) is basedon common shares outstanding plus shares considered to be common stock equivalents.

Fully diluted earnings per share (FDEPS) reflects the dilution of earnings per share that would occur if all possible convertible securities were converted.

Accounting Implications: An Optional Technical Note

18

Convertible bonds and convertible preferred

stock are considered common stock equivalents and are used in the PEPS calculation if their yield was less than two-thirds the yield of the average AA bond yield at the time the security was issued.

A convertible that is not a common stock equivalent is classified as an other potentially dilutive security and may be used in the FDEPS calculation.

Accounting Implications

19

Computation of PEPS

primaryearningsper share

net incomeavailable to

commonshareholders

adjustmentsfor

common stockequivalents

preferredstock

dividends

weighted average number of common andcommon stock equivalent shares outstanding

-

=

+

20

Computation of FDEPS

fullydiluted

earningsper share

adjustments for other potentially dilutive securities

weighted average number of common shares,common stock equivalent shares and

other potentially dilutive securitiesoutstanding during the reporting period

=

net incomeavailable to common

shareholders

adjustmentsfor common stock

equivalents

preferredstock

dividends-

+

+

21

Review

Convertible Bonds Characteristics Pricing of Convertible Bonds Why Companies Issue Convertible Bonds Unusual Features

Convertible Preferred Stock Background on Preferred Stock The Conversion Feature

22

Review

Warrants Characteristics Pricing of Warrants Warrants and Leverage

Accounting Implications: An Optional Technical Note Dilution of Earnings Common Stock Equivalents and

Other Potentially Dilutive Securities Computation of PEPS and FDEPS