Embed Size (px)

Citation preview

Characterising a Port for Implementation

through PPP in Indonesia

Presented by: David Wignall

Date: September 2018

Typical projects

Indonesia

2016 2017

Brunei 1.0% 2.5%

Cambodia 7.0% 7.1%

Indonesia 5.0% 5.1%

Laos 7.0% 0.0%

Malaysia 4.1% 4.4%

Myanmar 8.4% 8.3%

Philippines 6.4% 6.2%

Singapore 1.8% 2.0%

Thailand 3.2% 3.5%

Vietnam 6.0% 6.3%

Indonesia the last great container story

Driven by: Population (consumption), GDP, Manufacturing, Mining, FDI…

Probable headline container growth same as GDP (5 to 7%)

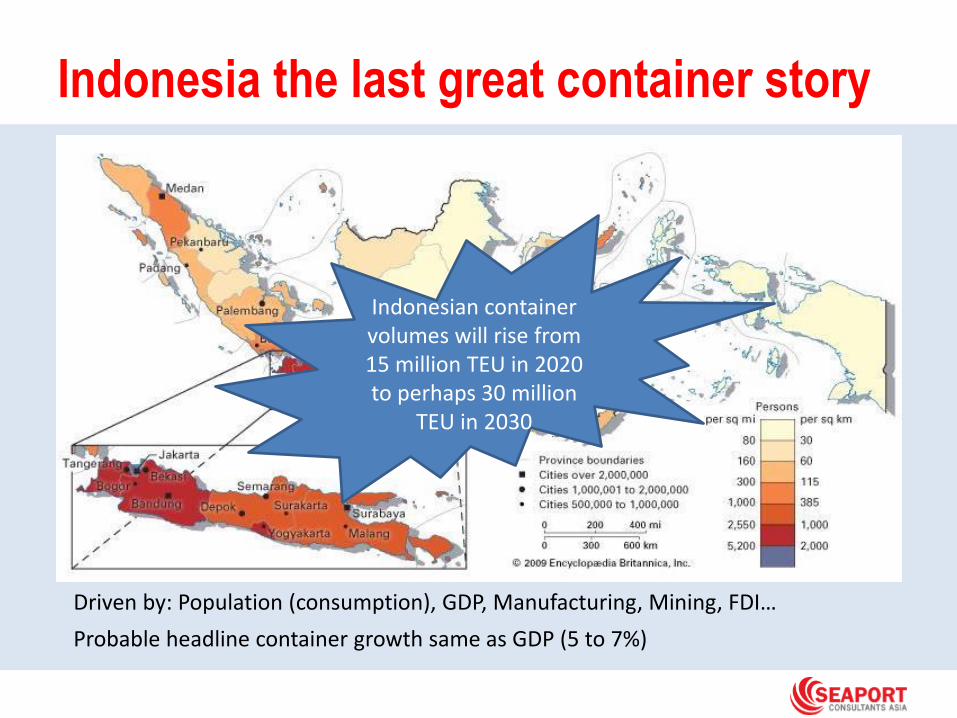

Indonesia the last great container story

Driven by: Population (consumption), GDP, Manufacturing, Mining, FDI…

Probable headline container growth same as GDP (5 to 7%)

Indonesian container volumes will rise from 15 million TEU in 2020 to perhaps 30 million

TEU in 2030

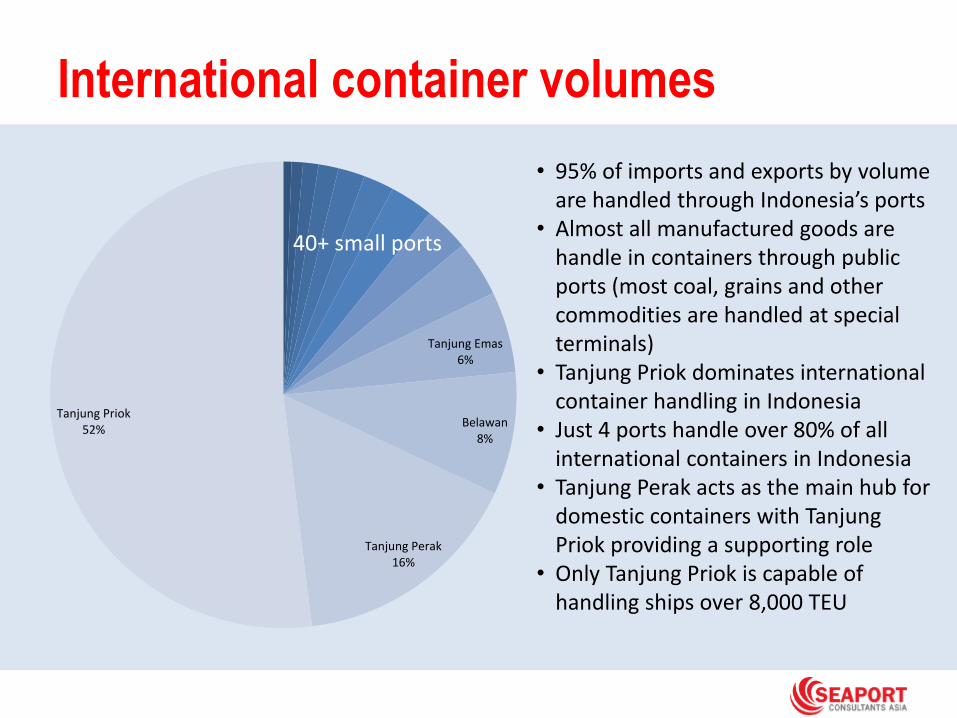

International container volumes

Tanjung Emas 6%

Belawan8%

Tanjung Perak16%

Tanjung Priok52%

• 95% of imports and exports by volume are handled through Indonesia’s ports

• Almost all manufactured goods are handle in containers through public ports (most coal, grains and other commodities are handled at special terminals)

• Tanjung Priok dominates international container handling in Indonesia

• Just 4 ports handle over 80% of all international containers in Indonesia

• Tanjung Perak acts as the main hub for domestic containers with Tanjung Priok providing a supporting role

• Only Tanjung Priok is capable of handling ships over 8,000 TEU

40+ small ports

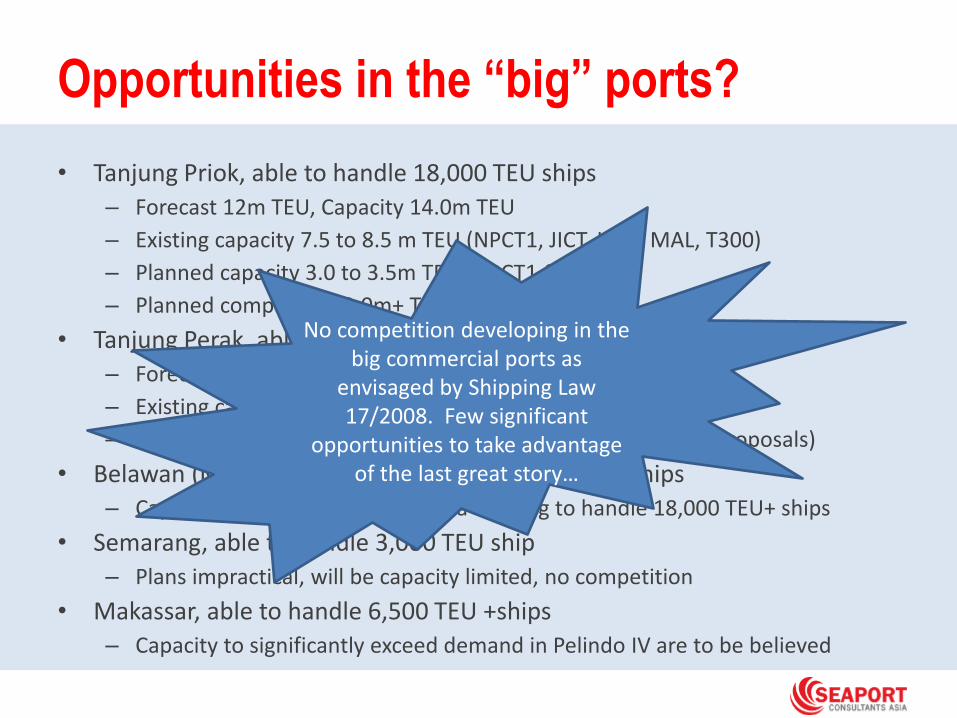

Opportunities in the “big” ports?

• Tanjung Priok, able to handle 18,000 TEU ships

– Forecast 12m TEU, Capacity 14.0m TEU

– Existing capacity 7.5 to 8.5 m TEU (NPCT1, JICT, Koja, MAL, T300)

– Planned capacity 3.0 to 3.5m TEU (NPCT1 & 2)

– Planned competitors 2.0m+ TEU (Pantimban)

• Tanjung Perak, able to handle light 5,000 TEU ships

– Forecast 6m TEU, Capacity 6.5m+ TEU

– Existing capacity 3.5+ (TPS, BJTI, Nilam, Lamong)

– Planned capacity 3.0+ (Lamong 2, AKR/PIII JV, other private proposals)

• Belawan (Medan), able to handle small container ships

– Capacity to exceed demand, Kuala Tanjung to handle 18,000 TEU+ ships

• Semarang, able to handle 3,000 TEU ship

– Plans impractical, will be capacity limited, no competition

• Makassar, able to handle 6,500 TEU +ships

– Capacity to significantly exceed demand in Pelindo IV are to be believed

Opportunities in the “big” ports?

• Tanjung Priok, able to handle 18,000 TEU ships

– Forecast 12m TEU, Capacity 14.0m TEU

– Existing capacity 7.5 to 8.5 m TEU (NPCT1, JICT, Koja, MAL, T300)

– Planned capacity 3.0 to 3.5m TEU (NPCT1 & 2)

– Planned competitors 2.0m+ TEU (Pantimban)

• Tanjung Perak, able to handle light 5,000 TEU ships

– Forecast 6m TEU, Capacity 6.5m+ TEU

– Existing capacity 3.5+ (TPS, BJTI, Nilam, Lamong)

– Planned capacity 3.0+ (Lamong 2, AKR/PIII JV, other private proposals)

• Belawan (Medan), able to handle small container ships

– Capacity to exceed demand, Kuala Tanjung to handle 18,000 TEU+ ships

• Semarang, able to handle 3,000 TEU ship

– Plans impractical, will be capacity limited, no competition

• Makassar, able to handle 6,500 TEU +ships

– Capacity to significantly exceed demand in Pelindo IV are to be believed

No competition developing in the big commercial ports as

envisaged by Shipping Law 17/2008. Few significant

opportunities to take advantage of the last great story…

Public Private Partnership

• Public-private partnership (PPP) describes a government service or private business venture which is funded and operated through a partnership of government and one or more private companies. These schemes are sometimes referred to as PPP, P3 or P3

• The standard model of public procurement of infrastructure came from concerns about the level of public debt

• Government sought to encourage private investment in infrastructure so that they did not have to make such investments

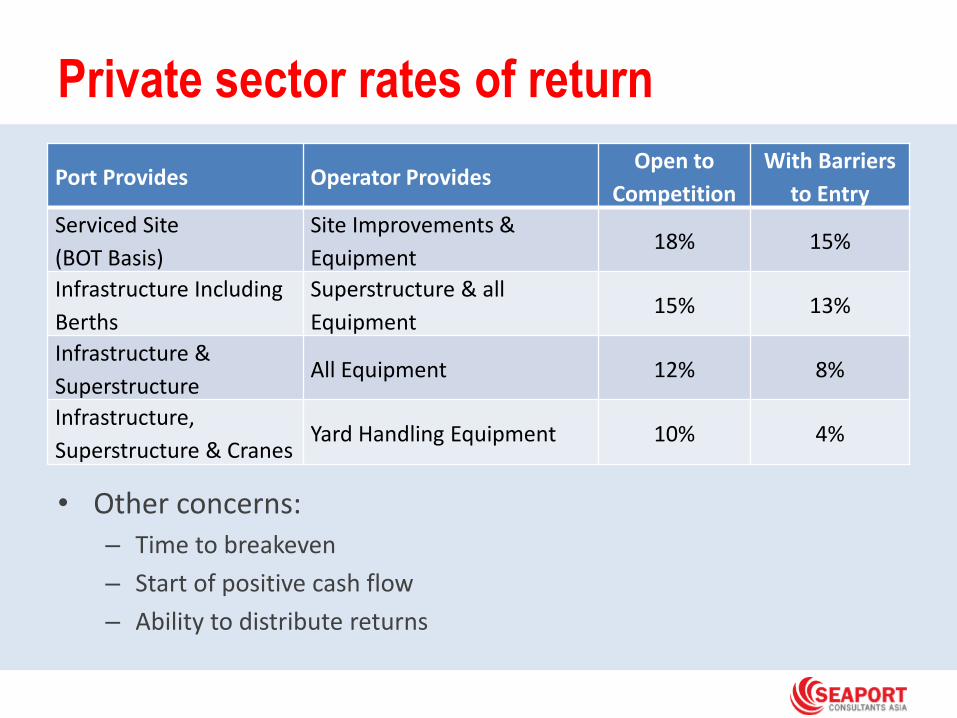

Private sector rates of return

Port Provides Operator ProvidesOpen to

Competition

With Barriers

to Entry

Serviced Site

(BOT Basis)

Site Improvements &

Equipment18% 15%

Infrastructure Including

Berths

Superstructure & all

Equipment15% 13%

Infrastructure &

SuperstructureAll Equipment 12% 8%

Infrastructure,

Superstructure & CranesYard Handling Equipment 10% 4%

• Other concerns:– Time to breakeven

– Start of positive cash flow

– Ability to distribute returns

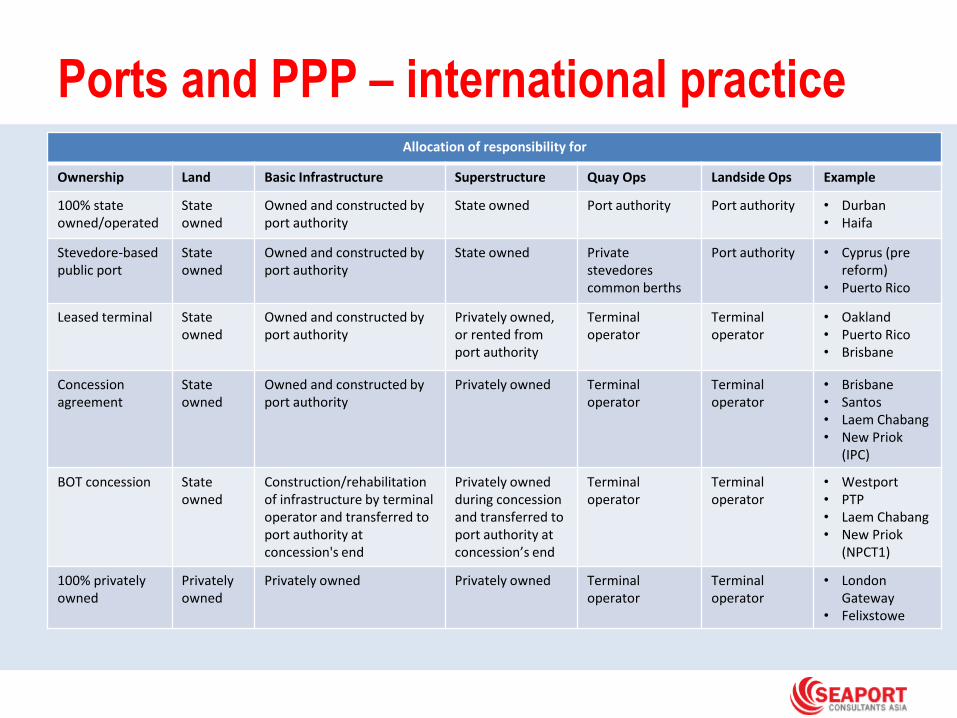

Ports and PPP – international practiceAllocation of responsibility for

Ownership Land Basic Infrastructure Superstructure Quay Ops Landside Ops Example

100% state owned/operated

State owned

Owned and constructed by port authority

State owned Port authority Port authority • Durban• Haifa

Stevedore-based public port

State owned

Owned and constructed by port authority

State owned Private stevedores common berths

Port authority • Cyprus (pre reform)

• Puerto Rico

Leased terminal State owned

Owned and constructed by port authority

Privately owned, or rented from port authority

Terminal operator

Terminal operator

• Oakland • Puerto Rico • Brisbane

Concession agreement

State owned

Owned and constructed by port authority

Privately owned Terminal operator

Terminal operator

• Brisbane• Santos• Laem Chabang • New Priok

(IPC)

BOT concession State owned

Construction/rehabilitation of infrastructure by terminal operator and transferred to port authority at concession's end

Privately owned during concession and transferred to port authority at concession’s end

Terminal operator

Terminal operator

• Westport• PTP• Laem Chabang • New Priok

(NPCT1)

100% privately owned

Privately owned

Privately owned Privately owned Terminal operator

Terminal operator

• London Gateway

• Felixstowe

PPP in Indonesian ports

• For the port sector, Shipping Law 17/2008

• For private provision of infrastructure, Presidential RegulationNo. 38/2015 concerning the Cooperation between the Government and the Business Entities in the Provision of Infrastructure

• The Bappenas Blue Book and annexes

• LKPP and the new Model Bid Documents

• There are going to be a lot of ports with limited commercial potential for investment

If Project non-commercial

• Government has two choices for a project that is economically justified but not commercial:– It can develop a design-build project from its own financing and

operate it, or

– It can develop a PPP project through a contractor in return for a government subvention

• In both cases, the government pays:– PPP does not necessarily widen availability of finance for non-

commercial infrastructure

– It does change the timing and amount of governmental cash flows and generally reduces risk-adjusted costs

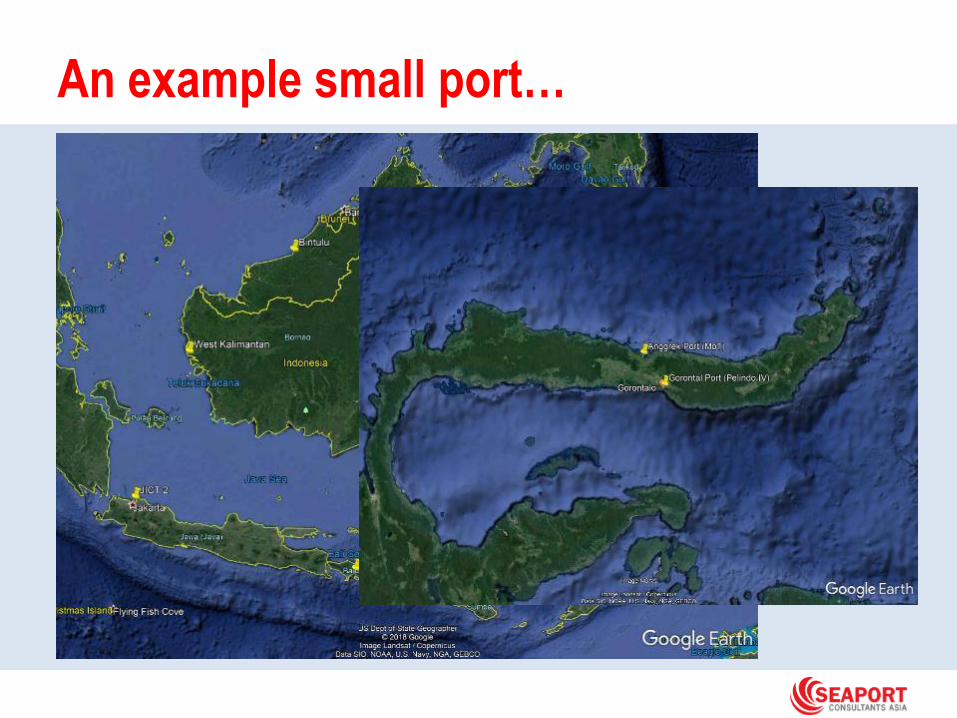

An example small port…

• Anggrek

Gorontalo Port – Pelindo IV

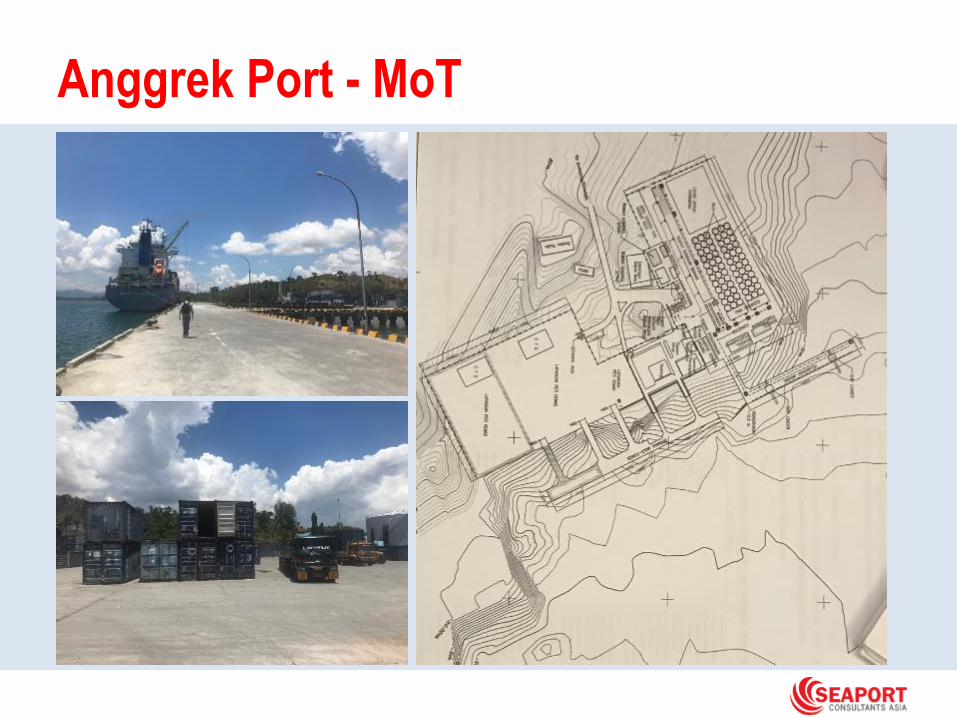

Anggrek Port - MoT

Designing a PPP for the port sector

• Economic impact/Commercial performance – Imbalance in trade– Regular, reliable services

• Level of leaderships from Government Contracting Agency – National Government– Provincial and city Government

• Private sector interest and the attitude of the local Pelindo • Level of technical difficulty, social and environmental impact • Implementation level

– Land acquisition – Regulatory approval

• Scale and PPP Modality:– CAPEX contribution – Subsidy to operations (availability payments)– Market intervention (monopoly or capacity control)

Thank you