Embed Size (px)

Citation preview

Universität Zürich

Characteristics of fixed-income securities

Angelo RanaldoUniversity of St. Gallen & University of Zurich

Public Debt ManagementFall term, University of Zurich

Universität Zürich Prof. Dr. Angelo Ranaldo

Master course Public Debt Management15. November 2013

1

Table of contents

1. Asset valuation of debt securities

2. Characteristics of fixed-income securities

3. Risks

4. Swiss bond market

5. Current issues

Universität Zürich Prof. Dr. Angelo Ranaldo

Master course Public Debt Management15. November 2013

2

Objectives of this lecture

Understand the main characteristics of a well-functioning market and take a critical view

Learn what is a primary and secondary market for government bonds

Understand why bonds indices have became so popular and study the specific case of the Swiss bond indices

Review the main characteristics of fixed income securities

Universität Zürich Prof. Dr. Angelo Ranaldo

Master course Public Debt Management15. November 2013

3

Well-functioning market

Efficiency — Prices quickly adjust to new information so that prevailing price

reflects all available information— Timely and accurate information on current and past price /

volume and on supply and demand.

Liquidity— Low transaction costs— Depth: Is the market able to absorb any volume size?— Breadth: The tightness of the market; the closeness between

demand and supply— Resiliency: Synonymous of elasticity or little trade impact— Time: Is it possible to trade any time?

Universität Zürich Prof. Dr. Angelo Ranaldo

Master course Public Debt Management15. November 2013

4

Well-functioning market

How does liquidity and prices relate each other?

“The flow of liquidity through the economy is similar to the flow of blood. In the body of the economy, prices are the nervous system, signaling the needs of different parts of the body. Money is the blood that dispatches resources in response to those signals.”

Nobu Kiyotaki (Princeton) and John Moore (University of Edinburgh), Clarendon Lectures, 26 November 2001.

Universität Zürich Prof. Dr. Angelo Ranaldo

Master course Public Debt Management15. November 2013

5

Well-functioning market

Are financial markets efficient?

Not always! For example:

On-the-run (i.e. newly issued) Treasuries trade at lower yields than identical off-the-run Treasuries.

Deviations from Covered Interest Parity — Mancini and Ranaldo “Limits to arbitrage during the crisis:

funding liquidity constraints & covered interest parity”, Swiss National Bank Working Paper.

Universität Zürich Prof. Dr. Angelo Ranaldo

Master course Public Debt Management15. November 2013

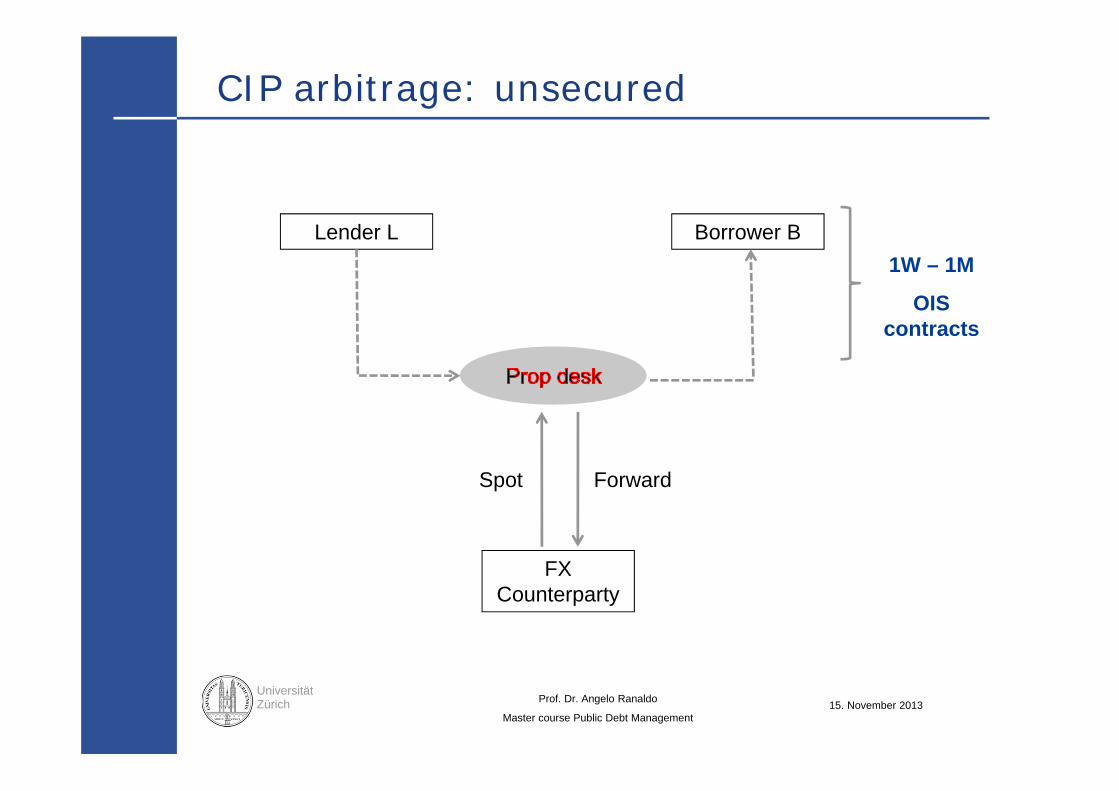

CIP arbitrage: unsecured

Lender L Borrower B

FX Counterparty

Spot Forward

1W – 1M

OIS contracts

Universität Zürich Prof. Dr. Angelo Ranaldo

Master course Public Debt Management15. November 2013

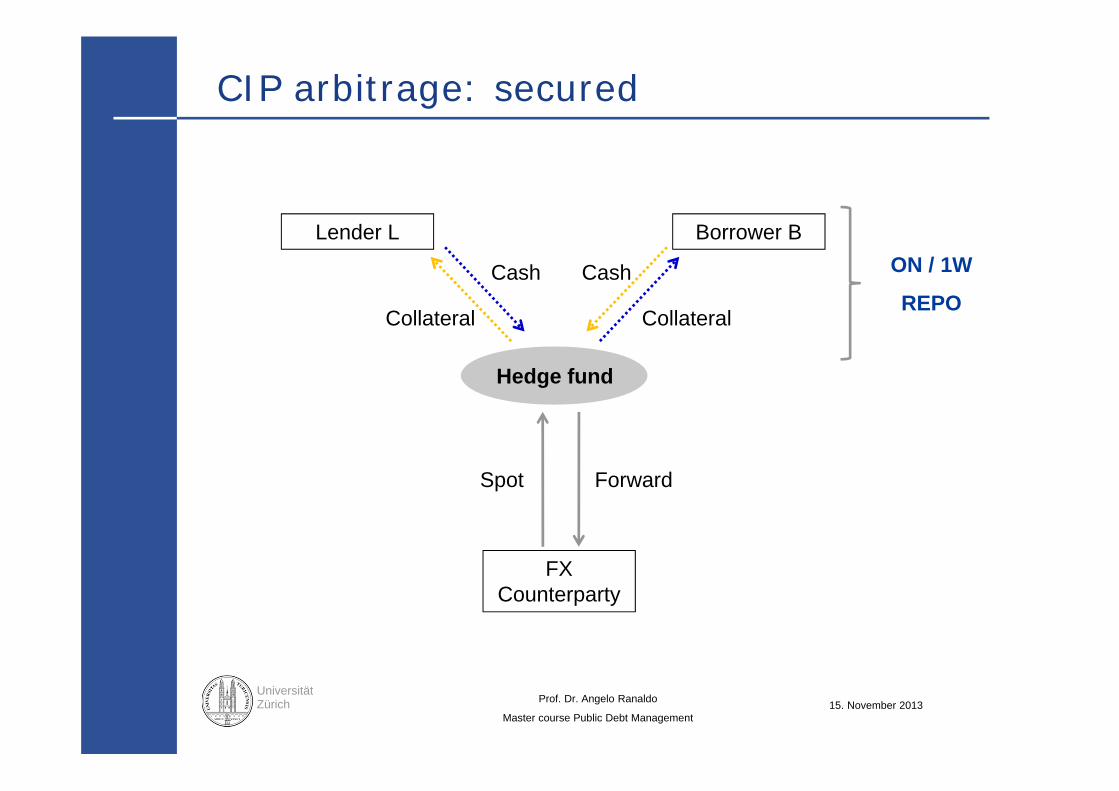

CIP arbitrage: secured

Lender L Borrower B

Hedge fund

FX Counterparty

Spot Forward

Cash

Collateral Collateral

Cash ON / 1W

REPO

Universität Zürich Prof. Dr. Angelo Ranaldo

Master course Public Debt Management15. November 2013

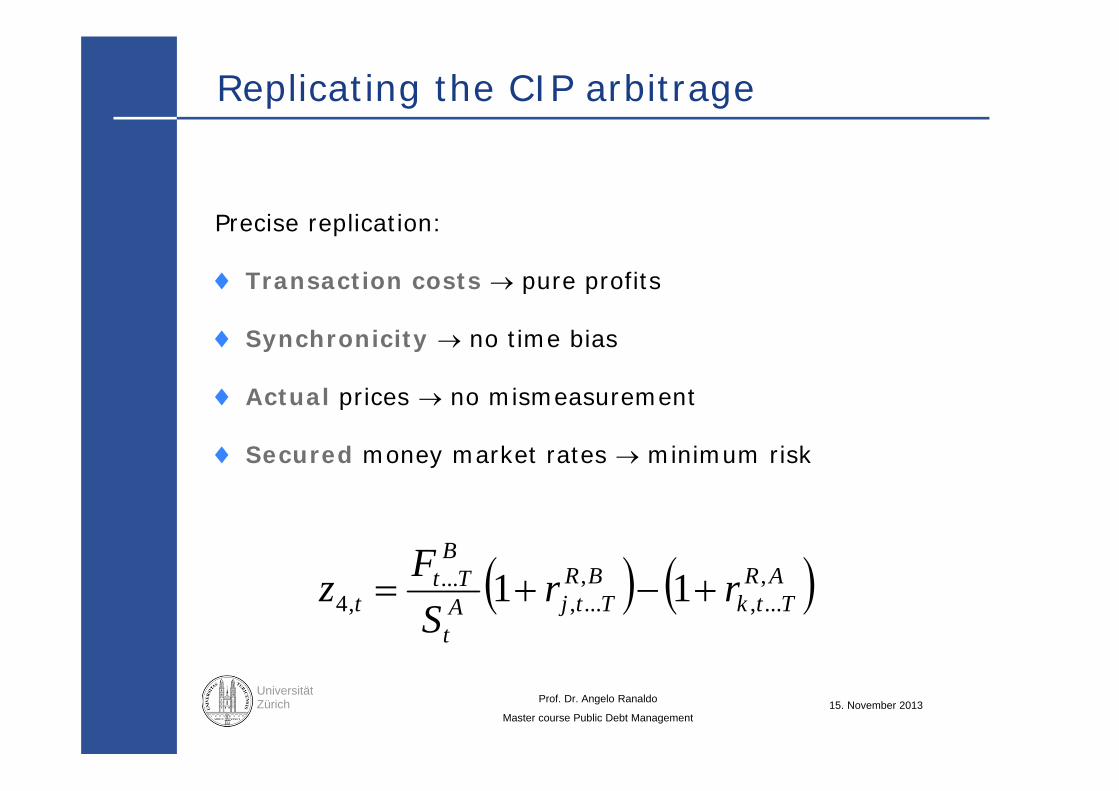

Replicating the CIP arbitrage

Precise replication:

Transaction costs pure profits

Synchronicity no time bias

Actual prices no mismeasurement

Secured money market rates minimum risk

ARTtk

BRTtjA

t

BTt

t rrSFz ,

...,,...,

...,4 11

Universität Zürich Prof. Dr. Angelo Ranaldo

Master course Public Debt Management15. November 2013

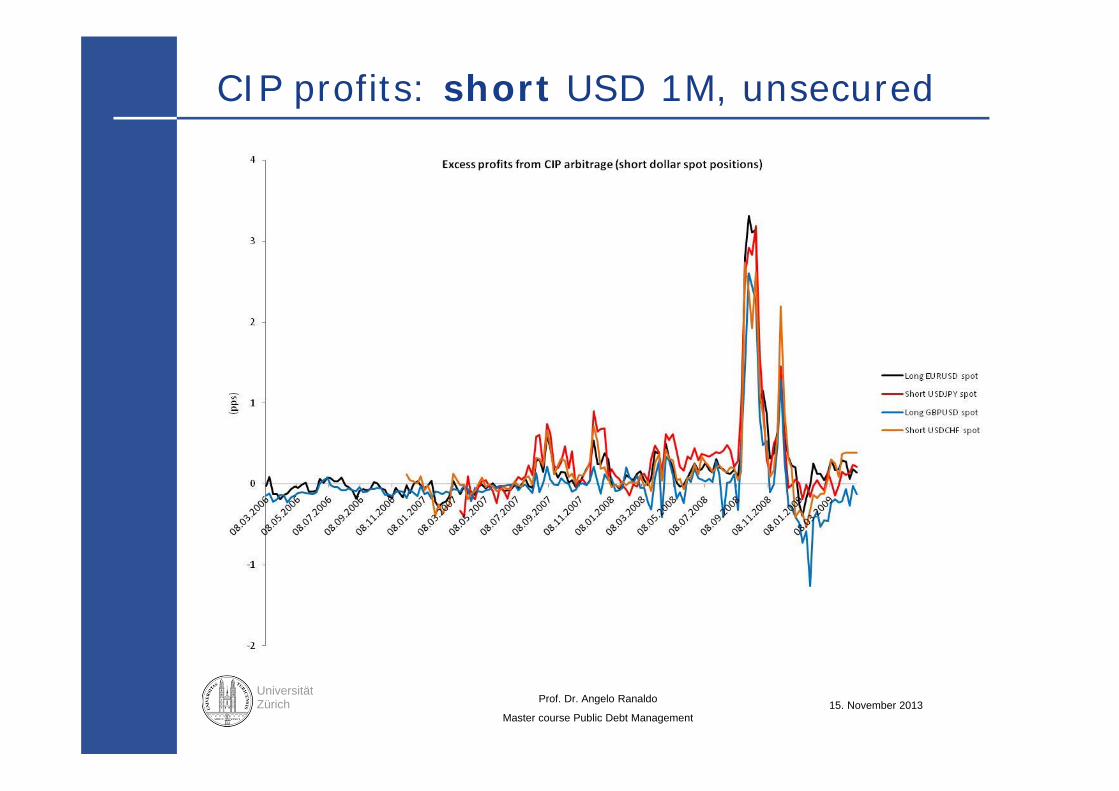

CIP profits: short USD 1M, unsecured

Universität Zürich Prof. Dr. Angelo Ranaldo

Master course Public Debt Management15. November 2013

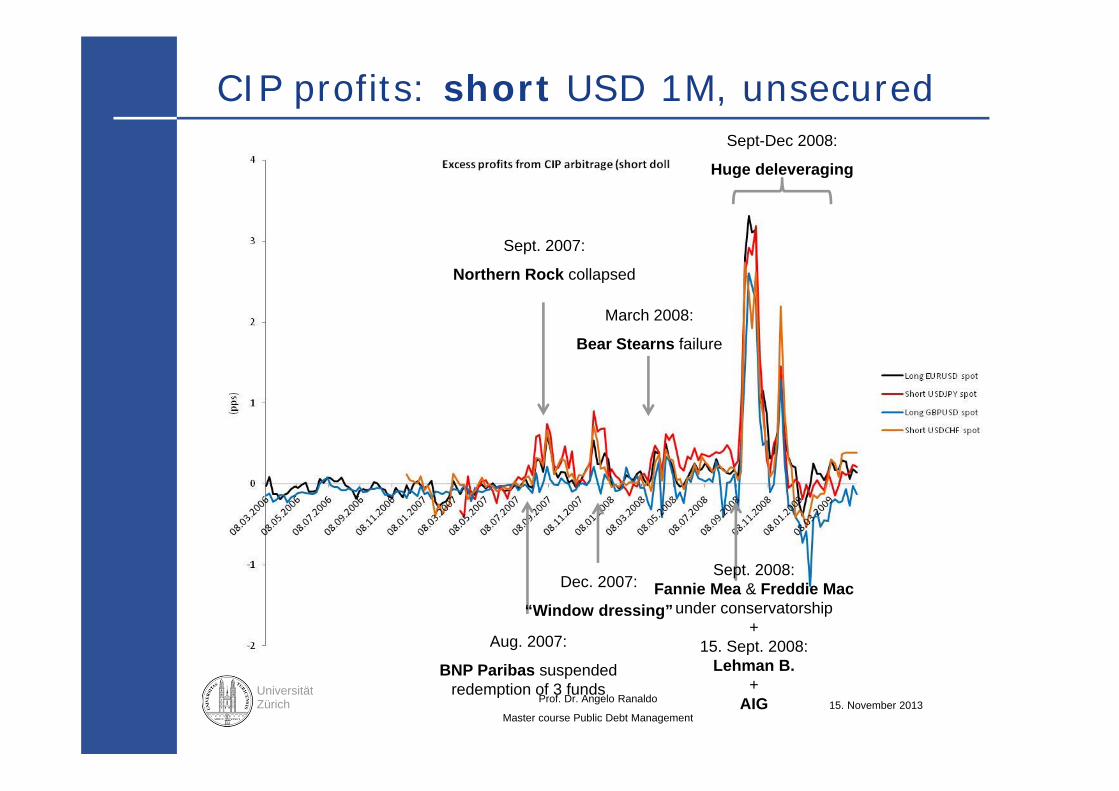

CIP profits: short USD 1M, unsecured

Aug. 2007:

BNP Paribas suspended redemption of 3 funds

Sept. 2007:

Northern Rock collapsed

Dec. 2007:

“Window dressing”

March 2008:

Bear Stearns failure

Sept. 2008: Fannie Mea & Freddie Mac

under conservatorship+

15. Sept. 2008:Lehman B.

+AIG

Sept-Dec 2008:

Huge deleveraging

Universität Zürich Prof. Dr. Angelo Ranaldo

Master course Public Debt Management15. November 2013

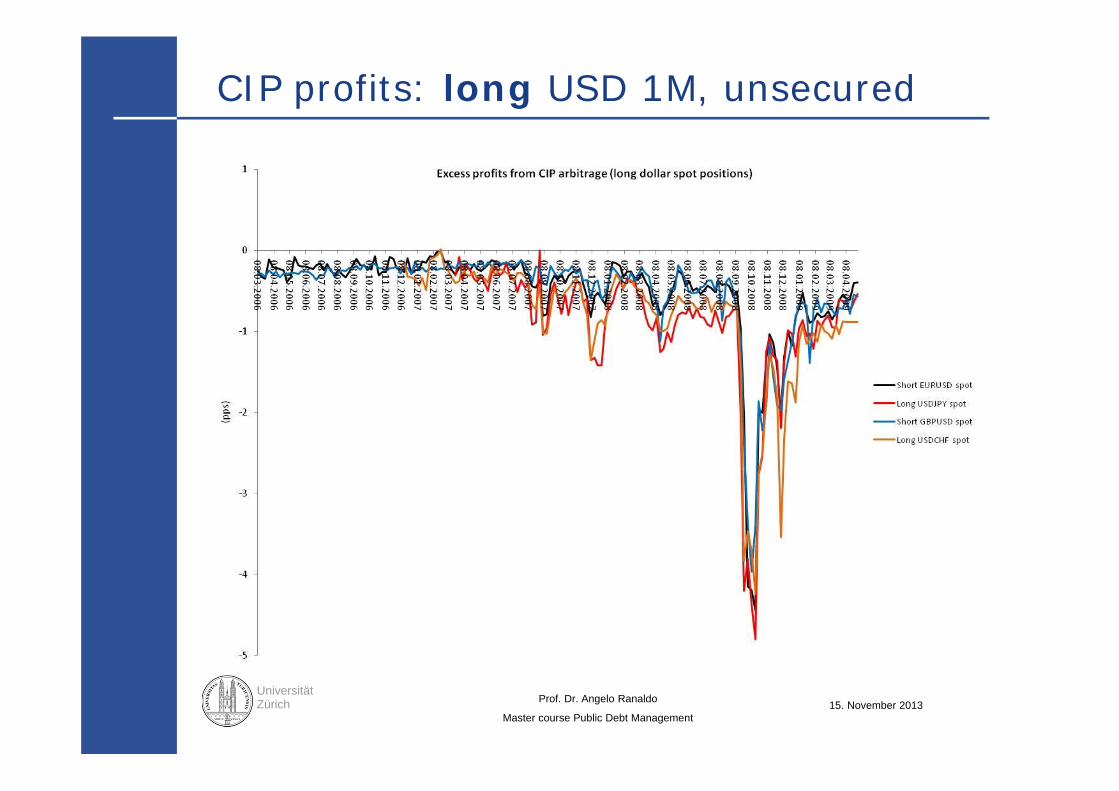

CIP profits: long USD 1M, unsecured

Universität Zürich Prof. Dr. Angelo Ranaldo

Master course Public Debt Management15. November 2013

12

Well-functioning market

Are financial assets liquid?

Not always! And cross-sectional differences.

Let us take what is supposed to be the most liquid market worldwide

Universität Zürich Prof. Dr. Angelo Ranaldo

Master course Public Debt Management15. November 2013

Measuring liquidity

Mancini, L., A. Ranaldo, J. Wrampelmeyer (2013): “Liquidity in the Foreign Exchange Market: Measurement, Commonality, and Risk Premiums”, Journal of Finance 68(5), 1805–1841.

Data— ICAP’s Electronic Broking Services (EBS): major leading platform

for spot FX interdealer trading.— Sample: 1/1/2007 – 31/12/2009 on a one-second basis.— Transaction price and volume; bid and ask quotes; precise trade

direction.— Measures:

– Price Impact, Return Reversal, Bid-Ask Spread, Effective Cost, Volatility.

— AUD/USD, EUR/CHF, EUR/GBP, EUR/JPY, EUR/USD, GBP/USD, NZD/USD, USD/CAD, USD/CHF, USD/DKK, USD/JPY and USD/SEK.

13

Universität Zürich Prof. Dr. Angelo Ranaldo

Master course Public Debt Management15. November 2013

14

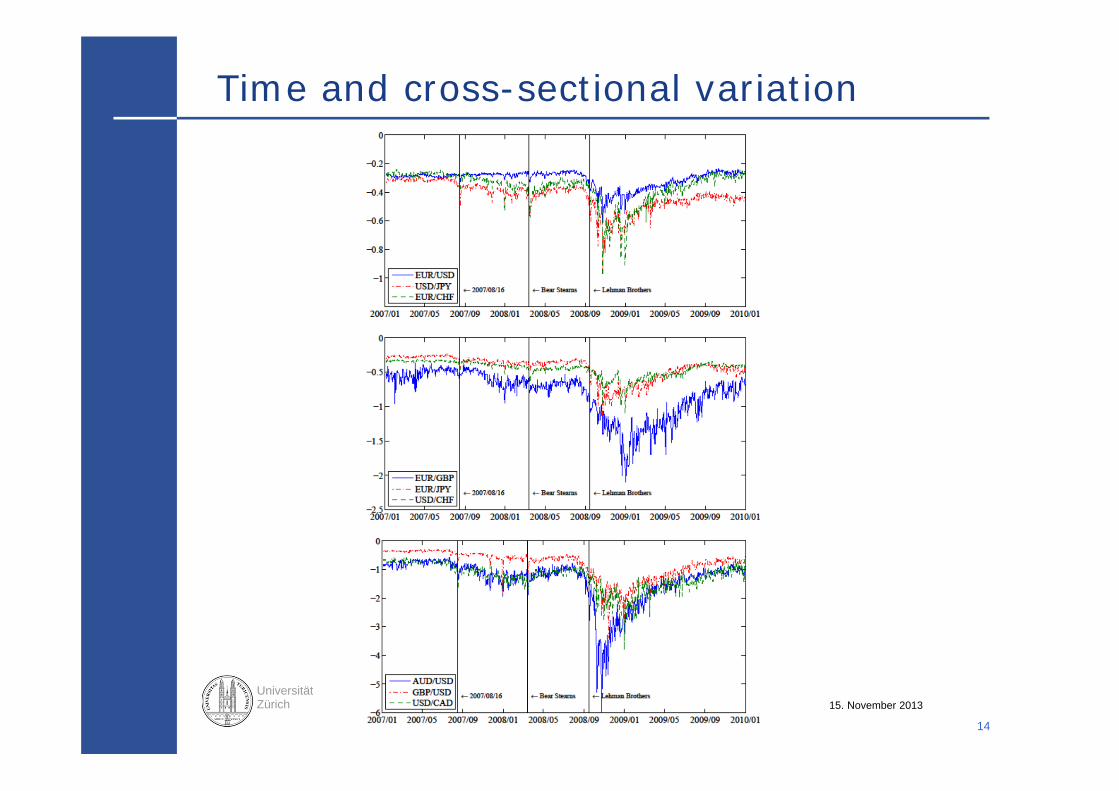

Time and cross-sectional variation

Universität Zürich Prof. Dr. Angelo Ranaldo

Master course Public Debt Management15. November 2013

15

Issuance and trading

How are securities issued?

How are securities traded?

Why are (bond) indices important?

Universität Zürich Prof. Dr. Angelo Ranaldo

Master course Public Debt Management15. November 2013

16

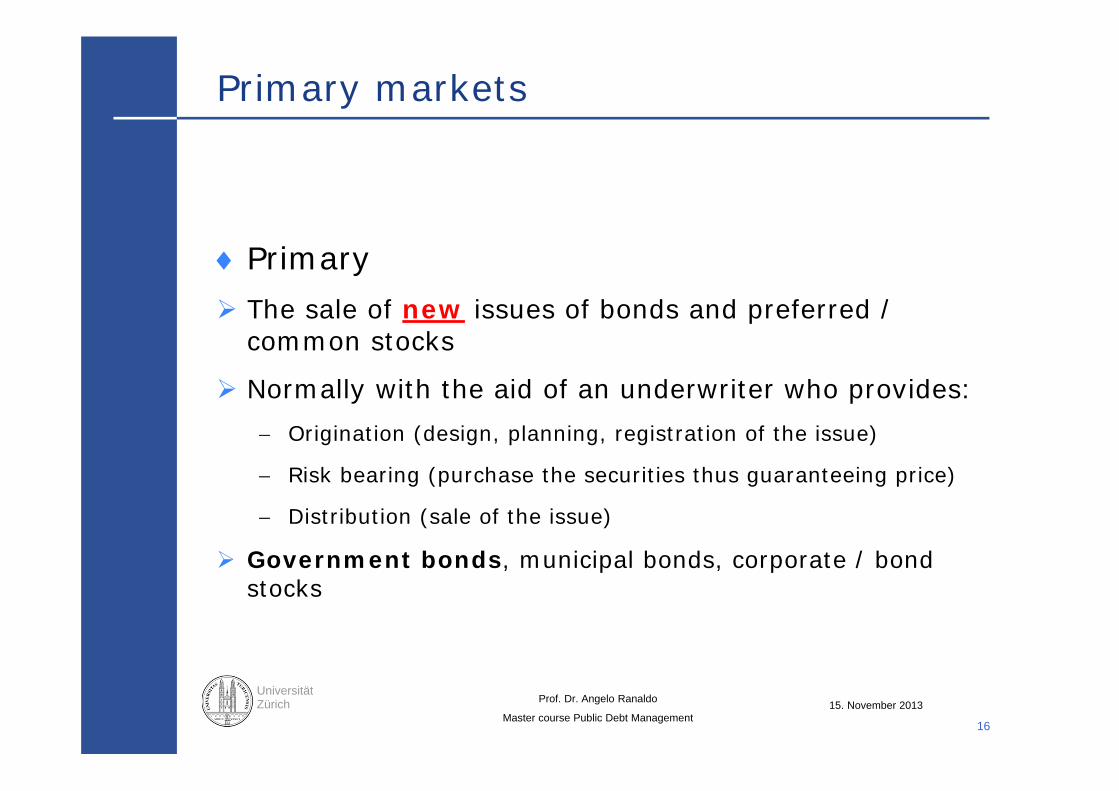

Primary markets

Primary The sale of new issues of bonds and preferred /

common stocks

Normally with the aid of an underwriter who provides: Origination (design, planning, registration of the issue)

Risk bearing (purchase the securities thus guaranteeing price)

Distribution (sale of the issue)

Government bonds, municipal bonds, corporate / bond stocks

Universität Zürich Prof. Dr. Angelo Ranaldo

Master course Public Debt Management15. November 2013

17

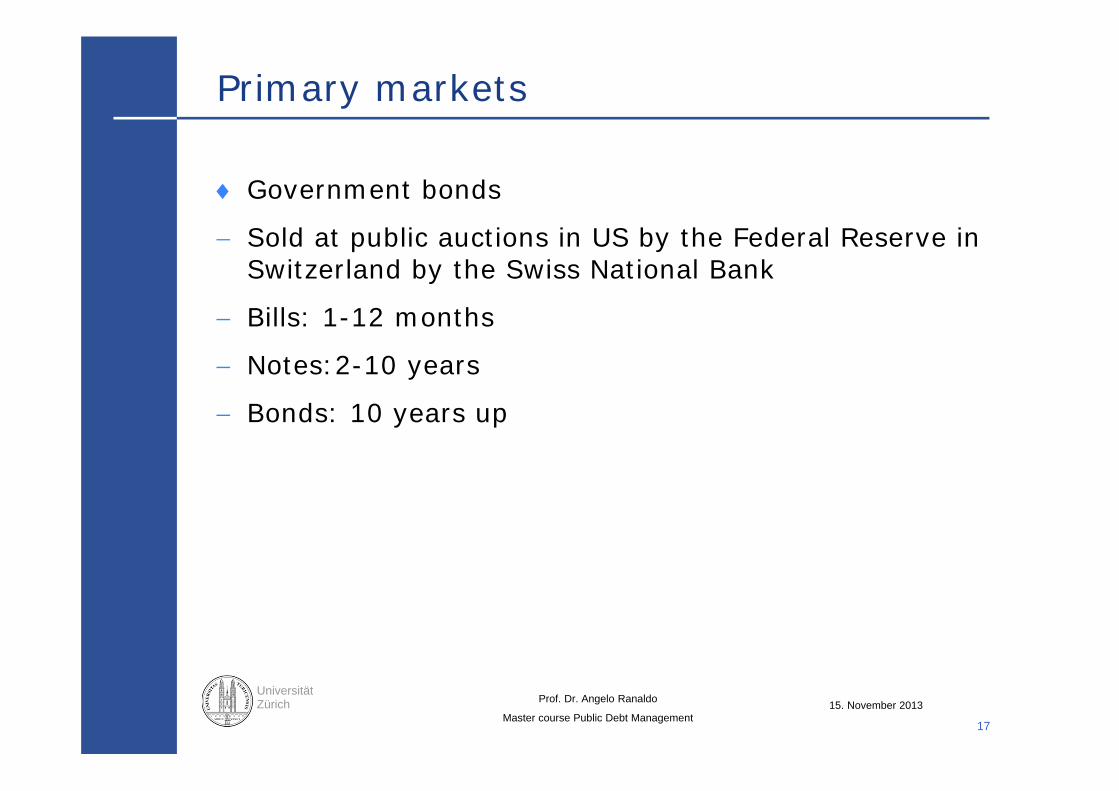

Primary markets

Government bonds

Sold at public auctions in US by the Federal Reserve in Switzerland by the Swiss National Bank

Bills: 1-12 months

Notes:2-10 years

Bonds: 10 years up

Universität Zürich Prof. Dr. Angelo Ranaldo

Master course Public Debt Management15. November 2013

18

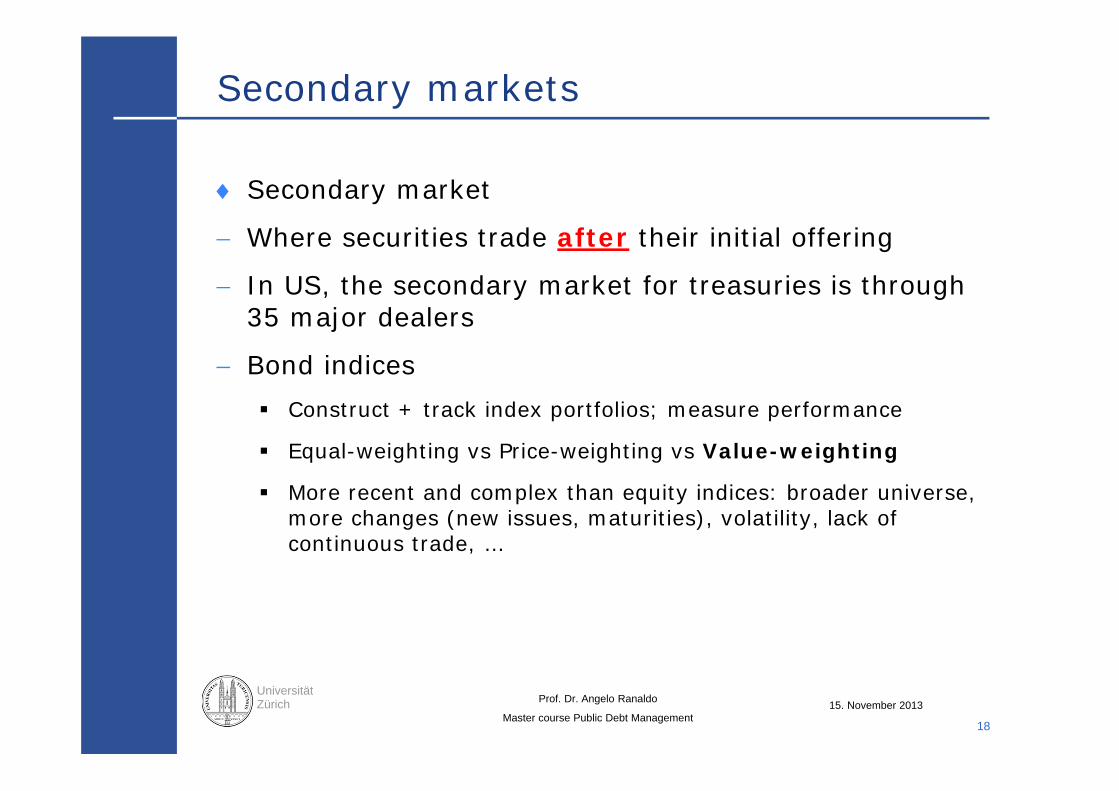

Secondary markets

Secondary market

Where securities trade after their initial offering

In US, the secondary market for treasuries is through 35 major dealers

Bond indices Construct + track index portfolios; measure performance

Equal-weighting vs Price-weighting vs Value-weighting

More recent and complex than equity indices: broader universe, more changes (new issues, maturities), volatility, lack of continuous trade, …

Universität Zürich Prof. Dr. Angelo Ranaldo

Master course Public Debt Management15. November 2013

19

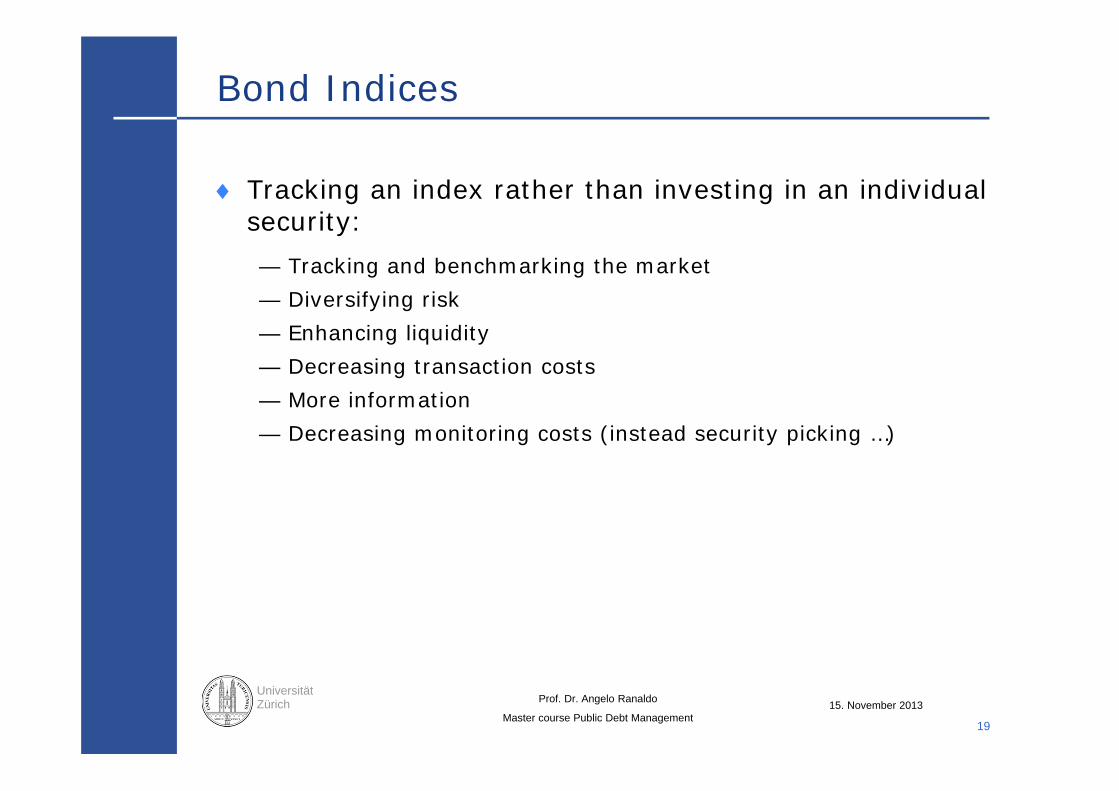

Bond Indices

Tracking an index rather than investing in an individual security:— Tracking and benchmarking the market— Diversifying risk— Enhancing liquidity— Decreasing transaction costs— More information— Decreasing monitoring costs (instead security picking …)

Universität Zürich Prof. Dr. Angelo Ranaldo

Master course Public Debt Management15. November 2013

20

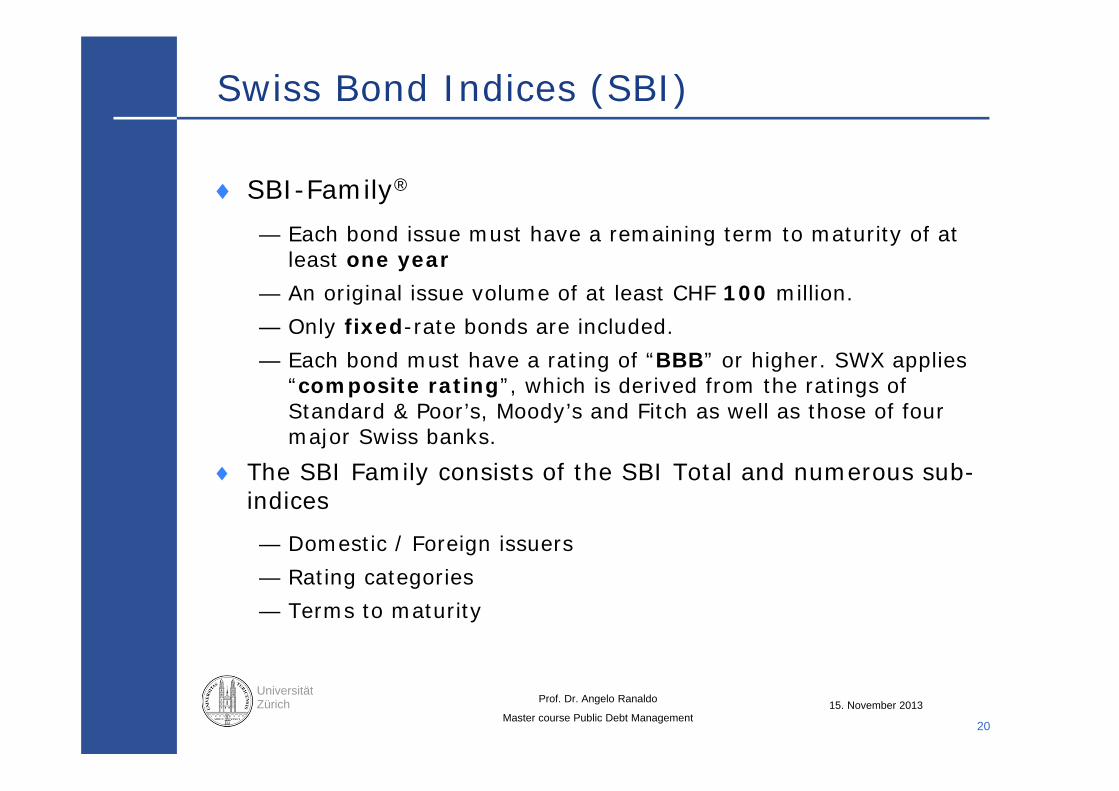

Swiss Bond Indices (SBI)

SBI-Family®

— Each bond issue must have a remaining term to maturity of at least one year

— An original issue volume of at least CHF 100 million. — Only fixed-rate bonds are included. — Each bond must have a rating of “BBB” or higher. SWX applies

“composite rating”, which is derived from the ratings of Standard & Poor’s, Moody’s and Fitch as well as those of four major Swiss banks.

The SBI Family consists of the SBI Total and numerous sub-indices

— Domestic / Foreign issuers— Rating categories— Terms to maturity

Universität Zürich Prof. Dr. Angelo Ranaldo

Master course Public Debt Management15. November 2013

21

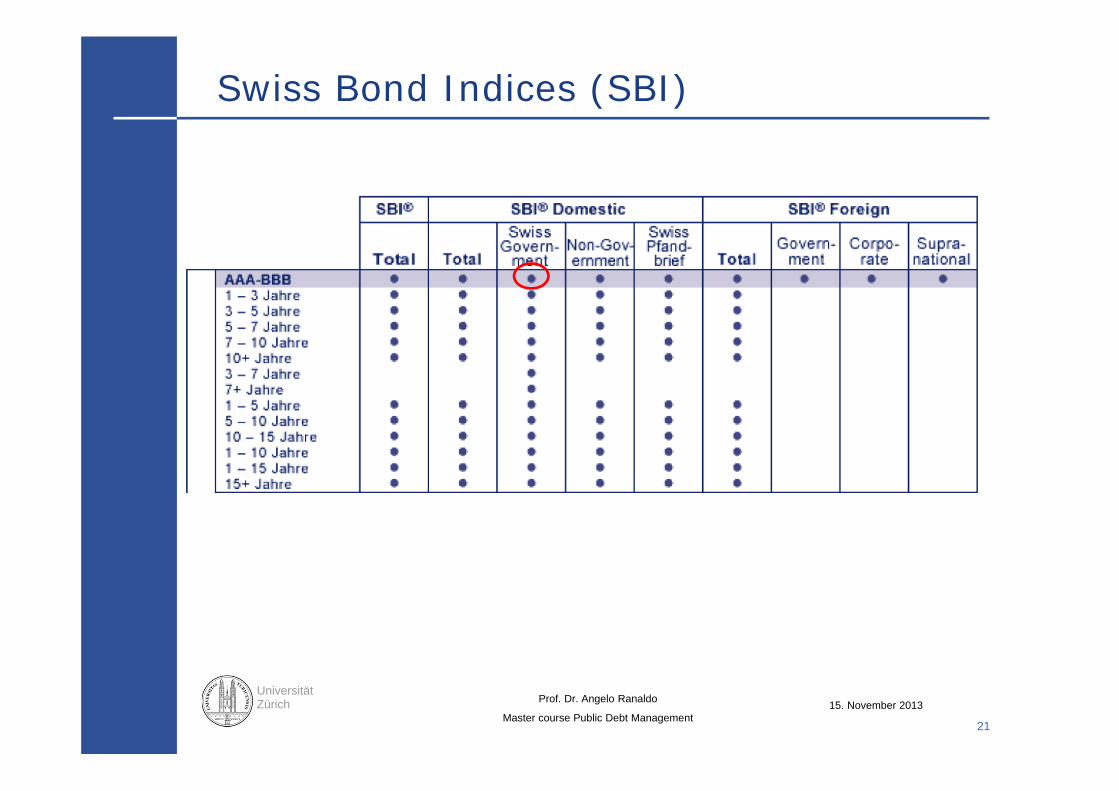

Swiss Bond Indices (SBI)

Universität Zürich Prof. Dr. Angelo Ranaldo

Master course Public Debt Management15. November 2013

22

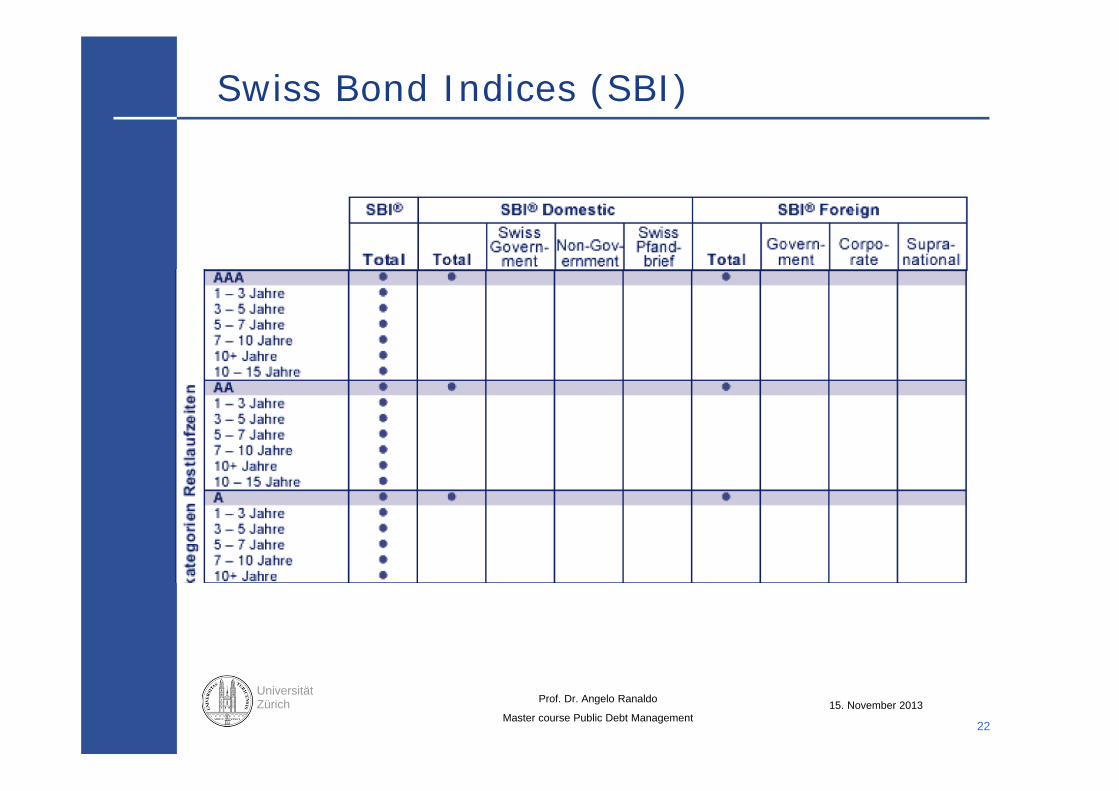

Swiss Bond Indices (SBI)

Universität Zürich Prof. Dr. Angelo Ranaldo

Master course Public Debt Management15. November 2013

23

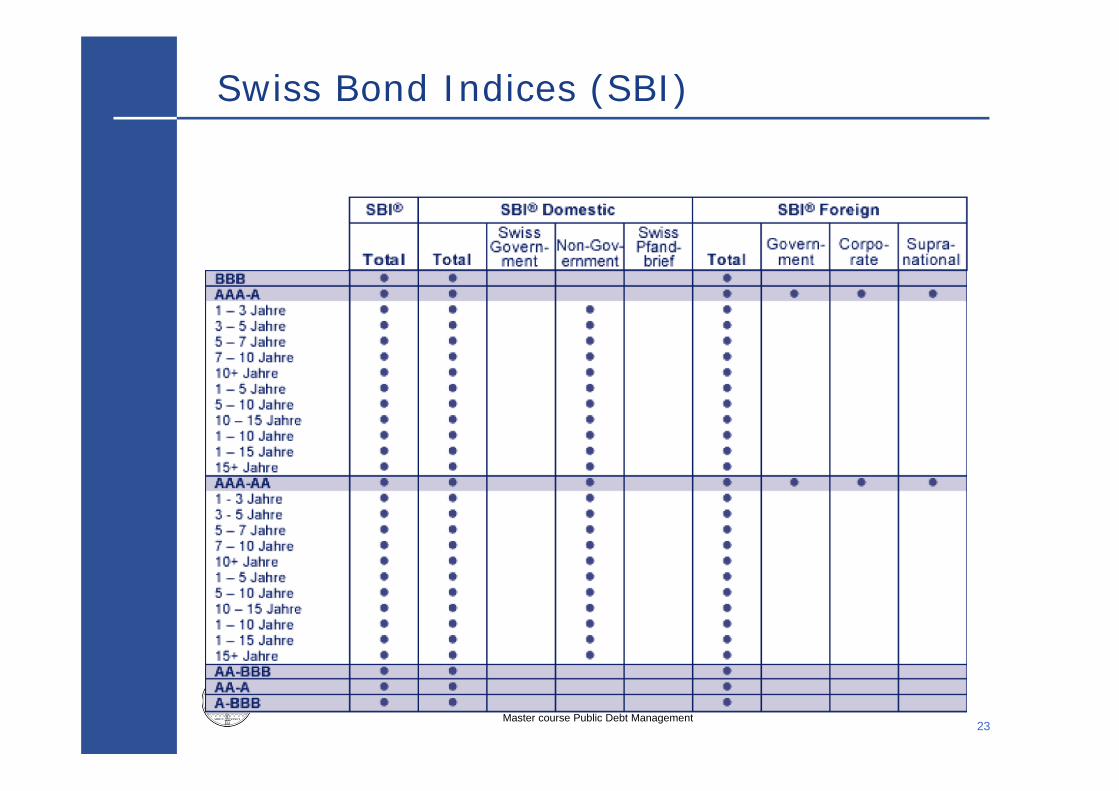

Swiss Bond Indices (SBI)

Universität Zürich Prof. Dr. Angelo Ranaldo

Master course Public Debt Management15. November 2013

24

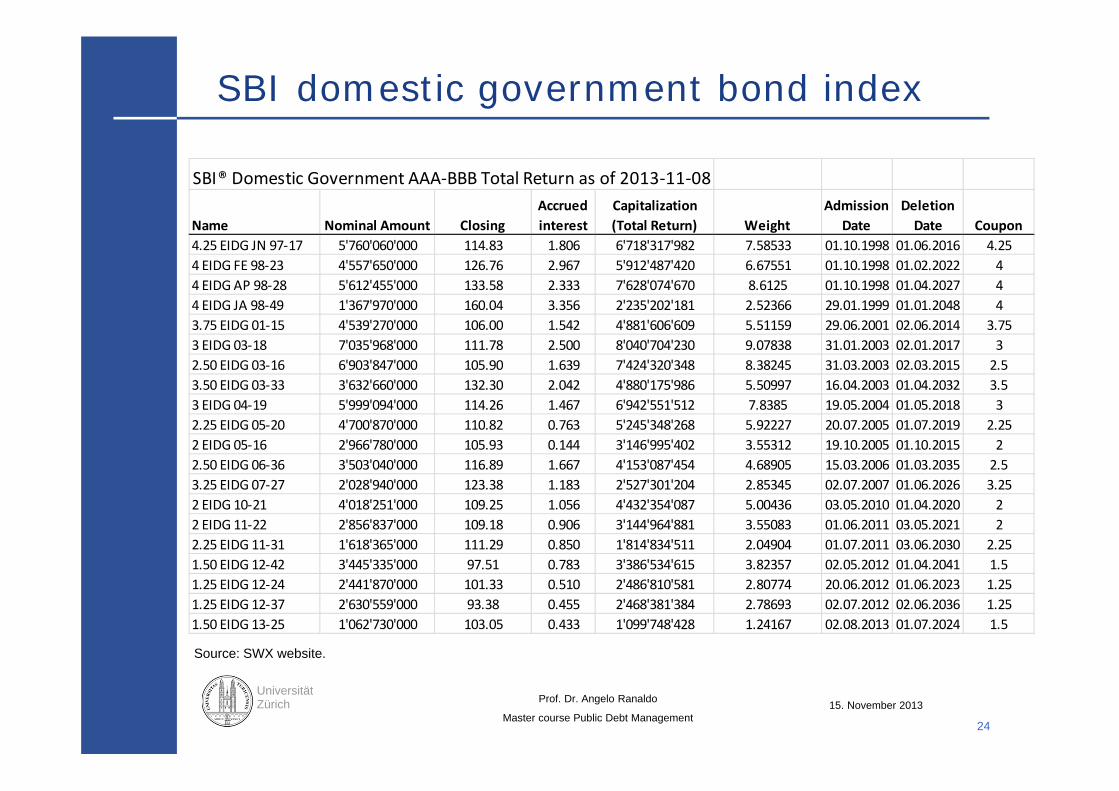

SBI domestic government bond index

SBI® Domestic Government AAA‐BBB Total Return as of 2013‐11‐08

Name Nominal Amount ClosingAccrued interest

Capitalization (Total Return) Weight

Admission Date

Deletion Date Coupon

4.25 EIDG JN 97‐17 5'760'060'000 114.83 1.806 6'718'317'982 7.58533 01.10.1998 01.06.2016 4.254 EIDG FE 98‐23 4'557'650'000 126.76 2.967 5'912'487'420 6.67551 01.10.1998 01.02.2022 44 EIDG AP 98‐28 5'612'455'000 133.58 2.333 7'628'074'670 8.6125 01.10.1998 01.04.2027 44 EIDG JA 98‐49 1'367'970'000 160.04 3.356 2'235'202'181 2.52366 29.01.1999 01.01.2048 43.75 EIDG 01‐15 4'539'270'000 106.00 1.542 4'881'606'609 5.51159 29.06.2001 02.06.2014 3.753 EIDG 03‐18 7'035'968'000 111.78 2.500 8'040'704'230 9.07838 31.01.2003 02.01.2017 32.50 EIDG 03‐16 6'903'847'000 105.90 1.639 7'424'320'348 8.38245 31.03.2003 02.03.2015 2.53.50 EIDG 03‐33 3'632'660'000 132.30 2.042 4'880'175'986 5.50997 16.04.2003 01.04.2032 3.53 EIDG 04‐19 5'999'094'000 114.26 1.467 6'942'551'512 7.8385 19.05.2004 01.05.2018 32.25 EIDG 05‐20 4'700'870'000 110.82 0.763 5'245'348'268 5.92227 20.07.2005 01.07.2019 2.252 EIDG 05‐16 2'966'780'000 105.93 0.144 3'146'995'402 3.55312 19.10.2005 01.10.2015 22.50 EIDG 06‐36 3'503'040'000 116.89 1.667 4'153'087'454 4.68905 15.03.2006 01.03.2035 2.53.25 EIDG 07‐27 2'028'940'000 123.38 1.183 2'527'301'204 2.85345 02.07.2007 01.06.2026 3.252 EIDG 10‐21 4'018'251'000 109.25 1.056 4'432'354'087 5.00436 03.05.2010 01.04.2020 22 EIDG 11‐22 2'856'837'000 109.18 0.906 3'144'964'881 3.55083 01.06.2011 03.05.2021 22.25 EIDG 11‐31 1'618'365'000 111.29 0.850 1'814'834'511 2.04904 01.07.2011 03.06.2030 2.251.50 EIDG 12‐42 3'445'335'000 97.51 0.783 3'386'534'615 3.82357 02.05.2012 01.04.2041 1.51.25 EIDG 12‐24 2'441'870'000 101.33 0.510 2'486'810'581 2.80774 20.06.2012 01.06.2023 1.251.25 EIDG 12‐37 2'630'559'000 93.38 0.455 2'468'381'384 2.78693 02.07.2012 02.06.2036 1.251.50 EIDG 13‐25 1'062'730'000 103.05 0.433 1'099'748'428 1.24167 02.08.2013 01.07.2024 1.5

Source: SWX website.

Universität Zürich Prof. Dr. Angelo Ranaldo

Master course Public Debt Management15. November 2013

25

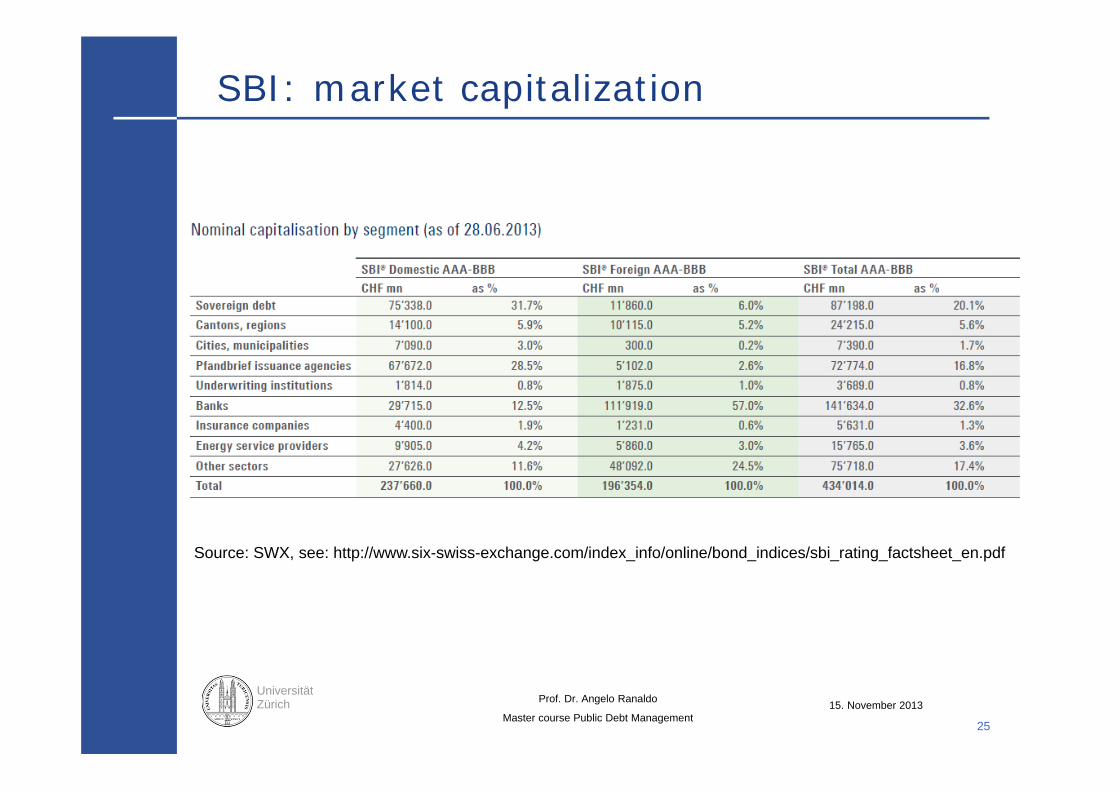

SBI: market capitalization

Source: SWX, see: http://www.six-swiss-exchange.com/index_info/online/bond_indices/sbi_rating_factsheet_en.pdf

Universität Zürich Prof. Dr. Angelo Ranaldo

Master course Public Debt Management15. November 2013

26

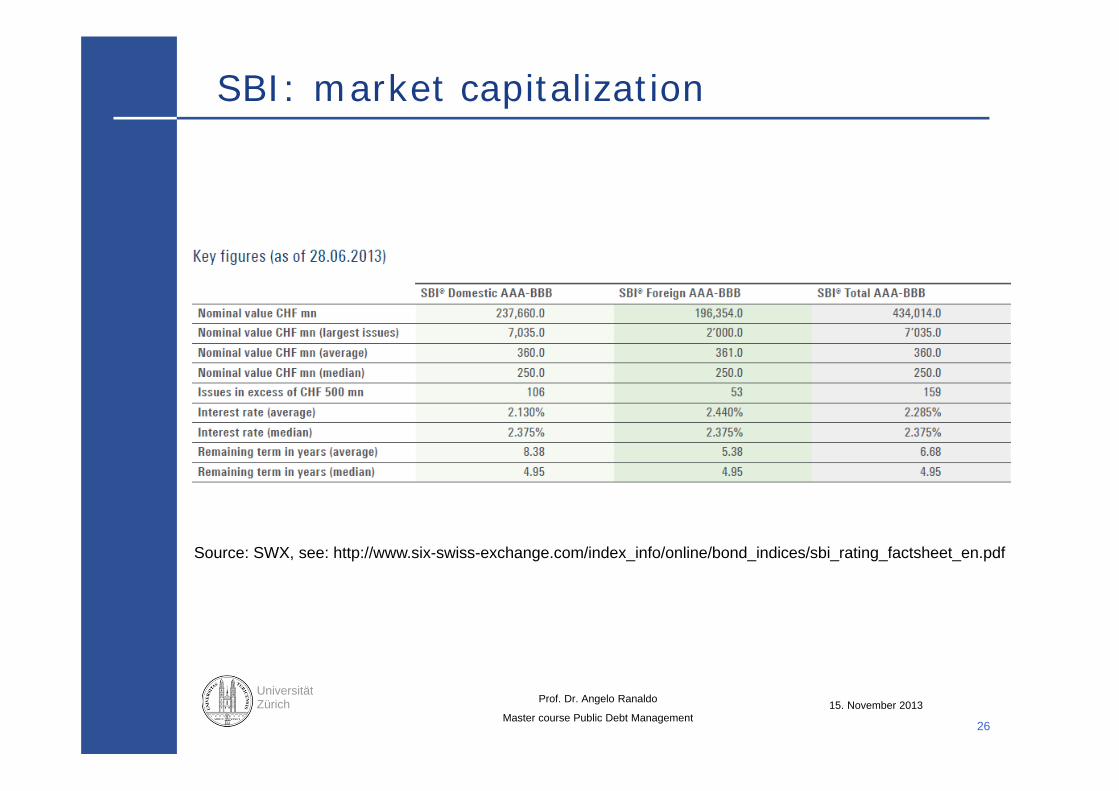

SBI: market capitalization

Source: SWX, see: http://www.six-swiss-exchange.com/index_info/online/bond_indices/sbi_rating_factsheet_en.pdf

Universität Zürich Prof. Dr. Angelo Ranaldo

Master course Public Debt Management15. November 2013

27

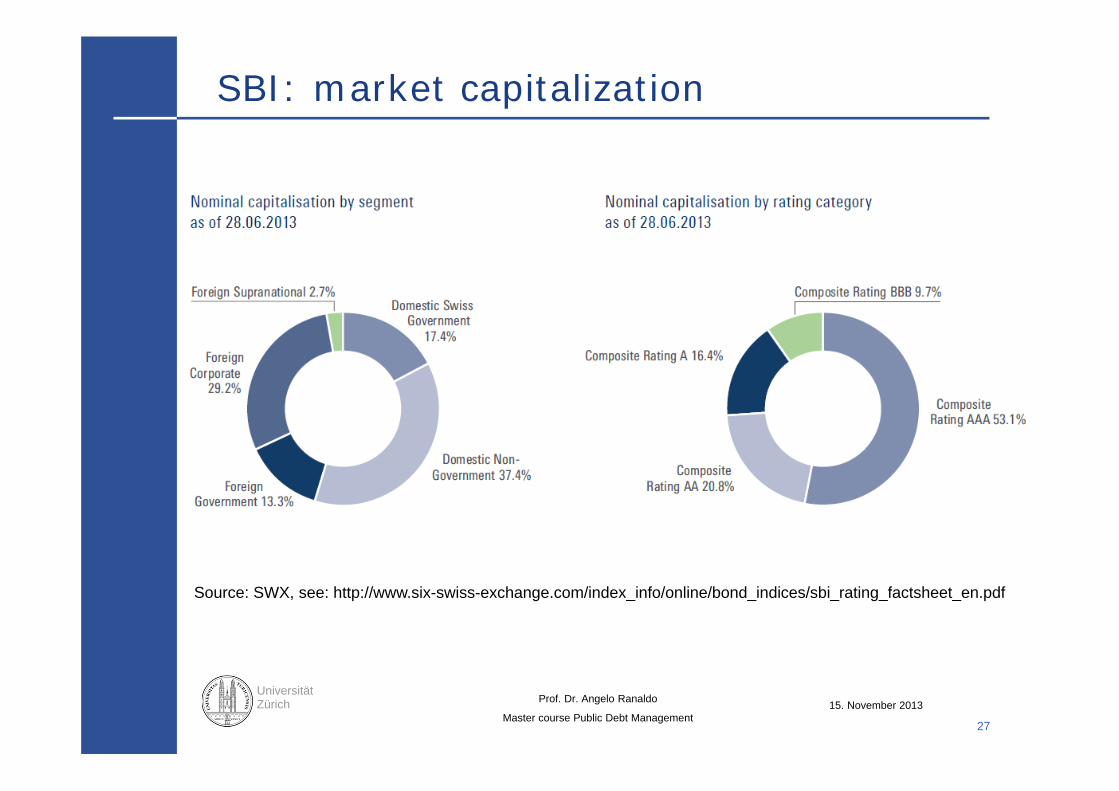

SBI: market capitalization

Source: SWX, see: http://www.six-swiss-exchange.com/index_info/online/bond_indices/sbi_rating_factsheet_en.pdf

Universität Zürich Prof. Dr. Angelo Ranaldo

Master course Public Debt Management15. November 2013

28

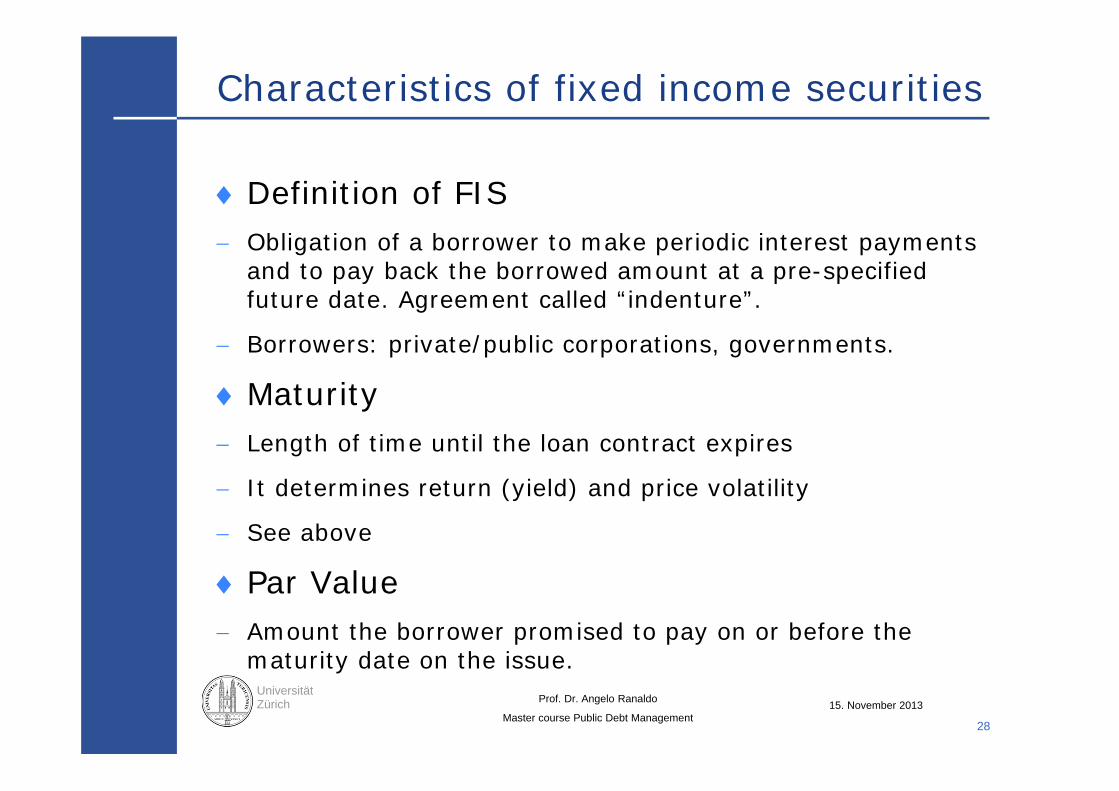

Characteristics of fixed income securities

Definition of FIS Obligation of a borrower to make periodic interest payments

and to pay back the borrowed amount at a pre-specified future date. Agreement called “indenture”.

Borrowers: private/public corporations, governments.

Maturity Length of time until the loan contract expires

It determines return (yield) and price volatility

See above

Par Value Amount the borrower promised to pay on or before the

maturity date on the issue.

Universität Zürich Prof. Dr. Angelo Ranaldo

Master course Public Debt Management15. November 2013

29

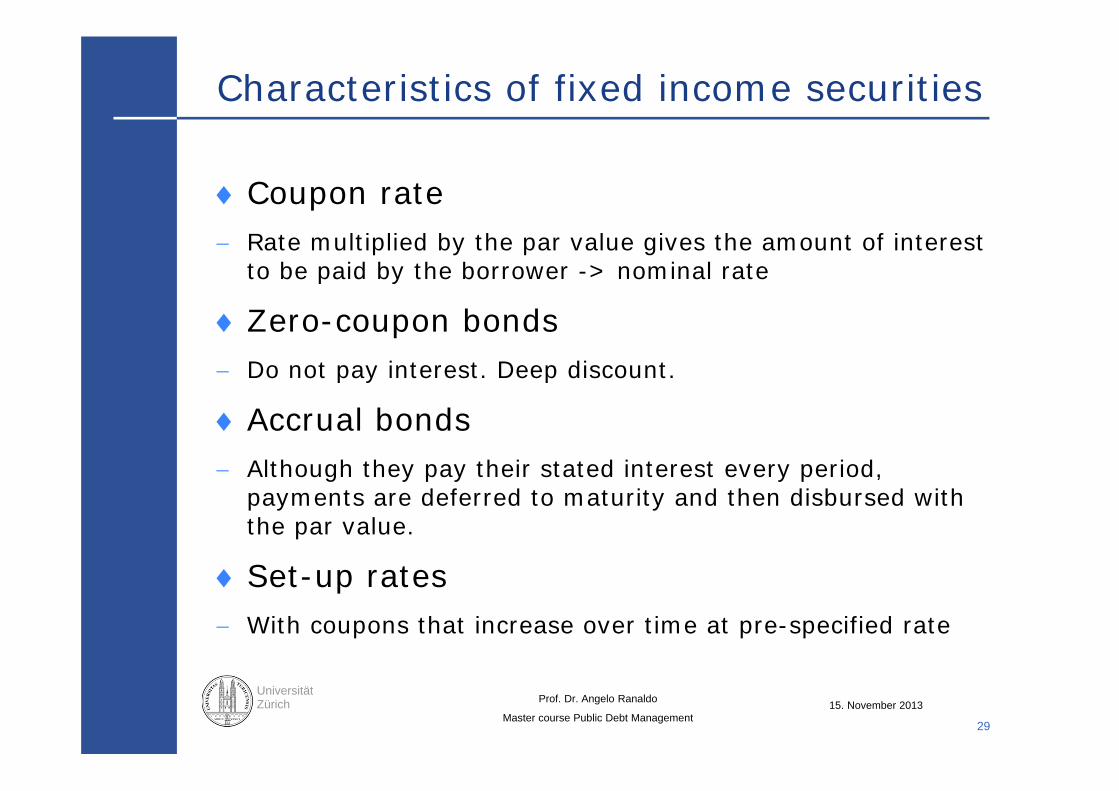

Characteristics of fixed income securities

Coupon rate Rate multiplied by the par value gives the amount of interest

to be paid by the borrower -> nominal rate

Zero-coupon bonds Do not pay interest. Deep discount.

Accrual bonds Although they pay their stated interest every period,

payments are deferred to maturity and then disbursed with the par value.

Set-up rates With coupons that increase over time at pre-specified rate

Universität Zürich Prof. Dr. Angelo Ranaldo

Master course Public Debt Management15. November 2013

30

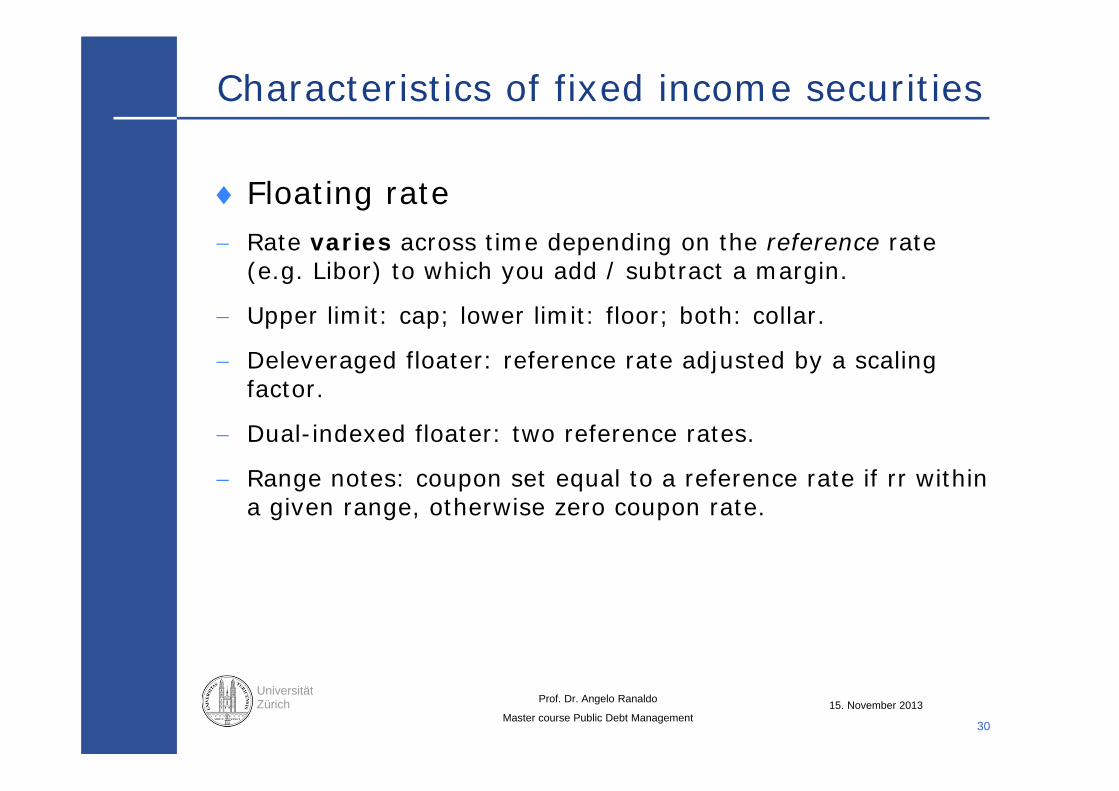

Characteristics of fixed income securities

Floating rate Rate varies across time depending on the reference rate

(e.g. Libor) to which you add / subtract a margin.

Upper limit: cap; lower limit: floor; both: collar.

Deleveraged floater: reference rate adjusted by a scaling factor.

Dual-indexed floater: two reference rates.

Range notes: coupon set equal to a reference rate if rr within a given range, otherwise zero coupon rate.

Universität Zürich Prof. Dr. Angelo Ranaldo

Master course Public Debt Management15. November 2013

31

Characteristics of fixed income securities

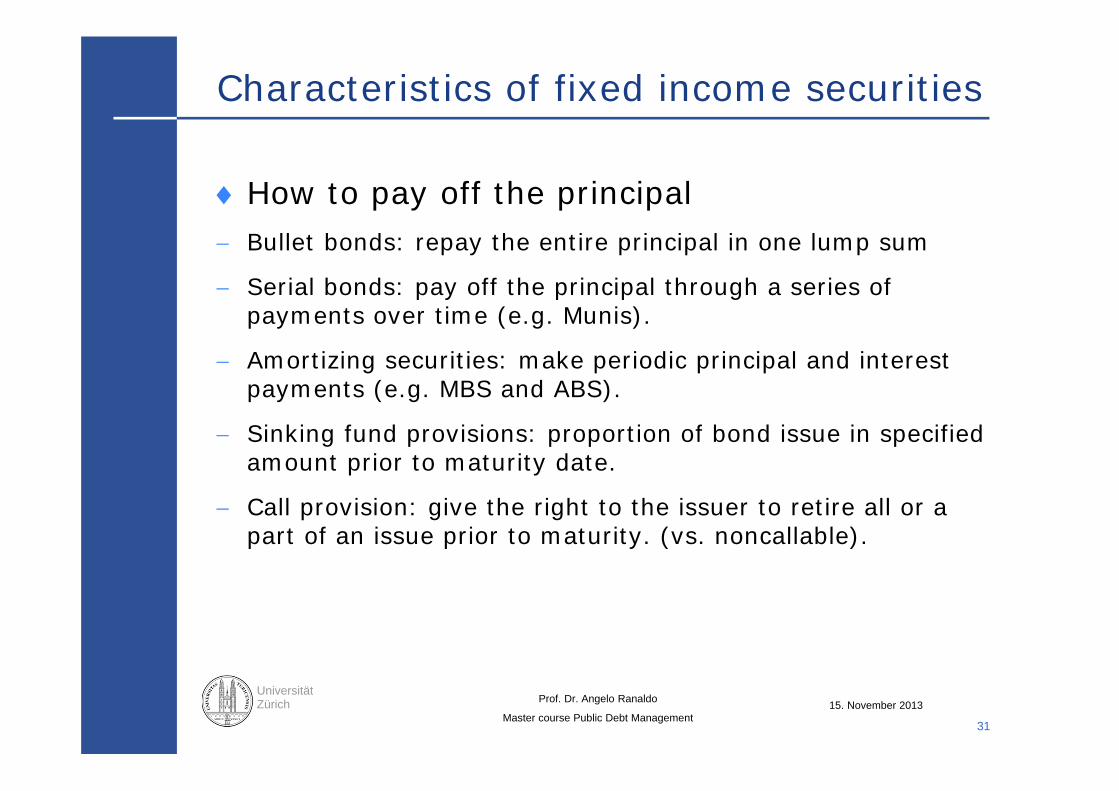

How to pay off the principal Bullet bonds: repay the entire principal in one lump sum

Serial bonds: pay off the principal through a series of payments over time (e.g. Munis).

Amortizing securities: make periodic principal and interest payments (e.g. MBS and ABS).

Sinking fund provisions: proportion of bond issue in specified amount prior to maturity date.

Call provision: give the right to the issuer to retire all or a part of an issue prior to maturity. (vs. noncallable).

Universität Zürich Prof. Dr. Angelo Ranaldo

Master course Public Debt Management15. November 2013

32

Characteristics of fixed income securities

Currency denomination The issuer can make payments to bondholders in any

currency.

Dual-currency bond: interest payments in one currency and principal in another one

Financing the purchase of bonds Margin buying: borrowing funds from brokers or banks to

purchase securities.

Repurchase (repo) agreement: arrangement by which an institution sells a security with a commitment to buy it back at later date, at a pre-established price.

Universität Zürich Prof. Dr. Angelo Ranaldo

Master course Public Debt Management15. November 2013

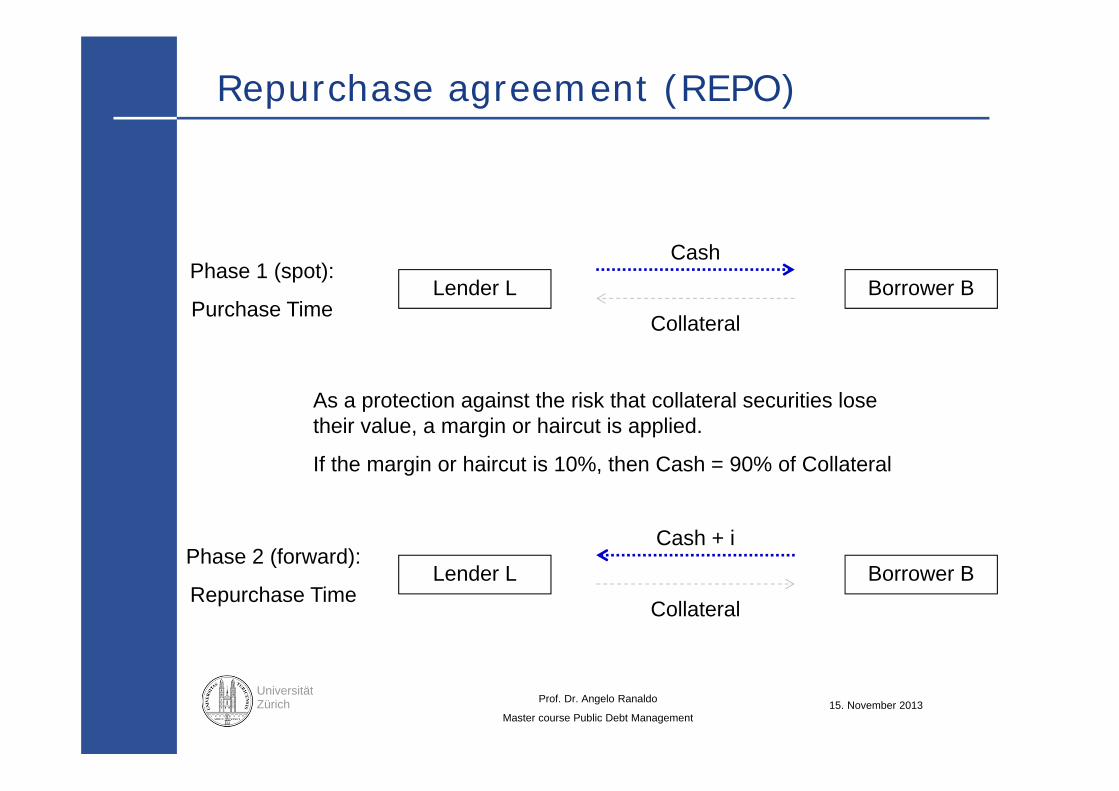

Repurchase agreement (REPO)

Lender L Borrower B

Cash

Collateral

Phase 1 (spot):

Purchase Time

Lender L Borrower B

Cash + i

Collateral

Phase 2 (forward):

Repurchase Time

As a protection against the risk that collateral securities lose their value, a margin or haircut is applied.

If the margin or haircut is 10%, then Cash = 90% of Collateral

Universität Zürich Prof. Dr. Angelo Ranaldo

Master course Public Debt Management15. November 2013

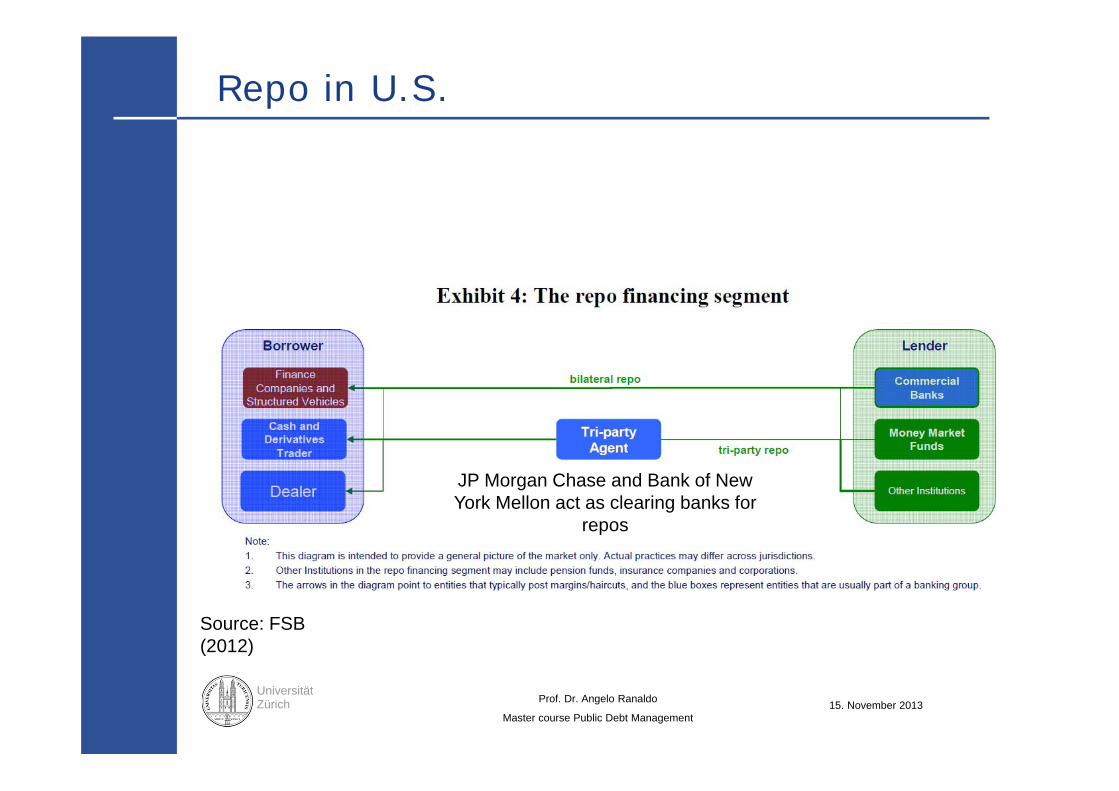

Repo in U.S.

Source: FSB (2012)

JP Morgan Chase and Bank of New York Mellon act as clearing banks for

repos