Embed Size (px)

Citation preview

Chartered Institute of Purchasing and Supply –Your liberty could be at stake! - Compliance and trade controls you need to be aware of

Ross Denton, PartnerJennifer Revis, Senior Associate

Thursday 16 May 2013

2

What is trade compliance?– Traditional “customs” issues

– classification of goods– valuation of goods– origin of goods– procedures

– Export controls– export of certain sensitive goods and technologies– export of certain goods with problematic end uses

– Trade sanctions– dealing with “bad” third parties– dealing with “bad” countries

– Supply chain security– how do we know what we are shipping?

– Dealing with third parties– are they creating issues for us? E.g. paying bribes or mis-declaring goods?

– All these issues will occur on cross-border trade, but can also occur on trade within the EU

3

Why do we care about trade compliance?– Prison sentences for individuals

– e.g. up to 10 years in UK, and 20 years in US– Extradition (e.g. Tappin)– Significant fines for companies (e.g. $619 fine on ING for Iran

payments )– Denial of export privileges (e.g. licences withdrawn or not

renewed)– Forfeiture of goods– Debarment from government contracting– Listing in the US as a restricted party (e.g. for association with

terrorist or WMD proliferator) – Reputational harm and CSR concerns (e.g banks and Iran)– Management time\legal expenses– Enforcement is on the rise!

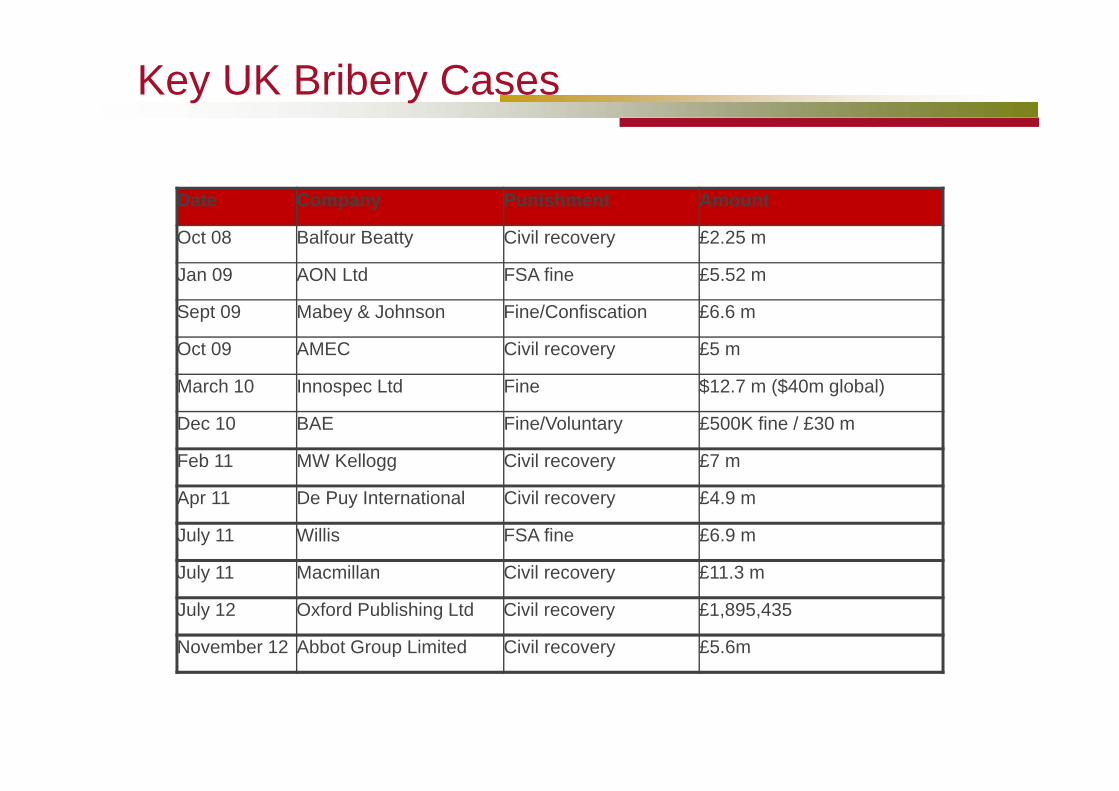

Date Company Punishment Amount

Oct 08 Balfour Beatty Civil recovery £2.25 m

Jan 09 AON Ltd FSA fine £5.52 m

Sept 09 Mabey & Johnson Fine/Confiscation £6.6 m

Oct 09 AMEC Civil recovery £5 m

March 10 Innospec Ltd Fine $12.7 m ($40m global)

Dec 10 BAE Fine/Voluntary £500K fine / £30 m

Feb 11 MW Kellogg Civil recovery £7 m

Apr 11 De Puy International Civil recovery £4.9 m

July 11 Willis FSA fine £6.9 m

July 11 Macmillan Civil recovery £11.3 m

July 12 Oxford Publishing Ltd Civil recovery £1,895,435

November 12 Abbot Group Limited Civil recovery £5.6m

Key UK Bribery Cases

5

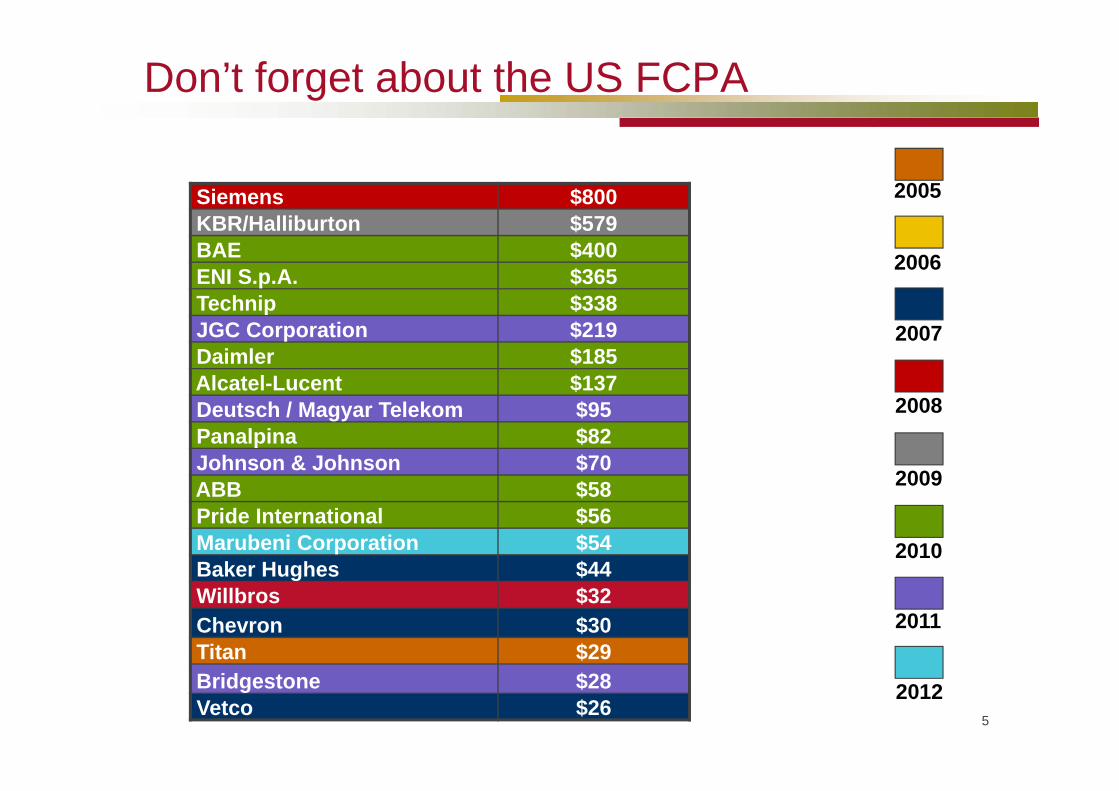

Don’t forget about the US FCPA

Siemens $800KBR/Halliburton $579BAE $400ENI S.p.A. $365Technip $338JGC Corporation $219Daimler $185Alcatel-Lucent $137Deutsch / Magyar Telekom $95Panalpina $82Johnson & Johnson $70ABB $58Pride International $56Marubeni Corporation $54Baker Hughes $44Willbros $32Chevron $30Titan $29Bridgestone $28Vetco $26

2007

2008

2009

2010

2006

2005

2011

2012

© 2012 Baker & McKenzie 6

Agenda

–Identifying key compliance and trade controls risks in the supply chain

–How to manage these risks–Top tips

© 2012 Baker & McKenzie 7

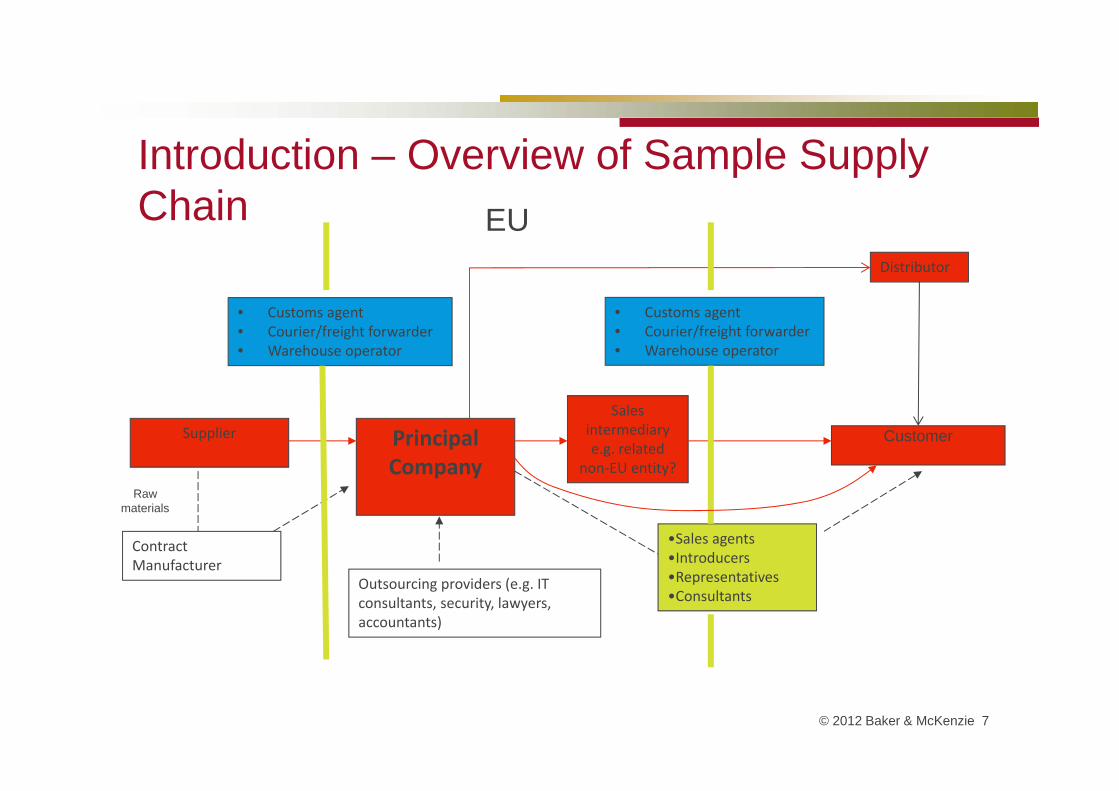

Contract Manufacturer

Introduction – Overview of Sample Supply Chain

• Customs agent• Courier/freight forwarder• Warehouse operator

Distributor

Principal Company

•Sales agents•Introducers •Representatives•Consultants

Outsourcing providers (e.g. IT consultants, security, lawyers, accountants)

Sales intermediary e.g. related

non‐EU entity?

CustomerSupplier

• Customs agent• Courier/freight forwarder• Warehouse operator

Raw materials

EU

Introduction - Key Considerations

– Identify key risk areas– or what are you doing and who are you dealing with?

– Where does the liability lie?– How do you manage third party risk?

© 2012 Baker & McKenzie 8

© 2012 Baker & McKenzie 9

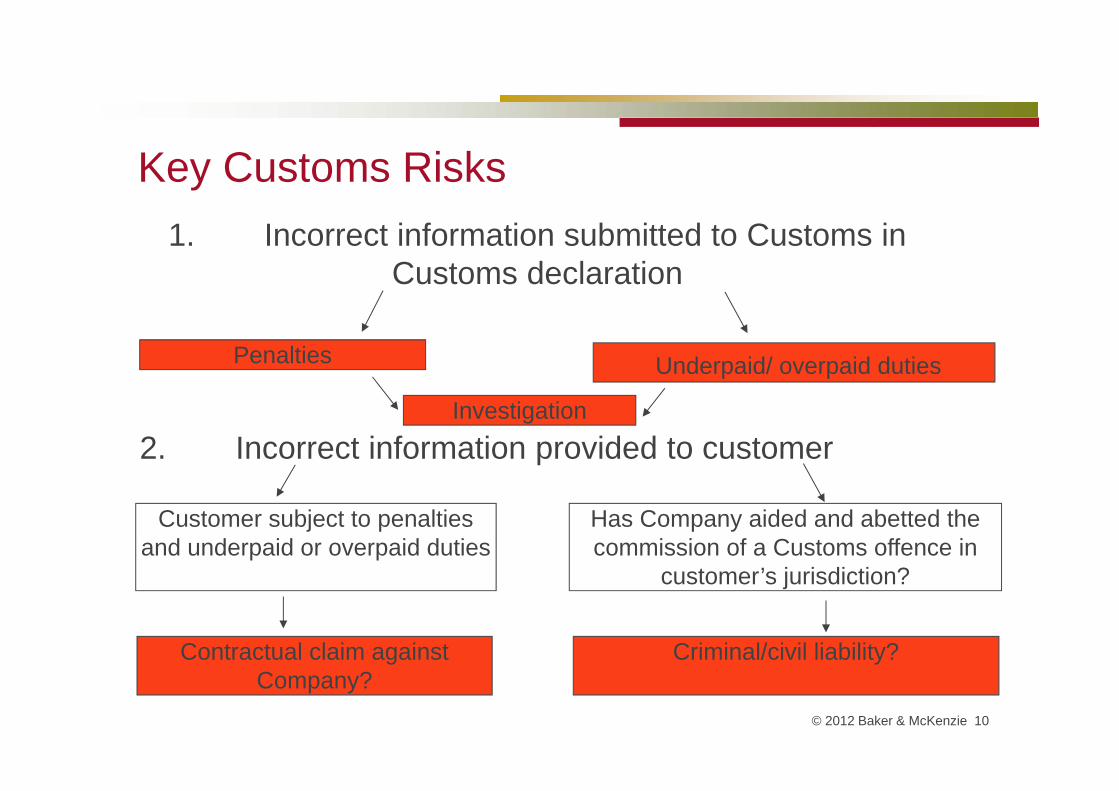

Key Customs Risks

© 2012 Baker & McKenzie 10

Key Customs Risks1. Incorrect information submitted to Customs in

Customs declaration

Penalties Underpaid/ overpaid duties

2. Incorrect information provided to customer

Customer subject to penalties and underpaid or overpaid duties

Has Company aided and abetted the commission of a Customs offence in

customer’s jurisdiction?

Contractual claim against Company?

Criminal/civil liability?

Investigation

© 2012 Baker & McKenzie 11

Why Getting It Right Matters– Import declarations

– Responsibility for complete and accurate information – Tariff classification, valuation, origin etc.

– Export declarations required for– Export compliance verification – VAT refund claims – Trade statistical purposes

– Relationships with, and allocation of responsibility between, importers and Customs brokers

Recordkeeping and reporting requirements

© 2012 Baker & McKenzie 12

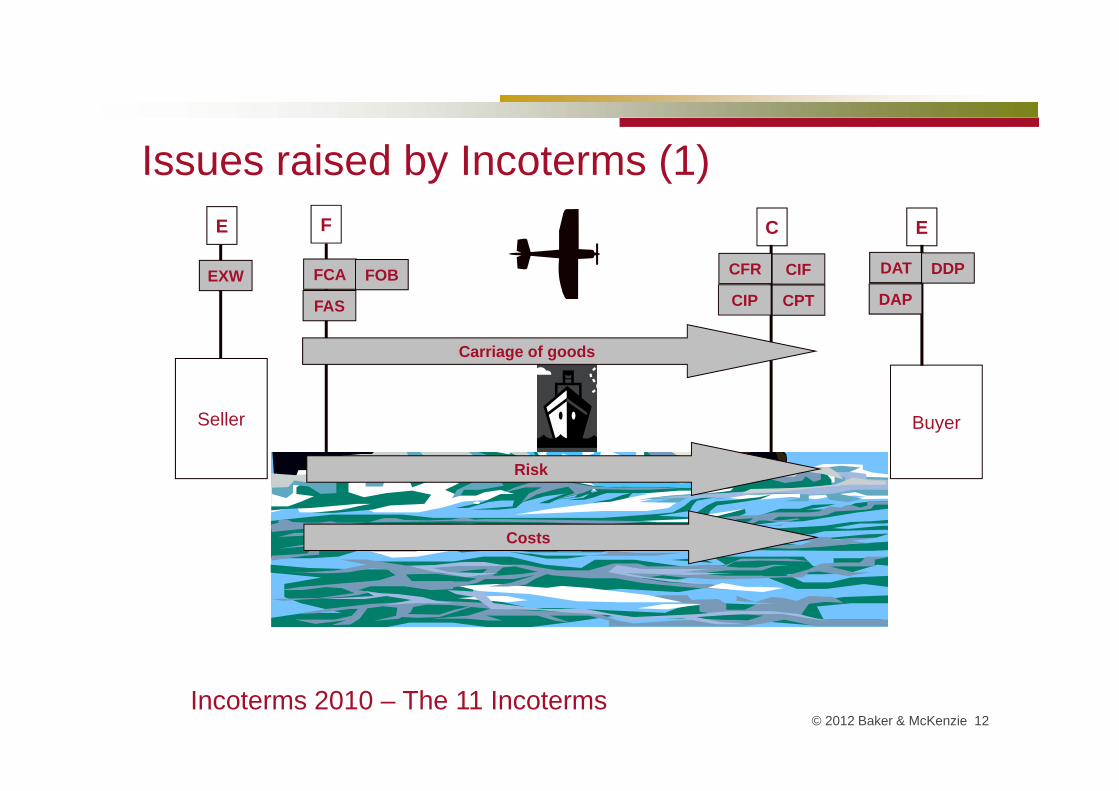

Seller

EXW

E F

FCA FOB

FAS

C

CFR CIF

CIP CPT

E

Buyer

Carriage of goods

Risk

Costs

Incoterms 2010 – The 11 Incoterms

Issues raised by Incoterms (1)

DAT DDP

DAP

Issues raised by Incoterms (2)– According to Incoterms, who is responsible for customs declaration

– On import? On export?– Who is responsible for physical shipment of the goods and will file

declaration on importer/ exporter’s behalf? (e.g. Ex-Works)– Who owns the goods at the time of export?– For valuation purposes on import, what is included in the price?

– Valuation based on (EC Customs Code (CC) (EC Reg 2913/92, Articles 28-36)):– “price paid or payable for the goods when sold for export to the

EU” – with certain additions (e.g. transport/ insurance costs to the EU)– with certain deductions if shown separately on invoice (e.g.

import duties)– Who is legally responsible for filing customs declaration? Legal

position will override Incoterms (or other contractual provisions)

© 2012 Baker & McKenzie 13

© 2012 Baker & McKenzie 14

Dealing with your Customs Broker– Outsourcing customs clearance to a broker

– Direct– 3rd party makes customs entry in the name of Co. and on its

behalf (Co. liable for customs debt)– Indirect representation

– 3rd party makes entry in its own name (broker is jointly & severally liable with Co. for customs debt)

– Representative has to be established in the EU– Problems with reliance upon freight forwarders and Customs brokers

– Recordkeeping– Accuracy of information submitted to Customs– Providing clear instructions/delegation of responsibilities and

accurate data to customer broker is vital

© 2012 Baker & McKenzie 15

Dealing with your Customs Broker (2)

– What is your current position?– No agreement – are services governed by 3rd party’s

standard terms?– Many 3rd parties are freight-forwarders, and

use standard terms – Standard terms drafted for logistics and freight-forwarding

– not necessarily appropriate for customs work

© 2012 Baker & McKenzie 16

Customer Nominated Customs Broker

– Remember that if import/ export declaration is made in your name, you are liable for accuracy

– Check legal position: in whose name should the declaration be made?

– What controls can you put in place to check accuracy of declaration?– Contractual protection– Review declarations for accuracy and request

amendments where required

© 2012 Baker & McKenzie 17

Information given to/ received from Third Parties

– Key risk area: country of origin information– Issuing preferential certificates or invoice statements. If information

is incorrect:– Compliance risk with Customs– Contractual risk with customer

– Relevant also for product marking– Challenge with changes in supply chain

– Similar risks equally apply in other areas – e.g., classification, valuation – remember you are responsible for your declaration and must not over-rely on information from third parties

– Do not forget risks re information you provide to your customers

© 2012 Baker & McKenzie 18

Key Export Controls and Sanctions Risks

© 2012 Baker & McKenzie 19

Export Risk AssessmentFirst: who is responsible for export compliance?

– Who is the “exporter”? – Which party is responsible for obtaining a licence?– Which is the competent licensing/enforcement authority?

Risk profile will then depend on nature of transaction:1. What are you supplying?

– Item included on a control list (dual-use, military, sanctions)?2. What will the item be used for?

– Controlled activity or end-use?3. Where are you supplying to?

– Country subject to sanctions or embargo?– Which other countries are involved in the supply route?

4. Who are you supplying to?– Counterparty or related party subject to sanctions?– Method of payment/funds flow?– Blocking or freezing of funds?

© 2012 Baker & McKenzie 20

Key Risks: What is your product and what is it used for?– Remember to consider:

– EU dual-use controls– Additional unilateral UK dual-use controls– Military controls (EU Common Military List/ national lists) (including

“specially designed or modified”)– Military and WMD end-use controls– Product controls under specific sanctions regimes (e.g., Iran, Syria)– NB: Trafficking and brokering controls

Key Risks: Where are you supplying to?

© 2012 Baker & McKenzie 21

– For most intra-EU shipments, no licence will be required (except for military items and more sensitive (Annex IV) dual-use items)

– Commercial documents must clearly state whether the items are controlled if exported outside the EU– EU Member State authority may impose export licensing requirement on intra-EU transfers where the

exporter knows that the controlled item will subsequently be exported outside the EU without any processing or working within the EU. This requirement has been adopted by the UK, but not all Member States.

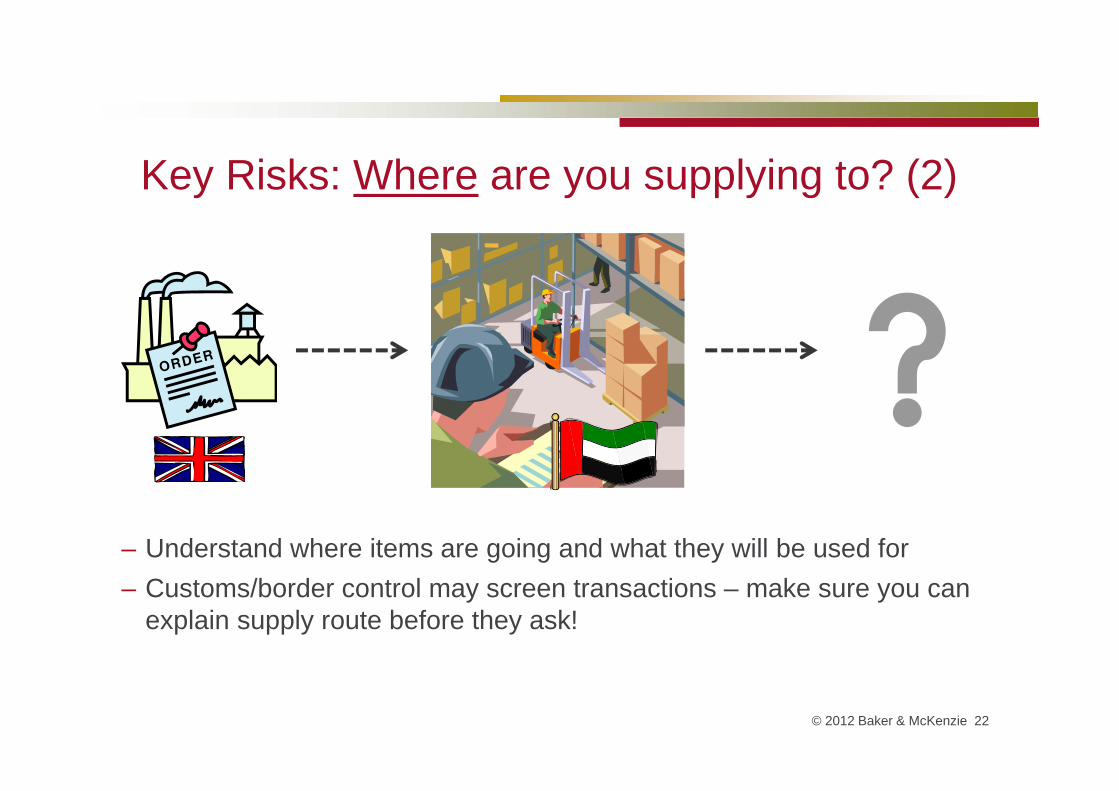

Key Risks: Where are you supplying to? (2)

© 2012 Baker & McKenzie 22

– Understand where items are going and what they will be used for– Customs/border control may screen transactions – make sure you can

explain supply route before they ask!

© 2012 Baker & McKenzie 23© 2012 Baker & McKenzie 23

Key Risks: Who are you supplying to?– Designated Person controls– Freeze on funds and economic resources belonging to, owned, held or

controlled by DPs– Prohibitions on making funds or economic resources available, directly

or indirectly, to or for the benefit of DPs– Concepts of “funds” and “economic resources” very broadly defined– DPs can include wide range of parties (e.g. entities, banks, individuals)– Knowledge defence if “did not know, and had no reasonable cause to

suspect”– Breach of contractual obligation will not give rise to liability if based on

good faith implementation of sanctions

© 2012 Baker & McKenzie 24© 2012 Baker & McKenzie 24

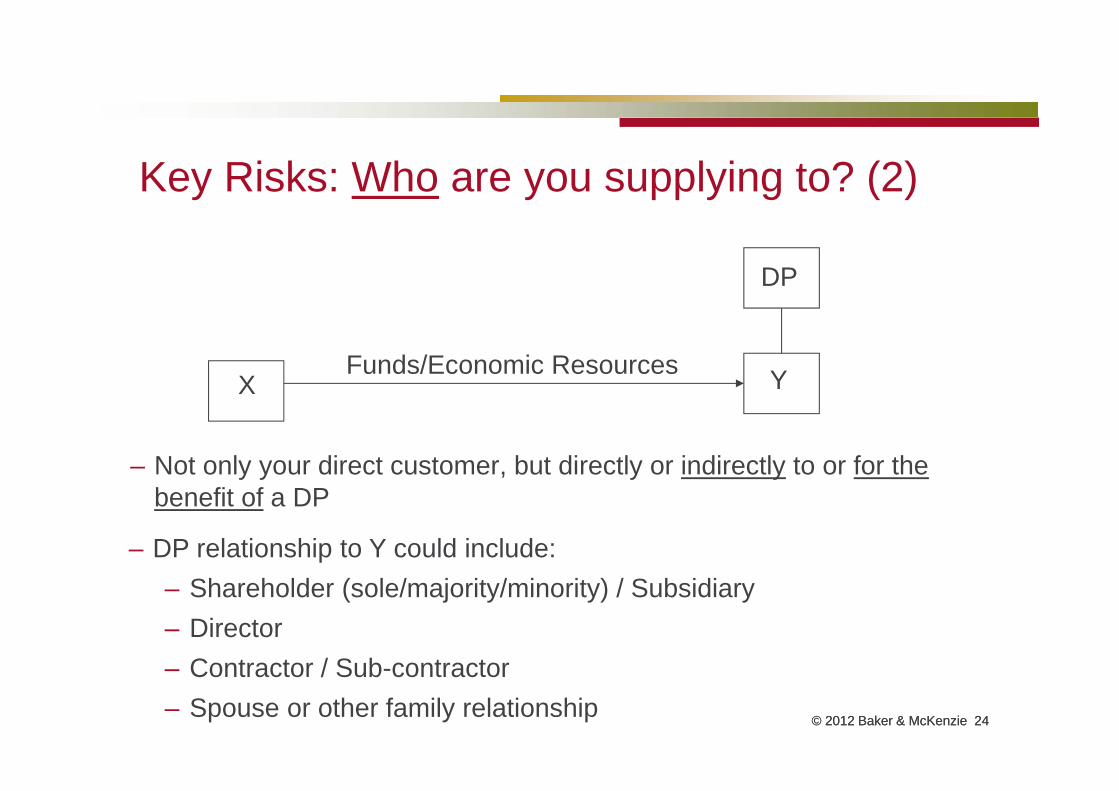

Key Risks: Who are you supplying to? (2)

– Not only your direct customer, but directly or indirectly to or for the benefit of a DP

X

DP

YFunds/Economic Resources

– DP relationship to Y could include:– Shareholder (sole/majority/minority) / Subsidiary– Director – Contractor / Sub-contractor– Spouse or other family relationship

Key Risks: Getting Paid– Financial restrictions on dealings with Iran:

– EU controls on transfer of funds to/from Iranian persons (including revised stricter controls on transactions involving EU and Iranian banks)

– Prior notification and authorisation requirements – allow four weeks lead time for authorisation

– Prohibition on relationships between UK and Iranian banks– Enhanced vigilance requirements and other restrictions on EU banks dealing with

Iranian financial entities– Financial restrictions (albeit not funds transfer controls) in place in respect of other

sanctioned countries (e.g., Syria)– General reluctance on part of banks to deal with sanctioned countries, particularly

following US investigations/enforcement actions against EU banks– May be practical difficulties in obtaining payment even where transaction is not

expressly prohibited, and even where competent authority has granted authorisation– Consider potential US sanctions implications for US dollar transactions– Consider how to mitigate dependency on payments from higher risk jurisdictions

© 2012 Baker & McKenzie 25

© 2012 Baker & McKenzie 26

Anti-Bribery & Corruption

© 2012 Baker & McKenzie 27

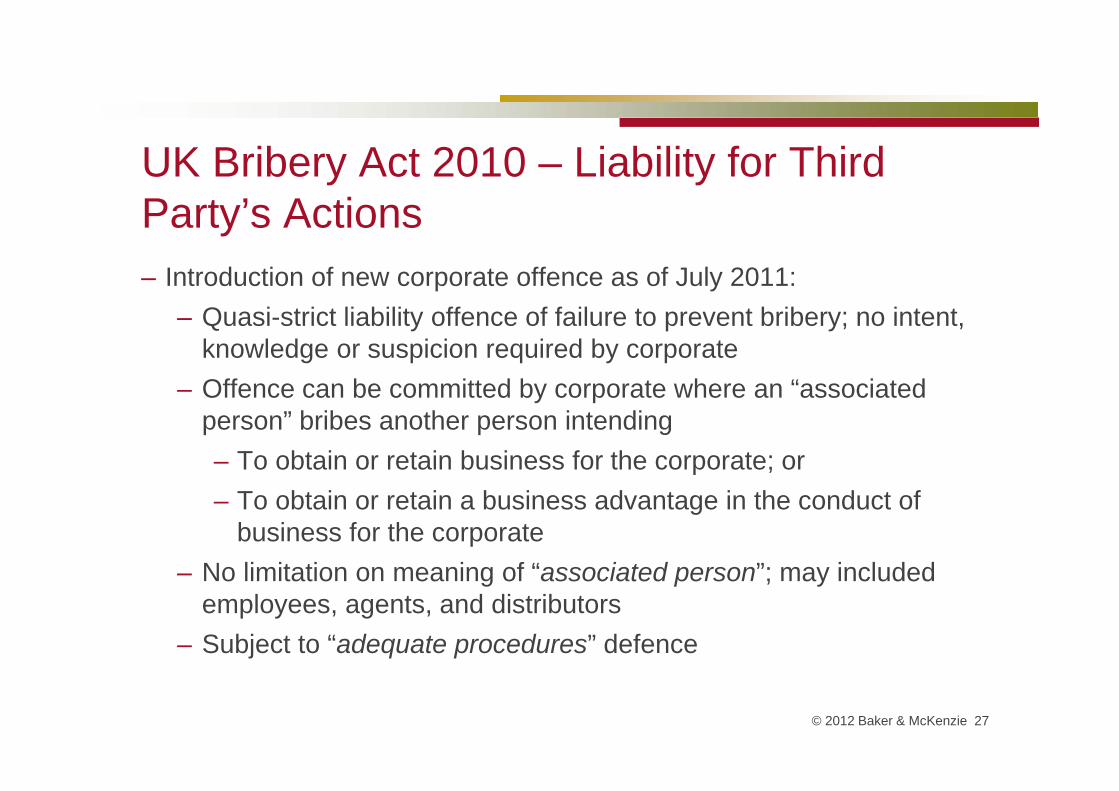

UK Bribery Act 2010 – Liability for Third Party’s Actions– Introduction of new corporate offence as of July 2011:

– Quasi-strict liability offence of failure to prevent bribery; no intent, knowledge or suspicion required by corporate

– Offence can be committed by corporate where an “associated person” bribes another person intending– To obtain or retain business for the corporate; or– To obtain or retain a business advantage in the conduct of

business for the corporate– No limitation on meaning of “associated person”; may included

employees, agents, and distributors– Subject to “adequate procedures” defence

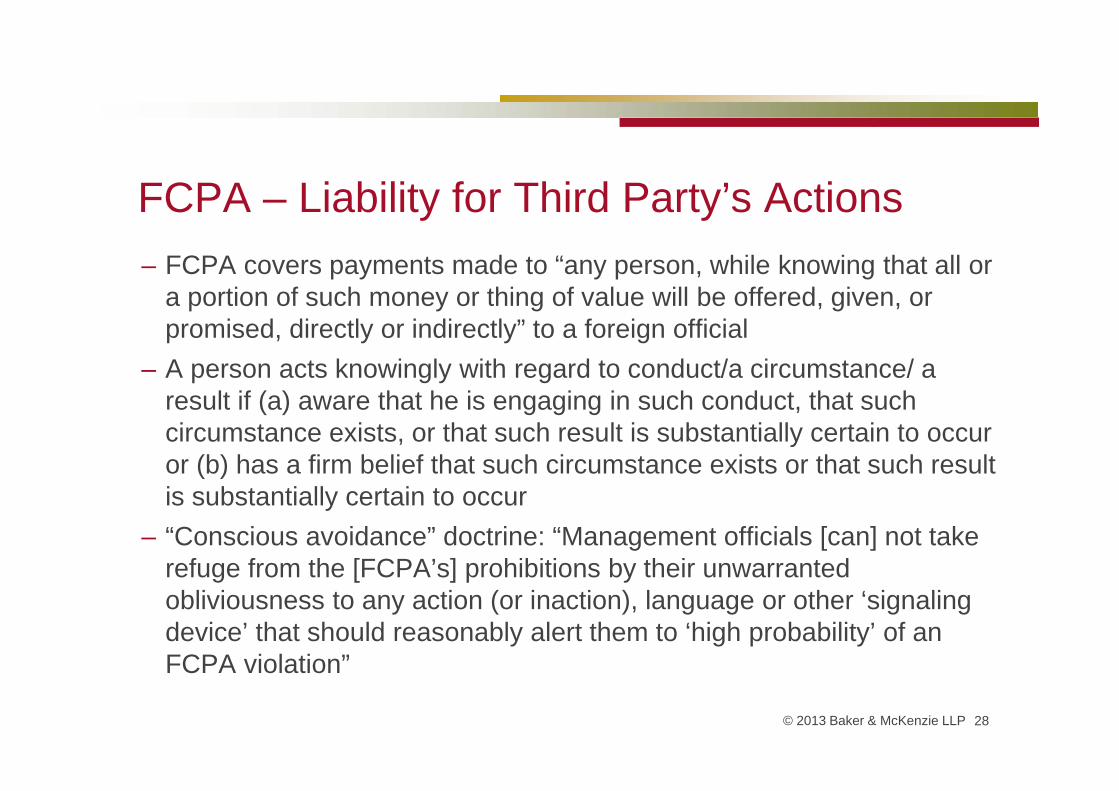

FCPA – Liability for Third Party’s Actions– FCPA covers payments made to “any person, while knowing that all or

a portion of such money or thing of value will be offered, given, or promised, directly or indirectly” to a foreign official

– A person acts knowingly with regard to conduct/a circumstance/ a result if (a) aware that he is engaging in such conduct, that such circumstance exists, or that such result is substantially certain to occur or (b) has a firm belief that such circumstance exists or that such result is substantially certain to occur

– “Conscious avoidance” doctrine: “Management officials [can] not take refuge from the [FCPA’s] prohibitions by their unwarranted obliviousness to any action (or inaction), language or other ‘signaling device’ that should reasonably alert them to ‘high probability’ of an FCPA violation”

© 2013 Baker & McKenzie LLP 28

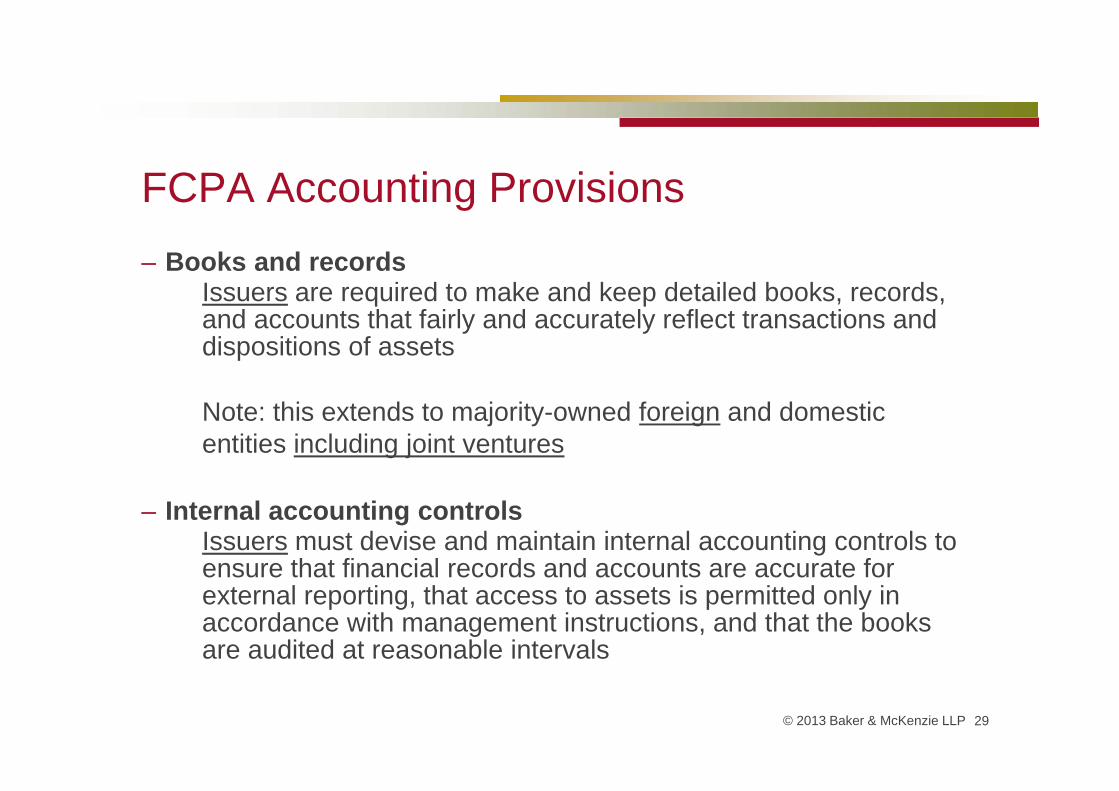

FCPA Accounting Provisions– Books and records

Issuers are required to make and keep detailed books, records, and accounts that fairly and accurately reflect transactions and dispositions of assets

Note: this extends to majority-owned foreign and domestic entities including joint ventures

– Internal accounting controlsIssuers must devise and maintain internal accounting controls to ensure that financial records and accounts are accurate for external reporting, that access to assets is permitted only in accordance with management instructions, and that the books are audited at reasonable intervals

29© 2013 Baker & McKenzie LLP

© 2012 Baker & McKenzie 30

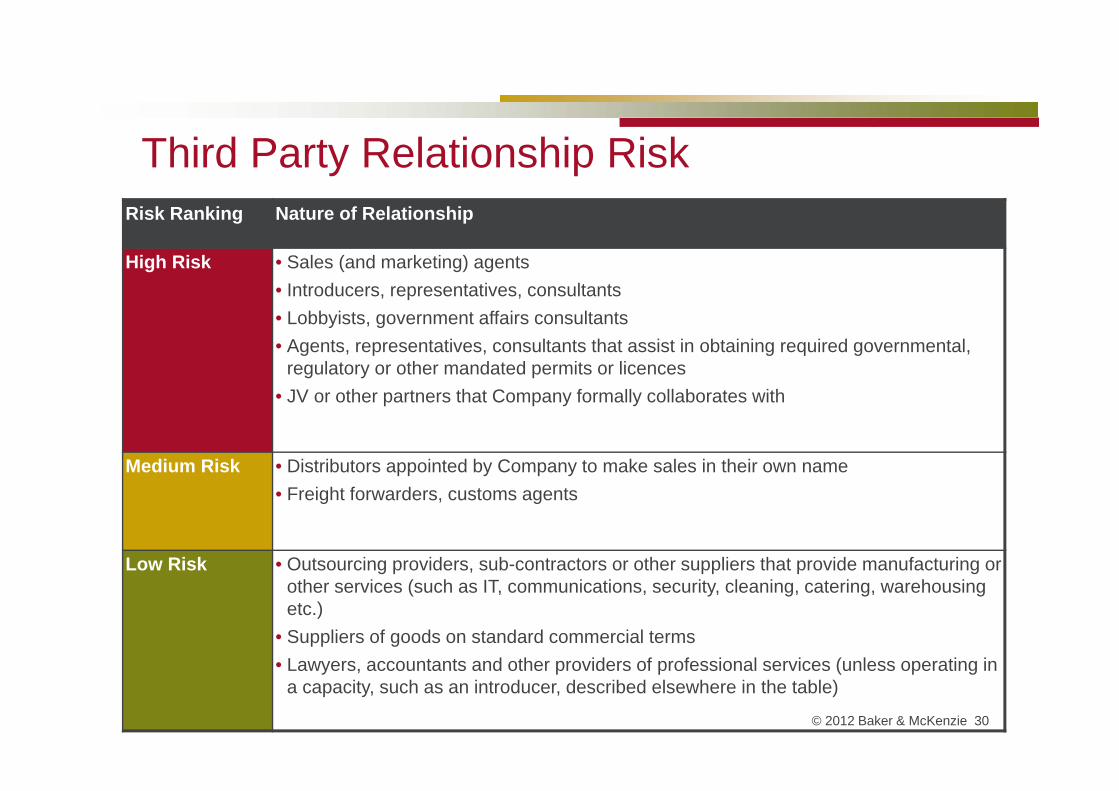

Third Party Relationship RiskRisk Ranking Nature of Relationship

High Risk • Sales (and marketing) agents • Introducers, representatives, consultants • Lobbyists, government affairs consultants • Agents, representatives, consultants that assist in obtaining required governmental,

regulatory or other mandated permits or licences• JV or other partners that Company formally collaborates with

Medium Risk • Distributors appointed by Company to make sales in their own name • Freight forwarders, customs agents

Low Risk • Outsourcing providers, sub-contractors or other suppliers that provide manufacturing or other services (such as IT, communications, security, cleaning, catering, warehousing etc.)

• Suppliers of goods on standard commercial terms• Lawyers, accountants and other providers of professional services (unless operating in

a capacity, such as an introducer, described elsewhere in the table)

Jurisdictional RiskCorruption Perceptions Index 2012

© 2013 Baker & McKenzie LLP 31

Managing compliance and trade control risks

32

Overview of how to manage those risks

– Upfront due diligence– Appropriate contractual clauses

© 2012 Baker & McKenzie 33

© 2012 Baker & McKenzie 34

Customs

© 2012 Baker & McKenzie 35

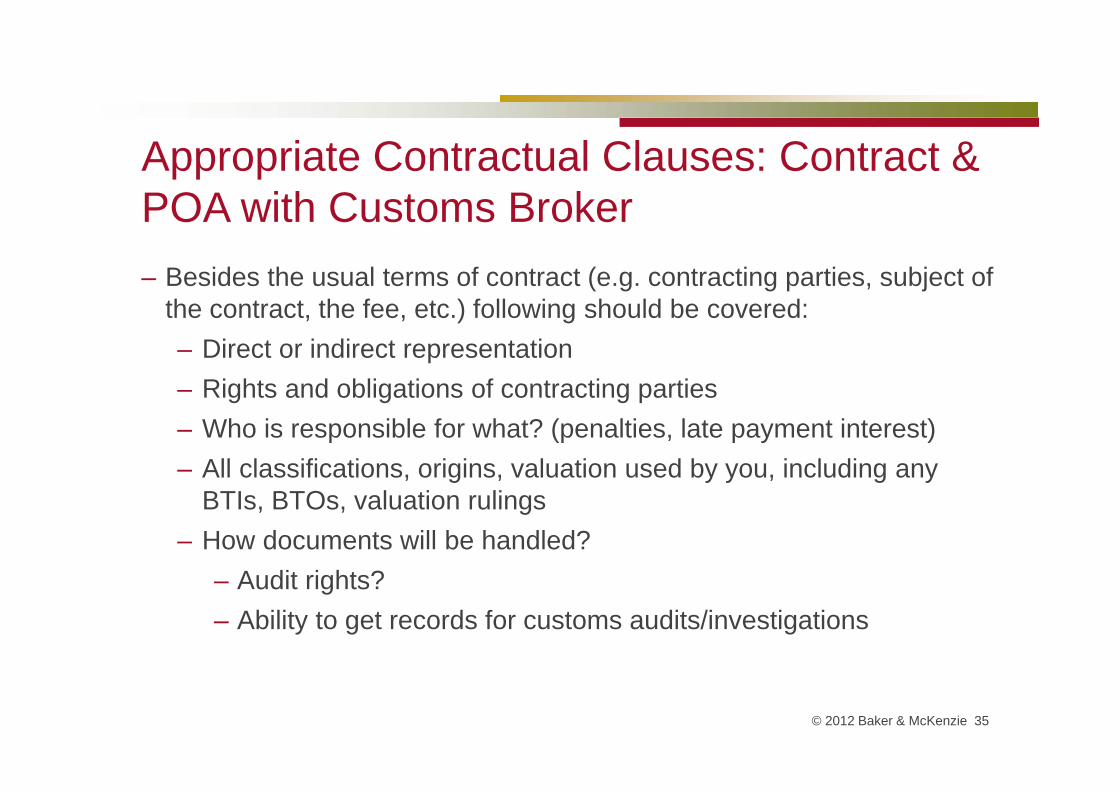

– Besides the usual terms of contract (e.g. contracting parties, subject of the contract, the fee, etc.) following should be covered:– Direct or indirect representation– Rights and obligations of contracting parties– Who is responsible for what? (penalties, late payment interest)– All classifications, origins, valuation used by you, including any

BTIs, BTOs, valuation rulings– How documents will be handled?

– Audit rights?– Ability to get records for customs audits/investigations

Appropriate Contractual Clauses: Contract & POA with Customs Broker

Appropriate Contractual Clauses: Reducing Third Party Risk– Consider including language in agreements with third

parties (particularly distributors and agents, but also customers/other third parties), requiring compliance with applicable export controls and sanctions (including, e.g.: that export licences will be obtained where applicable; that nothing will be made available, directly or indirectly, to or for the benefit of a DP)

– But remember – cannot contract out of export control requirements where you are the “exporter”

© 2012 Baker & McKenzie 36

© 2012 Baker & McKenzie 3737

Supply Chain Security

WCO Safe Framework of Standards

- An authorized economic operator, or AEO, is defined as:“ ...a party involved in the international movement of goods in whatever function that has been approved by or on behalf of a national Customs administration as complying with WCO or equivalent supply chain security standards. AEOs include inter alia manufacturers, importers, exporters, brokers, carriers, consolidators, intermediaries, ports, airports, terminal operators, integrated operators, warehouses, distributors”

May reduce risk rating from an anti-bribery DD perspective

© 2012 Baker & McKenzie 38

Export Controls and Trade Sanctions

– Is the item controlled?– Individual assessment required in respect of each different product line (and

parts/components when sent separately)– When to consider export classification?

– Vital: before shipping– Better: design/production/planning stage

– Get input from technical experts where necessary– NB: some tools available to assist with classification

– EU Commission Correlation Table matches up the TARIC customs codes with dual-use codes

– http://trade.ec.europa.eu/doclib/docs/2012/july/tradoc_149781.pdf– EU TARIC database also flags potential concerns– May appear helpful, but should not be relied upon!

© 2012 Baker & McKenzie 39

Upfront Due Diligence: What?

Upfront Due Diligence: What for?

– Do you know that the items will be used for military use in an embargoed country?

– Do you know or do you suspect that the items will be used for WMD end-use?

– Are the items being supplied to a country subject to sanctions? Have you checked any product controls under the sanctions regime?

– Do you require an end-user undertaking?– Do you need more information from your

distributor/customer?

© 2012 Baker & McKenzie 40

Upfront Due Diligence: Where?

– Do you have a “countries of concern” list? – If so, how is this updated (if at all)?– Do you know which sanctions measures are in place

against destination country? Are there any additional product controls (e.g., Iran, North Korea, Syria, etc.)

– How do you check where your goods are going?– Speak to customer?– Manual checks of shipping documents prior to

shipment?– Automatic blocking in ERP?

© 2012 Baker & McKenzie 41

© 2012 Baker & McKenzie 42

Upfront Due Diligence: Who?– Clearly documented standardised approach to screening (including

allocation of responsibilities)– Consider incorporating as part of customer/intake process into ERP or

otherwise, with additional ongoing checks (at a minimum screening prior to supply or transferring funds)

– Screen against all information in your possession (may need to request further information from the customer in some cases)

– Due diligence on parents, directors and other associated third parties– Risk based approach for more problematic territories– Customer/end-user undertakings?

© 2012 Baker & McKenzie 42

Upfront Due Diligence: Who? (2)

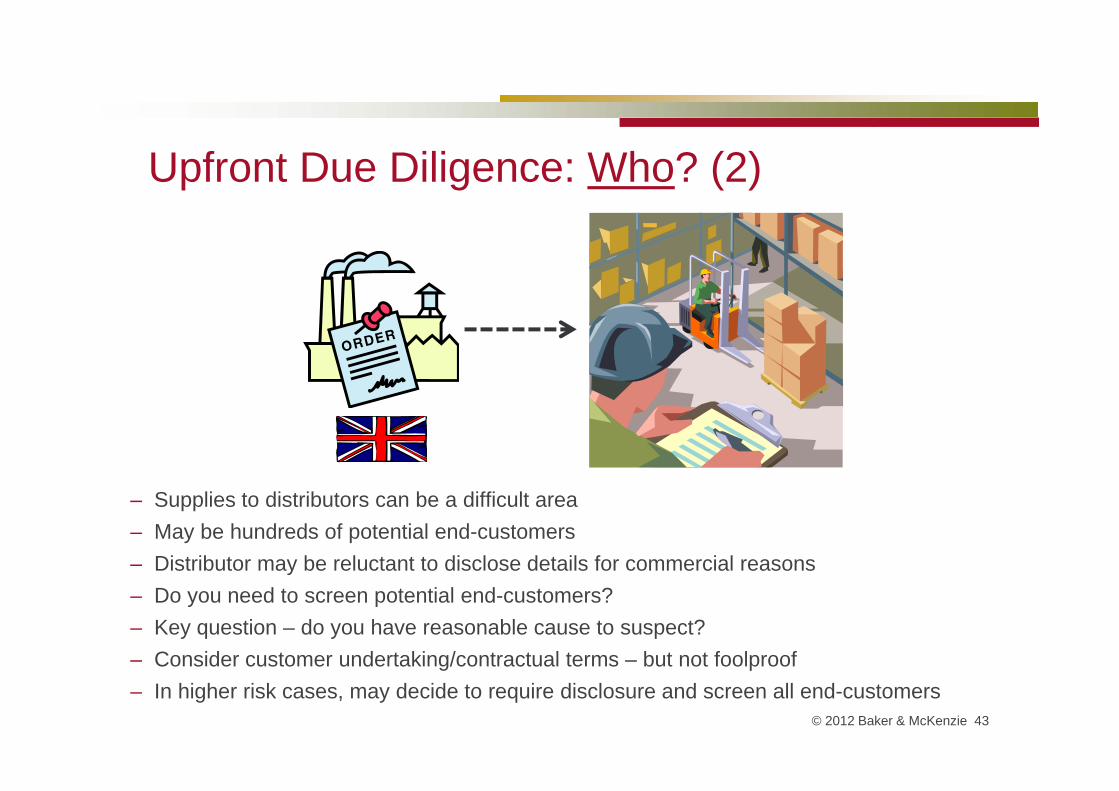

– Supplies to distributors can be a difficult area– May be hundreds of potential end-customers– Distributor may be reluctant to disclose details for commercial reasons– Do you need to screen potential end-customers?– Key question – do you have reasonable cause to suspect?– Consider customer undertaking/contractual terms – but not foolproof– In higher risk cases, may decide to require disclosure and screen all end-customers

© 2012 Baker & McKenzie 43

– Consider need to terminate in order to comply with export controls or sanctions (e.g., not able to obtain export licence; adoption of new sanctions prohibiting supply to a particular country and/or party):

– EU sanctions regimes provide some protection:– against liability for refusal to make payment or to supply goods

based on good faith reliance on sanctions– against claims from Iranian parties or designated persons for

breaches of contracts affected by sanctions– However, no blanket right to cancel contracts – consider contractual

clauses giving additional protection, allowing termination if prohibited by new sanctions (NB: Burma)

– Caution with relying upon more general “force majeure”

© 2012 Baker & McKenzie 44

Appropriate Contractual Clauses: Ability to Terminate

Managing Export Risks - Tips– Review product controls (including end-use)– Undertake appropriate, risk-based due diligence– Importance of documenting analysis– Consider need for contractual provisions– How will you receive payment? – Be aware of enforcement environment in relevant Member

State(s)– Outcome will depend in part on risk appetite

© 2012 Baker & McKenzie 45

© 2012 Baker & McKenzie 46

Anti-Bribery and Corruption

© 2012 Baker & McKenzie 47

Third Party Due Diligence

– Almost always highest risk– Lack of control– May be working at “sharp end” in places you are unfamiliar with

– Need to ensure that third parties are– Checked carefully – proper due diligence– Locked into clear obligations – proper contractual provisions– Where possible trained and audited

– Calibrate screening for different categories of risk; principally determined by jurisdiction and nature of third party – e.g. Sales intermediary operating in a high risk country

© 2012 Baker & McKenzie 48

Delivering an Effective Third Party Process – Process must be clearly defined– Promote timely submission of third party approval requests– Consider who needs to input, ownership and structure of the

process– Business– Legal / Compliance– Finance

– Ensure consistent application of standards (e.g. third party rejected by one part of the business must not be approved by another part)

– Adoption of a Third Party Code of Conduct?– Defined process for monitoring and reviewing third party

relationships– Thorough documentation of process; “adequate procedures”– Effective verification of payments to third parties through back-end

financial controls

© 2012 Baker & McKenzie 49

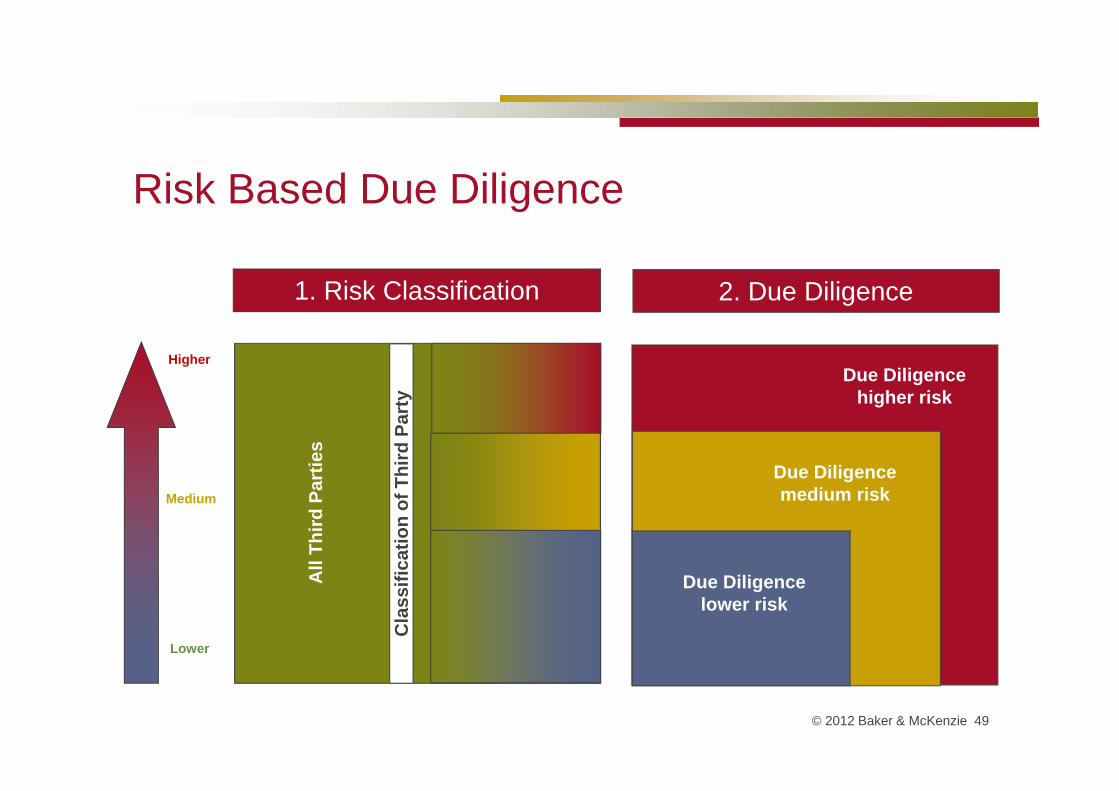

Risk Based Due Diligence

1. Risk Classification

Higher

Medium

Lower

Due Diligencelower risk

Due Diligencemedium risk

Due Diligencehigher risk

2. Due Diligence

Cla

ssifi

catio

n of

Thi

rd P

arty

All

Third

Par

ties

© 2012 Baker & McKenzie 50

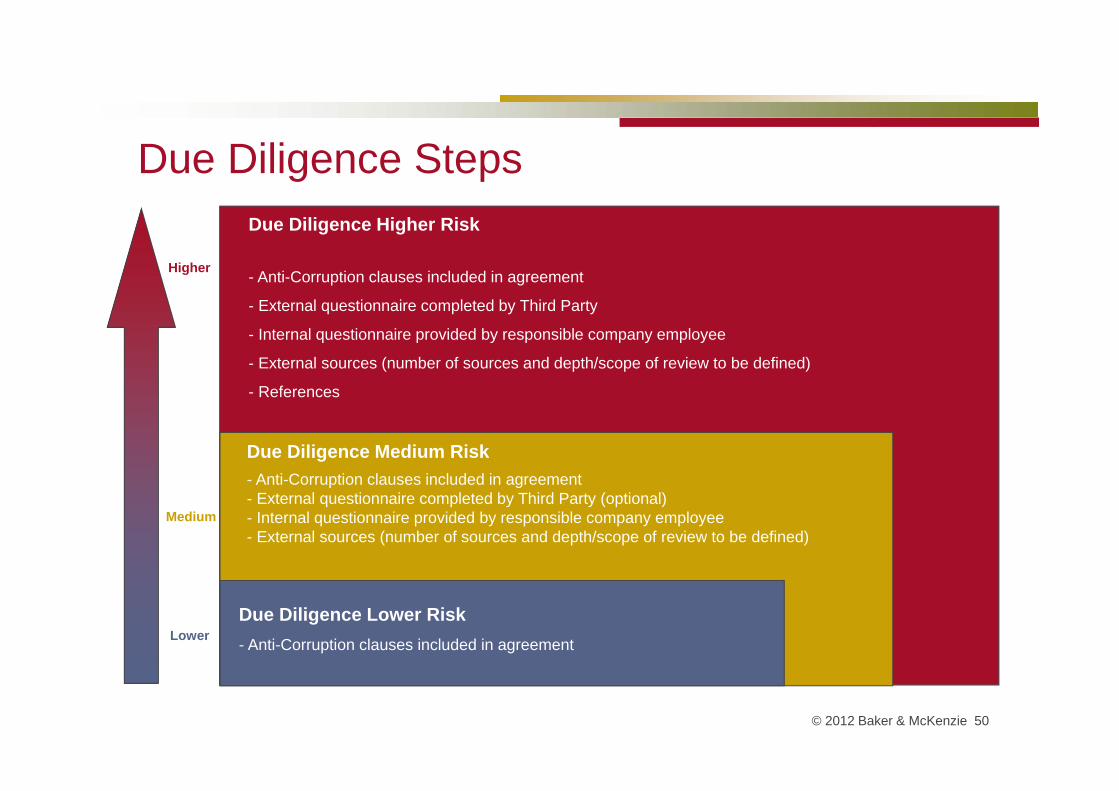

Higher

Medium

LowerDue Diligence Lower Risk- Anti-Corruption clauses included in agreement

Due Diligence Medium Risk- Anti-Corruption clauses included in agreement- External questionnaire completed by Third Party (optional)- Internal questionnaire provided by responsible company employee- External sources (number of sources and depth/scope of review to be defined)

Due Diligence Higher Risk

- Anti-Corruption clauses included in agreement

- External questionnaire completed by Third Party

- Internal questionnaire provided by responsible company employee

- External sources (number of sources and depth/scope of review to be defined)

- References

Due Diligence Steps

© 2012 Baker & McKenzie 51

Key Issues for Third Party Screening – Necessity

– “Do we need the third party?”– Qualification

– “Is the third party qualified?”– “Is the third party competent / experienced?”

– Reasonableness of the compensation– “Is the compensation commensurate with the services being

provided?”– “How does the compensation compare to other benchmarks,

such as industry practice or our practice in comparable situations?”

– Integrity– “Who is the third party?”– “What does the third party request?”

© 2012 Baker & McKenzie 52

Third Party Agreements – Discussion Points– Content of anti-bribery clause:

– Address: behaviour; compliance with laws; record keeping; audit rights; rights of termination and indemnification

– Reference to compliance with the Company’s Policy or Code of Conduct?

– When should an anti-bribery clause be included:– For all relationships? Short form vs. long form?

– When is the Company willing to negotiate the content of the anti-bribery clause?– What procedure should be followed in respect of variation

requests? What if a third party outright rejects the inclusion of an anti-bribery clause?

– What is the Company’s stance regarding an obligation to comply with a third party’s policy?– What should the standard response be? Is it ever acceptable to

contractually commit the Company to adherence to a third party’s policy?

© 2012 Baker & McKenzie 53

Top Tips

Top Tips

– Can you identify and eliminate risk before you enter into a transaction?

– Or can you control risk afterwards?Balance between due diligence and contract techniques

– As a general principle, the highest risk a business has are the third parties it deals with

© 2012 Baker & McKenzie 54

Key protections– Follow compliance “best practice”

– “tone from the top”– risk assessment– policies and procedures– training and communication– monitoring and feedback

– As an easy “win” only deal with trusted third parties– screen all third parties (including on M&A, JVs)– key third parties must be bound to clear contracts (e.g

all brokers)© 2012 Baker & McKenzie 55

© 2012 Baker & McKenzie 56

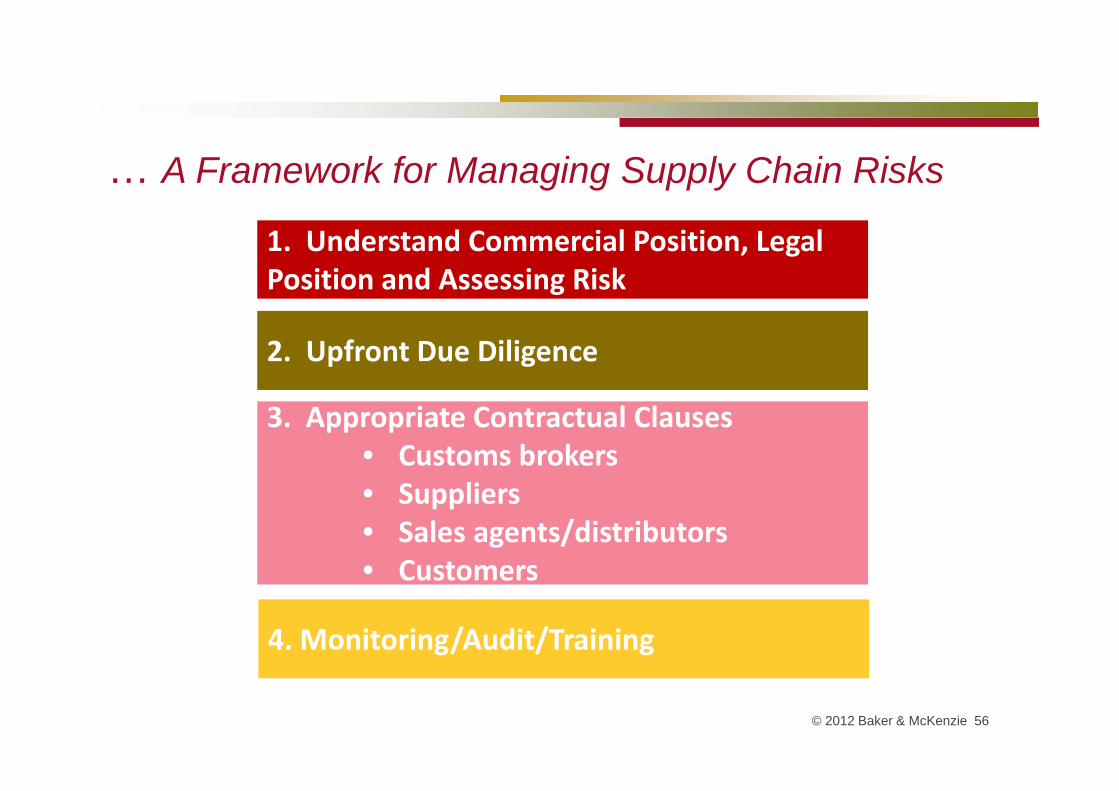

1. Understanding Incoterms

2. Upfront Due Diligence

3. Appropriate Contractual Clauses• Customs brokers• Suppliers• Sales agents/distributors• Customers

1. Understand Commercial Position, Legal Position and Assessing Risk

4. Monitoring/Audit/Training

… A Framework for Managing Supply Chain Risks

© 2012 Baker & McKenzie 57

Any Questions?

Chartered Institute of Purchasing and Supply –Your liberty could be at stake! - Compliance and trade controls you need to be aware of

[email protected]@bakermckenzie.com

Thursday 16 May 2013

Baker & McKenzie LLP is a member firm of Baker & McKenzie International, a Swiss Verein with member law firms around the world. In accordance with the common terminology used in professional service organisations, reference to a "partner" means a person who is a partner, or equivalent, in such a law firm. Similarly, reference to an "office" means an office of any such law firm.© 2012 Baker & McKenzie LLP