Embed Size (px)

Citation preview

Charting China’s Booming Outbound M&A Activity

March 10th, 2015

Page 1

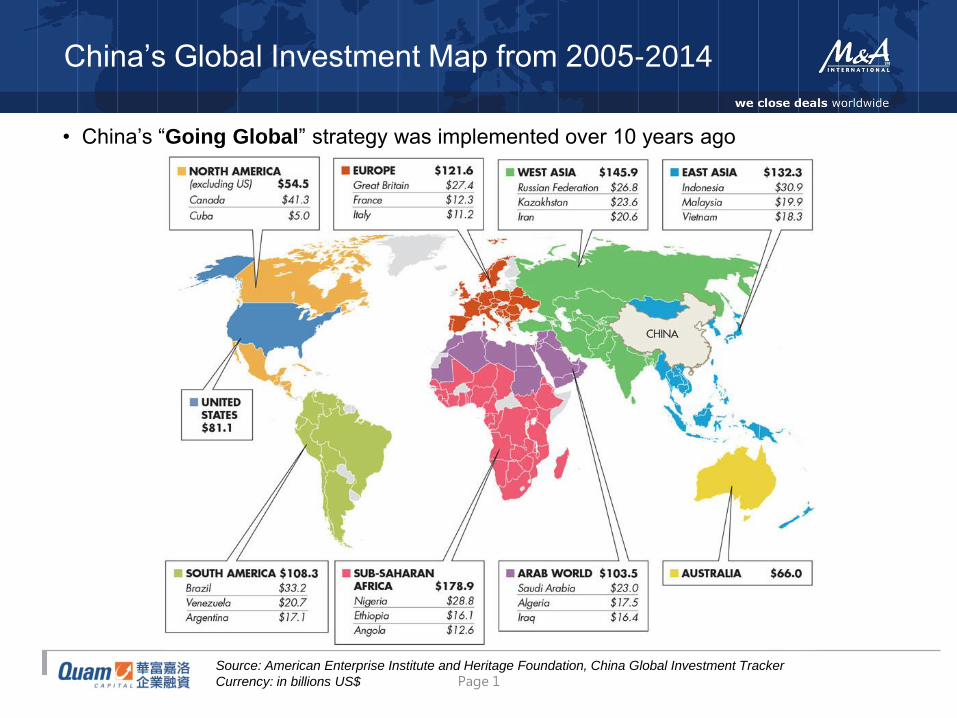

China’s Global Investment Map from 2005-2014

Source: American Enterprise Institute and Heritage Foundation, China Global Investment Tracker

Currency: in billions US$

• China’s “Going Global” strategy was implemented over 10 years ago

Page 2

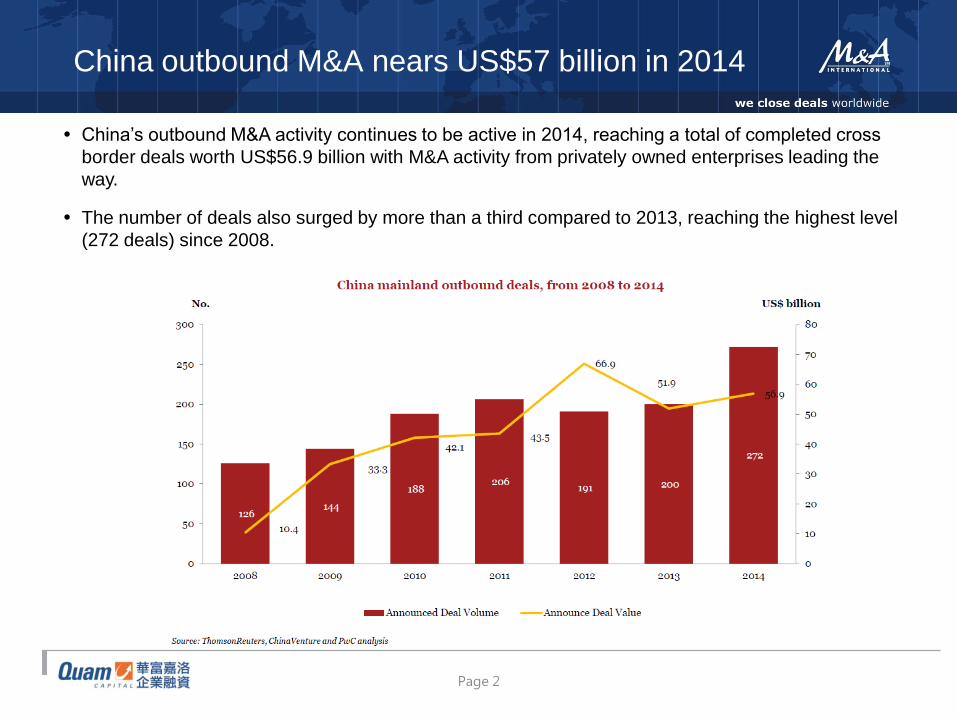

China’s outbound M&A activity continues to be active in 2014, reaching a total of completed cross

border deals worth US$56.9 billion with M&A activity from privately owned enterprises leading the

way.

The number of deals also surged by more than a third compared to 2013, reaching the highest level

(272 deals) since 2008.

China outbound M&A nears US$57 billion in 2014

Page 3

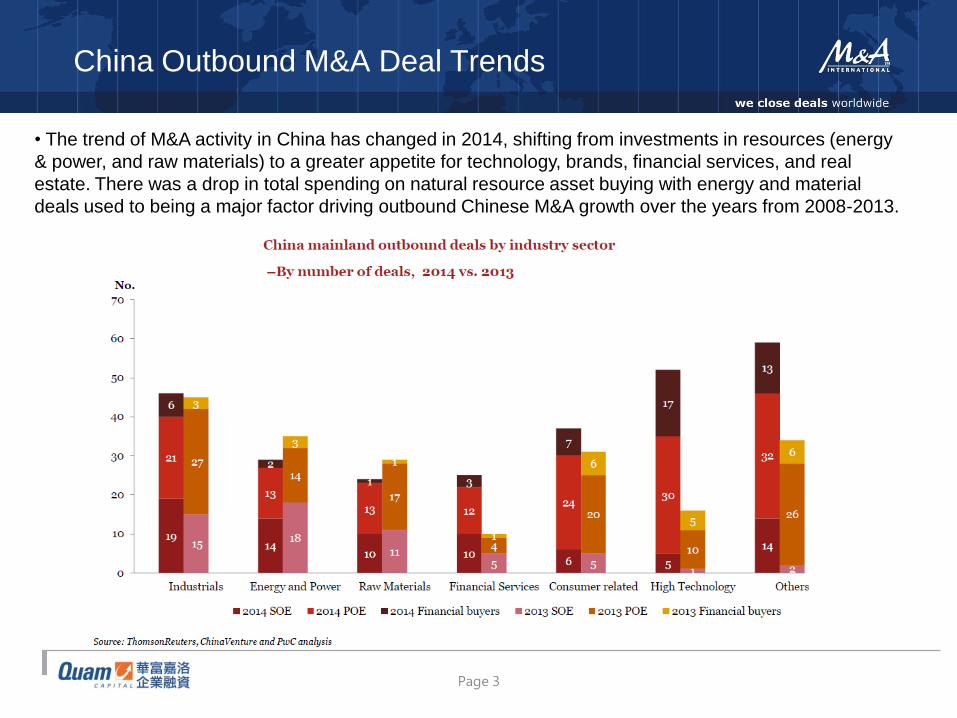

China Outbound M&A Deal Trends

• The trend of M&A activity in China has changed in 2014, shifting from investments in resources (energy

& power, and raw materials) to a greater appetite for technology, brands, financial services, and real

estate. There was a drop in total spending on natural resource asset buying with energy and material

deals used to being a major factor driving outbound Chinese M&A growth over the years from 2008-2013.

Page 4

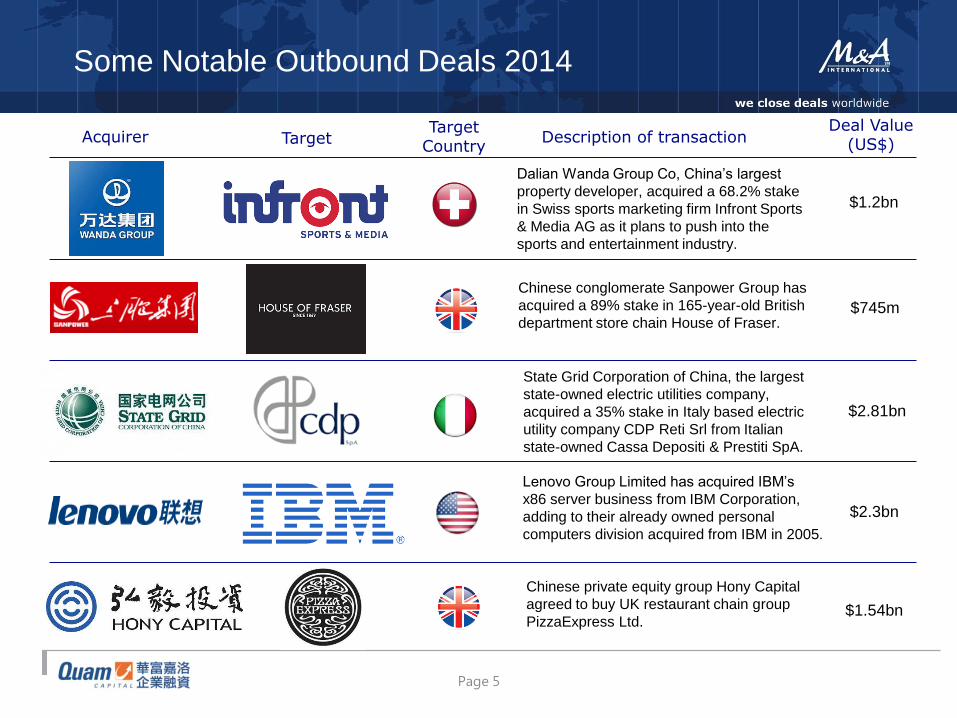

Some Notable Outbound Deals 2014

Acquirer Target

Country Target Description of transaction

Chinese insurer Anbang has acquired a

controlling stake of 57.5% in South Korean

insurer Tong Yang Life Insurance Co., Ltd.

Lenovo Group Limited has acquired US TMT

company Motorola Mobility Holdings, Inc. from

Google Inc. to boost its smartphone business.

Fosun International and its partners acquired

a stake of 92.8% in French resorts company

Club Méditerranée (Club Med) .

Deal Value (US$)

$1bn

$1bn

$5.85bn

$2.91bn

Glencore Xstrata has agreed to sell its entire

interest in its Las Bambas copper mine in

Peru to a consortium led by MMG Ltd., a unit

of state-controlled China Minmetals Corp.

China National Cereals, Oils and Foodstuffs

Corporation (COFCO), one of China’s largest

state-owned food processing holding

companies, has acquired a 51% stake in Dutch

grain trader Nidera B.V.

$2.84bn

Glencore Xstrata

Las Bambas

Page 5

Acquirer Target

Country Target Description of transaction

Deal Value (US$)

Some Notable Outbound Deals 2014

$745m

$1.54bn

$1.2bn

$2.3bn

$2.81bn

Dalian Wanda Group Co, China’s largest

property developer, acquired a 68.2% stake

in Swiss sports marketing firm Infront Sports

& Media AG as it plans to push into the

sports and entertainment industry.

Lenovo Group Limited has acquired IBM’s

x86 server business from IBM Corporation,

adding to their already owned personal

computers division acquired from IBM in 2005.

Chinese conglomerate Sanpower Group has

acquired a 89% stake in 165-year-old British

department store chain House of Fraser.

Chinese private equity group Hony Capital

agreed to buy UK restaurant chain group

PizzaExpress Ltd.

State Grid Corporation of China, the largest

state-owned electric utilities company,

acquired a 35% stake in Italy based electric

utility company CDP Reti Srl from Italian

state-owned Cassa Depositi & Prestiti SpA.

Page 6

Drivers of Outbound M&A

• An excess surplus of foreign exchange

• Growth of Chinese population and their standard of living

• Chinese market becoming very competitive and saturated

• Domestic firms moving up the value chain

• Growing demand for safer and more reliable consumer products

• Global downturn has created cheaper valuations of overseas targets

Page 7

Drivers of Outbound M&A

• Government backing via easing of regulations and availability of funding

• China’s 12th Five Year Plan focuses on seven priority industries including

green energy, advanced IT, and high-end manufacturing

• Chinese companies internationalize their operations and strategies to

become competitive on a global scale, and especially to:

1) Obtain access to natural resources

2) Obtain access to more advanced technology and know-how

3) Improve brand awareness in domestic market

4) Entry into new markets and expand distribution

network

Page 8

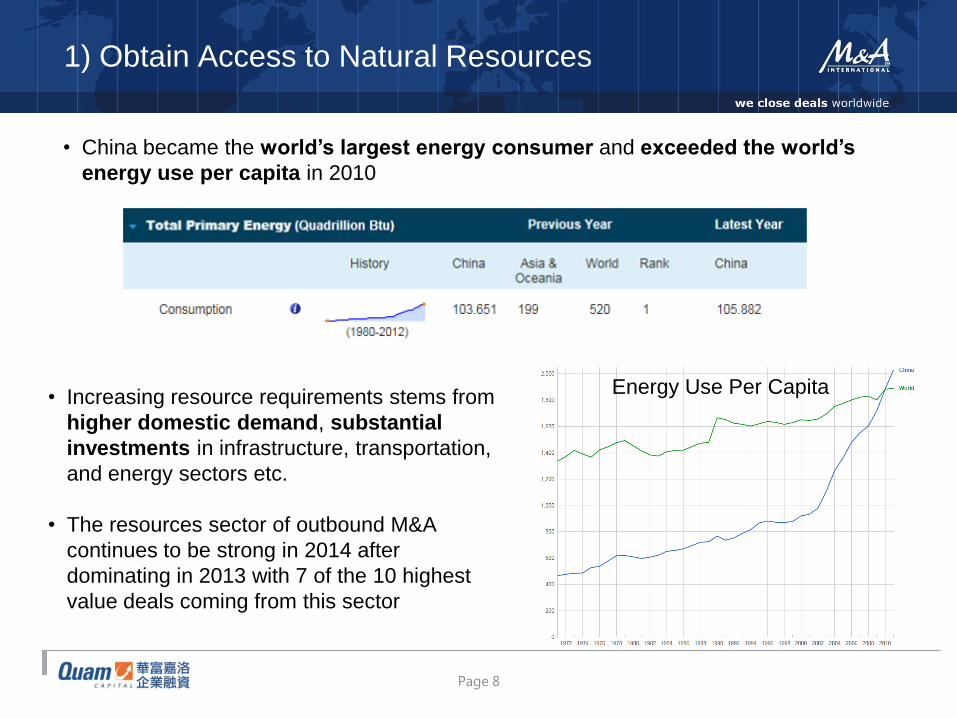

• China became the world’s largest energy consumer and exceeded the world’s

energy use per capita in 2010

1) Obtain Access to Natural Resources

Energy Use Per Capita • Increasing resource requirements stems from

higher domestic demand, substantial

investments in infrastructure, transportation,

and energy sectors etc.

• The resources sector of outbound M&A

continues to be strong in 2014 after

dominating in 2013 with 7 of the 10 highest

value deals coming from this sector

Page 9

• Chinese firms investing overseas to acquire technology and know-how, as well as to

enhance R&D capability

• Target higher value (margin) products / moving up the value chain

• Especially interested in companies with advanced technology in developed

economies located in the US and Western Europe

• The TMT sector constituted 10% of outbound M&A transactions in 2013 and 20% in

2014 based on data from Mergermarket and PwC

2) Obtain Access to Technology & Know-How

Page 10

• Chinese companies acquiring international brands to enhance image and

competitiveness mainly in the domestic market

• Shifting from manufacturing OEM products to providing own branded products (higher

margins)

• Growth of China’s middle class has increased demand for safe and high quality

supply of food resources, leading to an increased number of outbound acquisitions in

the food & beverage sector

• Consumer sector represented approximately 15% of China’s outbound M&As in 2013

and 2014

3) Improve Brand Awareness in Domestic Market

Page 11

• Although most Chinese companies are still very much focused on the domestic

market, some are looking to acquire overseas to seek relief from domestic

competition (overcapacity) and saturation.

• Entry into new markets represents opportunity to obtain new customers

• Acquiring overseas to expand distribution network and secure supplies of

commodities

4) Entry into New Markets & Expand Distribution Network

Page 12

• China’s policy response to an overheated domestic real estate market has been a

mix of restrictive measures designed to cool the market. Chinese developers have

started to look abroad for opportunities.

• One key emerging institutional player - Chinese insurance companies. Reforms in

the regulatory framework governing China’s insurance companies have opened the

door to outbound investments into real estate with the UK and the US topping the

favourite’s list.

Hot Sector #1: Real Estate Investment Abroad

China’s Ping An Insurance Group has made its second

acquisition of a major London real estate asset by

acquiring Tower Place for US$490 million.

China’s Anbang Insurance has acquired New York’s

historic Waldorf Astoria hotel for US$1.95 billion and an

office building in New York’s Fifth avenue for between

US$400-500 million.

China Life Insurance has acquired 70% of an office

building along London’s Canary Wharf in a deal worth

US$1.35 billion.

Notable Real Estate Outbound Deals 2014

Page 13

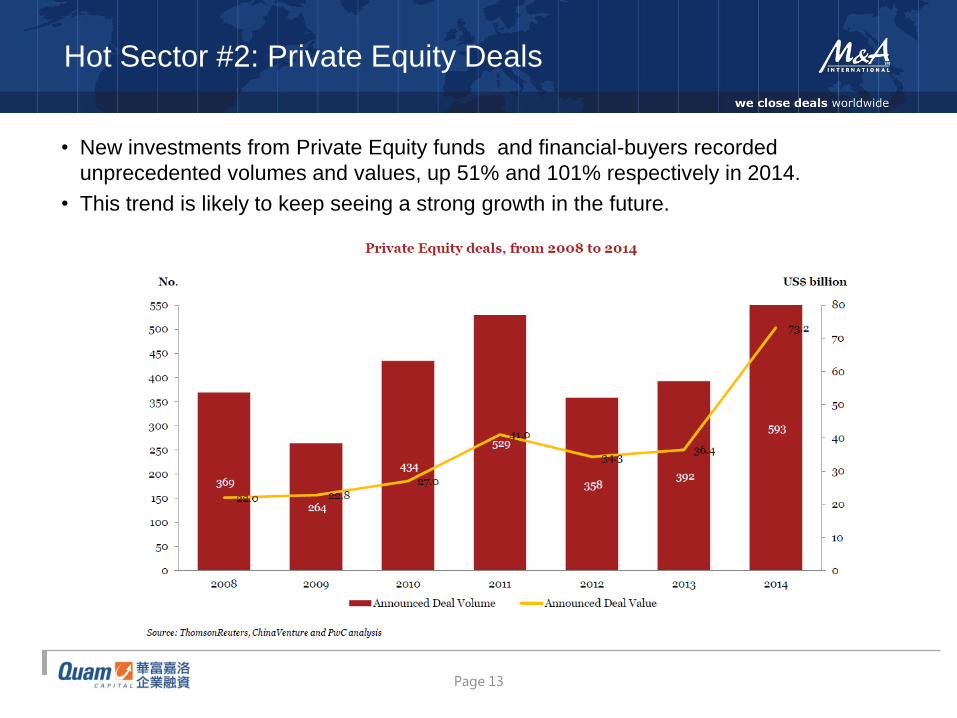

Hot Sector #2: Private Equity Deals

• New investments from Private Equity funds and financial-buyers recorded

unprecedented volumes and values, up 51% and 101% respectively in 2014.

• This trend is likely to keep seeing a strong growth in the future.

Page 14

Conclusions

• Outbound M&A could remain at a strong level

• Foreign inbound activity, though increased, remains at a modest level compared with

outbound activity

• Natural Resources, Brands, Technology, and Real Estate remain key focus areas of

Chinese companies acquiring overseas

• More private and medium size enterprises are

expected to acquire target overseas as

opposed to previous domination by large

corporations and state-owned enterprises

• Mid-market deals are relatively less vulnerable

to political interference, but completion is a key

area to improve

• President Xi Jinping foresees China’s

outbound investment to reach US$1.25 trillion

in the next decade

Strictly private & confidential

0, 0, 128

51, 102, 255

204, 229, 255

128, 100, 162

0, 117, 119

217, 217, 217

IFLR ASIA M&A FORUM

PANEL DISCUSSION MATERIALS

MARCH 10TH

0, 0, 128

51, 102, 255

204, 229, 255

128, 100, 162

0, 117, 119

217, 217, 217

Strictly Confidential 2

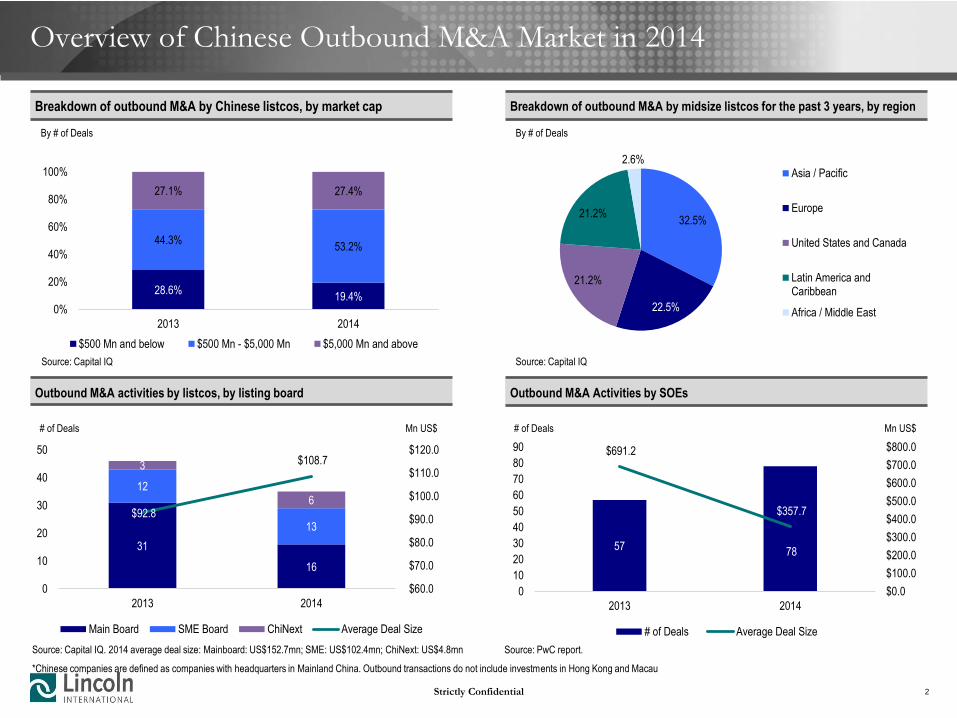

Overview of Chinese Outbound M&A Market in 2014

Breakdown of outbound M&A by Chinese listcos, by market cap Breakdown of outbound M&A by midsize listcos for the past 3 years, by region

28.6% 19.4%

44.3% 53.2%

27.1% 27.4%

0%

20%

40%

60%

80%

100%

2013 2014

$500 Mn and below $500 Mn - $5,000 Mn $5,000 Mn and above

32.5%

22.5%

21.2%

21.2%

2.6% Asia / Pacific

Europe

United States and Canada

Latin America andCaribbean

Africa / Middle East

57 78

$691.2

$357.7

$0.0

$100.0

$200.0

$300.0

$400.0

$500.0

$600.0

$700.0

$800.0

0

10

20

30

40

50

60

70

80

90

2013 2014

Outbound M&A activities by Chinese SOEs

# of Deals Average Deal Size

# of Deals Mn US$

Source: Capital IQ Source: Capital IQ

31

16

12

13

3

6 $92.8

$108.7

$60.0

$70.0

$80.0

$90.0

$100.0

$110.0

$120.0

0

10

20

30

40

50

2013 2014

Outbound M&A activities, by listing board

Main Board SME Board ChiNext Average Deal Size

# of Deals Mn US$

Source: Capital IQ. 2014 average deal size: Mainboard: US$152.7mn; SME: US$102.4mn; ChiNext: US$4.8mn

*Chinese companies are defined as companies with headquarters in Mainland China. Outbound transactions do not include investments in Hong Kong and Macau

Source: PwC report.

Outbound M&A activities by listcos, by listing board Outbound M&A Activities by SOEs

By # of Deals By # of Deals

0, 0, 128

51, 102, 255

204, 229, 255

128, 100, 162

0, 117, 119

217, 217, 217

Strictly Confidential 3

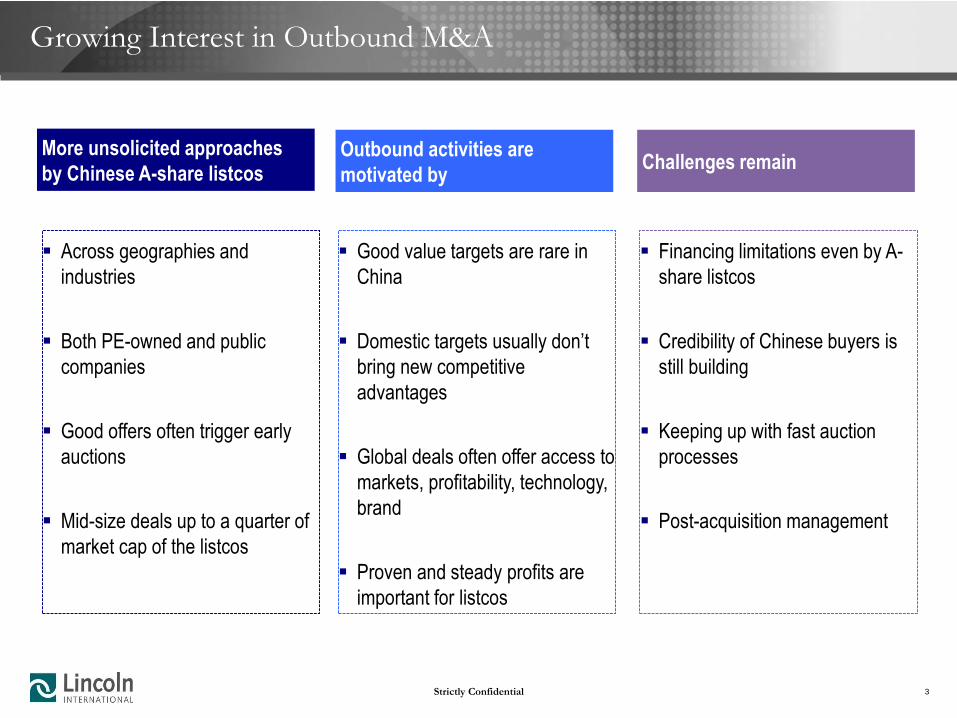

Growing Interest in Outbound M&A

More unsolicited approaches

by Chinese A-share listcos

Across geographies and

industries

Both PE-owned and public

companies

Good offers often trigger early

auctions

Mid-size deals up to a quarter of

market cap of the listcos

Outbound activities are

motivated by

Good value targets are rare in

China

Domestic targets usually don’t

bring new competitive

advantages

Global deals often offer access to

markets, profitability, technology,

brand

Proven and steady profits are

important for listcos

Challenges remain

Financing limitations even by A-

share listcos

Credibility of Chinese buyers is

still building

Keeping up with fast auction

processes

Post-acquisition management

0, 0, 128

51, 102, 255

204, 229, 255

128, 100, 162

0, 117, 119

217, 217, 217

Strictly Confidential 4

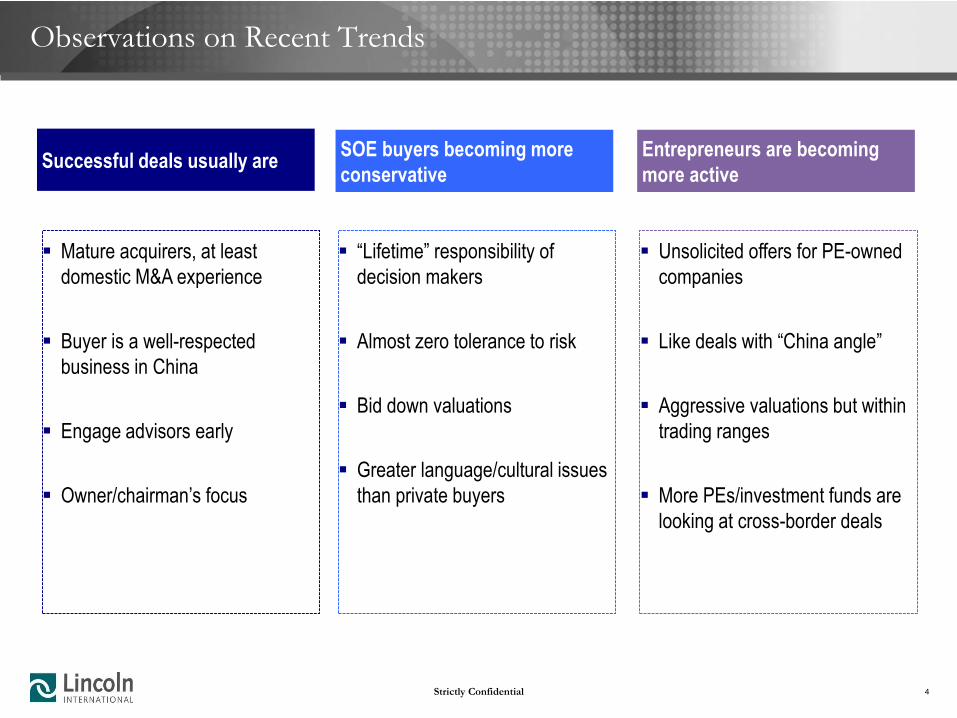

Observations on Recent Trends

Successful deals usually are

Mature acquirers, at least

domestic M&A experience

Buyer is a well-respected

business in China

Engage advisors early

Owner/chairman’s focus

SOE buyers becoming more

conservative

“Lifetime” responsibility of

decision makers

Almost zero tolerance to risk

Bid down valuations

Greater language/cultural issues

than private buyers

Entrepreneurs are becoming

more active

Unsolicited offers for PE-owned

companies

Like deals with “China angle”

Aggressive valuations but within

trading ranges

More PEs/investment funds are

looking at cross-border deals

Paul, Weiss, Rifkind, Wharton & Garrison LLP

China Outbound Investment – Regulatory Regime

March 2015

ASIA1: 3883195.1

Paul, Weiss, Rifkind, Wharton & Garrison LLP

Since December 2013, the PRC State Council, the PRC National Development and Reform Commission (“NDRC”), the PRC Ministry of Commerce (“MOFCOM”) and the PRC State Administration of Foreign Exchange (“SAFE”) issued various rules in respect of outbound investments.

These legislations superseded the previous regime for outbound investments that had been in place since 2004. They significantly reduced the scope of outbound investments that required approvals of State Council, NDRC and MOFCOM.

2

Overview

Paul, Weiss, Rifkind, Wharton & Garrison LLP

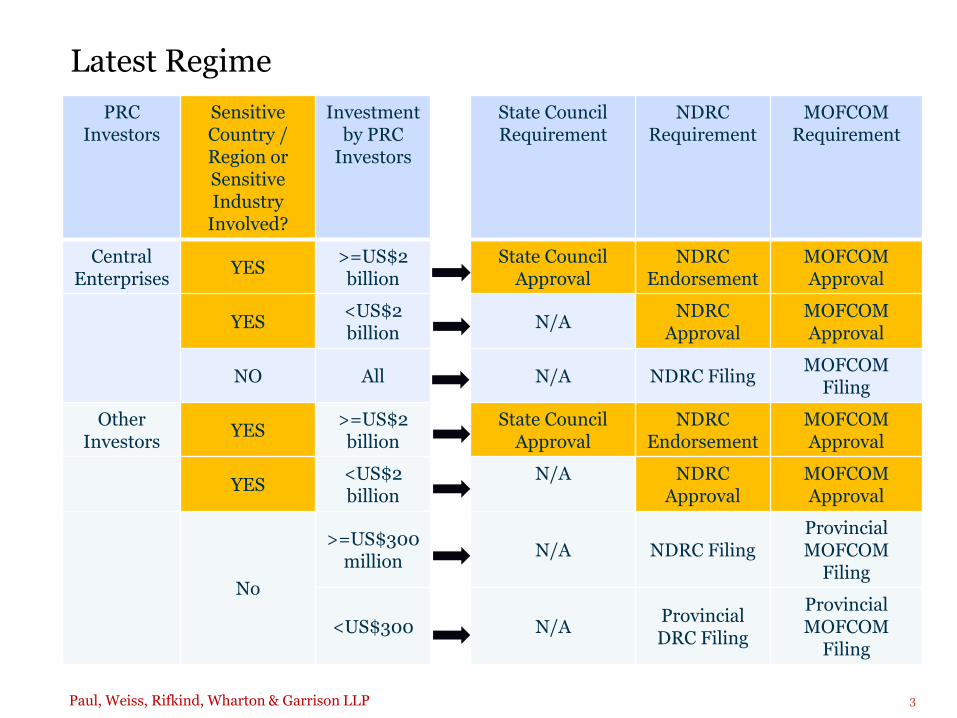

Latest Regime

3

PRC Investors

Sensitive Country / Region or Sensitive Industry

Involved?

Investment by PRC

Investors

State Council Requirement

NDRC Requirement

MOFCOM Requirement

Central Enterprises YES >=US$2

billion State Council

Approval NDRC

Endorsement MOFCOM Approval

YES <US$2 billion N/A NDRC

Approval MOFCOM Approval

NO All N/A NDRC Filing MOFCOM Filing

Other Investors YES >=US$2

billion State Council

Approval NDRC

Endorsement MOFCOM Approval

YES <US$2 billion

N/A

NDRC Approval

MOFCOM Approval

No

>=US$300 million N/A NDRC Filing

Provincial MOFCOM

Filing

<US$300 N/A Provincial DRC Filing

Provincial MOFCOM

Filing

Paul, Weiss, Rifkind, Wharton & Garrison LLP

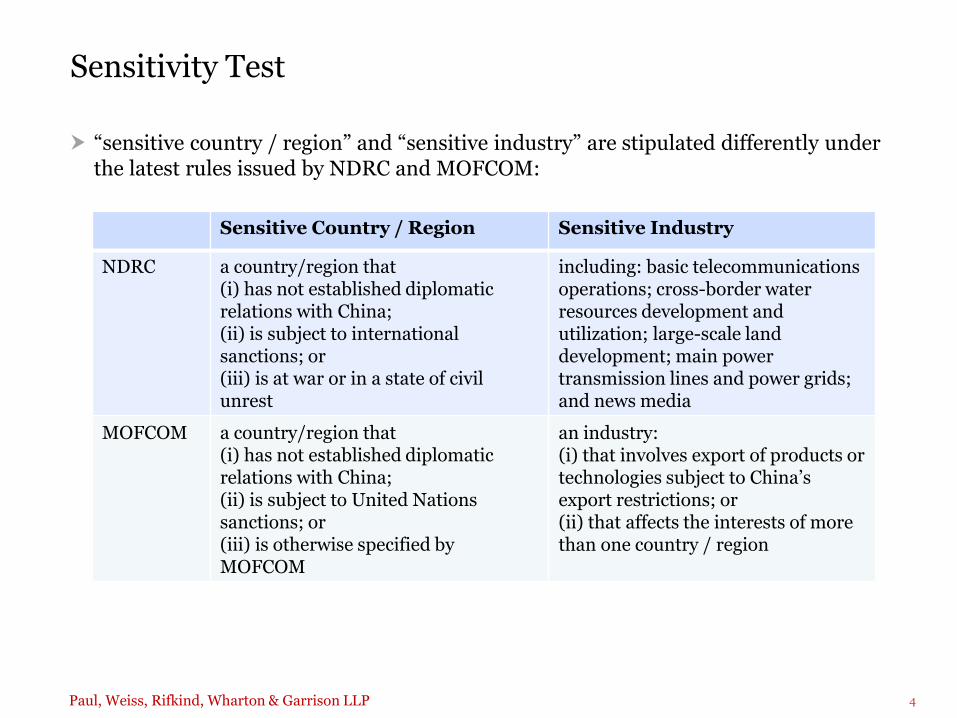

“sensitive country / region” and “sensitive industry” are stipulated differently under the latest rules issued by NDRC and MOFCOM:

Sensitivity Test

4

Sensitive Country / Region Sensitive Industry

NDRC a country/region that (i) has not established diplomatic relations with China; (ii) is subject to international sanctions; or (iii) is at war or in a state of civil unrest

including: basic telecommunications operations; cross-border water resources development and utilization; large-scale land development; main power transmission lines and power grids; and news media

MOFCOM a country/region that (i) has not established diplomatic relations with China; (ii) is subject to United Nations sanctions; or (iii) is otherwise specified by MOFCOM

an industry: (i) that involves export of products or technologies subject to China’s export restrictions; or (ii) that affects the interests of more than one country / region

Paul, Weiss, Rifkind, Wharton & Garrison LLP

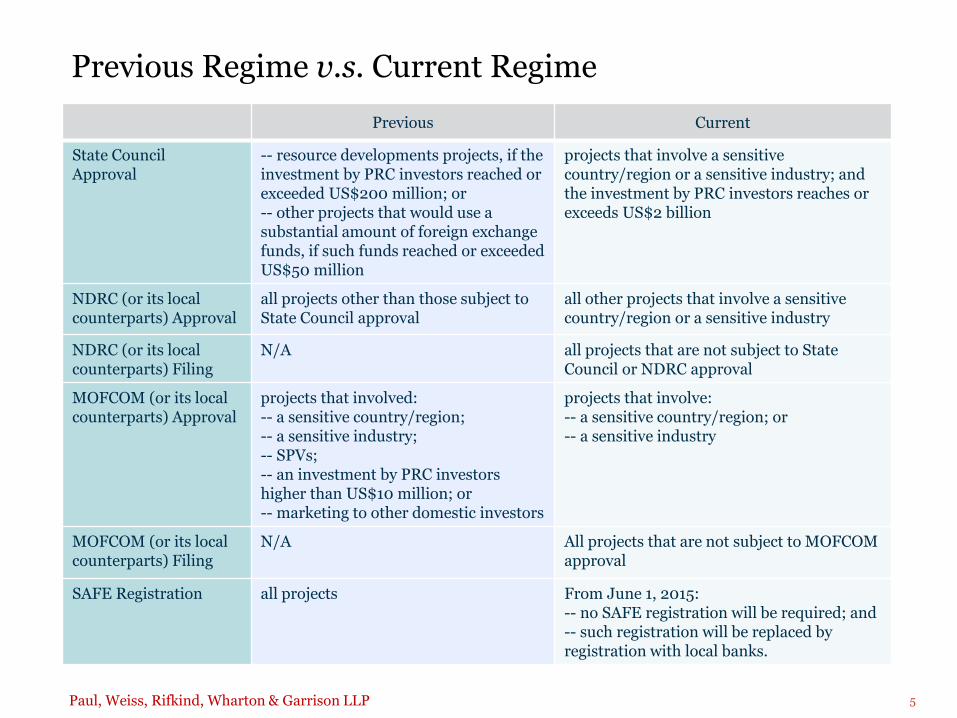

Previous Regime v.s. Current Regime

5

Previous Current

State Council Approval

-- resource developments projects, if the investment by PRC investors reached or exceeded US$200 million; or -- other projects that would use a substantial amount of foreign exchange funds, if such funds reached or exceeded US$50 million

projects that involve a sensitive country/region or a sensitive industry; and the investment by PRC investors reaches or exceeds US$2 billion

NDRC (or its local counterparts) Approval

all projects other than those subject to State Council approval

all other projects that involve a sensitive country/region or a sensitive industry

NDRC (or its local counterparts) Filing

N/A all projects that are not subject to State Council or NDRC approval

MOFCOM (or its local counterparts) Approval

projects that involved: -- a sensitive country/region; -- a sensitive industry; -- SPVs; -- an investment by PRC investors higher than US$10 million; or -- marketing to other domestic investors

projects that involve: -- a sensitive country/region; or -- a sensitive industry

MOFCOM (or its local counterparts) Filing

N/A All projects that are not subject to MOFCOM approval

SAFE Registration all projects From June 1, 2015: -- no SAFE registration will be required; and -- such registration will be replaced by registration with local banks.