Embed Size (px)

DESCRIPTION

CIMB

Citation preview

CIMBCIMBGateway to Southeast AsiaGateway to Southeast Asia

CIMB P t ti t E C fCIMB Presentation at Euromoney Conference

Beijing, 17 November 2010

Investing in Southeast Asian Quasi Sovereign Corporate Debt and Investing in Southeast Asian Quasi Sovereign, Corporate Debt and Sukuk Markets

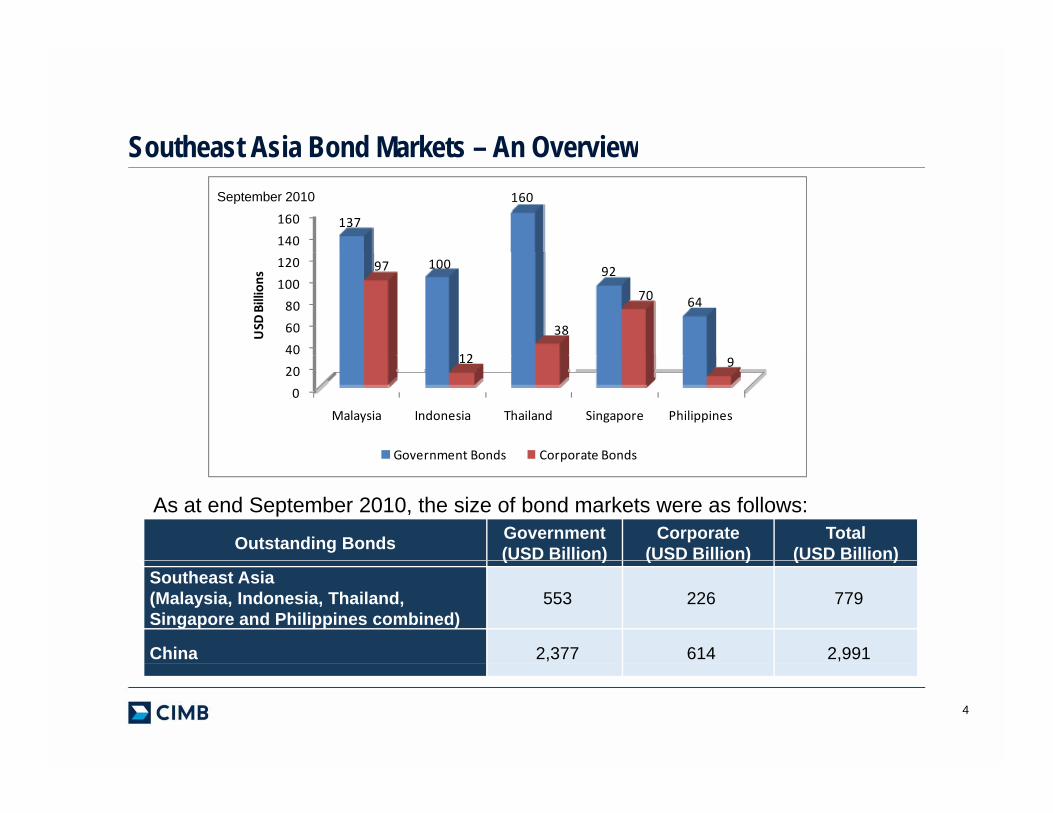

Southeast Asia Bond Markets – An OverviewSoutheast Asia Bond Markets – An Overview

140

160 137

160September 2010

40

60

80

100

120 100 92

64

97

12

38

70

USD

Billions

0

20

Malaysia Indonesia Thailand Singapore Philippines

12 9

Government Bonds Corporate BondsGovernment Bonds Corporate Bonds

As at end September 2010, the size of bond markets were as follows:

Outstanding Bonds Government(USD Billion)

Corporate(USD Billion)

Total(USD Billion)( ) ( ) ( )

Southeast Asia (Malaysia, Indonesia, Thailand, Singapore and Philippines combined)

553 226 779

China 2,377 614 2,991

4

Size of AAA and AA Rated (Local) Corporate Bonds Size of AAA and AA Rated (Local) Corporate Bonds MALAYSIA (Approx. USD65.75 Billion) INDONESIA (Approx. USD6.33 Billion)

SINGAPORE* (Approx. USD44.57 Billion) THAILAND (Approx. USD15.52 Billion)

Source: Bloomberg, 31October 2010 and based on exchange rate RM3.09:USD1.00 Source: Bloomberg, 31 October 2010 and based on exchange rate IDR8,908:USD1.00

Source: Bloomberg, 31 October 2010 and based on exchange rate THB2,965:USD1.00Source: Bloomberg, 31 October 2010 and based on exchange rate SGD1.29:USD1.00

5

g, g ,g g*Total Corporate Bonds issued for all rating scales. Note that most of the issuers are non-rated.

Legal FrameworkLegal Framework

Malaysia Indonesia Singapore Thailand

RegulatorSecurities

Commission Malaysia (“SC”)

Badan Pengawas Pasar Modal dan

Lembaga Keuangan

(“Bapepam-LK”)

Monetary Authority of Singapore

(“MAS”)

Securities and Exchange

Commission

Bonds Regulations

•Securities Commission Act 1993, replaced by Capital Markets and Services Act 2007

Undang-Undang Republik Indonesia

Nomor 8 Tahun 1995

Securities & Futures Act (Cap. 289)

Securities and Exchange Act

B.E.2535(A.D.1992)Services Act 2007

Is there trust law? Yes No Yes Yes

Are thereYes

•Companies Act Yes Yes•Companies Act

Yes•Bankruptcy Act Are there

bankruptcy & liquidation laws?

Companies Act 1965• Bankruptcy Act 1967

•Undang-undang Nomor 4 tahun 1998 (Bankruptcy)

Companies Act (Cap. 50) •Bankruptcy Act (Cap. 20)

B.E.2483 (A.D.1940)Amended up to Bankruptcy Act No.7 B.E.2547 (A.D.2004)

6

Rating Requirement & Rating AgenciesRating Requirement & Rating Agencies

Malaysia Indonesia Singapore Thailand

CompulsoryCompulsory Rating Requirement

Yes Yes Not required Yes

•RAM Rating • PT Pemeringkat

Local Rating Agencies

Services Berhad (“RAM”)

•Malaysian Rating

Efek Indonesia (“Pefindo”)

• PT Fitch Ratings Indonesia (“Fitch

Not available

• TRIS Rating Co. Ltd (“TRIS”)

• Fitch (Thailand)Rating Corporation Berhad (“MARC”)

Indonesia ( Fitch Indonesia”)

7

Average Annual Rating Migration – Malaysia (1992 – 2009) - RAMAverage Annual Rating Migration – Malaysia (1992 – 2009) - RAM

Rating (From/To)

(%)AAA AA A BBB BB B CCC D

iAAA 98.39 1.61 0.00 0.00 0.00 0.00 0.00 0.00

AA 1.62 94.65 2.43 0.97 0.16 0.00 0.16 0.00

A 0.13 4.05 87.99 6.45 0.25 0.25 0.00 0.88

BBB 0.20 0.61 5.73 79.96 9.82 1.23 1.02 1.43

BB 0.00 0.00 0.51 7.69 70.26 7.69 3.59 10.26

B 0.00 0.00 0.00 0.00 6.25 84.38 5.21 4.17

C 0.00 0.00 3.45 0.00 0.00 0.00 58.62 37.93

Source: RAM, April 2010

8

Average Annual Rating Migration – Indonesia (1996 – 2009) - PefindoAverage Annual Rating Migration – Indonesia (1996 – 2009) - Pefindo

Rating (From/To)

(%)idAAA idAA idA idBBB idBB idB idCCC idD NR

iidAAA 73.33 0.00 0.00 0.00 0.00 0.00 0.00 0.00 26.67

idAA 4.49 77.53 5.62 0.00 1.12 0.00 0.00 1.12 10.11

idA 0.28 6.41 73.26 1.95 0.56 0.00 0.00 2.51 15.04

idBBB 0.00 0.54 8.13 48.78 3.52 0.81 1.63 6.50 30.08

idBB 0.00 0.00 0.00 6.60 12.26 2.83 2.83 16.98 58.49

idBBB 0.00 0.00 0.00 4.35 13.04 39.13 4.35 21.74 17.39

idCCC 0.00 0.00 0.00 7.69 0.00 7.69 0.00 0.00 15.38

Source: Pefindo, April 2010

9

Average Annual Rating Migration – Thailand (2002 – 2009) - FitchAverage Annual Rating Migration – Thailand (2002 – 2009) - Fitch

Rating (From/To)

(%)AAA(tha) AA(tha) A(tha) BBB(tha) BB(tha) B(tha) CCC to

C(tha) D(tha) Total

AAA(tha) 100.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 100.00

AA(tha) 3.92 96.08 0.00 0.00 0.00 0.00 0.00 0.00 100.00

A(tha) 0.00 2.30 94.25 3.45 0.00 0.00 0.00 0.00 100.00

BBB(tha) 0.00 0.00 10.91 87.27 1.82 0.00 0.00 0.00 100.00

BB(tha) 0.00 0.00 0.00 33.33 66.67 0.00 0.00 0.00 100.00

B(tha) 0.00 0.00 0.00 0.00 100.00 0.00 0.00 0.00 100.00

CCC to C(tha) 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

Source: Fitch Thailand, July 2010

10

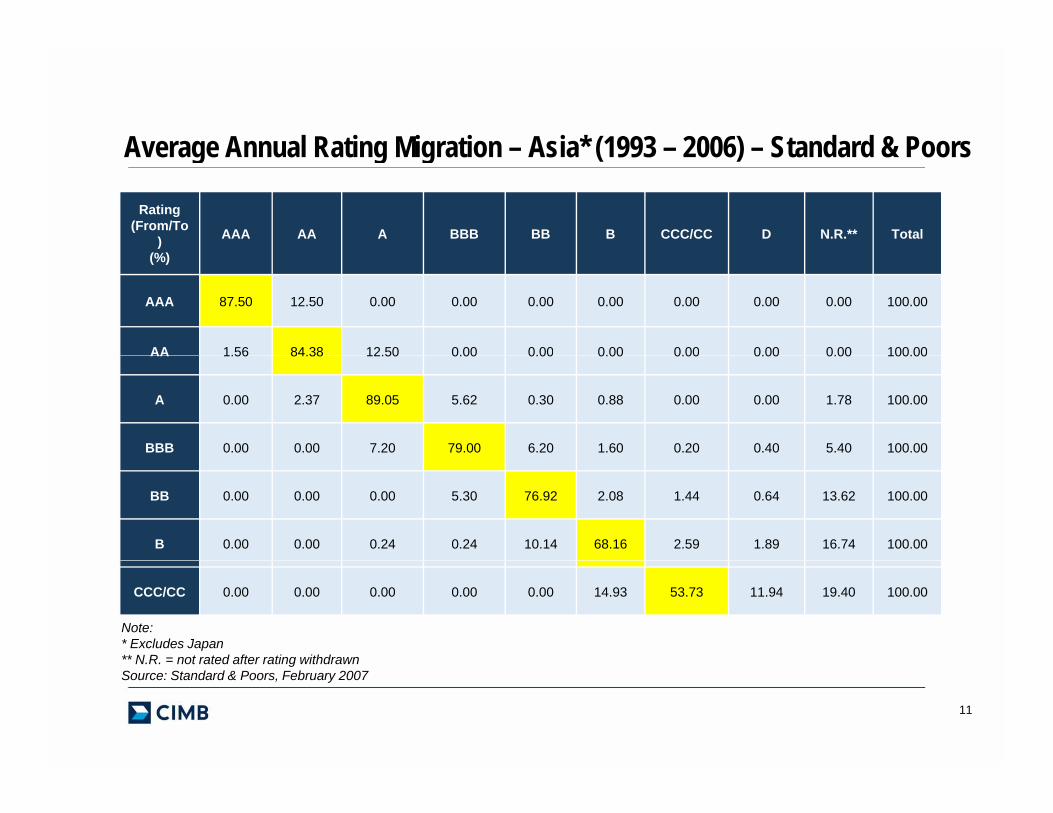

Average Annual Rating Migration – Asia* (1993 – 2006) – Standard & PoorsAverage Annual Rating Migration – Asia (1993 – 2006) – Standard & Poors

Rating (From/To

)(%)

AAA AA A BBB BB B CCC/CC D N.R.** Total

(%)

AAA 87.50 12.50 0.00 0.00 0.00 0.00 0.00 0.00 0.00 100.00

AA 1.56 84.38 12.50 0.00 0.00 0.00 0.00 0.00 0.00 100.00AA 1.56 84.38 12.50 0.00 0.00 0.00 0.00 0.00 0.00 100.00

A 0.00 2.37 89.05 5.62 0.30 0.88 0.00 0.00 1.78 100.00

BBB 0.00 0.00 7.20 79.00 6.20 1.60 0.20 0.40 5.40 100.00

BB 0.00 0.00 0.00 5.30 76.92 2.08 1.44 0.64 13.62 100.00

B 0.00 0.00 0.24 0.24 10.14 68.16 2.59 1.89 16.74 100.00

CCC/CC 0.00 0.00 0.00 0.00 0.00 14.93 53.73 11.94 19.40 100.00

Note: * Excludes Japan** N.R. = not rated after rating withdrawn N.R. not rated after rating withdrawnSource: Standard & Poors, February 2007

11

In ConclusionIn Conclusion…Local Currency Corporate Bonds in South East Asia are…

sizable

with well tested legal framework

& of high credit quality& of high credit quality

Source of Credit InformationSource of Credit Information

Malaysia Indonesia Singapore Thailand

Are information memorandum or offering circulars available?

Yes Yes Yes Yes

available?

Are there credit research by investment b k ?

Yes Yes Yes Yes

banks?

Website

•Securities Commission

•RAM • Pefindo • S&P • Moody’s

•The Thai Bond Market Association

•Securities and Exchangesources RAM

•MARC • Fitch Indonesia • Fitch Exchange Commission

•TRIS and Fitch Thailand

13

Taxation on Non-Resident Investors on Local Currencies Government and Corporate Bondson Local Currencies Government and Corporate Bonds

Malaysia Indonesia Singapore Thailand

Withholding tax (“WHT”) on Interest Income from Government Bonds

Exempted Yes Exempted Yes

Exempted if derived from Exempted if derivedWHT on Interest Income from Corporate Bonds

Exempted if derived from bonds approved by

Securities CommissionYes

Exempted if derived from Qualifying Debt

SecuritiesYes

15% 20% 15% 15%

Based on the Double Taxation Agreement (“DTA”) between China and Malaysia IndonesiaWHT rate on interest income (if applicable)

Based on the Double Taxation Agreement ( DTA ) between China and Malaysia, Indonesia, Singapore and Thailand respectively:

• The WHT rate for interest would be reduced to a maximum 10%. However, this would not apply if the non-resident has a permanent establishment in the respective countries.

Capital Gains Tax Not subject to tax Yes, 20% * Not subject to tax Yes, 15%

* Pursuant to China-Indonesia DTA, the capital gain tax is only taxable in country where the investor is resident

14

5-year CNY/MYR, CNY/IDR, CNY/SGD, CNY/THB Index5 year CNY/MYR, CNY/IDR, CNY/SGD, CNY/THB Index

CNY/MYR CNY/IDR CNY/SGD CNY/THB

110.00

120.00

130.00

80 00

90.00

100.00

60.00

70.00

80.00

50.00Jan-05 Jul-05 Jan-06 Jul-06 Jan-07 Jul-07 Jan-08 Jul-08 Jan-09 Jul-09 Jan-10 Jul-10

15

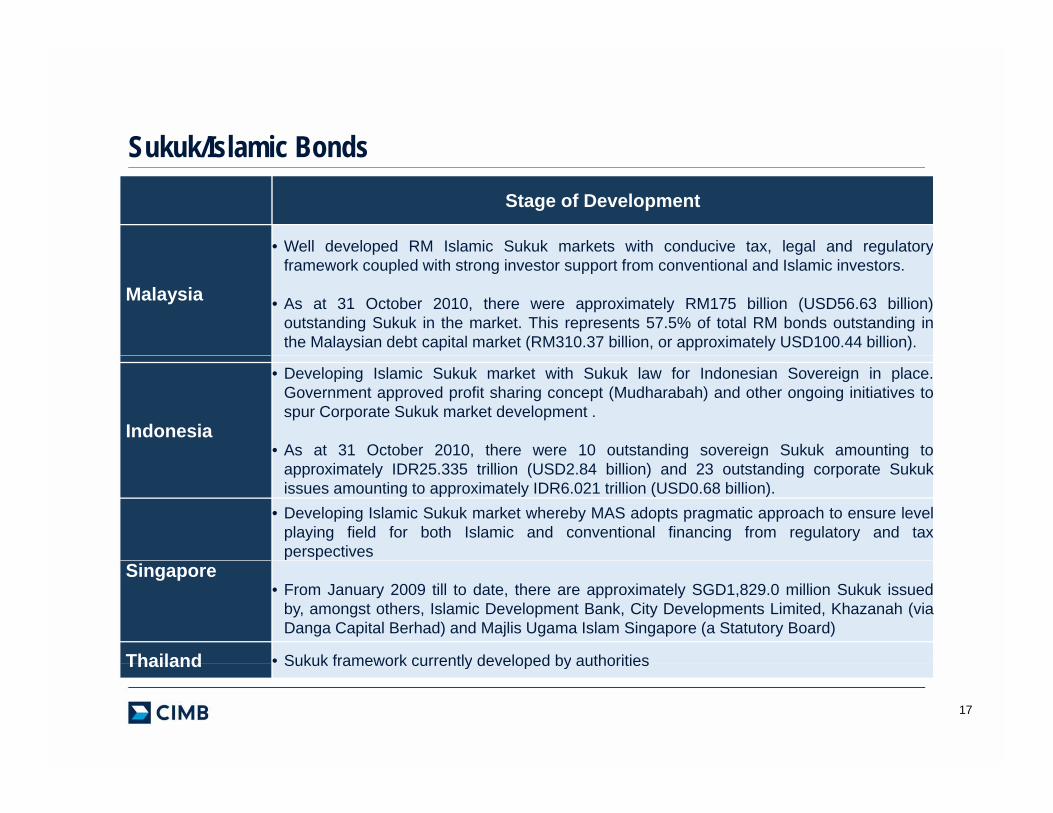

Sukuk/Islamic BondsSukuk/Islamic Bonds

C i l S k k

• Sukuk are Syariah Compliant Bonds

• No Interest

• Underlying

Conventional Sukuk

• Underlying Asset/business is Syariah compliant

Bondholders Sukuk Holders

• The difference is in the way indebtedness is created

Interest Rental/Profit

• All the rights of the investors are the same

Borrowed Money Asset/Business

Sukuk/Islamic BondsSukuk/Islamic BondsStage of Development

• Well developed RM Islamic Sukuk markets with conducive tax, legal and regulatory

Malaysia

p , g g yframework coupled with strong investor support from conventional and Islamic investors.

• As at 31 October 2010, there were approximately RM175 billion (USD56.63 billion)outstanding Sukuk in the market. This represents 57.5% of total RM bonds outstanding inthe Malaysian debt capital market (RM310.37 billion, or approximately USD100.44 billion).

Indonesia

• Developing Islamic Sukuk market with Sukuk law for Indonesian Sovereign in place.Government approved profit sharing concept (Mudharabah) and other ongoing initiatives tospur Corporate Sukuk market development .

• As at 31 October 2010, there were 10 outstanding sovereign Sukuk amounting tog g gapproximately IDR25.335 trillion (USD2.84 billion) and 23 outstanding corporate Sukukissues amounting to approximately IDR6.021 trillion (USD0.68 billion).

• Developing Islamic Sukuk market whereby MAS adopts pragmatic approach to ensure levelplaying field for both Islamic and conventional financing from regulatory and taxperspectives

Singapore• From January 2009 till to date, there are approximately SGD1,829.0 million Sukuk issued

by, amongst others, Islamic Development Bank, City Developments Limited, Khazanah (viaDanga Capital Berhad) and Majlis Ugama Islam Singapore (a Statutory Board)

Thailand • Sukuk framework currently developed by authoritiesThailand Sukuk framework currently developed by authorities

17

Analysis of the Global Sukuk MarketNew Global Sukuk Issues by Country: Jan to Oct 2010

Analysis of the Global Sukuk Market

35

New Global Sukuk Issues by Value Others9.3%Singapore

0.6%

Saudi Arabia9.8%

Bahrain3.5%

31.6

25

30

35

USD

Billions

Malaysia

UAE17.8%

Indonesia4.1%

18.0

15.7

21.5

13.815

20

y54.9%

Outstanding Global Sukuk as at 31 October 2010

8.7

5

10

Saudi Arabia13 1%

Others7.2%

Bahrain2.5%

Indonesia1.6%

Singapore0.1%

0

2005 2006 2007 2008 2009 2010 Malaysia54.4%UAE

21.1%

13.1%

Source: Bloomberg

18

DisclaimerDisclaimerThis presentation was prepared exclusively by CIMB Investment Bank Berhad (“CIMB”) exclusively for information and discussion purposes only. In preparing this presentation, we have relied upon and assumed, without independent verification, the accuracy and completeness of all p , p , y pinformation available from public sources or which was provided to us by or on behalf of CIMB or which was otherwise reviewed by us.

CIMB is not acting as an advisor or agent to any person to whom this presentation is directed. S h t k th i i d d t t f th t t f thi t tiSuch persons must make their own independent assessment of the contents of this presentation, should not treat such content as advice relating to legal, accounting, taxation or investment matters and should consult their own advisers.

Neither CIMB nor its directors officers or employees make any guarantee representation orNeither CIMB, nor its directors, officers or employees make any guarantee, representation or warranty, express or implied, as to the adequacy, accuracy, completeness, reliability or fairness of any such information and accordingly, neither CIMB nor its directors, officers or employees shall be liable in any manner whatsoever for any consequences (including but not limited to any direct, indirect or consequential losses, loss of profits and damages) of any reliance thereon or

th fusage thereof.

This presentation may not be copied, duplicated, reproduced or redistributed, in whole or in part by any means, without the prior written permission of CIMB. CIMB and its affiliates accepts no liability whatsoever for the actions of any party in this respectliability whatsoever for the actions of any party in this respect.

THANK YOU

20