Embed Size (px)

Citation preview

Morning Notes China/Hong Kong

China & HK Research Team (852) 2600 8593 Monday, 04 November 2013

Please see important notice on last page Page 1 of 2

Find CLSA research on Bloomberg, Thomson Reuters, CapIQ and themarkets.com - and profit from our evalu@tor proprietary database at clsa.com

Conviction calls

Ticker Company Rec Target

return P/E(x) EPSg(%) Yield(%) P/B(x) ROE(%) 1M YTD

BIDU US Baidu BUY 31 26.2 21.9 0.0 6.9 30.3 0.1 59.6

293 HK Cathay Pacific BUY 16 9.6 114.3 4.2 1.0 10.4 0.6 9.0

1 HK Cheung Kong BUY 20 9.1 11.7 3.0 0.7 8.5 (0.2) 2.9

2007 HK Country Garden BUY 36 6.6 39.8 5.7 1.5 25.6 4.9 31.8

CTRP US Ctrip BUY 8 42.2 27.0 0.0 4.7 12.1 (8.3) 142.4

992 HK Lenovo BUY 7 15.8 13.8 2.6 3.5 24.8 4.2 20.2

MPEL US Melco Crown BUY 26 23.4 32.3 0.0 3.7 17.2 1.6 98.3

NTES US NetEase BUY 26 10.2 17.4 2.5 2.3 25.3 (7.4) 57.7

3968 HK CMB SELL (13) 5.9 5.1 4.2 1.0 18.1 8.5 (10.2)

1072 HK Dongfang SELL (25) 12.3 (12.3) 1.1 1.1 9.2 13.4 (17.9)

2727 HK Shanghai Electric SELL (17) 12.5 (4.5) 2.4 0.8 6.7 (0.7) (17.8)

3 HK HK & China Gas SELL (10) 25.9 5.6 2.1 3.4 13.4 (2.8) (5.3)

Performance(%)Valuations 14CL

MSCI China vs MSCI Asia ex-Japan

China & HK Indices

Last 1D 1M 3M

HSCEI 10,679 0.5 1.5 9.7

HSCCI 4,537 (0.3) 0.8 9.0

Shanghai A 2,250 0.4 (1.2) 5.9

Shanghai B 249 (0.0) (1.3) 3.8

Shenzhen A 1,061 (0.4) (3.8) 4.2

Shenzhen B 834 0.6 0.8 6.4

HSI 23,250 0.2 0.5 4.8

Finance 32,405 0.2 1.4 3.7

Properties 30,164 0.6 (1.6) 0.2

Utilities 50,060 (0.0) (1.5) (5.7)

Comm & Ind. 13,604 0.1 0.2 8.8

Yesterday's top five gainers and losers

% change

Top gainers Ticker 1D 1M YTD

Future Bright 703 HK 9.7 29.1 170.6

China Taiping 966 HK 7.3 11.3 (17.3)

Tingyi 322 HK 6.4 16.7 8.1

EVA Precision 838 HK 6.3 13.5 (6.3)

Gome 493 HK 5.0 20.0 37.0

Top losers

Shanda Games GAME US (4.5) 6.3 39.1

Antonoil 3337 HK (4.3) (7.3) 14.7

GCL-Poly 3800 HK (2.5) (4.5) 48.7

Techtronic 669 HK (2.4) (6.4) 32.6

Hysan 14 HK (2.2) 2.5 (4.8)

Upcoming Key Economic Data

05-Nov Oct

08-Nov Oct

09-Nov Oct

09-Nov Oct

09-Nov Oct

09-Nov Oct

Upcoming CLSA Events

15Oct - 4 Nov HK

4-5 Nov HK

28 Oct - 5 Nov HK

31 Oct-1 Nov SG

31 Oct-1 Nov HK

HSI vs CSI300 vs HSCEI

Consumer Price Index

Asia Transportation roadshow - Paul Wan

e-normous - Paul McKenzie

HK Banks - A City of Two Tales - Derek Ovington

% change

HSBC Services PMI

Import & Export Trade

Fixed Assets Investment

Korean Conglomerates & Construction - Steve Chung

Gaming & Consumer Roadshow - Aaron Fischer

Producer Price Index

Retail Sales Value

(25)

(20)

(15)

(10)

(5)

0

5

10

15

20

25

Nov-12 Feb-13 May-13 Aug-13

Hang Seng

HSCEI

CSI 300

(%)

(20)

(15)

(10)

(5)

0

5

10

15

Nov-12 Feb-13 May-13 Aug-13

MSCI China

MSCI Asia x Japan

(%) What’s inside: Sector Outlook. China Property Sector. Untightening.

ASM Pacific (522 HK - BUY). A Mixed Bag.

Sector Outlook. China Property Sector. Untightening.

We expect more stable policy environment, and hence better growth visibility for listed developers after the Third Plenary Meeting. Trading at an average

6.3x FY14 PE despite an average 25% net profit growth, the sector looks due for a re-rating and we reiterate OVERWEIGHT. Our top picks: Country Garden for its sustainable high growth and COLI for potentially earnings accretive asset injection.

ASM Pacific (522 HK - BUY). A Mixed Bag.

3Q13 results were a mixed bag. Share gains in semi and SMT equipment allay concerns of structural loss in competitiveness. In semi equipment, ASM’s sales declines was -6% YoY (1Q-3Q13) vs -7% for BESI, -41% for K&S. In SMT, ASM’s sales grew 5% YoY in 1Q-3Q13 vs Fuji’s 32% YoY drop. However, margins are faring worse, notably in SMT where Japanese rivals are aided by a weak yen. We cut our margin forecasts to reflect this. The stock

trading at low end of P/BV range appears to have priced in the negatives. Steps ASM is taking –a more flexible cost structure, leadership in next generation technology –have us keeping BUY.

News headlines China Services Index Rises to Year’s High in Rebound Sign A Chinese services-industry index rose to the highest level this year, adding to evidence the nation’s economic rebound is sustaining momentum as leaders prepare to map out a blueprint for reform. - Bloomberg Manufacturing Strengthens From China to South Korea Manufacturing strengthened from China to South Korea last month in a sign that growth risks are abating in Asia and expansion may pick up this quarter. - Bloomberg Macau Casino Revenue Rises to Record in October Macau casino revenue jumped 32% to a record of 36.5 billion patacas (US$4.57 billion) in October, boosted by mainland Chinese visitors who spent their Golden Week holiday in the world’s largest gambling hub. - Bloomberg

Home prices still rising in major cities Some top-tier cities are likely to miss targets set at the beginning of the year to stabilize home prices, as prices in China's 100 major cities continued to rise in October, a survey showed. - China Daily China, US 'ready to engage' on TPP talks China and the United States strongly intend to engage each other in the Trans-Pacific Partnership, a "high-standard" trade agreement involving the US and other countries including Japan and Australia, according to insiders close to both governments. – China Daily

Prepared for: [email protected] FIRST LAST 11/04/13 12:33:55 AM Samsung Information Systems of

Morning Notes - China/Hong Kong

Page 2 of 2

Find CLSA research on Bloomberg, Thomson Reuters, CapIQ and themarkets.com - and profit from our evalu@tor proprietary database at clsa.com

Research subscriptions To change your report distribution requirements, please contact your CLSA sales representative or email us at [email protected].

You can also fine-tune your Research Alert email preferences at https://www.clsa.com/member/tools/email_alert/.

Key to CLSA/CA Taiwan investment rankings: BUY: Total return expected to exceed market return AND provide 20% or greater absolute

return; O-PF: Total return expected to be greater than market return but less than 20% absolute return; U-PF: Total return expected to be less

than market return but expected to provide a positive absolute return; SELL: Total return expected to be less than market return AND to provide a

negative absolute return. For relative performance, we benchmark the 12-month total return (including dividends) for the stock against the 12-month forecast return (including dividends) for the local market where the stock is traded. We define stocks we expect to provide returns of 100%

or higher including dividends within three years as “Double Baggers”.

©2013 CLSA Limited (for research compiled by non-Taiwan analyst(s)) and/or Credit Agricole Securities Taiwan Co., Ltd (for research

compiled by Taiwan analyst(s)). Note: In the interests of timeliness, this document has not been edited.

The analyst/s who compiled this publication/communication hereby state/s and confirm/s that the contents hereof truly reflect his/her/their views and opinions on the subject matter and that the analyst/s has/have not been placed under any undue influence, intervention or pressure by any person/s in

compiling such publication/communication.

CLSA group of companies (excluding CLSA Americas, LLC) (“CLSA”), Credit Agricole Securities Taiwan Co., Ltd. (“CA Taiwan”), CLSA/CA Taiwan's

analysts and/or their associates do and from time to time seek to establish business or financial relationships with companies covered in their

research reports. As a result, investors should be aware that CLSA and/or such individuals may have one or more conflicts of interests that could

affect the objectivity of this report. Regulations or market practice of some jurisdictions/markets prescribe certain disclosures to be made for

certain actual, potential or perceived conflicts of interests relating to research reports and such details are available at

www.clsa.com/member/research_disclosures/. Disclosures therein include the position of CLSA, CLSA Americas, LLC and CA Taiwan only and do not reflect those of CITIC Securities International Company Limited, Credit Agricole Corporate & Investment Bank and/or their respective affiliates. If

investors have any difficulty accessing this website, please contact [email protected] or +852 2600 8111. If you require disclosure information

on previous dates, please contact [email protected]

IMPORTANT: The content of this report is subject to and should be read in conjunction with the disclaimer and CLSA's Legal and Regulatory Notices as set

out at www.clsa.com/disclaimer.html, a hard copy of which may be obtained on request from CLSA Publications or CLSA Compliance Group (18/F, One Pacific Place, 88 Queensway, Hong Kong, telephone +852 2600 8888) and/or CA Taiwan Compliance (27/F, 95, Section 2 Dun Hua South Road, Taipei

10682, Taiwan, telephone +886 2 2326 8188). 05/08/2013

Prepared for: [email protected] FIRST LAST 11/04/13 12:33:55 AM Samsung Information Systems of

China PropertySector outlook

Find CLSA research on Bloomberg, Thomson Reuters, CapIQ and themarkets.com - and profit from our evalu@tor proprietary database at clsa.com

Nicole [email protected]+852 2600 8207

Susanna Leung+852 2600 8597

Jackson Hui+852 2600 8723

4 November 2013

ChinaProperty

Country Garden (2007 HK)Rec: BUYTarget price: HK$7.0Upside: +32%

COLI (688 HK)Rec: BUYTarget price: HK$31.4Upside:+31%

Evergrande (3333 HK)Rec: U-PFTarget price: HK$3.60Upside: +10%

www.clsa.com

UntighteningWe expect more stable policy environment, and hence better growth visibility for listed developers after the Third Plenary Meeting. Trading at an average 6.3x FY14 PE despite an average 25% net profit growth, the sector looks due for a re-rating and we reiterate OVERWEIGHT. Our top picks: Country Garden for its sustainable high growth and COLI for potentially earnings accretive asset injection.

A different approachq In the past 5 years the China property market was characterized by sharp policy

swings: from tightening in 2007-2008, to loosening in 2009, to tightening in 2010-2011, to loosening in 2012, to a “false” tightening in Feb 2013.

q We believe such days of sharp policy swings are due for an overhaul as these swings disrupt supply and causes more harm than good over the long term. We expect “untightening” to replace the previous tightening/loosening cycles with emphasis shifting from direct intervention measures to use of market tools such as tax and credit control, the shift away from direct invention being unspoken and hence the sector re-rating to happen over subtle signals.

q Bridging measures may be seen in selective markets with sharp supply/demand mismatch (recent measures in Shenzhen and Beijing are examples) but we expect no nation-wide application.

Three key property focus measures in Third Plenary Meetingq Property tax – neutral to positive: has been expected for years and the actual

implementation actually removes overhang. We expect the tax will be set low initially to gain acceptance.

q Land supply increase – positive: the new government may emphasize a steady land supply which will make land replenishment easier for developers.

q Subsidized social housing - positive: We believe will relieve social pressure on private developers.

BUY Country Garden – almost a COLIq We raised our Country Garden FY13 contract sale forecast by 7% on 30 Oct to

RMB90bn on back of strong launches and sale in Sep and Oct.q The point to note here is that this number is an equivalence of COLI’s (also a BUY)

FY12 contract sale (HK$112bn or RMB91bn).q Only three years ago in FY10, CG’s contract sale at RMB32.9bn was just 56% of

COLI’s HK$67.1bn or RMB58.4bn. q We believe this is result of Country Garden’s successful entry into less competitive

markets in lower tier two and upper tier three cities, which offers ample room for growth.

q This growth model will be replicable in more markets and with FY13 new start likely up 41% plus y-y and land acquisition in 1H13 (12.97mn sqm) already almost equal to FY12 (15.6mn sqm) FY13 will certainly not be the last year of high growth for CG. Our target price of HK$7 is based on 8.5x FY14CL PER and suggests 31% upside. Conviction BUY.

BUY COLI – Change under wayq We are also BUYer of COLI where we expect 25% earnings CAGR for the next three

years with construction new start in FY13 expected to increase 21% plus y-y, and YTD Sep land acquisition already up 155% y-y (Report link: Coli - BUY (Change under way)).

q The above is before we consider the asset injection program from parent company CSCEC.

q We believe COLI is beginning to take over some CSCEC projects. In the best case scenario, the asset injection may happen in 1H14 and COLI may lift its scale of sale by 15% given CSCEC’s scale of sale in FY12 was about 25% of COLI’s and COLI is likely to cherry pick 30-50% of CSCEC’s projects.

q Our target price of HK$31.4 is set at 10x FY14 PE (par to 5-year historic average) and also suggests 31% upside. BUY.

Prepared for: [email protected] FIRST LAST 11/04/13 12:33:55 AM Samsung Information Systems of

Untightening China Property

4 November 2013 [email protected] 2

A different approachIn the past 5 years the China property market was characterized by sharp policy swings: from tightening in 2007-2008, to loosening in 2009, to tightening in 2010-2011, to loosening in 2012, to a “false” tightening in Feb 2013. We believe such days of sharp policy swings are due for an overhaul as these swings disrupt supply and causes more harm than good over the long term. We expect “untightening” to replace the previous tightening/loosening cycles with emphasis shifting from direct intervention measures to use of market tools such as tax and credit control. Bridging measures may be seen in selective markets with sharp supply/demand mismatch (tier one cities for example) but we expect no nation-wide application.

Property tax – will likely be rolled out in more cities. CLSA’s view: neutral to positive. As we believe the key objective is to establish a recurrent income base for local governments we believe the tax will likely be set low in order to gain acceptance. The announcement of actual implementation of property tax, which has been a worry of the market for more than five years, could hence be a removal of an overhang.

Land supply – aiming at steady supply. CLSA’s view: positive. A steady land supply will make land replenishment easier and also reduce volatility in land price and hence reduce operational risk of developers.

Subsidized social housing: on 29 Oct President Xi reiterated the target to build 36mn social housing flats between 2010-15 remains unchanged and the goal is to have 20% of households accommodated in such housing by 2015.CLSA’s view: positive. The increase in social housing will relief the social pressure on the private property market.

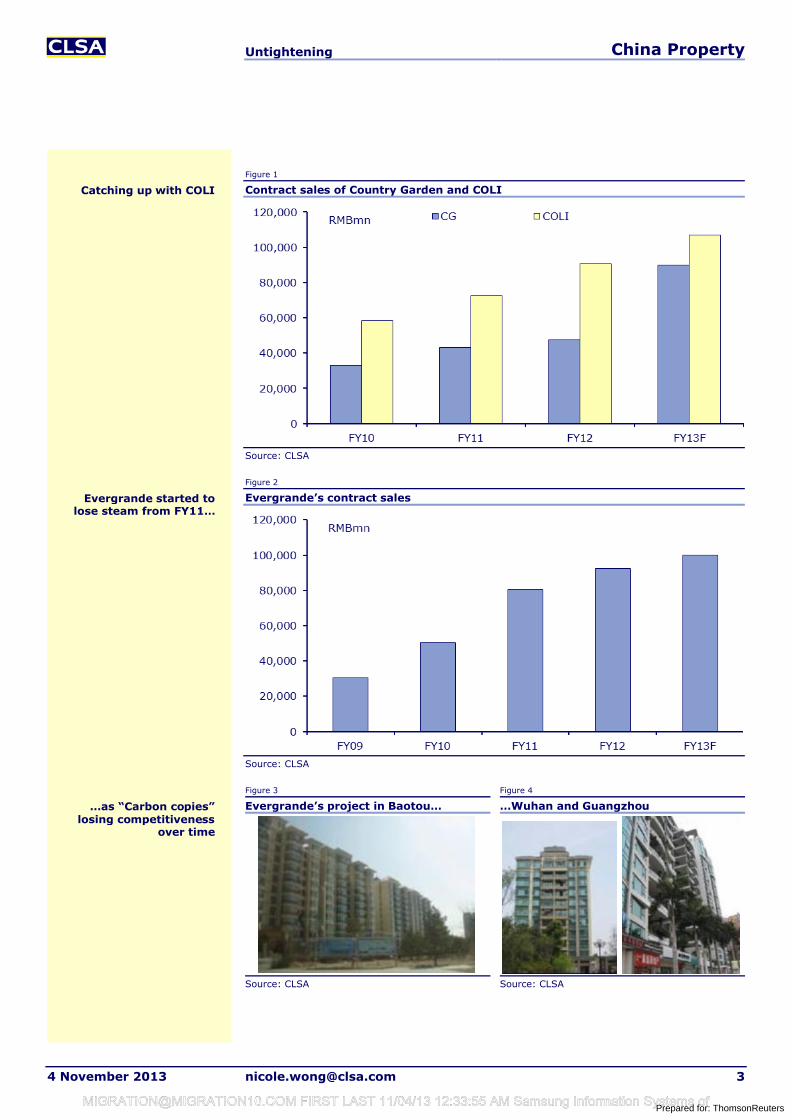

Country GardenWe raised our Country Garden FY13 contract sale forecast by 7% on 30 Oct to RMB90bn on back of strong launches and sale in Sep and Oct. The point to note here is that this number is an equivalence of COLI’s (also a BUY) FY12 contract sale (HK$112bn or RMB91bn). Only three years ago in FY10, CG’s contract sale at RMB32.9bn was just 56% of COLI’s HK$67.1bn or RMB58.4bn. We believe this is result of Country Garden’s successful entry into less competitive markets in lower tier two and upper tier three cities, which offers ample room for growth. This growth model will be replicable in more markets and with FY13 new start likely up 41% plus y-y and land acquisition in 1H13 (12.97mn sqm) already almost equal to FY12 (15.6mn sqm) FY13 will certainly not be the last year of high growth for CG. Our target price of HK$7 is based on 8.5x FY14CL PER and suggests 31% upside. Conviction BUY.

Shift in emphasis

Removal of an overhang

Steady land supply

Increase in subsidized social housing

The fourth raise in contract sale target

Prepared for: [email protected] FIRST LAST 11/04/13 12:33:55 AM Samsung Information Systems of

Untightening China Property

4 November 2013 [email protected] 3

Figure 1

Contract sales of Country Garden and COLI

Source: CLSA

Figure 2

Evergrande’s contract sales

Source: CLSA

Figure 3 Figure 4

Evergrande’s project in Baotou… …Wuhan and Guangzhou

Source: CLSA Source: CLSA

Catching up with COLI

Evergrande started to lose steam from FY11…

…as “Carbon copies” losing competitiveness

over time

Prepared for: [email protected] FIRST LAST 11/04/13 12:33:55 AM Samsung Information Systems of

Untightening China Property

4 November 2013 [email protected] 4

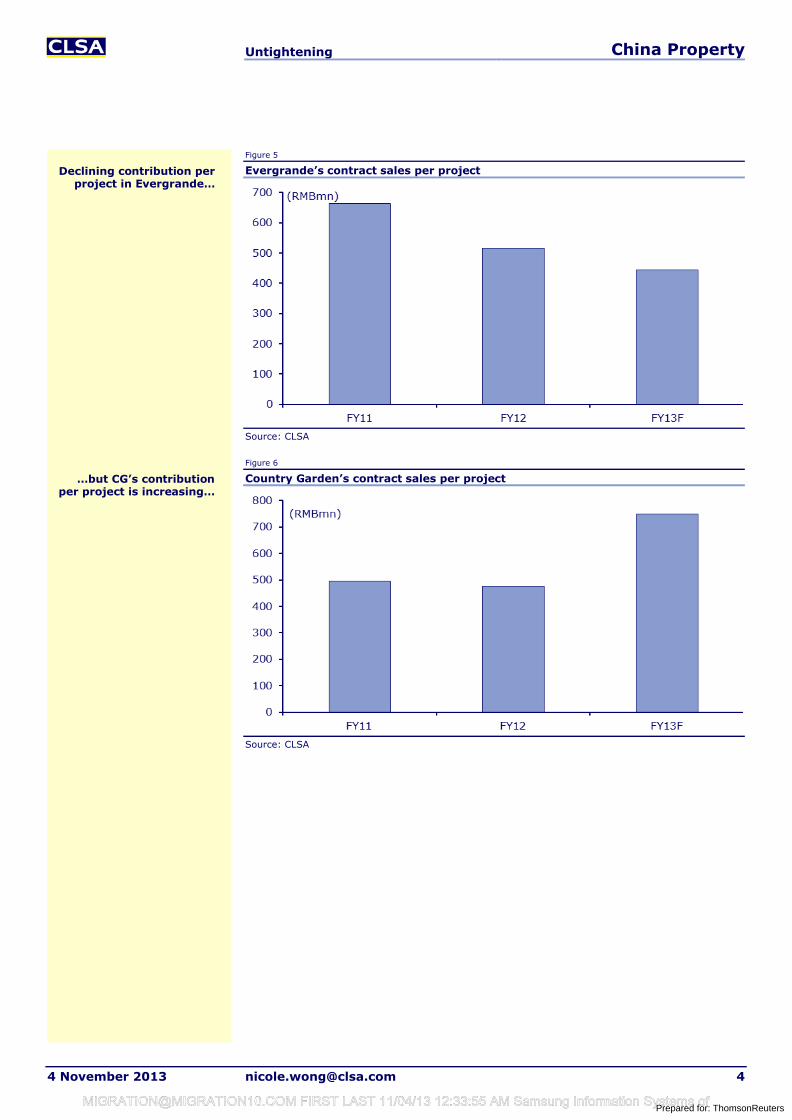

Figure 5

Evergrande’s contract sales per project

Source: CLSA

Figure 6

Country Garden’s contract sales per project

Source: CLSA

Declining contribution per project in Evergrande…

…but CG’s contribution per project is increasing…

Prepared for: [email protected] FIRST LAST 11/04/13 12:33:55 AM Samsung Information Systems of

Untightening China Property

4 November 2013 [email protected] 5

Figure 7 Figure 8

CG’s projects in Huizhou… …Danga Bay Malaysia, and Shenyang

Source: CLSA Source: CLSA

COLIWe are also BUYer of COLI where we expect 25% earnings CAGR for the next three years with construction new start in FY13 expected to increase 21% plus y-y, and YTD Sep land acquisition already up 155% y-y. This is before we consider the asset injection program from parent company CSCEC. We believe COLI is beginning to take over some CSCEC projects. In the best case scenario, the asset injection may happen in 1H14 and COLI may lift its scale of sale by 15% given CSCEC’s scale of sale in FY12 was about 25% of COLI’s and COLI is likely to cherry pick 30-50% of CSCEC’s projects. Our target price of HK$31.4 is set at 10x FY14 PE (par to 5-year historic average) and also suggests 31% upside. BUY.

COLI’s contract sale YTD September is on track with our target. At HK$98,600mn 73% of our (ex COGO) target of HK$136bn has been achieved.

Figure 9

Sale YTD

YTD sale (HK$mn)

YTD sale ex COGO (HK$mn)

YTD GFA (sqm mn)

YTD GFA ex COGO (sqm mn)

ASP (HK$psm)

ASP ex COGO (HK$psm)

Sep 12 91,900 80,100 5.86 5.00 15,696 16,006Sep 13 111,800 98,600 7.36 6.12 15,186 16,124Growth (%, y-y)

22 23 26 22 (3) 1

Source: CLSA

Figure 10

FY13 sale target achievement ratio

Agile CRLand COLI China Vanke B

R&F KWG Shimao Country Garden

Evergrd Longfor COGO

FY13 sale target achieved

68% 80% 73% 72% 72% 71% 67% 76% 82% 76% 66%

Source: CLSA

… and products are more “adaptive”

Contract sale YTD

Potential accretive asset injection

Prepared for: [email protected] FIRST LAST 11/04/13 12:33:55 AM Samsung Information Systems of

Untightening China Property

4 November 2013 [email protected] 6

Land acquisition YTD of RMB23bn (for 5.03mn sqm of GFA) is up 155% y-y (or up 149% y-y by GFA). This along with the facts that 1) 70% of FY12 land acquisition was made in 4Q, and many projects acquired are yet to be launched, and 2) 1H13 construction new start at 6.8mn sqm was up 21% y-y,suggest strong saleable resource growth in FY14.

Figure 11

Land acquisition progress

YTD land acq (RMBmn)

YTD GFA acq (sqm mn)

Land acq to contract sale (%)

Land acq to contract GFA (%)

Sep 12 9,071 2.02 11 40Sep 13 23,147 5.03 23 82Growth (%, y-y) 155 149 n.a. n.a.Source: CLSA

CSCEC asset injectionIn the best case scenario, the asset injection may happen in 1H14 and COLI may lift its scale of sale by 15% given CSCEC’s scale of sale in FY12 was about 25% of COLI’s and COLI is likely to cherry pick 30-50% of CSCEC’s projects. Hence the deal should be positive for COLI.

In execution there are four key concerns regarding the parent company asset injection: the choice of assets, timing of injection, pricing of injection and the financing arrangement.

We believe the parent company asset injection will happen earlier than expected as there are evidence that COLI is taking over projects in some cities already.

According to local news COLI is taking over CSCEC projects in Wuhan and Changsha. In channel checks we find COLI’s logo already displayed at sale office of the Wuhan Tang Xun Hu project, the most sizeable and upper market project among CSCEC’s projects in the city. Over the phone we are informed by sale representatives that sale contract will be signed with COLI rather than CSCEC. In Changsha a local developer contact informed us that the soon to launch Mei Xi Hu project will be launched under COLI. The reason for choice of project seems to be proximity to COLI’s own International Community project and the villa component of the Mei Xi Hu project.

The choice of assets has always been the biggest concern as 1) CSCEC’s products are at a significantly lower price point. In FY12 CSCEC’s ASP of RMb8,619psm was 34% lower than COLI’s, 2) 46% of CSCEC’s land bought over the past 5 years was bought in 2011 when the land market was at its peak. From the projects being taken over it seems that sizeable and upper market projects are prioritized.

Figure 12

FY12 contract sale by company

CSCEC COLI* COGO*Contract sale (RMBmn) 20,600 81,746 10,976Contracted GFA (mn sqm) 2.39 6.26 1.03Contracted ASP (RMBpsm) 8,619 13,056 10,656Source: CLSA *RMB to HKD exchange rate at 1.23

COLI taking over

Four key concerns

Timing: earlier than expected

CSCEC: 25% of COLI’s contract sale scale, but at

just 66% of COLI’s ASP

Choice of assets

Best case scenario

155% y-y growth in land acquisition

Prepared for: [email protected] FIRST LAST 11/04/13 12:33:55 AM Samsung Information Systems of

Untightening China Property

4 November 2013 [email protected] 7

Figure 13

FY08-12 land acquisition

GFA acq (mn sqm) CSCEC COLI % by year CSCEC % by year COLI2008 1.92 2.79 6.9 8.32009 6.06 11.65 21.9 34.72010 2.29 3.43 8.3 10.22011 12.61 9.06 45.6 27.02012 4.76 6.64 17.2 19.8Source: CLSA

Figure 14

COLI taking over

Source: Soufun

COLI’s logo displayed in CSCEC’s Wuhan Tang Xun

Hu project (汤逊湖壹号)

Prepared for: [email protected] FIRST LAST 11/04/13 12:33:55 AM Samsung Information Systems of

Untightening China Property

4 November 2013 [email protected] 8

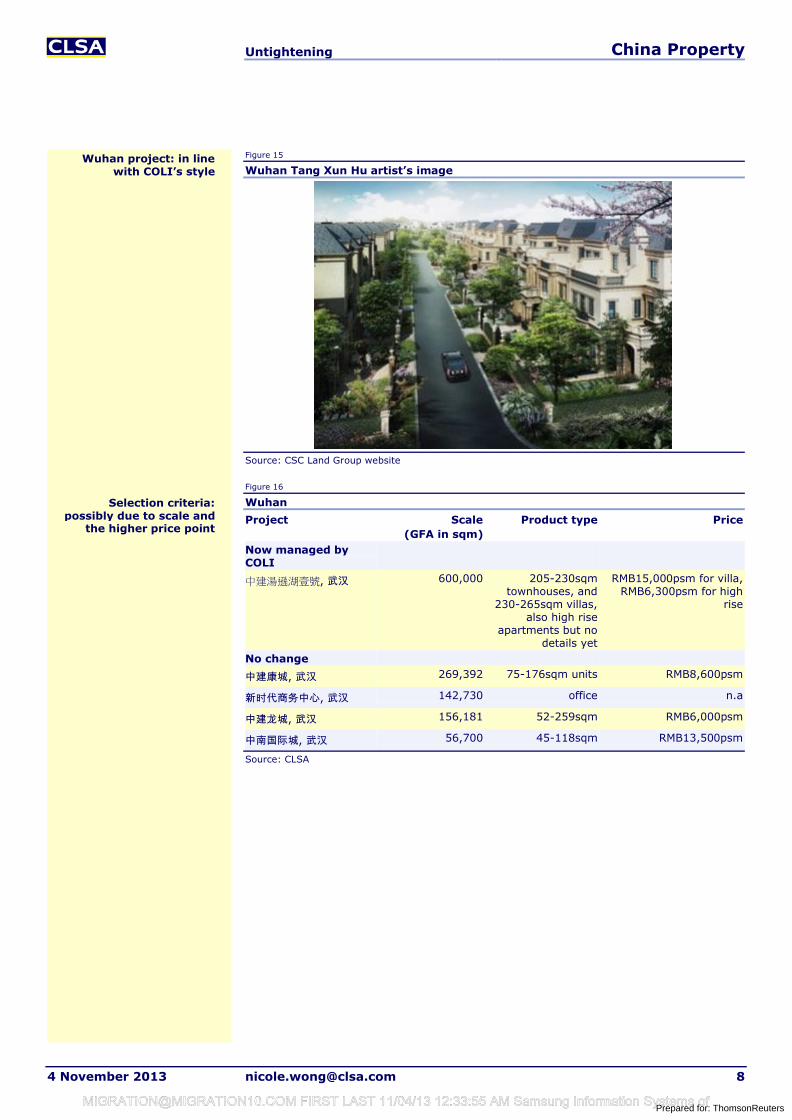

Figure 15

Wuhan Tang Xun Hu artist’s image

Source: CSC Land Group website

Figure 16

Wuhan

Project Scale (GFA in sqm)

Product type Price

Now managed by COLI

中建湯遜湖壹號, 武汉 600,000 205-230sqm townhouses, and

230-265sqm villas, also high rise

apartments but no details yet

RMB15,000psm for villa, RMB6,300psm for high

rise

No change

中建康城, 武汉 269,392 75-176sqm units RMB8,600psm

新时代商务中心, 武汉 142,730 office n.a

中建龙城, 武汉 156,181 52-259sqm RMB6,000psm

中南国际城, 武汉 56,700 45-118sqm RMB13,500psm

Source: CLSA

Wuhan project: in line with COLI’s style

Selection criteria: possibly due to scale and

the higher price point

Prepared for: [email protected] FIRST LAST 11/04/13 12:33:55 AM Samsung Information Systems of

Untightening China Property

4 November 2013 [email protected] 9

Figure 17

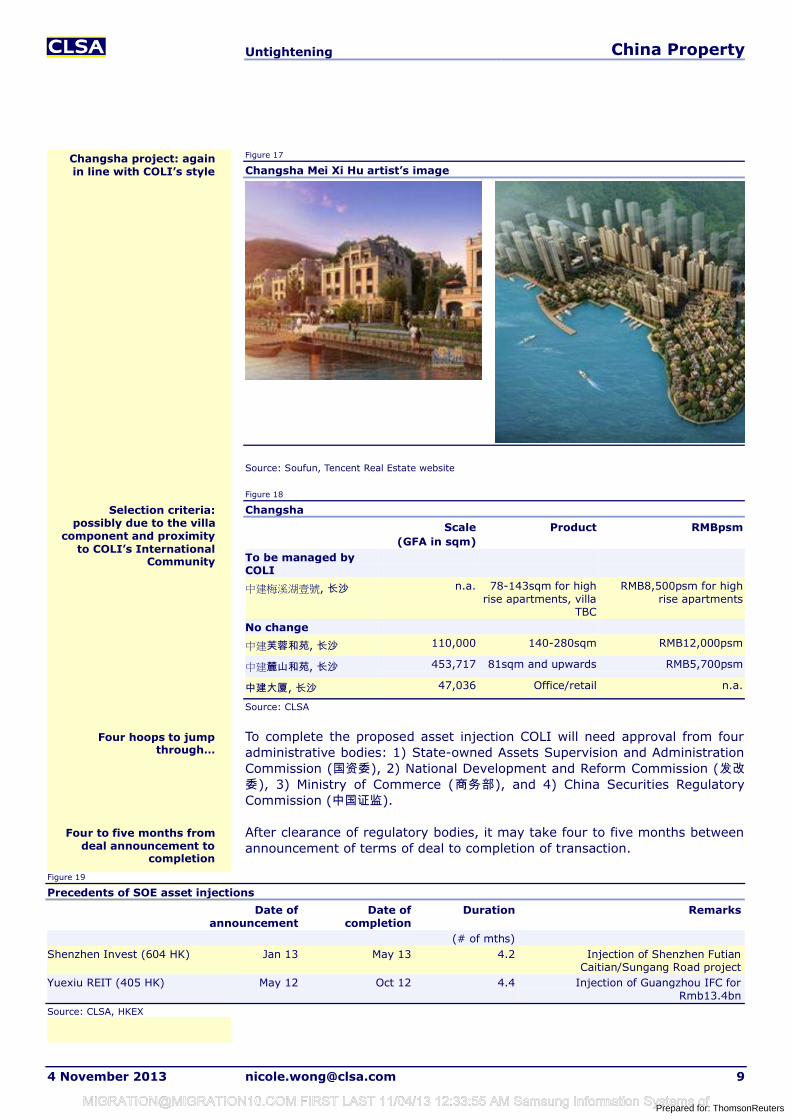

Changsha Mei Xi Hu artist’s image

Source: Soufun, Tencent Real Estate website

Figure 18

Changsha

Scale(GFA in sqm)

Product RMBpsm

To be managed by COLI

中建梅溪湖壹號, 长沙 n.a. 78-143sqm for high rise apartments, villa

TBC

RMB8,500psm for high rise apartments

No change

中建芙蓉和苑, 长沙 110,000 140-280sqm RMB12,000psm

中建麓山和苑, 长沙 453,717 81sqm and upwards RMB5,700psm

中建大厦, 长沙 47,036 Office/retail n.a.

Source: CLSA

To complete the proposed asset injection COLI will need approval from four administrative bodies: 1) State-owned Assets Supervision and Administration Commission (国资委), 2) National Development and Reform Commission (发改委), 3) Ministry of Commerce (商务部), and 4) China Securities Regulatory Commission (中国证监).

After clearance of regulatory bodies, it may take four to five months between announcement of terms of deal to completion of transaction.

Figure 19

Precedents of SOE asset injections

Date of announcement

Date of completion

Duration Remarks

(# of mths)Shenzhen Invest (604 HK) Jan 13 May 13 4.2 Injection of Shenzhen Futian

Caitian/Sungang Road projectYuexiu REIT (405 HK) May 12 Oct 12 4.4 Injection of Guangzhou IFC for

Rmb13.4bnSource: CLSA, HKEX

Four hoops to jump through…

Four to five months from deal announcement to

completion

Changsha project: again in line with COLI’s style

Selection criteria: possibly due to the villa

component and proximity to COLI’s International

Community

Prepared for: [email protected] FIRST LAST 11/04/13 12:33:55 AM Samsung Information Systems of

Untightening China Property

4 November 2013 [email protected] 10

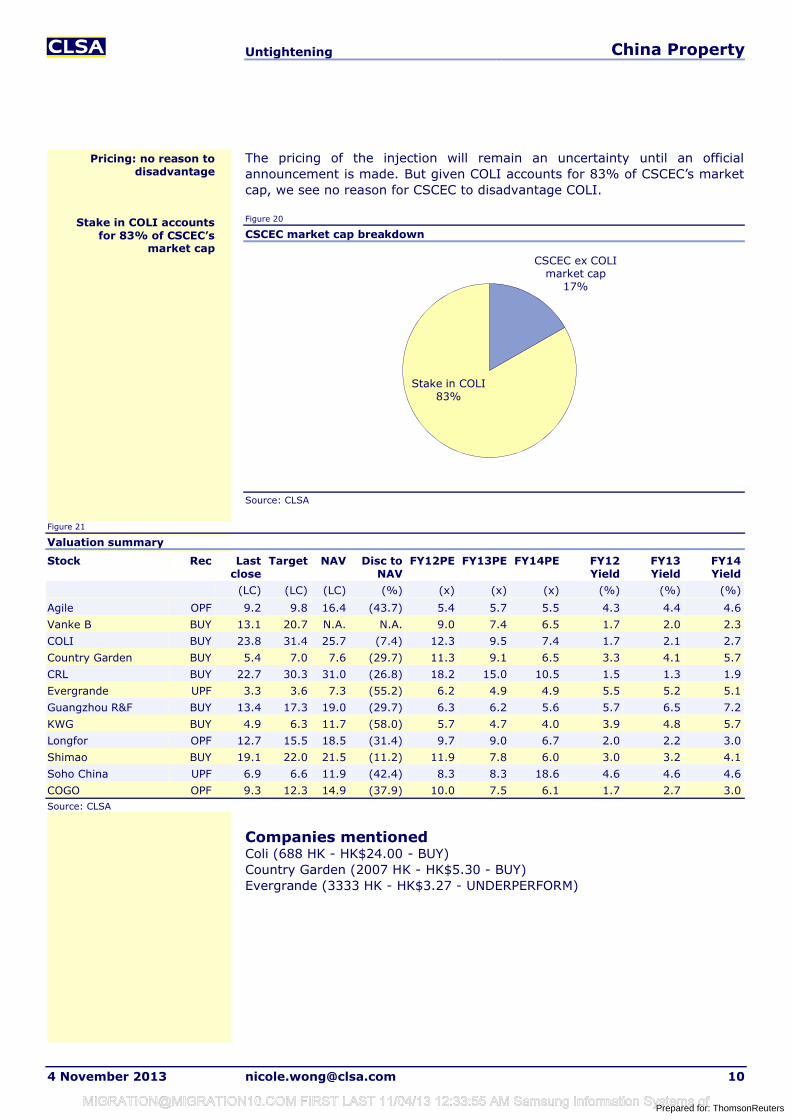

The pricing of the injection will remain an uncertainty until an official announcement is made. But given COLI accounts for 83% of CSCEC’s market cap, we see no reason for CSCEC to disadvantage COLI.

Figure 20

CSCEC market cap breakdown

Source: CLSA

Figure 21

Valuation summary

Stock Rec Last close

Target NAV Disc to NAV

FY12PE FY13PE FY14PE FY12 Yield

FY13 Yield

FY14 Yield

(LC) (LC) (LC) (%) (x) (x) (x) (%) (%) (%)

Agile OPF 9.2 9.8 16.4 (43.7) 5.4 5.7 5.5 4.3 4.4 4.6

Vanke B BUY 13.1 20.7 N.A. N.A. 9.0 7.4 6.5 1.7 2.0 2.3

COLI BUY 23.8 31.4 25.7 (7.4) 12.3 9.5 7.4 1.7 2.1 2.7

Country Garden BUY 5.4 7.0 7.6 (29.7) 11.3 9.1 6.5 3.3 4.1 5.7

CRL BUY 22.7 30.3 31.0 (26.8) 18.2 15.0 10.5 1.5 1.3 1.9

Evergrande UPF 3.3 3.6 7.3 (55.2) 6.2 4.9 4.9 5.5 5.2 5.1

Guangzhou R&F BUY 13.4 17.3 19.0 (29.7) 6.3 6.2 5.6 5.7 6.5 7.2

KWG BUY 4.9 6.3 11.7 (58.0) 5.7 4.7 4.0 3.9 4.8 5.7

Longfor OPF 12.7 15.5 18.5 (31.4) 9.7 9.0 6.7 2.0 2.2 3.0

Shimao BUY 19.1 22.0 21.5 (11.2) 11.9 7.8 6.0 3.0 3.2 4.1

Soho China UPF 6.9 6.6 11.9 (42.4) 8.3 8.3 18.6 4.6 4.6 4.6

COGO OPF 9.3 12.3 14.9 (37.9) 10.0 7.5 6.1 1.7 2.7 3.0Source: CLSA

Companies mentioned Coli (688 HK - HK$24.00 - BUY)Country Garden (2007 HK - HK$5.30 - BUY)Evergrande (3333 HK - HK$3.27 - UNDERPERFORM)

CSCEC ex COLI market cap

17%

Stake in COLI83%

Pricing: no reason to disadvantage

Stake in COLI accounts for 83% of CSCEC’s

market cap

Prepared for: [email protected] FIRST LAST 11/04/13 12:33:55 AM Samsung Information Systems of

Untightening China Property

4 November 2013 [email protected] 11

Research subscriptionsTo change your report distribution requirements, please contact your CLSA sales representative or email us at [email protected] can also fine-tune your Research Alert email preferences at https://www.clsa.com/member/tools/email_alert/.

Key to CLSA/CA Taiwan investment rankings: BUY: Total return expected to exceed market return AND provide 20% or greater absolute return; O-PF: Total return expected to be greater than market return but less than 20% absolute return; U-PF: Total return expected to be less than market return but expected to provide a positive absolute return; SELL: Total return expected to be less than market return AND to provide a negative absolute return. For relative performance, we benchmark the 12-month total return (including dividends) for the stock against the 12-month forecast return (including dividends) for the local market where the stock is traded. We define stocks we expect to provide returns of 100% or higher including dividends within three years as “Double Baggers”.

©2013 CLSA Limited (for research compiled by non-Taiwan analyst(s)) and/or Credit Agricole Securities Taiwan Co., Ltd (for research compiled by Taiwan analyst(s)). Note: In the interests of timeliness, this document has not been edited.

The analyst/s who compiled this publication/communication hereby state/s and confirm/s that the contents hereof truly reflect his/her/their views and opinions on the subject matter and that the analyst/s has/have not been placed under any undue influence, intervention or pressure by any person/s in compiling such publication/communication.

CLSA group of companies (excluding CLSA Americas, LLC) (“CLSA”), Credit Agricole Securities Taiwan Co., Ltd. (“CA Taiwan”), CLSA/CA Taiwan's analysts and/or their associates do and from time to time seek to establish business or financial relationships with companies covered in their research reports. As a result, investors should be aware that CLSA and/or such individuals may have one or more conflicts of interests that could affect the objectivity of this report. Regulations or market practice of some jurisdictions/markets prescribe certain disclosures to be made for certain actual, potential or perceived conflicts of interests relating to research reports and such details are available at www.clsa.com/member/research_disclosures/. Disclosures therein include the position of CLSA, CLSA Americas, LLC and CA Taiwan only and do not reflect those of CITIC Securities International Company Limited, Credit Agricole Corporate & Investment Bank and/or their respective affiliates. If investors have any difficulty accessing this website, please contact [email protected] or +852 2600 8111. If you require disclosure information on previous dates, please contact [email protected]

IMPORTANT: The content of this report is subject to and should be read in conjunction with the disclaimer and CLSA's Legal and Regulatory Notices as set out at www.clsa.com/disclaimer.html, a hard copy of which may be obtained on request from CLSA Publications or CLSA Compliance Group (18/F, One Pacific Place, 88 Queensway, Hong Kong, telephone +852 2600 8888) and/or CA Taiwan Compliance (27/F, 95, Section 2 Dun Hua South Road, Taipei 10682, Taiwan, telephone +886 2 2326 8188). 05/08/2013

Prepared for: [email protected] FIRST LAST 11/04/13 12:33:55 AM Samsung Information Systems of

ASM PacificHK$74.65 - BUY

FinancialsYear to 31 December 11A 12A 13CL 14CL 15CLRevenue (HK$m) 12,915 10,461 10,666 12,336 14,347Rev forecast change (%) - - (2.6) (6.4) (0.7)Net profit (HK$m) 2,025 689 702 1,481 2,010NP forecast change (%) - - (36.2) (17.7) (11.7)EPS (HK¢) 512.2 173.9 177.2 373.8 507.4EPS growth (% YoY) (29.1) (66.0) 1.9 110.9 35.7PE (x) 14.6 42.9 42.1 20.0 14.7Dividend yield (%) 3.2 1.2 1.2 3.3 4.4ROE (%) 35.5 10.7 10.3 19.4 23.1Net debt/equity (%) (20.7) (10.1) (13.8) (22.1) (22.6)Source: CLSA

Find CLSA research on Bloomberg, Thomson Reuters, CapIQ and themarkets.com - and profit from our evalu@tor proprietary database at clsa.com

Chitra Gopal, [email protected]

+65 6416 7816

3 November 2013

Hong KongTechnology

Reuters 0522.HKBloomberg 522 HK

Priced on 1 November 2013HK HSI @ 23,249.8

12M hi/lo HK$104.60/73.35

12M price target HK$93.35±% potential +25%

Shares in issue 396.1mFree float (est.) 38.0%

Market cap US$3,845m

3M average daily volumeHK$48.8m (US$6.3m)

Major shareholdersASMI 40.1%

Stock performance (%)1M 3M 12M

Absolute (6.7) (10.9) (12.8)Relative (7.8) (15.0) (17.1)Abs (US$) (6.7) (10.9) (12.9)

0

50

100

150

200

250

300

350

19

44

68

93

117

Nov-08 Mar-10 Jul-11 Nov-12ASM Pacific (LHS)

Rel to HS I (RHS)

(HK$) (%)

Source: Bloomberg

www.clsa.com

Resu

lts revie

w

A mixed bag 3Q13 results were a mixed bag. Share gains in semi and SMT equipmentallay concerns of structural loss in competitiveness. In semi equipment, ASM’s sales declines was -6% YoY (1Q-3Q13) vs -7% for BESI, -41% for K&S. In SMT, ASM’s sales grew 5% YoY in 1Q-3Q13 vs Fuji’s 32% YoY drop. However, margins are faring worse, notably in SMT where Japanese rivals are aided by a weak yen. We cut our margin forecasts to reflect this. The stock trading at low end of P/BV range appears to have priced in the negatives. Steps ASM is taking –a more flexible cost structure, leadership in next generation technology –have us keeping BUY.

Semi equipment: ASM clawing back market shareIn a tough semi equipment market, YTD sales declines was -6% YoY for ASM(1Q-3Q13) vs -7% for BESI and -41% for K&S. On a QoQ basis, ASM’s sales growth outperformed rivals for the fourth successive quarter. OPM (which fell to levels below those of rivals in 2012) are now on par. These suggest ASM, having missed a product cycle, is coming back.

SMT: share gains, but margins under pressureIn SMT, share gains continue. ASM has been No 1 SMT vendor in Europe historically. It became No 1 in Americas in 1H13, and is now growing in China, in line with its aim of becoming No 1 SMT vendor globally by 2016. Rival Fuji’s sales (last reported: 1H13) fell 32% YoY in Yen terms (-44% YoY in US$). ASM’s 1Q13-3Q13 SMT sales grew +5% YoY. The challenge, has been margins. Despite strong sales in 3Q13 (+24% QoQ), SMT OPM remained flat QoQ at 6.5%, owing Yen depreciation and mix shift to China.

Outsourcing to help in more flexible cost structure4Q13 is seeing cyclical correction. Peer BESI forecast a 20% QoQ drop in 4Q13 sales. ASM’s order backlog at end-3Q13 fell 9% QoQ. A more flexible production model should help manage trough margins better. Outsourced production comprised 15% of total in 3Q13 and temporary workforce was raised to 660 people (348 at 2Q13) or 7% of manufacturing workforce.

Trading at low end of P/BV valuation bandWe cut our margin forecasts to reflect Yen depreciation delaying recovery in SMT margins, thus cutting FY14-15 earnings by 12-18%. Note: Percentage changes for 2013 are meaningless given the low base of earnings. The stock trades at 4.1x 13 PB, at the low end of the five-year range. Our TP is based on 18.4x cross cycle EPS at HK$93.4 from HK$107.3.

Prepared for: [email protected] FIRST LAST 11/04/13 12:33:55 AM Samsung Information Systems of

A mixed bag ASM Pacific - BUY

3 November 2013 [email protected] 2

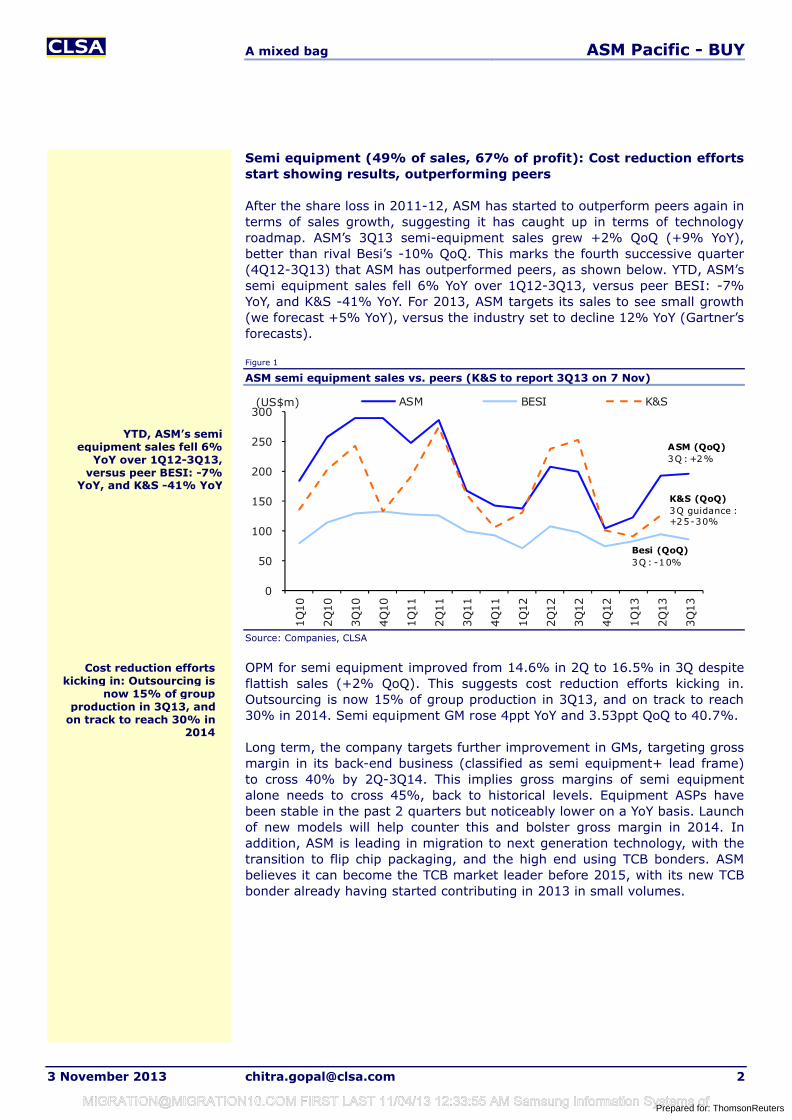

Semi equipment (49% of sales, 67% of profit): Cost reduction efforts start showing results, outperforming peers

After the share loss in 2011-12, ASM has started to outperform peers again in terms of sales growth, suggesting it has caught up in terms of technology roadmap. ASM’s 3Q13 semi-equipment sales grew +2% QoQ (+9% YoY), better than rival Besi’s -10% QoQ. This marks the fourth successive quarter (4Q12-3Q13) that ASM has outperformed peers, as shown below. YTD, ASM’s semi equipment sales fell 6% YoY over 1Q12-3Q13, versus peer BESI: -7% YoY, and K&S -41% YoY. For 2013, ASM targets its sales to see small growth(we forecast +5% YoY), versus the industry set to decline 12% YoY (Gartner’sforecasts).

Figure 1

ASM semi equipment sales vs. peers (K&S to report 3Q13 on 7 Nov)

Source: Companies, CLSA

OPM for semi equipment improved from 14.6% in 2Q to 16.5% in 3Q despite flattish sales (+2% QoQ). This suggests cost reduction efforts kicking in. Outsourcing is now 15% of group production in 3Q13, and on track to reach 30% in 2014. Semi equipment GM rose 4ppt YoY and 3.53ppt QoQ to 40.7%.

Long term, the company targets further improvement in GMs, targeting gross margin in its back-end business (classified as semi equipment+ lead frame)to cross 40% by 2Q-3Q14. This implies gross margins of semi equipment alone needs to cross 45%, back to historical levels. Equipment ASPs havebeen stable in the past 2 quarters but noticeably lower on a YoY basis. Launch of new models will help counter this and bolster gross margin in 2014. In addition, ASM is leading in migration to next generation technology, with the transition to flip chip packaging, and the high end using TCB bonders. ASM believes it can become the TCB market leader before 2015, with its new TCB bonder already having started contributing in 2013 in small volumes.

0

50

100

150

200

250

300

1Q

10

2Q

10

3Q

10

4Q

10

1Q

11

2Q

11

3Q

11

4Q

11

1Q

12

2Q

12

3Q

12

4Q

12

1Q

13

2Q

13

3Q

13

(US$m) ASM BESI K&S

ASM (QoQ)3Q : +2%

Besi (QoQ)3Q : -10%

K&S (QoQ)3Q guidance : +25-30%

Cost reduction efforts kicking in: Outsourcing is

now 15% of group production in 3Q13, and

on track to reach 30% in 2014

YTD, ASM’s semi equipment sales fell 6%

YoY over 1Q12-3Q13, versus peer BESI: -7%

YoY, and K&S -41% YoY

Prepared for: [email protected] FIRST LAST 11/04/13 12:33:55 AM Samsung Information Systems of

A mixed bag ASM Pacific - BUY

3 November 2013 [email protected] 3

Figure 2

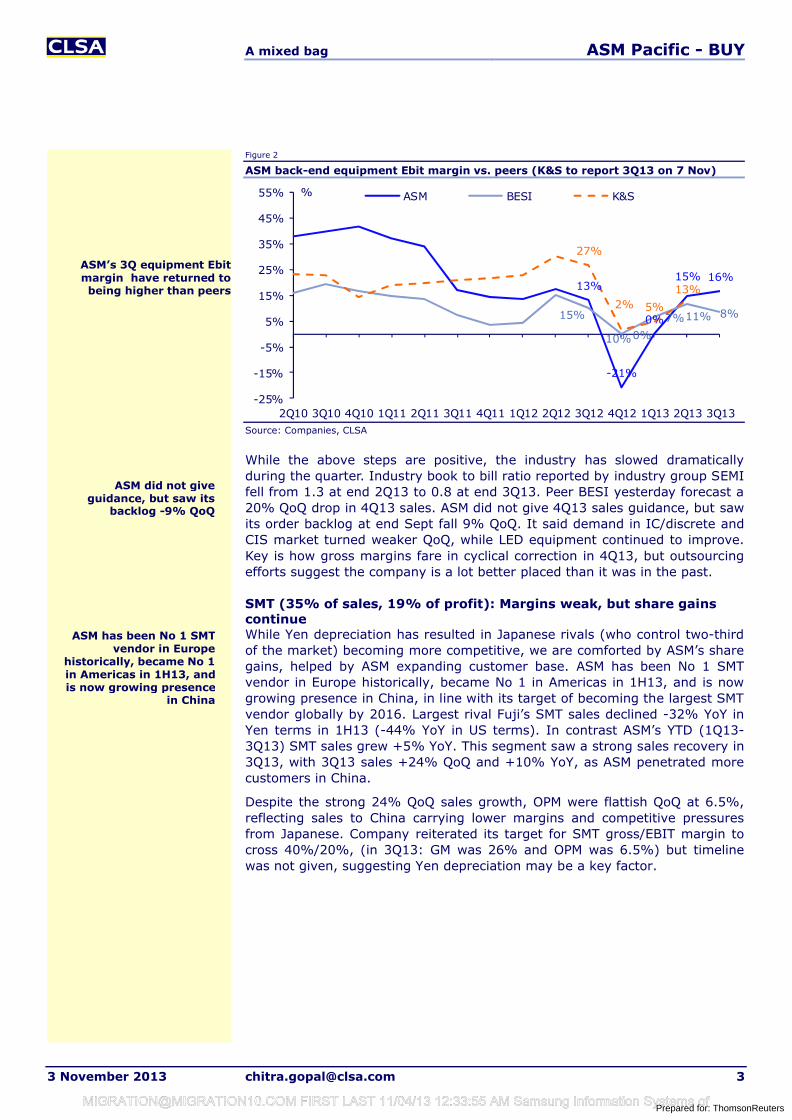

ASM back-end equipment Ebit margin vs. peers (K&S to report 3Q13 on 7 Nov)

Source: Companies, CLSA

While the above steps are positive, the industry has slowed dramatically during the quarter. Industry book to bill ratio reported by industry group SEMI fell from 1.3 at end 2Q13 to 0.8 at end 3Q13. Peer BESI yesterday forecast a 20% QoQ drop in 4Q13 sales. ASM did not give 4Q13 sales guidance, but saw its order backlog at end Sept fall 9% QoQ. It said demand in IC/discrete and CIS market turned weaker QoQ, while LED equipment continued to improve. Key is how gross margins fare in cyclical correction in 4Q13, but outsourcing efforts suggest the company is a lot better placed than it was in the past.

SMT (35% of sales, 19% of profit): Margins weak, but share gains continue While Yen depreciation has resulted in Japanese rivals (who control two-third of the market) becoming more competitive, we are comforted by ASM’s share gains, helped by ASM expanding customer base. ASM has been No 1 SMT vendor in Europe historically, became No 1 in Americas in 1H13, and is now growing presence in China, in line with its target of becoming the largest SMT vendor globally by 2016. Largest rival Fuji’s SMT sales declined -32% YoY in Yen terms in 1H13 (-44% YoY in US terms). In contrast ASM’s YTD (1Q13-3Q13) SMT sales grew +5% YoY. This segment saw a strong sales recovery in 3Q13, with 3Q13 sales +24% QoQ and +10% YoY, as ASM penetrated more customers in China.

Despite the strong 24% QoQ sales growth, OPM were flattish QoQ at 6.5%, reflecting sales to China carrying lower margins and competitive pressures from Japanese. Company reiterated its target for SMT gross/EBIT margin to cross 40%/20%, (in 3Q13: GM was 26% and OPM was 6.5%) but timeline was not given, suggesting Yen depreciation may be a key factor.

13%

-21%

0%

15% 16%

15%

10%0%

7%11% 8%

27%

2% 5%

13%

-25%

-15%

-5%

5%

15%

25%

35%

45%

55%

2Q10 3Q10 4Q10 1Q11 2Q11 3Q11 4Q11 1Q12 2Q12 3Q12 4Q12 1Q13 2Q13 3Q13

% ASM BESI K&S

ASM did not give guidance, but saw its

backlog -9% QoQ

ASM’s 3Q equipment Ebit margin have returned to being higher than peers

ASM has been No 1 SMT vendor in Europe

historically, became No 1 in Americas in 1H13, and is now growing presence

in China

Prepared for: [email protected] FIRST LAST 11/04/13 12:33:55 AM Samsung Information Systems of

A mixed bag ASM Pacific - BUY

3 November 2013 [email protected] 4

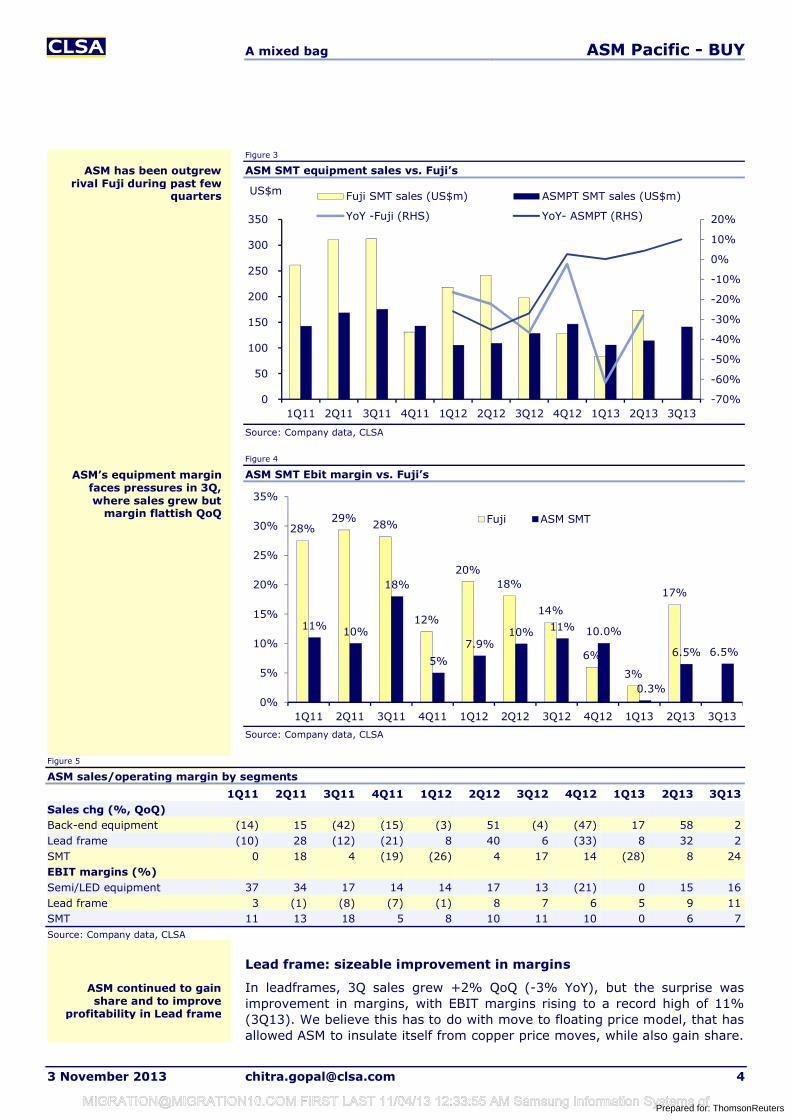

Figure 3

ASM SMT equipment sales vs. Fuji’s

Source: Company data, CLSA

Figure 4

ASM SMT Ebit margin vs. Fuji’s

Source: Company data, CLSA

Figure 5

ASM sales/operating margin by segments

1Q11 2Q11 3Q11 4Q11 1Q12 2Q12 3Q12 4Q12 1Q13 2Q13 3Q13Sales chg (%, QoQ)Back-end equipment (14) 15 (42) (15) (3) 51 (4) (47) 17 58 2Lead frame (10) 28 (12) (21) 8 40 6 (33) 8 32 2SMT 0 18 4 (19) (26) 4 17 14 (28) 8 24EBIT margins (%)Semi/LED equipment 37 34 17 14 14 17 13 (21) 0 15 16Lead frame 3 (1) (8) (7) (1) 8 7 6 5 9 11SMT 11 13 18 5 8 10 11 10 0 6 7Source: Company data, CLSA

Lead frame: sizeable improvement in margins

In leadframes, 3Q sales grew +2% QoQ (-3% YoY), but the surprise was improvement in margins, with EBIT margins rising to a record high of 11% (3Q13). We believe this has to do with move to floating price model, that has allowed ASM to insulate itself from copper price moves, while also gain share.

-70%

-60%

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

0

50

100

150

200

250

300

350

1Q11 2Q11 3Q11 4Q11 1Q12 2Q12 3Q12 4Q12 1Q13 2Q13 3Q13

US$m Fuji SMT sales (US$m) ASMPT SMT sales (US$m)

YoY -Fuji (RHS) YoY- ASMPT (RHS)

28%29%

28%

12%

20%18%

14%

6%

3%

17%

11% 10%

18%

5%

7.9%10% 11% 10.0%

0.3%

6.5% 6.5%

0%

5%

10%

15%

20%

25%

30%

35%

1Q11 2Q11 3Q11 4Q11 1Q12 2Q12 3Q12 4Q12 1Q13 2Q13 3Q13

Fuji ASM SMT

ASM continued to gain share and to improve

profitability in Lead frame

ASM has been outgrew rival Fuji during past few

quarters

ASM’s equipment margin faces pressures in 3Q, where sales grew but

margin flattish QoQ

Prepared for: [email protected] FIRST LAST 11/04/13 12:33:55 AM Samsung Information Systems of

A mixed bag ASM Pacific - BUY

3 November 2013 [email protected] 5

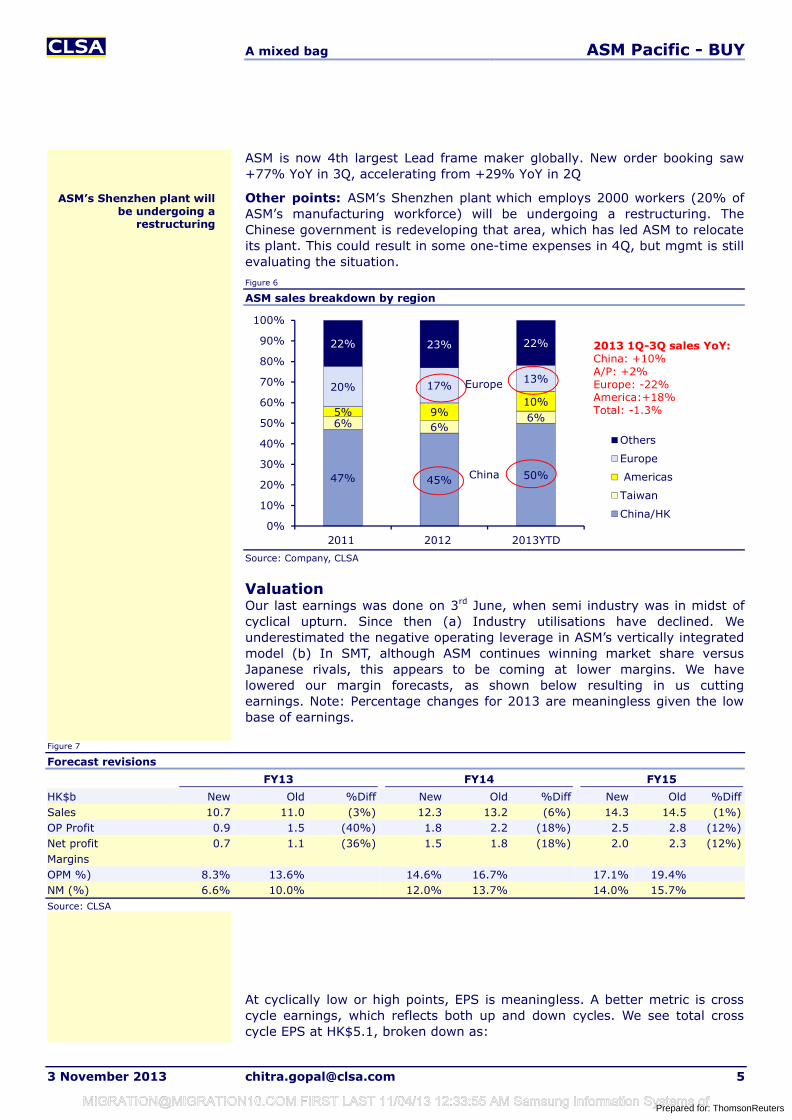

ASM is now 4th largest Lead frame maker globally. New order booking saw +77% YoY in 3Q, accelerating from +29% YoY in 2Q

Other points: ASM’s Shenzhen plant which employs 2000 workers (20% of ASM’s manufacturing workforce) will be undergoing a restructuring. The Chinese government is redeveloping that area, which has led ASM to relocate its plant. This could result in some one-time expenses in 4Q, but mgmt is still evaluating the situation.

Figure 6

ASM sales breakdown by region

Source: Company, CLSA

ValuationOur last earnings was done on 3rd June, when semi industry was in midst of cyclical upturn. Since then (a) Industry utilisations have declined. We underestimated the negative operating leverage in ASM’s vertically integrated model (b) In SMT, although ASM continues winning market share versus Japanese rivals, this appears to be coming at lower margins. We have lowered our margin forecasts, as shown below resulting in us cutting earnings. Note: Percentage changes for 2013 are meaningless given the low base of earnings.

Figure 7

Forecast revisions

FY13 FY14 FY15

HK$b New Old %Diff New Old %Diff New Old %DiffSales 10.7 11.0 (3%) 12.3 13.2 (6%) 14.3 14.5 (1%)OP Profit 0.9 1.5 (40%) 1.8 2.2 (18%) 2.5 2.8 (12%)Net profit 0.7 1.1 (36%) 1.5 1.8 (18%) 2.0 2.3 (12%)MarginsOPM %) 8.3% 13.6% 14.6% 16.7% 17.1% 19.4%NM (%) 6.6% 10.0% 12.0% 13.7% 14.0% 15.7%Source: CLSA

At cyclically low or high points, EPS is meaningless. A better metric is crosscycle earnings, which reflects both up and down cycles. We see total crosscycle EPS at HK$5.1, broken down as:

47% 45% 50%

6% 6%6%5% 9%10%

20% 17%13%

22% 23% 22%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2011 2012 2013YTD

Others

Europe

Americas

Taiwan

China/HK

2013 1Q-3Q sales YoY:China: +10%A/P: +2%Europe: -22%America:+18%Total: -1.3%

China

Europe

ASM’s Shenzhen plant will be undergoing a

restructuring

Prepared for: [email protected] FIRST LAST 11/04/13 12:33:55 AM Samsung Information Systems of

A mixed bag ASM Pacific - BUY

3 November 2013 [email protected] 6

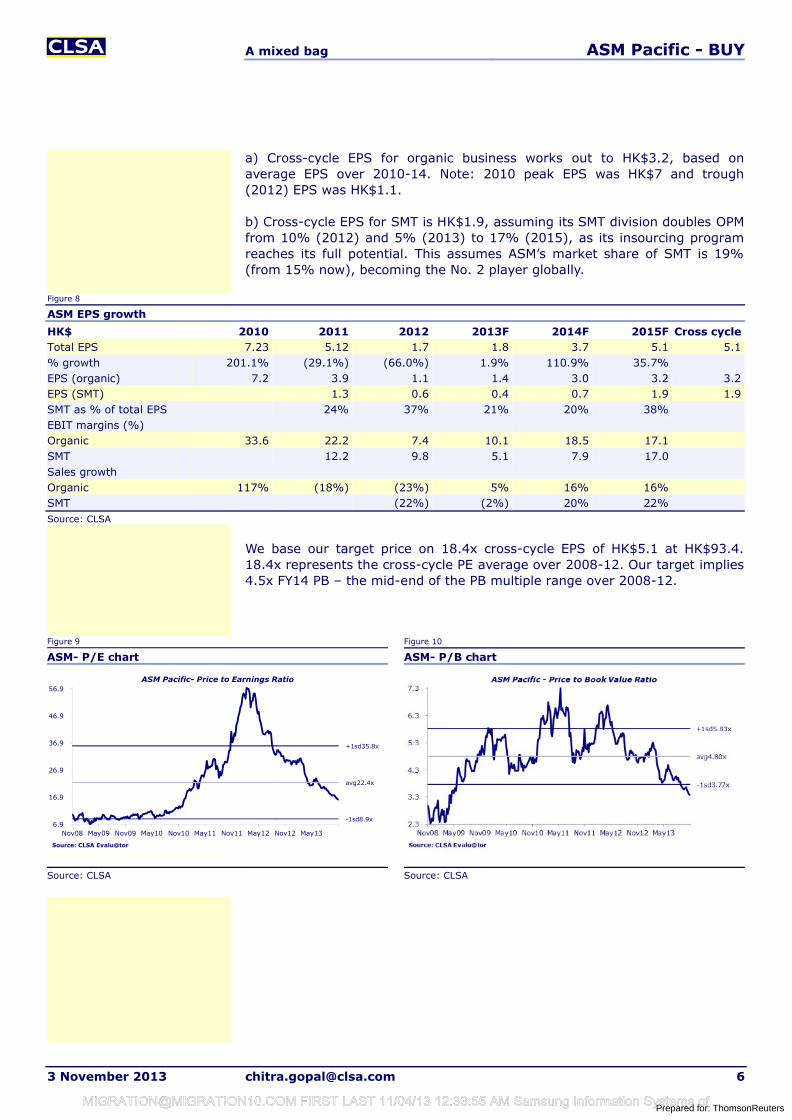

a) Cross-cycle EPS for organic business works out to HK$3.2, based on average EPS over 2010-14. Note: 2010 peak EPS was HK$7 and trough (2012) EPS was HK$1.1.

b) Cross-cycle EPS for SMT is HK$1.9, assuming its SMT division doubles OPM from 10% (2012) and 5% (2013) to 17% (2015), as its insourcing program reaches its full potential. This assumes ASM’s market share of SMT is 19% (from 15% now), becoming the No. 2 player globally.

Figure 8

ASM EPS growth

HK$ 2010 2011 2012 2013F 2014F 2015F Cross cycleTotal EPS 7.23 5.12 1.7 1.8 3.7 5.1 5.1% growth 201.1% (29.1%) (66.0%) 1.9% 110.9% 35.7%EPS (organic) 7.2 3.9 1.1 1.4 3.0 3.2 3.2EPS (SMT) 1.3 0.6 0.4 0.7 1.9 1.9SMT as % of total EPS 24% 37% 21% 20% 38%EBIT margins (%)Organic 33.6 22.2 7.4 10.1 18.5 17.1SMT 12.2 9.8 5.1 7.9 17.0Sales growthOrganic 117% (18%) (23%) 5% 16% 16%SMT (22%) (2%) 20% 22%Source: CLSA

We base our target price on 18.4x cross-cycle EPS of HK$5.1 at HK$93.4. 18.4x represents the cross-cycle PE average over 2008-12. Our target implies 4.5x FY14 PB – the mid-end of the PB multiple range over 2008-12.

Figure 9 Figure 10

ASM- P/E chart ASM- P/B chart

Source: CLSA Source: CLSA

-1sd8.9x

avg22.4x

+1sd35.8x

6.9

16.9

26.9

36.9

46.9

56.9

Nov08 May09 Nov09 May10 Nov10 May11 Nov11 May12 Nov12 May13

ASM Pacific- Price to Earnings Ratio

Source: CLSA Evalu@tor

Prepared for: [email protected] FIRST LAST 11/04/13 12:33:55 AM Samsung Information Systems of

A mixed bag ASM Pacific - BUY

3 November 2013 [email protected] 7

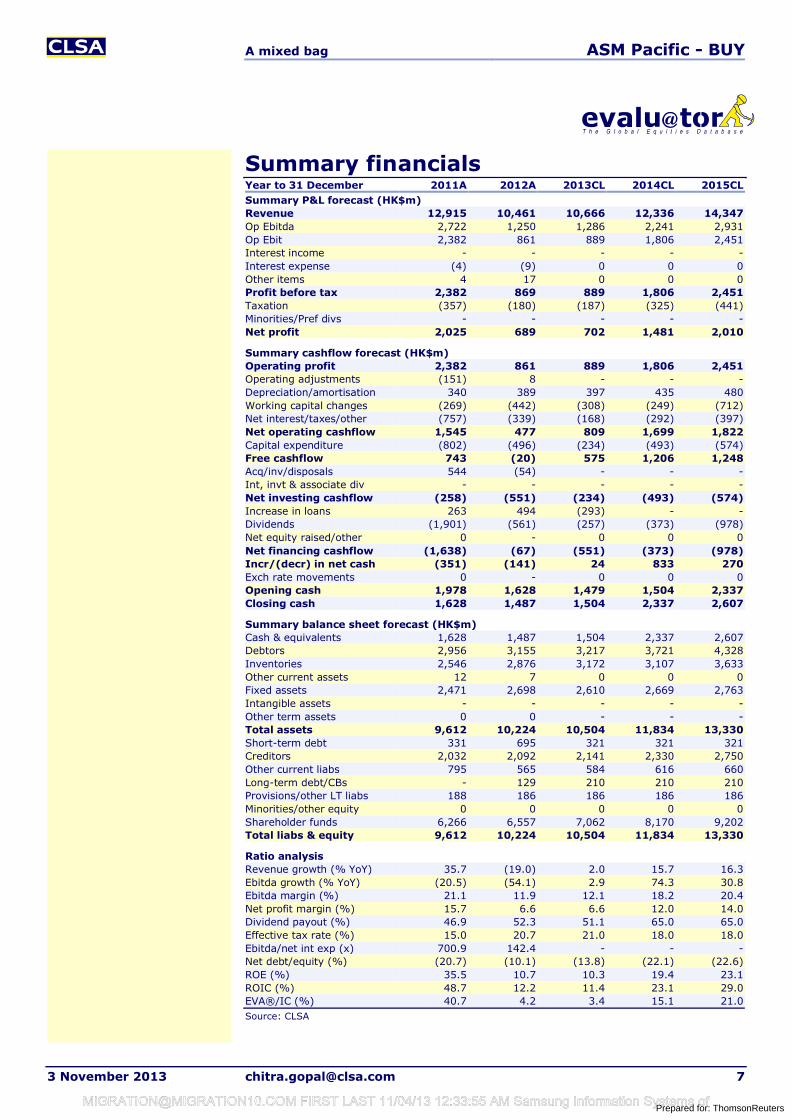

Summary financialsYear to 31 December 2011A 2012A 2013CL 2014CL 2015CLSummary P&L forecast (HK$m)Revenue 12,915 10,461 10,666 12,336 14,347Op Ebitda 2,722 1,250 1,286 2,241 2,931Op Ebit 2,382 861 889 1,806 2,451Interest income - - - - -Interest expense (4) (9) 0 0 0Other items 4 17 0 0 0Profit before tax 2,382 869 889 1,806 2,451Taxation (357) (180) (187) (325) (441)Minorities/Pref divs - - - - -Net profit 2,025 689 702 1,481 2,010

Summary cashflow forecast (HK$m)Operating profit 2,382 861 889 1,806 2,451Operating adjustments (151) 8 - - -Depreciation/amortisation 340 389 397 435 480Working capital changes (269) (442) (308) (249) (712)Net interest/taxes/other (757) (339) (168) (292) (397)Net operating cashflow 1,545 477 809 1,699 1,822Capital expenditure (802) (496) (234) (493) (574)Free cashflow 743 (20) 575 1,206 1,248Acq/inv/disposals 544 (54) - - -Int, invt & associate div - - - - -Net investing cashflow (258) (551) (234) (493) (574)Increase in loans 263 494 (293) - -Dividends (1,901) (561) (257) (373) (978)Net equity raised/other 0 - 0 0 0Net financing cashflow (1,638) (67) (551) (373) (978)Incr/(decr) in net cash (351) (141) 24 833 270Exch rate movements 0 - 0 0 0Opening cash 1,978 1,628 1,479 1,504 2,337Closing cash 1,628 1,487 1,504 2,337 2,607

Summary balance sheet forecast (HK$m)Cash & equivalents 1,628 1,487 1,504 2,337 2,607Debtors 2,956 3,155 3,217 3,721 4,328Inventories 2,546 2,876 3,172 3,107 3,633Other current assets 12 7 0 0 0Fixed assets 2,471 2,698 2,610 2,669 2,763Intangible assets - - - - -Other term assets 0 0 - - -Total assets 9,612 10,224 10,504 11,834 13,330Short-term debt 331 695 321 321 321Creditors 2,032 2,092 2,141 2,330 2,750Other current liabs 795 565 584 616 660Long-term debt/CBs - 129 210 210 210Provisions/other LT liabs 188 186 186 186 186Minorities/other equity 0 0 0 0 0Shareholder funds 6,266 6,557 7,062 8,170 9,202Total liabs & equity 9,612 10,224 10,504 11,834 13,330

Ratio analysisRevenue growth (% YoY) 35.7 (19.0) 2.0 15.7 16.3Ebitda growth (% YoY) (20.5) (54.1) 2.9 74.3 30.8Ebitda margin (%) 21.1 11.9 12.1 18.2 20.4Net profit margin (%) 15.7 6.6 6.6 12.0 14.0Dividend payout (%) 46.9 52.3 51.1 65.0 65.0Effective tax rate (%) 15.0 20.7 21.0 18.0 18.0Ebitda/net int exp (x) 700.9 142.4 - - -Net debt/equity (%) (20.7) (10.1) (13.8) (22.1) (22.6)ROE (%) 35.5 10.7 10.3 19.4 23.1ROIC (%) 48.7 12.2 11.4 23.1 29.0EVA®/IC (%) 40.7 4.2 3.4 15.1 21.0Source: CLSA

Prepared for: [email protected] FIRST LAST 11/04/13 12:33:55 AM Samsung Information Systems of

A mixed bag ASM Pacific - BUY

3 November 2013 [email protected] 8

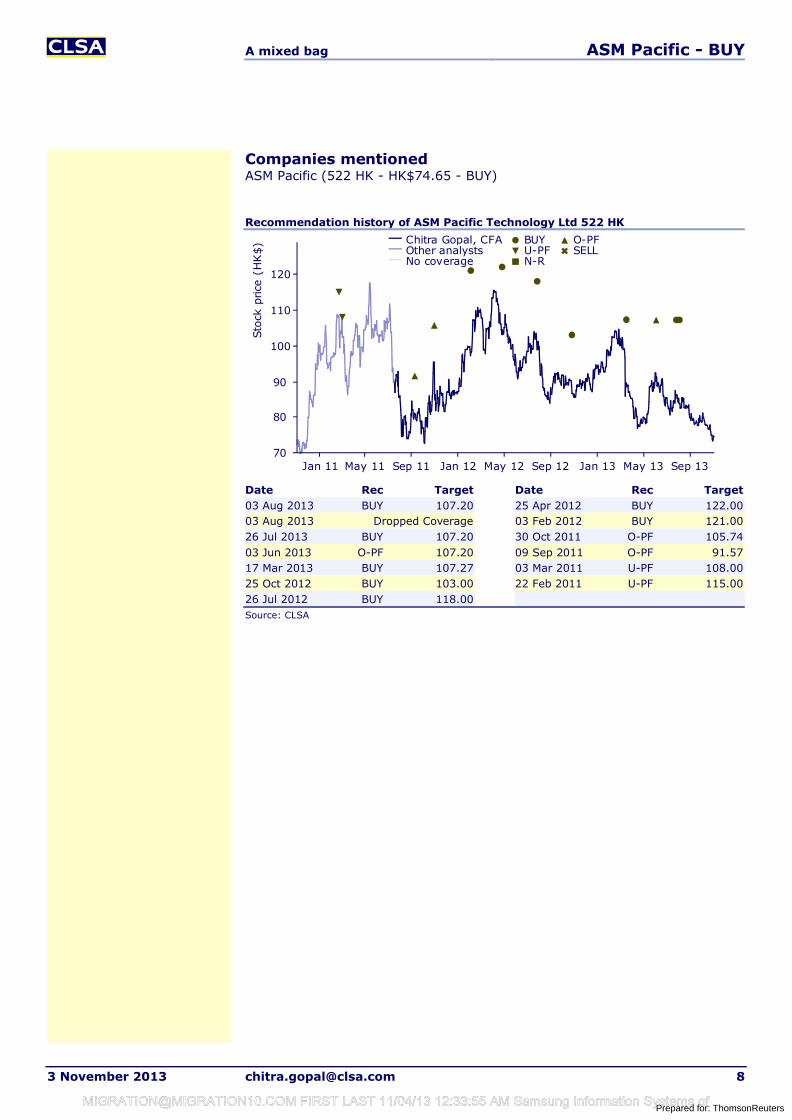

Companies mentionedASM Pacific (522 HK - HK$74.65 - BUY)

Recommendation history of ASM Pacific Technology Ltd 522 HK

Date Rec Target Date Rec Target03 Aug 2013 BUY 107.20 25 Apr 2012 BUY 122.0003 Aug 2013 Dropped Coverage 03 Feb 2012 BUY 121.0026 Jul 2013 BUY 107.20 30 Oct 2011 O-PF 105.7403 Jun 2013 O-PF 107.20 09 Sep 2011 O-PF 91.5717 Mar 2013 BUY 107.27 03 Mar 2011 U-PF 108.0025 Oct 2012 BUY 103.00 22 Feb 2011 U-PF 115.0026 Jul 2012 BUY 118.00Source: CLSA

70

80

90

100

110

120

Sto

ckpr

ice

(HK

$)

Jan 11 May 11 Sep 11 Jan 12 May 12 Sep 12 Jan 13 May 13 Sep 13

Chitra Gopal, CFAOther analystsNo coverage

BUYU-PFN-R

O-PFSELL

Prepared for: [email protected] FIRST LAST 11/04/13 12:33:55 AM Samsung Information Systems of

A mixed bag ASM Pacific - BUY

3 November 2013 [email protected] 9

Research subscriptionsTo change your report distribution requirements, please contact your CLSA sales representative or email us at [email protected] can also fine-tune your Research Alert email preferences at https://www.clsa.com/member/tools/email_alert/.

Key to CLSA/CA Taiwan investment rankings: BUY: Total return expected to exceed market return AND provide 20% or greater absolute return; O-PF: Total return expected to be greater than market return but less than 20% absolute return; U-PF: Total return expected to be less than market return but expected to provide a positive absolute return; SELL: Total return expected to be less than market return AND to provide a negative absolute return. For relative performance, we benchmark the 12-month total return (including dividends) for the stock against the 12-month forecast return (including dividends) for the local market where the stock is traded. We define stocks we expect to provide returns of 100% or higher including dividends within three years as “Double Baggers”.

©2013 CLSA Limited (for research compiled by non-Taiwan analyst(s)) and/or Credit Agricole Securities Taiwan Co., Ltd (for research compiled by Taiwan analyst(s)). Note: In the interests of timeliness, this document has not been edited.

The analyst/s who compiled this publication/communication hereby state/s and confirm/s that the contents hereof truly reflect his/her/their views and opinions on the subject matter and that the analyst/s has/have not been placed under any undue influence, intervention or pressure by any person/s in compiling such publication/communication.

CLSA group of companies (excluding CLSA Americas, LLC) (“CLSA”), Credit Agricole Securities Taiwan Co., Ltd. (“CA Taiwan”), CLSA/CA Taiwan's analysts and/or their associates do and from time to time seek to establish business or financial relationships with companies covered in their research reports. As a result, investors should be aware that CLSA and/or such individuals may have one or more conflicts of interests that could affect the objectivity of this report. Regulations or market practice of some jurisdictions/markets prescribe certain disclosures to be made for certain actual, potential or perceived conflicts of interests relating to research reports and such details are available at www.clsa.com/member/research_disclosures/. Disclosures therein include the position of CLSA, CLSA Americas, LLC and CA Taiwan only and do not reflect those of CITIC Securities International Company Limited, Credit Agricole Corporate & Investment Bank and/or their respective affiliates. If investors have any difficulty accessing this website, please contact [email protected] or +852 2600 8111. If you require disclosure information on previous dates, please contact [email protected]

IMPORTANT: The content of this report is subject to and should be read in conjunction with the disclaimer and CLSA's Legal and Regulatory Notices as set out at www.clsa.com/disclaimer.html, a hard copy of which may be obtained on request from CLSA Publications or CLSA Compliance Group (18/F, One Pacific Place, 88 Queensway, Hong Kong, telephone +852 2600 8888) and/or CA Taiwan Compliance (27/F, 95, Section 2 Dun Hua South Road, Taipei 10682, Taiwan, telephone +886 2 2326 8188). 05/08/2013

Prepared for: [email protected] FIRST LAST 11/04/13 12:33:55 AM Samsung Information Systems of

High conviction calls

Analyst Rec Ticker Sector MktCap 3m AVTO Close Target otal retur Date includedElinor Leung, CFA BUY BIDU US Internet US$57.69b US$522m 160.80 210.00 31% 05 Aug 2013

Analyst Rec Ticker Sector MktCap 3m AVTO Close Target otal retur Date includedPaul Wan BUY 293 HK Transport US$7.8b US$6m 15.38 17.43 17% 06 May 2013

Analyst Rec Ticker Sector MktCap 3m AVTO Close Target otal retur Date includedJonathan Galligan BUY 1 HK Property US$36.65b US$61m 121.20 143.00 21% 18 Sep 2013

Analyst Rec Ticker Sector MktCap 3m AVTO Close Target otal retur Date includedSusanna Leung BUY 2007 HK Property US$12.14b US$16m 5.30 7.00 38% 10 May 2013

Analyst Rec Ticker Sector MktCap 3m AVTO Close Target otal retur Date includedElinor Leung, CFA BUY CTRP US Internet US$7.11b US$130m 54.26 59.50 10% 05 Aug 2013

• Company gave a confident outlook and is guiding higher revenue growth of 20-25% for 3Q13 (vs 15-20%YoY for 2Q). We believe Ctrip is still at the beginning of turning around its business. Revenue growth will accelerate with new leisure products and mobile migration. Margin could eventually expand to 30% in-line with global peers.

Cheung Kong

• Catalysts for CK in the near term include acquisitions driven by an undergeared balance sheet as well as the launch of the afore mentioned 5k unit HK pipeline.

• Structural improvements at Hutchison have delivered sustainable double digit earnings growth, The positive improvements at Hutch have yet to be reflected at the CK level. Going forward, recurrent profit growth at Hutch will be the most substantial driver to CK's core

fit

• The run in Hutch's share price has yet to be reflected in CK. Cheung Kong is trading at a wide stub discount. While we continue to like Hutch, we believe the risk reward balance for CK has become increasingly attractive.

• Ctrip’s 2Q13 results were very strong beating expectations by 25%. Operating profits grew 16.6%YoY to Rmb196m benefiting from faster revenue growth, operating leverage and margin expansion.

• Aggressive marketing strategy and new leisure products (Tujia, Songguo, Smartchoice and Groupbuy) have accelerated market share gain. Sales volume of hotel booking and air ticketing were up by strong 30-40%YoY. Mobile migration has become a new growth

Country Garden

• Country Garden is not just ahead of the pack in sales achieved YTD, the pace of sales is likely to accelerate with five projects scheduled for launch in May and June, versus three new launches in 1Q.

• Country Garden has contracted Rmb23.05bn of sales in 4M13, up 153% YoY, thanks to 134% YoY in GFA sold to 3.44m sqm and 8% YoY increase in ASP. This represents 38% of our full year sales estimate, one of the highest among peers.

• The company is also preparing for growth beyond 2013 by building and land replenishment, and living up to its promise to diversify away its old problem of geographic concentration by extending its footprint carefully.

Ctrip

• Above street earnings forecast. The street is factoring in a gradual recovery scenario for the cargo business in 2014, which we believe will be more like a rebound as this is a highly cyclical business, margins will recover sharply when global trades recover.

Cathay Pacific

China/HK top ideas

There are 8 buys and 4 sells in our high conviction list. The favoured stocks play to current investment themes such as, smartphone/internet growth, outbound travel and consumption. We sell stocks that are overvalued or gets negatively impacted by policy. Our latest change was removal of Samsonite.

Market strategy

Baidu

• Baidu is guiding stronger than expected 4Q revenue growth of 45.5-49.6%YoY due to mobile monetization. Mobile monetization has been boosted by the new integrated mobile and PC ad platform.

• Cathay Pacific has a history of being first off the ground in the early stages of an upcycle. While HK’s flagship carrier has yet to recover from its multiyear price-book contraction, we expect air traffic to take off in 2H13 as the global economy starts to regain its footing.

• We expect inbound passenger traffic to grow by 8.1% in 2013 and 10% in 2014, which is based on in-house GDP forecasts. Air freight has shown higher beta than sea freight in the past, we expect 2014 to be a much better year as global trades recover. We expect air cargo throughput to HK to rise 3.4% in 2013, and 8.9% in 2014.

• Baidu’s mobile products have also gained strong momentum. Its search app download jumped 50%QoQ in 3Q. Traffic acquisition cost increase slowed in 3Q13. TAC as a percentage of revenues was flat QoQ at 11.7% in 3Q13.

• Baidu earning is recovering. Operating profit was up 1.2%YoY to Rmb3.05bn in 3Q13 (vs -4.5%YoY in 2Q13). Earning recovery will be faster over next two quarters given the easier comparison. Share could continue to re-rate with accelerated revenue growth and multiple expansion.

Prepared for: ThomsonReuters

[email protected] FIRST LAST 11/04/13 12:33:55 AM Samsung Information Systems of

China/HK top ideas Market strategy

Analyst Rec Ticker Sector MktCap 3m AVTO Close Target otal retur Date includedChitra Gopal, CFA BUY 992 HK Technology US$10.97b US$34m 8.30 8.78 8% 22 Mar 2013

Analyst Rec Ticker Sector MktCap 3m AVTO Close Target otal retur Date includedAaron Fischer, CFA BUY MPEL US Hotels & Leisure US$18.69b US$83m 33.16 42.00 27% 08 Jun 2012

Analyst Rec Ticker Sector MktCap 3m AVTO Close Target otal retur Date includedJialong Shi BUY NTES US Internet US$8.72b US$55m 67.51 83.00 25% 04 Mar 2013

Analyst Rec Ticker Sector MktCap 3m AVTO Close Target otal retur Date includedChen Huang SELL 3968 HK Financial services US$46.06b US$47m 15.4 12.71 -13% 08 Jun 2012

Analyst Rec Ticker Sector MktCap 3m AVTO Close Target otal retur Date includedRajesh Panjwani SELL 1072 HK Power US$3.61b US$2m 12.48 9.50 -23% 03 Jun 2013

• Solid earnings outlook. NetEase will likely grow its topline by 28% and earnings by 26% in 2013 driven by solid performance of its flagship titles, FWJ and WWJ2. Our earnings forecast is 13% above consensus. We believe street will likely upgrade their forecasts on the back of recent price hikes for FWJ and WWJ2, which will likely act as a catalyst for share prices.

• We believe China’s coal-fired power capacity addition is in a structural decline as power demand growth slows and China tries to reduce its reliance on coal to curb pollution.

• Falling demand has led to 10-20% lower prices for boilers, turbines and generators over last two years and this will start to impact margins from 2013 onwards.

NetEase

• It has a strong pipeline with five to six new titles for 2013. Its upcoming new game, Dragon Sword, is promising and may become a catalyst upon its debut in 2H13.

• The bank’s capital position has been week with the Tier-1 CAR of 8.49% as of end 2012, the second-lowest among H-share banks.

CMB

• Valuation remains attractive trading at 9.0x PE/5.5x ex-cash PE with ~40% of its market cap in net cash. We believe company will likely begin to pay regular dividend in 2013 with a 25% payout and 2.8% yield.

• The Rmb35bn A+H rights issue is long-overdue and will remain an overhang. • Further disruption to that should constrain CMB’s dividend payout and loan growth in 2013. As the most expensive bank under our coverage, the premium is unjustified and we rate the stock a conviction SELL.

• Margins in wind power remain low and we do not expect a significant recovery in nuclear power before 2015. Our EPS estimates are 18-29% below consensus. Maintain SELL.

Dongfang

• Lenovo is No 2 PC maker globally and sets to become No 1 in 2013. In addition, Lenovo now becomes No 2 smartphone brand in China – ranking as the fastest growing smartphone maker, and looks to overtake leader Samsung in 2013.

• Melco Crown has one of the strongest development pipelines with Belle Grande Manila and Macau Studio City set to open in 2014-15. The company also has the optionality to develop City of Dream Phase 3, which is estimated to have 1.5m sq ft gross floor area.

• Our target price on Melco Crown is HK$25.60, based on 11x EV/Ebitda and HK$2.40 per share from Macau Studio City. While not including any value into our price target for the Belle Grande Manila and City of Dreams Phase 3.

Melco Crown

• Macau Studio City, together with Galaxy Macau Phase II should be the Cotai properties to open first. As a result of the better growth prospects, we are not disappointed by the lack of dividend in the next 12 months.

Lenovo

• We expect Lenovo capex of US$300-400m in 2013, directed to its new smartphone plant in Wuhan. It views in-house manufacturing as critical to developing innovative designs, and helping improve PC margins. Results are reflected in progress in high-end consumer notebooks. In the US, Lenovo achieved a 49% share in notebooks priced at >US$900, helped by the success of Yoga, in Dec quarter 2012.

• Unlike peers who have been bleeding money in phones, Lenovo achieved breakeven in Dec quarter 2012. It is on track to achieve 2% OPM in next 18 months. We have modelled MIDH division (smartphones, tablets, TV) to remain at breakeven, with OPM of -0.7% in year end Mar 14 and -0.5% in Mar 15, up from -2.0% in Mar 13. There is upside to our forecasts, as mix shifts to retail channels where margins are higher.

Prepared for: ThomsonReuters

[email protected] FIRST LAST 11/04/13 12:33:55 AM Samsung Information Systems of

China/HK top ideas Market strategy

Analyst Rec Ticker Sector MktCap 3m AVTO Close Target otal retur Date includedRajesh Panjwani SELL 2727 HK Power US$7.06b US$3m 2.74 2.20 -17% 13 Sep 2013

Analyst Rec Ticker Sector MktCap 3m AVTO Close Target otal retur Date includedRajesh Panjwani SELL 3 HK Power US$22.49b US$24m 18.12 16.00 -10% 03 Jun 2013

Sector analyst's top picksSectorAutosBanks CNBanks HKCementConglomerates HKConsumer CNConsumer HKFinancial ServicesHealthcareInsuranceInternetMacau gamingMachineryOil & GasPower & renewablesProperty CNProperty HKResourcesSteelSmall capsTransportTechnologyTelecomUtilities HK

• As the share of earnings from China, coal and oil rises, the halo effect of HKCG should fade, making it difficult to justify 29x PE and 3.9x PB when yield is below 2%. SELL.

- CLP, CKI, Power Assets

AAC, Lenovo ZTE

Chalco, Hidili Industry, Yanzhou Coal

Want Want, Mengniu, Belle

-

BOC, Citic Bank

CR Gas, Longyuan, CR Power, HuanengShanghai PetrochemDongfang, Shanghai Electric

Melco Crown, SJM

Link Reit, Henderson Land, Kerry

China Mobile China Unicom

Hengdeli, Yingde GasesChina CoscoCathay Pacific, CSD

Tiangong, Future Bright

Stocks to avoidStocks to buy

Shanghai Electric

• Shanghai Electric’s 1H13 net profit down 25% YoY. Overall profit was also supported by subsidies going up 169%YoY to Rmb373mn,

• We recently cut our earnings for SEG by 11-15%, taking us 20-35% below consensus and target price to HK$2.2.

HK & China Gas

• Reality has finally sunk in and management believes there will be more pressure on margins as intense competition keeps thermal equipment prices low.

Hang Seng

Zhengtong

Haitong, FEH HKEx

CNBM, Shanshui

Prada, Chow Tai Fook Li & Fung, Esprit

Angang, Magang

SunArt, Li Ning

Shougang

Coli, CRLand, Country Garden, Vanke, Guangzhou R&F

Shenhua, Zhaojin

Soho China, Evergrande

• HKCG’s gas-distribution business in Hong Kong is mature, while growth in China is past its peak.• The firm is focusing on “new energy” business to drive future expansion, most of which is coal mining and oil E&P. However, it lacks any strategic edge in these businesses, which are also clearly environmentally unfriendly.

Beijing Ent, Hopewell HighwayHutchison, Cheung KongConch, CR Cement

BYD

Bank of China (HK)CMB, Minsheng

Mindray, Sino Biopharm

Hongkong Land, New World, Wharf

PetroChina, Sinopec

PICC Group, China PacificShanda Games, Perfect World-

Ping An

Zoomlion, Weifu High Tech, Sany Heavy Weichai Power, Sinotruk

Baidu, Tencent, Ctrip, NetEase

Key to CLSA/CLSA Americas/CA Taiwan investment rankings: BUY: Total return expected to exceed market return AND provide 20% or greater absolute return; O-PF: Total return expected to be greater than market return but less than 20% absolute return; U-PF: Total return expected to be less than market return but expected to provide a positive absolute return; SELL: Total return expected to be less than market return AND to provide a negative absolute return. For relative performance, we benchmark the 12-month total return (including dividends) for the stock against the 12-month forecast return (including dividends) for the local market where the stock is traded. We define stocks we expect to provide returns of 100% or higher including dividends within three years as “Double Baggers”.

The analyst/s who compiled this publication/communication hereby state/s and confirm/s that the contents hereof truly reflect his/her/their views and opinions on the subject matter and that the analyst/s has/have not been placed under any undue influence, intervention or pressure by any person/s in compiling such publication/communication. CLSA group of companies (excluding CLSA Americas, LLC) (“CLSA”), Credit Agricole Securities Taiwan Co., Ltd. (“CA Taiwan”), CLSA/CA Taiwan's analysts and/or their associates do and from time to time seek to establish business or financial relationships with companies covered in their research reports. As a result, investors should be aware that CLSA and/or such individuals may have one or more conflicts of interests that could affect the objectivity of this report. Regulations or market practice of some jurisdictions/markets prescribe certain disclosures to be made for certain actual, potential or perceived conflicts of interests relating to research reports and such details are available at www.clsa.com/member/research_disclosures/. Disclosures therein include the position of CLSA, CLSA Americas, LLC and CA Taiwan only and do not reflect those of CITIC Securities International Company Limited, Credit Agricole Corporate & Investment Bank and/or their respective affiliates. If investors have any difficulty accessing this website, please contact [email protected] or +852 2600 8111. If you require disclosure information on previous dates, please contact

IMPORTANT: The content of this report is subject to and should be read in conjunction with the disclaimer and CLSA's Legal and Regulatory Notices as set out at www.clsa.com/disclaimer.html, a hard copy of which may be obtained on request from CLSA Publications or CLSA Compliance Group (18/F, One Pacific Place, 88 Queensway, Hong Kong, telephone +852 2600 8888) and/or CA Taiwan Compliance (27/F, 95, Section 2 Dun Hua South Road, Taipei 10682, Taiwan, telephone +886 2 2326 8188). 05/08/2013

©2013 CLSA Limited (for research compiled by non-Taiwan analyst(s)) and/or Credit Agricole Securities Taiwan Co., Ltd (for research compiled by Taiwan Note: In the interests of timeliness, this document has not been

Prepared for: ThomsonReuters

[email protected] FIRST LAST 11/04/13 12:33:55 AM Samsung Information Systems of

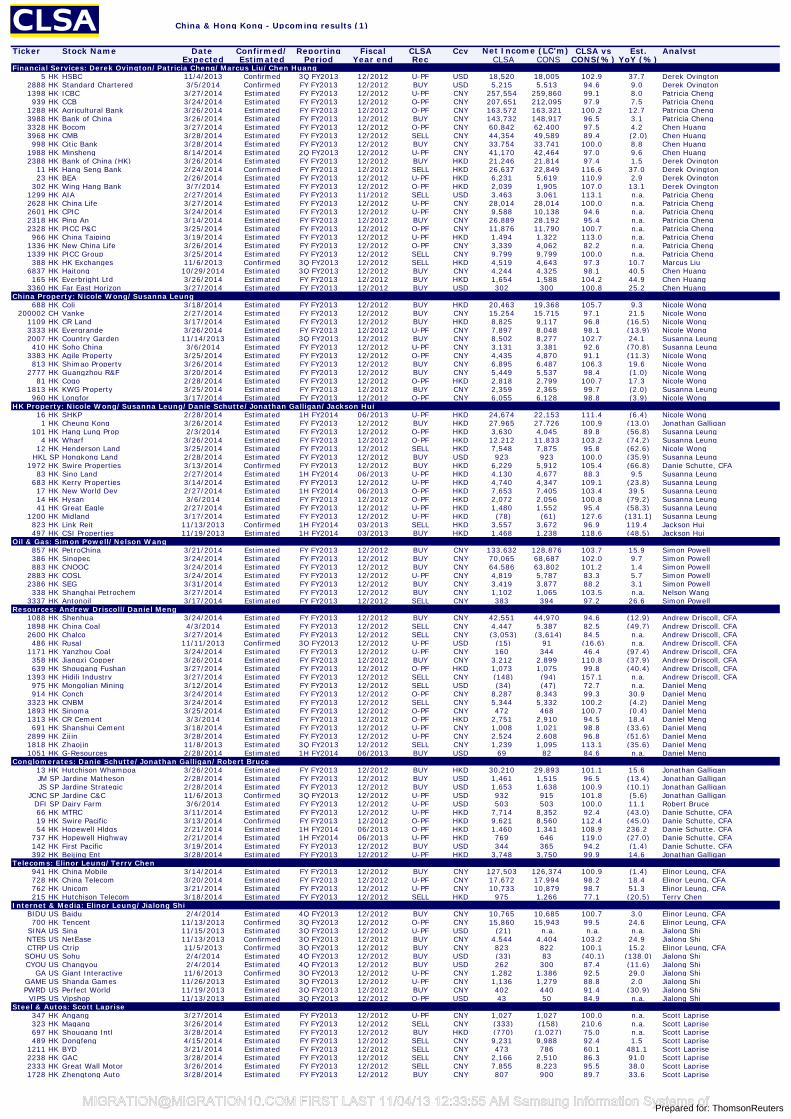

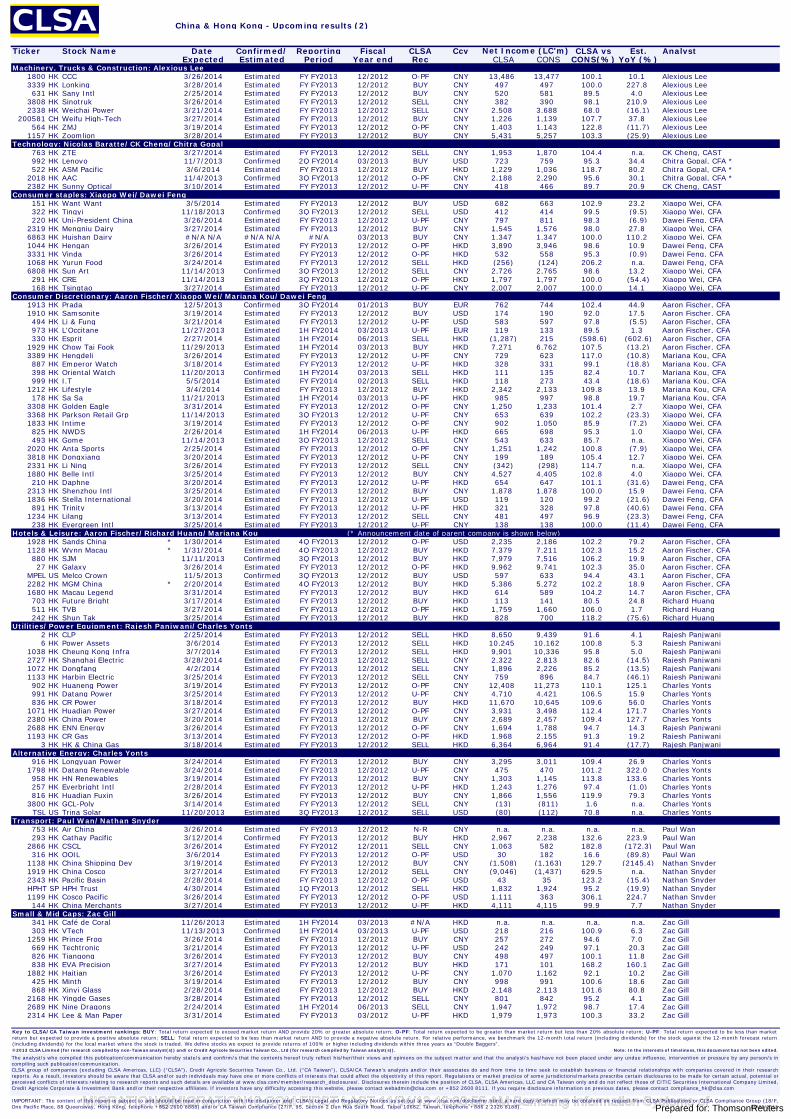

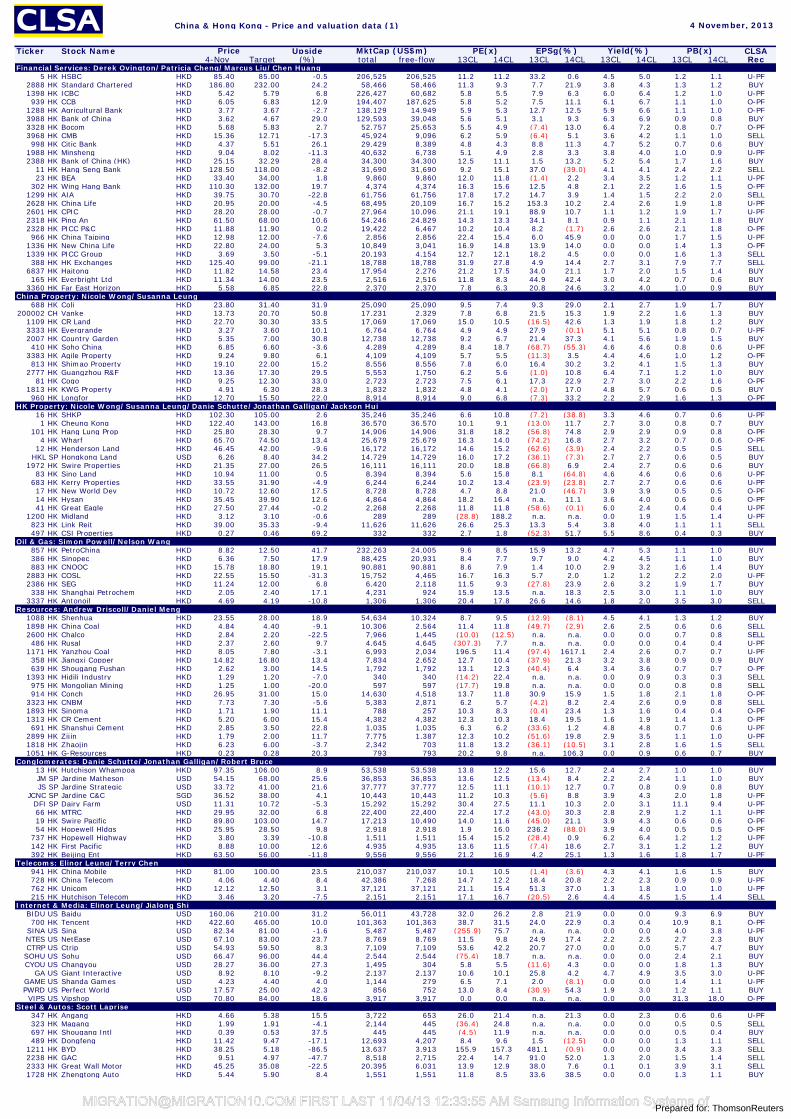

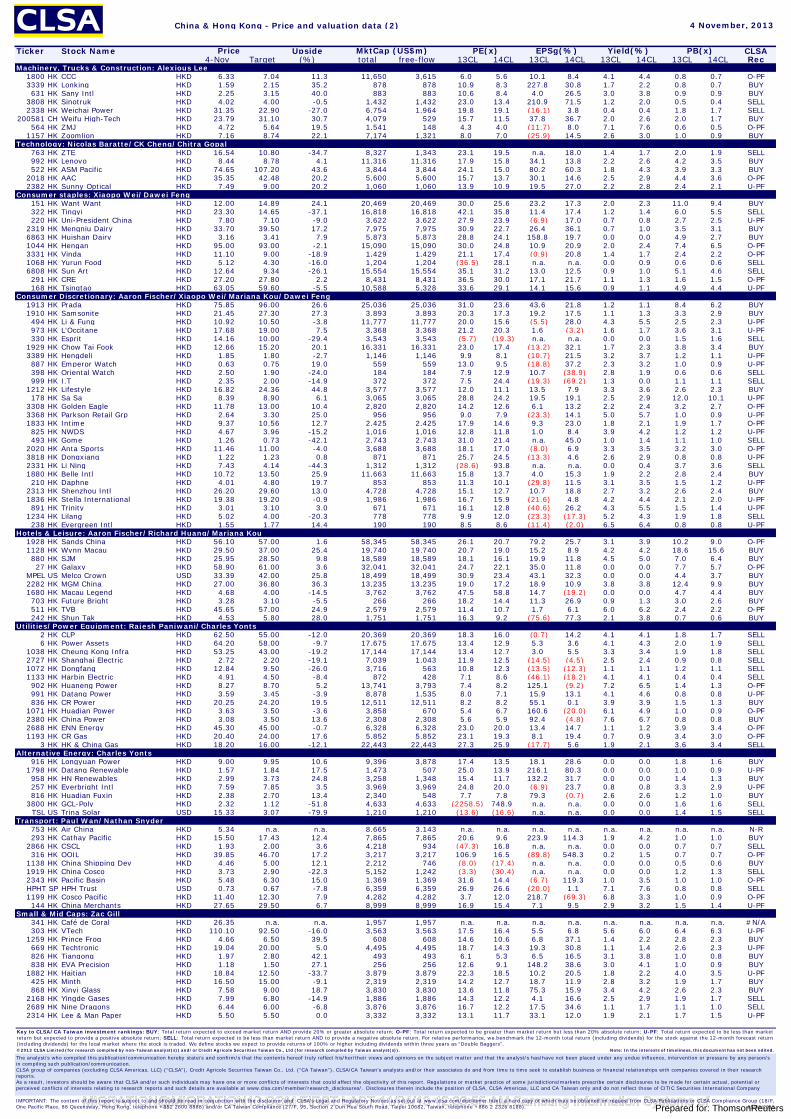

China & Hong Kong - Upcoming results (1)

Ticker Stock Name Date Confirmed/ Reporting Fiscal CLSA Ccy CLSA vs Est. AnalystExpected Estimated Period Year end Rec CLSA CONS CONS(%) YoY (%)

Financial Services: Derek Ovington/Patricia Cheng/Marcus Liu/Chen Huang5 HK HSBC 11/4/2013 Confirmed 3Q FY2013 12/2012 U-PF USD 18,520 18,005 102.9 37.7 Derek Ovington

2888 HK Standard Chartered 3/5/2014 Confirmed FY FY2013 12/2012 BUY USD 5,215 5,513 94.6 9.0 Derek Ovington1398 HK ICBC 3/27/2014 Estimated FY FY2013 12/2012 U-PF CNY 257,554 259,860 99.1 8.0 Patricia Cheng939 HK CCB 3/24/2014 Estimated FY FY2013 12/2012 O-PF CNY 207,651 212,095 97.9 7.5 Patricia Cheng

1288 HK Agricultural Bank 3/26/2014 Estimated FY FY2013 12/2012 O-PF CNY 163,572 163,321 100.2 12.7 Patricia Cheng3988 HK Bank of China 3/26/2014 Estimated FY FY2013 12/2012 BUY CNY 143,732 148,917 96.5 3.1 Patricia Cheng3328 HK Bocom 3/27/2014 Estimated FY FY2013 12/2012 O-PF CNY 60,842 62,400 97.5 4.2 Chen Huang3968 HK CMB 3/28/2014 Estimated FY FY2013 12/2012 SELL CNY 44,354 49,589 89.4 (2.0) Chen Huang998 HK Citic Bank 3/28/2014 Estimated FY FY2013 12/2012 BUY CNY 33,754 33,741 100.0 8.8 Chen Huang

1988 HK Minsheng 8/14/2014 Estimated 2Q FY2013 12/2012 U-PF CNY 41,170 42,464 97.0 9.6 Chen Huang2388 HK Bank of China (HK) 3/26/2014 Estimated FY FY2013 12/2012 BUY HKD 21,246 21,814 97.4 1.5 Derek Ovington

11 HK Hang Seng Bank 2/24/2014 Confirmed FY FY2013 12/2012 SELL HKD 26,637 22,849 116.6 37.0 Derek Ovington23 HK BEA 2/26/2014 Estimated FY FY2013 12/2012 U-PF HKD 6,231 5,619 110.9 2.9 Derek Ovington

302 HK Wing Hang Bank 3/7/2014 Estimated FY FY2013 12/2012 O-PF HKD 2,039 1,905 107.0 13.1 Derek Ovington1299 HK AIA 2/27/2014 Estimated FY FY2013 11/2012 SELL USD 3,463 3,061 113.1 n.a. Patricia Cheng2628 HK China Life 3/27/2014 Estimated FY FY2013 12/2012 U-PF CNY 28,014 28,014 100.0 n.a. Patricia Cheng2601 HK CPIC 3/24/2014 Estimated FY FY2013 12/2012 U-PF CNY 9,588 10,138 94.6 n.a. Patricia Cheng2318 HK Ping An 3/14/2014 Estimated FY FY2013 12/2012 BUY CNY 26,889 28,192 95.4 n.a. Patricia Cheng2328 HK PICC P&C 3/25/2014 Estimated FY FY2013 12/2012 O-PF CNY 11,876 11,790 100.7 n.a. Patricia Cheng966 HK China Taiping 3/19/2014 Estimated FY FY2013 12/2012 U-PF HKD 1,494 1,322 113.0 n.a. Patricia Cheng

1336 HK New China Life 3/26/2014 Estimated FY FY2013 12/2012 O-PF CNY 3,339 4,062 82.2 n.a. Patricia Cheng1339 HK PICC Group 3/25/2014 Estimated FY FY2013 12/2012 SELL CNY 9,799 9,799 100.0 n.a. Patricia Cheng388 HK HK Exchanges 11/6/2013 Confirmed 3Q FY2013 12/2012 SELL HKD 4,519 4,643 97.3 10.7 Marcus Liu

6837 HK Haitong 10/29/2014 Estimated 3Q FY2013 12/2012 BUY CNY 4,244 4,325 98.1 40.5 Chen Huang165 HK Everbright Ltd 3/26/2014 Estimated FY FY2013 12/2012 BUY HKD 1,654 1,588 104.2 44.9 Chen Huang

3360 HK Far East Horizon 3/27/2014 Estimated FY FY2013 12/2012 BUY USD 302 300 100.8 25.2 Chen HuangChina Property: Nicole Wong/Susanna Leung

688 HK Coli 3/18/2014 Estimated FY FY2013 12/2012 BUY HKD 20,463 19,368 105.7 9.3 Nicole Wong200002 CH Vanke 2/27/2014 Estimated FY FY2013 12/2012 BUY CNY 15,254 15,715 97.1 21.5 Nicole Wong

1109 HK CR Land 3/17/2014 Estimated FY FY2013 12/2012 BUY HKD 8,825 9,117 96.8 (16.5) Nicole Wong3333 HK Evergrande 3/26/2014 Estimated FY FY2013 12/2012 U-PF CNY 7,897 8,048 98.1 (13.9) Nicole Wong2007 HK Country Garden 11/14/2013 Estimated 3Q FY2013 12/2012 BUY CNY 8,502 8,277 102.7 24.1 Susanna Leung410 HK Soho China 3/6/2014 Estimated FY FY2013 12/2012 U-PF CNY 3,131 3,381 92.6 (70.8) Susanna Leung

3383 HK Agile Property 3/25/2014 Estimated FY FY2013 12/2012 O-PF CNY 4,435 4,870 91.1 (11.3) Nicole Wong813 HK Shimao Property 3/26/2014 Estimated FY FY2013 12/2012 BUY CNY 6,895 6,487 106.3 19.6 Nicole Wong

2777 HK Guangzhou R&F 3/20/2014 Estimated FY FY2013 12/2012 BUY CNY 5,449 5,537 98.4 (1.0) Nicole Wong81 HK Cogo 2/28/2014 Estimated FY FY2013 12/2012 O-PF HKD 2,818 2,799 100.7 17.3 Nicole Wong

1813 HK KWG Property 3/25/2014 Estimated FY FY2013 12/2012 BUY CNY 2,359 2,365 99.7 (2.0) Susanna Leung960 HK Longfor 3/17/2014 Estimated FY FY2013 12/2012 O-PF CNY 6,055 6,128 98.8 (3.9) Nicole Wong

HK Property: Nicole Wong/Susanna Leung/Danie Schutte/Jonathan Galligan/Jackson Hui16 HK SHKP 2/28/2014 Estimated 1H FY2014 06/2013 U-PF HKD 24,674 22,153 111.4 (6.4) Nicole Wong1 HK Cheung Kong 3/26/2014 Estimated FY FY2013 12/2012 BUY HKD 27,965 27,726 100.9 (13.0) Jonathan Galligan

101 HK Hang Lung Prop 2/3/2014 Estimated FY FY2013 12/2012 O-PF HKD 3,630 4,045 89.8 (56.8) Susanna Leung4 HK Wharf 3/26/2014 Estimated FY FY2013 12/2012 O-PF HKD 12,212 11,833 103.2 (74.2) Susanna Leung

12 HK Henderson Land 3/25/2014 Estimated FY FY2013 12/2012 SELL HKD 7,548 7,875 95.8 (62.6) Nicole WongHKL SP Hongkong Land 2/28/2014 Estimated FY FY2013 12/2012 BUY USD 923 923 100.0 (35.9) Susanna Leung

1972 HK Swire Properties 3/13/2014 Confirmed FY FY2013 12/2012 BUY HKD 6,229 5,912 105.4 (66.8) Danie Schutte, CFA83 HK Sino Land 2/27/2014 Estimated 1H FY2014 06/2013 U-PF HKD 4,130 4,677 88.3 9.5 Susanna Leung

683 HK Kerry Properties 3/14/2014 Estimated FY FY2013 12/2012 U-PF HKD 4,740 4,347 109.1 (23.8) Susanna Leung17 HK New World Dev 2/27/2014 Estimated 1H FY2014 06/2013 O-PF HKD 7,653 7,405 103.4 39.5 Susanna Leung14 HK Hysan 3/6/2014 Estimated FY FY2013 12/2012 O-PF HKD 2,072 2,056 100.8 (79.2) Susanna Leung41 HK Great Eagle 2/27/2014 Estimated FY FY2013 12/2012 U-PF HKD 1,480 1,552 95.4 (58.3) Susanna Leung

1200 HK Midland 3/17/2014 Estimated FY FY2013 12/2012 U-PF HKD (78) (61) 127.6 (131.1) Susanna Leung823 HK Link Reit 11/13/2013 Confirmed 1H FY2014 03/2013 SELL HKD 3,557 3,672 96.9 119.4 Jackson Hui497 HK CSI Properties 11/19/2013 Estimated 1H FY2014 03/2013 BUY HKD 1,468 1,238 118.6 (48.5) Jackson Hui

Oil & Gas: Simon Powell/Nelson Wang857 HK PetroChina 3/21/2014 Estimated FY FY2013 12/2012 BUY CNY 133,632 128,876 103.7 15.9 Simon Powell386 HK Sinopec 3/24/2014 Estimated FY FY2013 12/2012 BUY CNY 70,065 68,687 102.0 9.7 Simon Powell883 HK CNOOC 3/24/2014 Estimated FY FY2013 12/2012 BUY CNY 64,586 63,802 101.2 1.4 Simon Powell

2883 HK COSL 3/24/2014 Estimated FY FY2013 12/2012 U-PF CNY 4,819 5,787 83.3 5.7 Simon Powell2386 HK SEG 3/31/2014 Estimated FY FY2013 12/2012 BUY CNY 3,419 3,877 88.2 3.1 Simon Powell338 HK Shanghai Petrochem 3/27/2014 Estimated FY FY2013 12/2012 BUY CNY 1,102 1,065 103.5 n.a. Nelson Wang

3337 HK Antonoil 3/17/2014 Estimated FY FY2013 12/2012 SELL CNY 383 394 97.2 26.6 Simon PowellResources: Andrew Driscoll/Daniel Meng

1088 HK Shenhua 3/24/2014 Estimated FY FY2013 12/2012 BUY CNY 42,551 44,970 94.6 (12.9) Andrew Driscoll, CFA1898 HK China Coal 4/3/2014 Estimated FY FY2013 12/2012 SELL CNY 4,447 5,387 82.5 (49.7) Andrew Driscoll, CFA2600 HK Chalco 3/27/2014 Estimated FY FY2013 12/2012 SELL CNY (3,053) (3,614) 84.5 n.a. Andrew Driscoll, CFA486 HK Rusal 11/11/2013 Confirmed 3Q FY2013 12/2012 U-PF USD (15) 91 (16.6) n.a. Andrew Driscoll, CFA

1171 HK Yanzhou Coal 3/24/2014 Estimated FY FY2013 12/2012 U-PF CNY 160 344 46.4 (97.4) Andrew Driscoll, CFA358 HK Jiangxi Copper 3/26/2014 Estimated FY FY2013 12/2012 BUY CNY 3,212 2,899 110.8 (37.9) Andrew Driscoll, CFA639 HK Shougang Fushan 3/27/2014 Estimated FY FY2013 12/2012 O-PF HKD 1,073 1,075 99.8 (40.4) Andrew Driscoll, CFA

1393 HK Hidili Industry 3/27/2014 Estimated FY FY2013 12/2012 SELL CNY (148) (94) 157.1 n.a. Andrew Driscoll, CFA975 HK Mongolian Mining 3/12/2014 Estimated FY FY2013 12/2012 SELL USD (34) (47) 72.7 n.a. Daniel Meng914 HK Conch 3/24/2014 Estimated FY FY2013 12/2012 O-PF CNY 8,287 8,343 99.3 30.9 Daniel Meng

3323 HK CNBM 3/24/2014 Estimated FY FY2013 12/2012 SELL CNY 5,344 5,332 100.2 (4.2) Daniel Meng1893 HK Sinoma 3/25/2014 Estimated FY FY2013 12/2012 O-PF CNY 472 468 100.7 (0.4) Daniel Meng1313 HK CR Cement 3/3/2014 Estimated FY FY2013 12/2012 O-PF HKD 2,751 2,910 94.5 18.4 Daniel Meng691 HK Shanshui Cement 3/18/2014 Estimated FY FY2013 12/2012 U-PF CNY 1,008 1,021 98.8 (33.6) Daniel Meng

2899 HK Zijin 3/28/2014 Estimated FY FY2013 12/2012 U-PF CNY 2,524 2,608 96.8 (51.6) Daniel Meng1818 HK Zhaojin 11/8/2013 Estimated 3Q FY2013 12/2012 SELL CNY 1,239 1,095 113.1 (35.6) Daniel Meng1051 HK G-Resources 2/28/2014 Estimated 1H FY2014 06/2013 BUY USD 69 82 84.6 n.a. Daniel Meng

Conglomerates: Danie Schutte/Jonathan Galligan/Robert Bruce13 HK Hutchison Whampoa 3/26/2014 Estimated FY FY2013 12/2012 BUY HKD 30,210 29,893 101.1 15.6 Jonathan GalliganJM SP Jardine Matheson 2/28/2014 Estimated FY FY2013 12/2012 BUY USD 1,461 1,515 96.5 (13.4) Jonathan GalliganJS SP Jardine Strategic 2/28/2014 Estimated FY FY2013 12/2012 BUY USD 1,653 1,638 100.9 (10.1) Jonathan Galligan

JCNC SP Jardine C&C 11/6/2013 Confirmed 3Q FY2013 12/2012 U-PF USD 932 915 101.8 (5.6) Jonathan GalliganDFI SP Dairy Farm 3/6/2014 Estimated FY FY2013 12/2012 U-PF USD 503 503 100.0 11.1 Robert Bruce66 HK MTRC 3/11/2014 Estimated FY FY2013 12/2012 U-PF HKD 7,714 8,352 92.4 (43.0) Danie Schutte, CFA19 HK Swire Pacific 3/13/2014 Confirmed FY FY2013 12/2012 O-PF HKD 9,621 8,560 112.4 (45.0) Danie Schutte, CFA54 HK Hopewell Hldgs 2/21/2014 Estimated 1H FY2014 06/2013 O-PF HKD 1,460 1,341 108.9 236.2 Danie Schutte, CFA

737 HK Hopewell Highway 2/21/2014 Estimated 1H FY2014 06/2013 U-PF HKD 769 646 119.0 (27.0) Danie Schutte, CFA142 HK First Pacific 3/19/2014 Estimated FY FY2013 12/2012 BUY USD 344 365 94.2 (1.4) Danie Schutte, CFA392 HK Beijing Ent 3/28/2014 Estimated FY FY2013 12/2012 U-PF HKD 3,748 3,750 99.9 14.6 Jonathan Galligan

Telecoms: Elinor Leung/Terry Chen941 HK China Mobile 3/14/2014 Estimated FY FY2013 12/2012 BUY CNY 127,503 126,374 100.9 (1.4) Elinor Leung, CFA728 HK China Telecom 3/20/2014 Estimated FY FY2013 12/2012 U-PF CNY 17,672 17,994 98.2 18.4 Elinor Leung, CFA762 HK Unicom 3/21/2014 Estimated FY FY2013 12/2012 U-PF CNY 10,733 10,879 98.7 51.3 Elinor Leung, CFA215 HK Hutchison Telecom 3/18/2014 Estimated FY FY2013 12/2012 SELL HKD 975 1,266 77.1 (20.5) Terry Chen

Internet & Media: Elinor Leung/Jialong ShiBIDU US Baidu 2/4/2014 Estimated 4Q FY2013 12/2012 BUY CNY 10,765 10,685 100.7 3.0 Elinor Leung, CFA700 HK Tencent 11/13/2013 Confirmed 3Q FY2013 12/2012 O-PF CNY 15,860 15,943 99.5 24.6 Elinor Leung, CFA