Embed Size (px)

Citation preview

© 2016 IHS Markit. All Rights Reserved. © 2016 IHS Markit. All Rights Reserved.

China smartphone market dynamic

and local panel makers strategy The supply chain dynamic and intensive investment

Nov.3th , 2016

Terry Yu, Senior Analyst

IHS Markit | Technology

© 2016 IHS Markit. All Rights Reserved.

2

Ou

tline

s

Brand transfer wave and supply chain adjustment

in China domestic market

Major panel makers strategy outlook

© 2016 IHS Markit. All Rights Reserved.

3

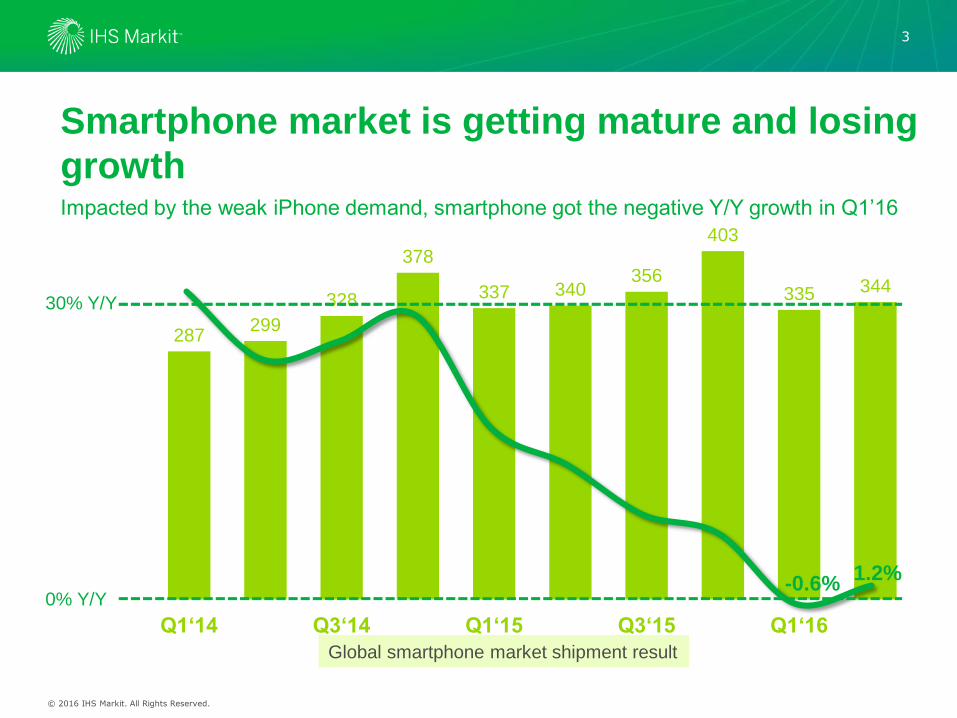

Smartphone market is getting mature and losing

growth Impacted by the weak iPhone demand, smartphone got the negative Y/Y growth in Q1’16

Global smartphone market shipment result

287 299

328

378

337 340 356

403

335 344

0

50

100

150

200

250

300

350

400

450

Q1‘14 Q3‘14 Q1‘15 Q3‘15 Q1‘16

-0.6%1.2%

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

30% Y/Y

0% Y/Y

© 2016 IHS Markit. All Rights Reserved.

4

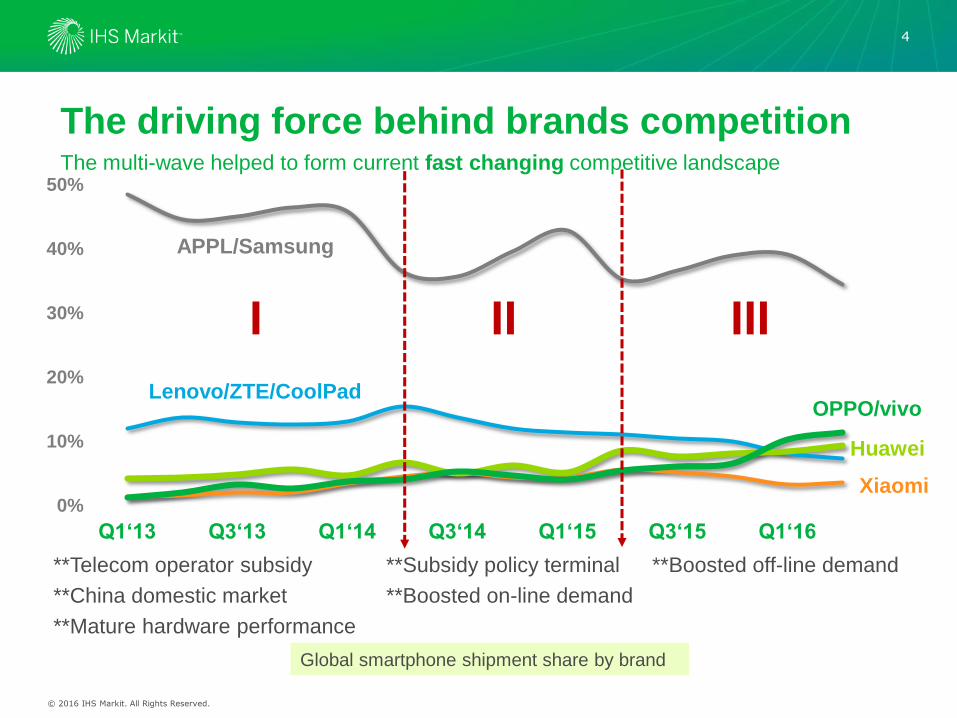

The driving force behind brands competition The multi-wave helped to form current fast changing competitive landscape

Global smartphone shipment share by brand

**Subsidy policy terminal

**Boosted on-line demand

**Boosted off-line demand

0%

10%

20%

30%

40%

50%

Q1‘13 Q3‘13 Q1‘14 Q3‘14 Q1‘15 Q3‘15 Q1‘16

I II III

OPPO/vivo

APPL/Samsung

Xiaomi

Huawei

Lenovo/ZTE/CoolPad

**Telecom operator subsidy

**China domestic market

**Mature hardware performance

© 2016 IHS Markit. All Rights Reserved.

5

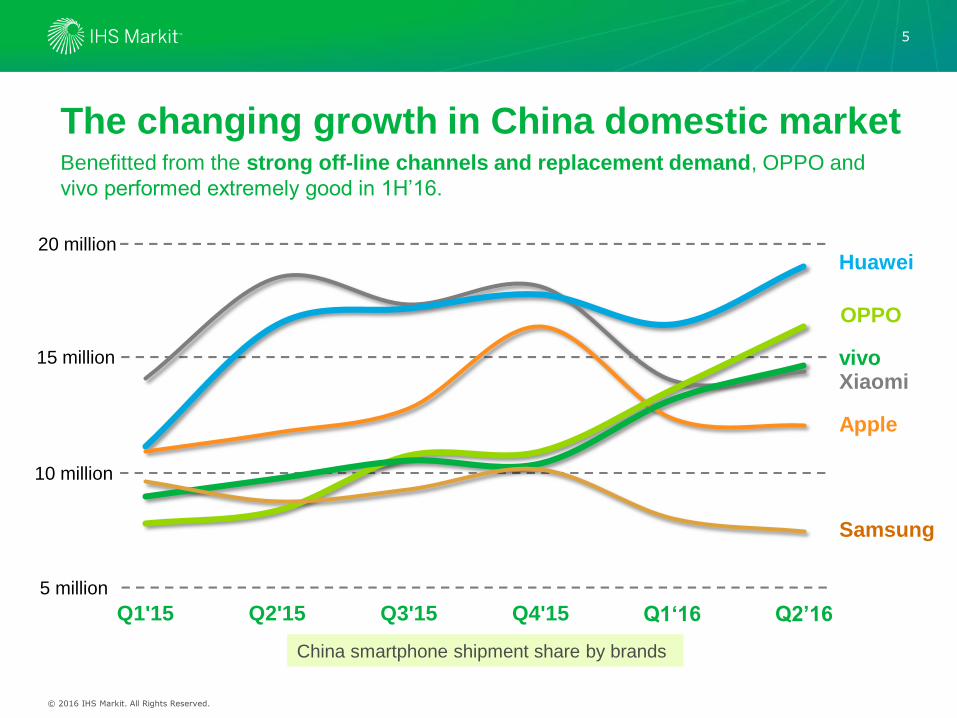

The changing growth in China domestic market Benefitted from the strong off-line channels and replacement demand, OPPO and

vivo performed extremely good in 1H’16.

China smartphone shipment share by brands

5

10

15

20

Q1'15 Q2'15 Q3'15 Q4'15 Q1‘16 Q2’16

Xiaomi

Huawei

Apple

OPPO

vivo

Samsung

5 million

10 million

15 million

20 million

OPPO

Huawei

vivoXiaomi

Apple

Samsung

© 2016 IHS Markit. All Rights Reserved.

6

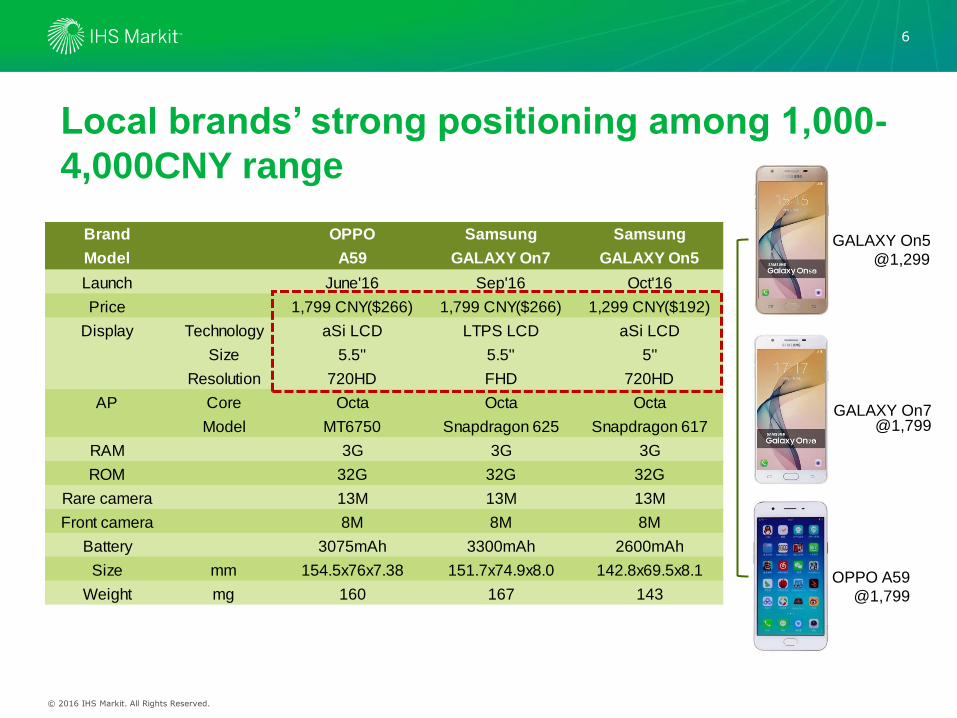

Local brands’ strong positioning among 1,000-

4,000CNY range

Brand OPPO Samsung Samsung

Model A59 GALAXY On7 GALAXY On5

Launch June'16 Sep'16 Oct'16

Price 1,799 CNY($266) 1,799 CNY($266) 1,299 CNY($192)

Display Technology aSi LCD LTPS LCD aSi LCD

Size 5.5'' 5.5'' 5''

Resolution 720HD FHD 720HD

AP Core Octa Octa Octa

Model MT6750 Snapdragon 625 Snapdragon 617

RAM 3G 3G 3G

ROM 32G 32G 32G

Rare camera 13M 13M 13M

Front camera 8M 8M 8M

Battery 3075mAh 3300mAh 2600mAh

Size mm 154.5x76x7.38 151.7x74.9x8.0 142.8x69.5x8.1

Weight mg 160 167 143

GALAXY On7

GALAXY On5

OPPO A59

@1,299

@1,799

@1,799

© 2016 IHS Markit. All Rights Reserved.

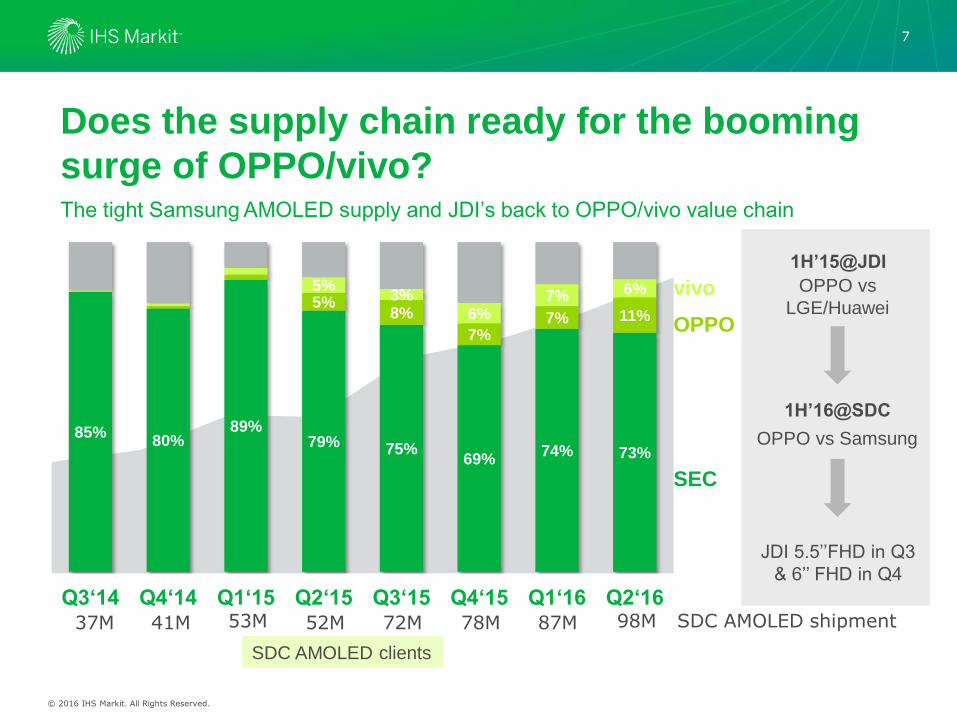

7

Does the supply chain ready for the booming

surge of OPPO/vivo? The tight Samsung AMOLED supply and JDI’s back to OPPO/vivo value chain

1H’15@JDI

OPPO vs

LGE/Huawei

1H’16@SDC

OPPO vs Samsung

JDI 5.5’’FHD in Q3

& 6’’ FHD in Q4

SDC AMOLED clients

SEC

85%80%

89%79% 75%

69%74% 73%

5%8%

7%7% 11%

5%3%

6%7% 6%

Q3‘14 Q4‘14 Q1‘15 Q2‘15 Q3‘15 Q4‘15 Q1‘16 Q2‘1637M 41M 53M 52M 72M 78M 87M 98M SDC AMOLED shipment

OPPO

vivo

© 2016 IHS Markit. All Rights Reserved.

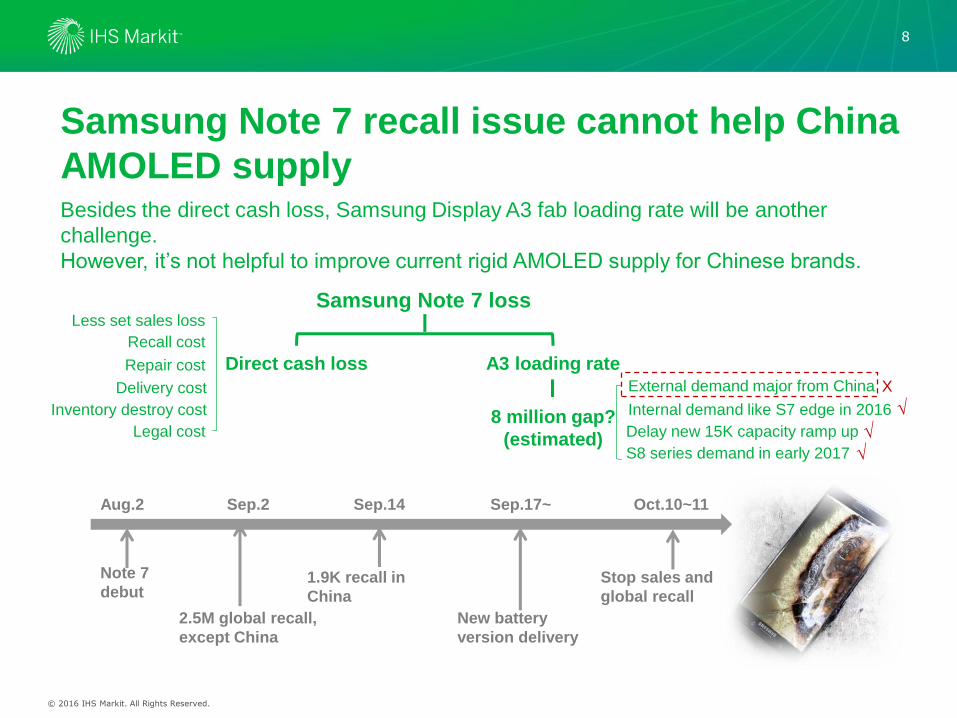

8

Samsung Note 7 recall issue cannot help China

AMOLED supply Besides the direct cash loss, Samsung Display A3 fab loading rate will be another

challenge.

However, it’s not helpful to improve current rigid AMOLED supply for Chinese brands.

Aug.2

Note 7

debut

2.5M global recall,

except China

Sep.2 Sep.14

1.9K recall in

China

Sep.17~

New battery

version delivery

Oct.10~11

Stop sales and

global recall

Samsung Note 7 loss

Direct cash loss A3 loading rate

Less set sales loss

Recall cost

Repair cost

Delivery cost

Inventory destroy cost 8 million gap?

(estimated)

External demand major from China

Internal demand like S7 edge in 2016

Delay new 15K capacity ramp up

√

√

X

S8 series demand in early 2017 √

Legal cost

© 2016 IHS Markit. All Rights Reserved.

9

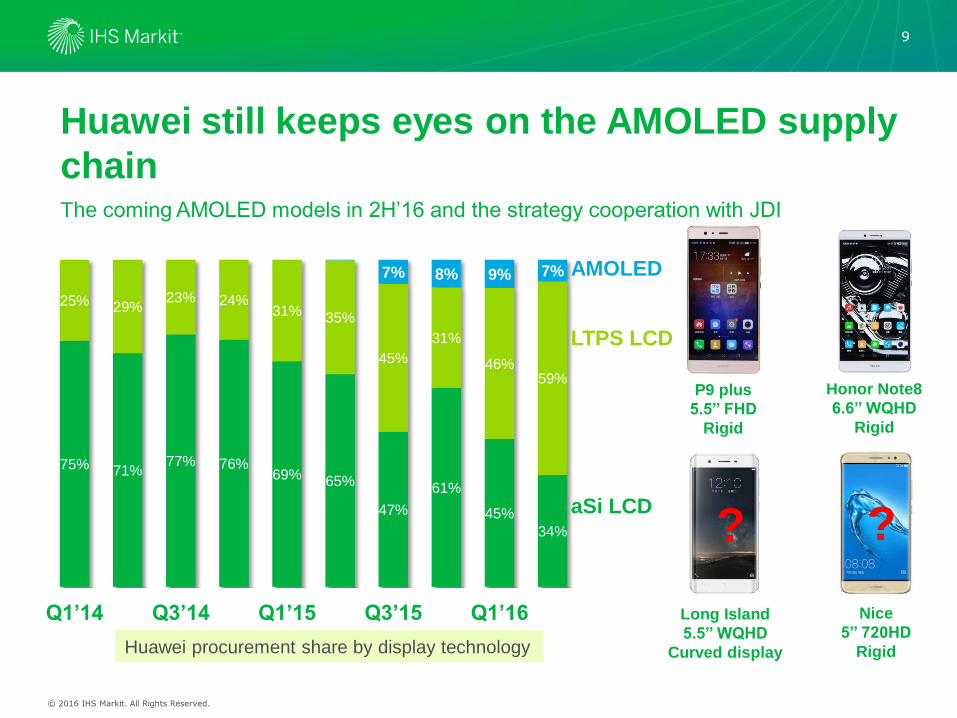

Huawei still keeps eyes on the AMOLED supply

chain The coming AMOLED models in 2H’16 and the strategy cooperation with JDI

? ?

Long Island

5.5’’ WQHD

Curved display

Nice

5’’ 720HD

Rigid Huawei procurement share by display technology

P9 plus

5.5’’ FHD

Rigid

Honor Note8

6.6’’ WQHD

Rigid

75% 71%77% 76%

69% 65%

47%

61%

45%

34%

25% 29%23% 24%

31% 35%

45%

31%

46%59%

7% 8% 9% 7%

Q1’14 Q3’14 Q1’15 Q3’15 Q1’16

aSi LCD

LTPS LCD

AMOLED

© 2016 IHS Markit. All Rights Reserved.

10

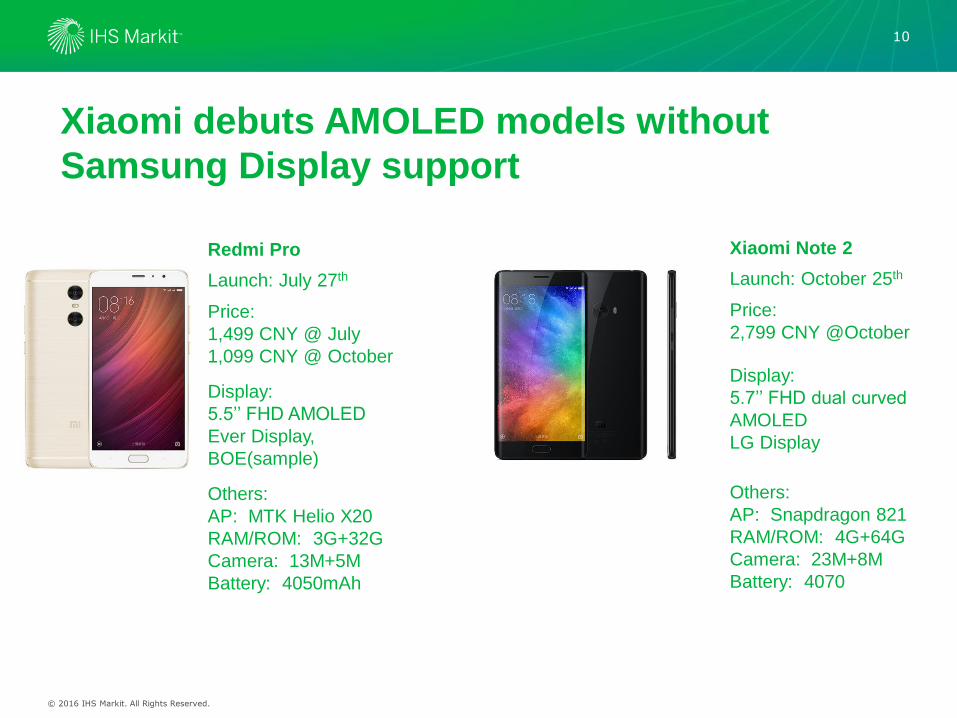

Xiaomi debuts AMOLED models without

Samsung Display support

Redmi Pro

Launch: July 27th

Price:

1,499 CNY @ July

1,099 CNY @ October

Display:

5.5’’ FHD AMOLED

Ever Display,

BOE(sample)

Others:

AP: MTK Helio X20

RAM/ROM: 3G+32G

Camera: 13M+5M

Battery: 4050mAh

Xiaomi Note 2

Launch: October 25th

Price:

2,799 CNY @October

Display:

5.7’’ FHD dual curved

AMOLED

LG Display

Others:

AP: Snapdragon 821

RAM/ROM: 4G+64G

Camera: 23M+8M

Battery: 4070

© 2016 IHS Markit. All Rights Reserved.

11

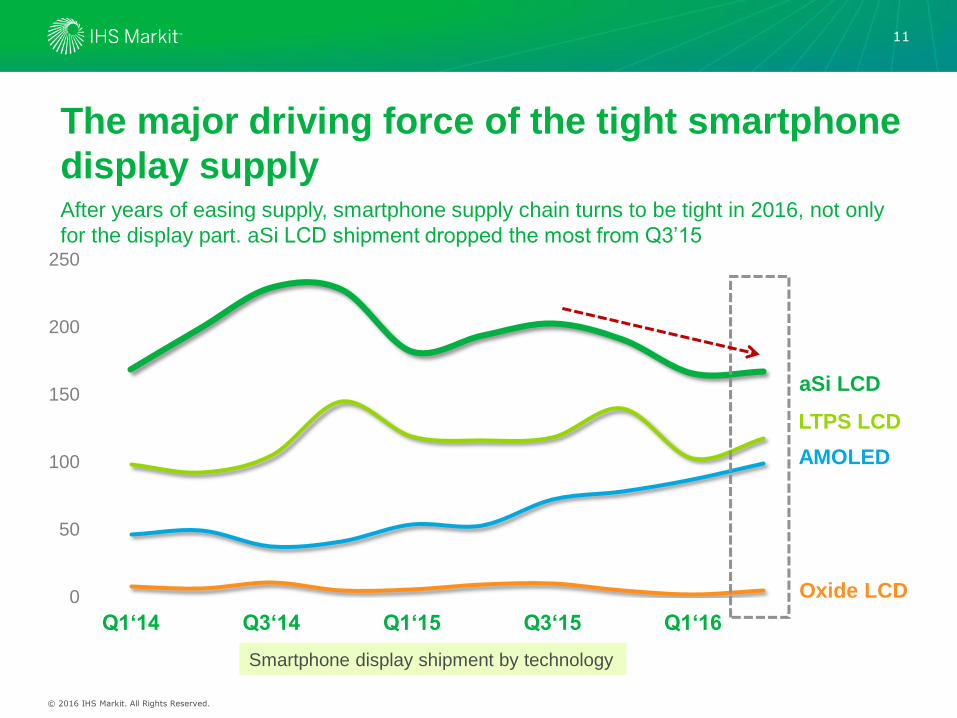

The major driving force of the tight smartphone

display supply

Smartphone display shipment by technology

After years of easing supply, smartphone supply chain turns to be tight in 2016, not only

for the display part. aSi LCD shipment dropped the most from Q3’15

0

50

100

150

200

250

Q1‘14 Q3‘14 Q1‘15 Q3‘15 Q1‘16

aSi LCD

LTPS LCD

AMOLED

Oxide LCD

© 2016 IHS Markit. All Rights Reserved.

12

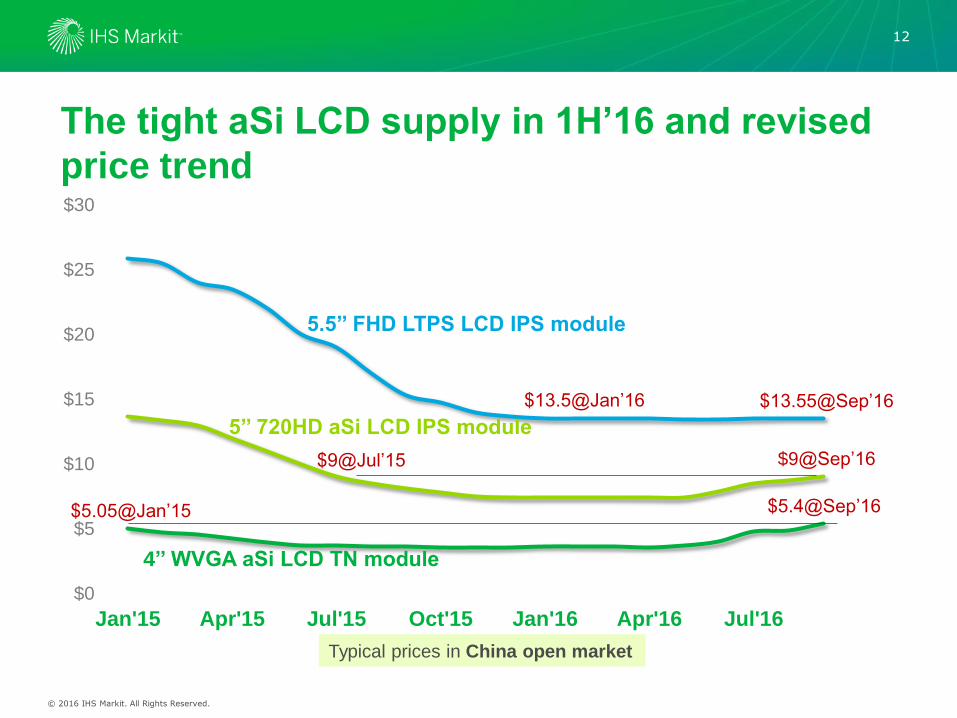

The tight aSi LCD supply in 1H’16 and revised

price trend

Typical prices in China open market

$0

$5

$10

$15

$20

$25

$30

Jan'15 Apr'15 Jul'15 Oct'15 Jan'16 Apr'16 Jul'16

5.5’’ FHD LTPS LCD IPS module

5’’ 720HD aSi LCD IPS module

4’’ WVGA aSi LCD TN module

$5.4@Sep’16$5.05@Jan’15

$9@Sep’16$9@Jul’15

$13.55@Sep’16$13.5@Jan’16

© 2016 IHS Markit. All Rights Reserved.

13

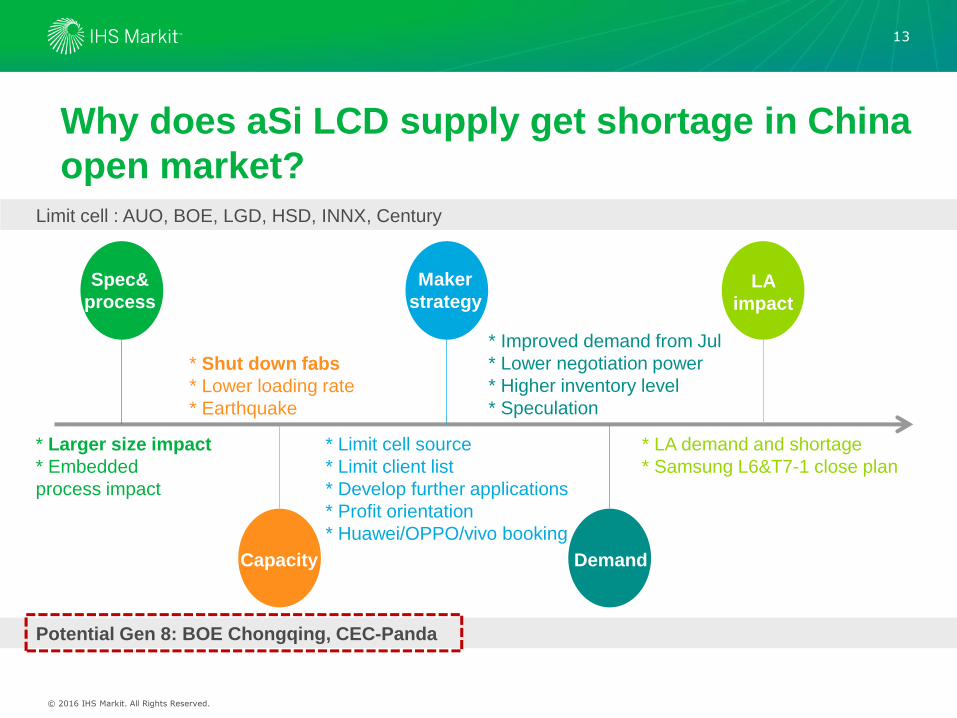

Why does aSi LCD supply get shortage in China

open market?

Spec&

process

Maker

strategyLA

impact

DemandCapacity

* Larger size impact

* Embedded

process impact

* Shut down fabs

* Lower loading rate

* Earthquake

* Limit cell source

* Limit client list

* Develop further applications

* Profit orientation

* Huawei/OPPO/vivo booking

* Improved demand from Jul

* Lower negotiation power

* Higher inventory level

* Speculation

* LA demand and shortage

* Samsung L6&T7-1 close plan

Limit cell : AUO, BOE, LGD, HSD, INNX, Century

Potential Gen 8: BOE Chongqing, CEC-Panda

© 2016 IHS Markit. All Rights Reserved.

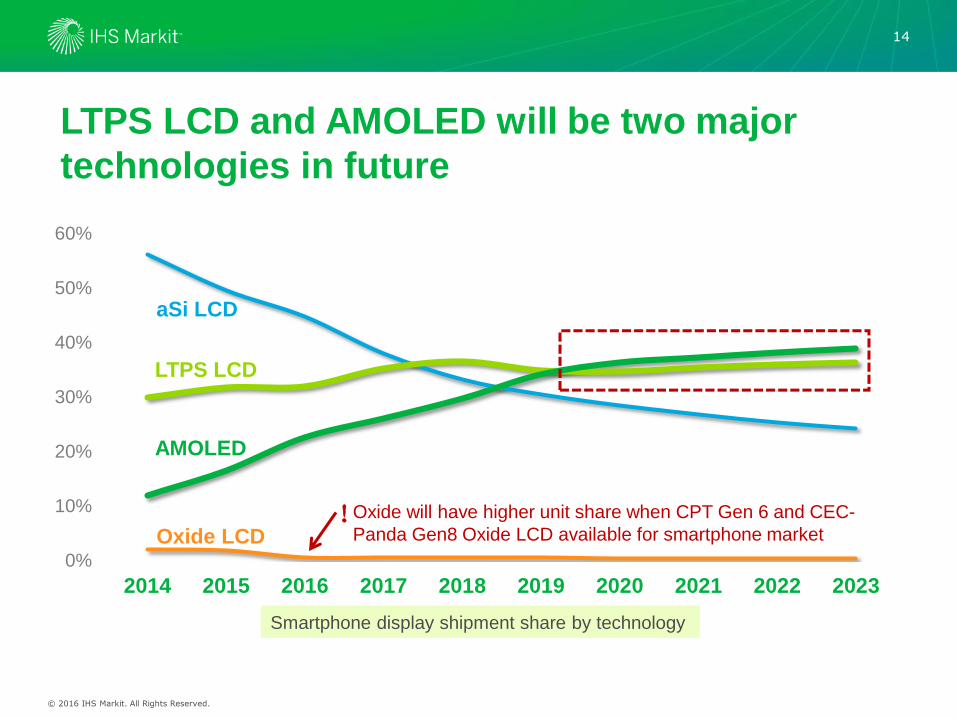

14

LTPS LCD and AMOLED will be two major

technologies in future

Smartphone display shipment share by technology

0%

10%

20%

30%

40%

50%

60%

2014 2015 2016 2017 2018 2019 2020 2021 2022 2023

Oxide will have higher unit share when CPT Gen 6 and CEC-

Panda Gen8 Oxide LCD available for smartphone market!

LTPS LCD

AMOLED

aSi LCD

Oxide LCD

© 2016 IHS Markit. All Rights Reserved.

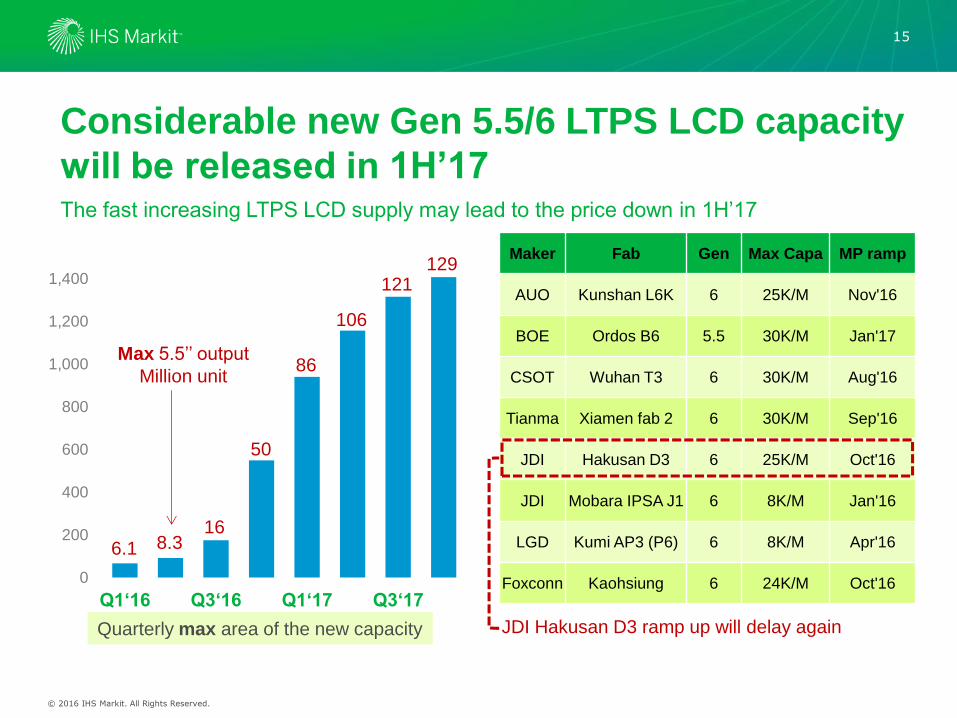

15

Considerable new Gen 5.5/6 LTPS LCD capacity

will be released in 1H’17 The fast increasing LTPS LCD supply may lead to the price down in 1H’17

0

200

400

600

800

1,000

1,200

1,400

1,600

Q1‘16 Q3‘16 Q1‘17 Q3‘17

Maker Fab Gen Max Capa MP ramp

AUO Kunshan L6K 6 25K/M Nov'16

BOE Ordos B6 5.5 30K/M Jan'17

CSOT Wuhan T3 6 30K/M Aug'16

Tianma Xiamen fab 2 6 30K/M Sep'16

JDI Hakusan D3 6 25K/M Oct'16

JDI Mobara IPSA J1 6 8K/M Jan'16

LGD Kumi AP3 (P6) 6 8K/M Apr'16

Foxconn Kaohsiung 6 24K/M Oct'16

Quarterly max area of the new capacity

6.1 8.316

50

86

106

121129

Max 5.5’’ output

Million unit

JDI Hakusan D3 ramp up will delay again

© 2016 IHS Markit. All Rights Reserved.

16

Ou

tline

s

Brand transfer wave and supply chain adjustment

in China domestic market

Major panel makers strategy outlook

© 2016 IHS Markit. All Rights Reserved.

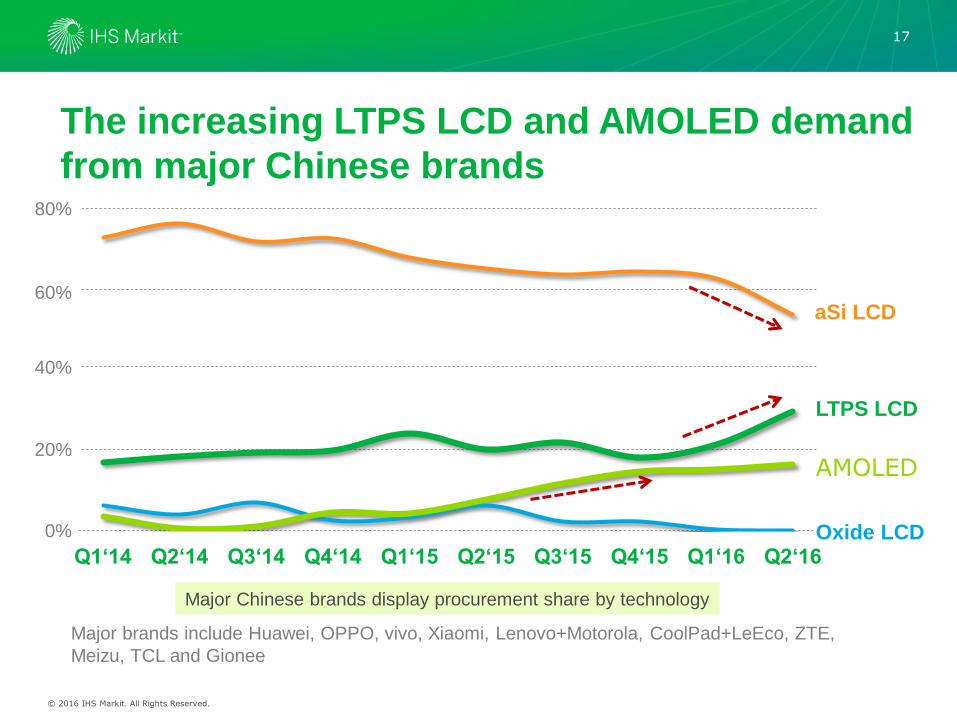

17

The increasing LTPS LCD and AMOLED demand

from major Chinese brands

Major Chinese brands display procurement share by technology

Major brands include Huawei, OPPO, vivo, Xiaomi, Lenovo+Motorola, CoolPad+LeEco, ZTE,

Meizu, TCL and Gionee

80%

60%

40%

20%

0%0%

20%

40%

60%

80%

Q1‘14 Q2‘14 Q3‘14 Q4‘14 Q1‘15 Q2‘15 Q3‘15 Q4‘15 Q1‘16 Q2‘16

aSi LCD

LTPS LCD

AMOLED

Oxide LCD

© 2016 IHS Markit. All Rights Reserved.

18

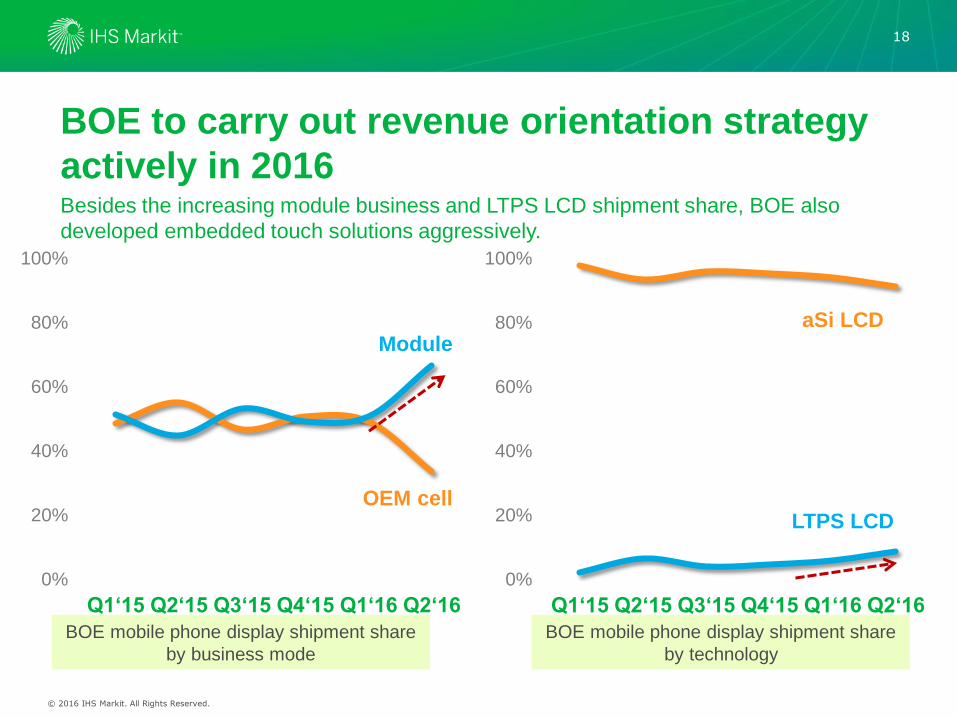

BOE to carry out revenue orientation strategy

actively in 2016 Besides the increasing module business and LTPS LCD shipment share, BOE also

developed embedded touch solutions aggressively.

BOE mobile phone display shipment share

by business mode

BOE mobile phone display shipment share

by technology

0%

20%

40%

60%

80%

100%

Q1‘15 Q2‘15 Q3‘15 Q4‘15 Q1‘16 Q2‘16

0%

20%

40%

60%

80%

100%

Q1‘15 Q2‘15 Q3‘15 Q4‘15 Q1‘16 Q2‘16

OEM cell

Module

LTPS LCD

aSi LCD

© 2016 IHS Markit. All Rights Reserved.

19

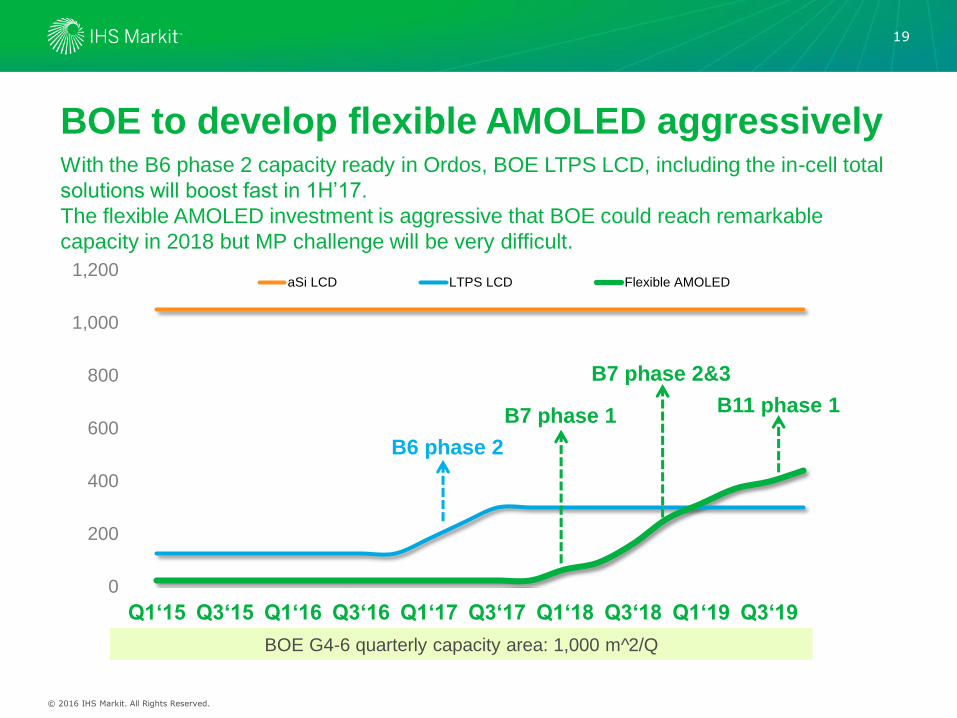

BOE to develop flexible AMOLED aggressively With the B6 phase 2 capacity ready in Ordos, BOE LTPS LCD, including the in-cell total

solutions will boost fast in 1H’17.

The flexible AMOLED investment is aggressive that BOE could reach remarkable

capacity in 2018 but MP challenge will be very difficult.

BOE G4-6 quarterly capacity area: 1,000 m^2/Q

0

200

400

600

800

1,000

1,200

Q1‘15 Q3‘15 Q1‘16 Q3‘16 Q1‘17 Q3‘17 Q1‘18 Q3‘18 Q1‘19 Q3‘19

aSi LCD LTPS LCD Flexible AMOLED

B6 phase 2

B7 phase 1

B7 phase 2&3

B11 phase 1

© 2016 IHS Markit. All Rights Reserved.

20

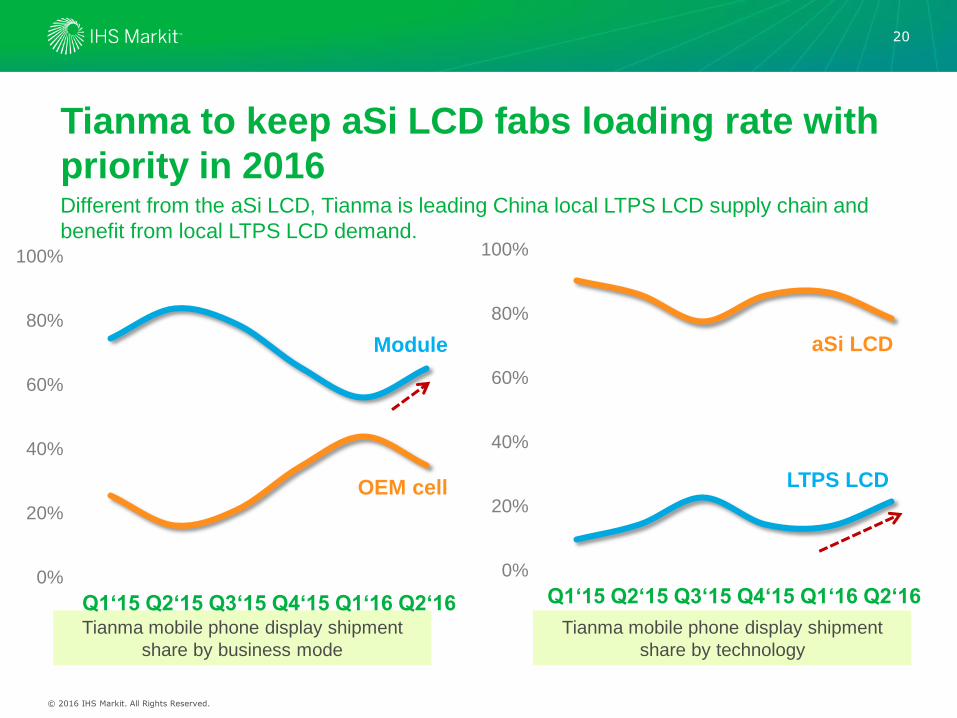

Tianma to keep aSi LCD fabs loading rate with

priority in 2016 Different from the aSi LCD, Tianma is leading China local LTPS LCD supply chain and

benefit from local LTPS LCD demand.

Tianma mobile phone display shipment

share by business mode

Tianma mobile phone display shipment

share by technology

0%

20%

40%

60%

80%

100%

Q1‘15 Q2‘15 Q3‘15 Q4‘15 Q1‘16 Q2‘16

0%

20%

40%

60%

80%

100%

Q1‘15 Q2‘15 Q3‘15 Q4‘15 Q1‘16 Q2‘16

OEM cell

Module

LTPS LCD

aSi LCD

© 2016 IHS Markit. All Rights Reserved.

21

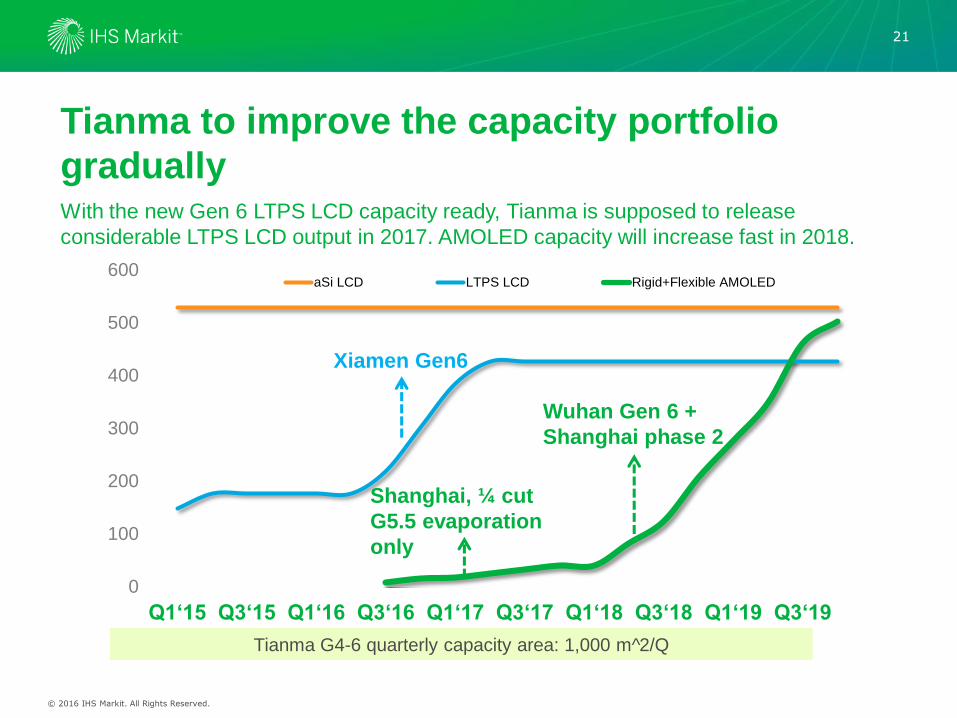

Tianma to improve the capacity portfolio

gradually With the new Gen 6 LTPS LCD capacity ready, Tianma is supposed to release

considerable LTPS LCD output in 2017. AMOLED capacity will increase fast in 2018.

Tianma G4-6 quarterly capacity area: 1,000 m^2/Q

0

100

200

300

400

500

600

Q1‘15 Q3‘15 Q1‘16 Q3‘16 Q1‘17 Q3‘17 Q1‘18 Q3‘18 Q1‘19 Q3‘19

aSi LCD LTPS LCD Rigid+Flexible AMOLED

Xiamen Gen6

Wuhan Gen 6 +

Shanghai phase 2

Shanghai, ¼ cut

G5.5 evaporation

only

© 2016 IHS Markit. All Rights Reserved.

22

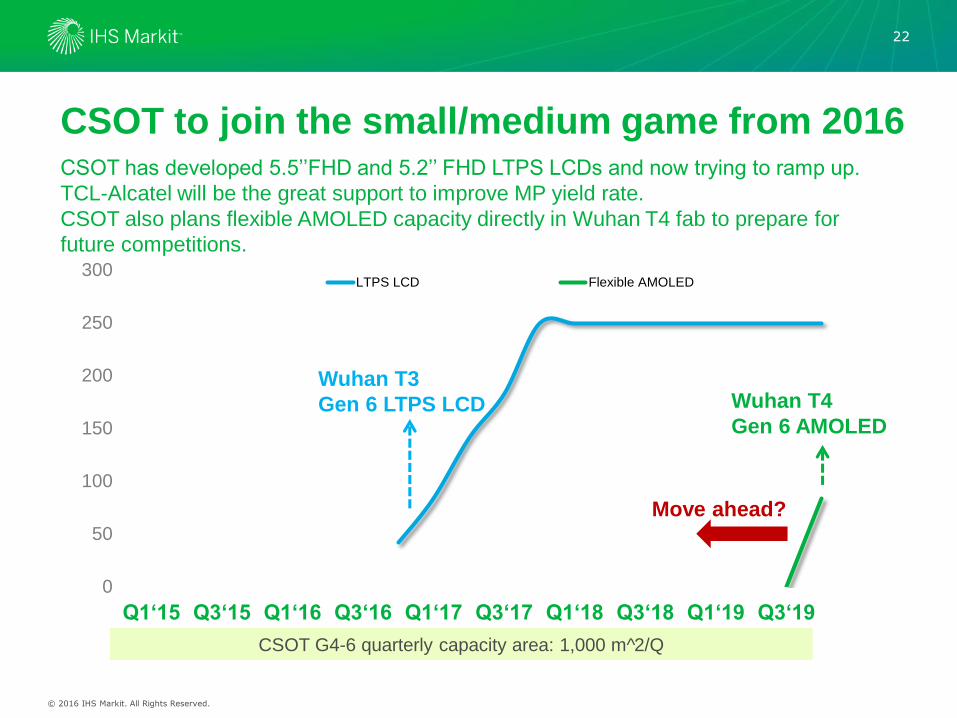

CSOT to join the small/medium game from 2016 CSOT has developed 5.5’’FHD and 5.2’’ FHD LTPS LCDs and now trying to ramp up.

TCL-Alcatel will be the great support to improve MP yield rate.

CSOT also plans flexible AMOLED capacity directly in Wuhan T4 fab to prepare for

future competitions.

CSOT G4-6 quarterly capacity area: 1,000 m^2/Q

0

50

100

150

200

250

300

Q1‘15 Q3‘15 Q1‘16 Q3‘16 Q1‘17 Q3‘17 Q1‘18 Q3‘18 Q1‘19 Q3‘19

LTPS LCD Flexible AMOLED

Wuhan T3

Gen 6 LTPS LCD Wuhan T4

Gen 6 AMOLED

Move ahead?

© 2016 IHS Markit. All Rights Reserved.

23

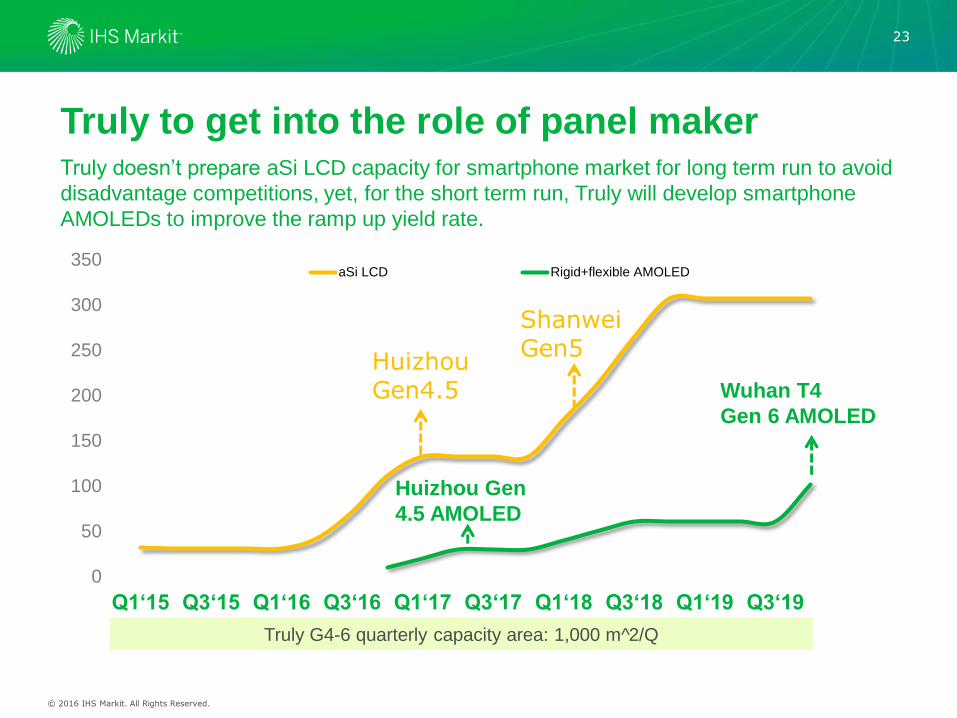

Truly to get into the role of panel maker Truly doesn’t prepare aSi LCD capacity for smartphone market for long term run to avoid

disadvantage competitions, yet, for the short term run, Truly will develop smartphone

AMOLEDs to improve the ramp up yield rate.

Truly G4-6 quarterly capacity area: 1,000 m^2/Q

0

50

100

150

200

250

300

350

Q1‘15 Q3‘15 Q1‘16 Q3‘16 Q1‘17 Q3‘17 Q1‘18 Q3‘18 Q1‘19 Q3‘19

aSi LCD Rigid+flexible AMOLED

Huizhou Gen4.5 Wuhan T4

Gen 6 AMOLED

ShanweiGen5

Huizhou Gen

4.5 AMOLED

© 2016 IHS Markit. All Rights Reserved.

24

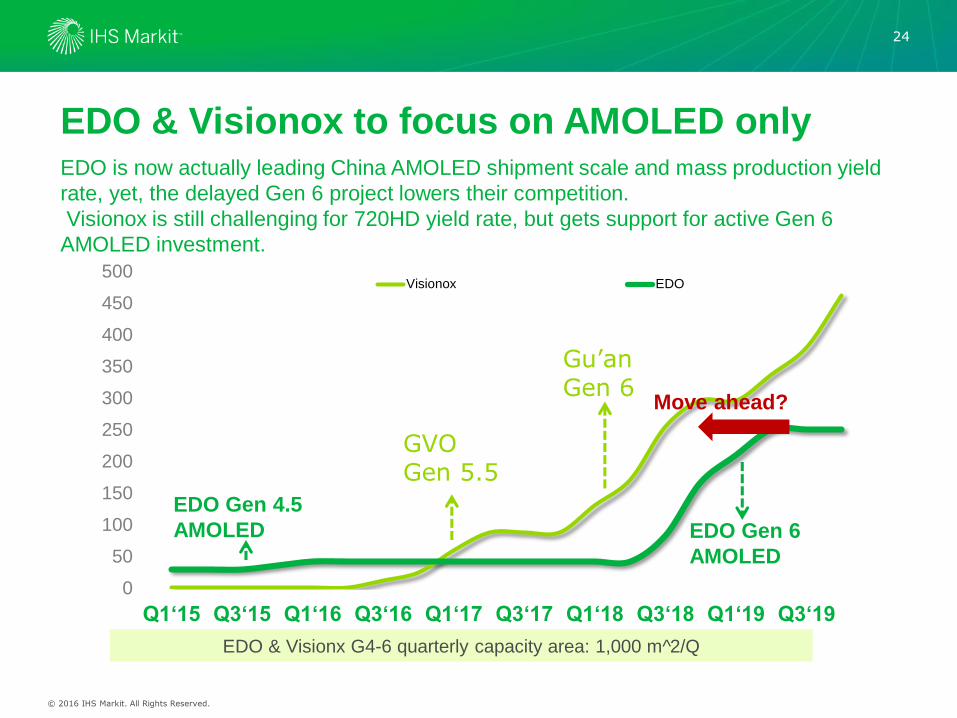

EDO & Visionox to focus on AMOLED only EDO is now actually leading China AMOLED shipment scale and mass production yield

rate, yet, the delayed Gen 6 project lowers their competition.

Visionox is still challenging for 720HD yield rate, but gets support for active Gen 6

AMOLED investment.

EDO & Visionx G4-6 quarterly capacity area: 1,000 m^2/Q

0

50

100

150

200

250

300

350

400

450

500

Q1‘15 Q3‘15 Q1‘16 Q3‘16 Q1‘17 Q3‘17 Q1‘18 Q3‘18 Q1‘19 Q3‘19

Visionox EDO

GVO Gen 5.5

EDO Gen 6

AMOLED

Gu’anGen 6

EDO Gen 4.5

AMOLED

Move ahead?

© 2016 IHS Markit. All Rights Reserved.

25

Terry Yu

Senior Analyst

IHS Markit | Technology | Small/Medium & AMOLED

Thank You