Embed Size (px)

Citation preview

China Structured Finance Quarterly – 2Q16

1www.fitchratings.com | September 2016

China Structured Finance Quarterly – 2Q16

Contents

Ben McCarthy +61 2 8256 0388 [email protected]

Contacts: Analytical

Contacts: Business Relationship Management

Kit Chan +852 2263 9970 [email protected]

Kan Zhou +8610 8517 2112 [email protected]

Market Update 2Regulatory Update 4Fitch Ratings Criteria Update 5Auto-Loan ABS and RMBS Issuance in 2Q16 6Shelf Registration and Draw Down 7Chinese Auto ABS Performance: Defaults 8Chinese Auto ABS Performance: Delinquency 9Chinese Auto ABS Performance: Prepayment 10Chinese RMBS Performance: Defaults 11Chinese RMBS Performance: Delinquency 12Chinese RMBS Performance: Prepayment 13Fitch Criteria and Research Relevant to China 14 Henry Hung

+86 21 5097 3080 [email protected]

Hilary Tan +852 2263 9904 [email protected]

Grace Li +852 2263 9936 [email protected]

2www.fitchratings.com | September 2016

China Structured Finance Quarterly – 2Q16

Issuance in China’s structured finance market was CNY193.4bn (USD29.8bn) in 2Q16, representing a 102% increase from 1Q16 and 96% yoy growth. More diversified asset-classes featured in the second quarter’s issuance and Fitch Ratings expects the structured finance market to continue expanding in both scope and scale in 2H16.

Of total 2Q16 issuance, 52% was under the China Securities Regulatory Commission regulated Asset-Backed Specific Plan (ABSP) scheme and was largely undertaken by corporates. A further 46% of 2Q16 issuance was under the Credit Asset Securitization (CAS) scheme, governed by the People’s Bank of China (PBoC) and China Banking Regulatory Commission (CBRC), and used by financial institutions. The remaining 2% are asset-backed notes (ABN), which are regulated by the National Association of Financial Market Institutional Investors (NAFMII). The ABSP scheme issuance was up by approximately 242% yoy, while issuance under the CAS scheme rose by 43% yoy, the lower growth due to further falls in collaterised loan obligation (CLO) issuance. The CLO asset-class has dropped by 58% yoy due to weak corporate borrowing demand.

Marked growth in residential mortgage-backed securities (RMBS) issuance volume was the main driver for CAS scheme issuance in 2Q16. Three RMBS issues totalling CNY40.9bn were completed, exceeding the total volume of RMBS issues in 2015. Two of the deals were from housing provident funds and one was from a commercial bank. We expect RMBS issuance to continue increasing in 2H16. Postal Savings Bank of China Co Ltd, China’s sixth biggest commercial bank, issued a CNY3.8bn RMBS transaction in July 2016. This was the first Fitch-rated China RMBS transaction.

There were six Chinese auto-loan asset-backed security (ABS) transactions in the quarter, with total issuance of nearly CNY16bn. The number of issuers doubled from 1Q15, although issue volume was down by 7% yoy. ABS as a funding source has been used by thirteen auto-finance companies and banks as at end-2Q16, two of which used securitisation for the first time in 2Q16. Fitch expects auto-loan ABS issuance to remain strong in the coming quarters, with two auto-finance companies obtaining shelf registration in 2Q16 and one in July 2016. Some issuers are also reaching or have already reached their registered quota limits. SAIC-GMAC Automotive Finance Company Limited is the first company to receive registration quota for the second time.

Issuance in 2Q16 was highlighted by three non-performing loans (NPL) ABS transactions, the first of their kind in China since 2008. One was collateralised by trade finance NPLs originated by Bank of China Ltd. (A/Stable) and the other two by credit card and SME NPLs originated by China Merchants Bank (BBB/Stable). The three NPL ABS deals were pilot transactions, as the regulators restricted the market during the 2008 global financial crisis. Fitch expects more NPL ABS to be launched in the near-term, as the government has granted quotas of CNY50bn to six commercial banks to help them deal with rising NPL ratios. The NPL ratios of China’s commercial banks have risen for eight consecutive quarters, to 1.75% at end-2Q16.

There were two ABN securitisation deals closed in 2Q16 in China’s interbank bond market (CIBM). The ABN market was started in 2012 and is an instrument for non-financial corporates to issue notes in the CIBM. The two transactions utilised a special-purpose trust structured that is similar to auto-loan ABS transactions. The opening up of the interbank securitisation market to non-financial corporates leads Fitch to expect a continued flow of ABN issuance, as it provides a deeper investor-base than the stock-exchange bond market. Fitch also expects this to lead to further expansion of asset-types securitised in China.

The performance of outstanding auto-loan ABS and RMBS transactions remains stable. The highest default rate from all auto-loan ABS issues reached approximately 1.6% (see Chinese Auto ABS Performance: Defaults) and slightly less than 1% for all RMBS issues as at end-2Q16. Recent transactions are not yet sufficiently mature to provide meaningful performance data, though Fitch has not observed any significant deterioration in the credit-quality of newly issued rated auto-loan ABS.

Market Update

3www.fitchratings.com | September 2016

China Structured Finance Quarterly – 2Q16

Market Update (continued)

6

66

106

15

22

0

20

40

60

80

100

120

0

100

200

300

400

500

2013 2014 2015 2Q15 2Q16

(CNYbn)

Credit Asset Securitisation IssuanceCorporate loans Auto loansResidential mortgage loans Consumer loans / credit cardsOthers No. of issuances (RHS)

Source: Wind Info, Fitch

Issuances No.

8

28

212

37

84

0

50

100

150

200

250

0

100

200

300

400

500

2013 2014 2015 2Q15 2Q16

(CNYbn)

Asset Backed Specific Plan IssuanceRental Lease Infrastructure charges Account receivablesTrust certificates SME private debts OthersNo. of issuances (RHS)

Source: Wind Info, Fitch

Issuances No.

The below charts demonstrate the gradual shift from a CLO-dominated market to a more asset-diversified market. In addition to auto loans, we have also seen an increase in the proportion of

residential mortgages and consumer loans/credit cards. Fitch expects RMBS issuance to continue increasing in 2H16.

4www.fitchratings.com | September 2016

China Structured Finance Quarterly – 2Q16

Regulatory Update

China Further Opens-Up Bond Market: PBoC and the State Administration of Foreign Exchange published rules in May 2016 to give most foreign financial institutions quota-free access to the CIBM to promote foreign funds inflow and RMBS globalisation. Investing in CIBM is no longer subject to prior approval for eligible foreign institutional investors, with only filing requirements needing to be fulfilled.

Central Bank Support for Consumer Finance Development: To implement State Council of the People’s Republic of China’s guidance on new consumption development and to fulfill associated financial needs, PBoC and CBRC issued guidelines on 30 March 2016 to enhance support for consumer finance. The guidelines specifically encourage innovation of consumer credit products. Auto-finance companies can provide extra financing to augmented products appertaining to the purchased vehicles, such as navigation equipment, charging facility, extended warranties and vehicle insurance.

According to Fitch’s Global Consumer ABS Rating Criteria, set-off risk may arise where the originator and debtor are parties to another contract that relates to securitised receivables; for example, if the insurance premiums are financed upfront by the securitised loan agreement and repaid by the borrowers over the term of the loan. Fitch expects the legal risks of set-off to be addressed in a transaction legal opinion.

The guidelines also encourage securitisation of various asset types, including auto-loan, consumer credit and credit cards, to diversify funding sources, revitalise existing credit, expand the scope of consumer credit and improve credit supply capability.

Second-Tier Cities Tighten Home-Purchase Rules: Suzhou, a city west of Shanghai, is initiating home-purchase restrictions to curb surging home-prices that have occurred since February 2016. This follows Shanghai, Shenzhen, Wuhan and Nanjing, which tightened rules on home-purchases in March 2016. Hefei and Xiamen are also likely to release new policies to shield the local housing market from speculators after the recent hike in home prices.

Differentiated Land-Supply Policies: The Ministry of Land and Resources stated in the 13th Five-Year Plan for Land and Resources, released on 12 April 2016, that land supply for residential use will be lowered – or even suspended – in cities where a high level of housing inventory exists and moderately increased where housing supply barely meets – or lags – demand. Fitch believes China’s government is attempting to manage housing supply and, in turn, prices across the market, due to the wide price gap and divergent trends between first- and second-tier cities and third- and fourth-tier cities.

Central Government Supports Residential Leasing: China’s State Council released new guidelines on residential-property leasing on 3 June 2016, which allow developers to convert commercial properties to residential-leasing units. It also offers value-added tax reductions or exemptions to landlords and encourages the development of home-leasing companies.

5www.fitchratings.com | September 2016

China Structured Finance Quarterly – 2Q16

Fitch updated the Counterparty Criteria for Structured Finance and Covered Bonds and Counterparty Criteria for Structured Finance and Covered Bonds: Derivative Addendum on 18 July 2016. Both criteria outline Fitch’s approach to counterparty risk in structured finance transactions and covered bond programmes.

Fitch separates counterparties into three categories, based on the role of each entity in the transaction:

1. Direct support counterparties, for example, issuer account banks or liquidity facility providers

2. Derivative counterparties, for example, swap providers

3. Indirect support counterparties, for example, collection account banks or servicers.

Fitch expects derivative counterparties and direct support counterparties to meet the key characteristics outlined in the table below. The minimum ratings shown in the table are not directly applicable to entities acting as indirect support counterparties. While indirect support counterparties are expected to have adequate operational capacities, the minimum rating is assessed taking into account the nature of the exposure and the presence of other structural mitigants within each transaction. At the time of assigning new ratings, Fitch expects counterparties with a rating at the minimum level for a given note rating to

demonstrate advanced preparation of remedial actions. Once the lower minimum eligibility counterparty ratings are met, Fitch further assess counterparty risks in the transaction from aspects such as commitment to remedial action, timing of remedial actions, availability of replacement counterparties and counterparty excessive exposure. See “Counterparty Criteria for Structured Finance and Covered Bonds” for more detail.

Fitch also articulates the collateralisation criteria, how to determine the collateral amount, advance rates and termination payments in the “Counterparty Criteria for Structured Finance and Covered Bonds: Derivative Addendum”. For auto ABS transactions Fitch has rated so far where the highest achieved rating has been ‘AAsf’, the minimum direct support counterparty rating should be ‘A-’ or ‘F1’. In RMBS transactions where the highest achieved rating is ‘A+sf’, the minimum rating should be ‘BBB’ or ‘F2’.

This article represents a brief summary of Fitch’s counterparty criteria. Market participants wanting to fully understand Fitch’s criteria should review the full report titled “Counterparty Criteria for Structured Finance and Covered Bonds” and “Counterparty Criteria for Structured Finance” and “Covered Bonds: Derivative Addendum” at www.fitchratings.com

Fitch Ratings Criteria Update

Minimum Direct Support and Derivative Counterparty Long-Term or Short-Term Issuer Default Rating1,2

Category of highest-rated note3 Without collateral With collateral – Flip Clause With collateral – No Flip clause

AAAsf A or F1 BBB− or F3 BBB+ or F2

AAsf A− or F1 BBB− or F3 BBB+ or F2

Asf BBB or F2 BB+ BBB or F2

BBBsf BBB− or F3 BB− BBB- or F3

BBsf Note rating B+ BB-

Bsf Note rating B- B- Source: Fitch 1 In case of third-parties guaranteeing the obligations of a derivative counterparty, Fitch considers the highest of the guarantor’s and counterparty’s rating. For example, ‘AAAsf’ bonds can be supported by a ‘BBB-’ entity guaranteeing a collateralised derivative provider (or post collateral itself). 2 Special considerations apply for banks rated ‘AA-’ or ‘F1+’. See “Counterparty Criteria for Structured Finance and Covered Bonds: Derivative Addendum” - Specific Considerations for Highly-Rated Banks section3 For example, an issuer account bank rated ‘BBB’ or ‘F2’ can support a sf note rated up to ‘A+sf’, but not ‘AA-sf’.

6www.fitchratings.com | September 2016

China Structured Finance Quarterly – 2Q16

Auto-Loan ABS and RMBS Issuance in 2Q16

Auto-Loan ABS Issuance

Originator / seriesOriginal note balance

(CNYm)Credit enhancement to highest rated Note (%)

Weighted average LTV at origination (%)

Weighted average seasoning

at cut-off dates (months)Weighted average

original term (months)Average loan size at

origination (CNY)

Ford 2016-1 2,977 (USD458)

13.8 62.2 5.9 33.1 88,023 (USD13,542)

Jincheng Bank 2016-1 928 (USD143)

24.7 62.2 2.8 32.8 50,400 (USD7,754)

Dongfeng Peugeot Citroen 2016-1

1,000 (USD154)

16.1 59.2 6.9 31.1 64,300 (USD9,892)

Dongfeng Nissan 2016-1 3,000 (USD462)

14.0 65.8 9.4 34.2 79,867 (USD12,287)

BMW 2016-1 4,000 (USD615)

18.5 64.0 9.6 34.4 257,515 (USD39,618)

SAIC-GMAC 2016-2 4,000 (USD615)

10.5 65.6 6.5 32.6 49,648 (USD7,638)

RMBS Issuance

Originator / seriesOriginal note balance

(CNYm)Credit enhancement to highest rated Note (%)

Weighted average LTV at origination (%)

Weighted average seasoning

at cut-off dates (months)Weighted average

original term (months)Average loan size at

origination (CNY)

CCB 2016-1 9,749 (USD1,500)

10.9 48.9 72.0 206.0 283,300 (USD43,585)

Shanghai Housing Provident Fund 2016-1

14,842 (USD2,283)

7.4 45.6 36.8 174.5 415,700 (USD63,954)

Shanghai Housing Provident Fund 2016-2

16,317 (USD2,510)

6.9 63.9 43.9 238.8 348,137 (USD53,560)

7www.fitchratings.com | September 2016

China Structured Finance Quarterly – 2Q16

Shelf Registration and Draw Down

Asset type Originator Trust nameRegistered

quota (CNYbn)Registered

quota (USDbn)Registered No.

of ABS issuanceDrawn down percentage*

Effective date

Expiration date

Auto Loans SAIC-GMAC Rong Teng 10 1.5 3 100 26-May-15 26-May-17Auto Loans BMW Automotive Finance (China) Co., Ltd De Bao Tian Yuan 12 1.8 4 84 26-May-15 26-May-17Auto Loans Volkswagen Finance (China) Co., Ltd. Hua Yu 12 1.8 4 41 26-May-15 26-May-17Auto Loans China Merchants Bank He Xin 30 4.6 4-5 18 26-May-15 26-May-17Auto Loans Ford Automotive Finance (China) Limited Fu Yuan 12 1.8 4-6 50 6-Nov-15 6-Nov-17Auto Loans China Minsheng Banking Corp Qi Fu 10 1.5 5-8 10 8-Dec-15 8-Dec-17Auto Loans Dongfeng Nissan Auto Finance Co., Ltd. Wei Ying 12 1.8 4 25 13-May-16 13-May-18Auto Loans SAIC-GMAC Rong Teng 15 2.3 4 27 TBD TBDAuto Loans Beijing Hyundai Auto Finance Co., Ltd. Rui Cheng 10 1.5 3 0 TBD TBDResidential Mortgage Loans China Construction Bank Jian Yuan 50 7.7 5 39 29-Jun-15 29-Jun-17Residential Mortgage Loans China Minsheng Banking Corp Qi Fu 10 1.5 4 8 29-Jun-15 29-Jun-17Residential Mortgage Loans Bank of China Zhong Ying 100 15.4 20 5 17-Jul-15 17-Jul-17Residential Mortgage Loans China Merchants Bank He Jia 40 6.2 6-8 10 17-Jul-15 17-Jul-17Residential Mortgage Loans Jiangnan Rural Commercial Bank Ju Rong 5 0.8 5 17 27-Aug-15 27-Aug-17Residential Mortgage Loans Bank of Beijing Jing Cheng 10 1.5 3 30 21-Sep-15 21-Sep-17Residential Mortgage Loans Shunde Rural Commercial Bank Xin Rong 5 0.8 3 38 18-Feb-16 18-Feb-18Residential Mortgage Loans Postal Savings Bank of China Jia Mei 30 4.6 8 0 19-Apr-16 19-Apr-18Residential Mortgage Loans Huishang Bank Chuang Ying 5 0.8 5 0 TBD TBDConsumer Credit China Merchants Bank He Xiang 40 6.2 5-10 8 10-Oct-15 10-Oct-17Consumer Credit Bank of Ningbo Yong Dong 20 3.1 6-8 10 12-Oct-15 12-Oct-17Consumer Credit China Minsheng Banking Corp Qi Fu 10 1.5 4-6 0 31-Dec-15 31-Dec-17Consumer Credit Bank of Nanjing Xin Ning 5 0.8 2-4 0 TBD TBDCredit Card Bank of Communications Jiao Yuan 50 7.7 10 10 12-Oct-15 12-Oct-17Shantytown Reconstruction Loans China Development Bank Kai Yuan 10 1.5 2-3 0 31-Jul-15 31-Jul-17Property Secured Loans Ping An Bank Co., Ltd. Cheng Yi 5 0.8 2-3 20 20-Jan-16 20-Jan-18

Total Amount 518 79.7Source: www.pbc.gov.cn; www.chinabond.com.cn

USDCNY = 6.5 *As of end-June 2016

SAIC-GMAC is the first company to receive registration quota for the second time (more details yet to be published). Fitch expects China’s auto-loan ABS market to be further exploited, with some issuers reaching or having already reached their registered quota limits.

8www.fitchratings.com | September 2016

China Structured Finance Quarterly – 2Q16

Chinese Auto ABS Performance: Defaults

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

0 5 10 15 20 25 30 35

(%)

Months since closing

China Auto ABS - Cumulative Default Rates % as of Original Balance

CMB 2014-1 Toyota 2014-1 (PIF) Ford 2014-1 (PIF) Dongfeng Nissan 2014-1 (PIF) BMW 2014-1 (PIF)VW 2014-1 (PIF) GAC-SOFINCO 2014-1 GMAC-SAIC 2014-1 Ford 2015-1 SAIC-GMAC 2015-1BMW 2015-1 CMB 2015-2 (Zhao Yuan) VW 2015-1 PingAn Bank 2015-1 Dongfeng Nissan 2015-1SAIC-GMAC 2015-2 BMW 2015-2 CMB 2015-2 (He Xin) Ford 2015-2 CMBC 2015-5VW 2016-1 Beijing Hyundai 2016-1 SAIC-GMAC 2016-1 Mercedes-Benz 2016-1 Ford 2016-1Jincheng Bank 2016-1 DPCAFC 2016-1 Dongfeng Nissan 2016-1 BMW 2016-1 SAIC-GMAC 2016-2

Source: Fitch, Trustee reports

Overall, the performance of auto-loan ABS has not seen major deterioration despite slowing economic growth. The average cumulative default rate for Chinese auto ABS was below 1.5% as at 2Q16, and Fitch expects the rate to remain below this level as underlying auto-loans have positive credit features of high

seasoning and low LVR. However, Fitch believes delinquency rates will edge up, as GDP growth is expected to slow to 6.5% in 2016, from 6.9% in 2015.

9www.fitchratings.com | September 2016

China Structured Finance Quarterly – 2Q16

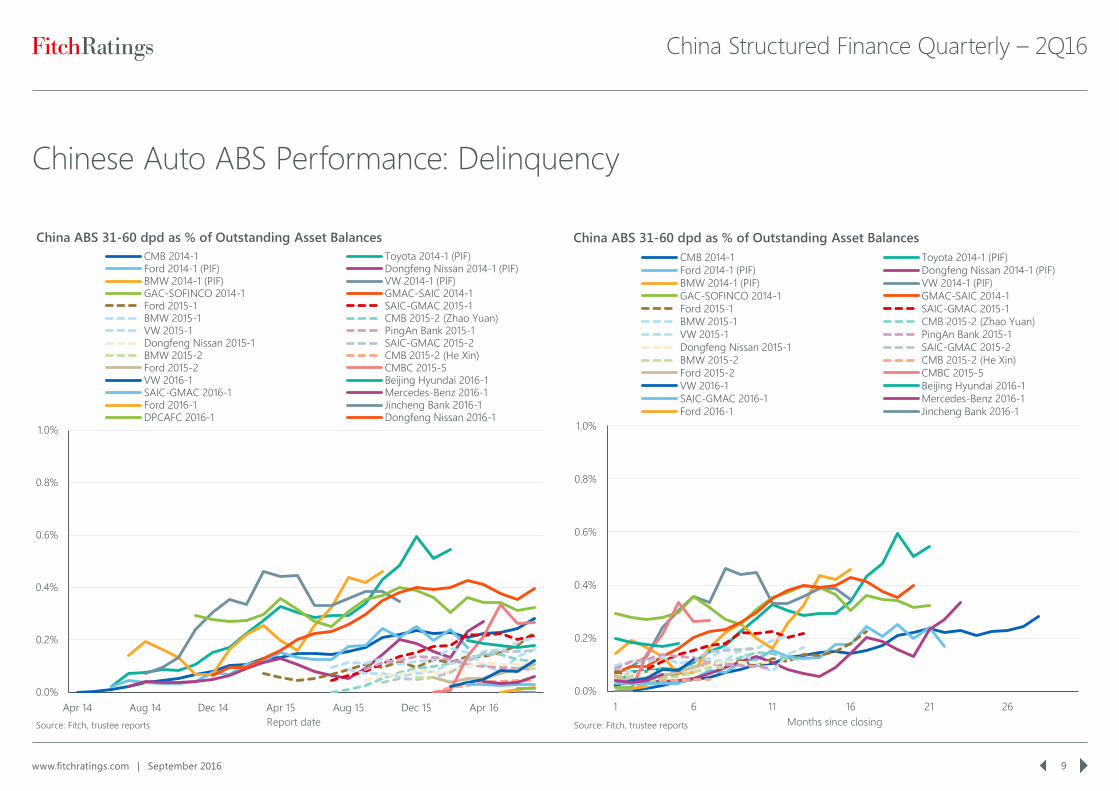

Chinese Auto ABS Performance: Delinquency

0.0%

0.2%

0.4%

0.6%

0.8%

1.0%

Apr 14 Aug 14 Dec 14 Apr 15 Aug 15 Dec 15 Apr 16Report date

China ABS 31-60 dpd as % of Outstanding Asset BalancesCMB 2014-1 Toyota 2014-1 (PIF)Ford 2014-1 (PIF) Dongfeng Nissan 2014-1 (PIF)BMW 2014-1 (PIF) VW 2014-1 (PIF)GAC-SOFINCO 2014-1 GMAC-SAIC 2014-1Ford 2015-1 SAIC-GMAC 2015-1BMW 2015-1 CMB 2015-2 (Zhao Yuan)VW 2015-1 PingAn Bank 2015-1Dongfeng Nissan 2015-1 SAIC-GMAC 2015-2BMW 2015-2 CMB 2015-2 (He Xin)Ford 2015-2 CMBC 2015-5VW 2016-1 Beijing Hyundai 2016-1SAIC-GMAC 2016-1 Mercedes-Benz 2016-1Ford 2016-1 Jincheng Bank 2016-1DPCAFC 2016-1 Dongfeng Nissan 2016-1

Source: Fitch, trustee reports

0.0%

0.2%

0.4%

0.6%

0.8%

1.0%

1 6 11 16 21 26Months since closing

China ABS 31-60 dpd as % of Outstanding Asset BalancesCMB 2014-1 Toyota 2014-1 (PIF)Ford 2014-1 (PIF) Dongfeng Nissan 2014-1 (PIF)BMW 2014-1 (PIF) VW 2014-1 (PIF)GAC-SOFINCO 2014-1 GMAC-SAIC 2014-1Ford 2015-1 SAIC-GMAC 2015-1BMW 2015-1 CMB 2015-2 (Zhao Yuan)VW 2015-1 PingAn Bank 2015-1Dongfeng Nissan 2015-1 SAIC-GMAC 2015-2BMW 2015-2 CMB 2015-2 (He Xin)Ford 2015-2 CMBC 2015-5VW 2016-1 Beijing Hyundai 2016-1SAIC-GMAC 2016-1 Mercedes-Benz 2016-1Ford 2016-1 Jincheng Bank 2016-1

Source: Fitch, trustee reports

10www.fitchratings.com | September 2016

China Structured Finance Quarterly – 2Q16

Chinese Auto ABS Performance: Prepayment1

0%

4%

8%

12%

16%

20%

24%

May 14 Jul 14 Sep 14 Nov 14 Jan 15 Mar 15 May 15 Jul 15 Sep 15 Nov 15 Jan 16 Mar 16 May 16 Jul 16

Report date

China Auto Loans Conditional Prepayment RatesCMB 2014-1 Toyota 2014-1 (PIF)Ford 2014-1 (PIF) Dongfeng Nissan 2014-1 (PIF)BMW 2014-1 (PIF) VW 2014-1 (PIF)GAC-SOFINCO 2014-1 GMAC-SAIC 2014-1Ford 2015-1 SAIC-GMAC 2015-1CMB 2015-2 (Zhao Yuan) VW 2015-1PingAn Bank 2015-1 Dongfeng Nissan 2015-1SAIC-GMAC 2015-2 BMW 2015-2

Source: Fitch

0%

4%

8%

12%

16%

20%

24%

1 6 11 16 21 26

Months since closing

China Auto Loans Conditional Prepayment RatesCMB 2014-1 Toyota 2014-1 (PIF)Ford 2014-1 (PIF) Dongfeng Nissan 2014-1 (PIF)BMW 2014-1 (PIF) VW 2014-1 (PIF)GAC-SOFINCO 2014-1 GMAC-SAIC 2014-1Ford 2015-1 SAIC-GMAC 2015-1CMB 2015-2 (Zhao Yuan) VW 2015-1PingAn Bank 2015-1 Dongfeng Nissan 2015-1SAIC-GMAC 2015-2 BMW 2015-2

Source: Fitch

1 Unless otherwise stated, the prepayment rates in this report are conditional prepayment rates (CPR). CPR is calculated as 1-(1-SMM)^12, where Single Monthly Mortality (SMM) = Principal Prepayment Collectionn/(Outstanding Asset Balancen-1 – Scheduled Principal Collectionn).

11www.fitchratings.com | September 2016

China Structured Finance Quarterly – 2Q16

Chinese RMBS Performance: Defaults

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1.0

0 5 10 15 20 25 30 35 40 45 50 55 60 65 70 75 80 85 90 95 100 105 110 115 120 125 130 135

(%)

Months since closing

China RMBS - Cumulative Default Rates % as of Original BalanceCCB 2005-1 CCB 2007-1 PSB 2014-1 CMB 2015-1 (Zhao Yuan)

CMBC 2015-1 CMB 2015-1 (He Jia) Jiangnan Rural Commercial Bank 2015-1 CCB 2015-1

Bank of Beijing 2015-2 BOC 2015-2 CCB 2015-2 Shunde Rural Commercial Bank 2016-1

CCB 2016-1

Source: Fitch, trustee reports

The 13 existing RMBS transactions have performed well to date. Fitch expects RMBS performance to continue its stable status despite slowing economic growth.

12www.fitchratings.com | September 2016

China Structured Finance Quarterly – 2Q16

Chinese RMBS Performance: Delinquency

0.0%

0.2%

0.4%

0.6%

Jan 06 Jan 07 Jan 08 Jan 09 Jan 10 Jan 11 Jan 12 Jan 13 Jan 14 Jan 15 Jan 16Report date

China RMBS 91-180 dpd as % of Outstanding Asset Balances (Three-Month Moving Average)

CCB 2005-1 CCB 2007-1

PSB 2014-1 CMB 2015-1 (Zhao Yuan)

CMBC 2015-1 CMB 2015-1 (He Jia)

Jiangnan Rural Commercial Bank 2015-1 CCB 2015-1

Bank of Beijing 2015-2 CCB 2015-2

Shunde Rural Commercial Bank 2016-1 CCB 2016-1

Source: Fitch, trustee reports

0.0%

0.2%

0.4%

0.6%

1 6 11 16 21 26 31 36 41 46 51 56 61 66 71 76 81 86 91 96 101 106 111 116 121 126

Months since closing

China RMBS 91-180 dpd as % of Outstanding Asset Balances (Three-Month Moving Average)

CCB 2005-1 CCB 2007-1

PSB 2014-1 CMB 2015-1 (Zhao Yuan)

CMBC 2015-1 CMB 2015-1 (He Jia)

Jiangnan Rural Commercial Bank 2015-1 CCB 2015-1

Bank of Beijing 2015-2 CCB 2015-2

Shunde Rural Commercial Bank 2016-1 CCB 2016-1

Source: Fitch, trustee reports

13www.fitchratings.com | September 2016

China Structured Finance Quarterly – 2Q16

Chinese RMBS Performance: Prepayment

0%

5%

10%

15%

20%

25%

30%

35%

Jan 06 Jan 07 Jan 08 Jan 09 Jan 10 Jan 11 Jan 12 Jan 13 Jan 14 Jan 15 Jan 16Report date

China Residential Mortgage Loans Conditional Prepayment RatesCCB 2005-1 CCB 2007-1PSB 2014-1 CMB 2015-1 (Zhao Yuan)CMBC 2015-1 CMB 2015-1 (He Jia)Jiangnan Rural Commercial Bank 2015-1 CCB 2015-1Bank of Beijing 2015-2 BOC 2015-2CCB 2015-2 Shunde Rural Commercial Bank 2016-1

Source: Fitch

0%

5%

10%

15%

20%

25%

30%

1 6 11 16 21 26 31 36 41 46 51 56 61 66 71 76 81 86 91 96 101 106 111 116 121 126Months since closing

China Residential Mortgage Loans Conditional Prepayment RatesCCB 2005-1 CCB 2007-1PSB 2014-1 CMB 2015-1 (Zhao Yuan)CMBC 2015-1 CMB 2015-1 (He Jia)Jiangnan Rural Commercial Bank 2015-1 CCB 2015-1Bank of Beijing 2015-2 BOC 2015-2CCB 2015-2 Shunde Rural Commercial Bank 2016-1

Source: Fitch

14www.fitchratings.com | September 2016

China Structured Finance Quarterly – 2Q16

Fitch Criteria and Research Relevant to China

Criteria

Counterparty Criteria for Structured Finance and Covered Bonds 01 Sep 2016

Global Consumer ABS Rating Criteria 19 Aug 2016

Global Structured Finance Rating Criteria 27 Jun 2016

Criteria for Rating Securitizations in Emerging Markets 6 Nov 2014

Criteria for Rating Caps and Limitations in Global Structured Finance Transactions 16 Jun 2016

Fitch Research

China Auto Watch 22 Aug 2016

China Property Watch 24 Aug 2016

China’s Housing Demand to Stay Resilient Through 2030 07 Aug 2016

China Banks’ Potential NPL Securitisations Will Challenge Investors 8 May 2016

China Structured Finance Quarterly - 4Q15 28 Mar 2016

Revolving Structures in Chinese Securitisation Warrant Closer Scrutiny 29 Feb 2016

China Residential Mortgage Securitisation: Frequently Asked Questions 01 Feb 2016

China’s Credit Bureau Important for Consumer Finance Development 17 Dec 2015

New China ABS Structures to Reduce Liquidity Risk 10 Dec 2015

China CLO Structural Risk Exposed by a Corporate Default 17 Nov 2015

China’s New ABS Disclosure Rules to Improve Transparency 11 Nov 2015

15www.fitchratings.com | September 2016

China Structured Finance Quarterly – 2Q16

ALL FITCH CREDIT RATINGS ARE SUBJECT TO CERTAIN LIMITATIONS AND DISCLAIMERS. PLEASE READ THESE LIMITATIONS AND DISCLAIMERS BY FOLLOWING THIS LINK: HTTPS://FITCHRATINGS.COM/UNDERSTANDINGCREDITRATINGS. IN ADDITION, RATING DEFINITIONS AND THE TERMS OF USE OF SUCH RATINGS ARE AVAILABLE ON THE AGENCY’S PUBLIC WEB SITE AT WWW.FITCHRATINGS.COM. PUBLISHED RATINGS, CRITERIA, AND METHODOLOGIES ARE AVAILABLE FROM THIS SITE AT ALL TIMES. FITCH’S CODE OF CONDUCT, CONFIDENTIALITY, CONFLICTS OF INTEREST, AFFILIATE FIREWALL, COMPLIANCE, AND OTHER RELEVANT POLICIES AND PROCEDURES ARE ALSO AVAILABLE FROM THE CODE OF CONDUCT SECTION OF THIS SITE. FITCH MAY HAVE PROVIDED ANOTHER PERMISSIBLE SERVICE TO THE RATED ENTITY OR ITS RELATED THIRD PARTIES. DETAILS OF THIS SERVICE FOR RATINGS FOR WHICH THE LEAD ANALYST IS BASED IN AN EU-REGISTERED ENTITY CAN BE FOUND ON THE ENTITY SUMMARY PAGE FOR THIS ISSUER ON THE FITCH WEBSITE.

Copyright © 2016 by Fitch Ratings, Inc., Fitch Ratings Ltd. and its subsidiaries. 33 Whitehall Street, NY, NY 10004. Telephone: 1-800-753-4824, (212) 908-0500. Fax: (212) 480-4435. Reproduction or retransmission in whole or in part is prohibited except by permission. All rights reserved. In issuing and maintaining its ratings and in making other reports (including forecast information), Fitch relies on factual information it receives from issuers and underwriters and from other sources Fitch believes to be credible. Fitch conducts a reasonable investigation of the factual information relied upon by it in accordance with its ratings methodology, and obtains reasonable verification of that information from independent sources, to the extent such sources are available for a given security or in a given jurisdiction. The manner of Fitch’s factual investigation and the scope of the third-party verification it obtains will vary depending on the nature of the rated security and its issuer, the requirements and practices in the jurisdiction in which the rated security is offered and sold and/or the issuer is located, the availability and nature of relevant public information, access to the management of the issuer and its advisers, the availability of pre-existing third-party verifications such as audit reports, agreed-upon procedures letters, appraisals, actuarial reports, engineering reports, legal opinions and other reports provided by third parties, the availability of independent and competent third-party verification sources with respect to the particular security or in the particular jurisdiction of the issuer, and a variety of other factors. Users of Fitch’s ratings and reports should understand that neither an enhanced factual investigation nor any third-party verification can ensure that all of the information Fitch relies on in connection with a rating or a report will be accurate and complete. Ultimately, the issuer and its advisers are responsible for the accuracy of the information they provide to Fitch and to the market in offering documents and other reports. In issuing its ratings and its reports, Fitch must rely on the work of experts, including independent auditors with respect to financial statements and attorneys with respect to legal and tax matters. Further, ratings and forecasts of financial and other information are inherently forward-looking and embody assumptions and predictions about future events that by their nature cannot be verified as facts. As a result, despite any verification of current facts, ratings and forecasts can be affected by future events or conditions that were not anticipated at the time a rating or forecast was issued or affirmed.

The information in this report is provided as is without any representation or warranty of any kind, and Fitch does not represent or warrant that the report or any of its contents will meet any of the requirements of a recipient of the report. A Fitch rating is an opinion as to the creditworthiness of a security. This opinion and reports made by Fitch are based on established criteria and methodologies that Fitch is continuously evaluating and updating. Therefore, ratings and reports are the collective work product of Fitch and no individual, or group of individuals, is solely responsible for a rating or a report. The rating does not address the risk of loss due to risks other than credit risk, unless such risk is specifically mentioned. Fitch is not engaged in the offer or sale of any security. All Fitch reports have shared authorship. Individuals identified in a Fitch report were involved in, but are not solely responsible for, the opinions stated therein. The individuals are named for contact purposes only. A report providing a Fitch rating is neither a prospectus nor a substitute for the information assembled, verified and presented to investors by the issuer and its agents in connection with the sale of the securities. Ratings may be changed or withdrawn at any time for any reason in the sole discretion of Fitch. Fitch does not provide investment advice of any sort. Ratings are not a recommendation to buy, sell, or hold any security. Ratings do not comment on the adequacy of market price, the suitability of any security for a particular investor, or the tax-exempt nature or taxability of payments made in respect to any security. Fitch receives fees from issuers, insurers, guarantors, other obligors, and underwriters for rating securities. Such fees generally vary from US$1,000 to US$750,000 (or the applicable currency equivalent) per issue. In certain cases, Fitch will rate all or a number of issues issued by a particular issuer, or insured or guaranteed by a particular insurer or guarantor, for a single annual fee. Such fees are expected to vary from US$10,000 to US$1,500,000 (or the applicable currency equivalent). The assignment, publication, or dissemination of a rating by Fitch shall not constitute a consent by Fitch to use its name as an expert in connection with any registration statement filed under the United States securities laws, the Financial Services and Markets Act of 2000 of the United Kingdom, or the securities laws of any particular jurisdiction. Due to the relative efficiency of electronic publishing and distribution, Fitch research may be available to electronic subscribers up to three days earlier than to print subscribers.

For Australia, New Zealand, Taiwan and South Korea only: Fitch Australia Pty Ltd holds an Australian financial services license (AFS license no. 337123) which authorizes it to provide credit ratings to wholesale clients only. Credit ratings information published by Fitch is not intended to be used by persons who are retail clients within the meaning of the Corporations Act 2001. 160147