Embed Size (px)

Citation preview

PROPOSAL OF INSURANCE

For

Finest City Acoustics, Inc.

August 4, 2015

Choosing a Commercial

Insurance Broker

Reducing overpayment of premium

Maximizing coverage

Are You Comparing Apples To Apples?

Brown & Brown Insurance Brokers of Sacramento, Inc.

CA License #: 0H38004 | NYSE: BRO

5750 West Oaks Blvd, Suite 140, Rocklin, CA 95765

CHOOSING A COMMERICAL INSURANCE BROKER

Confidential and Proprietary

Page 1

Maximize the risk transfer model and reduce overpayment of premium

Selecting a commercial insurance broker is a decision that can have a meaningful impact on the

bottom line. However, the process can be difficult to manage. In order to make the best choice

possible, Brown & Brown recommends a company has a complete understanding of the process

when seeking to evaluate or change brokers. This white paper offers a clear point-of-view on the

following:

• Common Concerns with Business Insurance

o Overpayment

o Painful Process

o Underwriters Receiving Different Stories

o Limited Options & Last Minute Renewal

THE PROBLEM

It is virtually impossible to determine every potential cause of loss. If we could do that, then we

would only buy insurance for those causes of loss we have identified. Insurance policies are

restrictive in nature; they protect insurance companies NOT policyholders.

Financial executives typically have responsibility for managing a company’s business insurance.

In many instances, the task is overly complicated because the process is not transparent and

comparing quotes is difficult due to a lack of information provided to the underwriter. In most

cases only a transactional limit to limit comparison is performed. However, limits of insurance

DO NOT determine coverage. Coverage is found within the policy language.

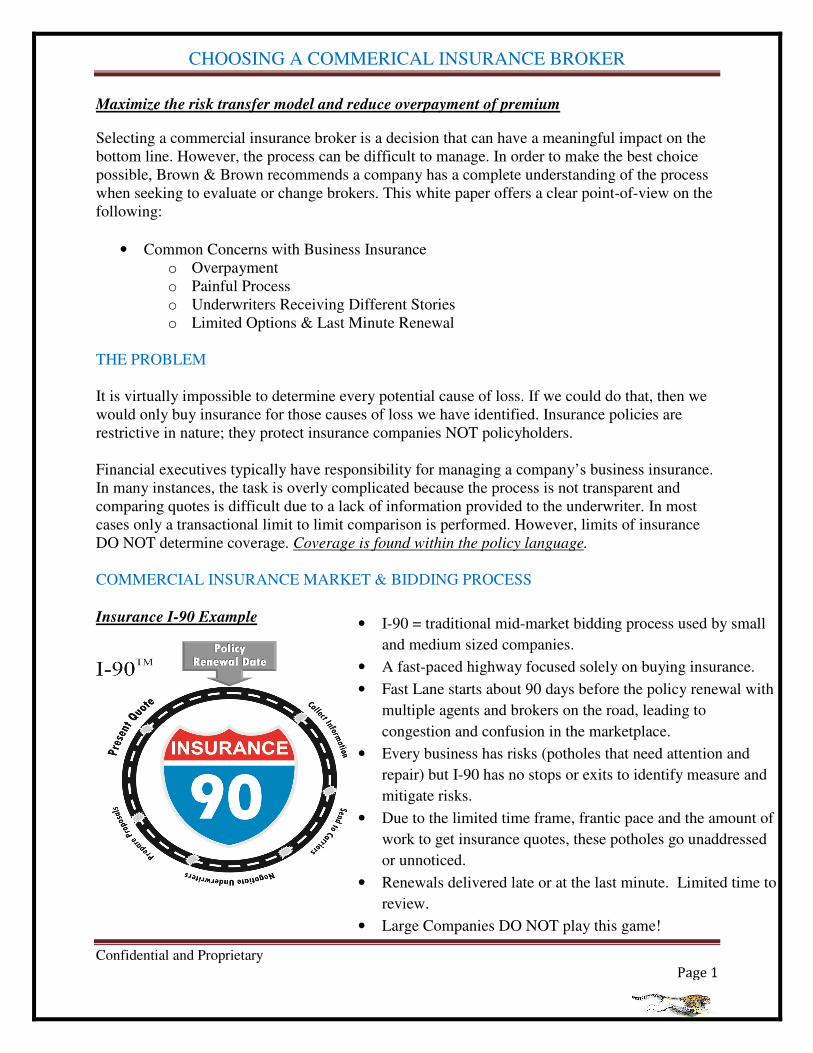

COMMERCIAL INSURANCE MARKET & BIDDING PROCESS

Insurance I-90 Example

• I-90 = traditional mid-market bidding process used by small

and medium sized companies.

• A fast-paced highway focused solely on buying insurance.

• Fast Lane starts about 90 days before the policy renewal with

multiple agents and brokers on the road, leading to

congestion and confusion in the marketplace.

• Every business has risks (potholes that need attention and

repair) but I-90 has no stops or exits to identify measure and

mitigate risks.

• Due to the limited time frame, frantic pace and the amount of

work to get insurance quotes, these potholes go unaddressed

or unnoticed.

• Renewals delivered late or at the last minute. Limited time to

review.

• Large Companies DO NOT play this game!

CHOOSING A COMMERICAL INSURANCE BROKER

Confidential and Proprietary

Page 2

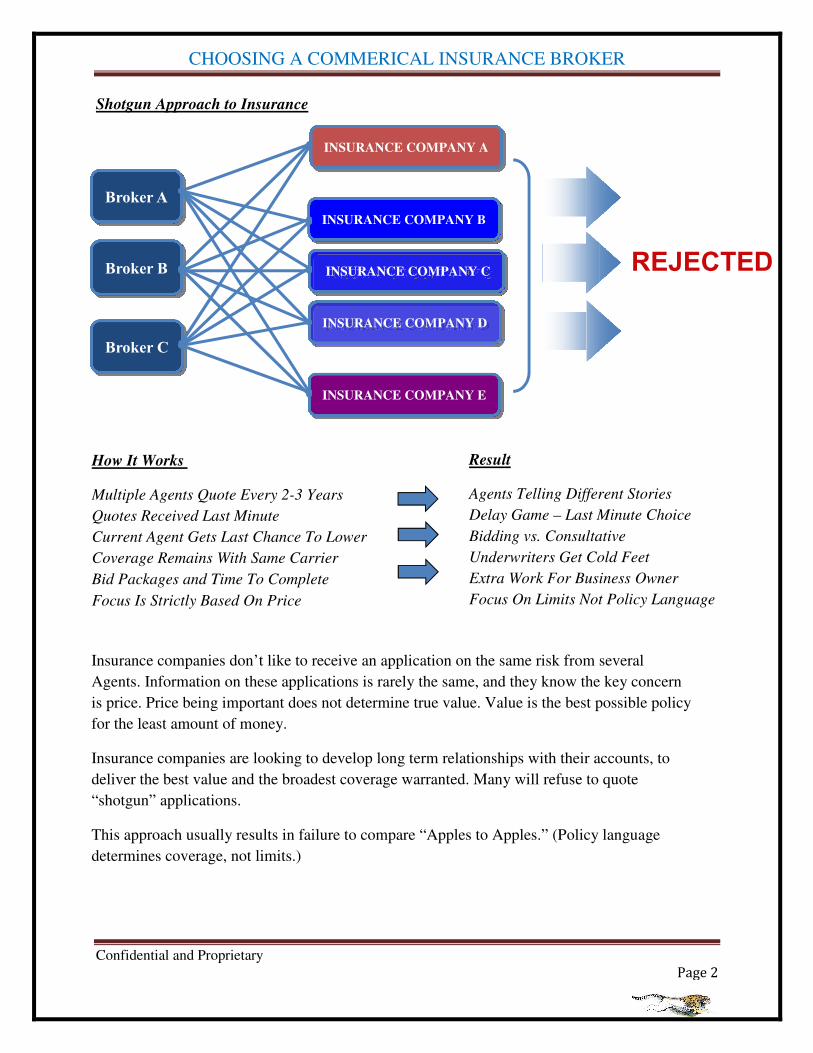

Shotgun Approach to Insurance

INSURANCE COMPANY A

INSURANCE COMPANY B

INSURANCE COMPANY C

INSURANCE COMPANY D

INSURANCE COMPANY E

Broker B

Broker C

Broker A

REJECTED

How It Works

Multiple Agents Quote Every 2-3 Years

Quotes Received Last Minute

Current Agent Gets Last Chance To Lower

Coverage Remains With Same Carrier

Bid Packages and Time To Complete

Focus Is Strictly Based On Price

Result

Agents Telling Different Stories

Delay Game – Last Minute Choice

Bidding vs. Consultative

Underwriters Get Cold Feet

Extra Work For Business Owner

Focus On Limits Not Policy Language

Insurance companies don’t like to receive an application on the same risk from several

Agents. Information on these applications is rarely the same, and they know the key concern

is price. Price being important does not determine true value. Value is the best possible policy

for the least amount of money.

Insurance companies are looking to develop long term relationships with their accounts, to

deliver the best value and the broadest coverage warranted. Many will refuse to quote

“shotgun” applications.

This approach usually results in failure to compare “Apples to Apples.” (Policy language

determines coverage, not limits.)

CHOOSING A COMMERICAL INSURANCE BROKER

Confidential and Proprietary

Page 3

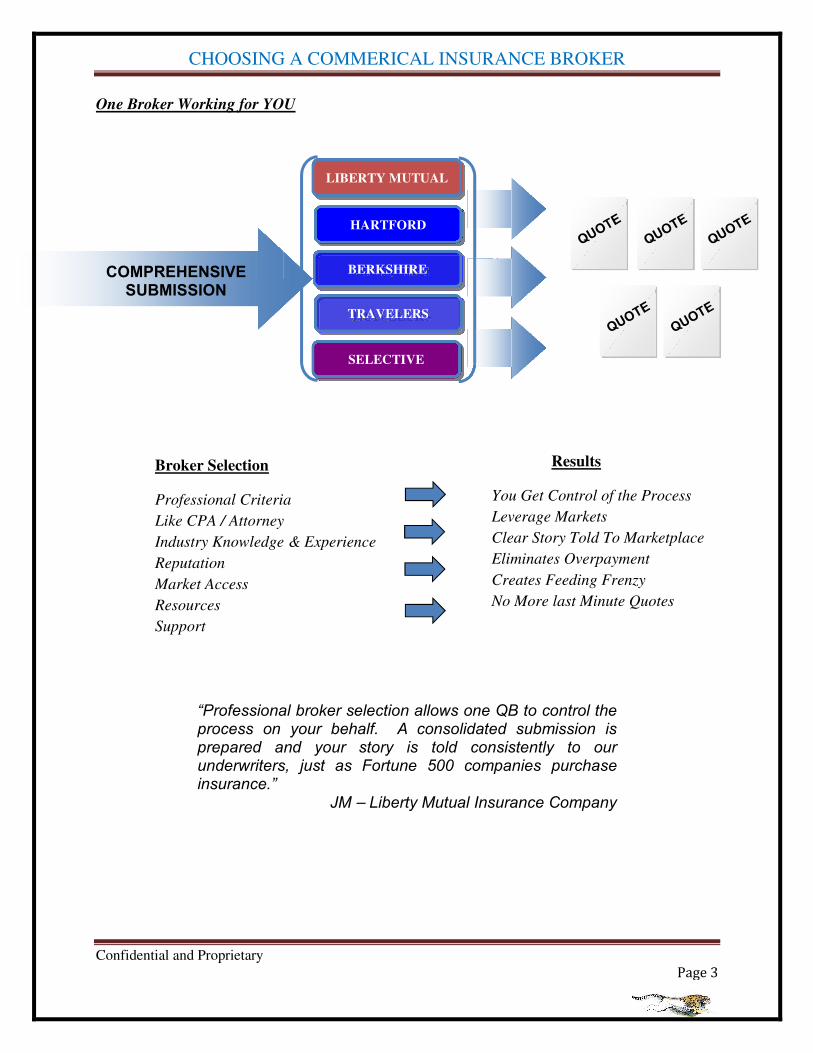

One Broker Working for YOU

LIBERTY MUTUAL

HARTFORD

BERKSHIRE

TRAVELERS

SELECTIVE

COMPREHENSIVE

SUBMISSION

Broker Selection

Professional Criteria

Like CPA / Attorney

Industry Knowledge & Experience

Reputation

Market Access

Resources

Support

Results

You Get Control of the Process

Leverage Markets

Clear Story Told To Marketplace

Eliminates Overpayment

Creates Feeding Frenzy

No More last Minute Quotes

“Professional broker selection allows one QB to control the process on your behalf. A consolidated submission is prepared and your story is told consistently to our underwriters, just as Fortune 500 companies purchase insurance.”

JM – Liberty Mutual Insurance Company

CHOOSING A COMMERICAL INSURANCE BROKER

Confidential and Proprietary

Page 4

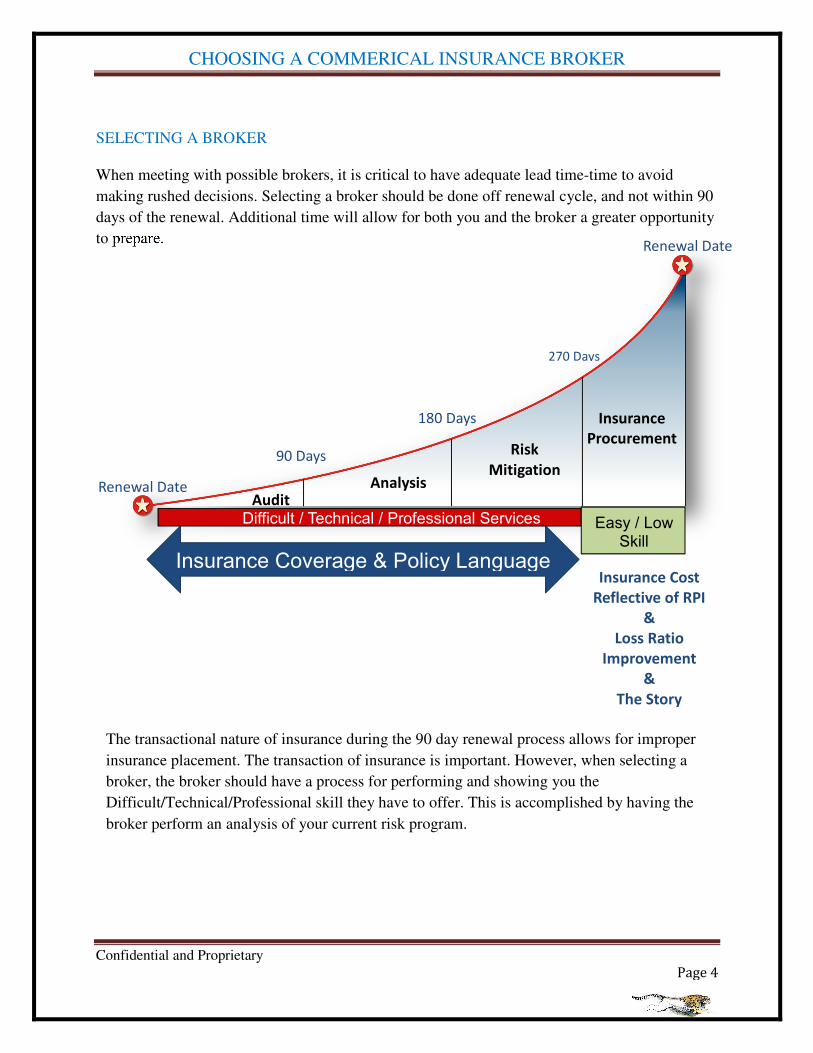

SELECTING A BROKER

When meeting with possible brokers, it is critical to have adequate lead time-time to avoid

making rushed decisions. Selecting a broker should be done off renewal cycle, and not within 90

days of the renewal. Additional time will allow for both you and the broker a greater opportunity

to prepare.

90 Days

180 Days

270 Days

Renewal Date

Insurance Cost

Reflective of RPI

&

Loss Ratio

Improvement

&

The Story

Analysis

Risk

Mitigation

Insurance

Procurement

Insurance Coverage & Policy Language

Audit

Difficult / Technical / Professional Services Easy / Low Skill

Renewal Date

The transactional nature of insurance during the 90 day renewal process allows for improper

insurance placement. The transaction of insurance is important. However, when selecting a

broker, the broker should have a process for performing and showing you the

Difficult/Technical/Professional skill they have to offer. This is accomplished by having the

broker perform an analysis of your current risk program.

CHOOSING A COMMERICAL INSURANCE BROKER

Confidential and Proprietary

Page 5

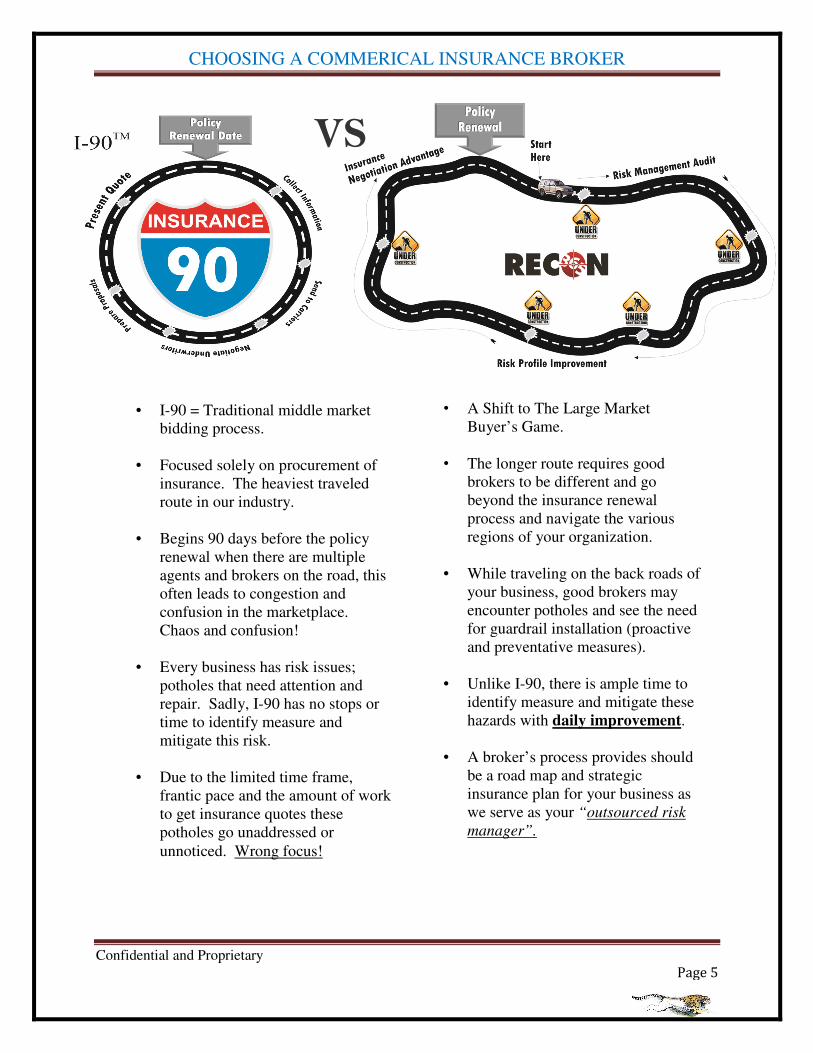

VS

• I-90 = Traditional middle market

bidding process.

• Focused solely on procurement of

insurance. The heaviest traveled

route in our industry.

• Begins 90 days before the policy

renewal when there are multiple

agents and brokers on the road, this

often leads to congestion and

confusion in the marketplace.

Chaos and confusion!

• Every business has risk issues;

potholes that need attention and

repair. Sadly, I-90 has no stops or

time to identify measure and

mitigate this risk.

• Due to the limited time frame,

frantic pace and the amount of work

to get insurance quotes these

potholes go unaddressed or

unnoticed. Wrong focus!

• A Shift to The Large Market

Buyer’s Game.

• The longer route requires good

brokers to be different and go

beyond the insurance renewal

process and navigate the various

regions of your organization.

• While traveling on the back roads of

your business, good brokers may

encounter potholes and see the need

for guardrail installation (proactive

and preventative measures).

• Unlike I-90, there is ample time to

identify measure and mitigate these

hazards with daily improvement.

• A broker’s process provides should

be a road map and strategic

insurance plan for your business as

we serve as your “outsourced risk

manager”.

CHOOSING A COMMERICAL INSURANCE BROKER

Confidential and Proprietary

Page 6

CHANGING BROKERS

Broker of Record

If you decide to change brokers, there are procedures which need to be followed. However, this

depends on the brokers recommendations. If the broker of your choosing decides the current

carriers are the best fit, but are not being utilized to their fullest a Broker of Record will be

needed. The letter will need to be printed on a company’s letterhead, and signed by the company

decision-maker. Once the letter is sent to the broker they in turn will forward the letter to the

insurance carrier letting them know you are naming the new broker as your insurance

representative.

Once the carrier receives the letter, there is typically a 10-day waiting period. During this time,

the carrier will inform the current broker of the clients desire to change brokers. We encourage

clients to contact the prior broker to let them know of the upcoming change. The client can share

as much as they want about the reasons for the change.

New Carriers

If you decide to change brokers, and the new broker decides there are better options available to

protect your business, and reduce overpayment of premium standard insurance placement will

follow. This is why the transaction of insurance is important. However, it is the byproduct of the

work performed before approaching insurance carriers. In some cases a Broker of Record may be

required to access carriers the prior broker approached, but it did not maximize coverage.

CONCLUSION

A single broker representing your business can be an effective solution for maximizing coverage,

and reducing overpayment of premium by negotiating with carriers in a more effective manner.

They should be designing and negotiating an insurance program to meet your needs, handle

complex claim situations, and proactively address ongoing business needs. Essentially, your

broker should be acting as your outsourced risk manager with your business best interest as a

priority.