Embed Size (px)

Citation preview

Choosing a Form of BusinessChoosing a Form of Business

Basis for DecisionBasis for Decision

• TaxesTaxes

• Legal liabilityLegal liability

• ExpensesExpenses

Types of EntitiesTypes of Entities• Sole ProprietorSole Proprietor• PartnershipPartnership

– General General – LimitedLimited– Limited liability (LLP)Limited liability (LLP)

• CorporationCorporation– Regular “C” corpRegular “C” corp– ““S” CorpS” Corp– Limited liability company (LLC)Limited liability company (LLC)

Available OptionsAvailable Options

Sole Sole Prop. Prtshp. Corp.Prop. Prtshp. Corp.

Single Owner X XSingle Owner X X

Multiple Multiple Owners X XOwners X X

Multiple OwnersMultiple Owners

• The partnership is the default option The partnership is the default option for businesses with multiple ownersfor businesses with multiple owners– A partnership, unless business is A partnership, unless business is

incorporatedincorporated

• Owners may frequently refer to their Owners may frequently refer to their “partner”, even when the business is “partner”, even when the business is incorporatedincorporated– A business incorporates by filing articles A business incorporates by filing articles

of incorporation with the stateof incorporation with the state

Popularity of Business FormsPopularity of Business Forms

S. Prop Ptrshp. Corp0

10

20

30

40

50

60

70

80

S. Prop Ptrshp. Corp

Number

Sales

Business Tax DifferencesBusiness Tax Differences

• Pass-through Pass-through (not taxed at business (not taxed at business entity level)entity level)

• Deductibility of fringesDeductibility of fringes

• Double taxation of corporate Double taxation of corporate dividendsdividends– Generally not applicable for non-public Generally not applicable for non-public

companiescompanies

Tax AttributesTax Attributes

Type of Who isType of Who is Tax Top Tax Tax Top Tax PassPass

Entity TaxedEntity Taxed Form Rate Form Rate ThroughThrough

Sole Prop. Ind. Sch. C 39.6 N/ASole Prop. Ind. Sch. C 39.6 N/A

Ptrnshp. Ptnrs. 1065 39.6 YesPtrnshp. Ptnrs. 1065 39.6 Yes

C corp Corp. 1120 39 NoC corp Corp. 1120 39 No

S corp. Shrdlrs. 1120S 39.6 YesS corp. Shrdlrs. 1120S 39.6 Yes

LLCLLC Shrdlrs. 1065 39.6 Yes Shrdlrs. 1065 39.6 Yes

Only the C corporation is a separate Only the C corporation is a separate taxable entitytaxable entity

Top marginal rates are similarTop marginal rates are similar

What do we mean by a What do we mean by a marginal rate?marginal rate?

What do we mean by a marginal rate?What do we mean by a marginal rate?

The rate paid on the last dollar of The rate paid on the last dollar of incomeincome

((Effective rate on additional earnings)Effective rate on additional earnings)

What is the marginal rate at $150,000 What is the marginal rate at $150,000 for?:for?:

• Married individualMarried individual

• CorporationCorporation

Rate ComparisonRate Comparison

Individual Individual (married filing jointly) (married filing jointly) CorporationCorporation

Taxable Income Rate Taxable Income RateTaxable Income Rate Taxable Income Rate

0 - 42,350 15 0 - 50,000 150 - 42,350 15 0 - 50,000 15

42,351 - 102,300 28 50,000 - 75,000 2542,351 - 102,300 28 50,000 - 75,000 25

102,301 - 155,950 31 75,000 - 100,000 34102,301 - 155,950 31 75,000 - 100,000 34

155,951 - 278,450 36 100,000 - 335,000 39155,951 - 278,450 36 100,000 - 335,000 39

> 278,450 39.6 335,000 - 10 mil. 34> 278,450 39.6 335,000 - 10 mil. 34

> 10,000,000 35 > 10,000,000 35

Income SplittingIncome Splitting

The existence of lower marginal rates for The existence of lower marginal rates for both individuals and corporations both individuals and corporations creates a valuable creates a valuable income splittingincome splitting option to lower option to lower combined taxescombined taxes– Valuable in early stages of company to Valuable in early stages of company to

finance growthfinance growth– Most valuable for relatively small amounts Most valuable for relatively small amounts

of profit of profit – This option is only available with regular C This option is only available with regular C

corporationscorporations

Income Splitting ExampleIncome Splitting Example

Corp. A Corp. BCorp. A Corp. BNet income Net income 200,000200,000 200,000200,000

Net after salary Net after salary 0 0 100,000100,000

Tax on salary 55,629 22,495Tax on salary 55,629 22,495

Tax on corp. Tax on corp. 0 0 22,25022,250

Total Tax Total Tax 55,62955,629 44,74544,745

Available for use 144,371 155,255Available for use 144,371 155,255

Example - Corporation Example - Corporation with 100,000 of incomewith 100,000 of income

Tax computation:Tax computation:

IncomeIncome RateRate TaxTax 50,000 15 % 7,50050,000 15 % 7,500

25,000 25 % 6,25025,000 25 % 6,250 25,00025,000 34 % 34 % 8,5008,500 Total 100,000 22,250Total 100,000 22,250

Average rate = ?Average rate = ?

Marginal rate = ?Marginal rate = ?

ExampleExample

IncomeIncome RateRate TaxTax

50,000 15 % 7,50050,000 15 % 7,500 25,000 25 % 6,25025,000 25 % 6,250 25,00025,000 34 % 34 % 8,5008,500 Total 100,000 22,250Total 100,000 22,250

Average rate = (26,150/110,000) = Average rate = (26,150/110,000) = 22.3%22.3%

Marginal rate = Marginal rate = 34%34%

Miscellaneous IssuesMiscellaneous Issues

Personal Service CorporationPersonal Service Corporation

– Taxed at flat rate of 35%Taxed at flat rate of 35%

– Service fields such as law, Service fields such as law, accounting, architecture, accounting, architecture, performing arts and consultingperforming arts and consulting

Miscellaneous IssuesMiscellaneous Issues

Double Taxation of DividendsDouble Taxation of Dividends

• Dividends are taxed twiceDividends are taxed twice– Income taxed at corporate levelIncome taxed at corporate level

– Dividend taxed at individual levelDividend taxed at individual level

• Solution - don’t pay dividendsSolution - don’t pay dividends– Profits can be paid out as salary or Profits can be paid out as salary or

other forms of deductible compensationother forms of deductible compensation

Fringe BenefitsFringe Benefits

• Historically, fringe benefit laws have favored Historically, fringe benefit laws have favored corporationscorporations– Not many differences todayNot many differences today

• Health InsuranceHealth Insurance– Fully deductible for corp Fully deductible for corp (must cover other (must cover other

employees)employees)

– Partially deductible for sole proprietorPartially deductible for sole proprietor

• 30% allowed; increases to 70%30% allowed; increases to 70%

• Not deductible for partners or S corp.Not deductible for partners or S corp.

Conclusion:Conclusion: Tax law generally favors Tax law generally favors incorporationincorporation

Why is sole proprietor the most Why is sole proprietor the most popular form of business?popular form of business?

Why is sole proprietor the most Why is sole proprietor the most popular form of business?popular form of business?

• Many S.P.’s are very small or Many S.P.’s are very small or sideline businessessideline businesses

• Sole proprietor is the default for Sole proprietor is the default for individually-owned businessindividually-owned business

Limited LiabilityLimited LiabilityLiability to CreditorsLiability to Creditors

• Corporate liability limited to amount Corporate liability limited to amount investedinvested– Some benefit with trade creditorsSome benefit with trade creditors– Limited help with lendersLimited help with lenders

• Lender will usually require a personal Lender will usually require a personal guaranteeguarantee

Why is personal guarantee required?Why is personal guarantee required?

Debt AgreementsDebt Agreements

Owner-managers have the ability to Owner-managers have the ability to transfer funds to the detriment of transfer funds to the detriment of lenders. As a result, loan will lenders. As a result, loan will normally require:normally require:– Personal guaranteePersonal guarantee

– Restrictions on payment of salaries and Restrictions on payment of salaries and dividendsdividends

Legal LiabilityLegal Liability

• Corporate liability limited to amount Corporate liability limited to amount investedinvested– Protection is not as great as it appearsProtection is not as great as it appears– Still personally liable for own acts, and Still personally liable for own acts, and

acts of others under your supervisionacts of others under your supervision

• LLC and LLPLLC and LLP– Most states permit these business forms Most states permit these business forms – Provides limited liability for partners Provides limited liability for partners

(LLP) and shareholders (LLC)(LLP) and shareholders (LLC)– Taxed as pass-through entityTaxed as pass-through entity

ExpensesExpenses

• IncorporationIncorporation– Filed in state of incorporationFiled in state of incorporation

– Relatively inexpensive, can be done Relatively inexpensive, can be done yourselfyourself

• On-going filingOn-going filing– Corporations and partnerships must Corporations and partnerships must

file tax returnsfile tax returns

• Incremental cost not that significantIncremental cost not that significant

S CorporationsS Corporations

• S Corporations are a hybridS Corporations are a hybrid– Limited liability like corporationLimited liability like corporation– ““Pass-through” like a partnershipPass-through” like a partnership– S corp is a federal tax election S corp is a federal tax election

(incorporated with state like a regular (incorporated with state like a regular corp.)corp.)

• Tax reasons for S - corpTax reasons for S - corp– Corporation is losing moneyCorporation is losing money– Corporations is highly profitableCorporations is highly profitable– Expect to sell business at a profitExpect to sell business at a profit

Tax Reason for S corp.Tax Reason for S corp.

• Corporation is losing moneyCorporation is losing money– Valuable to have losses flow through to Valuable to have losses flow through to

individual tax returnindividual tax return• Only valuable if have other personal Only valuable if have other personal

income to offset againstincome to offset against– Losses are limited to basisLosses are limited to basis

• Basis is stock investment and loans to Basis is stock investment and loans to corporationcorporation

Tax Reasons for S CorpTax Reasons for S Corp

• Corporation is highly profitableCorporation is highly profitable– Although double taxation rarely Although double taxation rarely

applies, there is always the risk the IRS applies, there is always the risk the IRS will deem salaries “excessive”will deem salaries “excessive”

• Excess salaries are treated as Excess salaries are treated as dividendsdividends

– Issue of salary vs. dividend doesn’t Issue of salary vs. dividend doesn’t matter with S corp, since no corporate matter with S corp, since no corporate level taxlevel tax

Changing Popularity of Business FormsChanging Popularity of Business Forms

S. Prop C Corp S Corp Part.0

2000

4000

6000

8000

10000

12000

14000

16000

S. Prop C Corp S Corp Part.

1980

1992

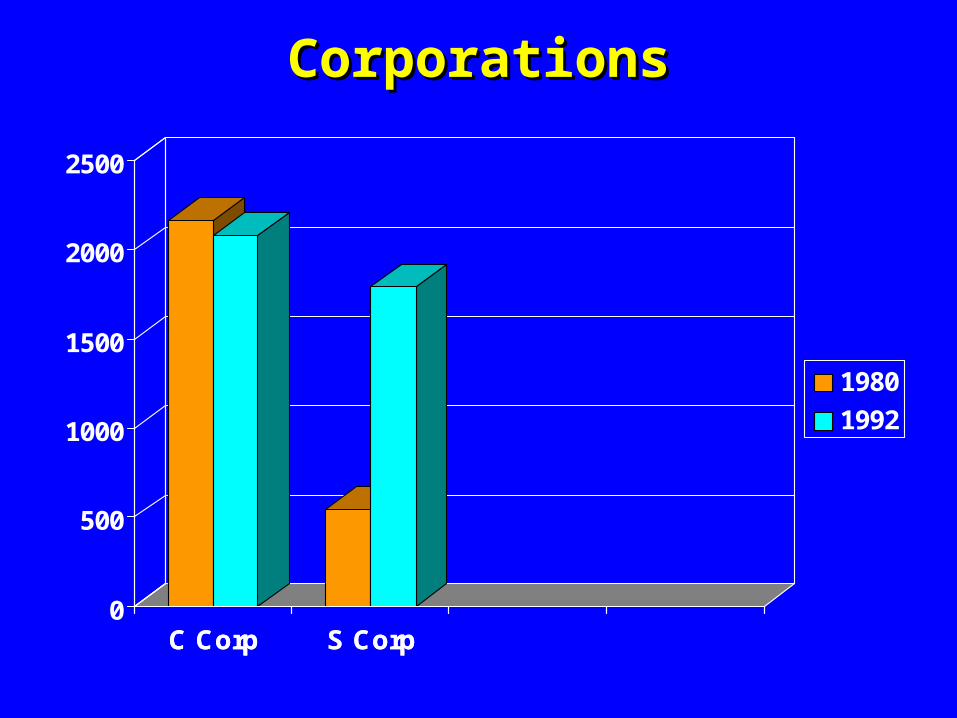

CorporationsCorporations

C Corp S Corp0

500

1000

1500

2000

2500

C Corp S Corp

1980

1992

Increasing Popularity of S CorpIncreasing Popularity of S Corp

1986 Tax Reform Act lowered 1986 Tax Reform Act lowered maximum individual ratemaximum individual rate – Historically, max individual rate higher Historically, max individual rate higher

than max corp ratethan max corp rate

– Created incentive to keep income in corpCreated incentive to keep income in corp

• 86 Act made max individual rate < max 86 Act made max individual rate < max corp ratecorp rate– Companies became S corps in drovesCompanies became S corps in droves

Popularity of Business FormsPopularity of Business Forms

• 1993 Tax Act increased individual rates1993 Tax Act increased individual rates– S corp is no longer as advantageousS corp is no longer as advantageous

• New kid on block - LLCNew kid on block - LLC– Offers limited liability with pass-Offers limited liability with pass-

throughthrough– More flexible than S corpMore flexible than S corp– Often better than limited partnership, Often better than limited partnership,

which must have one general partnerwhich must have one general partner

Ownership of Real EstateOwnership of Real Estate

• Business real property should be Business real property should be owned individuallyowned individually– Either by the entrepreneur, or other Either by the entrepreneur, or other

family membersfamily members– Allows payout to passive family membersAllows payout to passive family members– Allows payout to entrepreneur without Allows payout to entrepreneur without

payroll taxespayroll taxes– Some tax benefitsSome tax benefits

Section 1244 StockSection 1244 Stock

• Initial stock investment should be Initial stock investment should be characterized as “Section 1244” stockcharacterized as “Section 1244” stock– Loss up to $50,000 ($100,000 joint) is Loss up to $50,000 ($100,000 joint) is

deductible as ordinary lossdeductible as ordinary loss

• Otherwise, loss is capital lossOtherwise, loss is capital loss– Limited to $3,000 deduction plus any Limited to $3,000 deduction plus any

capital gains (unused) balance carried capital gains (unused) balance carried forward)forward)

Form of InvestmentForm of Investment

• Corporation must have some stockCorporation must have some stock

• Debt is preferred to stockDebt is preferred to stock– Interest is deductible to corporationInterest is deductible to corporation

• Not subject to employment taxesNot subject to employment taxes

– Repayment is tax-freeRepayment is tax-free

Ownership Allocation ExampleOwnership Allocation Example

Owner A Owner BOwner A Owner BCommon stock - $1,000 $1,000Common stock - $1,000 $1,000 $1.00 par$1.00 par

Additional paid-in Additional paid-in 0 0 9,0009,000

Total contributed $Total contributed $1,0001,000 $ $10,00010,000

Ownership 50% 50%Ownership 50% 50% (1000 shs.) (1000 shs.)(1000 shs.) (1000 shs.)

Working with PartnersWorking with Partners

• Power sharing is difficultPower sharing is difficult– Often better to maintain effective controlOften better to maintain effective control

– Having three owners is probably easier Having three owners is probably easier than two with 50/50 splitthan two with 50/50 split

• All significant issues should be spelled All significant issues should be spelled out in partnership agreement, or out in partnership agreement, or corporate by-lawscorporate by-laws

Issues to AddressIssues to Address

• CompensationCompensation

• Transfer and redemption of sharesTransfer and redemption of shares

• Generally want to restrict transfer of Generally want to restrict transfer of ownershipownership– Redemption - company purchasesRedemption - company purchases

– Cross-purchase - other shareholders Cross-purchase - other shareholders purchasepurchase

– Often funded by life-insuranceOften funded by life-insurance

– Price often based on formulaPrice often based on formula