Embed Size (px)

DESCRIPTION

research

Citation preview

This article was downloaded by: [Umeå University Library]On: 01 April 2015, At: 23:00Publisher: RoutledgeInforma Ltd Registered in England and Wales Registered Number: 1072954 Registeredoffice: Mortimer House, 37-41 Mortimer Street, London W1T 3JH, UK

Journal of Management InformationSystemsPublication details, including instructions for authors andsubscription information:http://www.tandfonline.com/loi/mmis20

The Impact of Cloud Computing: Shouldthe IT Department Be Organized as aCost Center or a Profit Center?Vidyanand Choudhary a & Joseph Vithayathil ba Merage School of Business, University of California, Irvineb Department of Management, Information Systems, andEntrepreneurship (MISE) at the College of Business, WashingtonState UniversityPublished online: 08 Dec 2014.

To cite this article: Vidyanand Choudhary & Joseph Vithayathil (2013) The Impact of CloudComputing: Should the IT Department Be Organized as a Cost Center or a Profit Center?, Journal ofManagement Information Systems, 30:2, 67-100

To link to this article: http://dx.doi.org/10.2753/MIS0742-1222300203

PLEASE SCROLL DOWN FOR ARTICLE

Taylor & Francis makes every effort to ensure the accuracy of all the information (the“Content”) contained in the publications on our platform. However, Taylor & Francis,our agents, and our licensors make no representations or warranties whatsoever as tothe accuracy, completeness, or suitability for any purpose of the Content. Any opinionsand views expressed in this publication are the opinions and views of the authors,and are not the views of or endorsed by Taylor & Francis. The accuracy of the Contentshould not be relied upon and should be independently verified with primary sourcesof information. Taylor and Francis shall not be liable for any losses, actions, claims,proceedings, demands, costs, expenses, damages, and other liabilities whatsoever orhowsoever caused arising directly or indirectly in connection with, in relation to or arisingout of the use of the Content.

This article may be used for research, teaching, and private study purposes. Anysubstantial or systematic reproduction, redistribution, reselling, loan, sub-licensing,systematic supply, or distribution in any form to anyone is expressly forbidden. Terms &Conditions of access and use can be found at http://www.tandfonline.com/page/terms-and-conditions

Journal of Management Information Systems / Fall 2013, Vol. 30, No. 2, pp. 67–100.

© 2013 M.E. Sharpe, Inc. All rights reserved. Permissions: www.copyright.com

ISSN 0742–1222 (print) / ISSN 1557–928X (online)

DOI: 10.2753/MIS0742-1222300203

The Impact of Cloud Computing: Should the IT Department Be Organized as a Cost Center or a Profit Center?

VIDyANAND ChOuDhAry AND JOSEPh VIthAyAthIl

Vidyanand (VC) Choudhary is an associate professor of information systems at the Merage School of Business, university of California, Irvine. he received his Ph.D. in management and an M.S. in industrial engineering from Purdue university, and a B.tech. in computer science and engineering from the Indian Institute of technol-ogy, Delhi. his research interests are broadly in the area of economics of information systems—industrial organization and game theory applied in the context of information systems. Specific research topics include governance of It, information goods pricing and product design, price discrimination and versioning strategy, and cloud computing. his research has been published in a number of journals, including Management Sci-ence, Information Systems Research, and Journal of Management Information Systems. he is a cofounder of the Workshop on theory in Economics of Information Systems (tEIS), which is in its third year. his research papers have won best paper awards at the twenty-Second International Conference on Information Systems (ICIS) and the tenth Workshop on Information technology and Systems (WItS).

Joseph Vithayathil is an assistant professor in the Department of Management, Information Systems, and Entrepreneurship (MISE) at the College of Business, Wash-ington State university. he received his Ph.D. in management from the university of California, Irvine, an MBA from harvard university, an M.S. in systems science and mathematics from Washington university in St. louis, and a B.tech. in electrical engineering from the Indian Institute of technology, Madras. his research interests are broadly in the area of economics of information systems and the application of economic theory, agency theory and the related issues of moral hazard, adverse selec-tion, information asymmetry, and incentives in the context of information systems. Specific research topics include governance of It, It-enabled corporate governance, and the impact of cloud computing and social media on organizations. he has signifi-cant professional and entrepreneurial experience in the It industry and in executive management.

abstraCt: how does the adoption of cloud computing by a firm affect the organiza-tional structure of its information technology (It) department? to analyze this ques-tion, we consider an It department that procures It services from a cloud computing vendor and enhances these services for consuming units within the firm. Our model incorporates the competitive environment faced by the cloud vendor, which affects the price of the cloud vendor. We find that when the cloud vendor faces intense competi-tion, the cost-center organizational model is preferred over the profit-center model. Infrastructure services such as basic storage, e-mail, and raw computing face intense competition, and our results suggest that such services be offered as a free corporate resource under the cost-center organizational structure. When the cloud vendor has

Dow

nloa

ded

by [

Um

eå U

nive

rsity

Lib

rary

] at

23:

01 0

1 A

pril

2015

68 ChOuDhAry AND VIthAyAthIl

pricing power, a profit-center organizational structure is likely to be preferred. Our results suggest that highly differentiated services such as cloud-based enterprise-wide enterprise resource planning or business intelligence be offered under the profit-center structure. Finally, the profit-center structure provides greater internal quality enhance-ment to cloud-based It services than the cost center.

Key words and phrases: chargeback, cloud, cloud computing, cost center, IaaS, It governance, PaaS, profit center, SaaS, supply chain.

Cloud Computing is a disruptiVe teChnology that provides an alternative or is an adjunct to in-house information technology (It) services. For example, Dropbox and Amazon.com are disrupting the market for traditional storage providers while Carbonite and Box are disrupting the market for backup services. Forrester research predicted that the public cloud computing market will grow from $26 billion in 2012 to $160 billion in 2020 [9]. this extraordinary growth forecast represents a com-pounded annual growth rate (CAGr) of 25 percent. International Data Corporation (IDC) [23] forecasted that public It cloud services would grow from $21.5 billion in 2010 to $72.9 billion in 2015, which represents a CAGr of 27.6 percent. IDC further noted that the cloud services growth rate surpasses the overall It services global growth rate of 6.7 percent. there are cloud services available for all major enterprise systems. For example, cloud-based enterprise resource planning (ErP) services are available from IBM, Microsoft, Oracle, and SAP. Similarly, customer relationship management (CrM) services are available on the cloud from Salesforce.com, Sage, and NetSuite.

the availability of on-demand It services and the pay-as-you-go pricing model makes it attractive for firms to source many It services from the cloud. the role of the It department within firms that source most of their It services from the cloud is likely to be very different from the current model where the It department provides captive services. In the former, the It department is likely to oversee vendor selec-tion, determine and enforce corporate standards for security and privacy, and provide enhancement to the incoming cloud services such as application and data integration. For example, the Avis Budget Group and Dell were using on-premises CrM solutions that were executed and maintained by their It departments. Now they use Salesforce.com as a cloud-based CrM vendor. the It department at the Avis Budget Group provides limited integration with legacy systems.

this changing role of the It department should affect the governance structure of the It department. Prior information systems (IS) literature and evidence from industry show that two forms of It governance are prevalent: the profit center and the cost center. In this paper we develop a stylized model to examine the impact of cloud computing and software as a service (SaaS) on the choice of organizational form. We address the following research questions:

Dow

nloa

ded

by [

Um

eå U

nive

rsity

Lib

rary

] at

23:

01 0

1 A

pril

2015

thE IMPACt OF ClOuD COMPutING 69

RQ1: When is it better for a firm that uses cloud-based services to organize the IT department as a cost center versus a profit center?

RQ2: What are the factors that drive the choice of organizational structure in this context?

RQ3: How much quality enhancement is provided by the IT department under the different organizational structures?

the National Institute of Standards and technologies (NISt) [28] has characterized cloud computing into three building layers: infrastructure as a service (IaaS), platform as a service (PaaS), and Saas. While there are other definitions proposed, the NISt definition is widely used. Amazon.com’s EC2 (Elastic Compute Cloud) offering is an example of an IaaS, and Microsoft’s Azure is an example of PaaS, while NetSuite and Salesforce.com are examples of SaaS. Armbrust et al. [2, 3] and Mell and Grance [28] provide the structure and characteristics of cloud computing; they note that cloud computing consists of software applications offered as a service as well as computing and storage infrastructure services. A distinctive benefit to users of cloud services is the pay-as-you-use attribute. A second important financial feature enabled by cloud computing, as noted by Armbrust et al. [2], is the ability for the firm to eliminate the fixed cost of a captive data center and only incur usage-based pricing for It services from the external cloud vendor. Choudhary [8] shows that the faster dissemination of new features under cloud-based SaaS can lead to higher quality of It services.

Gurbaxani and Kemerer [21, 22] and others note that It departments are commonly organized as either a profit center or a cost center. under the profit-center model, It services come with a pricing schedule that internal users pay. In contrast, the cost center offers internal It services at no charge to the internal users. Gurbaxani and Kemerer raise the issue of information asymmetry between the It department, internal It con-suming functional units, and the firm. Jensen and Meckling [24] argue that managers within a firm possess private knowledge that leads to information asymmetry. Such information asymmetry can make it difficult for the firm to determine the optimal price for It services. Our description of a cost center fits with their “expense center,” where It services are provided free of charge to internal consumers. the prior literature on the organizational structure for the It department is in the context of captive It ser-vices. the question regarding the impact of the It department procuring cloud-based It services on the choice of organizational structure has not been addressed.

Internal pricing of It services is analyzed in the prior literature by Dewan [12], Dewan and Mendelson [13], Mendelson [29], Pick and Whinston [30], Wang and Barron [35], and Whang [36]. Wang and Barron [35] also analyze the profit center and the cost center. they consider computer usage in their analysis, as well as the It department’s objective to maximize budget allocation to It. they conclude that the profit center is unable to overcome the rent that the It department can extract from information asymmetry; therefore, the cost center is always the preferred organizational structure. In contrast, we demonstrate that both organizational forms are viable and use an alternative approach to that of Wang and Barron by evaluating benefits to the firm

Dow

nloa

ded

by [

Um

eå U

nive

rsity

Lib

rary

] at

23:

01 0

1 A

pril

2015

70 ChOuDhAry AND VIthAyAthIl

from the use of It. under this approach, the It department maximizes profits when operated as a profit center and determines internal price and quality of It services; whereas when operated as a cost center, the firm determines the quality of It services. Jensen and Meckling [24] and Wang and Barron [35] consider the objective of the cost center to be cost minimization. A cost-minimization strategy may not account for the benefits that accrue from higher-quality services. We employ a model of the cost center where the objective of the firm is to maximize the benefits from It. Jensen and Meckling [24] and Wang and Barron [35] consider information asymmetry on the cost of It, to which we add information asymmetry of the demand profile for It services by the internal consumers.

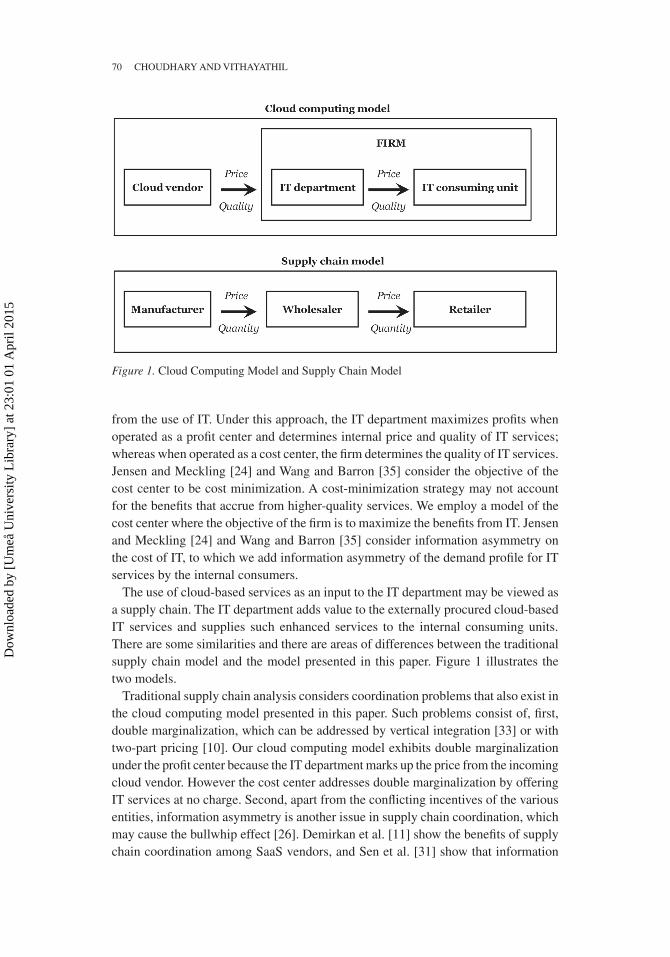

the use of cloud-based services as an input to the It department may be viewed as a supply chain. the It department adds value to the externally procured cloud-based It services and supplies such enhanced services to the internal consuming units. there are some similarities and there are areas of differences between the traditional supply chain model and the model presented in this paper. Figure 1 illustrates the two models.

traditional supply chain analysis considers coordination problems that also exist in the cloud computing model presented in this paper. Such problems consist of, first, double marginalization, which can be addressed by vertical integration [33] or with two-part pricing [10]. Our cloud computing model exhibits double marginalization under the profit center because the It department marks up the price from the incoming cloud vendor. however the cost center addresses double marginalization by offering It services at no charge. Second, apart from the conflicting incentives of the various entities, information asymmetry is another issue in supply chain coordination, which may cause the bullwhip effect [26]. Demirkan et al. [11] show the benefits of supply chain coordination among SaaS vendors, and Sen et al. [31] show that information

Figure 1. Cloud Computing Model and Supply Chain Model

Dow

nloa

ded

by [

Um

eå U

nive

rsity

Lib

rary

] at

23:

01 0

1 A

pril

2015

thE IMPACt OF ClOuD COMPutING 71

sharing in It services outsourcing is welfare enhancing. In our model, the cost cen-ter is characterized by information asymmetry, whereas in the profit center, the It department possesses cost and demand information and is responsible for pricing, thus alleviating the information problem. third, supply chain analysis also considers inventory optimization, which has solutions such as revenue-sharing contracts [6, 7], information sharing [19, 27], and quantity discounts [15]. In contrast, this paper is centered on It services without any physical goods. Fourth, quality is mostly absent from this literature and the primary considerations in the prior literature are price and quantity. however, there are limited exceptions such as Economides [16], who exam-ines supplier quality, where vertical integration can result in quality improvement.

Our cloud computing model conceptually resembles a supply chain structure. how-ever, there are important areas of differences. First, we include the firm as the govern-ing body over two of the supply chain entities: the It department and the consuming unit. Furthermore, the firm has the authority to impose the operating organizational structure, which is either the cost center or the profit center. the firm optimizes over the two supply chain entities under its purview, whereas the traditional supply chain models consider each entity as optimizing its own benefit separately, or the models optimize overall supply chain benefit. Second, the effect of double marginalization under the profit-center model is different from traditional supply chain setting because the profits from the It department remain within the firm. third, the cloud computing model in this paper considers It services and therefore does not encounter supply chain issues for physical goods such as stock-outs or excess inventory. Fourth, we include the quality of It services supplied as an important characteristic of It services under the cloud computing model. Moreover, the well-used news vendor model employed in the supply chain literature does not apply here because demand is modeled as deter-ministic and as private information of the consuming unit. Furthermore, traditional supply chains have characteristics such as long-term relationships, negotiated pricing, and revenue sharing, which are also present in outsourcing contracts as described later. In contrast, cloud computing services are defined in this paper by the characteristics of arm’s-length, take-it-or-leave-it standard pricing that is based on usage.

Most It services have marginal cost associated with the services. We draw a dis-tinction between such It services and information goods. Digital information goods such as music, books, and software have zero or almost zero marginal cost, whereas typical It services provided within a firm have nonzero marginal cost. Networking and storage services have a cost per unit such a megabits per second or megabytes, respectively, whereas other communication services have subscription costs. Allen [1] supports the notion of marginal cost of It services, while Dewan [12] analyzes pric-ing and suggests that computer services be priced at marginal cost. In this paper, the marginal cost has two parts: (1) a base marginal cost and (2) marginal cost of quality that is increasing in quality. the It department enhances the quality of It services, where quality can be defined as the service-level responsiveness or a low error rate in transaction processing. Quality improvement under such a definition is likely to have a fixed cost component as well as a quality-related marginal cost component. As a simple example, when the number of internal It consumers grow, the support required

Dow

nloa

ded

by [

Um

eå U

nive

rsity

Lib

rary

] at

23:

01 0

1 A

pril

2015

72 ChOuDhAry AND VIthAyAthIl

for maintaining the service-level quality may require a new fixed cost infrastructure as well as an increased, variable labor cost. In contrast to a fully captive It department, under our cloud computing setting in this paper, it is the cloud vendor who provides the initial quality of It service. this initial quality may be enhanced by the It depart-ment. Our marginal cost function captures the notion that modest enhancements can be accomplished within reasonable costs, but major enhancements are likely to be prohibitively expensive.

traditional It outsourcing has characteristics that are materially different from that of cloud computing. Outsourcing possesses one or more of the following character-istics: (1) medium- to long-term contracts; (2) a single customer per contract; (3) a contract structure that may be one or more of time and materials, performance-based, or incentive-based contracts; (4) customized covenants; (5) negotiated pricing; (6) a single vendor; (7) a custom product; and (8) is relationship specific. Furthermore, the It system or service development is fully customized; therefore, the constraints on quality improvement under outsourcing are similar to that faced under captive It service or system development.

In contrast, cloud computing vendors offer a standardized product to all custom-ers with take-it-or-leave-it pricing that has a metered or a pay-for-usage structure. Standardized cloud-based It services have a mass-market orientation, thus limiting the customization or customer-specific quality enhancements that are possible under traditional outsourcing. hence, the amount of customization to improve the elements of It quality may be more limited under cloud computing when compared to traditional It outsourcing or fully internal It development. therefore, internal quality enhance-ments to cloud-supplied services need to be incremental. We capture this dimension of cloud computing by normalizing the marginal cost of quality improvement by the base level of quality supplied by the vendor. under this setting, higher internal It quality levels will require a sufficiently high base level of quality from the cloud vendor because the cost of a substantial quality improvement is prohibitive. Because of these significant differences between traditional outsourcing and cloud computing, this paper focuses on cloud-sourced It services.

the It department is modeled as executing its task within each organizational structure without shirking. We also assume that the internal It-consuming functional units need the It department to add value to cloud-based It services before the final services are delivered to them. the value added to It services procured from the cloud vendor may take the form of quality improvement, monitoring, and ensuring vendor performance, selection, and administration of vendors, as well as adding software and other application functions on top of the procured services. For example, if the procured services are SaaS, the It department may add value by administering the services for internal clients or it may add user-specific applications on top of the SaaS offering by the use of application programming interfaces (APIs).

the effect of cloud computing on the choice of organizational model has not been studied previously. We examine whether a cost-center or profit-center organizational structure is better for the firm when the It department obtains services from a cloud vendor at a certain price and quality. We find that the pricing power of the cloud ven-

Dow

nloa

ded

by [

Um

eå U

nive

rsity

Lib

rary

] at

23:

01 0

1 A

pril

2015

thE IMPACt OF ClOuD COMPutING 73

dor affects the choice of organizational structure for the It department. In addition, we find that the choice of organizational structure affects the level of internal quality enhancement of the It services that are procured from a cloud vendor.

We find that the profit center is the preferred organizational structure for the It depart-ment when the cloud vendor is characterized by high pricing power as this structure generates greater benefits from It for the firm than the cost-center structure. When the cloud computing services are infrastructure oriented or commodity oriented, it is beneficial for the firm to organize the It department as a cost center. under the NISt description of cloud computing, IaaS provides the least value-added services within the gamut of cloud computing offerings. According to Knipp [25], IaaS has become a commodity, and IaaS services are subject to intense competition. Cloud services that constitute IaaS offering are services such as basic storage or raw computing resources. We find that such services should be offered as a free corporate resource under a cost-center organizational structure.

In contrast, when the It department deploys higher value-added or differentiated cloud-based services, the results indicate that a profit-center organizational structure is preferred. In the NISt cloud computing model, PaaS and SaaS constitute higher value-added services such as ErP, CrM, and business intelligence (BI).

We also find that the profit center offers higher internal quality enhancement when the cloud vendor’s pricing power is high, otherwise the cost center provides higher-quality enhancement. We find that quality enhancement and consumption of It services decrease with increasing pricing power of the cloud vendor for the profit center as well as the cost center. under the profit-center organizational structure, increasing pricing power of the cloud vendor can lead to a reduction in the price charged to the internal consuming units.

the sections that follow include the following: a description of the conceptual model followed by the development of the analytical model, which examines whether the cost-center or profit-center organizational structure is preferred. the analysis is followed by a discussion of the results, managerial implications, and concluding remarks.

Conceptual Model

this paper foCuses on the organizational struCture of the internal It department when the It department (1) procures cloud-based It services and (2) adds value to these procured services for delivery to internal consumers. We examine which organizational form for the It department, the cost center or the profit center, maximizes benefit to the firm from the use of It. We examine the impact of cloud-specific factors such as the competitive environment faced by the cloud vendor and the price and quality of services provided by the cloud vendor.

It Organizational Structure

there are four parties in our model: (1) the It department that provides It services to the internal consumers within the firm; (2) the internal consumers or consuming units

Dow

nloa

ded

by [

Um

eå U

nive

rsity

Lib

rary

] at

23:

01 0

1 A

pril

2015

74 ChOuDhAry AND VIthAyAthIl

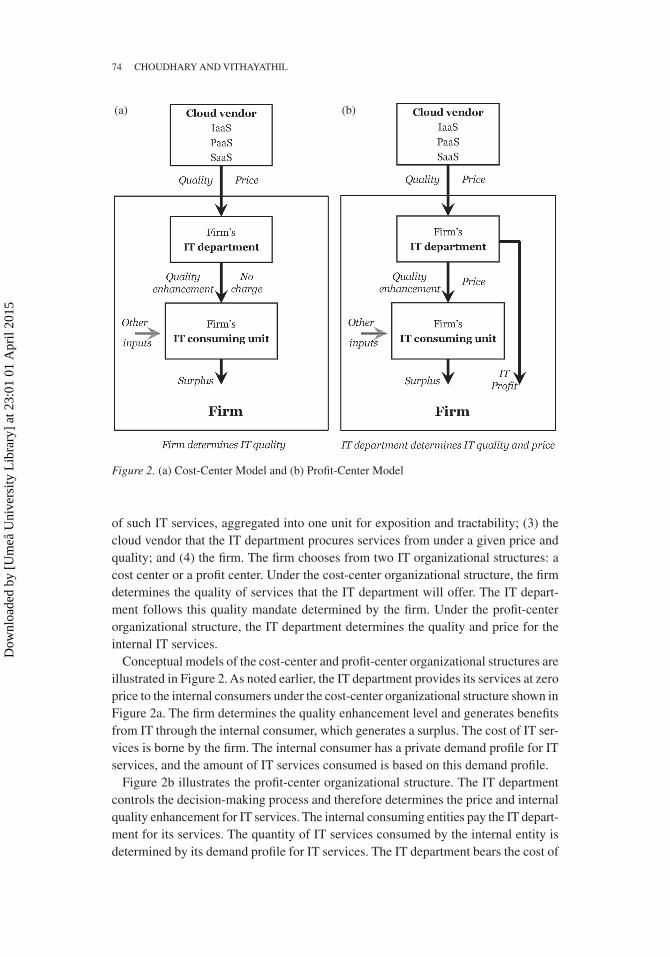

of such It services, aggregated into one unit for exposition and tractability; (3) the cloud vendor that the It department procures services from under a given price and quality; and (4) the firm. the firm chooses from two It organizational structures: a cost center or a profit center. under the cost-center organizational structure, the firm determines the quality of services that the It department will offer. the It depart-ment follows this quality mandate determined by the firm. under the profit-center organizational structure, the It department determines the quality and price for the internal It services.

Conceptual models of the cost-center and profit-center organizational structures are illustrated in Figure 2. As noted earlier, the It department provides its services at zero price to the internal consumers under the cost-center organizational structure shown in Figure 2a. the firm determines the quality enhancement level and generates benefits from It through the internal consumer, which generates a surplus. the cost of It ser-vices is borne by the firm. the internal consumer has a private demand profile for It services, and the amount of It services consumed is based on this demand profile.

Figure 2b illustrates the profit-center organizational structure. the It department controls the decision-making process and therefore determines the price and internal quality enhancement for It services. the internal consuming entities pay the It depart-ment for its services. the quantity of It services consumed by the internal entity is determined by its demand profile for It services. the It department bears the cost of

Figure 2. (a) Cost-Center Model and (b) Profit-Center Model

(a) (b)

Dow

nloa

ded

by [

Um

eå U

nive

rsity

Lib

rary

] at

23:

01 0

1 A

pril

2015

thE IMPACt OF ClOuD COMPutING 75

providing It services and receives the revenue from the internal consumers. Finally, the total benefit to the firm from the use of It is the sum of the It department profits and the surplus generated by the internal consumer.

Information asymmetry is present in our model with regard to the cost of It and internal demand for It services. Consistent with Jensen and Meckling [24] and Wang and Barron [35], the cost information is private to the It department. the internal It-consuming unit knows its demand and the willingness to pay (WtP) for It services, and this is private information in the cost-center organizational structure. however, when the It department is organized as a profit center, the buyer and seller relation-ship enables the It department to learn the aggregate demand profile of the internal consuming entity. the firm can estimate the cost of It and the consuming entity’s demand for It services.

Model

the analytiCal model we deVelop is stylized and includes simplifying assumptions that are necessary for tractability and clarity of exposition of the key results. We now describe the details of the model about the It department. the It department procures It services from the cloud vendor, enhances the cloud vendor’s incoming It quality, and supplies the enhanced It services to the internal consuming units. We refer to the internal consuming units as the “internal customer.” the quantity of It services provided to the internal customer is denoted as x, the quality of It services provided to the internal customer is denoted as q. the It department procures It services from the cloud vendor at a quality q

c and at a price p

c charged by the cloud

vendor. the It department enhances qc by an amount ∆q and supplies the resulting

quality q = qC +

∆q.

We assume that demand, cost, and profit functions are continuous, and the payoff functions are twice differentiable and concave. the demand for It services by the consuming unit is decreasing in price charged for the service and increasing in quality supplied. the consuming unit is assumed to have exogenously determined its demand for It services for any given price and quality. the base level of quality necessary to operate the firm is zero, and the base level of demand for It services is at zero quality and price. the demand profile of the internal consumer is such that at a sufficiently high price, there will be no consumption of It services.

When the It department operates under the cost-center organizational structure, the information asymmetry with regard to cost and demand renders the firm incapable of determining an optimal quality level based on full information. therefore, under such information asymmetry, the firm estimates its optimal quality level, and we use q*CC to denote the estimated quality. Firms use various methods such as benchmarking [20] to estimate quality. We capture the effect of information asymmetry in our model by introducing an error term in the firm’s estimate of demand and cost functions.

When the It department operates under the profit-center organizational structure, the It department sets the price and quality level for internal It services to maximize its profits π

IT . As noted in the introduction, the It department is informed of the demand

Dow

nloa

ded

by [

Um

eå U

nive

rsity

Lib

rary

] at

23:

01 0

1 A

pril

2015

76 ChOuDhAry AND VIthAyAthIl

function of the internal consumer as well as its own costs. the price and quality set by the It department operating as a profit center are p*PC and q*PC. the It department sets the price p*PC and quality q*PC in order to maximize its profits π

IT .

Next, we describe the details of the model as they pertain to the internal consumer of It services. the internal demand for It services x is characterized by a linear demand function. the quantity of It services consumed is a function of the price and quality of the internal It services as follows:

x = k – a · p + b · q.

the intercept for demand is denoted by a parameter k. the parameters a and b denote the marginal effect of price and quality of It services on the internal consumer, respectively. this linear demand specification is consistent with the prior literature (e.g., [4, 5, 14, 17, 18, 32, 34]). In order to capture the effect of information asym-metry, we assume that the firm is not fully informed about the value of the demand parameter b. the firm believes that this parameter is drawn from a uniform distribution U(b – ε, b + ε), where ε is a noise parameter for the estimate.

the WtP for It services by the consumer is specified by the inverse demand function (k + b · q – x)/a. thus, we can derive the surplus generated by the internal consumer by integrating the inverse demand:

Sk q x

dx x pI

x

=+ ⋅ −

− ⋅∫βα0

.

Now we describe the model details as they pertain to the cloud vendor. the cloud vendor serves the broader market for cloud services and will have many customers. the price and quality of its cloud-based It services such as IaaS, PaaS, and SaaS are determined by the market forces facing this vendor. Such market forces include com-petition, demand, and cost. the It department of the focal firm in this paper procures x quantity of cloud-based It services at a quality level q

C from the cloud vendor.

the price charged by the cloud vendor is denoted by pC , which depends on the qual-

ity of their service and various other factors such as competition, efficiencies from multitenancy, and scale and scope. We treat these competitive factors as exogenous, and they are captured in our model by a parameter θ ≥ 0. larger values of θ result in the increased pricing power of the cloud vendor. the price charged by the cloud vendor is p

C = c + θ · q

C . Pure competition in the cloud is represented by θ = 0, which

yields pC = c.

the It department procures It services at quality qC and price p

C charged by the

cloud vendor. the It department adds value to these cloud services by (1) monitoring the vendors and (2) endogenously optimizing and improving It service quality by an amount denoted as ∆q to an enhanced level q = q

C + ∆q; (3) delivering It services at

this quality q to the internal consuming units; (4) incurring the marginal cost of qual-ity improvement b · ∆q / q

C , which results in total marginal cost MC

IT = p

C + b · (∆q/

qC); and (5) incurring a convex fixed cost of quality improvement expressed as

FCITQ

= a · (q2 – qC2). the ratio ∆q/q

C ensures that large quality enhancements to the

cloud vendor’s service quality are substantially more expensive to the It department.

Dow

nloa

ded

by [

Um

eå U

nive

rsity

Lib

rary

] at

23:

01 0

1 A

pril

2015

thE IMPACt OF ClOuD COMPutING 77

In order to capture the effect of information asymmetry of It cost, we assume that the firm is not fully informed about the value of the cost parameter a. the firm believes that this parameter is drawn from a uniform distribution U(a – ε, a + ε), where ε is a noise parameter for the estimate.

Assumptions

We now state the assumptions in our model.

Assumption 1 (Regularity Conditions): Standard mathematical regularity condi-tions are assumed. The demand, cost, and profit functions are continuous, and the payoff functions are twice differentiable. Demand is increasing in quality and decreasing in price: ∂D/ ∂q = b > 0, ∂D/∂q = –a < 0. The cost of quality is increasing in quality: dFC

ITQ /dq = 2a · q > 0, d2FC

ITQ /dq2 = 2a > 0. Therefore,

the cost function is convex. The IT profit and firm value are evaluated net of IT cost and are concave functions. The inverse demand function p = (k + b · q – x)/a exists and ∂p/ ∂q = b/a > 0.

Assumption 2 (Intercept): For each quality level, there is a threshold of maximum consumption denoted by x = k + b · q when the price is zero. Similarly, at a suf-ficiently high price denoted by p = (k + b · q)/a , there will be no consumption of IT services. The demand for IT services at the base quality level of q = 0 is k units.

table 1 provides a list of parameters and variables with a brief description. the sections that follow analyze the effect of organizing the It department as either a cost center or a profit center. the two organizational structures are individually analyzed in each of the subsections. the individual analysis is followed by a comparison of the results from the analysis of the two organizational structures. the proofs for the lemmas and propositions that follow are presented in the Appendix.

It Organized as a Cost Center

When It is organized as a cost center, the internal consuming unit is provided with It services at no charge. the total surplus available for the consuming business unit is

Sk q z

dzICC

CCk q CC

=+ ( ) −+ ( )

∫ˆ

.

*ˆ *β

α

β

0

the firm determines the optimal level of quality enhancement by maximizing its expected benefits from It, Max

q{E[B{

FCC]}, where B{

FCC = S

ICC – x · MC

IT – FC

ITQ. the

sequence of events is shown in table 2.

Lemma 1 (Interior Solution—IT Organized as a Cost Center Under Cloud Com-puting): Under a cost-center organizational structure with cloud computing, the firm sets quality offered by the IT department to

Dow

nloa

ded

by [

Um

eå U

nive

rsity

Lib

rary

] at

23:

01 0

1 A

pril

2015

78 ChOuDhAry AND VIthAyAthIl

qb q k q k c q

aq b q

CC C C C

C C

* ,=−( ) + − +( )( )( )

+( ) − +( )3

6 3 2 2

α β β α θ

α β β ε

and the benefit to the firm is

Bk q

qq k b c q q b q

FCC

CC

CC C

CC CC**

* *=+

+ − −( ) +( ) −( )

−

βα

α θ β α2

2 2

aa q qCCC

* .( ) −

2 2

lemma 1 reports the optimal quality that the firm would set under the cost-center organizational structure. this is the quality level that the It department would be directed to offer to the internal consuming units. It can be established that the benefit to the firm is decreasing in the marginal effect of price and also decreasing in the marginal cost of It quality enhancement. Similarly, an increase in marginal cost of quality enhancement will result in decreased benefits to the firm.

the parameter ε captures the degree of information asymmetry. When ε = 0, the firm has perfect information. We find that the optimal quality set by the firm under information asymmetry is greater than the quality that would be set when the firm has perfect information. this occurs because the firm knows that any misestimation of the quality parameter leads to reduction of benefits to the firm, and the firm compensates by increasing internal quality enhancement.

Proposition 1 (Comparative Statics for the Cost Center with Cloud Computing): Increasing pricing power of the cloud vendor results in a reduction in quality

table 1. list of Model Variables, Functions, and Parameters

Symbol Description

pC Price charged by the cloud vendor for IT servicesqC IT service quality provided by the cloud vendorc + qC Cloud vendor’s marginal cost of IT servicesθ Competitive environment of the cloud vendorε Maximum error in firm’s estimation of b, aq Quality of IT services provided by the IT departmentπIT IT department profit under the profit-center organizational structureBF Benefit to the firm from ITSI Surplus generated by the internal IT consumer∆q Internal quality enhancement by the IT departmentx IT services quantity consumed by the firma Fixed cost of quality parametera Marginal effect of internal price on IT service consumptionb Marginal effect of quality on IT service consumptionk Intercept of the consumer demand function b Marginal cost of quality enhancement parameter

Dow

nloa

ded

by [

Um

eå U

nive

rsity

Lib

rary

] at

23:

01 0

1 A

pril

2015

thE IMPACt OF ClOuD COMPutING 79

enhancement by the IT department and lower consumption of IT services by the consuming unit: ∂(∆q*CC)/ ∂θ < 0, ∂x*CC/ ∂θ < 0.

Proposition 1 reports the effect of competition faced by the cloud vendor on the internal quality enhancement of It services by the It department. At first glance, the relationship between the level of competition in the cloud and the level of quality enhancement provided by the internal It department is not obvious. If the cloud vendor enjoys greater pricing power, then it charges higher prices. the firm could direct the It department to increase the level of internal quality enhancement to justify the higher cost and provide increased surplus for the consuming unit. however, Proposition 1 shows that the firm will instruct the It department to reduce quality enhancement when the cloud vendor has increased pricing power.

to understand this result, we begin by noting that under the cost-center organizational structure, It services are offered as a free corporate resource to the consuming unit. hence, there will be overconsumption of such It services. When the cloud vendor’s prices are increased, the firm finds such overconsumption to be even more detrimental to the benefits derived from It. under a cost-center structure, the firm can limit con-sumption by reducing internal quality enhancement. Consequently, it chooses to reduce internal quality enhancement when the cloud vendor has increased pricing power.

Differentiated and specialized cloud computing services such as cloud-based BI software services exemplified by IBM’s Cognos Express are likely to have increased pricing power. Such services may require ongoing technical support or customization by the It department. Our results indicate that the internal consumers of such ser-vices are likely to get minimal support from the It department under the cost-center model.

It Organized as a Profit Center

Organized as a profit center, the It department has the ability to charge for internal It services, bear the cost for It services, and make a corresponding profit. the profit generated by the It department constitutes part of the benefit to the firm from the

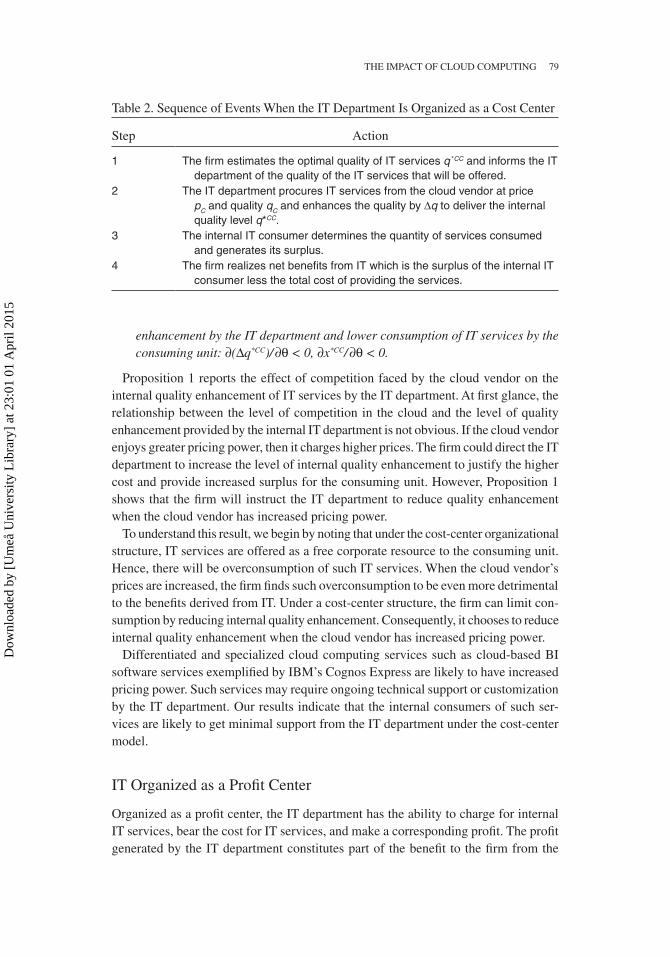

table 2. Sequence of Events When the It Department Is Organized as a Cost Center

Step Action

1 The firm estimates the optimal quality of IT services q *CC and informs the IT department of the quality of the IT services that will be offered.

2 The IT department procures IT services from the cloud vendor at price pC and quality qC and enhances the quality by ∆q to deliver the internal quality level q*CC.

3 The internal IT consumer determines the quantity of services consumed and generates its surplus.

4 The firm realizes net benefits from IT which is the surplus of the internal IT consumer less the total cost of providing the services.

Dow

nloa

ded

by [

Um

eå U

nive

rsity

Lib

rary

] at

23:

01 0

1 A

pril

2015

80 ChOuDhAry AND VIthAyAthIl

deployment and use of It. the internal consumer obtains value in the form of surplus from It services and pays the It department for such services. the It department is able to learn the demand profile of its internal consumer and procures It services from the cloud vendor at a base level of quality q

C and at a price p

C. the It depart-

ment determines the optimal internal price and quality enhancement by maximizing It profit: Max

p, q{π

IT}, where π

IT = x · pPC – MC

IT – FC

ITQ. the sequence of events is

shown in table 3.

Lemma 2 (Interior Solution: IT Organized as a Profit Center Under Cloud Com-puting): Under a profit-center organizational structure with cloud computing, the price and quality of IT services that maximizes benefit to the firm are

p

a q k b c q b q b k q q c

PC

C C C C C

* =

( ) + − + + ( )( )( ) − − ( )( ) + ( )( ) − ( ) +22 α θ α β β β qq

a q b q

C

C C

( )( )( )( ) − − ( )( )

θ

α α β∆ 2 2

qq q b k b c q

a q b q

PC C C C

C C

* ,=−( ) + −( ) −( )( ) − − ( )( )

β α α αθ

α α β42 2

and the benefit to the firm is

Bk p q

qq b q k b c qF

PCPC PC

C

PCC C

** *

*=− +

−( ) + + − −( ) +

α βα

β α α θ α2

2 2 pp

a q q

PC

PCC

*

* .

( )( )− ( ) −

2 2

lemma 2 reports the results from the solution to the first-order conditions when the It department maximizes its profits. the benefit to the firm from the use of It is the sum of the profits generated by the It department and the net surplus generated by the internal consumer. It can be seen that the benefit to the firm is decreasing in the marginal cost of It quality enhancement and the fixed cost of quality. the two

table 3. Sequence of Events When the It Department Is Organized as a Profit Center

Step Action

1 The IT department provides IT services at a price and quality denoted as {p*PC, q*PC} based on knowledge of the internal consumer’s demand function.

2 x *PC units of IT services are demanded as a function of the price and quality offered by the IT department, and a surplus to the consuming unit of SI*

PC is generated net of price for IT services.3 A profit of πIT is generated by the IT department.4 The firm realizes benefits from IT that is the sum of the net surplus of the

internal IT consumer and the profit of the IT department.

Dow

nloa

ded

by [

Um

eå U

nive

rsity

Lib

rary

] at

23:

01 0

1 A

pril

2015

thE IMPACt OF ClOuD COMPutING 81

organizational structures for the It department are compared to understand which organizational structure is favorable in terms of benefits to the firm from the use of It. the next section performs this analysis.

Proposition 2 (Comparative Statics for the Profit Center with Cloud Computing): (i) Increasing pricing power of the cloud vendor results in reduced internal IT prices, provided the cloud vendor’s quality is sufficiently high: ∂p*PC/ ∂θ < 0, q

C > bab /(b2 – 2aa), and increased internal IT prices otherwise. (ii) Increasing

pricing power of the cloud vendor results in decreasing quality enhancement by the IT department and decreasing consumption of IT services by the consuming unit ∂(∆q*PC)/ ∂θ < 0, ∂x*PC/∂θ < 0.

Proposition 2 reports the effect of increasing pricing power of the cloud vendor on internal prices for It services, internal quality enhancement of It services, and consumption of It services under the profit center. As reported in the first part of the proposition, the effect of the cloud vendor’s pricing power on internal It services is nonintuitive because it can increase or decrease internal price.

the intuition for this result is as follows: (1) when the cloud vendor supplies It services of sufficiently low quality and the cloud vendor increases price, the It depart-ment compensates by correspondingly increasing price. this in turn enables the It department to restrain the more costly internal consumption of It services by the consuming unit, whereas (2) when the cloud vendor supplies It services of sufficiently high quality and the cloud vendor raises price, the It department decreases internal quality enhancement and passes the cost savings from the lower-quality enhancement to the consuming unit in order to ensure profitable consumption of It services.

the comparative statics results in the second part of Proposition 2 with regard to quality enhancement and consumption are similar to that of the cost-center results. however, under the profit-center structure, the It department has the ability to recover the increased payments to the cloud vendor through internal pricing. this leads to lower demand, making it difficult for the It department to sustain the fixed cost of internal quality enhancement. thus, higher payments to the cloud vendor under the profit-center structure cause the It department to reduce quality enhancement when the external cloud vendor’s price increases. It follows that reduction in quality enhance-ment will reduce consumption.

Comparison of the Profit-Center and Cost-Center Organizational Models

the results from lemmas 1 and 2 can be used to generate a comparison between the two organizational structures. the comparison leads to the following propositions:

Proposition 3 (Competition in the Cloud and Choice of Organizational Structure): (a) The profit-center organizational structure is preferred if and only if the cloud vendor’s pricing power θ in the interior is (i) θ

1 < θ < θ

2 when Z

4 > 0 and (ii) θ < θ

2

or θ > θ1 when Z

4 < 0. (b) The cost-center organizational structure is preferred if

Dow

nloa

ded

by [

Um

eå U

nive

rsity

Lib

rary

] at

23:

01 0

1 A

pril

2015

82 ChOuDhAry AND VIthAyAthIl

and only if the cloud vendor’s pricing power in the interior is (i) θ < θ1 or θ > θ

2

when Z4 > 0 and (ii) θ

2 < θ < Z

1 when Z

4 < 0, where θ

1 , θ

2 , Z

4 are as defined in

the Appendix, and the feasibility conditions for interior solutions are satisfied.

Proposition 3 demonstrates that cloud services such as SaaS affects the choice of It organizational structure. Since SaaS and other cloud services are a relatively recent developments, prior literature such as Gurbaxani and Kemerer [21, 22], Jensen and Meckling [24], and Wang and Barron [35] did not consider a cloud-based environ-ment. Consequently, our result in Proposition 3 contributes to the understanding of the impact of cloud-based services such as SaaS on the choice of organizational structure for the It department.

Observation 1 (Competition in the Cloud and Choice of Organizational Struc-ture): The profit-center organizational structure is preferred when θ > θ

1 and the

cost-center organizational structure is preferred when θ < θ1.

Observation 1 is derived using numerical methods and combines the results of Proposition 3 with the feasibility conditions for interior solutions reported in lem-mas 1 and 2. We examine the interior region of the profit center and cost center across the parameter set and find that the profit center is preferred when the cloud vendor’s pricing power is sufficiently high. using SaaS as an example of a cloud-based It service, the intuition is that strong pricing power enables the SaaS vendor to charge higher prices. Because of higher pricing, under the cost-center organizational structure, the It department reduces quality enhancement. In contrast, under the profit-center structure, the It department is able to offer greater quality enhancement because of its ability to charge the internal users for such value addition. Whereas the profit cen-ter can observe changes in demand due to changes in price and quality, the decision maker in the cost center can observe the range for optimal quality but cannot pinpoint the precise level of quality to be offered. Figure 3 illustrates the effect of the cloud vendor’s pricing power from Proposition 3 and also illustrates the effect of the fixed cost of quality enhancement on the choice of organizational structure.

Proposition 4 (Competition in the Cloud and Internal IT Service Quality Enhance-ment): Under cloud computing, the profit center provides greater quality enhance-ment of IT services than the cost center if and only if the cloud vendor’s pricing power is sufficiently strong:

θ αα β α

α α β α β> − + ( )( ) +

−( ) − ( )( )+( ) + −

q b c kbk b q a q

a q b q b qC

C C

C C

/3 4

6

2 2

CC C

Cb q

q( ) −( )

( )3 2

2

αβ ε/ .

Proposition 4 demonstrates that the organizational structure of the It department under cloud computing affects the quality of internal It services. the cloud vendor’s pricing power, which is partly determined by the competitive environment of the cloud vendor, affects the magnitude and direction of the effect of internal It services quality. the prior literature has not addressed the question of cloud vendor quality or the internal quality enhancement of It services as reported in Proposition 4. Intuition may suggest that a profit center is likely to provide higher-quality enhancement than

Dow

nloa

ded

by [

Um

eå U

nive

rsity

Lib

rary

] at

23:

01 0

1 A

pril

2015

thE IMPACt OF ClOuD COMPutING 83

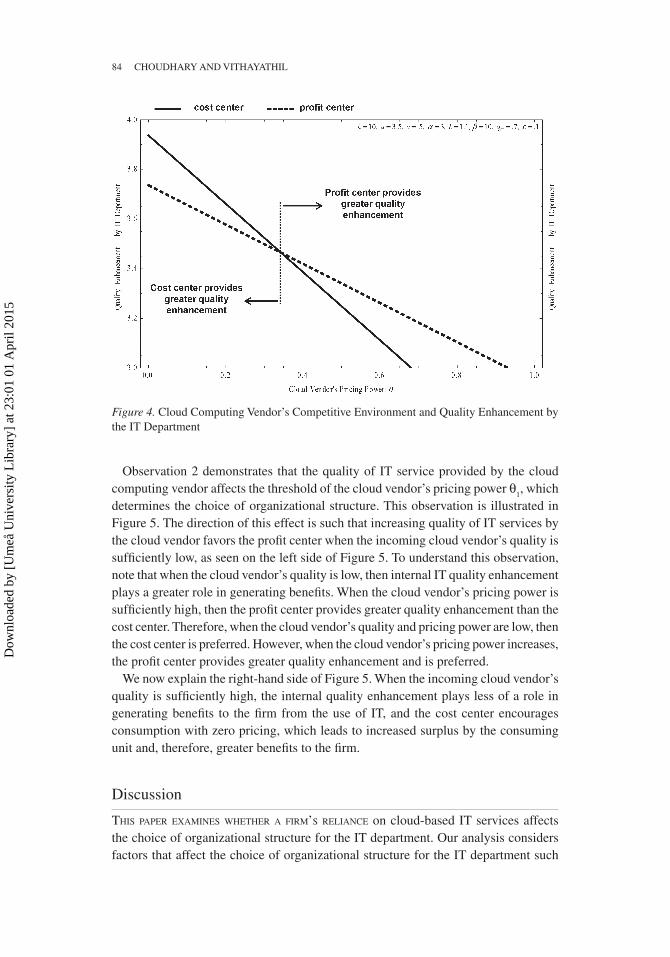

a cost center in the context of internally generated It services. Proposition 4 builds on such intuition by adding the dimension of cloud computing and the dimension of quality enhancement of It services supplied by the cloud vendor. A cloud vendor with low pricing power will supply low-priced It services, and the cost-center structure is able to spread the fixed cost of internal quality improvement over a larger consump-tion base. therefore, an It department organized as a cost center can provide greater quality enhancement than the profit center. Cloud-based storage services such as Carbonite are characterized by numerous vendors and intense competition. In such instances, the cost center is likely to provide greater quality enhancement. In con-trast, when the cloud vendor has strong pricing power, the It department organized as a profit center offers greater quality enhancement because the profit-center model allows the It department to charge for its higher-quality services. the high quality of It increases internal consumption of It services even though the consuming unit has to pay for such services. this is likely to be the case for higher-level services such as SaaS because such services are well differentiated with lower levels of competition and increased pricing power when compared to IaaS. Figure 4 illustrates the effect of the cloud vendor’s competitive environment on quality enhancement by the It department from Proposition 4.

Observation 2 (Impact of Cloud Vendor’s Quality on the Preferred Organizational Structure): The crossover threshold θ

1 defined in Proposition 3 (i) decreases with

increasing cloud vendor quality qC when the cloud vendor’s quality is sufficiently

low qC < 0.53 and (ii) increases with increasing cloud vendor quality q

C when the

cloud vendor’s quality is sufficiently high qC

> 0.71 when the parameter values are {k = 10, a = 3.5, c = 0.5, a = 3, b = 10, b = 1, ε = 0.1].

Figure 3. Cloud Computing Vendor’s Pricing Power, Fixed Cost of Quality Enhancement, and Choice of It Organizational Structure

Dow

nloa

ded

by [

Um

eå U

nive

rsity

Lib

rary

] at

23:

01 0

1 A

pril

2015

84 ChOuDhAry AND VIthAyAthIl

Observation 2 demonstrates that the quality of It service provided by the cloud computing vendor affects the threshold of the cloud vendor’s pricing power θ

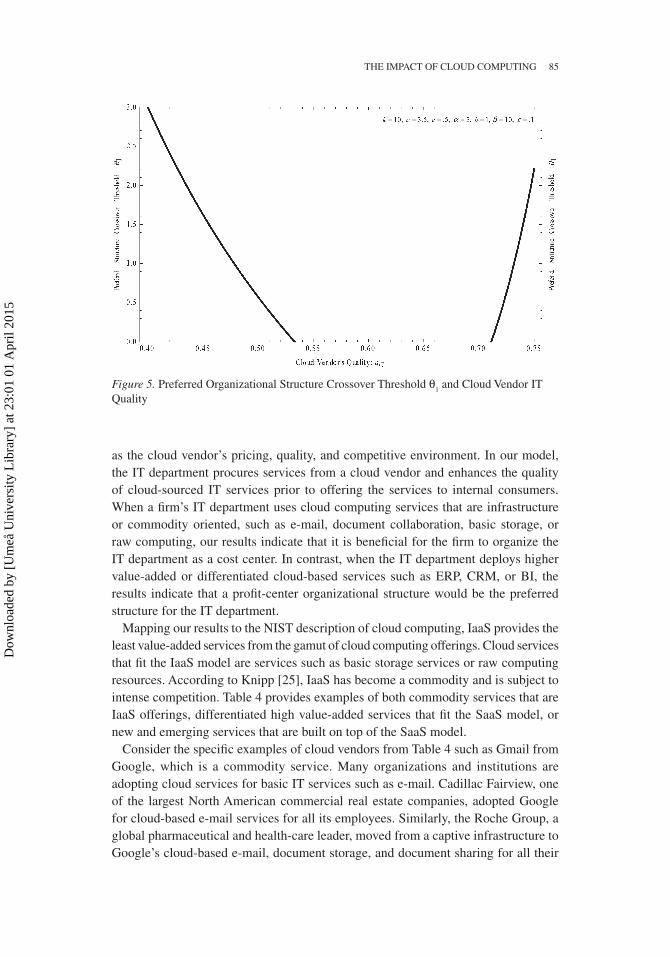

1, which

determines the choice of organizational structure. this observation is illustrated in Figure 5. the direction of this effect is such that increasing quality of It services by the cloud vendor favors the profit center when the incoming cloud vendor’s quality is sufficiently low, as seen on the left side of Figure 5. to understand this observation, note that when the cloud vendor’s quality is low, then internal It quality enhancement plays a greater role in generating benefits. When the cloud vendor’s pricing power is sufficiently high, then the profit center provides greater quality enhancement than the cost center. therefore, when the cloud vendor’s quality and pricing power are low, then the cost center is preferred. however, when the cloud vendor’s pricing power increases, the profit center provides greater quality enhancement and is preferred.

We now explain the right-hand side of Figure 5. When the incoming cloud vendor’s quality is sufficiently high, the internal quality enhancement plays less of a role in generating benefits to the firm from the use of It, and the cost center encourages consumption with zero pricing, which leads to increased surplus by the consuming unit and, therefore, greater benefits to the firm.

Discussion

this paper examines whether a firm’s relianCe on cloud-based It services affects the choice of organizational structure for the It department. Our analysis considers factors that affect the choice of organizational structure for the It department such

Figure 4. Cloud Computing Vendor’s Competitive Environment and Quality Enhancement by the It Department

Dow

nloa

ded

by [

Um

eå U

nive

rsity

Lib

rary

] at

23:

01 0

1 A

pril

2015

thE IMPACt OF ClOuD COMPutING 85

as the cloud vendor’s pricing, quality, and competitive environment. In our model, the It department procures services from a cloud vendor and enhances the quality of cloud-sourced It services prior to offering the services to internal consumers. When a firm’s It department uses cloud computing services that are infrastructure or commodity oriented, such as e-mail, document collaboration, basic storage, or raw computing, our results indicate that it is beneficial for the firm to organize the It department as a cost center. In contrast, when the It department deploys higher value-added or differentiated cloud-based services such as ErP, CrM, or BI, the results indicate that a profit-center organizational structure would be the preferred structure for the It department.

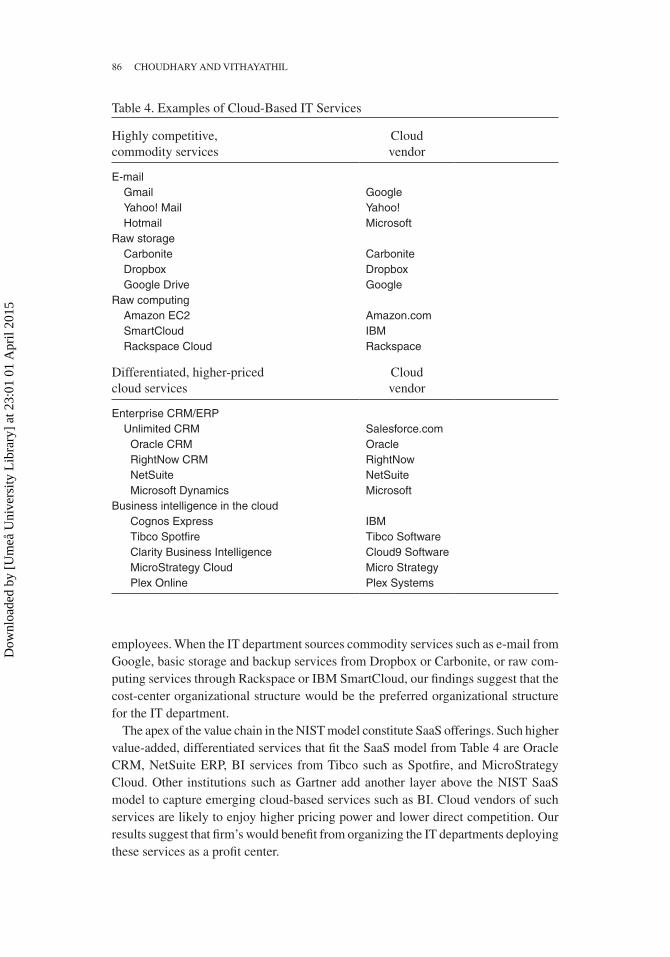

Mapping our results to the NISt description of cloud computing, IaaS provides the least value-added services from the gamut of cloud computing offerings. Cloud services that fit the IaaS model are services such as basic storage services or raw computing resources. According to Knipp [25], IaaS has become a commodity and is subject to intense competition. table 4 provides examples of both commodity services that are IaaS offerings, differentiated high value-added services that fit the SaaS model, or new and emerging services that are built on top of the SaaS model.

Consider the specific examples of cloud vendors from table 4 such as Gmail from Google, which is a commodity service. Many organizations and institutions are adopting cloud services for basic It services such as e-mail. Cadillac Fairview, one of the largest North American commercial real estate companies, adopted Google for cloud-based e-mail services for all its employees. Similarly, the roche Group, a global pharmaceutical and health-care leader, moved from a captive infrastructure to Google’s cloud-based e-mail, document storage, and document sharing for all their

Figure 5. Preferred Organizational Structure Crossover threshold θ1 and Cloud Vendor It

Quality

Dow

nloa

ded

by [

Um

eå U

nive

rsity

Lib

rary

] at

23:

01 0

1 A

pril

2015

86 ChOuDhAry AND VIthAyAthIl

employees. When the It department sources commodity services such as e-mail from Google, basic storage and backup services from Dropbox or Carbonite, or raw com-puting services through rackspace or IBM SmartCloud, our findings suggest that the cost-center organizational structure would be the preferred organizational structure for the It department.

the apex of the value chain in the NISt model constitute SaaS offerings. Such higher value-added, differentiated services that fit the SaaS model from table 4 are Oracle CrM, NetSuite ErP, BI services from tibco such as Spotfire, and MicroStrategy Cloud. Other institutions such as Gartner add another layer above the NISt SaaS model to capture emerging cloud-based services such as BI. Cloud vendors of such services are likely to enjoy higher pricing power and lower direct competition. Our results suggest that firm’s would benefit from organizing the It departments deploying these services as a profit center.

table 4. Examples of Cloud-Based It Services

highly competitive, commodity services

Cloud vendor

E-mailGmail GoogleYahoo! Mail Yahoo!Hotmail Microsoft

Raw storageCarbonite CarboniteDropbox DropboxGoogle Drive Google

Raw computingAmazon EC2 Amazon.comSmartCloud IBMRackspace Cloud Rackspace

Differentiated, higher-priced cloud services

Cloud vendor

Enterprise CRM/ERPUnlimited CRM Salesforce.com

Oracle CRM OracleRightNow CRM RightNowNetSuite NetSuiteMicrosoft Dynamics Microsoft

Business intelligence in the cloudCognos Express IBMTibco Spotfire Tibco SoftwareClarity Business Intelligence Cloud9 SoftwareMicroStrategy Cloud Micro StrategyPlex Online Plex Systems

Dow

nloa

ded

by [

Um

eå U

nive

rsity

Lib

rary

] at

23:

01 0

1 A

pril

2015

thE IMPACt OF ClOuD COMPutING 87

Vendors of SaaS services such as enterprise CrM and BI, with the characteristics of differentiated products and high value addition, are likely to enjoy greater pricing power than cloud vendors offering commodity services such as storage, backup, and e-mail. the profit-center structure is preferred when the former services are deployed because we find that the use of It under the profit center generates greater benefits to the firm than the cost center when the cloud vendor has high pricing power.

We model the quality of the internal It services as an important factor that affects the benefits that the firm derives from the use of It. In the context of internally gener-ated or captive It services, prior literature has noted that the profit center is likely to offer higher quality. this paper builds on the prior literature by analyzing the impact of the rapidly growing cloud-based sourcing of It services. In contrast, under cloud computing, the result from prior literature holds only when the cloud vendor’s pric-ing power is high. Otherwise the cost center organizational structure provides higher quality enhancement than the profit center.

Many cloud vendors, including Salesforce.com, offer APIs to enable in-house customization and quality enhancement. however, cloud vendors with proprietary technology may limit the API set, thereby increasing the cost of quality enhancement. Alternatively, cloud vendors with emerging technology such as advanced business analytics may have insufficient APIs, resulting in an increased cost of It quality enhancement. When internal quality enhancement is desirable, the client firm should consider the profit-center organizational structure if the cloud vendor has strong pric-ing power.

In our model, It services are abstracted to have one set of characteristics. In practice, though, It services have varying characteristics. Our results allow for a hybrid organiza-tional model where some services are offered at no cost to the user under a cost-center structure and others are offered under a profit-center structure. For example, table 4 shows commodity services that are characterized by intense competition and the low pricing power of the cloud vendor, and high value-added, differentiated services that are characterized by a high pricing power. When a firm offers a menu of services that cover both types of services, our results would indicate that the commodity services be offered as a free corporate resource, whereas the value-added services be offered under a profit-center model. Specifically, when a firm procures e-mail services and CrM from cloud vendors, our results suggest that the cloud-based e-mail service be offered under the cost-center model and the CrM service be offered under the profit-center model. As an example, the university of California, Irvine offers e-mail and other services at no charge, but there is a charge for other It services such as software and support for backup and recovery.

the use of cloud computing by the It department also introduces some character-istics that are similar to that of a supply chain. however, there are certain important differences. In our setting, the firm is making a decision on organizational structure instead of making decisions on inventory and related issues. the effect of double marginalization under the profit-center model is different from traditional supply chain models because the It department and the consuming unit are both part of the firm. the profits from the It department remain within the firm unlike an external

Dow

nloa

ded

by [

Um

eå U

nive

rsity

Lib

rary

] at

23:

01 0

1 A

pril

2015

88 ChOuDhAry AND VIthAyAthIl

vendor in a supply chain. this paper considers It services only and therefore we do not consider supply chain issues such as physical goods and inventory.

Conclusion

we employed a stylized model to analyze the impact of cloud computing on the choice of organizational structure for the It department. While the model makes simplifying assumptions, it produces a variety of results that add to the literature and have managerial implications. Clearly, any abstraction that is necessary for an analyti-cal model is limited in its ability to capture the complexity of It governance. Future work can relax some of the assumptions. For example, we assumed that all services are intermediated by the It department. however, future work could examine the case where some services are disintermediated such that the It consuming units procure services directly from cloud vendors. Future work could also include a hybrid cloud structure, where some services are procured from a public cloud and others are served from a private cloud. large companies with multiple users would be able to generate efficiencies comparable to that of a public cloud because they have sufficient diver-sity of internal consuming units to benefit from multitenancy and shared resources. As a result, efficiency arguments for using a public cloud become less compelling, and other factors such as control, security, and proprietary features may be the more dominant considerations. Commodity services are likely to be procured from a public cloud resulting in a hybrid structure. Future research may need to consider such a hybrid structure.

the adoption of cloud computing is likely to have other consequences for the It department. As more services are procured from cloud vendors, the need for func-tions within the It department that serve to administer, monitor, and maintain the It infrastructure will be considerably diminished or even eliminated. under cloud computing, the It department may need to increase the focus on adding value to the incoming cloud-based services. the mission of the It department would transition to determining the means by which the It personnel can ensure that enhancements to cloud-based services fit the current and future needs of the consuming units. the impact of such changes could be the subject of future research.

referenCes

1. Allen, B. Make information services pay its way. Harvard Business Review, 65, 1 (January–February, 1987), 57–63.

2. Armbrust, M.; Fox, A.; Griffith, r.; Joseph, A.D.; Katz, r.h.; Konwinski, A.; lee, G.; Patterson, D.A.; rabkin, A.; Stoica, I.; and Zaharia, M. Above the clouds: A Berkeley view of cloud computing. Department of Electrical Engineering and Computer Science, university of California, Berkeley, February 2009.

3. Armbrust, M.; Fox, A.; rean, G.; Joseph, A.D.; Katz, r.; Konwinski, A.; lee, G.; Pat-terson, D.; rabkin, A.; Ion, S.; and Zaharia, M. A view of cloud computing. Communications of the ACM, 53, 4 (2010), 50–58.

4. Banker, r.D.; Khosla, I.; and Sinha, K.K. Quality and competition. Management Science, 44, 9 (1998), 1179–1192.

Dow

nloa

ded

by [

Um

eå U

nive

rsity

Lib

rary

] at

23:

01 0

1 A

pril

2015

thE IMPACt OF ClOuD COMPutING 89

5. Bhargava, h.K., and Choudhary, V. Information goods and vertical differentiation. Journal of Management Information Systems, 18, 2 (Fall 2001), 89–106.

6. Cachon, G.P. Supply chain coordination with contracts. In A.G. de Kok, and S.C. Graves (eds.), Handbooks in Operations Research and Management Science, vol. 11. Amsterdam: North-holland, 2003, pp. 229–340.

7. Cachon, G.P., and lariviere, M.A. Supply chain coordination with revenue-sharing con-tracts: Strengths and limitations. Management Science, 51, 1 (2005), 30–44.

8. Choudhary, V. Comparison of software quality under perpetual licensing and software as a service. Journal of Management Information Systems, 24, 2 (Fall 2007), 141–165.

9. Columbus, l. roundup of cloud forecasts and market estimates. Cloudtech, 2012 (avail-able at www.cloudcomputing-news.net/blog-hub/2012/jan/18/roundup-of-cloud-computing-forecasts-and-market-estimates-2012).

10. Corbett, C.J.; Zhou, D.; and tang, C.S. Designing supply contracts: Contract type and information asymmetry. Management Science, 50, 4 (2004), 550–559.

11. Demirkan, h.; Cheng, h.K.; and Bandyopadhyay, S. Coordination strategies in an SaaS supply chain. Journal of Management Information Systems, 26, 4 (Spring 2010), 119–143.

12. Dewan, S. Pricing computer services under alternative control structures: tradeoffs and trends. Information Systems Research, 7, 3 (1996), 301–307.

13. Dewan, S., and Mendelson, h. user delay costs and internal pricing for a service facility. Management Science, 36, 12 (1990), 1502–1517.

14. Dixit, A. A model of duopoly suggesting a theory of entry barriers. Bell Journal of Eco-nomics, 10, 1 (Spring 1979), 20–32.

15. Dolan, r.J. Quantity discounts: Managerial issues and research opportunities. Marketing Science, 6, 1 (Winter 1987), 1–22.

16. Economides, N. Quality choice and vertical integration. International Journal of Industrial Organization, 17, 6 (1999), 903–914.

17. Gal-Or, E. Information sharing in oligopoly. Econometrica, 53, 2 (1985), 329–343.18. Gal-Or, E., and Ghose, A. the economic incentives for sharing security information.

Information Systems Research, 16, 2 (2005), 186–208.19. Gavirneni, S.; Kapuscinski, r.; and tayur, S. Value of information in capacitated supply

chains. Management Science, 45, 1 (1999), 16–24.20. Gordon, S. Benchmarking the information systems function. Working Paper Series 94-08,

Center for Information Management Studies (CIMS), Babson College, November 1994.21. Gurbaxani, V., and Kemerer, C.F. An agency theory view of the management of end-user

computing. Working Paper, Sloan School of Management, MIt, Cambridge, 1989.22. Gurbaxani, V., and Kemerer, C.F. An agent-theoretic perspective on the management of

information systems. In Proceedings of the 22nd Annual Hawaii International Conference on System Sciences. Kailua-Kona, hI: IEEE Computer Society Press, 1989, pp. 141–150.

23. IDC cloud research. International Data Corporation, Framingham, MA (available at www .idc.com/prodserv/idc_cloud.jsp).

24. Jensen, M.C., and Meckling, W.h. Divisional performance measurement. In M.C. Jensen (ed.), Foundations of Organizational Strategy. Cambridge: harvard university Press, 1998, pp. 345–361.

25. Knipp, E. Don’t bring a differentiated knife to a commodity gun fight. Gartner, Stamford, Ct, March 6, 2012 (available at http://blogs.gartner.com/eric-knipp/2012/03/06/dont-bring-a-differentiated-knife-to-a-commodity-gun-fight).

26. lee, h.l.; Padmanabhan, V.; and Whang, S. Information distortion in a supply chain: the bullwhip effect. Management Science, 43, 4 (1997), 546–558.

27. lee, h.l.; So, K.C.; and tang, C.S. 2000. the value of information sharing in a two-level supply chain. Management Science, 46, 5 (2000), 626–643.

28. Mell, P., and Grance, t. the NISt definition of cloud computing. Special Publica-tion 800-145, National Institute of Standards and technology, u.S. Department of Commerce, January 2011.

29. Mendelson, h. Pricing computer services: Queueing effects. Communications of the ACM, 28, 3 (1985), 312–321.

30. Pick, r.A., and Whinston, A.B. A computer charging mechanism for revealing user preferences within a large organization. Journal of Management Information Systems, 6, 1 (Summer 1989), 87–100.

Dow

nloa

ded

by [

Um

eå U

nive

rsity

Lib

rary

] at

23:

01 0

1 A

pril

2015

90 ChOuDhAry AND VIthAyAthIl

31. Sen, S.; raghu, t.S.; and Vinze, A. Demand information sharing in heterogeneous It service environments. Journal of Management Information Systems, 26, 4 (Spring 2010), 287–316.

32. Singh, N., and Vives, X. Price and quantity competition in a differentiated duopoly. Rand Journal of Economics, 15, 4 (Winter 1984), 546–554.

33. Spengler, J.J. Vertical integration and antitrust policy. Journal of Political Economy, 58, 4 (1950), 347–352.

34. Vives, X. Duopoly information equilibrium: Cournot and Bertrand. Journal of Economic Theory, 34, 1 (1984), 71–94.

35. Wang, E.t.G., and Barron, t. Controlling information system departments in the presence of cost information asymmetry. Information Systems Research, 6, 1 (1995), 24–50.

36. Whang, S. Alternative mechanisms of allocating computer resources under queuing delays. Information Systems Research, 1, 1 (1990), 71–88.

Dow

nloa

ded

by [

Um

eå U

nive

rsity

Lib

rary

] at

23:

01 0

1 A

pril

2015

thE IMPACt OF ClOuD COMPutING 91

Appendix

Proof of lemma 1

the firm is not perfeCtly informed of the demand parameter b and the cost parameter a. the firm estimates these parameters as b {, a[. these estimates are assumed to have an uniform error distribution U(b – ε, b + ε), U(a – ε, a + ε). Marginal cost and fixed cost of quality enhancement are

MCIT

= pC + b · (∆q /q

C ) (A1)

FCITQ

= a[ · (q2 – qC2). (A2)

the total surplus available for the consuming business unit when the firm sets It quality to be q*CC is obtained from integration of the inverse demand function as follows:

S

k q zdz k qI

CCCCk q

CC

CC

=+ ( ) −

= + ( )( )+ ( )

∫ˆ

ˆ / .

*ˆ

*

*β

αβ α

β

0

22

(A3)

the estimated benefit to the firm from It is the surplus in Equation (A3) minus the cost of It from Equations (A1) and (A2), as follows:

ˆ , ˆ

ˆ

*

*

B S x MC FC x k q

k q k

FCC

ICC

IT ITQCC CC

CC

= − ⋅ − = + ( )

=+ ( )( )

−+

β

β

α

2

2

ˆ̂ˆ ,

β θ∆ ∆∆ ∆

q q b q q c q

qa q q q

C C C

CC

+( )( ) + +( )( )− +( )

2

(A4)

where ∆q = (q*CC – qC). the firm’s problem is to maximize the expected benefit from It

expressed as E[BFCC] = E[S

ICC – (x · MC

IT + FC

ITQ)]. the expected benefit is computed

by integrating over the uniform probability density functions for b {, a[ and we have:

E B B d daFCC

fCC

a

a = ( )

−

+

−

+

∫1

2

1

2εβ

εβ ε

β ε

ε

ˆ ˆεε

αβ θ

αα β

∫

= + + +( )( ) − +( )( ) −+( )

−

kk q q b c q

k q q

qbk k qC C

C

CC

2

2∆

∆ (( ) + ( )

++( )

+( ) − +( )( )

a q

q q

qq b aq

C

C

CC C

2

22 2

63 6

∆α

β ε α β .

(A5)

Dow

nloa

ded

by [

Um

eå U

nive

rsity

Lib

rary

] at

23:

01 0

1 A

pril

2015

92 ChOuDhAry AND VIthAyAthIl

the problem statement and the first-order condition are as follows:

Max∆q

fCC

a

a

B d da( )

−

+

−

+

∫∫1

2

1

2εβ

εβ ε

β ε

ε

εˆ ˆ

++( ) +( )

− +( ) −

+ −( ) −

,

k q qa q q

bk

q

b c

CC

C

βα

β ε

α

β

∆∆

3

32

2 2

220

b q q

qqC

CC

ββθ

∆ +( )−

= .

(A6)

the optimal cost-center quality enhancement to offer is the solution to the first-order condition in Equation (A6) for (∆q), as follows:

∆qq k c q a b k q

aq b

CC C C C

C

* =−( ) + + −( ) −( )( ) − +( )

+(3 3 6 3

6

2β α ε β β αθ α α β

α β)) − +( )qC 3 2 2β ε.

(A7)

We also have q*CC = (∆q*CC + qC), which when substituted into Equation (A7) gener-

ates the optimal quality under the cost center as determined by the firm:

qb q k q c q k

aq b q

CC c C C

C C

* .=−( ) + +( ) −( )( )

+( ) − +( )3

6 3 2 2

α β β α θ

α β β ε

(A8)

Substitute Equation (A8) and optimal quality enhancement from Equation (A7) into the firm benefit expression (6), into the functional unit surplus expression (A3), and into the demand function x = (k + bq*CC). Simplifying and rearranging terms generates the additional results:

Bx

x c bq

qq q qF

CCCC

CCCC

CC

CCC

**

**

*=( )

− +

+

− ( ) − (

22

2αθ

∆ ))

= −

=( )

=+ +

2

2

2

6 3

,

,

* *

**

*

∆q q q

Sx

xak q b

CC CCC

ICC

CC

CC C

αα αβ βk qq q k c q

aq b q

C C C

C C

( ) − + +( )( )+( ) − +( )

ε αβ θ

α β β ε

2 2

2 2

3

6 3.

(A9)

Concavity condition for an interior solution: the second derivative of the objective function (A6) is

6 3

3

2 2α β β ε

α

aq b q

q

C C

C

+( ) − +( ).

(A10)

Concavity requires that the determinant (A10) is negative. this in turn requires that the numerator (6a(aq

C + bb) – q

C(3b2q