Embed Size (px)

Citation preview

Church FinanceSEMINAR

BY MAY HER(MAIV)

Bible A. Pay Taxes, Romans 13:1-7

Must pay Taxes, Romans 13: 6, 7 This is also why you pay taxes, for the authorities are God’s servants, who give their full time to governing. Give everyone that you owe him; if you owe taxes, pay taxes, ….

B. Avoid criticism, 2 Corinthians 8:20-21

“We want to avoid any criticism of the way we administer this liberal gift. For we are taking pains to do what is right not only in the eyes of the Lord but also the eyes of men.”

Albert Einstein says, The hardest thing in the world to understand is the income tax.

***Very tough Job, but don’t worry***Ephesians 1: 19-20 and his incomparably great power

for us who believe. That power is like the working of his mighty strength, which he exerted in Christ when he raised him from the dead and seated him at his right hand in the heavenly realms.

THE COMMON ERRORS OF CHURCHCommon error

1. Make payroll without an employer identification number.

2. The board allows the treasurer full authority to determination of Minister Status (W-2 or 1099).

3. Treating the Minister as an employee for social security purpose.

Correct procedure

New church must apply for an employer identification number from IRS before they can make any payment to a employee or contractor, by using the Form SS-4 from IRS office.

The board should use IRS form SS-8 to determination your Minister work Status.

Minister are always self-employed for social security purposes with respect to ministerial services. The Board designates a housing allowance and reimbursement for the Minister at the beginning of the year.

THE COMMON ERRORS OF CHURCHCommon error

4. Withholding taxes from Minister pay without authorization.

5. Not filing 941 or 944 forms

6. Not issuing W-2 or 1099MISC form.

7. Not retaining any church record.

Correct procedure

Minister is exempt from income tax withholding whether they report their income taxes as employees or self-employed; Minister who report their income taxes as an employee can request voluntary withholding by submitting a Form W-4 to the church.

Those forms must be filed quarterly or annually by a church with an employee.

A W-2 must be issued to each employee; and a 1099-MISC must be issued to each none employee (who received compensation of at least $600 during the year).

Follow the Finance Manual for Alliance Church Treasurers (and pastors) APPENDIX E. “Record Retention Periods.”

THE COMMON ERRORS OF CHURCH

Common error

8. Not complying with payroll tax deposit requirements.

9. Reimburse unaccountable to the minister and not report.

Correct procedure

The church must deposit the taxes it withholds.

The church has to deposits these taxes by the 15th of the following month with a qualified financial institution (along with a Form 8109).

Set an Accountable Reimbursement Plan for Minister.

Hmong Alliance Church of The Christian and Missionary Alliance

Hmong Alliance Church of The C&MA

May Her

P.O. Box 7

Denver, Colorado 12345

Adams

May Her 84-1234567

2284

1234 Main St.

January 1, 1984

Denver, Colorado 12345

Moob Xwbfwb 123 45 6789

7777 Forgiven Rd

Denver, CO 12345

Hmong Alliance Church 1234 Main St. Denver, CO 12345 84 1234567

1

2

3

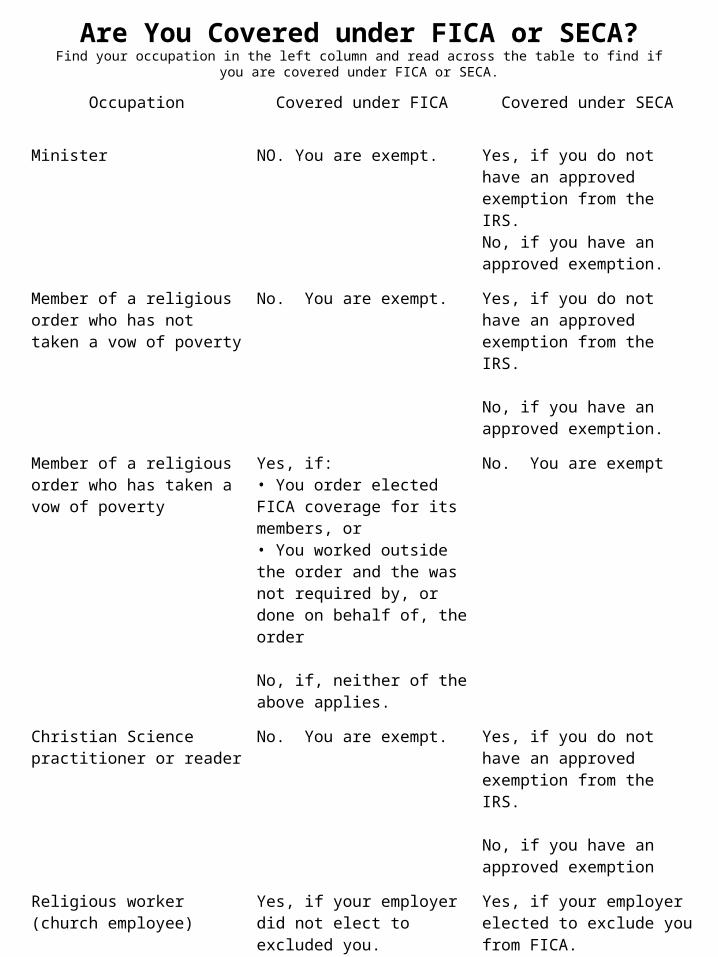

Social security and Medicare taxes are collected under two systems. Under the Self-Employment Contributions Act (SECA), the self-employed person pays all the taxes. Under the Federal Insurance Contributions Act (FICA), the em- ployee and the employer each pay half of the taxes. No earnings are subject to both systems.

• If you are an employee of a church or church organization that makes Election to Exclude Their Employees From FICA Coverage and pay you $108.28 or more in wages during the tax year, you must pay SE tax on those wage. (Publication 517, 2009) p.4

Are You Covered under FICA or SECA?Find your occupation in the left column and read across the table to find if you are covered under FICA or SECA.

Occupation Covered under FICA Covered under SECA

Minister NO. You are exempt. Yes, if you do not have an approved exemption from the IRS.No, if you have an approved exemption.

Member of a religious order who has not taken a vow of poverty

No. You are exempt. Yes, if you do not have an approved exemption from the IRS.

No, if you have an approved exemption.

Member of a religious order who has taken a vow of poverty

Yes, if:• You order elected FICA coverage for its members, or• You worked outside the order and the was not required by, or done on behalf of, the order

No, if, neither of the above applies.

No. You are exempt

Christian Science practitioner or reader

No. You are exempt. Yes, if you do not have an approved exemption from the IRS.

No, if you have an approved exemption

Religious worker (church employee)

Yes, if your employer did not elect to excluded you.

No, if your employer elected to excluded you.

Yes, if your employer elected to exclude you from FICA.

No, if you are under FICA

Member of a recognized religious sect.

Yes, if you are an employee and do not have an approved exemption from IRS.

No, if you have an approved exemption.

Yes, if you are self-employed and do not have an approved exemption from the IRS

No, if you have an approved exemption

Housing Allowance Expense Form For Clergy

Minister are permitted to exclude from their church income for federal income tax purposes a "housing allowance" designated by their employing church, to the extent that the allowance is used to pay housing expenses. To assist the HMONG DISTRICT in designating an appropriate amount, please estimate on this form the housing expenses you expect to pay next year, and then return to the finance officer of the Hmong District.

CATEGORY ESTIMATED AMOUNT

OF EXPENSE FOR 2010

1. Mortgage or Rental Payment_____________________

2. Utilities (electricity, gas water, trash pickup Local telephone charge)_____________________

3. Furnishings and Appliance (purchase and repair)___________________

4. Structural Repairs and Remodeling___________________

5. Yard Maintenance and Improvements___________________

6. Maintenance Items ( household cleansers, light bulbs, Pest control, etc... )

___________________7. Miscellaneous

_____________________

Total Estimated Expenses for 2010_________________

The above listed expenses represent a reasonable estimate of my housing expenses for next year.I understand and agree that:

The Hmong District will not designate a portion of my compensation as housing allowance until I complete

and return this form. Retroactive designations of housing allowances are not legally effective.

It is my responsibility to notify the Hmong District in the event that these estimates prove to be materially

inaccurate during the year.

My housing allowance exclusion is an exclusion for federal income taxes only. I must add

my housing allowance as income in reporting my self-employment taxes on Schedule SE

(unless I am exempt from self-employment taxes).

_______________________________________________

Signature of Minister Date

I attest that I received this form from the aboveminister on____________________, 2010

_____________________________________________________

Signature of DS Date

Amounts included in gross income. To figure your earnings from self-employment (on Schedule SE)

1. Salaries and fees for your qualified services,

2. Offerings you receive fro marriages, baptisms, funerals, messes, etc.

3. The value of meals and lodging provided to you, your spouse, and your dependents for your employer’s convenience,

4. The fair rental value of a parsonage provided to you (including the cost of utilities that are furnished) and the rental allowance (including an amount for payment of utilities) paid to you, and

5. Any amount a church pays toward your income tax or SE tax, other than withholding the amount from your salary. This amount also subject to income tax

Church Staff/Employee Compensation

• Compensation Package Examples:1. Clergy, Rev. Moob Xwbfwb

Salary:Base Salary …………………………… $20,000Housing Allowance………………. $10,000Reimbursement Allowance……… $5,500Employer Social Security Grant … $5,000Total………………………………….. ……. $40,500

Benefits:Heath/Dental Insurance …………. $5,000Total Package Value…………………. $45,500

2. Non-Clergy, Paaj SecretarySalary:Base Salary ……………………… …….. $12,100

Benefits:Heath/Dental Insurance …………. …… $2,500Total Package Value…………….. ….. $14,600

Reporting to Tax Authorities

Quarterly Reports

A. Form 941 Work-Sheet for Form 941

Base Salary for Rev. Moob, Xwbfwb $20,000Church Social Security Grant $5,000

Total………………$25,000 / 4 = $6,250

Base Salary for Paaj Secretary … ..$12,100 / 4 = $3,025

Then $6,250 + $3,025 = $9,275The $9,275 will be appear on Form 941 line 2

B. Form W-3 Work-Sheet for Form 941

Total of Rev. Moob, Xwbfwb $25,000 Total for Paaj Secretary…………………… $12,100

Totals………………………… $37,100

Then $37,100 will be appear on Form W-3 box 1

How to set up an Accountable Reimbursement Plan

The Church must have:1. The payment of expense must be for ordinary and necessary

expenses for job performance.2. There must be a written policy or plan.3. The employer (Church) must allocate expense fund that are

distinct from personal compensation.4. The employee (Minister must account for expenses in a

timely and proper manner.

The reporting system should require the pastor to submit written records and receipts that detail each expenditure.

These should include:5. The date6. The type of expense7. To whom it was paid8. The business or ministry purpose

If expenses exceed the amount allowance for reimbursement plan may not be paid or reimbursed by salary reduction. For example, if $5,500 is budgeted for the year but the minister actually spends $6,000 by year end, the extra $500 cannot be treated as a reimbursement by simply reducing the minister’s $500.

8 4 1 2 3 4 5 6 7

Hmong Alliance Church

1234 Main St.

DenverCO 12345

8 4 1 2 3 4 5 6 7

Hmong Alliance Church of the C&MA

1234 Main St

Denver, CO 12345

2

3,025 00

3,025 00

375 10

450 732,450 73

2,000 00

2,450 73

2,450 73

2,450 73

9,275 00

75 63

X

Hmong Treasurer

TreasurerSignature Goes Here

Pastor

123-45-6789

84-1234567

Hmong Alliance Church of the C&MA1234 Main StDenver, CO 12345

Rev. Moob Xwbfwb

7777 Forgiven Rd.Denver, CO 12345

Ordained – Not included above10,000 Housing Allowance

6,000

CO

25,000

22-123456789 25,000 0

X 403b

Secretary

222-33-4455

84-1234567

Hmong Alliance Church of the C&MA1234 Main StDenver, CO 12345

Paaj Secretary

7777 Forgiven Rd.Denver, CO 12345

12,100

12,100

2,000

750.00

175.46

CO

12,100

22-123456789 12,100 265.00

37,100

12,100

8,000

750.00

175.462 2

84-1234567

Hmong Alliance Church of the C&MA

1234 Main StDenver, CO 12345

CO 22-123456789 12,100 265.00

12,100

Hmong Treasure 303 123-4567

Hmong Alliance Church of C&MA1234 Main StDenver, CO 12345

100.00

100.00

100.00

100.00

100.00

100.00

100.00 100.00

100.00 100.00

100.00 100.00

84-1234567

100.00 100.00 100.00

Joe A. Smith

7777 Forgiven Rd

Denver, CO 12345