Embed Size (px)

DESCRIPTION

It's Chartered Institute of Management Accountants Course: C-01 Fundamentals of Management Accounting ,Class LSBF Manchester ,Q's By Sir Ian Wilson.

Citation preview

Fundamentals Of Management Accounting

Cost Bookkeeping

Fundamentals Of Management Accounting

Class Slides – Ian Wilson

� Your syllabus included the following:

� Explain the principles of Manufacturing Accounts & the integration of the Cost Accounts with the Financial Accounting System.

� Prepare a set of ‘Integrated Accounts’, showing Standard Cost Variances.

� There is NO statutory requirement to keep detailed ‘costing’ records.

� Many smaller companies will not bother, instead relying on ‘Financial’ records.

� In a larger, more complex business however, cost accounting records are vital to monitor and control what is taking place.

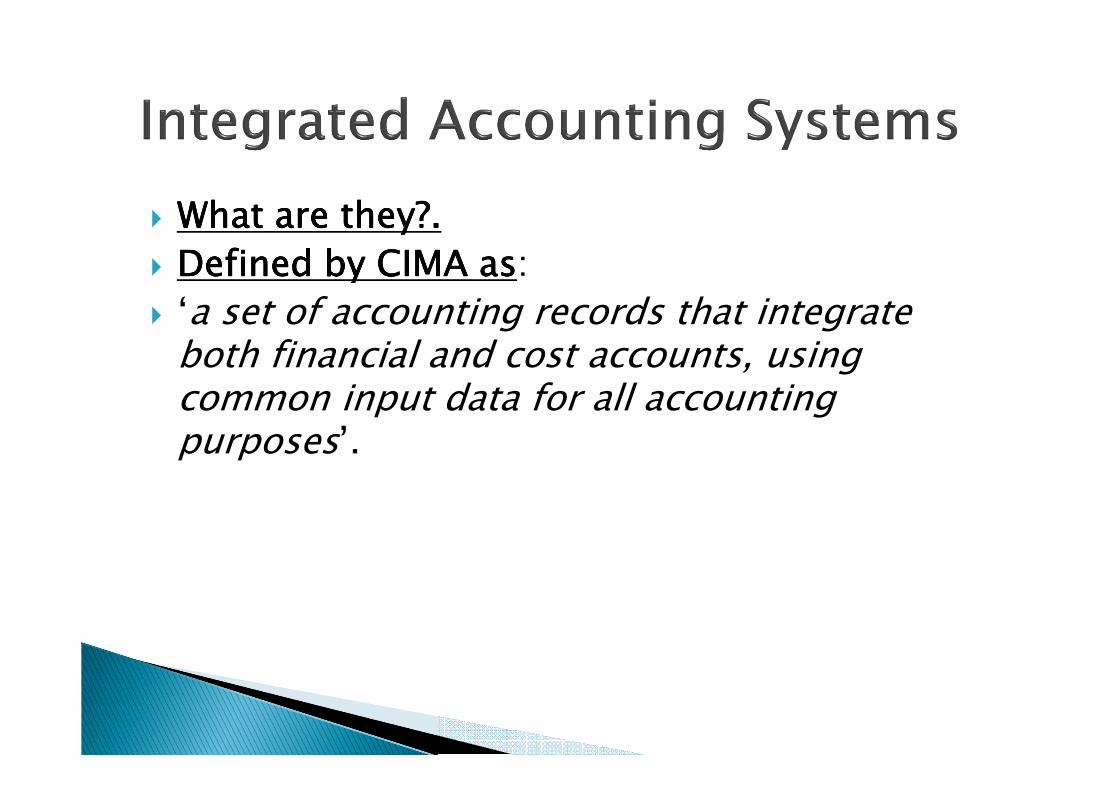

� What are they?.What are they?.What are they?.What are they?.

� Defined by CIMA asDefined by CIMA asDefined by CIMA asDefined by CIMA as:

� ‘a set of accounting records that integrate both financial and cost accounts, using common input data for all accounting purposes’.

� Principal accounts in an integrated system:

� 4 areas to deal with:

1. Resources Accounts – Materials/Wages etc

2. Cost of Production Accounts – costs from start to end of manufacture, Stock, Labour, WIP/Finished Goods/Cost of Sales

3. Sales Accounts – for invoicing customers

4. Income Statement – summary of Profit/Loss

� Simple RulesSimple RulesSimple RulesSimple Rules:

� A Flow into the Account is shown on the DEBIT side:

� A Flow out of the Account is shown on the CREDIT side:

� Both are Held in a ‘T’ Account:

� Obviously at the end of a period the account needs to be ‘balanced off’.

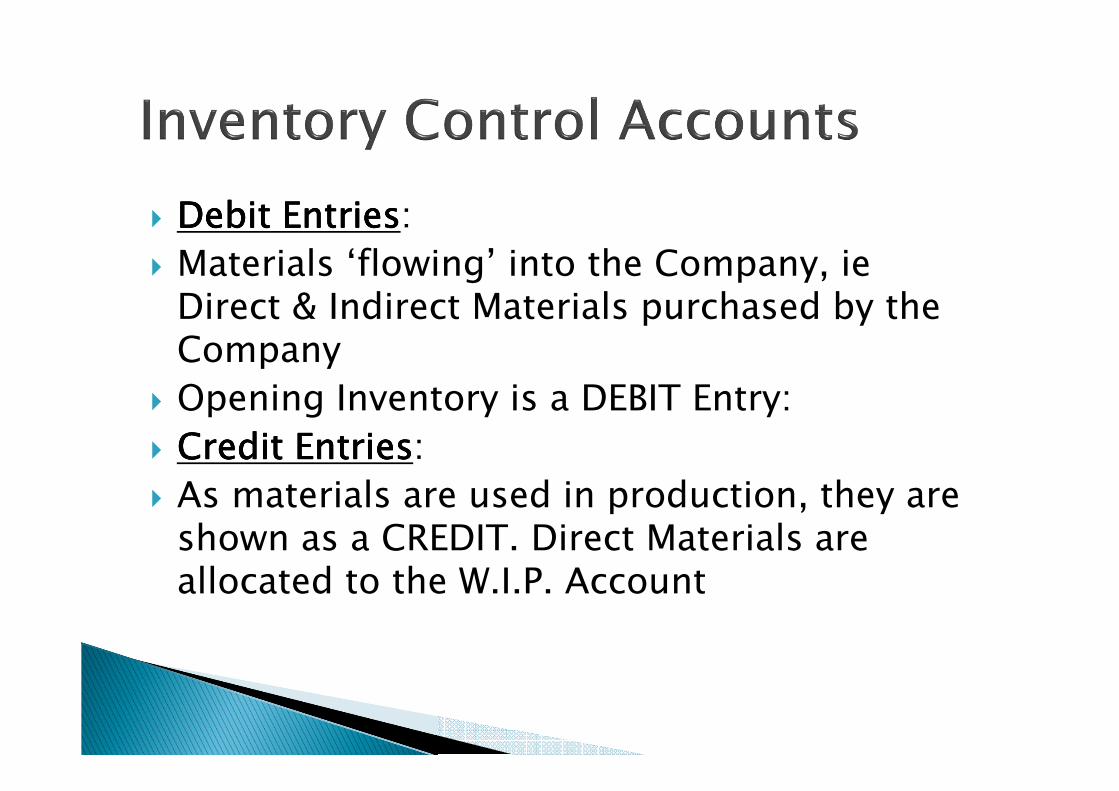

� Debit EntriesDebit EntriesDebit EntriesDebit Entries:

� Materials ‘flowing’ into the Company, ieDirect & Indirect Materials purchased by the Company

� Opening Inventory is a DEBIT Entry:

� Credit EntriesCredit EntriesCredit EntriesCredit Entries:

� As materials are used in production, they are shown as a CREDIT. Direct Materials are allocated to the W.I.P. Account

� Credit EntriesCredit EntriesCredit EntriesCredit Entries:

� Indirect Materials are allocated to the Production Overhead Account

� Closing Inventory values are the balancing figure on the Credit side of the ‘T’ account.

� No Opening or Closing Stock hereNo Opening or Closing Stock hereNo Opening or Closing Stock hereNo Opening or Closing Stock here!

� Debit EntriesDebit EntriesDebit EntriesDebit Entries:

� Reflect wages paid out to staff/operatives

� Credit EntriesCredit EntriesCredit EntriesCredit Entries:

� Wages split into Direct & Indirect Labour costs

� Debit EntriesDebit EntriesDebit EntriesDebit Entries:

� Costs associated with producing Units of output are built up on the debit side, likely to be Materials, Labour & Production Overheads

� Credit EntriesCredit EntriesCredit EntriesCredit Entries:

� This is the cost build up on the Debit side, shown on the Credit side as an output to Finished Goods

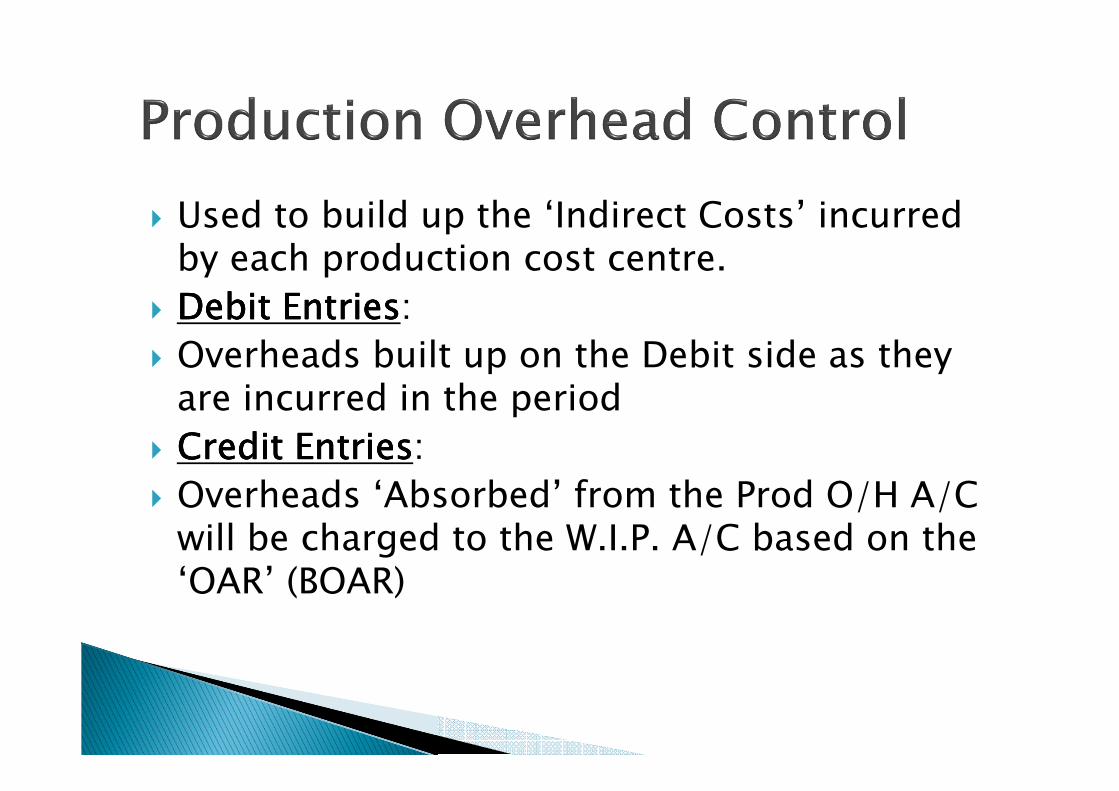

� Used to build up the ‘Indirect Costs’ incurred by each production cost centre.

� Debit EntriesDebit EntriesDebit EntriesDebit Entries:

� Overheads built up on the Debit side as they are incurred in the period

� Credit EntriesCredit EntriesCredit EntriesCredit Entries:

� Overheads ‘Absorbed’ from the Prod O/H A/C will be charged to the W.I.P. A/C based on the ‘OAR’ (BOAR)

� As we saw earlier, we may OVER or UNDER ‘Absorb’ Overheads.

� UNDER ABSORPTION – shown on CREDIT side of Production Overhead A/C – balancing figure

� OVER ABSORPTION – shown on DEBIT side of Production Overhead A/C – balancing figure

� The ‘other’ side of the Under/Over Absorption entry is in the P/L A/C

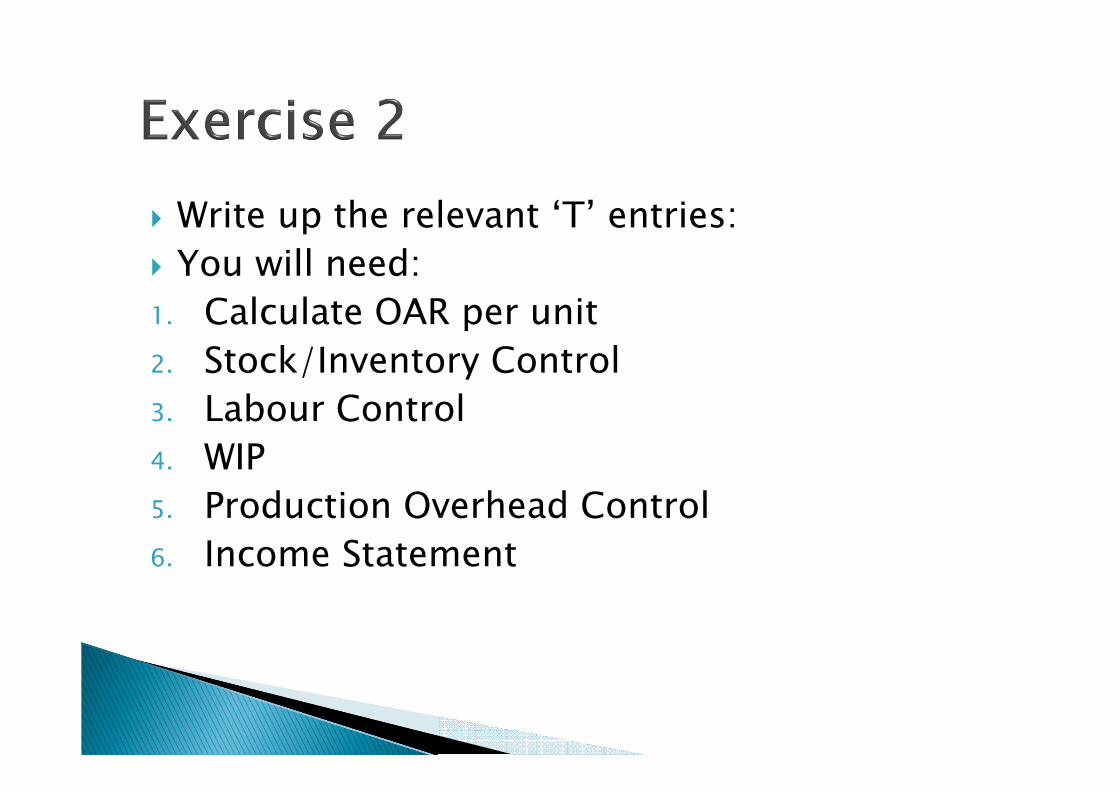

� Write up the relevant ‘T’ entries:

� You will need:

1. Calculate OAR per unit

2. Stock/Inventory Control

3. Labour Control

4. WIP

5. Production Overhead Control

6. Income Statement

� Write up the relevant ‘T’ entries:

� You will need:

1. Calculate OAR per unit

2. Stock/Inventory Control

3. Labour Control

4. WIP

5. Production Overhead Control

6. Income Statement

� In the last session we covered Standard Costing, remember:

� What is a VarianceWhat is a VarianceWhat is a VarianceWhat is a Variance?.

� ‘Difference between a planned, budgeted or standard cost and the actual cost incurred. The same comparison can be made for revenues’.

� The analysis of these ‘differences’ is called VARIANCE ANALYSIS.

� Types of VariancesTypes of VariancesTypes of VariancesTypes of Variances:

� FAVOURABLE VARIANCES: when actual results are better than expected, producing higher profits.

� ADVERSE VARIANCES: when actual results are worse than expected, producing lower than planned profits

� If a company uses ‘Standard Costing’ systems, account has to be taken of the VARIANCES that occur:

� Variances should be recorded in the account in which they first appear:

Variance:Variance:Variance:Variance: Account recorded in:Account recorded in:Account recorded in:Account recorded in:

Material Price Variance Stores/Materials Control

Labour Rate Variance Wages Control

Materials Usage Variance Work in Progress

Labour Efficiency variance Work in Progress

Idle Time Variance Work in Progress

Total Overhead Variance Overhead Control

� Variance Control Account (VCA)Variance Control Account (VCA)Variance Control Account (VCA)Variance Control Account (VCA):

� The other side of the entry will appear in the ‘Variance Control Account’

� An ADVERSE variance is a DEBIT in the VCA

� A FAVOURABLE variance is a CREDIT in the VCA

� Lets try this example:

� Materials & Overhead costs are given:

� You have specific details for the Labour costs including rate & efficiency variances

� This will test you relating to Materials with some Labour Variances thrown in.

� Advantages of integrationAdvantages of integrationAdvantages of integrationAdvantages of integration:

1. No duplication of effort

2. No need to reconcile financial & cost accounts

3. Simplicity

Exam: you will be presented with T accounts on screen with ‘missing’ entries.

You will have to complete the accounts.

![CIMA C1 Unit 8 2012 [Read-Only]](https://img.pdfslide.net/doc/110x75/563db87c550346aa9a942542/cima-c1-unit-8-2012-read-only.jpg)