Embed Size (px)

Citation preview

Justin Atwater, Meg Bartley, Mark Elghossain, Lindsey Herrala, Jake Seraphin

TAKINGOVER

Overview of Circuit City

Circuit City was an American multinational consumer electronics corporation. It was founded in 1949 and

pioneered the electronics superstore format in the 1970s.

Past Mission and Vision

"To make sure that we are all working in the same direction, each of us must live and breathe Circuit City's values and use them as a guidepost for our

actions and decisions." (2009)

Corporate Values:

Respect, Teach, Engage, Simplify, Maintain the Highest Integrity

Description of Key Competitors (2000)Superstores

ex. Best Buy

Description of Key Competitors (2000)Convenience Stores

ex. Radio Shack

Description of Key Competitors (2000)

Online Stores

ex. eBay

What Went Right: Circuit City’s Success In the beginning Circuit City displayed…

●Strong management

●Affordable prices and customer service orientation

●Good merchandising, capitalizing on innovative consumer products

Timeline- The Decline

1985 → CEO Alan Wurtzel (son of founder Sam Wurtzel), who led the company into an era of expansion during the 1970s, steps down

1993 → Circuit City introduces its first CarMax (bringing “big-box retailing” to used-car sales)

1995 → Circuit City enters the Fortune 500 at number 280

1998 → unsuccessful launch of DIVX, a new DVD technology (abandoned within year) ***Wurtzel: “costly but not critically wounding”

Timeline - The Downfall

2000 → Earnings and stock price have peaked with 615 stores, but Best Buy’s earnings and market share are higher, and their stores are more profitable

→ To reduce costs in warehouse storage and delivery, CEO Alan McCollough exits the appliance market (accounted for 14 percent of sales)

→ Store remodeling and restructuring program (all stores 20-30k sq. ft.)

2002 → Spin off of approximately 50 CarMax stores (over 120 today) → Best Buy introduces Geek Squad, quickly becoming the top

electronics service org.

2003 → “Bloody Wednesday” - Circuit City lays off 3,900 of it’s highest-paid commissioned sales force (previously seen as a differentiator/competitive adv.) By 2003, Best Buy has 10x the market cap. of Circuit City, and by 2004 has aggressively pursued/secured better “A” quality locations and real estate

Timeline - The End

2006 → Circuit City launches Firedog, offering tech. support and installation services

2007 → New CEO Philip Schoonover fires 3,400 of the company’s most knowledgeable, tenured, and highly compensated employees (while executives received bonuses) ***Circuit City engages in a $1 billion share buy-back from 2003-2007

2008 → 155 stores close and 17% of the workforce is laid off. One week later, Circuit City files for bankruptcy. After no success finding a suitable buyer, the company is forced to liquidate in January 2009.

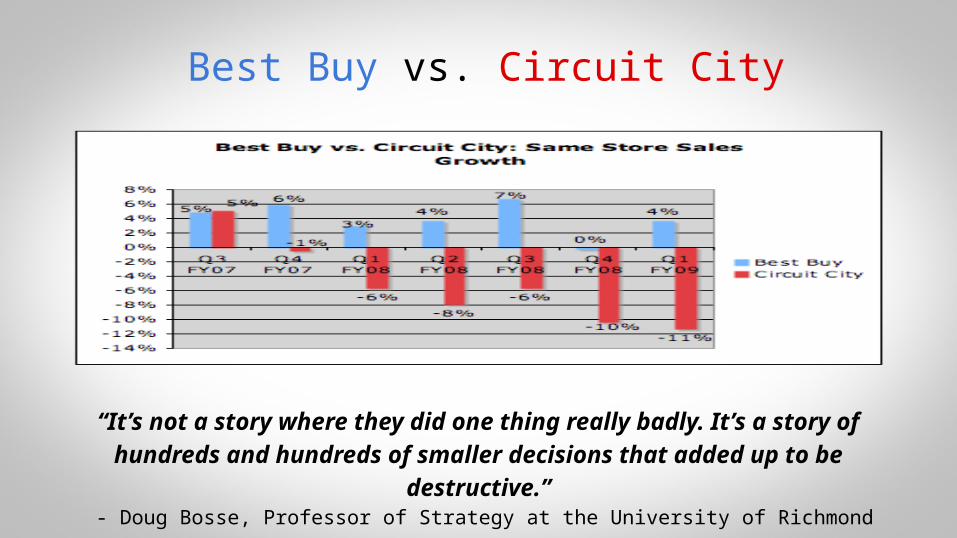

“It’s not a story where they did one thing really badly. It’s a story of hundreds and hundreds of smaller decisions that

added up to be destructive.” - Doug Bosse, Professor of Strategy at the University of Richmond

Best Buy vs. Circuit City

What Went Wrong: Circuit City’s DemiseIn the end Circuit City displayed...● Incompetent Management

○ Circuit City’s ventures with CarMax and DivX distracts from core business

○ Twice management laid off approximately 3500 of the company’s most knowledgeable and highly compensated employees

○ No cash reserves in ‘07 after 75% stock price decline during buy-back ○ Complacency

■ “We thought we were smarter than anybody.” - Alan Wurtzel■ Didn’t adapt to changing consumer preference towards

salespeople & high-margin products● Failure to adhere to their mission statement, values, and

operational philosophy

Taking Over

In 2000

How can we change it?

Agenda: Key Activities

LocationStore LayoutsStaffing ChangesOnline Presence

Competitive PositionTarget MarketMoving Forward

6

Proposed Changes: Location

Liquidate low profit superstores in an effort to reduce costs

As of 2000, Circuit city operates 573 Superstores and 45 smaller “Satellite” stores

Turn some into warehouses for:

Online retail inventory

Satellite store inventory

Secure prime real estate for Satellite stores

Cities, metropolitan areas, high foot traffic (malls, shopping centers)

Satellite stores within an hour from a Superstore

●Transfer superior employees from closing locations to remaining Superstores or new Satellite stores

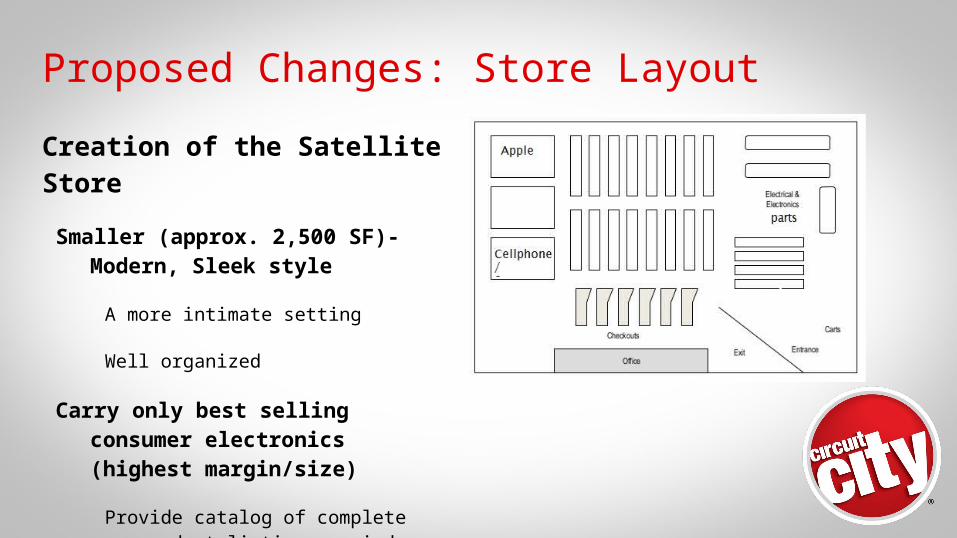

Proposed Changes: Store LayoutCreation of the Satellite StoreSmaller (approx. 2,500 SF)-

Modern, Sleek style

A more intimate setting

Well organized

Carry only best selling consumer electronics (highest margin/size)

Provide catalog of complete product listing carried exclusively at Superstores

Allow customers to order product and pick up at store (free) or do home delivery (fee)

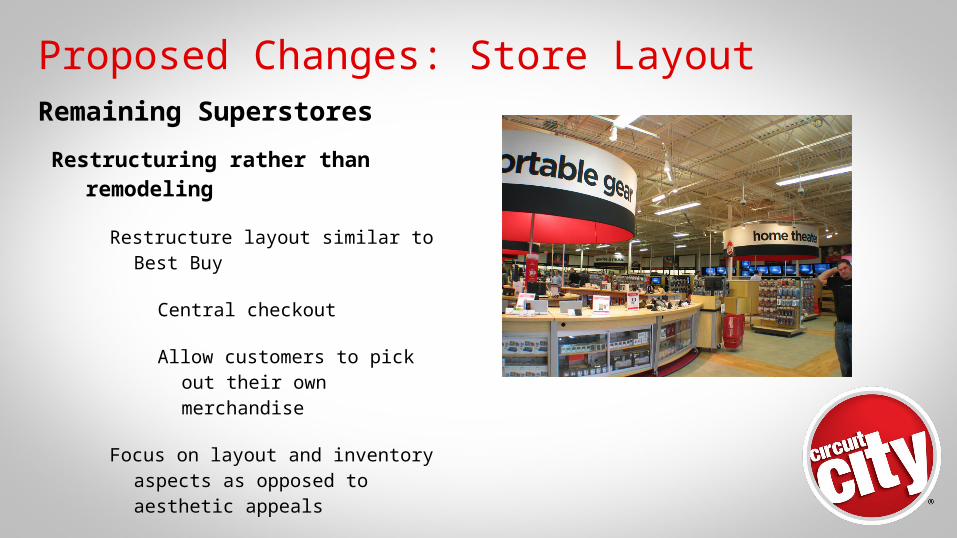

Proposed Changes: Store LayoutRemaining SuperstoresRestructuring rather than

remodeling

Restructure layout similar to Best Buy

Central checkout

Allow customers to pick out their own merchandise

Focus on layout and inventory aspects as opposed to aesthetic appeals

Superstores will take on more inventory management/storage capabilities as unprofitable stores are sold

Carry full inventory of consumer electronics and home appliances

Proposed Changes: StaffingFrom Commission to Salary Based

Employees will be more inclined to provide valuable customer service rather than just pushing products in order to make commission

Downsize sales force to retain only elite talent

Implement Self-Service StyleChanging consumer trends → consumers becoming more independent and

less in need of staff assistance

Emphasize Importance of Product and Industry KnowledgeMaintain a reputation of superior customer service, available upon request

Proposed Changes: OnlineProvide catalogs in

Satellite stores

To push online sales (for products not available in these stores)

Offer shipping to large Superstores to pick up for free or delivered to homes for a fee

Investigate the potential for online sales

To supplement to traditional avenues

Possibly generate revenues from Web advertising

New Competitive Position“Highest quality goods at a convenient location for a bargain

price”

Value Propositions Affordable PricesDesirable Products Exceptional Customer ServiceSuperior Industry and Product Knowledge

Key Resources● Strong relationships with suppliers to obtain low prices and quality products● Fewer, highly-trained employees; expertise● Satellite and Superstores

Cost StructureCost leadership

New Target Market Customer Segments

● Mass○ Young tech enthusiast (16 - 29)

■ Shopping for utility○ Suburban soccer mom (30 - 50)

■ Shopping for family○ Wealthy businessman (34 - 54)

■ Shopping for status

Main Target Market → Young Tech Enthusiasts (16 - 29)

Moving Forward From 2000Market Risks

Becoming negligent of competitive and market forces

○ Falling behind changing product and consumer trends●Market Research

○ Adjusting focus to external environment

○ Gaining insight on market trends and consumer demands:

■ Innovations: Apple, Microsoft, Gaming Systems, High Performance PCs, Tablets, etc.

■ Considering future product obsolescence (ie VHS, pagers, tapes, etc)

■ Residential real estate market outlook and its potential effect on appliance sales

■ Commercial real estate market outlook and its potential effect on establishing a larger satellite store footprint

Financial DataAssumptions: Operational efficiencies will be obtained as Circuit City transitions from Superstores to Satellite stores.

Current Costs of Goods Sold as a percentage of revenue is 77%. We estimate that the COGS as a percentage of revenue from Satellites will

be reduced to 70%. We also assume total expenses (S,G,&A + int. exp.) being 20% of revenue

for Superstores, would be 18% for Satellites.

8,359,428,000 COGS in the year 2000 / 618 stores = 13,526,582.52 / 15,000 avg. SF/store $901.77 Avg. COGS/ SF/store

We used an avg. SF times avg. COGS/SF/store to calculate the estimated COGS for each store:25,000 SF: $22.2 million COGS for Superstores

2,500 SF: $2.2 million COGS for Satellites

Financial Data Contd.We used the COGS times our numeric for COGS as a % of revenue to calculate avg. revenue per

store: $28.9 million Avg. Revenue from Superstores

$3.2 million Avg. Revenue from Satellites

We subtracted the COGS from the avg. revenue to get avg. ann. gross profit for each store:$6.3 million Avg. Ann. Gross Profit from Superstores$966 thousand Avg. Ann. Gross Profit from Satellites

Finally we multiplied the (S,G&A+int.exp.) by avg. ann. gross profit to get the avg. ann. net income for each store:

$5.1 million Avg. Ann. Net Inc. from Superstores$792 thousand Avg. Ann. Net Inc. from Satellites

Financial Data Contd. $5,085,911.66 Avg. Ann. Net Inc. from Superstores / $28,901,693.77 avg. Revenue from Superstores = 17.59% margin$792,271.26 Avg. Ann. Net Inc. from Superstores / $3,220,614.88 avg. Revenue from Satellites = 24.59% margin

● As of 2000, Circuit City operated 617 stores. Of those stores, 45 (7%) fit the description of our proposed Satellite stores, and the remaining 572 (93%) loosely fit the company’s Superstore profile

(17.59% Superstores marginX.93) + (24.59% Satellites marginX.07) = Weighted Average Profit Margin for 2000 = 18.08% margin

● Assuming a 7.5% reallocation towards Satellite stores and away from Superstores for the next 3 years…○ (17.59% X .855) + (24.59% X .145) = 18.61% margin in 2001○ (17.59% X .78) + (24.59% X .22) = 19.13% margin in 2002○ (17.59% X .705) + (24.59% X .295) = 19.67% margin in 2003

■ 19.67% P.M. in 2003 - 18.08% profit margin in 2000 = 1.59% increase in profit margin from 2000 to 2003 (an increase in efficiency), resulting from the transition of Superstores to Satellite stores

Questions?