Embed Size (px)

Citation preview

GSA Federal Supply Service

Citibank Presents:

Techniques to Grow Your Program

2004 Citibank® Commercial Cards, Government Services

The Sixth Annual GSA SmartPay® ConferenceSHERATON CONFERENCE CENTER, NEW ORLEANS, LOUISIANA, AUGUST 24-26, 2004

Citibank Presents:Techniques toGrow Your ProgramPatti WallsAugust 26, 2004

Citigroup® Global Transaction ServicesCopyright © 2004 Citibank, N.A. CITIBANK, CITIDIRECT, CITIGROUP and the Umbrella Device are registered service marks of Citicorp or its affiliates.

3

Goal & Objectives

Discover new ways to grow your existing card program

Find out about new areas of use, interchange, merchant acceptance and large-ticket purchases

4

Agenda

Evolution of the Purchase Card

Program Growth – Then and Now

Purchase Card Goals

Summary

5

Evolution of the Purchase Card

Government that works better and costs less– Presidential Executive Order 12352, March 1982– Government chose Purchase Card, 1989– 1993 National Performance Review

Why Purchase Card?– Streamline the purchase order process for micro-purchases– Replace petty cash or impress funds– Provide a better audit tool– Reduce resources

Traditionally used to purchase high-volume, low dollar transactions

– Maintenance, repairs, office supplies (MROs)– Services (training / education, technical)– Operations (under $2,500)

6

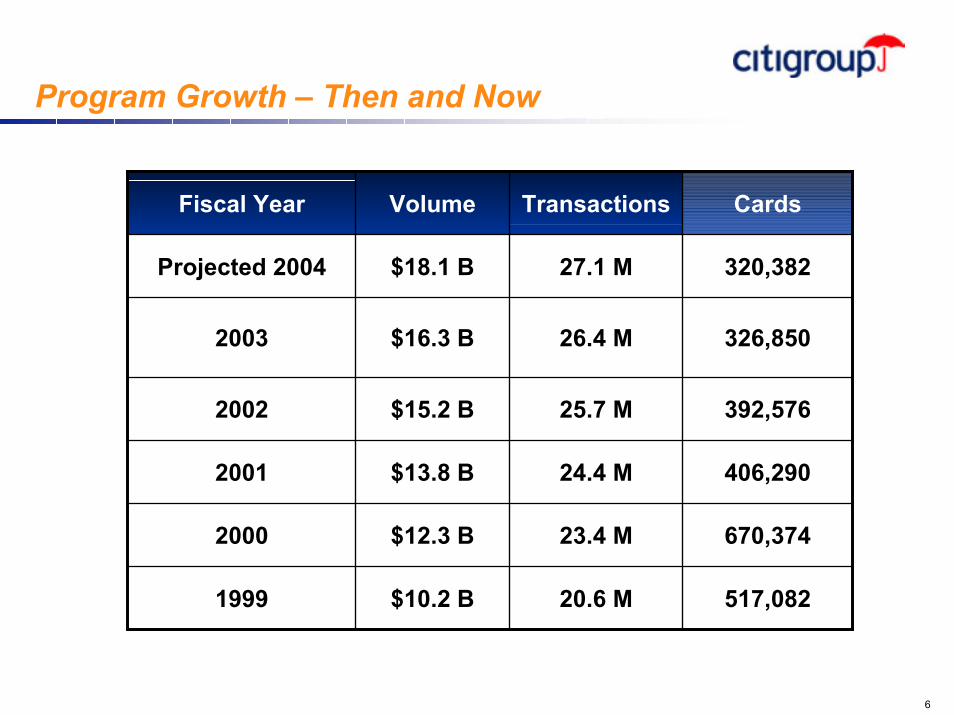

Program Growth – Then and Now

CardsTransactionsVolumeFiscal Year

320,38227.1 M$18.1 BProjected 2004

517,08220.6 M$10.2 B1999

670,37423.4 M$12.3 B2000

406,29024.4 M$13.8 B2001

392,57625.7 M$15.2 B2002

326,85026.4 M$16.3 B2003

7

Program Growth – Then and Now (continued)

Efficiencies and accomplishments

Employee empowerment– Faster ordering and receipt of goods / services– Elimination of pre-validation processes

Resource availability– Report generators– Common metrics

Transaction cost savings $1,830,576,000 / projected 2004– $69.34 x number of transactions / year

Rebates earned $70,613,385– Purchase card approximately $47M

8

Program Growth – Then and Now (continued)

Independent conclusions

1997 Army Audit Agency survey found: – DOD on average would save $92 per transaction using the

credit card versus the purchase order

– They also found that they saved 4 hours in processing time per transaction when using a credit card

In addition, they cited this independent review:– Ten Federal civilian agencies cited reduced administrative expenses

of $53.77 per transaction when buyers used a credit card instead of the old purchase order system

9

Program Growth – Then and Now (continued)

Independent conclusions

2003 Purchasing Card Benchmark Survey, Palmer & Gupta – The average administrative cost of procuring and paying for a good or

service via the purchase-order process is about $91, while the average cost with their purchasing card transaction is estimated to be about $21 - a net savings attributable to purchasing card use of $70 per transaction

– Estimated 8.3 days in time savings in card cycle versus procurement cycle

Importance is always relative– “Internal cost savings were 37 times greater than rebates received.”

10

Purchase Card Goals

As old goals have been obtained and efficiencies have been realized, the government is searching for new efficiencies

Simple Consolidated

PaymentControls, Reporting,Interfaces

e-ProcurementInterfaces &Functionality

AdvancedMIS Reporting

& Enhanced Data

ClientNeed

PaymentFunctionality

Redesigned Process

VendorNegotiations

e-enabledstrategic

purchasing

Sophisticated, High-Dollar,

StrategicPurchases

Information

Simple,Non-Strategic

Purchases

Enhanced Tools

Purchase Card Functionality

11

Purchase Card Goals (continued)

Goals are changing as programs mature

Goals at inception– Reduce process cost / increase process efficiency– Increase convenience for employee– Reduce procurement cycle

Emerging goals– Obtain better Purchase Card data– Increase controls – Improve vendor management– New uses for the Purchase Card

• Convert more purchase order transactions to Purchase Card

12

Purchase Card Goals (continued)

Emerging goals

Obtain better Purchase Card data– Citibank® Custom Reporting System– Citibank® Electronic Reporting System– Electronic file output

• SBF

• DEF

13

Purchase Card Goals (continued)

Emerging goals

Increase controls– CitiDirect® Card Management System– Citibank® Custom Reporting System– Citibank® Electronic Reporting System

14

Purchase Card Goals (continued)

Emerging goals

Improve vendor management– Reports can paint a bigger picture

• Identify top ten vendors

• Number of transactions per year

• Dollars spent per year

• Negotiate better pricing with identified vendors– Report sources

• Citibank® Custom Reporting System

• MasterCard’s Enhanced Merchant Reporting

• Visa’s Information Management

15

Purchase Card Goals (continued)

Emerging goals

New uses– Uniform cleaning– Security expenses

(fingerprinting, drug tests, etc.)– Spare parts– Software– Subscriptions – Rental equipment– Safety supplies– Premiums items– Utilities– Telecommunications– Courier services

– Licenses– Health services– Short-term leasing– Snow removal– Landscaping– Training– Furniture– Plumbing– HVAC– Travel agency fees

16

Purchase Card Goals (continued)

17

Purchase Card Goals (continued)

18

Purchase Card Goals (continued)

19

Purchase Card Goals (continued)

20

Purchase Card Goals (continued)

Emerging goals

Citibank® Electronic Reporting System

21

Purchase Card Goals (continued)

Future program audit tool

Data reporting and mining

Data available 48 hours after statement cycle

Mining criteria is configurable at the hierarchy level

One screen overview of the review status

Predefined report generation and distribution

Exception modeling capability

22

Purchase Card Goals (continued)

Future program audit tool

Product roll-out

– July 2004 – Single Client pilot– September 2004 – Full Client pilot– Late 2004 / early 2005 – general client base

23

Purchase Card Goals (continued)

Support for the program

Senior management support– “…increased likelihood of receiving endorsements and resources for

existing initiatives, encouraging compliance to policies, and increasing visibility and buy-in.” Deloitte & Touche 2003 Procure-to-Pay study

Strong A/OPC leadership– Influence current and potential procedures– Strongest knowledge of day-to-day operations

24

Summary

Benefits of expanded purchase card use

Facilitates vendor negotiations

Reduces volume of purchase orders

Streamlines accounting processes

Enables monitoring of policy compliance

Improves spending controls

Enables regulatory reporting

Improves supplier / buyer relations

Cost savings and rebates

25

Techniques to Grow Your Program

Questions?

26

Reminders

Thank you for attending this session!

Visit the Citibank Welcome Center– The Maurepas Suite, on the third floor at the Sheraton– Pick up and complete a Citibank survey during your visit– National Industries for the Blind will have a display of products

Visit the Citibank Technical Demonstration Center– Napoleon Ballroom D1, on the third floor at the Sheraton

Citibank hands-on training– Grand Ballroom C, on the fifth floor at the Sheraton

Please take a moment to complete your GSA survey for this session

27

Citigroup's Global Corporate and Investment Bank ("GCIB") maintains a policy of strict compliance to the anti-tying provisions of the Bank Holding Company Act of 1956, as amended, and the regulations issued by the Federal Reserve Board implementing the anti-tying rules (collectively, the "Anti-tying Rules"). Moreover, our credit policies provide that credit must be underwritten in a safe and sound manner and be consistent with Section 23B of the Federal Reserve Act and the requirements of federal law. Consistent with these requirements, and the GCIB's Anti-tying Policy:

� You will not be required to accept any particular product or service offered by Citibank or any Citigroup affiliate as a condition to the extension of commercial loans or other products or services to you by Citibank or any of its subsidiaries, unless such a condition is permitted under an exception to the Anti-tying Rules.

� GCIB will not vary the price or other terms of any Citibank product or service based on the condition that you purchase any particular product or service from Citibank or any Citigroup affiliate, unless we are authorized to do so under an exception to the Anti-tying Rules.

GCIB will not require you to provide property or services to Citibank or any affiliate of Citibank as a condition to the extension of a commercial loan to you by Citibank or any Citibank subsidiary, unless such a requirement is reasonably required to protect the safety and soundness of the loan.

GCIB will not require you to refrain from doing business with a competitor of Citigroup or any of its affiliates as a condition to receiving a commercial loan from Citibank or any of its subsidiaries, unless the requirement is reasonably designed to ensure the soundness of the loan.

This presentation is for informational purposes only. Citibank USA, N.A. and its affiliates does not warrant the accuracy or completeness of any

information or materials set forth herein. This material does not constitute a recommendation to take any action, and Citibank USA, N.A and its affiliates are not providing investment, tax or legal advice. Citibank USA, N.A. and its affiliates accept no liability whatsoever for any use of this presentation or any action taken based on or arising from the material contained herein.

28

Copyright © 2004 Citibank, N.A. CITIBANK, CITIDIRECT, CITIGROUP and the Umbrella Device are registered service marks of Citicorp or its affiliates.

![[Citibank] Asset Based Finance Citibank(Bookos-z1.Org)](https://img.pdfslide.net/doc/110x75/55cf97e7550346d033945106/citibank-asset-based-finance-citibankbookos-z1org.jpg)