Embed Size (px)

Citation preview

City of Phoenix Employees’ Retirement System (COPERS)

Real Estate PerformanceQ3 2020

PRIVATE and CONFIDENTIAL: These materials are strictly confidential and/or legally privileged. These materials are intended only for the use of the individual or entity namedherein (“Intended Recipient”) and may not be re-produced or distributed or posted electronically or incorporated into other documents in whole or in part except for the personal

reference of the Intended Recipient. If you are not the Intended Recipient you are hereby requested to either destroy or return these documents to Aksia Chicago LLC (“Aksia”).

Intended Recipient: City of Phoenix Employees’ Retirement System (COPERS)

Presented By: Mark Bartmann & Dan Krivinskas

1

SPOTLIGHT: Of f iceThe COVID-19 pandemic and associated stay-at-home measures have led to a dramatic reduction in office usage around the world through most of calendar year 2020. While collections fromtenants remain fairly high (given a variety of support structures, including governmental assistance in many markets), there are longer-term questions about how space usage may change in a post-COVID world. Competing dynamics are at play—while work-from-home has proven viable for some, the question is how resilient this trend will be after the COVID emergency passes. Olderreaders may recall prognostications of the “death of office” during the 1990s internet boom period as well as during the aftermath to the 9/11 terrorist attacks. On the other hand, the trend towardsdense user layouts may be changing. How these dynamics play out after the COVID period ends will likely impact returns in office going forward. Given these dynamics, office returns havegenerally been in the “middle of the pack” among the major property types, returning 0.3% in Q3 2020 and 2.9% over the last 12 months according to the NPI. However, not all office is createdequal. Generally, well-located suburban office has performed better than office in downtown locations over the last year, returning 4.8% vs CBD office returning 1.8%.2 Moreover, there are signsthat a shift away from more expensive, denser markets to “lifestyle” locations with a lower cost of living and lower tax rates may be accelerating. Several prominent firms have moved significantnumbers of employees (and, in some cases, their headquarters) to markets such as Austin, Denver, Miami, and Nashville during 2020.

Figure 1: Gross Quarterly Returns | %

3Q 2020 REAL ESTATE MARKET OVERVIEW | REAL ESTATE

Source: NCREIF, via Bloomberg

2

Real Estate OverviewTailwinds Headwinds Industrial sector is maintaining strength,

stemming from secular trend toward more e-commerce, accelerated by the pandemiceffect.

Re-pricing of assets across most sectors hasopened a potential window of opportunity toacquire good quality properties at a discountto pre-crisis levels; however, large bid-askspreads remain.

Life sciences and healthcare real estatevaluations are increasing based on growingdemand as well as the inability of tenants tooperate remotely.

Retail sector continues to be hit hard by seculartrends as well as pandemic-related slowdowns. Mosttypes of retail properties will be impacted to varyingextents, with urban infill mixed-use properties andcenters with heavy “experiential” tenant bases likelyto fare better in a post-pandemic period.

Class A urban multifamily properties areexperiencing operational struggles as demand hassubsided in many major metros, due to remoteworking and associated relocations to suburbanareas and lower cost markets.

Figure 2: Property Index Returns by Component | %

Performance at a Glance The NCREIF Open End Diversified Core (“ODCE”) and NCREIF Property Index

(“NPI”), both recovered to positive returns in Q3 2020, returning 0.48% and0.74%, respectively. 1,2

Transaction volumes remain substantially depressed. During 3Q 2020, the NPIreported approximately 50 transactions, up slightly from the 30 reported duringQ2 2020. Historically, NPI transaction volumes have typically been between 100to 200 per quarter. 2

By property type, industrial drastically outpaced the other sectors of the NPI, withhotels being the largest detractor. 2

The ODCE index returned to positive returns during 3Q 2020 with consistently-positive income return of 0.95%, despite the third consecutive quarter of negativeappreciation (-0.46%). LTM appreciation return is -2.49%.1

Source: NCREIF, via Bloomberg

Source: Aksia internal market views, based on Aksia’s opinion and not intended as personalized investment advice.

-2.0%

-1.5%

-1.0%

-0.5%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

NCREIF Property Index Open End Diversified Core

1.2%

3.2%

1.4%

0.2%

1.8%

0.5%

3.0%

0.3%

-0.5%

-4.2%-5.0%

-4.0%

-3.0%

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

Q3 2019 Q3 2020

Portfolio OverviewCity of Phoenix Employees’ Retirement System (COPERS)

3

InvestmentCOPERS

CommitmentStructure

Investment Period

ExpirationCommitment

Unfunded Commitment

% Funded 3 Status 4

Morgan Stanley Prime 3Q 2006 Open N/A $90,500,000 $0 100.0% StabilizedJPMorgan SPF 2Q 2007 Open N/A $87,380,529 $0 100.0% Stabilized

Realterm LIF 3Q 2020 Open N/A $30,000,000 $30,000,000 0.0% Recently ClosedTotal Core Portfolio $207,880,529 $30,000,000 85.6%JDM Partners I 1Q 2010 Closed Expired $20,000,000 $551,724 97.2% HarvestingRECAP III 1Q 2012 Closed Expired $30,000,000 $6,339,855 78.9% Nearly LiquidatedWheelock Street I 2Q 2012 Closed Expired $20,000,000 $3,724,018 81.4% Nearly LiquidatedNorthwood Series IV 1Q 2014 Closed Expired $20,000,000 $14,268,302 28.7% HarvestingWheelock Street II 3Q 2014 Closed Expired $30,000,000 $8,657,868 71.1% Nearly LiquidatedNorthwood Series V 1Q 2015 Closed Expired $30,000,000 $13,452,031 55.2% Harvesting

RECAP IV 1Q 2015 Closed Expired $30,000,000 $4,309,319 85.6% HarvestingHSI V 2Q 2016 Closed Expired $25,000,000 $6,494,485 74.0% HarvestingSC Core Fund 3Q 2016 Closed N/A $30,000,000 $47,806 97.3% StabilizedWheelock Street V 4Q 2016 Closed Expired $25,000,000 $6,537,907 73.9% HarvestingFocus Senior Housing I 2Q 2017 Closed 2Q 2021 $25,000,000 $15,974,345 36.1% InvestingHammes Partners III 2Q 2017 Closed 2Q 2022 $25,000,000 $20,027,310 19.9% InvestingRECAP V 4Q 2018 Closed 4Q 2021 $25,000,000 $14,835,342 40.7% InvestingAscentris Value Add Fund III 3Q 2019 Closed 3Q 2023 $25,000,000 $10,174,218 59.3% InvestingWheelock Street VI 4Q 2019 Closed 1Q 2024 $20,000,000 $20,000,000 0.0% InvestingTotal Non-Core Portfolio $380,000,000 $145,394,530 61.7%

Total Portfolio $587,880,529 $175,394,530 70.2%

Co

reN

on

-Co

re

Performance SummaryCity of Phoenix Employees’ Retirement System (COPERS)

4

Notes: Sub-Portfolio and Total Portfolio composite performance figures include data from liquidated investments not shown in table.

Investment Market Value% of RE Portfolio % Funded

1 % Realized5 SI IRR (Gross) 6 SI IRR (Net) 7Net Equity

Multip le 8

Morgan Stanley Prime $79,740,615 22.7% 100.0% 52.4% 6.2% 5.2% 1.70x

JPMorgan SPF $74,109,445 21.1% 100.0% 48.5% 4.7% 4.0% 1.49x

Realterm LIF $0 0.0% 0.0% 0.0% N/A N/A N/A$153,850,060 43.7% 85.6% 50.6% 5.5% 4.7% 1.60x

JDM Partners I $21,467,102 6.1% 97.2% 37.1% 8.0% 6.7% 1.73xRECAP III $4,118,686 1.2% 78.9% 89.1% 11.7% 8.1% 1.17xWheelock Street I $1,670,890 0.5% 81.4% 95.8% 35.5% 24.7% 1.70xNorthwood Series IV $16,499,642 4.7% 28.7% 53.8% 15.9% 11.1% 1.43xWheelock Street II $7,904,215 2.2% 71.1% 79.5% 26.4% 16.6% 1.49xNorthwood Series V $27,112,941 7.7% 55.2% 32.6% 11.4% 8.6% 1.36xRECAP IV $18,276,308 5.2% 85.6% 39.9% 8.7% 5.6% 1.17xHSI V $11,590,376 3.3% 74.0% 43.4% 10.9% 2.8% 1.05xSC Core Fund $31,209,141 8.9% 97.3% 7.3% 5.8% 4.9% 1.11xWheelock Street V $19,572,670 5.6% 73.9% 10.8% 7.3% 3.1% 1.05xFocus Senior Housing I $9,500,670 2.7% 36.1% 4.9% 9.7% 3.8% 1.05xHammes Partners III $4,066,248 1.2% 19.9% 14.1% 16.0% -5.6% 0.95x

RECAP V $11,342,819 3.2% 40.7% 9.9% 31.6% 14.5% 1.10x

Ascentris Value Add Fund III $13,833,254 3.9% 59.3% 4.9% N/A N/A N/A

Wheelock Street VI $0 0.0% 0.0% N/A N/A N/A N/A$198,164,962 56.3% 61.7% 52.6% 13.7% 9.5% 1.28x

$352,015,022 100.0% 70.2% 51.7% 7.4% 5.8% 1.40x

Co

re

Total Core Portfolio

Total Portfolio

Total Non-Core Portfolio

No

n-C

ore

Performance SummaryCity of Phoenix Employees’ Retirement System (COPERS)

5

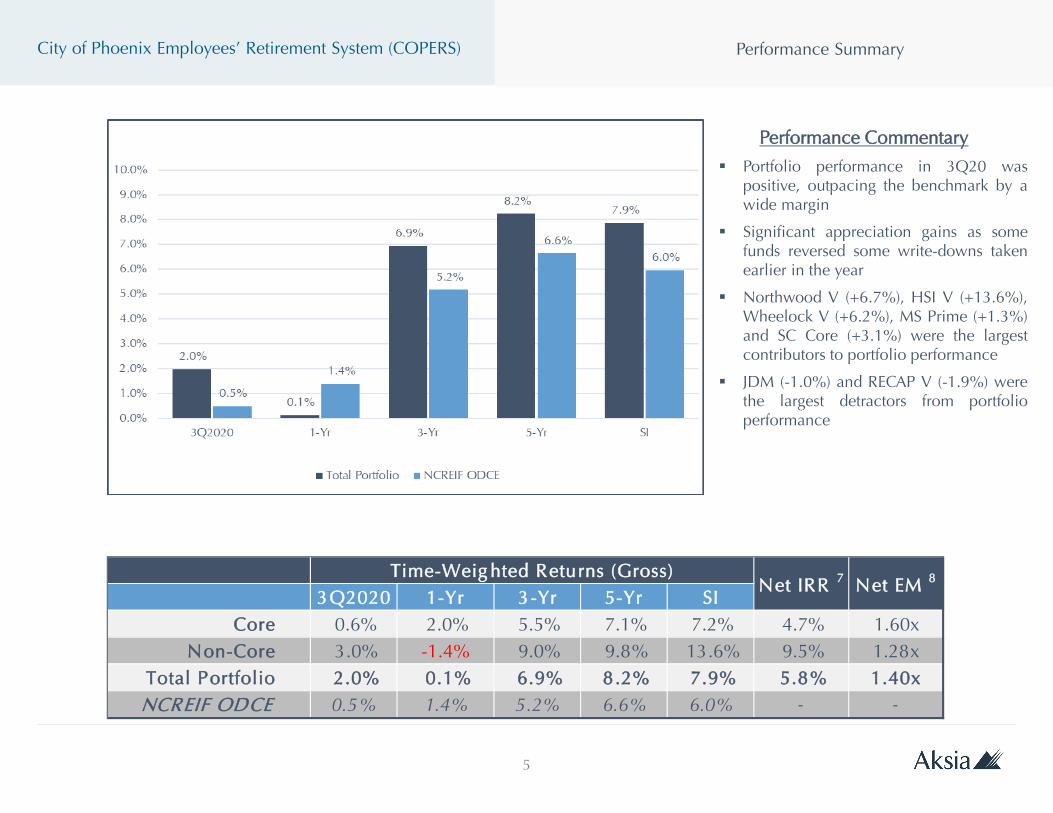

Performance Commentary

Portfolio performance in 3Q20 waspositive, outpacing the benchmark by awide margin

Significant appreciation gains as somefunds reversed some write-downs takenearlier in the year

Northwood V (+6.7%), HSI V (+13.6%),Wheelock V (+6.2%), MS Prime (+1.3%)and SC Core (+3.1%) were the largestcontributors to portfolio performance

JDM (-1.0%) and RECAP V (-1.9%) werethe largest detractors from portfolioperformance

3Q2020 1-Yr 3-Yr 5-Yr SICore 0.6% 2.0% 5.5% 7.1% 7.2% 4.7% 1.60x

Non-Core 3.0% -1.4% 9.0% 9.8% 13.6% 9.5% 1.28xTotal Portfolio 2.0% 0.1% 6.9% 8.2% 7.9% 5.8% 1.40xNCREIF ODCE 0.5% 1.4% 5.2% 6.6% 6.0% - -

Net IRR 7 Net EM 8Time-Weig hted Returns (Gross)

Portfolio DiversificationCity of Phoenix Employees’ Retirement System (COPERS)

6

Total North America

Portfolio Is Well-Diversified by Geography and Property Type• Unfunded commitments to a variety of strategies and regions will ensure the portfolio remains well diversified by

geography and property type

• Exposure to ‘other’ property types, including senior housing and medical office, will increase as Focus SH I andHammes III continue to call capital

• The addition of Realterm Logistics Income Fund (RLIF) to the portfolio will increase industrial exposure as capitalis drawn (first call occurred during 4Q2020)

Leverage ProfileCity of Phoenix Employees’ Retirement System (COPERS)

7

Total Portfolio Loan-toValue (LTV) 9: 42.9%Core Portfolio LTV: 22.5%Non-Core Portfolio LTV: 52.3%

Weighted-Average Interest Rate: 2.7%

Fee Summary10City of Phoenix Employees’ Retirement System (COPERS)

8

3Q2020 Fees Are In Line With Historical Averages Asset management fees charged during the quarter were driven by funds in their initial investment periods

(e.g., Hammes III, RECAP V, Wheelock V)

Incentive fees during the quarter were primarily driven by accruals in Northwood IV & V

Type 3Q2020Quarterly

Avg.As s etMgmt.

0.33% 0.29%

Incentive 0.10% 0.10%Other 0.00% 0.00%

Total 0.43% 0.39%

RE Portfolio Fees(% of Market Value)

Subsequent EventsCity of Phoenix Employees’ Retirement System (COPERS)

9

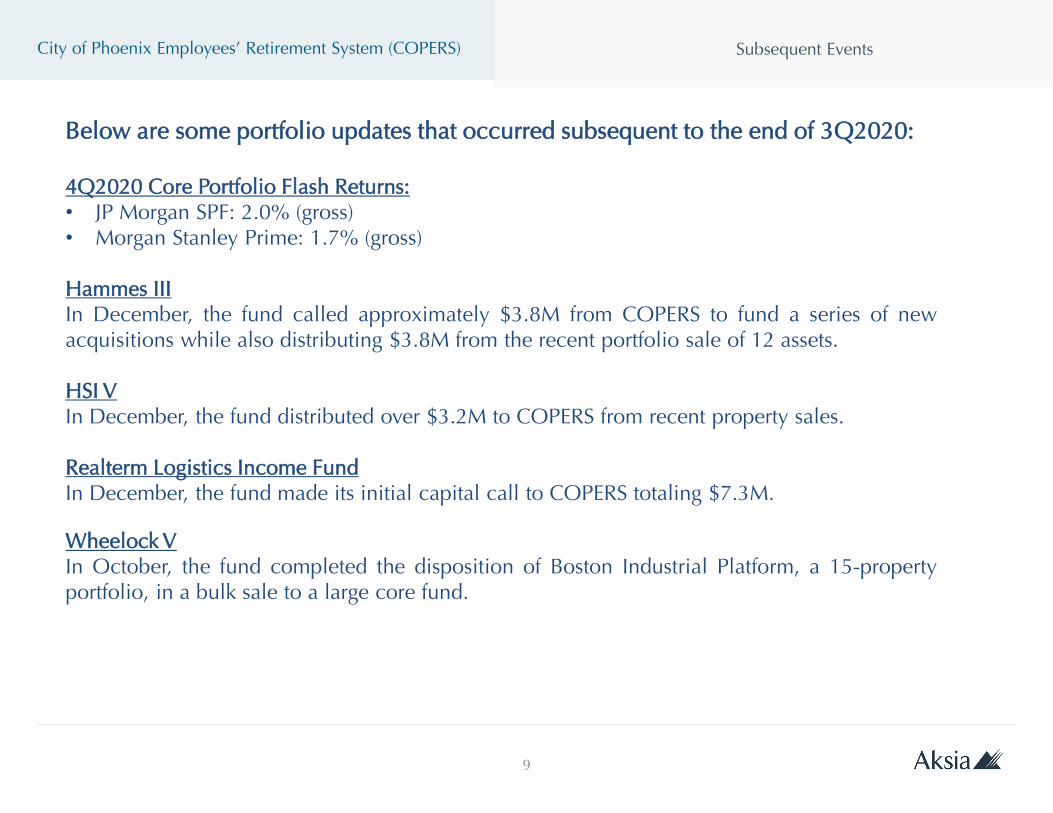

Below are some portfolio updates that occurred subsequent to the end of 3Q2020:

4Q2020 Core Portfolio Flash Returns:• JP Morgan SPF: 2.0% (gross)• Morgan Stanley Prime: 1.7% (gross)

Hammes IIIIn December, the fund called approximately $3.8M from COPERS to fund a series of newacquisitions while also distributing $3.8M from the recent portfolio sale of 12 assets.

HSI VIn December, the fund distributed over $3.2M to COPERS from recent property sales.

Realterm Logistics Income FundIn December, the fund made its initial capital call to COPERS totaling $7.3M.

Wheelock VIn October, the fund completed the disposition of Boston Industrial Platform, a 15-propertyportfolio, in a bulk sale to a large core fund.

Appendix

10

Appendix: Quarterly NAV SummaryCity of Phoenix Employees’ Retirement System (COPERS)

11

Inves tment Opening Value Net Income Net Appreciation Capital Called Capital Dis tributed E nding Value

Morgan S tanley Prime 79,679,753$ 514,110$ 333,712$ -$ 786,960$ 79,740,615$

J PMorgan S PF 74,814,321$ 475,208$ (680,852)$ 185,255$ 684,593$ 74,109,445$

Realterm Logis tics Income Fund -$ -$ -$ -$ -$ -$

154,494,074$ 989,318$ (347,140)$ 185,255$ 1,471,553$ 153,850,060$

J DM Partners I 21,763,196$ (296,094)$ -$ -$ -$ 21,467,102$

RE CAP III 4,198,277$ -$ (79,591)$ -$ -$ 4,118,686$

Wheelock S treet I 1,797,945$ (10,497)$ (116,558)$ -$ -$ 1,670,890$

Northwood S eries IV 16,215,988$ 145,877$ 259,539$ 92,587$ 214,349$ 16,499,642$

Wheelock S treet II 8,194,358$ (49,589)$ 54,351$ 294,904$ 589,809$ 7,904,215$

Northwood S eries V 26,011,759$ 171,713$ 1,066,513$ 119,629$ 256,675$ 27,112,941$

RE CAP IV 18,213,956$ (231)$ 62,583$ -$ -$ 18,276,308$

HS I V 10,321,350$ 209,160$ 1,396,446$ 153,246$ 495,042$ 11,590,376$

S C Core Fund 30,759,967$ 1,437,360$ (544,265)$ 54,325$ 498,246$ 31,209,141$

Wheelock S treet V 18,988,275$ (14,972)$ 1,072,368$ 799,133$ 1,272,134$ 19,572,670$

Focus S enior Hous ing I 9,418,167$ (37,689)$ 120,192$ -$ -$ 9,500,670$

Hammes Partners III 4,114,364$ 44,989$ 93,485$ -$ 186,590$ 4,066,248$

RE CAP V 9,265,719$ (3)$ (279,579)$ 2,410,529$ 53,846$ 11,342,819$

As centris Value Add Fund III 13,663,155$ (201,157)$ 269,032$ 102,224$ -$ 13,833,254$

Wheelock S treet VI -$ -$ -$ -$ -$ -$

192,926,476$ 1,398,867$ 3,374,516$ 4,026,577$ 3,566,691$ 198,164,962$

347,420,550$ 2,388,185$ 3,027,376$ 4,211,832$ 5,038,244$ 352,015,022$

Total Core Portfolio

Total Non- Core Portfolio

Total Portfolio

No

n-

Co

reC

ore

Definitions & FootnotesCity of Phoenix Employees’ Retirement System (COPERS)

12

1 Source: National Council of Real Estate Investment Fiduciaries (NCREIF) Open-ended Diversified Equity Index (“ODCE”) – www.ncreif.org

2 Source: National Council of Real Estate Investment Fiduciaries (NCREIF) Property Index (“NPI”) – www.ncreif.org

3 Commitment Funded Percentage (“% Funded”) – The percentage of the investor’s commitment that has been called by the manager to date, less any capital returned during the investment period that is deemed to be recallable.

4 Investment Status Definitions:

Recently Closed-Investment is awaiting first capital call designated for investment purposes

Investing- Investment actively making commitments to new underlying investments; within stated investment period

Stabilized- Investment is fully invested and unlikely to make near-term return of capital distributions

Harvesting- Investment is actively divesting

Nearly Liquidated- Investment is substantially divested of assets (typically > 80% realized)

Liquidated- Investment has divested of all assets and either holds cash or no balance at all

5 Realization Percentage (“% Realized”) – The percentage of an investment’s cumulative distributions to date relative to the total value of the fund, measured as a sum of the cumulative distributions to date and the remaining investment value.

6 Since Inception Gross Internal Rate of Return (“SI-IRR GROSS”) – Reflects the implied discount rate equating the present value of an investment’s cash outflows and the remaining market value to the present value of the investment’s cash inflows, excluding any impact of fees charged or accrued.

7 Since Inception Net Internal Rate of Return (“SI-IRR NET”) - Reflects the implied discount rate equating the present value of an investment’s cash outflows and the remaining market value to the present value of the investment’s cash inflows, accounting for the impact of fees.

8 Net Equity Multiple (“NET EM”) – The sum of cumulative distributions and remaining investment value divided by total paid-in-capital, accounting for the impact of fees.

9 Loan-to-Value Ratio (“LTV %”) – Ratio of all outstanding direct debt obligations divided by the fair value of the fund’s gross real estate asset value.

10 Fee Summary – Fees percentages shown reflect fees paid relative to beginning portfolio market value.

13

Disclaimer

This document was prepared by Aksia Chicago LLC (“Aksia”) and includes information and data from some or all of the following sources:investment managers, custodian banks, client staff, specialty investment consultants, actuaries, plan administrators/record-keepers, indexproviders, as well as other third-party sources as directed by the client or as we believe necessary or appropriate. Aksia makes no warrantiesand disclaims responsibility for the accuracy or completeness of information or data provided or methodologies employed by any externalsource. Aksia has taken reasonable care to ensure the accuracy of the information or data but disclaims responsibility for the accuracy ofinformation or data received from outside sources. This document is provided for the client’s internal use only and does not constitute arecommendation by Aksia or an offer of, or a solicitation for, any particular security and it is not intended to convey any guarantees as to thefuture performance of the investment products, asset classes, or capital markets.