Embed Size (px)

Citation preview

Republic of Tanzania

Ministry of Infrastructure Development

Civil Aviation Master Plan Pre-feasibility Study

Version 2.3

March 2010

2

Acronyms and Abbreviations

ADS-B Automatic Dependent Survey - Broadcast AFTN Aeronautical Fixed Telecommunications Network AIS Aeronautical Information Services ANS Air Navigation Services ATR Avions de Transport Regional ATS Air Traffic Services AVSEC Aviation Security BADEA Arab Bank for Economic Development in Africa CASSOA EAC Civil Aviation Safety and Security Oversight Agency CATC Civil Aviation Training Center COM Communications DAR FIR Dar es Salaam Flight Information Region DRC Democratic Republic of Congo EAC East African Community FDPS Flight Data Processing System FIR Flight Information Region FY Fiscal Year GA General Aviation GNI Gross National Income GNSS Global Navigation Satellite System GoT Government of Tanzania GPS Global Positioning System IATA International Air Transport Association ICAO International Civil Aviation Organization IDA International Development Agency (part of the World Bank) IFR Instrument Flight Rules JNIA Julius Nyerere International Airport KADCO Kilimanjaro Airports Development Corporation MCC Millennium Challenge Corporation MoID Ministry of Infrastructure Development NAV Navigation NDB Non-Directional Beacon OPEC Organization of the Petroleum Exporting Countries PPP Public-Private Partnership RGoZ Revolutionary Government of Zanzibar SADC South African Development Community TAA Tanzania Airports Authority TCAA Tanzania Civil Aviation Authority TORs Terms of References Tsh Tanzania Shilling TSIP Transport Sector Improvement Project TSSP Transport Sector Support Project VFR Visual Flight Rules VHF Very High Frequency VSAT Very Small Aperture Terminal

3

Table of Contents i. Introduction .......................................................................................................................................... 5

ii. Executive Summary ............................................................................................................................ 7

I. Country Overview .............................................................................................................................. 13

II. Sector Overview ............................................................................................................................... 16

1. Institutions and Agencies ............................................................................................................... 17

a. Ministry of Infrastructure Development ...................................................................................... 17

b. TCAA ........................................................................................................................................ 18

c. TAA .......................................................................................................................................... 23

2. Service Providers ........................................................................................................................... 25

Air Tanzania .................................................................................................................................. 25

III. Traffic Overview ............................................................................................................................. 28

1. International Travel ....................................................................................................................... 28

2. Domestic Travel ............................................................................................................................ 34

IV. Investments: An Overview .............................................................................................................. 40

1. Anticipated Needs.......................................................................................................................... 40

2. Summary of Traffic Projections ..................................................................................................... 41

3. Needs for Primary Airports ............................................................................................................ 47

a. Julius Nyerere International Airport ........................................................................................... 47

b. Zanzibar International Airport .................................................................................................... 48

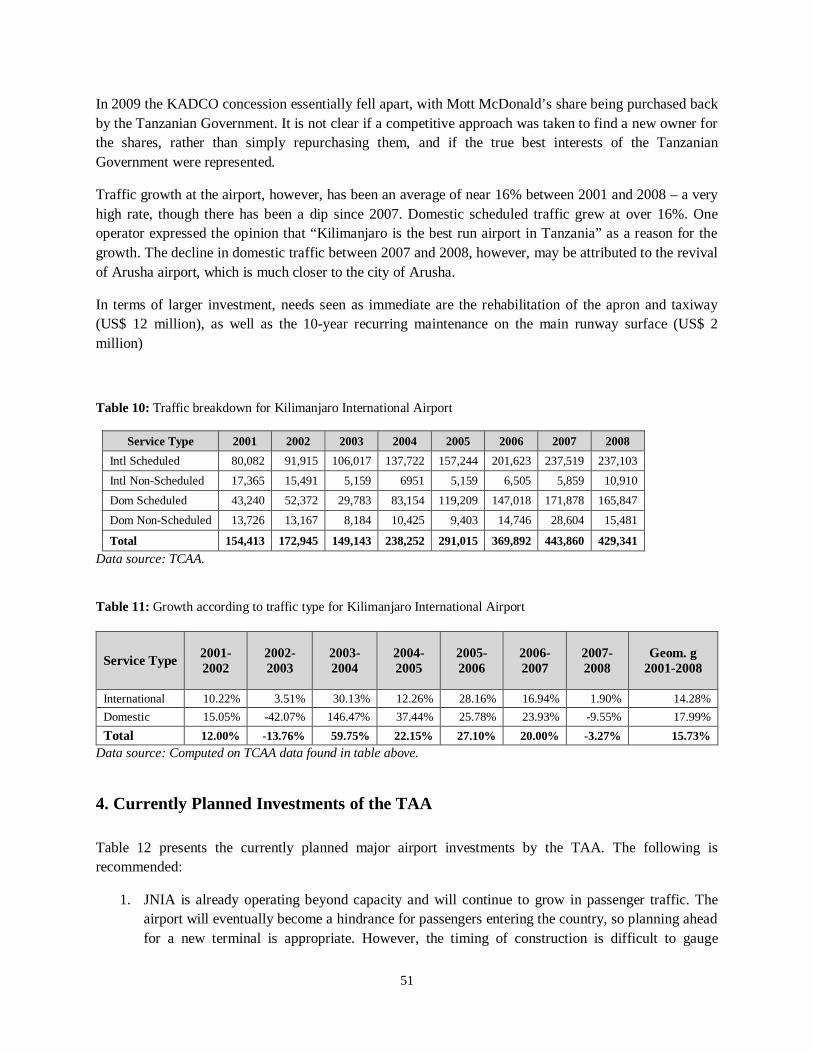

c. Kilimanjaro International Airport ............................................................................................... 50

4. Currently Planned Investments of the TAA .................................................................................... 51

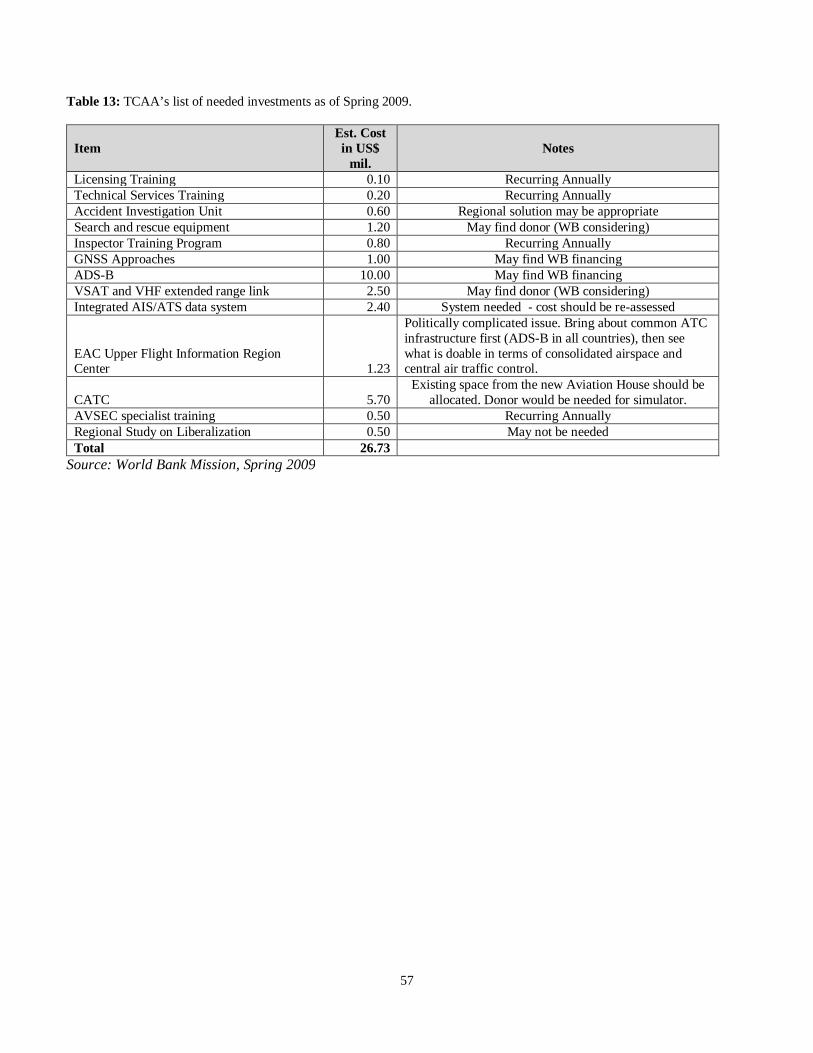

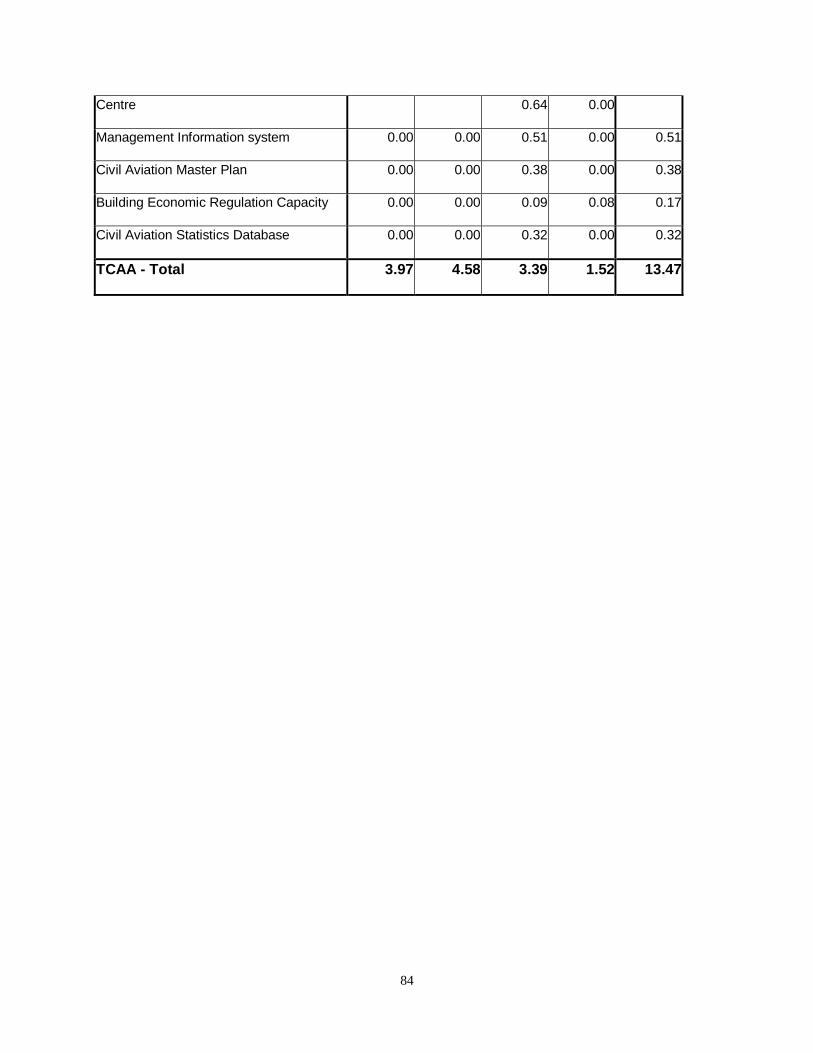

5. Currently Planned Investments of the TCAA ................................................................................. 55

V. Action Plan for the Meeting of Needs for the Air Transport Sector .................................................... 58

VI. Proposed Steps and Outline for Tanzania Civil Aviation Master Plan ............................................... 61

Appendix A: A hub in Dar es Salaam - two distinct concepts ................................................................. 63

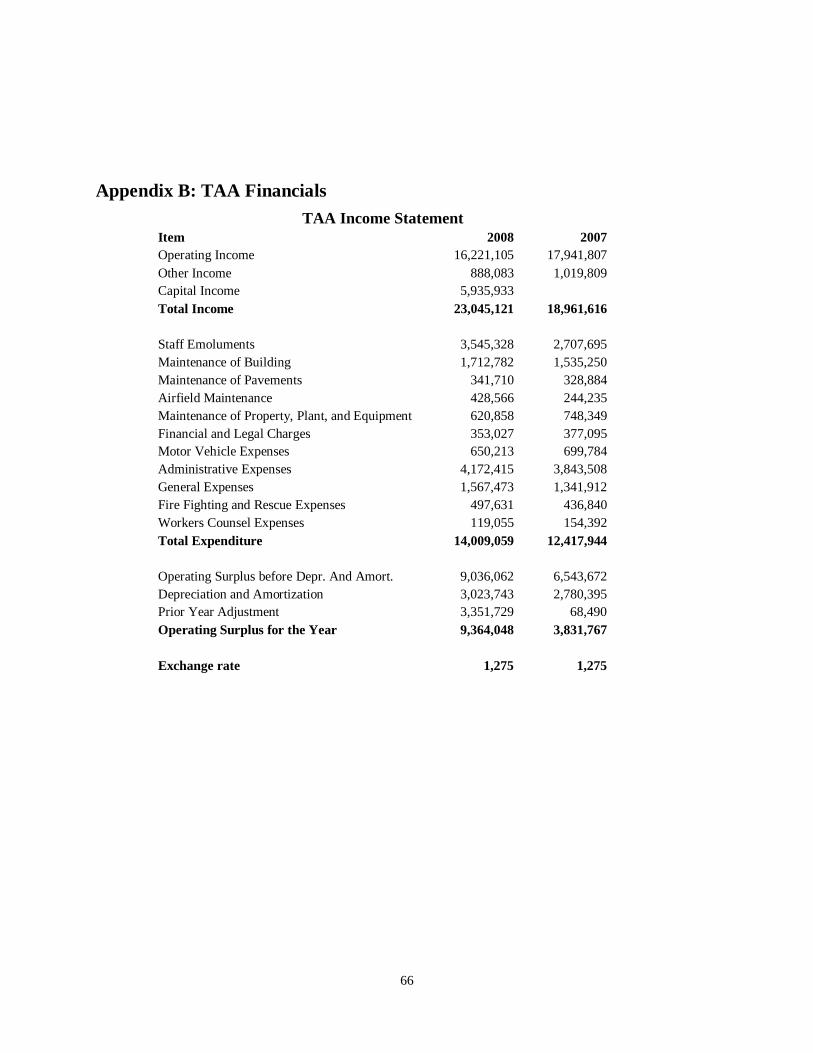

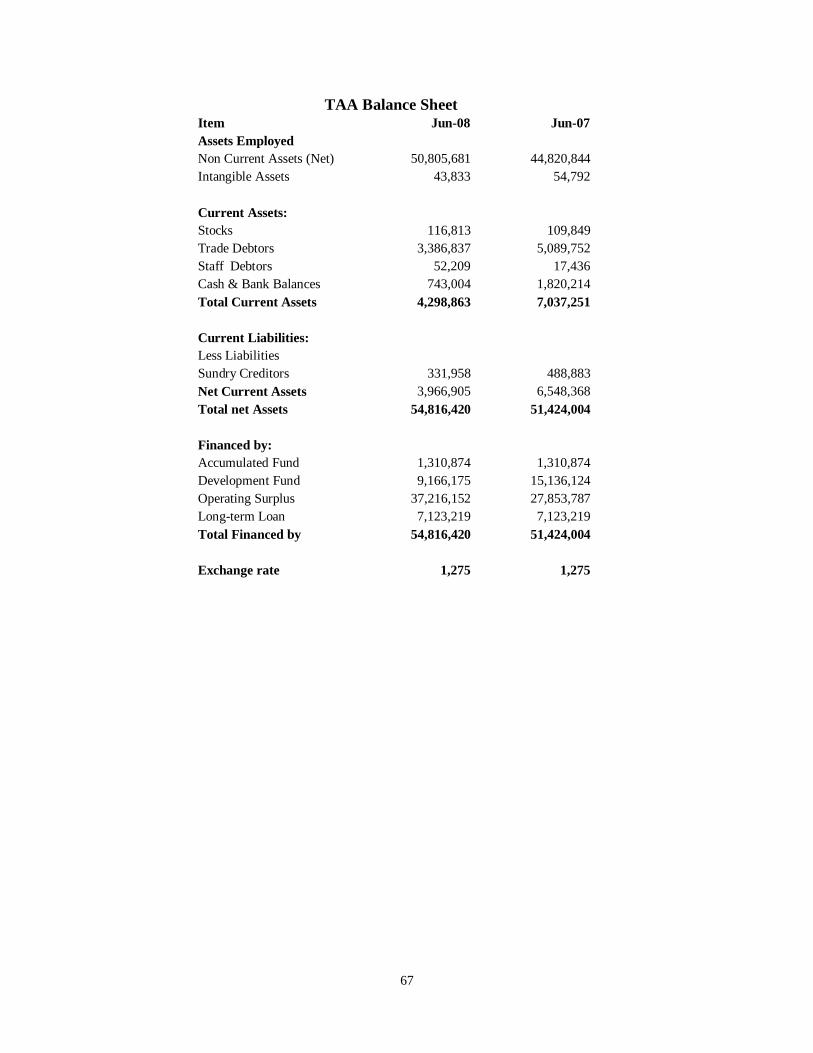

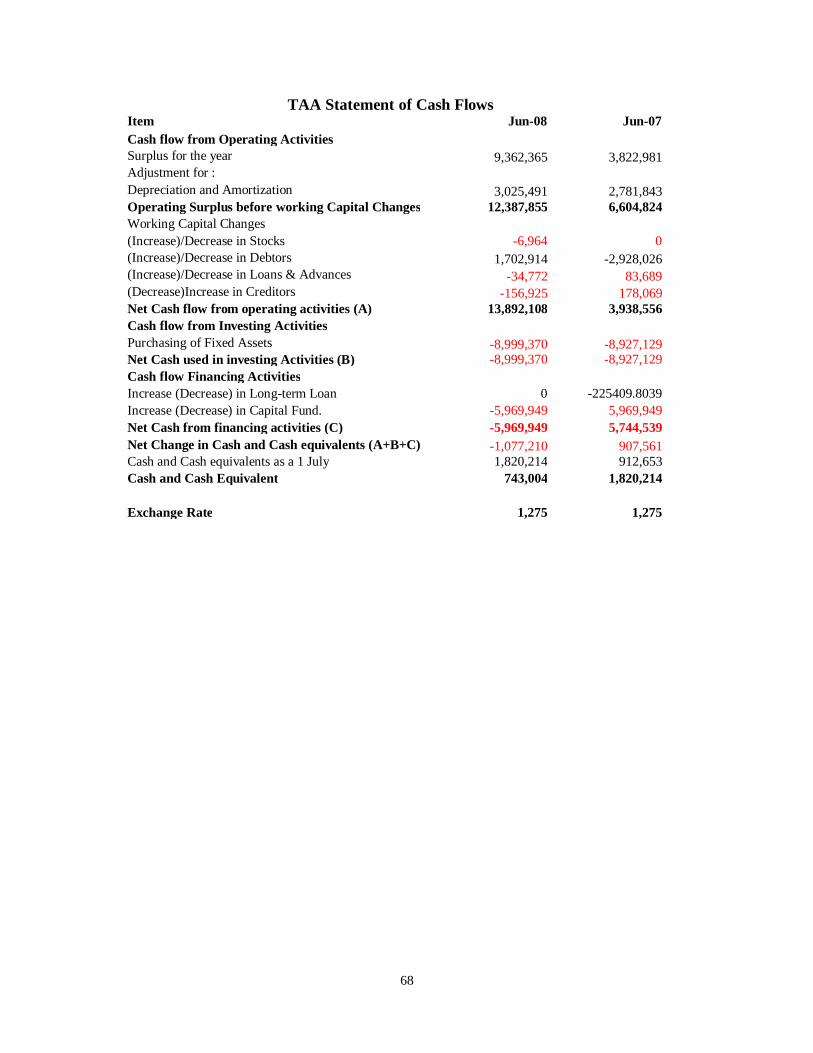

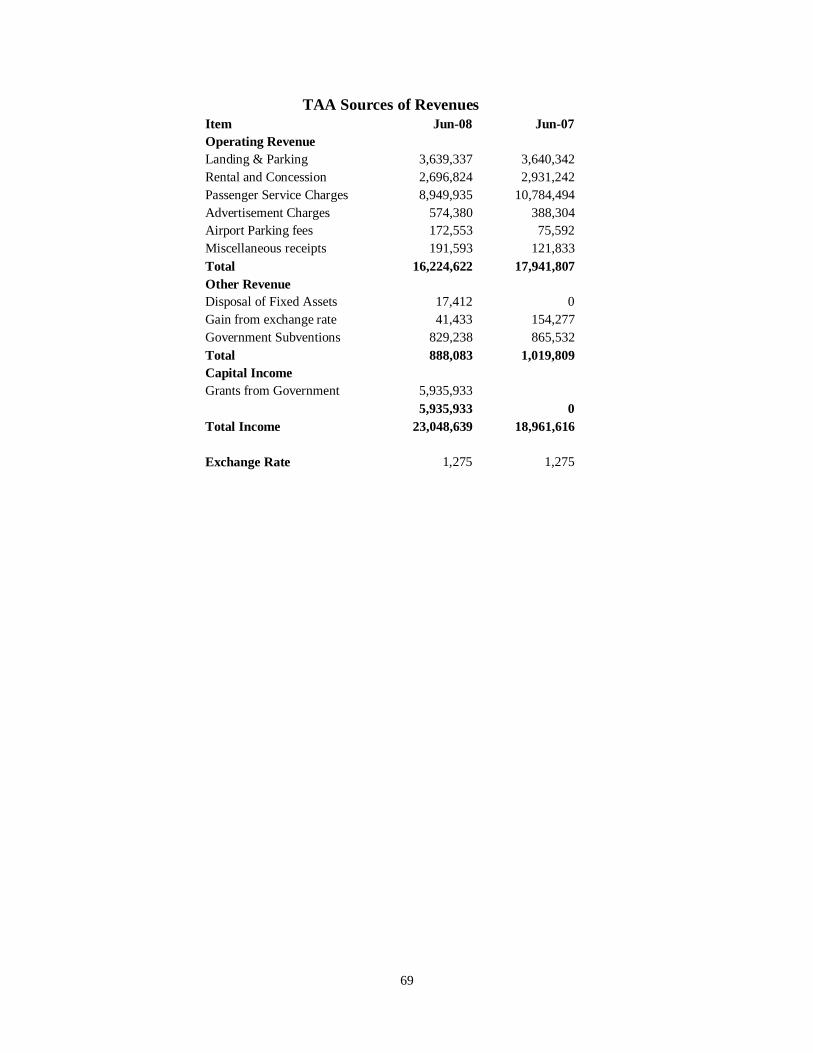

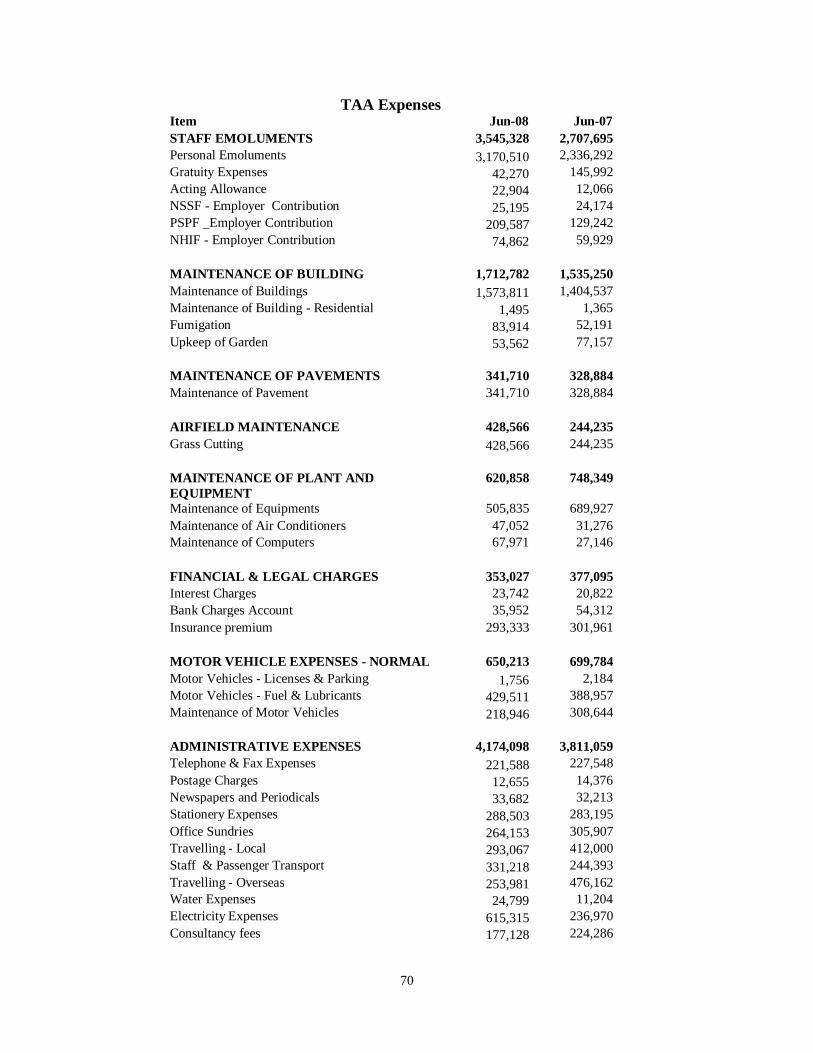

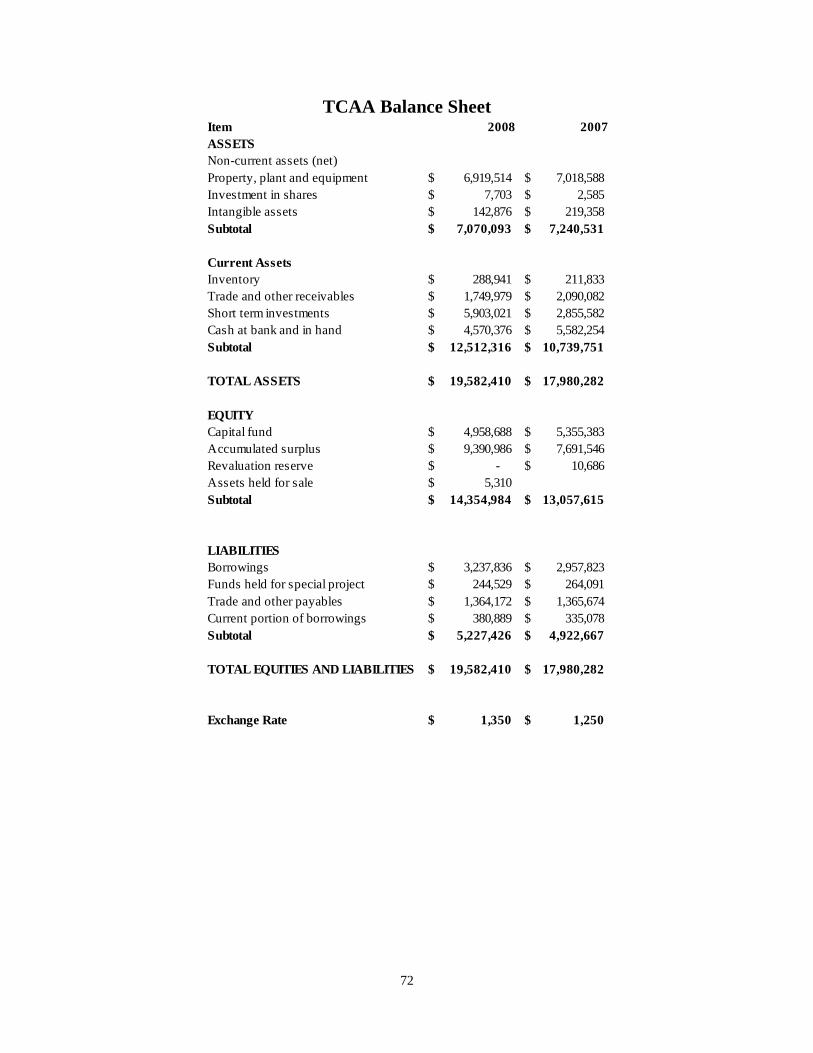

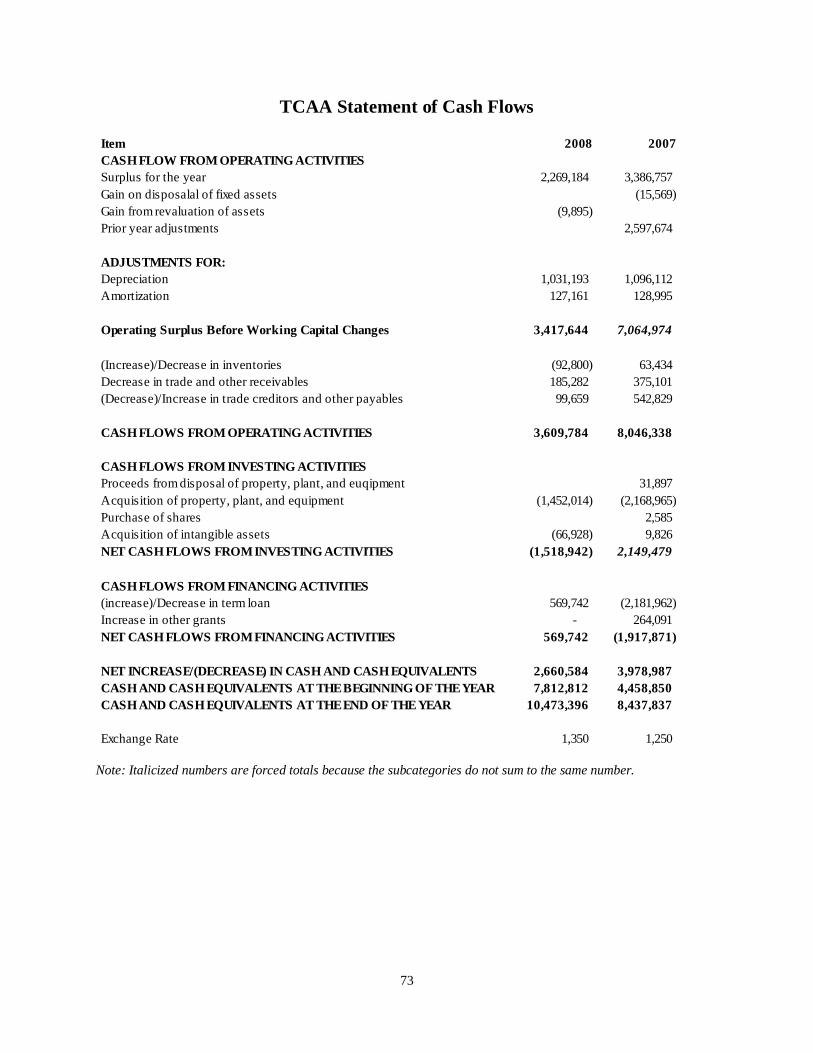

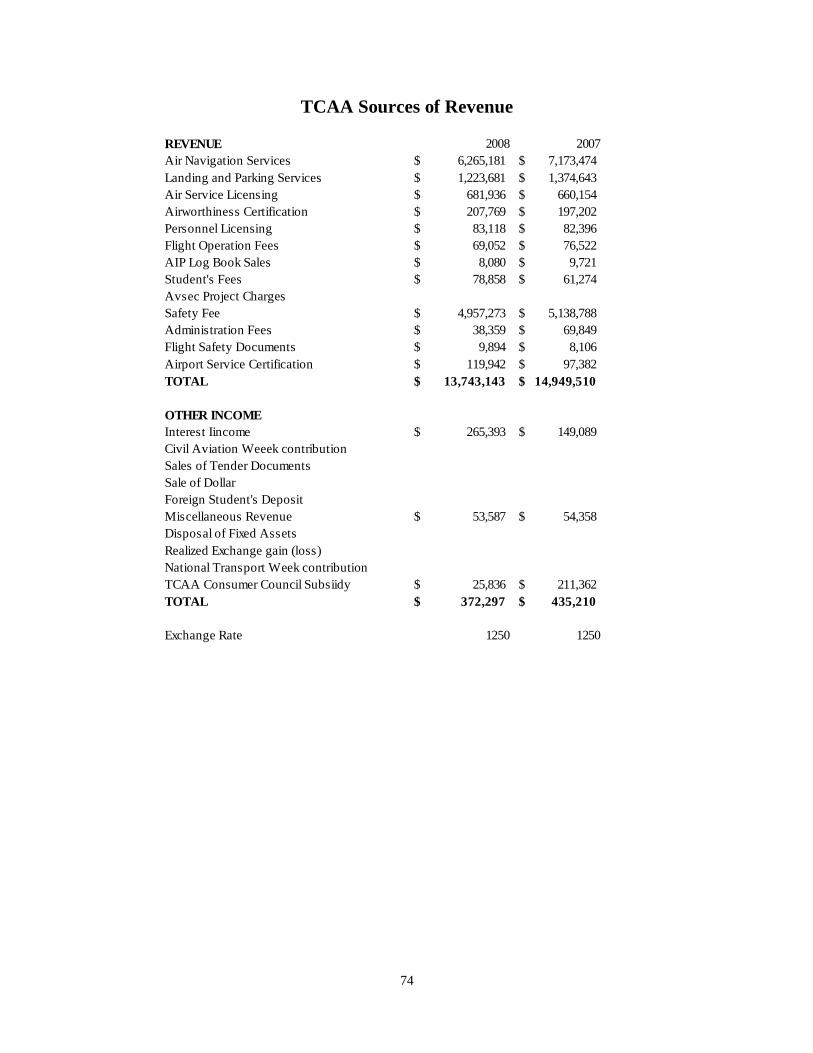

Appendix B: TAA Financials ................................................................................................................ 66

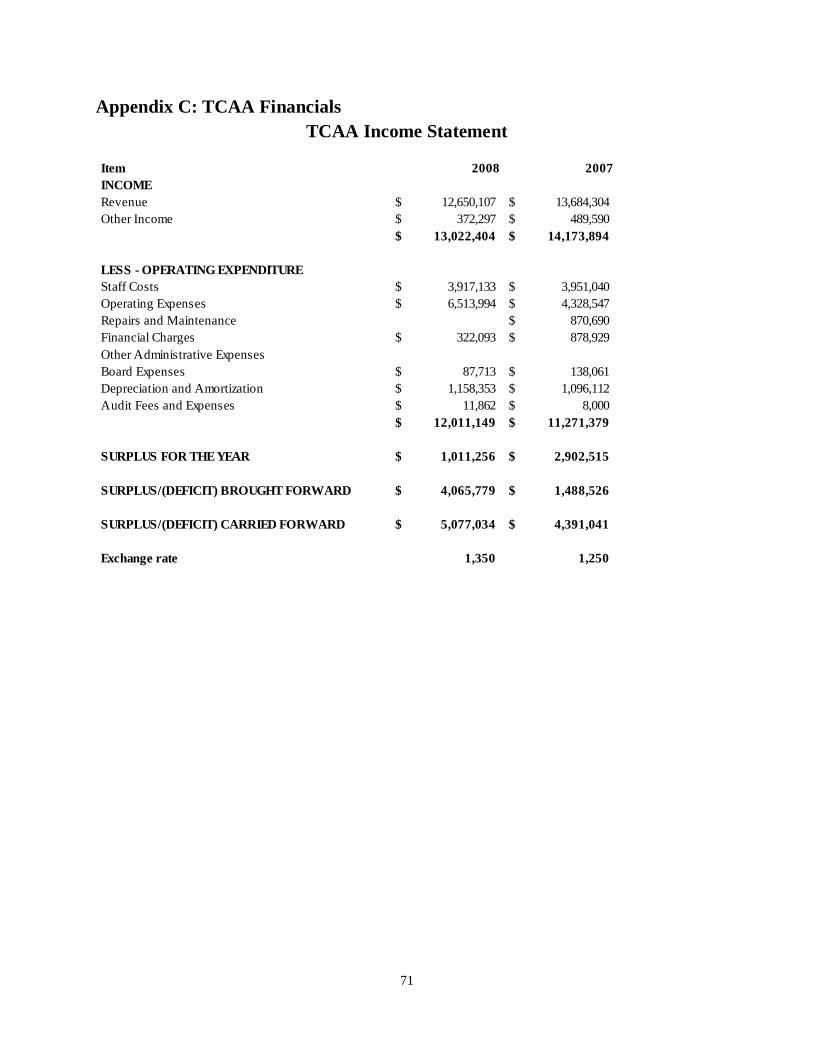

Appendix C: TCAA Financials .............................................................................................................. 71

Appendix D: Terms of references for the study ...................................................................................... 75

Appendix E: List of persons met for this study ....................................................................................... 85

4

This page intentionally blank

5

i. Introduction This Aviation Master Plan Pre-feasibility Study has been carried out within the framework of the project Management Consultancy for Institutional Support to Transport, funded by the EU. The study had several mandates: Initially conceived as a pre-feasibility study for a full civil aviation master plan, it was also intended to act in lieu of such a master plan for intermediate term financial planning within the Ministry of Infrastructure Development (MoID) as in input for the Short Transport Sector Investment Plan for the three year period between FY 2009/2010 and 2011/2012.

At the onset of this study funding for a full master plan seemed difficult to find, though fortunately sources for such a plan have been identified as this study neared completion. This implies that many of the issues identified in this report and perhaps deserving further research can be dealt with more thoroughly during the actual master plan development.

In addition, funding seems to be on the horizon for the development of a new master plan for Julius Nyerere International Airport in Dar es Salaam. As will be shown later in this report, the need for a new terminal for the airport is one of the main findings arriving from traffic projections. Both master plans were deemed a necessary component for the involvement of the private sector in the development of the new terminal, and are thus part of part the World Bank’s Transport Support Project now being prepared for World Bank Board Approval by end of May 2010.

The TORs for this study can be found in Appendix D. The study is the result of two visits to Tanzania, the first being between October 16 and October 30, 2009, and the second between February 22 and March 12, 2009. A presentation on the first draft of this study was held on March 4, with representatives from the MoID, TCAA, and TAA present. This final version of the report reflects the reviews given after the meeting.

6

This page intentionally blank

7

ii. Executive Summary Tanzania has a total of 368 airports and aerodromes on the mainland, with an additional at least one additional airport on each of the islands of Pemba and Zanzibar. The country, at 947 km2, is considered large, and there are substantial areas of land with low population densities and without much transport infrastructure. This set a unique environment, as Tanzania has much of a tourist industry from abroad and has a domestic air transport network in part relying on general aviation type operations.

The sector is at a critical stage, needing much investment. At the same time both domestic and international air transport has been growing considerably in Tanzania.

The country has three primary institutions, the Ministry of Infrastructure Development (MoID) responsible for overall policy, investment, and performance monitoring, the Tanzania Civil Aviation Authority (TCAA) as the main regulator and oversight agency, and the Tanzania Airports Authority as the main airports authority. In addition, the Kilimanjaro International Airport is managed by the Kilimanjaro Airports Development Corporation, and the Revolutionary Government of Zanzibar is responsible for Zanzibar International Airport and the airport in Pemba.

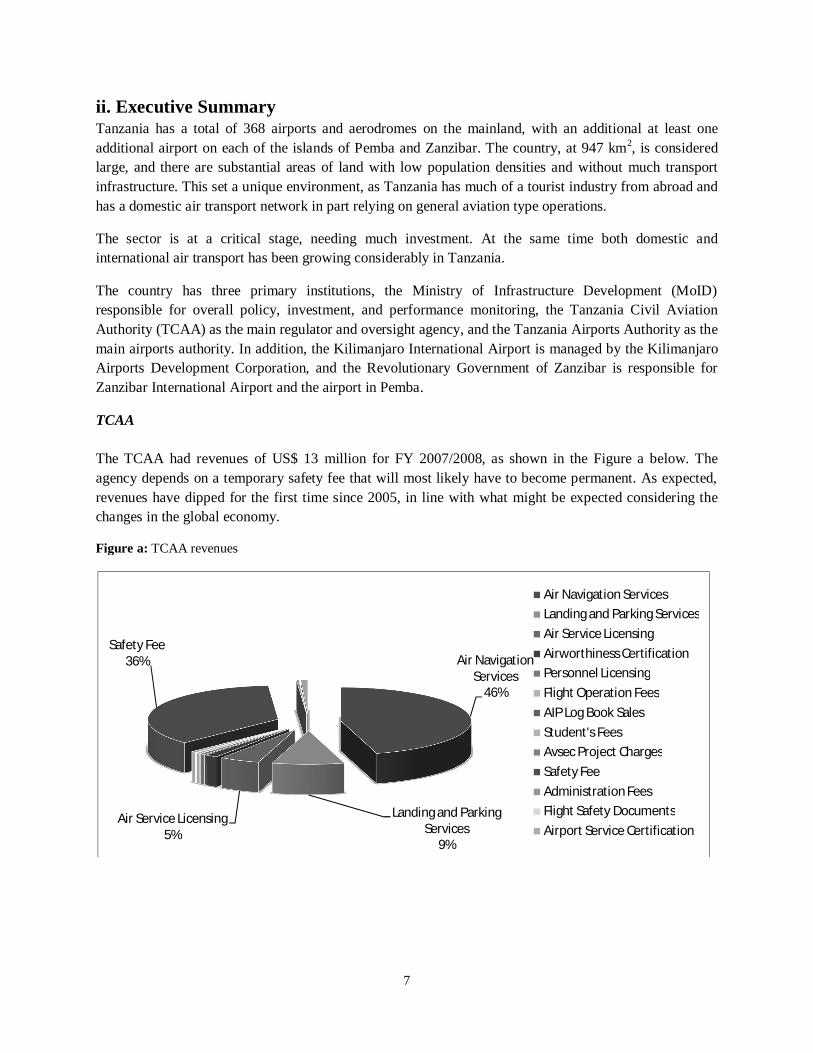

TCAA The TCAA had revenues of US$ 13 million for FY 2007/2008, as shown in the Figure a below. The agency depends on a temporary safety fee that will most likely have to become permanent. As expected, revenues have dipped for the first time since 2005, in line with what might be expected considering the changes in the global economy.

Figure a: TCAA revenues

Air Navigation Services

46%

Landing and Parking Services

9%

Air Service Licensing5%

Safety Fee36%

Air Navigation ServicesLanding and Parking ServicesAir Service LicensingAirworthiness CertificationPersonnel LicensingFlight Operation FeesAIP Log Book SalesStudent's FeesAvsec Project ChargesSafety FeeAdministration FeesFlight Safety DocumentsAirport Service Certification

8

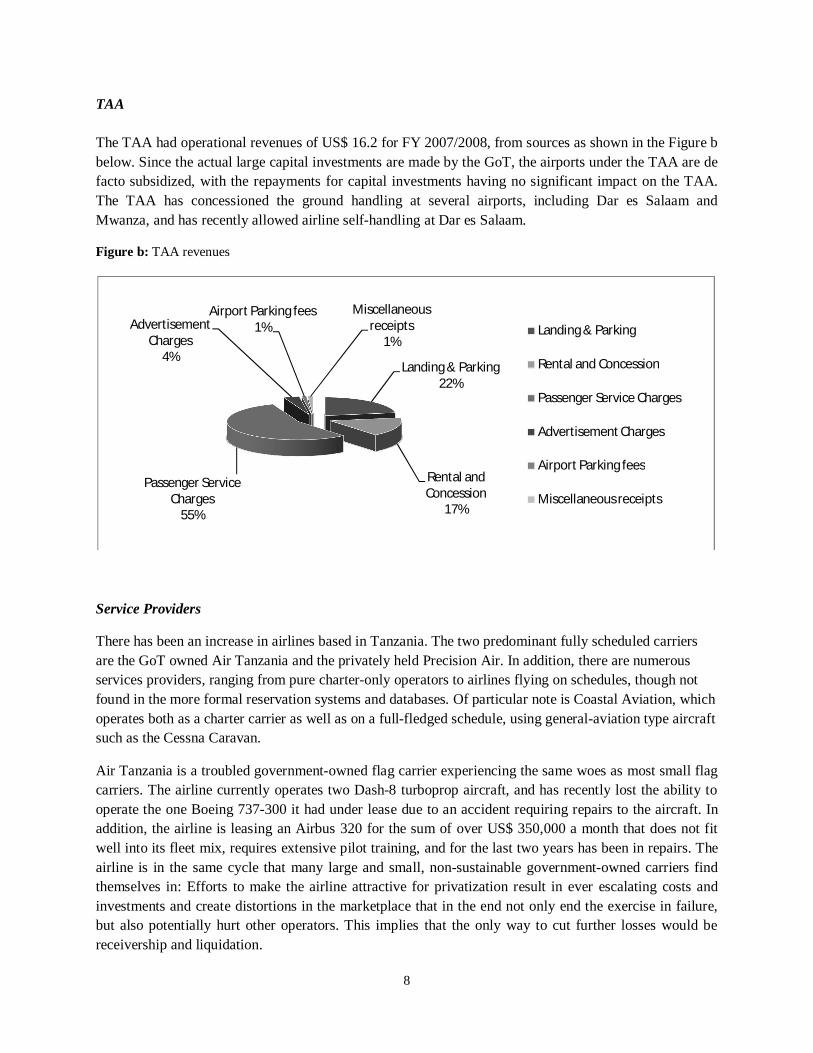

TAA The TAA had operational revenues of US$ 16.2 for FY 2007/2008, from sources as shown in the Figure b below. Since the actual large capital investments are made by the GoT, the airports under the TAA are de facto subsidized, with the repayments for capital investments having no significant impact on the TAA. The TAA has concessioned the ground handling at several airports, including Dar es Salaam and Mwanza, and has recently allowed airline self-handling at Dar es Salaam.

Figure b: TAA revenues

Service Providers

There has been an increase in airlines based in Tanzania. The two predominant fully scheduled carriers are the GoT owned Air Tanzania and the privately held Precision Air. In addition, there are numerous services providers, ranging from pure charter-only operators to airlines flying on schedules, though not found in the more formal reservation systems and databases. Of particular note is Coastal Aviation, which operates both as a charter carrier as well as on a full-fledged schedule, using general-aviation type aircraft such as the Cessna Caravan.

Air Tanzania is a troubled government-owned flag carrier experiencing the same woes as most small flag carriers. The airline currently operates two Dash-8 turboprop aircraft, and has recently lost the ability to operate the one Boeing 737-300 it had under lease due to an accident requiring repairs to the aircraft. In addition, the airline is leasing an Airbus 320 for the sum of over US$ 350,000 a month that does not fit well into its fleet mix, requires extensive pilot training, and for the last two years has been in repairs. The airline is in the same cycle that many large and small, non-sustainable government-owned carriers find themselves in: Efforts to make the airline attractive for privatization result in ever escalating costs and investments and create distortions in the marketplace that in the end not only end the exercise in failure, but also potentially hurt other operators. This implies that the only way to cut further losses would be receivership and liquidation.

Landing & Parking22%

Rental and Concession

17%

Passenger Service Charges

55%

Advertisement Charges

4%

Airport Parking fees1%

Miscellaneous receipts

1%Landing & Parking

Rental and Concession

Passenger Service Charges

Advertisement Charges

Airport Parking fees

Miscellaneous receipts

9

Traffic

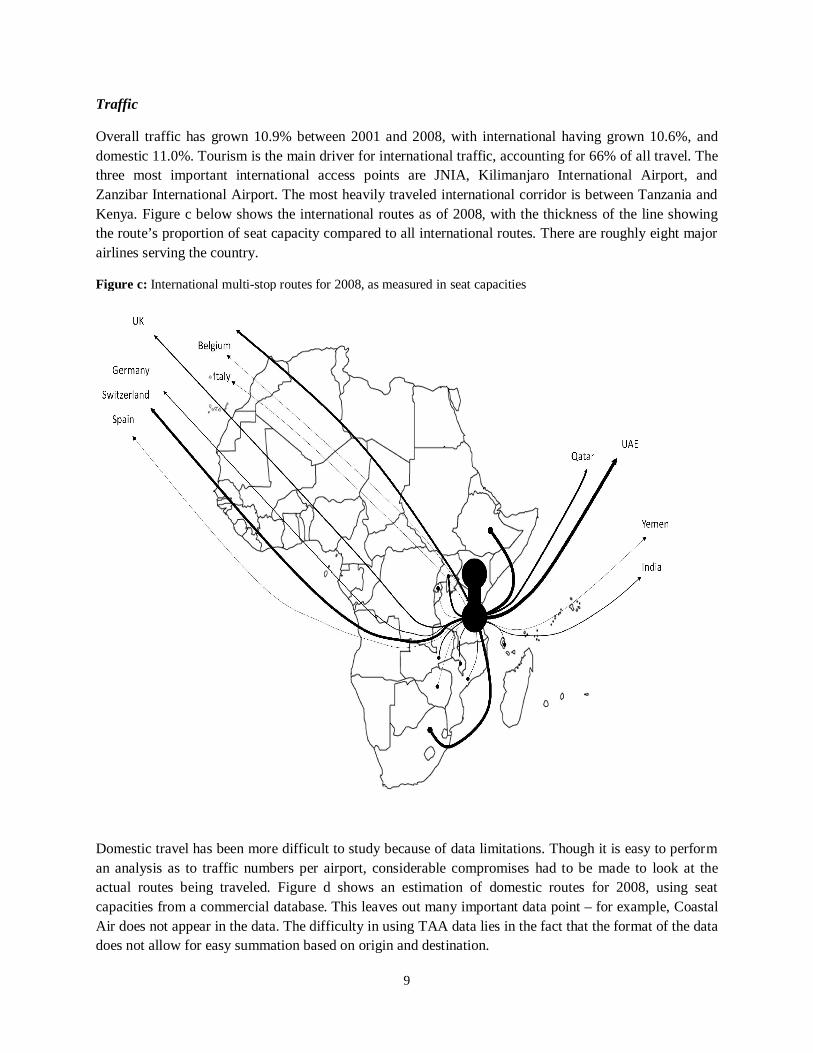

Overall traffic has grown 10.9% between 2001 and 2008, with international having grown 10.6%, and domestic 11.0%. Tourism is the main driver for international traffic, accounting for 66% of all travel. The three most important international access points are JNIA, Kilimanjaro International Airport, and Zanzibar International Airport. The most heavily traveled international corridor is between Tanzania and Kenya. Figure c below shows the international routes as of 2008, with the thickness of the line showing the route’s proportion of seat capacity compared to all international routes. There are roughly eight major airlines serving the country.

Figure c: International multi-stop routes for 2008, as measured in seat capacities

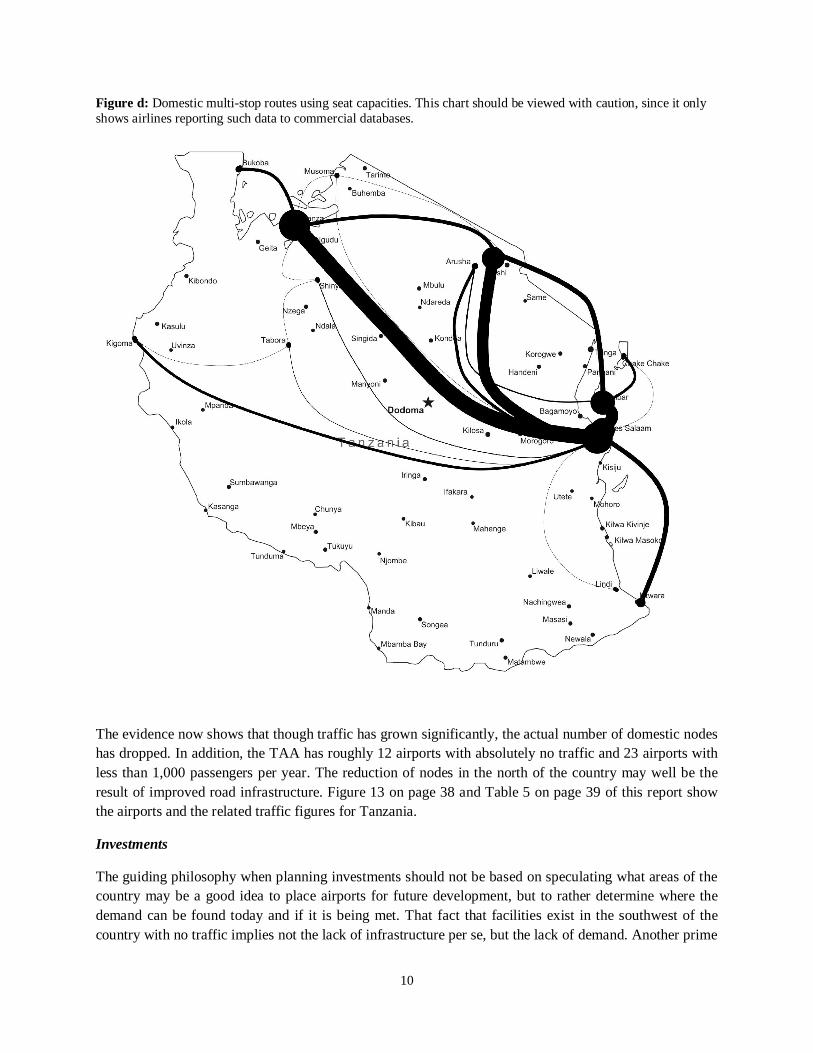

Domestic travel has been more difficult to study because of data limitations. Though it is easy to perform an analysis as to traffic numbers per airport, considerable compromises had to be made to look at the actual routes being traveled. Figure d shows an estimation of domestic routes for 2008, using seat capacities from a commercial database. This leaves out many important data point – for example, Coastal Air does not appear in the data. The difficulty in using TAA data lies in the fact that the format of the data does not allow for easy summation based on origin and destination.

10

Figure d: Domestic multi-stop routes using seat capacities. This chart should be viewed with caution, since it only shows airlines reporting such data to commercial databases.

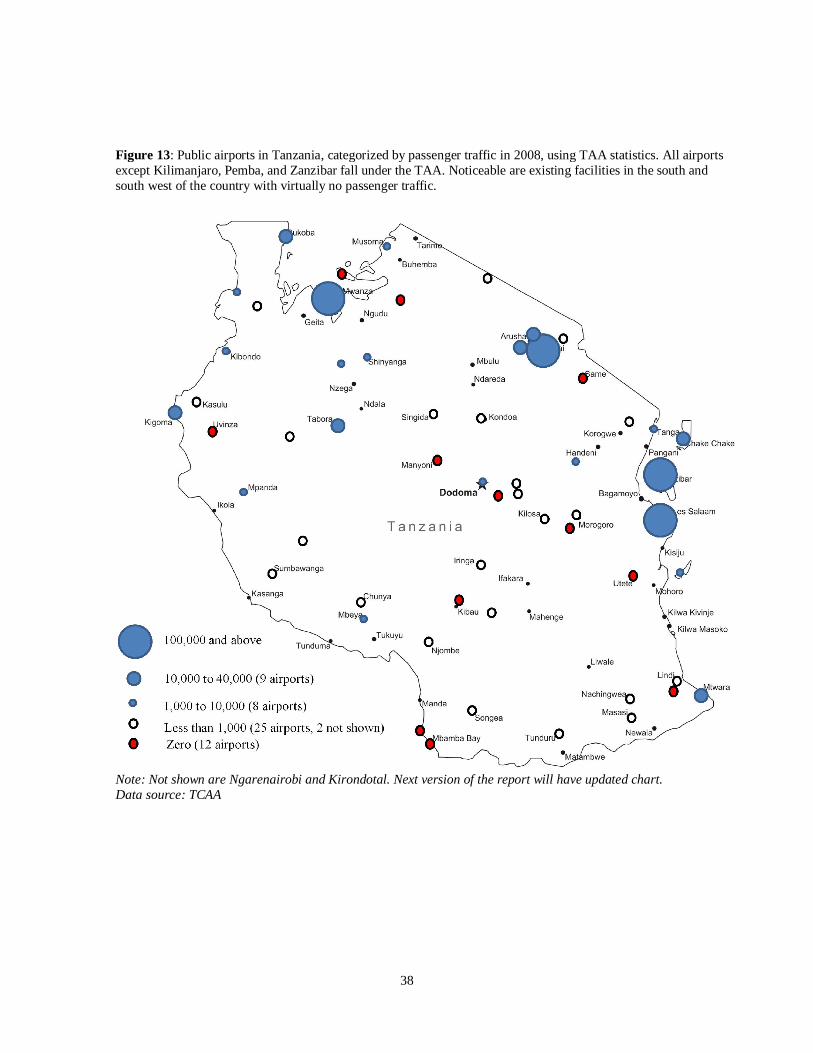

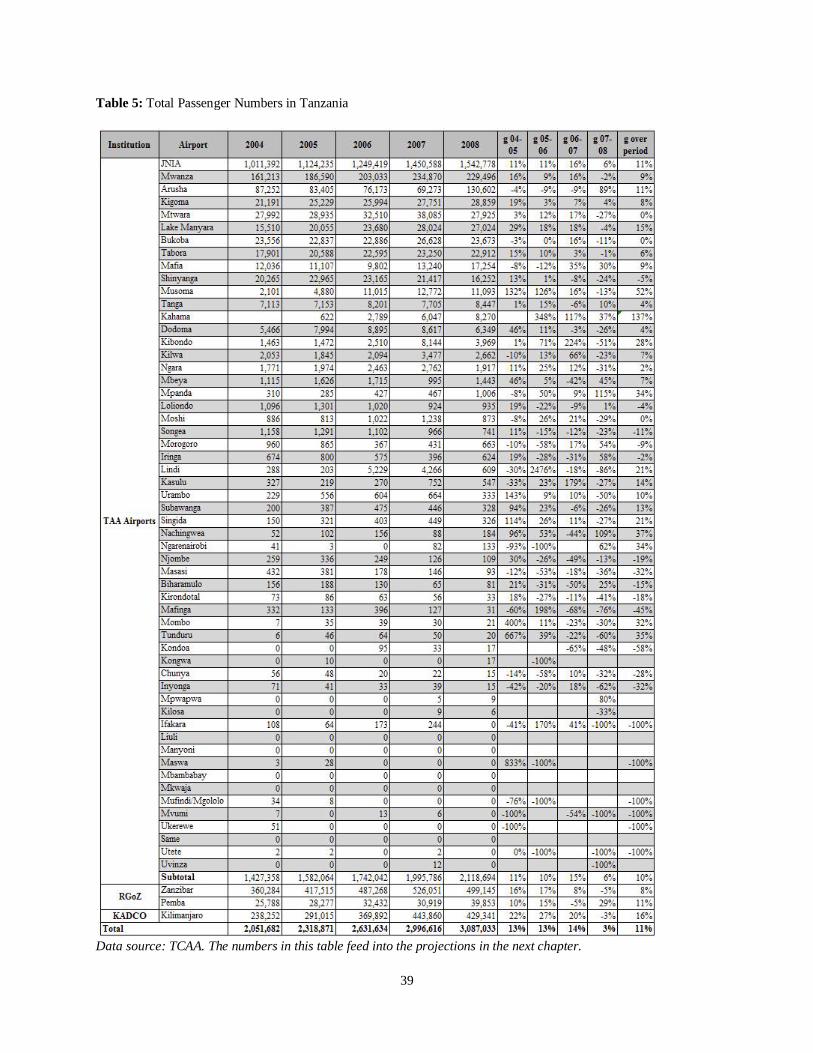

The evidence now shows that though traffic has grown significantly, the actual number of domestic nodes has dropped. In addition, the TAA has roughly 12 airports with absolutely no traffic and 23 airports with less than 1,000 passengers per year. The reduction of nodes in the north of the country may well be the result of improved road infrastructure. Figure 13 on page 38 and Table 5 on page 39 of this report show the airports and the related traffic figures for Tanzania.

Investments

The guiding philosophy when planning investments should not be based on speculating what areas of the country may be a good idea to place airports for future development, but to rather determine where the demand can be found today and if it is being met. That fact that facilities exist in the southwest of the country with no traffic implies not the lack of infrastructure per se, but the lack of demand. Another prime

11

example of this point is a comparison between an airport with an unpaved runway having over 23,000 passengers a year, yet an airport with a paved runway having barely any scheduled services and having 6,000 passengers a year. Bukoba, the unpaved airport, has significant demand. Dodoma, the capital with the paved runway, does not. In terms of looking at extensive hub development in Dar es Salaam, Appendix A found on page 63 discusses the feasibility or even desirability of such plans.

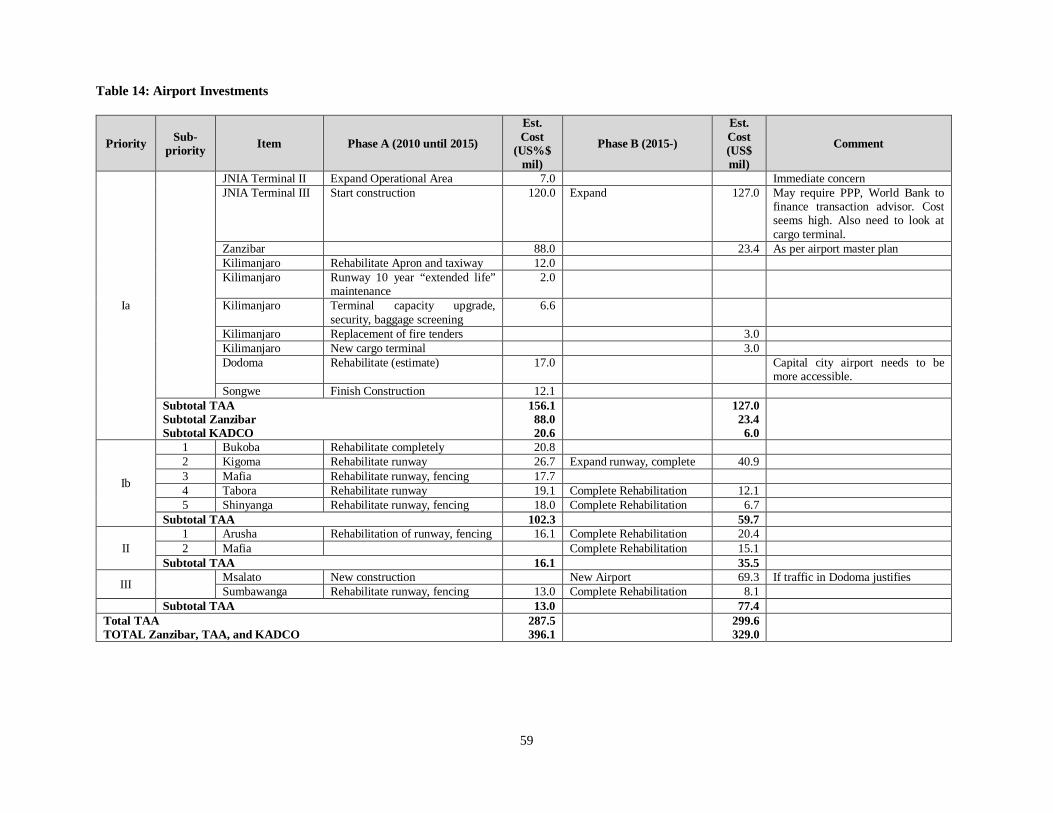

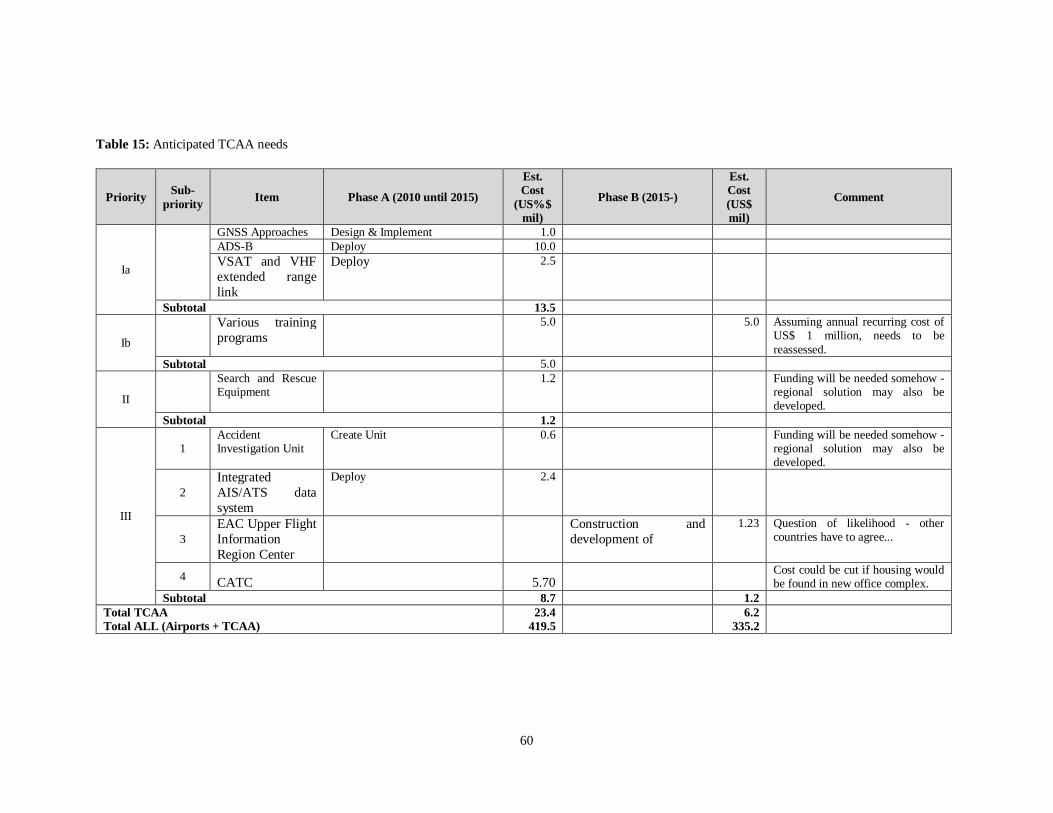

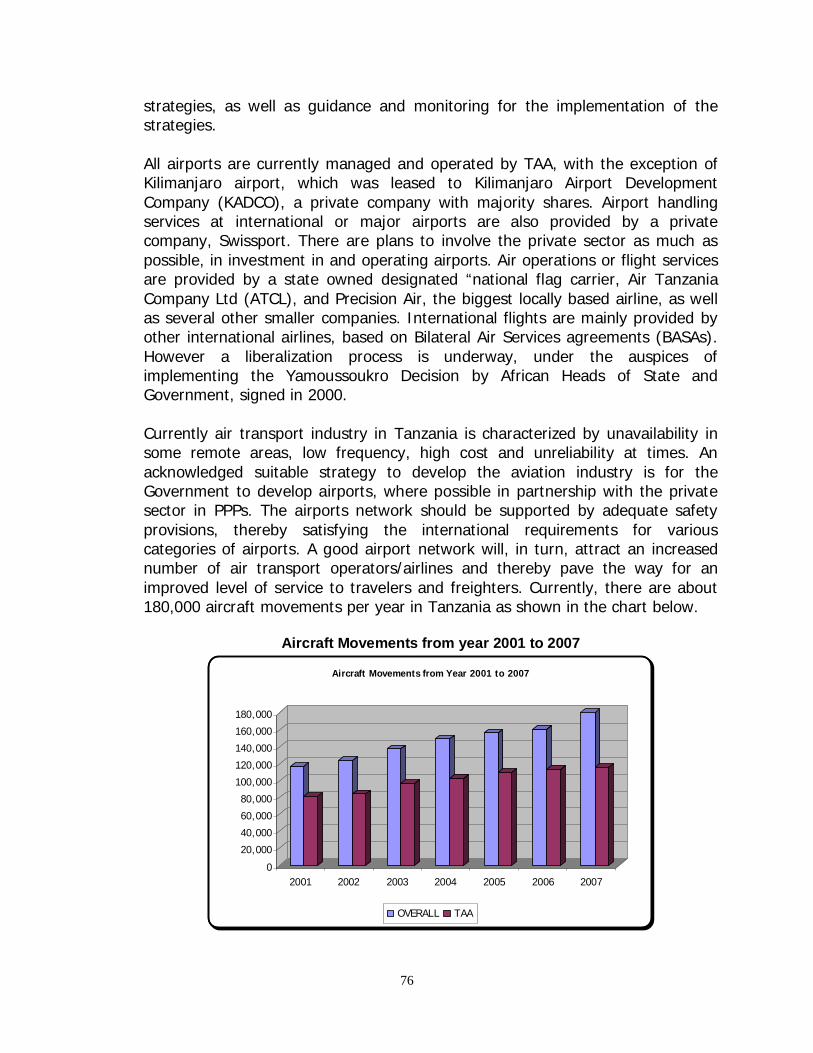

Projections with three scenarios, pessimistic, moderate, and high growth, show that overall system traffic could end being anywhere from 4.5 million passengers to roughly 12 million passengers by 2025, with JNIA’s traffic being anywhere from 2.3 million to over 5.5 million for the same period. These are conservative estimates, with growth rates being kept low anticipating a slower economic recovery and some more pessimistic assumptions on the long-term growth of air transport. They highlight the fact that even with very pessimistic assumptions it is clear that JNIA’s current terminal capacity will be exhausted to the point that expanding the current Terminal 2 will not be enough, and a third terminal needs to go into the planning stages early on. Therefore, the proposed investments in airports ranked in order of priority are outlined as found in Table 14 on page 59, with respective phasing from 2010 to 2015, and 2015 and beyond. The same ranking of proposed investments for the TCAA can be found in Table 15 on page 60.

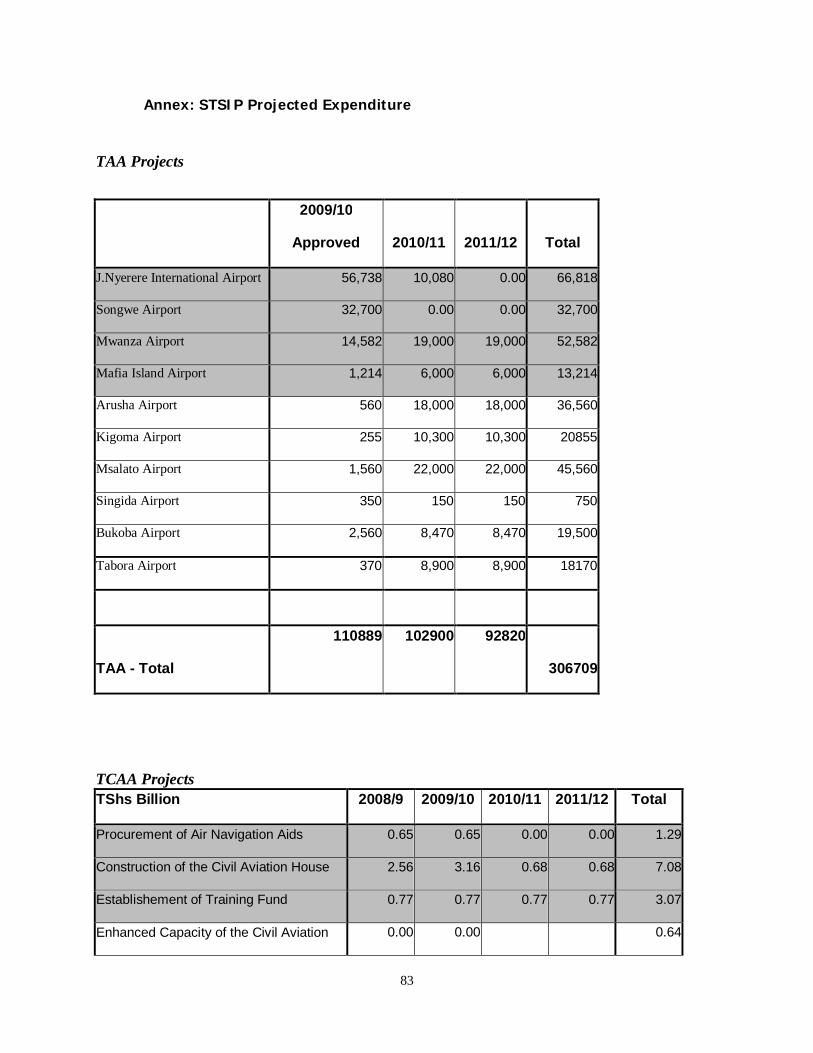

The World Bank is in the final stages of preparing the Transport Sector Support Project that beyond the airport investments in Bukoba, Kigoma, and Tabora found in Table 14 also includes financing a transaction advisor for the expansion of JNIA. As part of this component US$ 600,000 are being set aside for a civil aviation master plan for Tanzania, as well as an airport master plan for JNIA. The proposed outline for the civil aviation master plan can be found starting on 61. The board approval date for the loan is set for late May 2010, which implies that it is therefore timely to begin writing the TORs for such a master plan now (April 2010), so they are ready to be distributed when the studies are ready to be procured.

12

This page intentionally blank

13

I. Country Overview

The air transport sector in Tanzania consists of over 360 airports, two larger carriers, many smaller, usually general aviation (GA) operators, the Tanzania Civil Aviation Authority (TCAA), the Tanzania Airports Authority (TAA), and the airports authority of the Revolutionary Government of Zanzibar. Tanzania has a total of 2251 aircraft, helicopters, and balloons on the registry as of December 2008, and a total of 866 licensed pilots, of which 292 are both commercial and instrument rated. Tanzania is part of the East African Community, and contributes to the newly established EAC Civil Aviation Safety and Security Oversight Agency (CASSOA) in Arusha.

Tanzania is a large country, with a surface area of roughly 947 thousand km2, and a population of about 40 million2. It is bordered by Kenya, Uganda, Rwanda, Burundi, Congo DRC, Zambia, Malawi, and Mozambique. Beyond the mainland, there are three major islands (Pemba, Zanzibar, and Mafia) close to the shoreline on the Indian Ocean. Large bodies of water include Lake Victoria in the north, Lake Tanganyika on the very west along the border to Congo DRC, and Lake Nyasa along the border to Malawi. There are vast areas of thin population in the center and to the west. Dar es Salaam, on the shore of the Indian Ocean, is the business capital and has the highest population, with several other important centers including Arusha (the seat of the East African Community), Dodoma (the capital city), and Mwanza.

Tanzania is a recipient of World Bank IDA loans, and grants and loans from many other donor organizations. Though ranked as a low-income country by the World Bank, there has been significant growth in the years leading up to the global recession of 2008, with increased exports in minerals and tobacco. Tanzania also hosts some of Africa’s most renowned game parks and natural attractions, with the Serengeti and other famous parks (such as the Ngorogoro Crater) located in the African Rift Valley to the boarder of Kenya, and other game parks and potential tourist attractions located throughout the country.

Due to the vastness of the country, and the often lacking infrastructure for other modes, air transport plays a unique role. Much like Alaska in the United States, the rugged terrain and vast nearly empty-spaces have made a network of charter and scheduled small or general aviation aircraft indispensible. Beyond this network, Tanzania is dependent on the same air transport needs as any other larger country – a network for scheduled internal traffic, and international gateways to other countries and continents. Most airports in Tanzania are more in the order of private airstrips operated by mining and tour operators, while the TAA only has 58 of the country’s estimated 3703 airports and strips under its management.

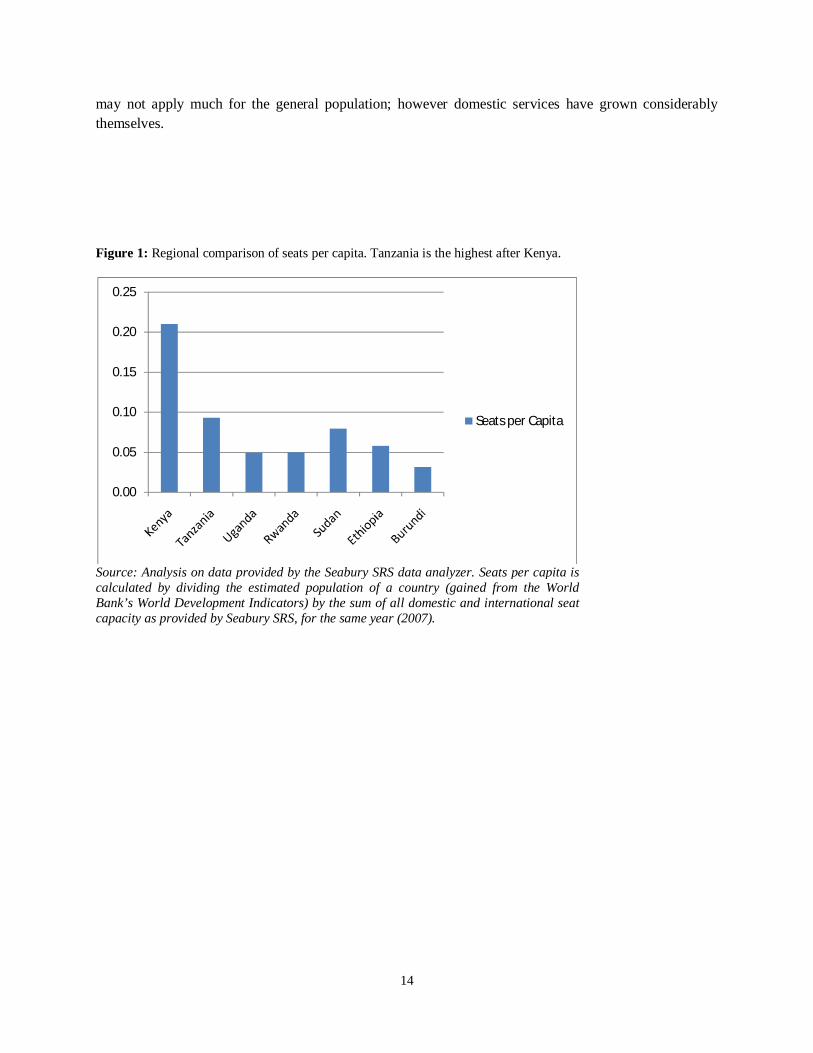

Tanzania’s air transport sector is at a critical stage. Much of the infrastructure is lacking and in dire need of investment. By the same token, the prospect for traffic growth in Tanzania is high in healthy global economic conditions. As shown in the graph below, Tanzania overall has the second highest provision of air transport services per capita, as measured in estimated seats per capita. For international services this 1 Civil Aviation Statistics of Tanzania, 2008, TCAA, p. 13 2 World Bank World Development Indicators 3 The total number of aerodromes on the mainland are 368, with the TAA operating 58 as of March 31, 2010, the Ministry of Wildlife and Natural Resources owns 71, Tanzania National Park 23, mining sector, private hospitals and others for special purposes 215, KADCO 1, and the Revolutionary Government of Zanzibar (not on the mainland) at least 2.

14

may not apply much for the general population; however domestic services have grown considerably themselves.

Figure 1: Regional comparison of seats per capita. Tanzania is the highest after Kenya.

Source: Analysis on data provided by the Seabury SRS data analyzer. Seats per capita is calculated by dividing the estimated population of a country (gained from the World Bank’s World Development Indicators) by the sum of all domestic and international seat capacity as provided by Seabury SRS, for the same year (2007).

0.00

0.05

0.10

0.15

0.20

0.25

Seats per Capita

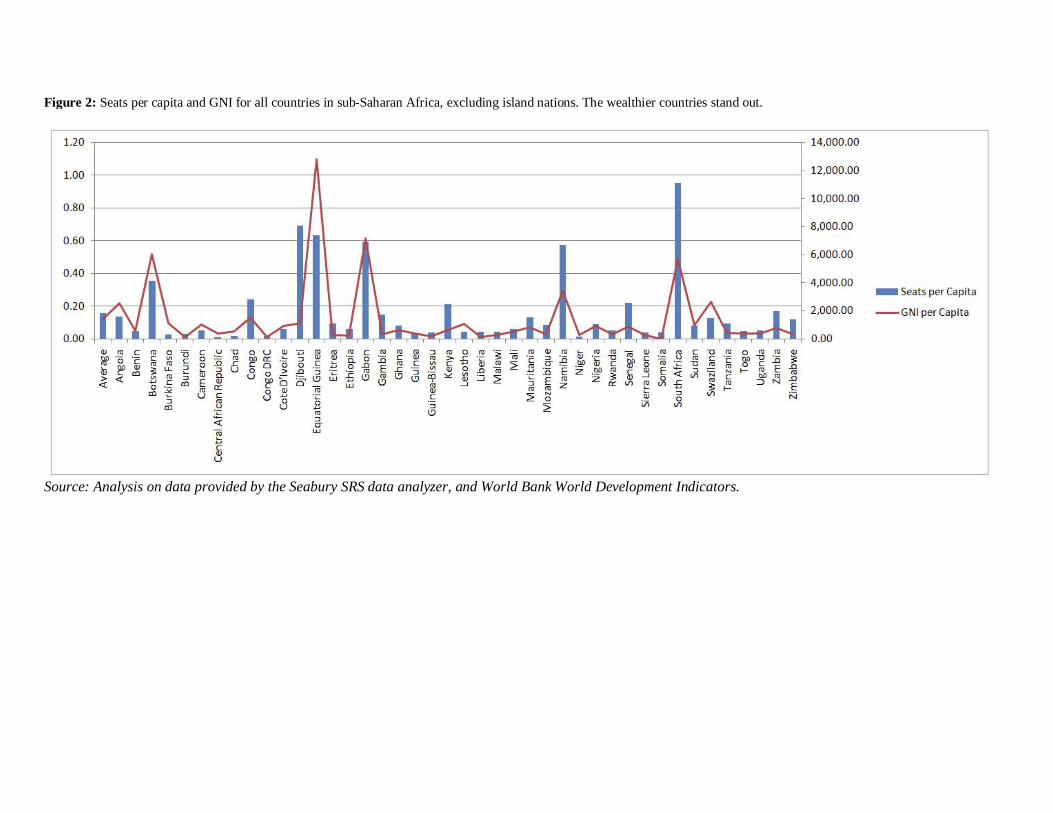

Figure 2: Seats per capita and GNI for all countries in sub-Saharan Africa, excluding island nations. The wealthier countries stand out.

Source: Analysis on data provided by the Seabury SRS data analyzer, and World Bank World Development Indicators.

II. Sector Overview

In the Transport Sector Investment Programme the sector is described as having a set of shortcomings. Specifically mentioned were

Deficiencies in the provision of international air navigation services Inadequate airport facilities Low human reserves to adequately manage and operate the air transport industry Inadequate airport planning and management skills A Civil Aviation Master Plan that is in place but does not accommodate the changes in the policy

framework that have taken place nationally, regionally and internationally Lack of knowledge of the emerging economic regulation concept Inadequate capacity in trained pilots and aircraft maintenance engineers Lack of a management system that will link the civil aviation headquarters and its centers around

the country Manual collection and distribution of aviation data.

The TSIP has identified a total of US$ 303 million as investment needs in the five fiscal years between 2007 and 2012. Other shortcomings in the infrastructure where also found by various consultants visiting the country, which ranged from security installations at major airports such as Mwanza and Zanzibar, to overall weather reporting and prediction capabilities. By the same token Tanzania has seen significant growth in air traffic at rates beyond the rest of the continent.

In this study the proposed investments in both the TAA and the TCAA will be reviewed.

17

1. Institutions and Agencies a. Ministry of Infrastructure Development

The Ministry of Infrastructure Development (MoID) is responsible for coordinating and financing the development Tanzania’s infrastructure. Sectors in its realm include marine, aviation, roads, and others, and its responsibilities include working with the National Assembly of Tanzania in creating budgets and long-term project planning. The ministry is split into divisions and sections. Specific air transport resources can be found in the following divisions and sections:

Transport Division: A dedicated section for Air Transport has two assistant directors, one for air services & meteorology, and one for airports and aerodromes

Policy and Planning Division: One dedicated specialist for air transport (a former Air Tanzania flight captain)

Safety and Environment Division: One dedicated specialist for air transport accidents, who is on loan from the TCAA.

The role of the ministry, in general, is not technical. It’s vital role is to assess policy and budgets. This implies that in terms of technical resources the MoID relies less on internal resources and more on the agencies reporting to it – the TAA, TCAA, and Air Tanzania. However, the MoID does have the final authority on many investments and expenditures, and as such does require expertise as to what larger investments are appropriate for an agency to accomplish its tasks. In this role there is still room for the agency to develop its capacities.

Safety and Environment Division A significant exception to the technical needs lies in the Safety and Environment Division. ICAO, in its recent updating of safety audits standards, is now insisting that the relevant ministries be the final oversight agency of the regulator. Therefore ICAO recommends that air transport accidents be investigated outside the regulating agency, in this case the TCAA. The new formation of the Safety and Environment Division, and its new role in air traffic investigations, is therefore structurally a sound implementation of the ICAO recommendations.

However, the division has no budget for a permanent investigator. The qualified accident investigator now reporting to the division is on loan from the TCAA, and being paid out of the TCAA’s funds. Though this arrangement is understandable in current circumstances, long term planning should focus on giving the division one permanent investigator, who, through building channels with regional and global resources, is able to implement an investigation team rapidly in the case of an accident.

18

b. TCAA

The Tanzania Civil Aviation Authority (TCAA) was an executive agency formed 1999, and became a corporate body in November 2003. In the process of becoming independent, the staffing was optimized, and the agency has gone from a total of roughly 400 employees to the neighborhood of 140. The agency has been growing again as it assumes additional functions in oversight, such as economic regulation of domestic markets.

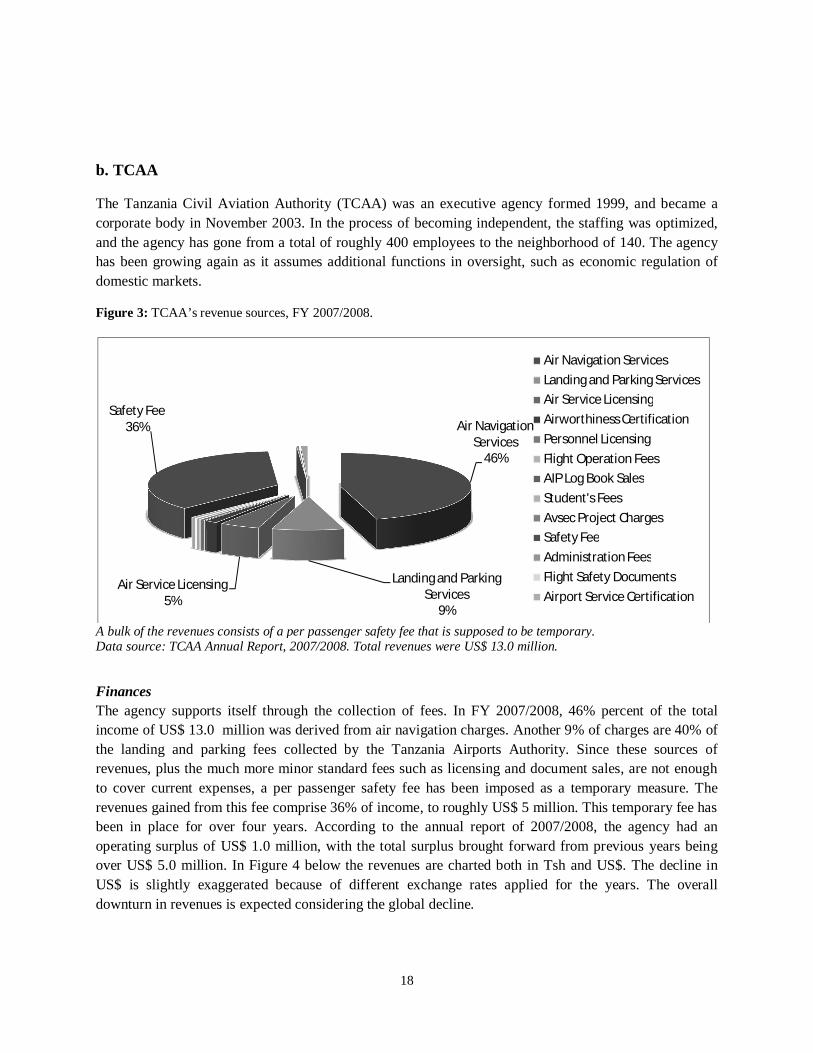

Figure 3: TCAA’s revenue sources, FY 2007/2008.

A bulk of the revenues consists of a per passenger safety fee that is supposed to be temporary. Data source: TCAA Annual Report, 2007/2008. Total revenues were US$ 13.0 million.

Finances The agency supports itself through the collection of fees. In FY 2007/2008, 46% percent of the total income of US$ 13.0 million was derived from air navigation charges. Another 9% of charges are 40% of the landing and parking fees collected by the Tanzania Airports Authority. Since these sources of revenues, plus the much more minor standard fees such as licensing and document sales, are not enough to cover current expenses, a per passenger safety fee has been imposed as a temporary measure. The revenues gained from this fee comprise 36% of income, to roughly US$ 5 million. This temporary fee has been in place for over four years. According to the annual report of 2007/2008, the agency had an operating surplus of US$ 1.0 million, with the total surplus brought forward from previous years being over US$ 5.0 million. In Figure 4 below the revenues are charted both in Tsh and US$. The decline in US$ is slightly exaggerated because of different exchange rates applied for the years. The overall downturn in revenues is expected considering the global decline.

Air Navigation Services

46%

Landing and Parking Services

9%

Air Service Licensing5%

Safety Fee36%

Air Navigation ServicesLanding and Parking ServicesAir Service LicensingAirworthiness CertificationPersonnel LicensingFlight Operation FeesAIP Log Book SalesStudent's FeesAvsec Project ChargesSafety FeeAdministration FeesFlight Safety DocumentsAirport Service Certification

19

Some of the revenue streams at times prompt complaints from some operators who wish to see a cap or reduction of charges and fees. The surpluses accumulated would indicate that the TCAA could ease charges on the sector; however new commitments made by the authority are most likely going to require the safety fees to become permanent, and maybe even be raised.

The TCAA is currently housed mainly in the IPS Building in downtown Dar es Salaam. While the entire authority is not housed here, the bulk of the TCAA resides in these offices. The authority quoted a figure of US$ 168,000 rent per annum for 2009. The November 2008 ICAO safety audit findings mention the current split in the office space as an issue needing corrective action. Combined offices are needed for the TCAA.

The TCAA has planned ahead and is scheduled to move to new offices by middle of calendar year 2010. A new office building is being constructed on a site by the airport, with an estimated cost of US$ 12 million. The concrete structure is nearing completion, waiting for interior and exterior finishing.

Since this building is being built by the TCAA, the construction required the TCAA to assume a commercial loan of US$ 6.5 million, with a five year repayment period and a three year grace period. With a fixed interest rate of 7.0 %, this would translate to over US$ 118,807 a month. The servicing of the loan is estimated to cost US$ 1.4 million a year, roughly 8 percent of total operating revenues, and being in the range of the landing and parking charges allocated to the authority.

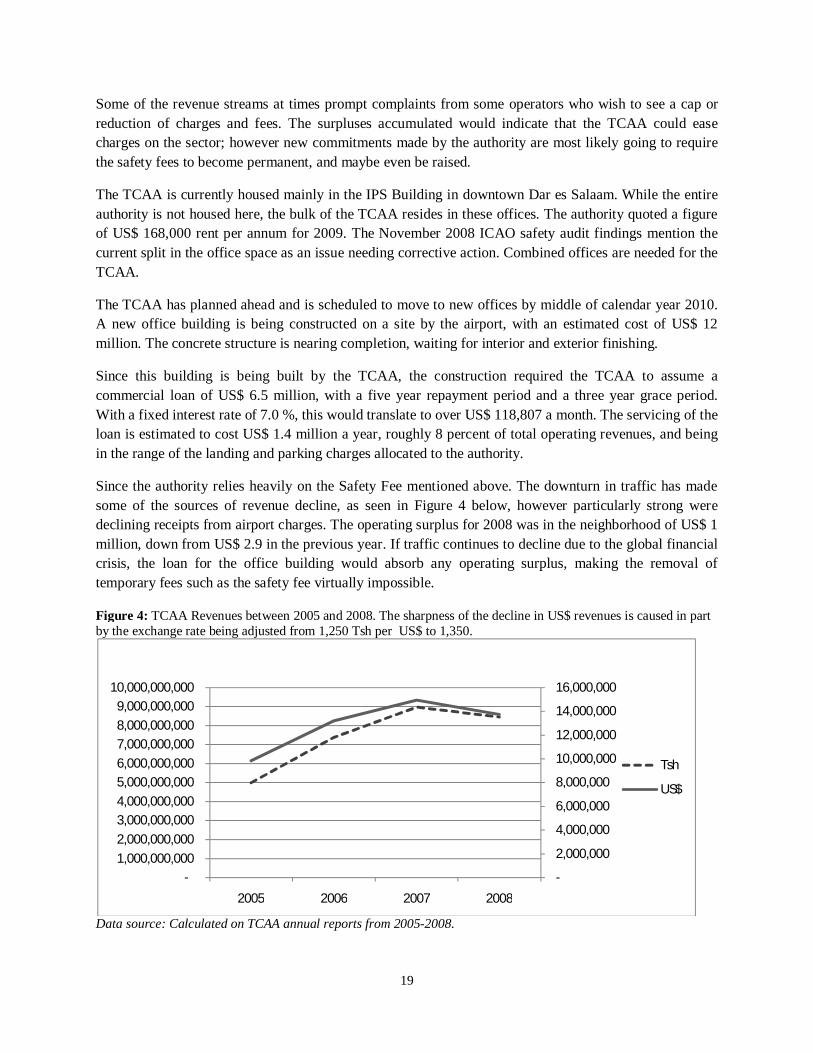

Since the authority relies heavily on the Safety Fee mentioned above. The downturn in traffic has made some of the sources of revenue decline, as seen in Figure 4 below, however particularly strong were declining receipts from airport charges. The operating surplus for 2008 was in the neighborhood of US$ 1 million, down from US$ 2.9 in the previous year. If traffic continues to decline due to the global financial crisis, the loan for the office building would absorb any operating surplus, making the removal of temporary fees such as the safety fee virtually impossible.

Figure 4: TCAA Revenues between 2005 and 2008. The sharpness of the decline in US$ revenues is caused in part by the exchange rate being adjusted from 1,250 Tsh per US$ to 1,350.

Data source: Calculated on TCAA annual reports from 2005-2008.

-

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

12,000,000

14,000,000

16,000,000

-1,000,000,000 2,000,000,000 3,000,000,000 4,000,000,000 5,000,000,000 6,000,000,000 7,000,000,000 8,000,000,000 9,000,000,000

10,000,000,000

2005 2006 2007 2008

Tsh

US$

20

This in general implies that the TCAA will need to re-assess its overall finances, and will need to do some additional planning for the next five years. It may be that the property being developed could be sold for other purposes to the private sector, or that the space inside be allocated in a way that the majority of the building is rented out and produces revenues.

Services The TCAA is the country’s service provider in air traffic control. Tanzania has one civilian radar stationed at JNIA, providing both primary and secondary coverage4 for up to 220 nautical miles. Though the radar had been purchased in 2001, radar based air traffic control, as opposed to procedural control, is just starting due to the difficulty of getting enough air traffic controllers to be certified in radar procedures. Air traffic control over the rest of the country outside the range of the radar is purely procedural. Tanzania is not unique in this: In Kenya, where radar coverage is above 90% for the country, radar procedures are in place only in Nairobi, and are used sporadically depending on weather in Mombasa5.

As part of upgrading and expanding the air traffic control system in Tanzania, one option proposed has been the implementation of ADS-B, a reporting system that uses GPS receivers within aircraft to pinpoint the location of the aircraft, and interconnected ground-based transceivers to received aircraft position reports and transfer these to the air traffic control system. Such a system is far more accurate over longer distances than radar, and considerably less expensive.

The implementation of ADS-B also has a regional element: Kenya, Uganda, Rwanda, and Burundi are also considering this technology, and a common platform would allow the regional integration of the upper airspace. Plans for unifying the upper airspace for the EAC, and also for SADC members, have recently been openly discussed.

Overflights over Tanzania’s airspace (referred to as the Dar-es-Salaam flight information region, or DAR FIR) number roughly 65 thousand in 2008, and have been increasing because of growth in Qatar and Kenyan airways flights6. The overflights represent an important source of revenues. ICAO, however, insists that overflight charges should not be seen as a cash cow, and that charges should be applied as to cover the costs of the service being provided. The reality is that with poorer countries this imperative simply cannot be followed. However, Tanzania could further justify its revenue from these overflights by increasing the level of air traffic control services being offered. This argument also supports the longer-term notion of implementing ADS-B.

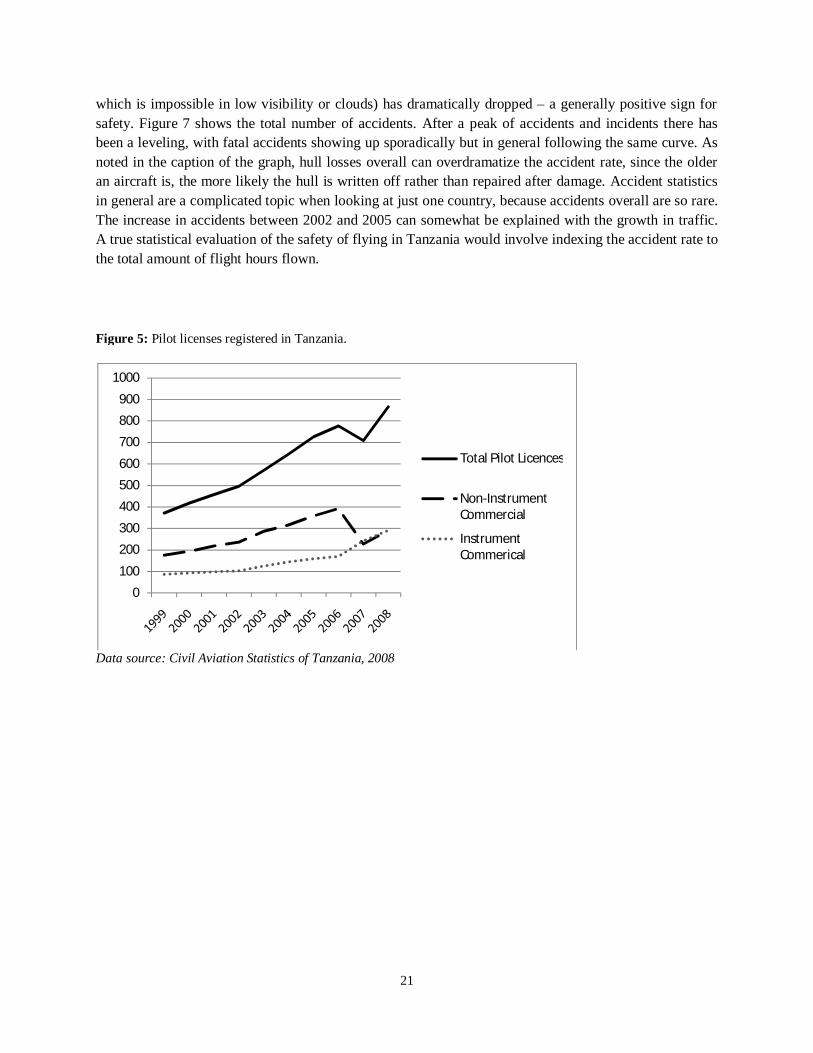

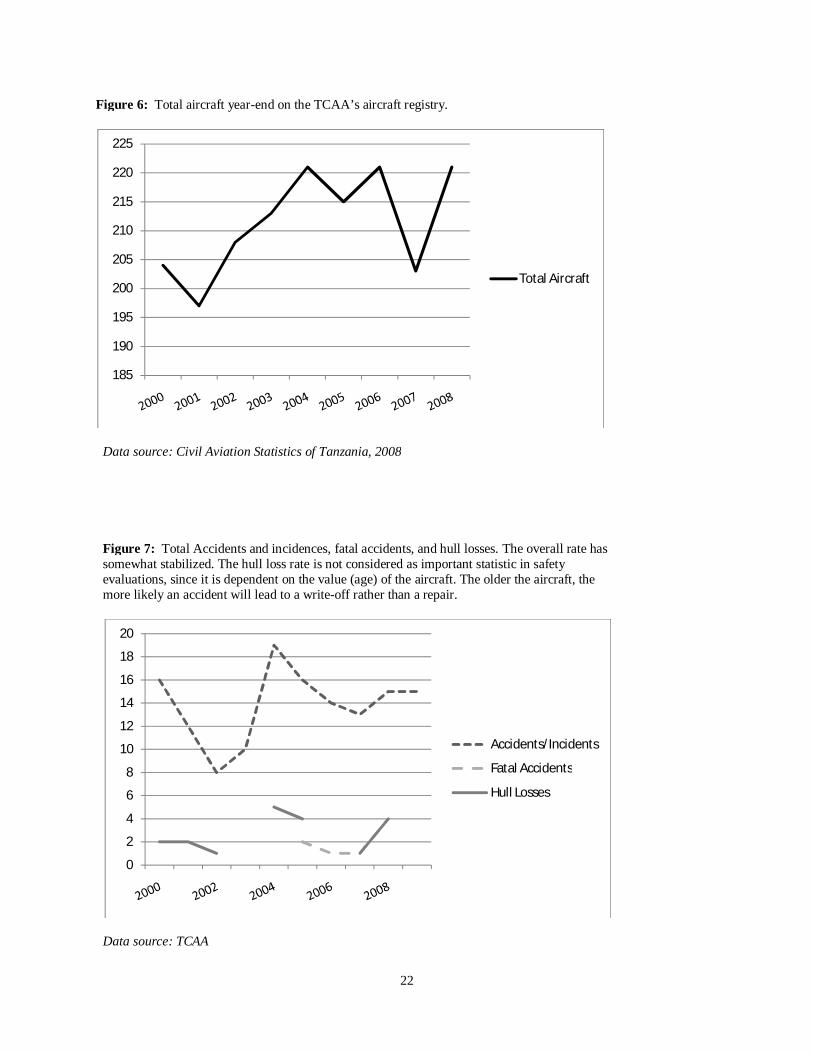

Figure 5, Figure 6, and Figure 7 below reflect some general statistics for the TCAA. Figure 5 shows the total number of pilot licenses in Tanzania. The interesting movements are between 2006 and 2007: The number of commercial pilots without an instrument rating (i.e. only able to fly looking out the window,

4 Primary coverage includes being able to view generally all flying man-made objects within an area, whereas secondary radar provides much more detail for aircraft equipped with transponders. Secondary radar is generally the standard used for air traffic control. 5 In clear weather, separation between approaching aircraft could be done visually. In clouds, however, pilots have to rely solely on the controller’s knowledge of nearby traffic, making radar more necessary. 6 Civil Aviation Statistics of Tanzania 2008, TCAA, p. vii.

21

which is impossible in low visibility or clouds) has dramatically dropped – a generally positive sign for safety. Figure 7 shows the total number of accidents. After a peak of accidents and incidents there has been a leveling, with fatal accidents showing up sporadically but in general following the same curve. As noted in the caption of the graph, hull losses overall can overdramatize the accident rate, since the older an aircraft is, the more likely the hull is written off rather than repaired after damage. Accident statistics in general are a complicated topic when looking at just one country, because accidents overall are so rare. The increase in accidents between 2002 and 2005 can somewhat be explained with the growth in traffic. A true statistical evaluation of the safety of flying in Tanzania would involve indexing the accident rate to the total amount of flight hours flown.

Figure 5: Pilot licenses registered in Tanzania.

Data source: Civil Aviation Statistics of Tanzania, 2008

0

100

200

300

400

500

600

700

800

900

1000

Total Pilot Licences

Non-Instrument Commercial

Instrument Commerical

22

Figure 6: Total aircraft year-end on the TCAA’s aircraft registry.

Data source: Civil Aviation Statistics of Tanzania, 2008

Figure 7: Total Accidents and incidences, fatal accidents, and hull losses. The overall rate has somewhat stabilized. The hull loss rate is not considered as important statistic in safety evaluations, since it is dependent on the value (age) of the aircraft. The older the aircraft, the more likely an accident will lead to a write-off rather than a repair.

Data source: TCAA

185

190

195

200

205

210

215

220

225

Total Aircraft

0

2

4

6

8

10

12

14

16

18

20

Accidents/Incidents

Fatal Accidents

Hull Losses

23

c. TAA

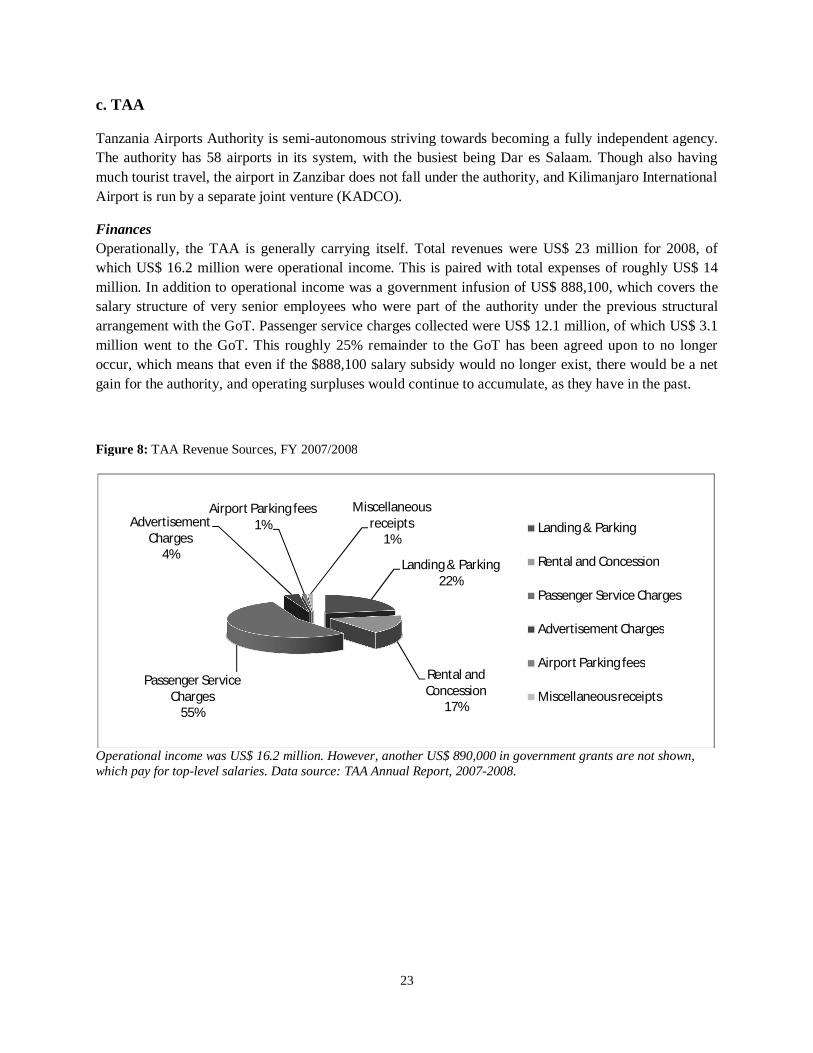

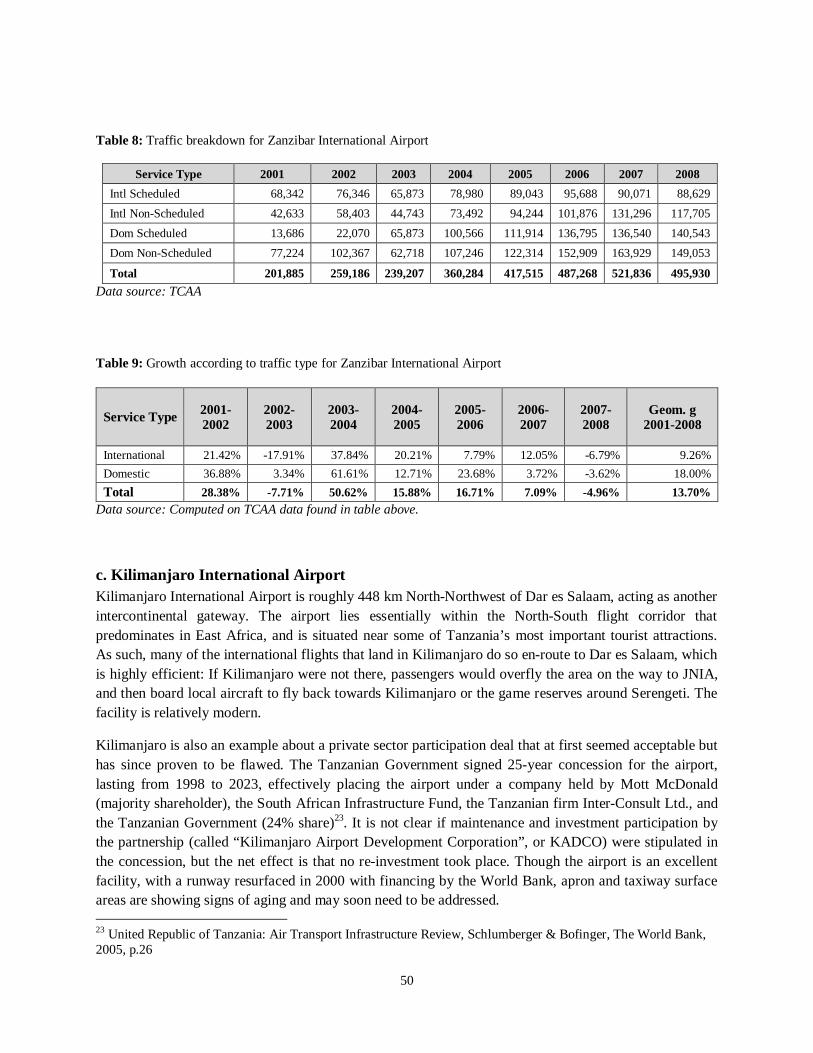

Tanzania Airports Authority is semi-autonomous striving towards becoming a fully independent agency. The authority has 58 airports in its system, with the busiest being Dar es Salaam. Though also having much tourist travel, the airport in Zanzibar does not fall under the authority, and Kilimanjaro International Airport is run by a separate joint venture (KADCO).

Finances Operationally, the TAA is generally carrying itself. Total revenues were US$ 23 million for 2008, of which US$ 16.2 million were operational income. This is paired with total expenses of roughly US$ 14 million. In addition to operational income was a government infusion of US$ 888,100, which covers the salary structure of very senior employees who were part of the authority under the previous structural arrangement with the GoT. Passenger service charges collected were US$ 12.1 million, of which US$ 3.1 million went to the GoT. This roughly 25% remainder to the GoT has been agreed upon to no longer occur, which means that even if the $888,100 salary subsidy would no longer exist, there would be a net gain for the authority, and operating surpluses would continue to accumulate, as they have in the past.

Figure 8: TAA Revenue Sources, FY 2007/2008

Operational income was US$ 16.2 million. However, another US$ 890,000 in government grants are not shown, which pay for top-level salaries. Data source: TAA Annual Report, 2007-2008.

Landing & Parking22%

Rental and Concession

17%

Passenger Service Charges

55%

Advertisement Charges

4%

Airport Parking fees1%

Miscellaneous receipts

1%Landing & Parking

Rental and Concession

Passenger Service Charges

Advertisement Charges

Airport Parking fees

Miscellaneous receipts

24

In terms of the capital structure, the Authority is heavily dependent on government and donor infusions for improvements or heavier-duty maintenance to its airports. Under its current income structure, the TAA has reported to be capable to raise between US$ 12 million to US$ 22 million with commercial banks, with this amount having risen as operational surpluses have accumulated. However, these amounts are marginal if compared to the overall need for infrastructure investment in the airport sector in Tanzania, demonstrating the need for larger partners to help finance development.

The debt for airport projects does not show in the balance sheets of the authority. Upon further inquiry, it was determined that the GoT itself carries the debt for airport improvements, and that the TAA makes payments on this debt from funds received from the GoT. Payments for these debts amounted to roughly US$ 6 million for 2007/2008. In this sense, the TAA infrastructure is clearly subsidized, and so far capital investments and their repayments have had no significant impact on the TAA’s finances.

Services The TAA has provided concessions for the handling of passenger and cargo at JNIA and Mwanza. Since both Kilimanjaro International and Zanzibar International airports are not in the realm of the TAA, these two airports carry the TAA’s highest volume (84% of TAA’s system), with the rest being a very distant 16% of volume spread over 57 airports. In general, most services consist of facilities maintenance such as upkeep of buildings and air-side pavements and other surfaces (in 2008, grass cutting for all airfields accumulated to an annual expense of US$ 428,000), and airport planning. The TAA is an authority more focused on the necessary infrastructure upkeep and concessioning of essential terminal services, whereas the TCAA provides lighter infrastructure (limited to ATC and navigation systems) and more direct services in terms of oversight, information dissemination, training, navigation, and air traffic control.

25

2. Service Providers There are three general types of service providers in Tanzania. On the scheduled side, within Tanzania there is the nationally owned flag carrier, Air Tanzania, and Precision Air, a carrier privately held with Kenyan Airways as a partial shareholder. A second level of carrier also abounds in Tanzania, with the prime example being Coastal Air. Operating officially as charter carriers, these carriers actually also provide scheduled service, and in Coastal's case actually have a broad and expansive network within the country, essentially flying the same routes as the bigger carriers, but with smaller aircraft and at times (such as between Dar es Salaam and Zanzibar) at much higher frequencies. The third type of carrier is the pure charter operator, of which there are many. It is important to note that the unscheduled carriers and the hybrid charter operators provide a larger chunk of the domestic services than one might expect. For example, Coastal alone has about a 30% market share for all domestic services flying out of Dar es Salaam, which is significant considering that the biggest route, between Mwanza and Dar es Salaam, is also served by the Precision Air and Air Tanzania, both of whom fly larger aircraft, though Air Tanzania’s 737-200 had an unfortunate accident in March 2010 and will be in repairs for some time.

Service providers come and go over time, so it is difficult to make long-term projections as to who will be carrying far into the future. However, the troubles of Air Tanzania play an important role in the overall role of the service providers.

Air Tanzania The last iteration of Air Tanzania was 49% owned by South African Airlines, having been launched in March 2003. The partnership did not end well, and was dissolved by March 2006, after having lost a total of nearly US$ 20 million, with the airline once again being 100% government owned, as a separate agency to the Ministry of Infrastructure Development7. What followed was a subsequent decline in the fleet, and corresponding less frequencies. The overall decline of the airline including even the period before South African's involvement, coupled with the demand for growth and a more open policy of allowing other players to provide service, ended up being a boost for Precision Air, which subsequently became the dominant domestic carrier. Precision Air renewed its turbine fleet with new ATR aircraft from France, and eventually started jet service between destinations such as Nairobi and Dar es Salaam.

Today the climate in Tanzania towards service providers from the outside for international service may well yield towards liberalization as stipulated in the Yamoussoukro decision; however there are serious considerations for economic regulation of domestic services, with the argument that Precision Air is now monopolizing domestic routes, and a government-owned flag carrier is needed to provide competition and make sure thin routes do not get dropped out of the network. There is also ample evidence, however, that private carriers are interested in establishing themselves in Tanzania, as some smaller start-ups are now showing.

Weak state-owned flag carriers become a significant financial drain for their government. With Air Tanzania this came to a high point towards the end of 2008: As ICAO performed its audit of the safety oversight system in Tanzania, the lack of technical documents (manuals) for the aircraft being operated was discovered. The TCAA had no option but to ground the airline until remedies were in place.

7 See http://www.infrastructure.go.tz/index.php/ministry/category/ministry_departments/

26

However, since the purchase of the technical documentation, in the end, came out of the GoT’s pocket, the TCAA, even though representing the enforcement side of the safety oversight, also had to financially participate in the remedy. This leads to a troubling conflict of interest: If a regulator is forced to contribute to the cost of the remedy of a standards violation, it is in the regulator's self interest not to enforce all applicable safety standards.

The future of Air Tanzania should be more carefully examined. The airline currently operates two Dash-8s, purchased with the assistance of Sonangol, and one 737-200 that unfortunately has a mishap in early 2010, and now in need of repairs. In addition, it has now leased an Airbus 320, with monthly lease costs of over US$ 350,000. This fleet composition presents several problems:

The Airbus is not really economically usable for current routes other than Dar – Johannesburg. The Airbus does not fit in well with the fleet mix. Having many different types of aircraft

increases operating costs and the general logistics of flying, since generally pilots get trained on and certified on only on type of transport aircraft at a time. On the other hand, having several aircraft of the same type increases flexibility and serviceability. Another Boeing 737-200 would have been more suitable.

The Airbus, though lease payments have been made for at least two years, is not flying, since extensive maintenance is being performed.

Currently, Air Tanzania has transport pilots on its payroll that are not flying, certified for the Boeing 737. The Airbus will require a resource shift in flying skills, while not taking advantage of already existing capacity being paid for.

The string of mishaps and financial losses are typical for a small nationally owned flag carrier that should actually be closed down. Though this is a strongly worded recommendation, there are several reasons for stating this:

Attempting to find a private sector investor to take over the airline plays into an ever repeating vicious cycle of trying to make the airline more attractive while investing (and losing) more and more money. In small African airlines the losses run into the tens of millions US$, in large carriers such as found in South East Asia losses above US$ 600 million have been experienced in one year alone for one carrier, all in the efforts to privatize the airlines, with failed outcomes. In some cases these efforts have lasted over at least a decade.

Keeping the airline as is brings about significant market distortions. For example, it is typical for small nationally owned carriers not to pay their parking and landing fees, creating large accounts payable balances at domestic airports that can never be collected, and in effect crowding out those that do have to pay. In addition, these mechanisms also impeded the efficient setting of fares: The nationally owned flag carrier actually has an advantage in setting fares because it does not have to compensate for all of its true economic cost of operating.

Following the previous point, private sector carriers can never trust the government and the regulator if they are in the same business, competing with them. This may be keeping new entrants from entering the market.

Government-owned flag carriers can attract substantial governance issues. Not only are there large risks that some passengers will never fly as revenue passengers, but investment, leasing, and

27

acquisition decisions may not be done on a sound business or economic basis, and offer opportunities for governance to go awry.

Text Box: Flag carriers—a pattern in attempting privatization8 Not only in Africa but in much of the developing world, the national flag carrier plays a visible role, though one whose economics are often questionable. In most cases, the state-owned and operated flag carrier was established decades ago. The carrier grows at first, partly because of market protection—competition is prohibited on some or all of its routes. Over time, service quality declines and losses mount, until a change in government forces a rethinking of policy. Proponents of maintaining the carrier argue as follows: (i) without it, little-traveled, subsidized domestic routes would be dropped, creating regional isolation; (ii) the carrier can potentially create revenues for the government, especially from foreigners traveling within the country; and (iii) a flag carrier must be maintained as a matter of national pride.

As losses mount, though, advisers recommend the sale of the airline. To attract potential private sector buyers, the airline must first be restructured and made viable. During that process, the carrier realizes that routes are only profitable if it remains a state-sanctioned monopoly and that its aircraft in use do not really meet the demands of the public. In addition, the carrier identifies new potential routes for expansion.

With additional investment from the government, the carrier buys new aircraft and brings new routes into service, while maintaining its monopoly on current routes. Over time, it becomes apparent that the new aircraft are too expensive to operate and have a load factor too low to be profitable on the routes for which they were bought (incurring losses of staggering proportions). The private sector is even less interested in the airline as a result of the restructuring. Barring liquidation, the process will start all over again.

Generally, the best solution is to completely liquidate the carrier and have a successful outside operator provide international services. A flag carrier from another country could potentially play this role. Compromises could be made, such as painting the outside operator’s aircraft in the flag carrier’s colors and hiring crew for passenger services within the country. For domestic routes, it makes sense to let small, local operators develop from the private sector.

8 Adapted from Bofinger, Heinrich, An Unsteady Course: Growth and Challenges in Africa’s Air Transport Industry, Pre-Release Edition, Africa Infrastructure Diagnostic, the World Bank, p.7

28

III. Traffic Overview Tanzania's total traffic per airport is summarized in Table 5 at the end of this chapter, using mostly TAA data. Using TCAA data dating back to 2001, overall traffic has grown 10.9% between 2001 and 2008, with international having grown 10.6%, and domestic 11.0%. Beyond the airports of the TAA, there are also Kilimanjaro, Pemba, and Zanzibar. The total system throughput in 2008 was 3.09 million passengers9, with an annual geometric growth rate of 11 % between 2004 and 2008, higher than the industry average globally of 5-6 percent during the same period10. The traffic measured is passenger traffic as reported by the TAA, and the TCAA with respect to Pemba and Zanzibar. Kilimanjaro, notably, had grown at rates above 20% between 2004 and 2007, only to have its overall growth rate decline to 16% after registering an actual decline between 2007 and 2008. Also of note are the number of airports in the system with very little or no passenger traffic at all.

1. International Travel Tanzania currently has roughly ten major airlines providing international service into three airports, Julius Nyerere International Airport in Dar es Salaam, Zanzibar International Airport on the island of Zanzibar, and Kilimanjaro International Airport in the Kilimanjaro region. By far the most important airport is the international airport in Dar es Salaam, though Kilimanjaro has been growing rapidly.

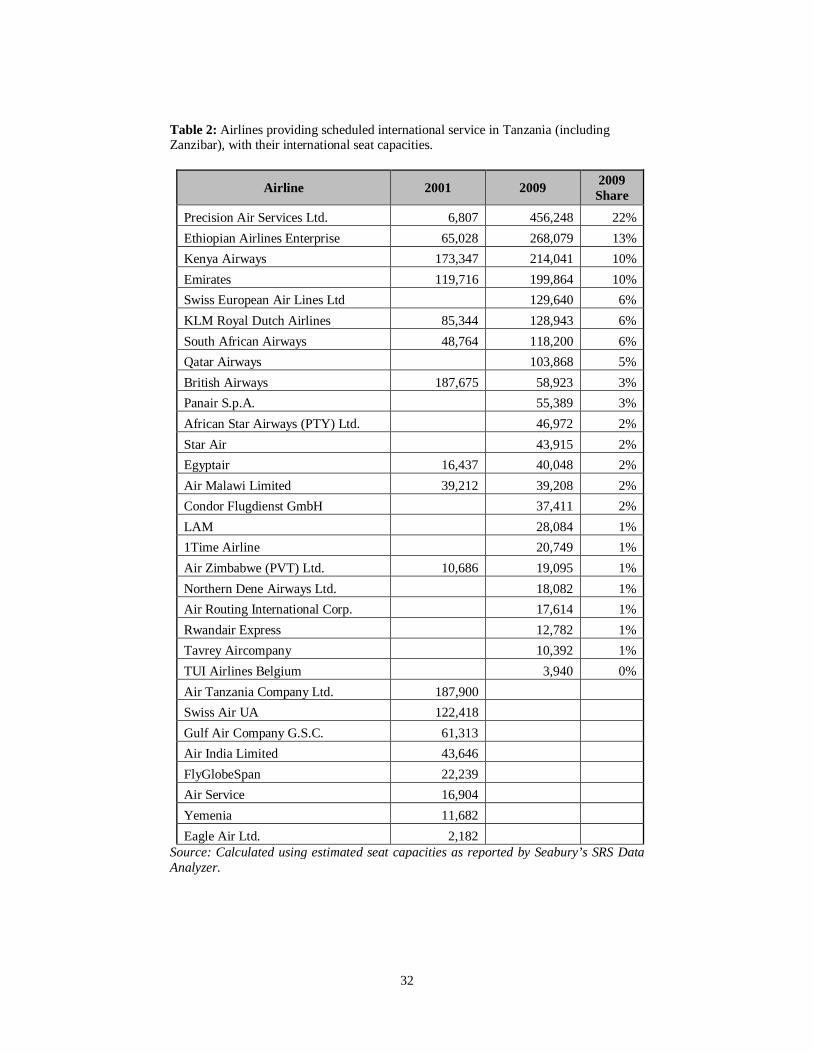

Tourism accounts for a large chunk of passenger traffic arriving internationally, with the game reserves in the north and Zanzibar being major attractions. An estimated 66.8 of all arrivals are tourism related11. By far the strongest route is between Kenya and Tanzania, since Nairobi is one of the three import air transport hubs in Sub-Saharan Africa. Table 2 shows a breakdown of airlines with their respective market share for 2008, using capacity estimates.

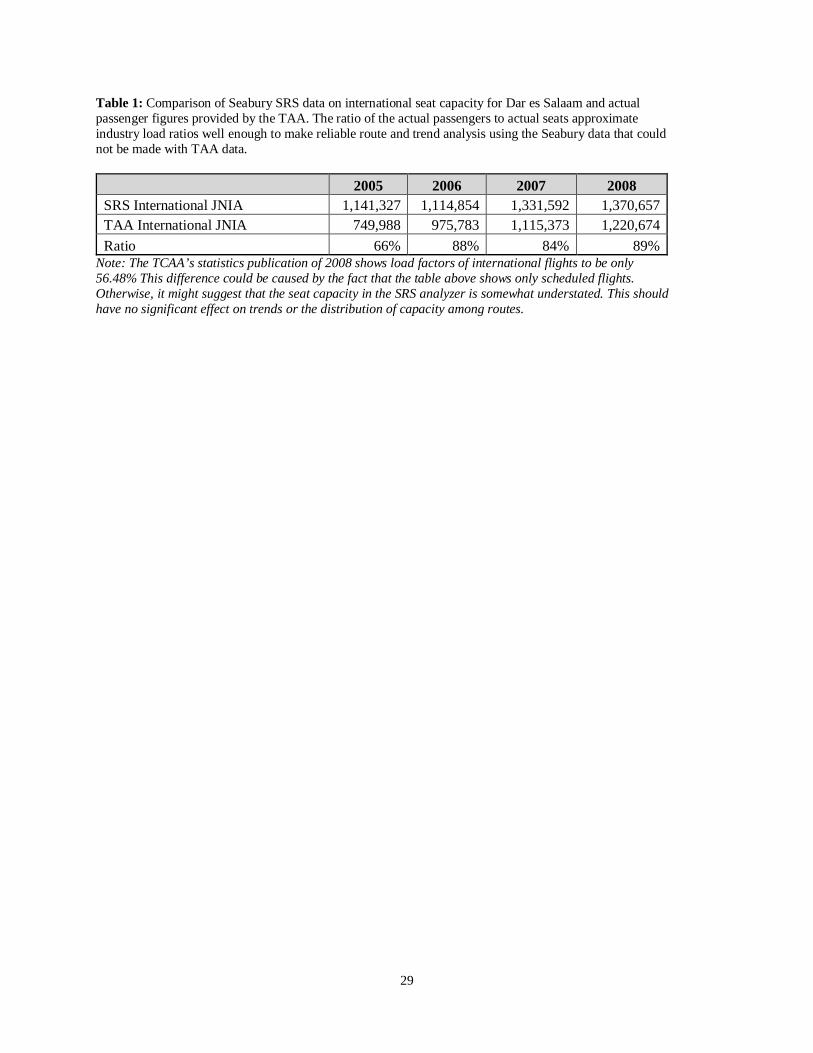

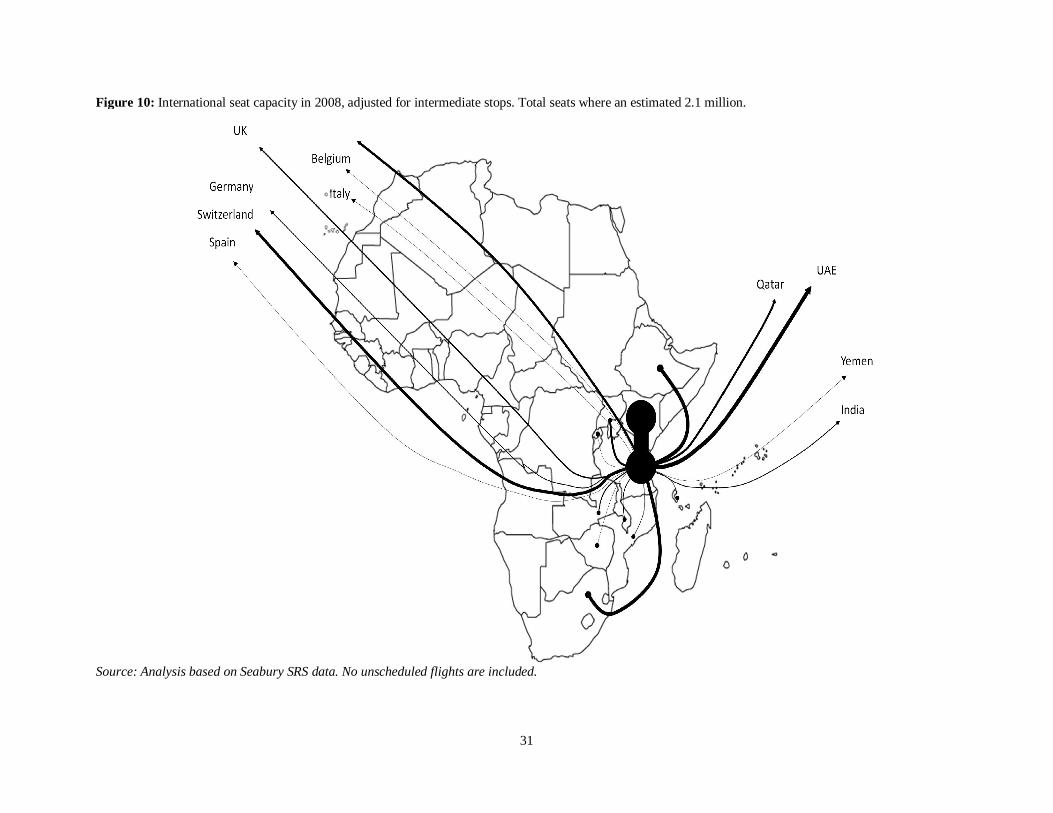

Figure 10 shows the major international routes for all of Tanzania for 2008. The data used for this analysis is from the Seabury SRS data analyzer, which measures scheduled capacity, not actual passenger flows. However, an extract of this data for Dar es Salaam has been compared with the actual passenger data from the TAA for Dar es Salaam, and a remarkable consistency has been found between 2005 and 2008, as shown in Table 1. The ratio of the estimated scheduled seat capacity to actual passengers should approximate load factors, and indeed the climb of this ratio from roughly 66% to between 80 and 90% does somewhat follow the global industry trend in load factors.

9 There are slight variances in the totals when comparing TCAA and TAA’s statistics. The TCAA published a total system traffic number of 2.90 million, a roughly 6% difference. In most cases, the TCAA’s numbers are being used, however, since the TAA has a published breakdown of all of its airports between 2004 and 2008, for system-wide traffic the TAA’s numbers are used, in conjunction with TCAA’s numbers for Zanzibar, Pemba, and Kilimanjaro. 10 The long-term global average is about 10% growth. However, during the period in question Tanzania clearly outperformed global growth rates. 11 Computed using numbers found in Tourism Statistical Bulletin 2008, Ministry of Natural Resources and Tourism (Tanzania), Tourism Department, p. 8

29

Table 1: Comparison of Seabury SRS data on international seat capacity for Dar es Salaam and actual passenger figures provided by the TAA. The ratio of the actual passengers to actual seats approximate industry load ratios well enough to make reliable route and trend analysis using the Seabury data that could not be made with TAA data.

2005 2006 2007 2008 SRS International JNIA 1,141,327 1,114,854 1,331,592 1,370,657 TAA International JNIA 749,988 975,783 1,115,373 1,220,674 Ratio 66% 88% 84% 89%

Note: The TCAA’s statistics publication of 2008 shows load factors of international flights to be only 56.48% This difference could be caused by the fact that the table above shows only scheduled flights. Otherwise, it might suggest that the seat capacity in the SRS analyzer is somewhat understated. This should have no significant effect on trends or the distribution of capacity among routes.

30

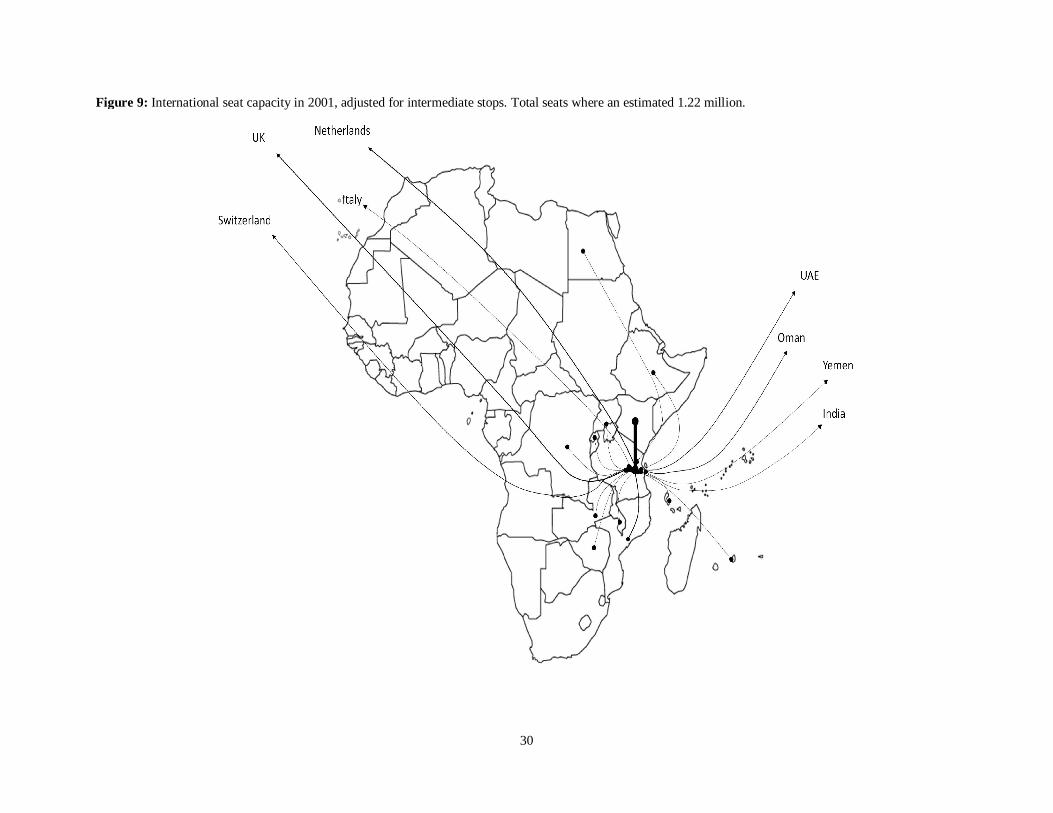

Figure 9: International seat capacity in 2001, adjusted for intermediate stops. Total seats where an estimated 1.22 million.

31

Figure 10: International seat capacity in 2008, adjusted for intermediate stops. Total seats where an estimated 2.1 million.

Source: Analysis based on Seabury SRS data. No unscheduled flights are included.

32

Table 2: Airlines providing scheduled international service in Tanzania (including Zanzibar), with their international seat capacities.

Airline 2001 2009 2009 Share

Precision Air Services Ltd. 6,807 456,248 22% Ethiopian Airlines Enterprise 65,028 268,079 13% Kenya Airways 173,347 214,041 10% Emirates 119,716 199,864 10% Swiss European Air Lines Ltd

129,640 6%

KLM Royal Dutch Airlines 85,344 128,943 6% South African Airways 48,764 118,200 6% Qatar Airways

103,868 5%

British Airways 187,675 58,923 3% Panair S.p.A.

55,389 3%

African Star Airways (PTY) Ltd.

46,972 2% Star Air

43,915 2%

Egyptair 16,437 40,048 2% Air Malawi Limited 39,212 39,208 2% Condor Flugdienst GmbH

37,411 2%

LAM

28,084 1% 1Time Airline

20,749 1%

Air Zimbabwe (PVT) Ltd. 10,686 19,095 1% Northern Dene Airways Ltd.

18,082 1%

Air Routing International Corp.

17,614 1% Rwandair Express

12,782 1%

Tavrey Aircompany

10,392 1% TUI Airlines Belgium

3,940 0%

Air Tanzania Company Ltd. 187,900 Swiss Air UA 122,418 Gulf Air Company G.S.C. 61,313 Air India Limited 43,646 FlyGlobeSpan 22,239 Air Service 16,904 Yemenia 11,682 Eagle Air Ltd. 2,182

Source: Calculated using estimated seat capacities as reported by Seabury’s SRS Data Analyzer.

33

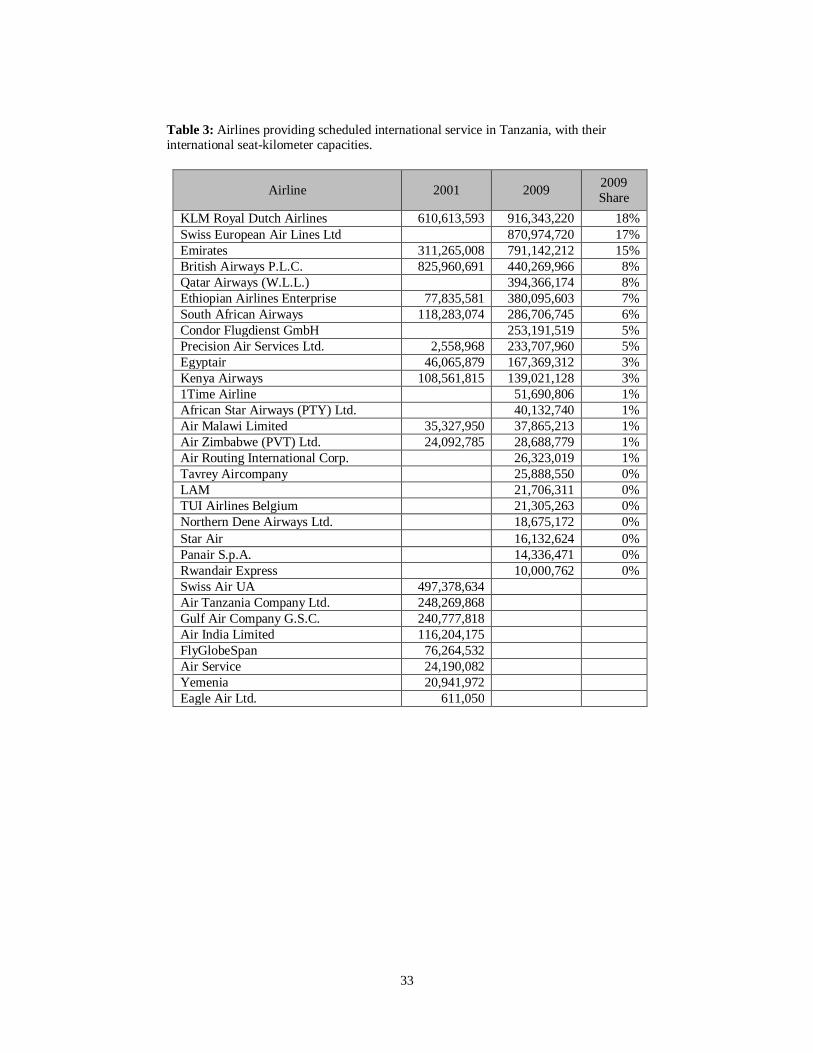

Table 3: Airlines providing scheduled international service in Tanzania, with their international seat-kilometer capacities.

Airline 2001 2009 2009 Share

KLM Royal Dutch Airlines 610,613,593 916,343,220 18% Swiss European Air Lines Ltd

870,974,720 17%

Emirates 311,265,008 791,142,212 15% British Airways P.L.C. 825,960,691 440,269,966 8% Qatar Airways (W.L.L.)

394,366,174 8%

Ethiopian Airlines Enterprise 77,835,581 380,095,603 7% South African Airways 118,283,074 286,706,745 6% Condor Flugdienst GmbH

253,191,519 5%

Precision Air Services Ltd. 2,558,968 233,707,960 5% Egyptair 46,065,879 167,369,312 3% Kenya Airways 108,561,815 139,021,128 3% 1Time Airline

51,690,806 1%

African Star Airways (PTY) Ltd.

40,132,740 1% Air Malawi Limited 35,327,950 37,865,213 1% Air Zimbabwe (PVT) Ltd. 24,092,785 28,688,779 1% Air Routing International Corp.

26,323,019 1%

Tavrey Aircompany

25,888,550 0% LAM

21,706,311 0%

TUI Airlines Belgium

21,305,263 0% Northern Dene Airways Ltd.

18,675,172 0%

Star Air

16,132,624 0% Panair S.p.A.

14,336,471 0%

Rwandair Express

10,000,762 0% Swiss Air UA 497,378,634

Air Tanzania Company Ltd. 248,269,868 Gulf Air Company G.S.C. 240,777,818 Air India Limited 116,204,175 FlyGlobeSpan 76,264,532 Air Service 24,190,082 Yemenia 20,941,972 Eagle Air Ltd. 611,050

34

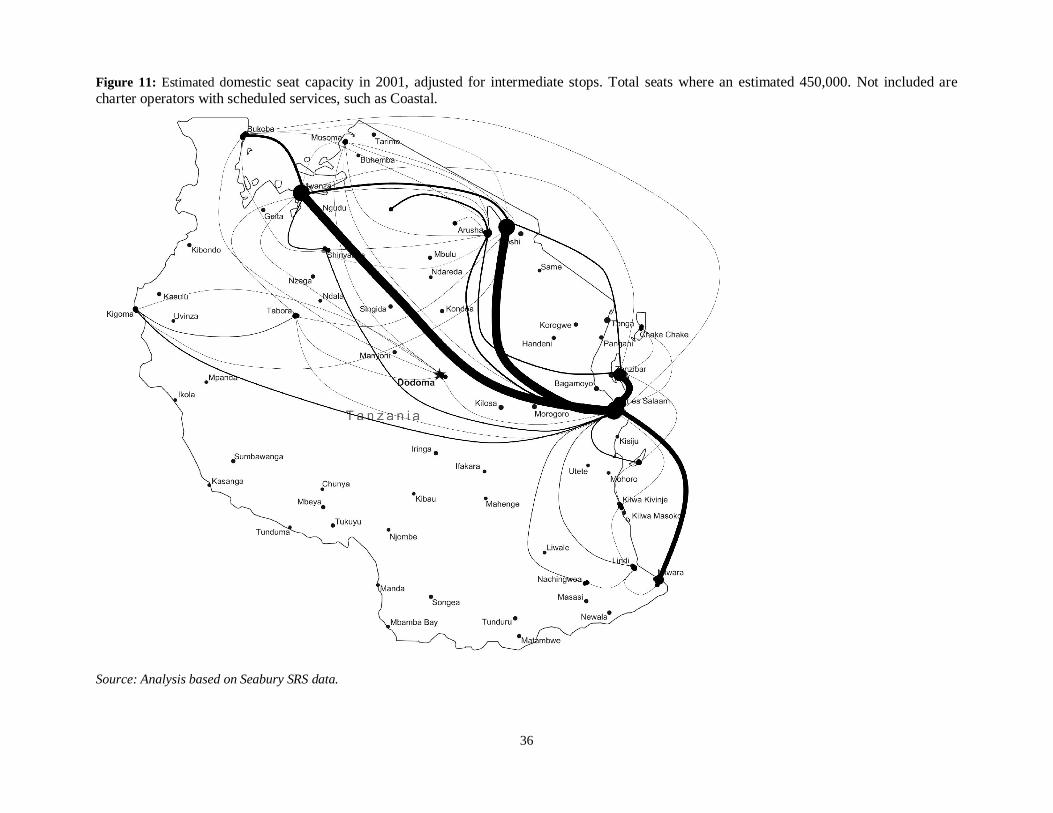

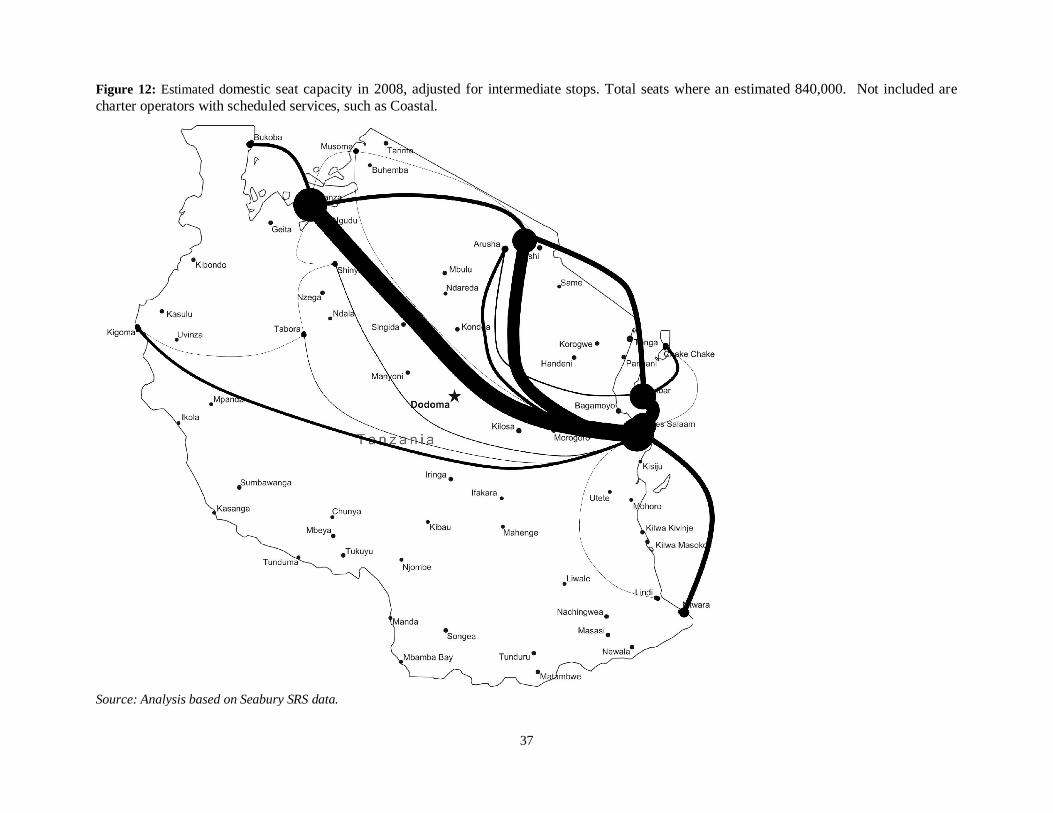

2. Domestic Travel Tanzania's domestic system will require further study in the proposed civil aviation master plan before any firm conclusions can be made. Though airport statistics for the airports in the TAA's system are readily available, the statistics that would analyze the actual routes being flown are much more difficult to process. Data from the SRS Analyzer is proving to be unreliable due to the fact that only formal, scheduled, and advertised services could be found. However, much of the domestic network is serviced by carrier such as Coastal (which now has an estimated 30% of the domestic traffic related to Dar es Salaam) that are formally classified as charter operators, but act as scheduled carriers. This makes an analysis of the domestic network dependent on highly granular data for each airport in the system, rather than a global repository. Though such data is being collected by the TAA, due to its volume the TAA could not assemble the data into a complete package for this report.

Using the SRS analyzer tool, the domestic system between 2001 and 2008 looks as described in figures Figure 11 and Figure 12. It would appear that many airports have dropped off the system. However, when comparing the TAA's airport summaries with the SRS system, the SRS system is clearly understating service. The dramatic reduction in the route network may well a be function of both overall decline in service and a shift from formal scheduled services to non-scheduled services acting as scheduled services as Precision Airways (formal scheduled), Coastal Aviation (informal, i.e. charter, but acting as scheduled), and others fill the vacuum caused by the severe reduction in Air Tanzania's (formal scheduled) network. In addition, the route consolidation in the north of the country may also be a result of a more extensive road networking having developed.

Tanzania's domestic traffic has gone through a significant set of changes in the last ten years. In 2001 a thin but expansive route network existed, with much higher connectivity than today. Though the traffic has grown by 11.1 percent, this route network has significantly reduced in terms of the number of nodes. Especially noticeable is the lack of any destinations in the lower west of the country. This region of Tanzania has low population densities, but also carries high potential for mining gold and coal, especially around Iringa, and further development of game parks as tourist attractions. However, mining activities in general do not increase scheduled passenger services.

An interesting aspect of Tanzania's domestic traffic is the general aviation (GA) component12. Though the most important route between Dar es Salaam and Mwanza, is serviced in a fully scheduled manner by Air Tanzania and Precision Air, Coastal Air, which does not fully fall under the term "scheduled services", provides an extensive network of scheduled flights, using Cessna Caravans, throughout Tanzania. The frequency of these flights are a significant addition to the transport network.

The TAA has 58 airports in its current system, however only 13 receive what could be formally called regularly scheduled services, down from 19 from 200113. There are, in addition to the TAA's airports, a high number of private strips serving both game parks and hte mining industry. The estimated number of such strips is 309.

12 General Aviation refers to smaller, propeller aircraft and includes almost all private aircraft. The Cessna Caravan is a high wing, single-engine, turbine-driven propeller aircraft, and is classified as GA. 13 These figures are from the Seabury’s SRS data analyzer tool. As mentioned in other sections of the report, they omit operators such as Coastal, and should be read with caution.

35

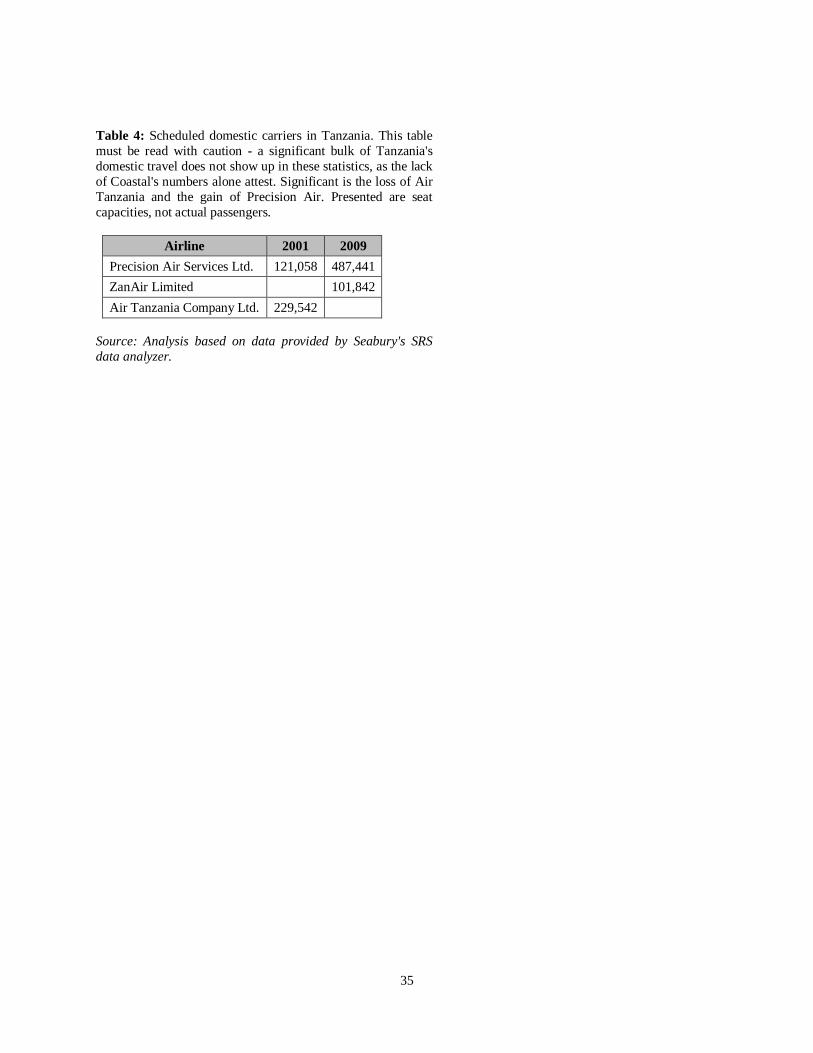

Table 4: Scheduled domestic carriers in Tanzania. This table must be read with caution - a significant bulk of Tanzania's domestic travel does not show up in these statistics, as the lack of Coastal's numbers alone attest. Significant is the loss of Air Tanzania and the gain of Precision Air. Presented are seat capacities, not actual passengers.

Airline 2001 2009 Precision Air Services Ltd. 121,058 487,441 ZanAir Limited 101,842 Air Tanzania Company Ltd. 229,542

Source: Analysis based on data provided by Seabury's SRS data analyzer.

36

Source: Analysis based on Seabury SRS data.

Figure 11: Estimated domestic seat capacity in 2001, adjusted for intermediate stops. Total seats where an estimated 450,000. Not included are charter operators with scheduled services, such as Coastal.

37

Figure 12: Estimated domestic seat capacity in 2008, adjusted for intermediate stops. Total seats where an estimated 840,000. Not included are charter operators with scheduled services, such as Coastal.

Source: Analysis based on Seabury SRS data.

38

Figure 13: Public airports in Tanzania, categorized by passenger traffic in 2008, using TAA statistics. All airports except Kilimanjaro, Pemba, and Zanzibar fall under the TAA. Noticeable are existing facilities in the south and south west of the country with virtually no passenger traffic.

Note: Not shown are Ngarenairobi and Kirondotal. Next version of the report will have updated chart. Data source: TCAA

39

Table 5: Total Passenger Numbers in Tanzania

Data source: TCAA. The numbers in this table feed into the projections in the next chapter.

40

IV. Investments: An Overview

1. Anticipated Needs Airport investments are complicated because of (a) their intermodal play and (b) simply the speculative nature of a new transport node. The notion of "build, and they will come" may work in some infrastructure arenas, but in the air transport (particularly airports) sector this notion has had very mixed results, with the example of the Montréal-Mirabel airport often cited as the most astounding as the airport failed as a passenger airport and was relegated to cargo-only operations.

In Tanzania, there are some clear examples of truly needed investments in existing facilities, while the development of new facilities may be more questionable for future payback. For Tanzania, for example, the eventual addition of a new international terminal in Dar es Salaam, as well as a new additional terminal in Zanzibar, are mathematically determined "must-haves". These are existing airports with determined levels of growth that can be easily projected into the future. Given the nature of Tanzania's domestic services, however, the true analysis of where future demand lies not in the prediction of where good anchors, or nodes, may be placed, but by looking at what operators are already doing. The most informative set of needs for future domestic air transport investment, or even other modal investments such as roads, may lie in where operators are placing their private airstrips today. At the same time, an analysis of the current airports in the TAA's system could well demonstrate that there are nodes worthwhile dropping altogether.

Figure 13 in the previous section helps illustrate the point. There are 37 airports with less than 1,000 passengers in 2008, of which 12 have no passengers at all. If this is compared to the actual traffic charts showing domestic passenger movements (Figure 12 earlier in this report), it would seem that the lack of traffic in the lower western portion of the country is not caused by lack or airports or airstrips, but simply by lack of demand for services at current cost levels.

41

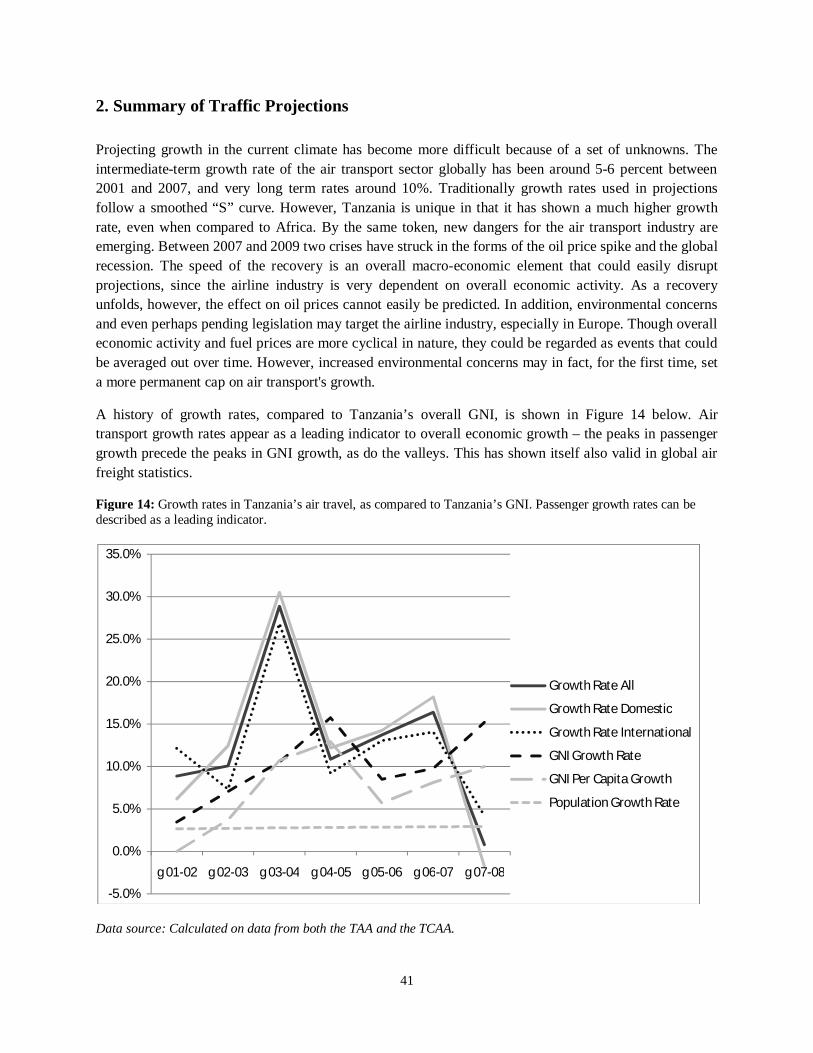

2. Summary of Traffic Projections Projecting growth in the current climate has become more difficult because of a set of unknowns. The intermediate-term growth rate of the air transport sector globally has been around 5-6 percent between 2001 and 2007, and very long term rates around 10%. Traditionally growth rates used in projections follow a smoothed “S” curve. However, Tanzania is unique in that it has shown a much higher growth rate, even when compared to Africa. By the same token, new dangers for the air transport industry are emerging. Between 2007 and 2009 two crises have struck in the forms of the oil price spike and the global recession. The speed of the recovery is an overall macro-economic element that could easily disrupt projections, since the airline industry is very dependent on overall economic activity. As a recovery unfolds, however, the effect on oil prices cannot easily be predicted. In addition, environmental concerns and even perhaps pending legislation may target the airline industry, especially in Europe. Though overall economic activity and fuel prices are more cyclical in nature, they could be regarded as events that could be averaged out over time. However, increased environmental concerns may in fact, for the first time, set a more permanent cap on air transport's growth.

A history of growth rates, compared to Tanzania’s overall GNI, is shown in Figure 14 below. Air transport growth rates appear as a leading indicator to overall economic growth – the peaks in passenger growth precede the peaks in GNI growth, as do the valleys. This has shown itself also valid in global air freight statistics.

Figure 14: Growth rates in Tanzania’s air travel, as compared to Tanzania’s GNI. Passenger growth rates can be described as a leading indicator.

Data source: Calculated on data from both the TAA and the TCAA.

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

g 01-02 g 02-03 g 03-04 g 04-05 g 05-06 g 06-07 g 07-08

Growth Rate All

Growth Rate Domestic

Growth Rate International

GNI Growth Rate

GNI Per Capita Growth

Population Growth Rate

42

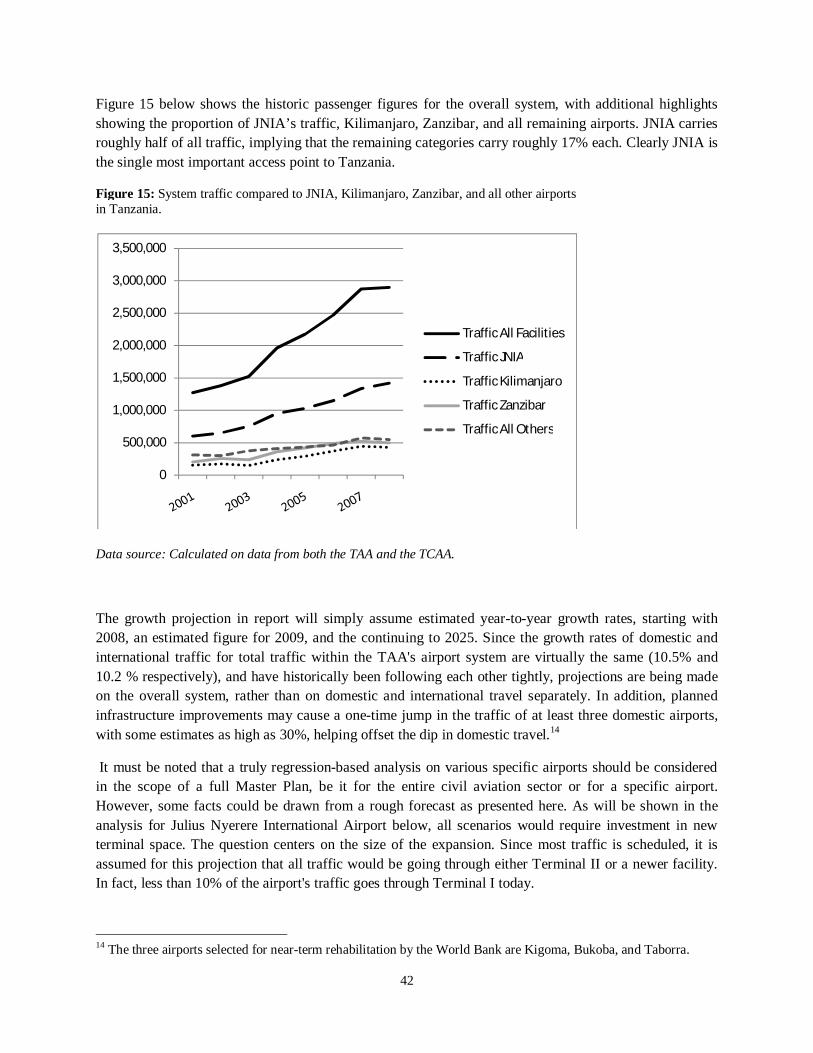

Figure 15 below shows the historic passenger figures for the overall system, with additional highlights showing the proportion of JNIA’s traffic, Kilimanjaro, Zanzibar, and all remaining airports. JNIA carries roughly half of all traffic, implying that the remaining categories carry roughly 17% each. Clearly JNIA is the single most important access point to Tanzania.

Figure 15: System traffic compared to JNIA, Kilimanjaro, Zanzibar, and all other airports in Tanzania.

Data source: Calculated on data from both the TAA and the TCAA.

The growth projection in report will simply assume estimated year-to-year growth rates, starting with 2008, an estimated figure for 2009, and the continuing to 2025. Since the growth rates of domestic and international traffic for total traffic within the TAA's airport system are virtually the same (10.5% and 10.2 % respectively), and have historically been following each other tightly, projections are being made on the overall system, rather than on domestic and international travel separately. In addition, planned infrastructure improvements may cause a one-time jump in the traffic of at least three domestic airports, with some estimates as high as 30%, helping offset the dip in domestic travel.14

It must be noted that a truly regression-based analysis on various specific airports should be considered in the scope of a full Master Plan, be it for the entire civil aviation sector or for a specific airport. However, some facts could be drawn from a rough forecast as presented here. As will be shown in the analysis for Julius Nyerere International Airport below, all scenarios would require investment in new terminal space. The question centers on the size of the expansion. Since most traffic is scheduled, it is assumed for this projection that all traffic would be going through either Terminal II or a newer facility. In fact, less than 10% of the airport's traffic goes through Terminal I today.

14 The three airports selected for near-term rehabilitation by the World Bank are Kigoma, Bukoba, and Taborra.

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

Traffic All Facilities

Traffic JNIA

Traffic Kilimanjaro

Traffic Zanzibar

Traffic All Others

43

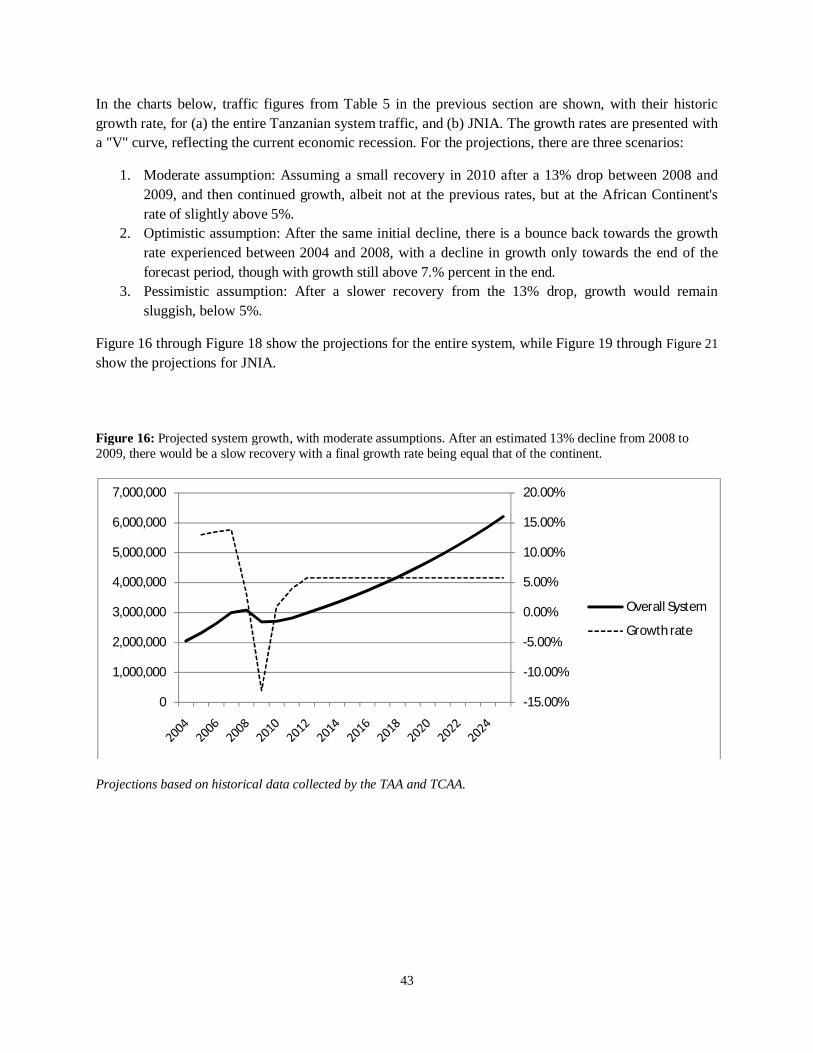

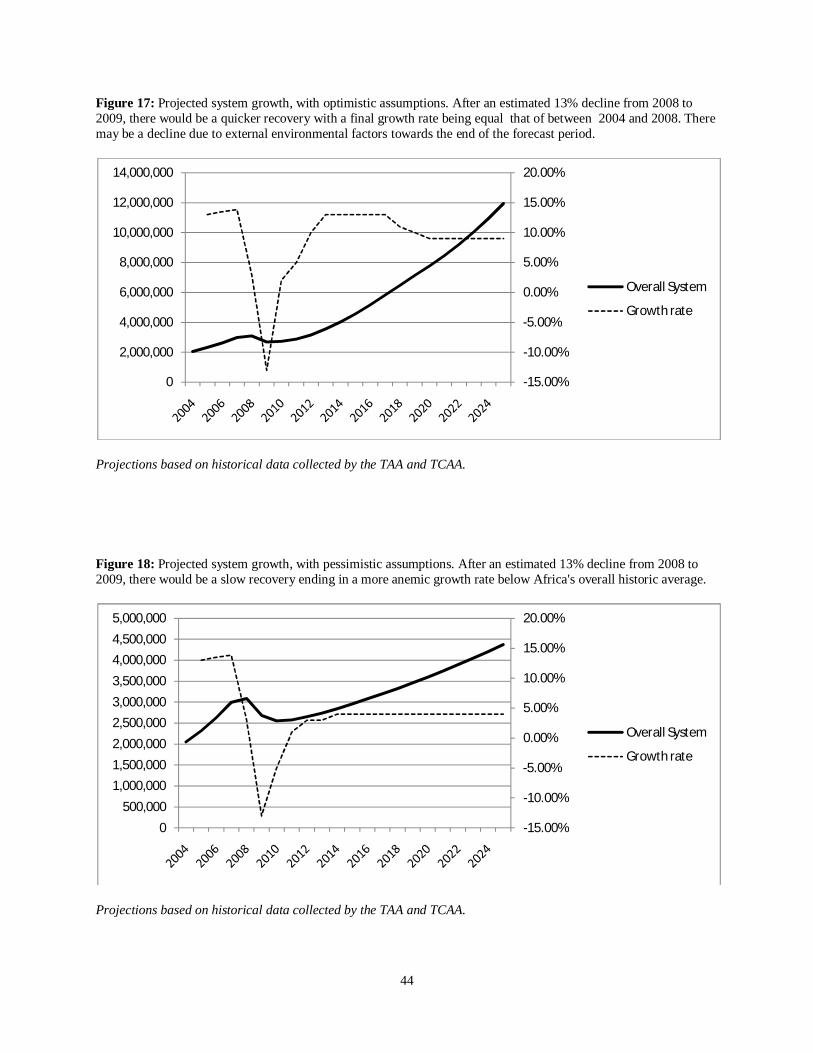

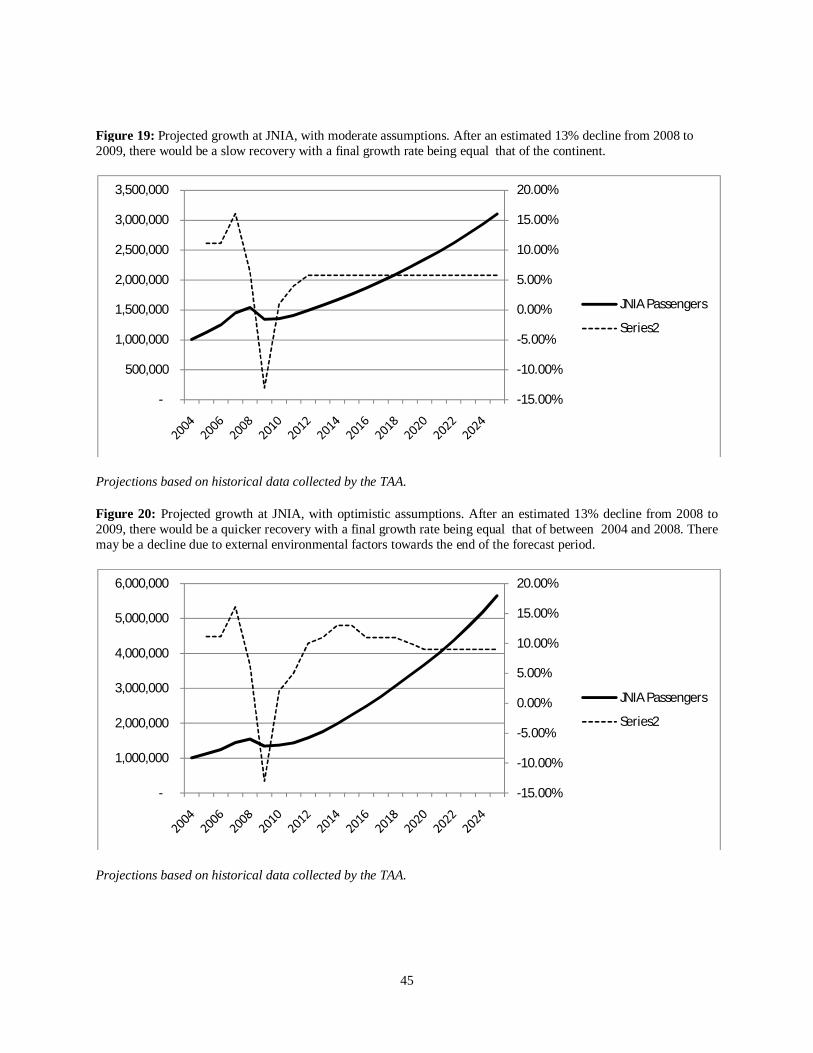

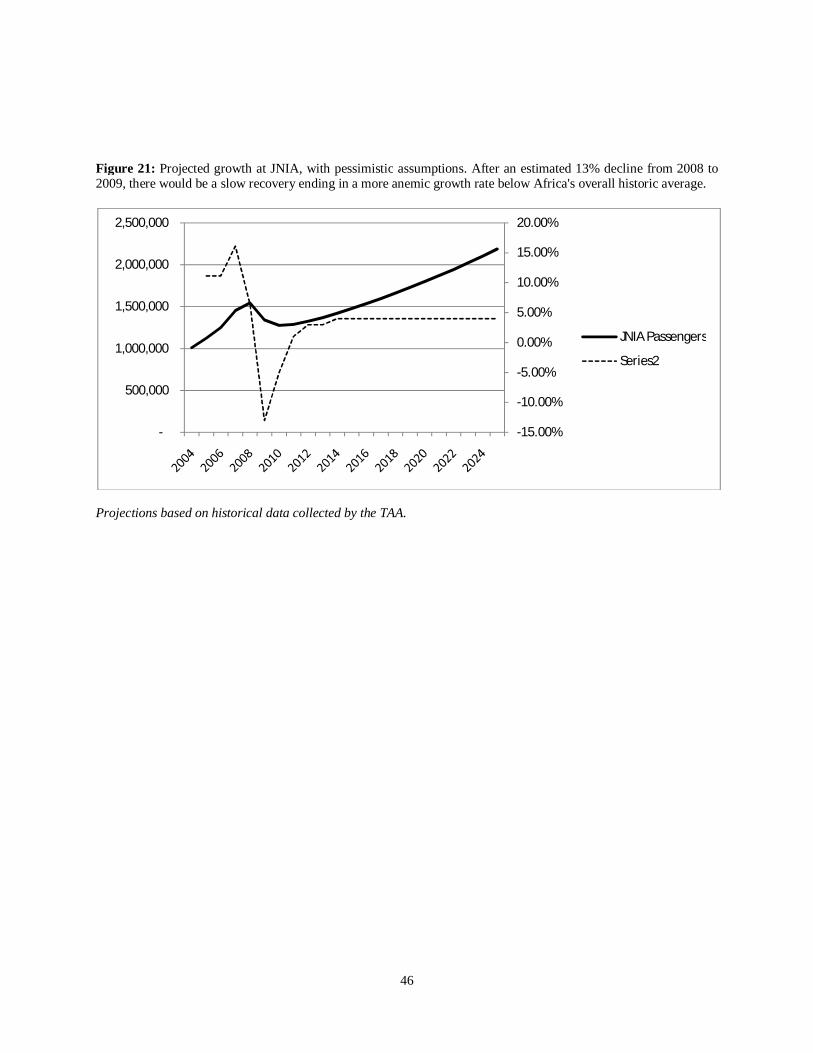

In the charts below, traffic figures from Table 5 in the previous section are shown, with their historic growth rate, for (a) the entire Tanzanian system traffic, and (b) JNIA. The growth rates are presented with a "V" curve, reflecting the current economic recession. For the projections, there are three scenarios:

1. Moderate assumption: Assuming a small recovery in 2010 after a 13% drop between 2008 and 2009, and then continued growth, albeit not at the previous rates, but at the African Continent's rate of slightly above 5%.

2. Optimistic assumption: After the same initial decline, there is a bounce back towards the growth rate experienced between 2004 and 2008, with a decline in growth only towards the end of the forecast period, though with growth still above 7.% percent in the end.

3. Pessimistic assumption: After a slower recovery from the 13% drop, growth would remain sluggish, below 5%.

Figure 16 through Figure 18 show the projections for the entire system, while Figure 19 through Figure 21 show the projections for JNIA.

Projections based on historical data collected by the TAA and TCAA.

Figure 16: Projected system growth, with moderate assumptions. After an estimated 13% decline from 2008 to 2009, there would be a slow recovery with a final growth rate being equal that of the continent.

-15.00%

-10.00%

-5.00%

0.00%

5.00%

10.00%

15.00%

20.00%

0

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

7,000,000

Overall System

Growth rate

44

Figure 17: Projected system growth, with optimistic assumptions. After an estimated 13% decline from 2008 to 2009, there would be a quicker recovery with a final growth rate being equal that of between 2004 and 2008. There may be a decline due to external environmental factors towards the end of the forecast period.

Projections based on historical data collected by the TAA and TCAA.

Projections based on historical data collected by the TAA and TCAA.

-15.00%

-10.00%

-5.00%

0.00%

5.00%

10.00%

15.00%

20.00%

0

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

12,000,000

14,000,000

Overall System

Growth rate

Figure 18: Projected system growth, with pessimistic assumptions. After an estimated 13% decline from 2008 to 2009, there would be a slow recovery ending in a more anemic growth rate below Africa's overall historic average.

-15.00%

-10.00%

-5.00%

0.00%

5.00%

10.00%

15.00%

20.00%

0500,000

1,000,0001,500,0002,000,0002,500,0003,000,0003,500,0004,000,0004,500,0005,000,000

Overall System

Growth rate

45

Figure 19: Projected growth at JNIA, with moderate assumptions. After an estimated 13% decline from 2008 to 2009, there would be a slow recovery with a final growth rate being equal that of the continent.

Projections based on historical data collected by the TAA. Figure 20: Projected growth at JNIA, with optimistic assumptions. After an estimated 13% decline from 2008 to 2009, there would be a quicker recovery with a final growth rate being equal that of between 2004 and 2008. There may be a decline due to external environmental factors towards the end of the forecast period.

Projections based on historical data collected by the TAA.

-15.00%

-10.00%

-5.00%

0.00%

5.00%

10.00%

15.00%

20.00%

-

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

JNIA Passengers

Series2

-15.00%

-10.00%

-5.00%

0.00%

5.00%

10.00%

15.00%

20.00%

-

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

JNIA Passengers

Series2

46

Figure 21: Projected growth at JNIA, with pessimistic assumptions. After an estimated 13% decline from 2008 to 2009, there would be a slow recovery ending in a more anemic growth rate below Africa's overall historic average.

Projections based on historical data collected by the TAA.

-15.00%

-10.00%

-5.00%

0.00%

5.00%

10.00%

15.00%

20.00%

-

500,000

1,000,000

1,500,000

2,000,000

2,500,000

JNIA Passengers

Series2

47

3. Needs for Primary Airports

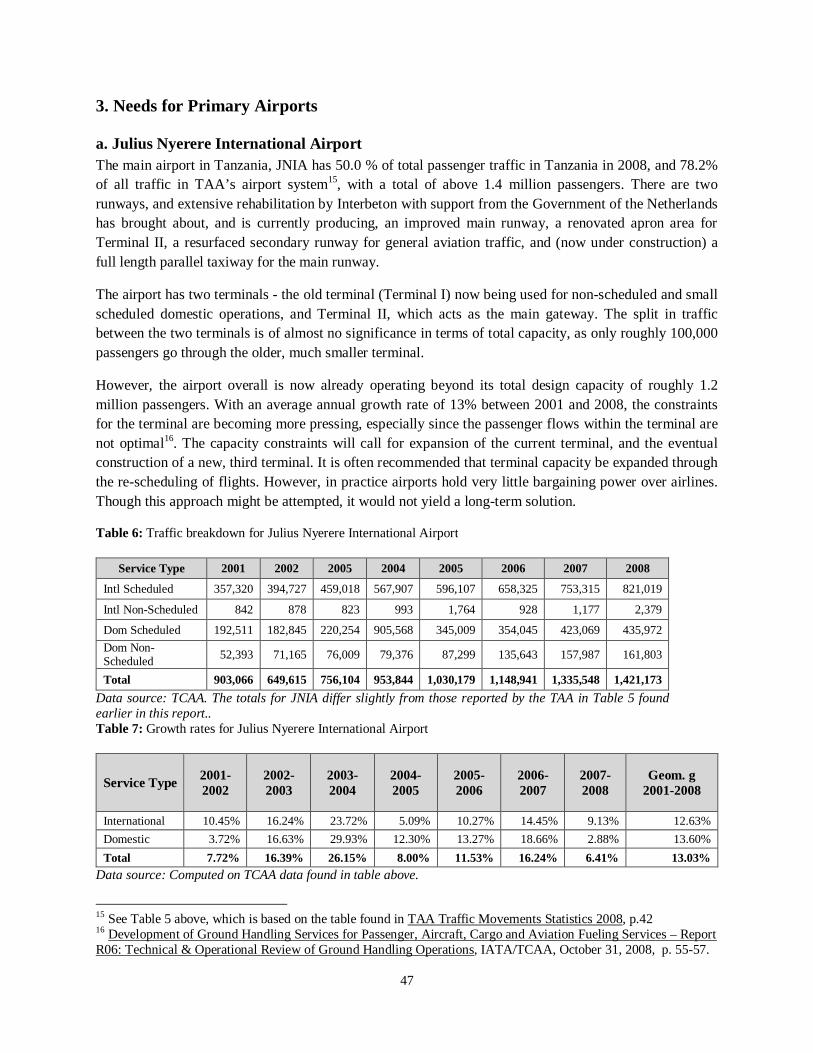

a. Julius Nyerere International Airport The main airport in Tanzania, JNIA has 50.0 % of total passenger traffic in Tanzania in 2008, and 78.2% of all traffic in TAA’s airport system15, with a total of above 1.4 million passengers. There are two runways, and extensive rehabilitation by Interbeton with support from the Government of the Netherlands has brought about, and is currently producing, an improved main runway, a renovated apron area for Terminal II, a resurfaced secondary runway for general aviation traffic, and (now under construction) a full length parallel taxiway for the main runway.

The airport has two terminals - the old terminal (Terminal I) now being used for non-scheduled and small scheduled domestic operations, and Terminal II, which acts as the main gateway. The split in traffic between the two terminals is of almost no significance in terms of total capacity, as only roughly 100,000 passengers go through the older, much smaller terminal.

However, the airport overall is now already operating beyond its total design capacity of roughly 1.2 million passengers. With an average annual growth rate of 13% between 2001 and 2008, the constraints for the terminal are becoming more pressing, especially since the passenger flows within the terminal are not optimal16. The capacity constraints will call for expansion of the current terminal, and the eventual construction of a new, third terminal. It is often recommended that terminal capacity be expanded through the re-scheduling of flights. However, in practice airports hold very little bargaining power over airlines. Though this approach might be attempted, it would not yield a long-term solution.

Table 6: Traffic breakdown for Julius Nyerere International Airport

Service Type 2001 2002 2005 2004 2005 2006 2007 2008

Intl Scheduled 357,320 394,727 459,018 567,907 596,107 658,325 753,315 821,019

Intl Non-Scheduled 842 878 823 993 1,764 928 1,177 2,379

Dom Scheduled 192,511 182,845 220,254 905,568 345,009 354,045 423,069 435,972 Dom Non-Scheduled 52,393 71,165 76,009 79,376 87,299 135,643 157,987 161,803

Total 903,066 649,615 756,104 953,844 1,030,179 1,148,941 1,335,548 1,421,173

Data source: TCAA. The totals for JNIA differ slightly from those reported by the TAA in Table 5 found earlier in this report.. Table 7: Growth rates for Julius Nyerere International Airport

Service Type 2001-2002

2002-2003

2003-2004

2004-2005

2005-2006

2006-2007

2007-2008

Geom. g 2001-2008

International 10.45% 16.24% 23.72% 5.09% 10.27% 14.45% 9.13% 12.63% Domestic 3.72% 16.63% 29.93% 12.30% 13.27% 18.66% 2.88% 13.60% Total 7.72% 16.39% 26.15% 8.00% 11.53% 16.24% 6.41% 13.03%

Data source: Computed on TCAA data found in table above.

15 See Table 5 above, which is based on the table found in TAA Traffic Movements Statistics 2008, p.42 16 Development of Ground Handling Services for Passenger, Aircraft, Cargo and Aviation Fueling Services – Report R06: Technical & Operational Review of Ground Handling Operations, IATA/TCAA, October 31, 2008, p. 55-57.

48

The year 2009 may well be a year of actual decline in traffic numbers, due to the global recession. Overall, the growth rates have been declining since 2007, when growth dropped from 16% from the previous year to only 6%17. The overall system saw a similar level of decline, falling from 13% to 7% and having an average growth rate of 13% between 2004 and 2008. The average growth rate for all of Africa, for all traffic, has been estimated to be 5.8% between 2001 and 2007. Though the years do not exactly match, it is apparent, by looking at the overall year - to - year system growth rates, that Tanzania has outperformed the rest of the continent.

Both the cargo terminal and Terminal II’s operations have been concessioned to SwissPort, with the contract up for rebidding soon. In addition, recently the TAA has allowed air service providers to perform their own passenger processing if they prefer. The model of having a contractor manage the actual passenger operations rather than a government-based entity seems to have worked well, though the actual passenger checking process is still in much need of further computerization.

A recent study by IATA recommends that cargo facilities be improved dramatically, citing significant shortcomings in the cargo terminal. In addition, the report also highlights some security concerns found in both the layout of Terminal 1 and the quality of security checks at other entry points to the airside. During the development of the civil aviation master plan, and any airport master plan for JNIA, the concerns of this report should be reflected18.