Embed Size (px)

Citation preview

NO. 0602S P D I S C U S S I O N P A P E R

Civil-service PensionSchemes Around theWorld

Robert PalaciosEdward Whitehouse

May 2006

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Civil-service pension schemes around the world

Robert Palacios and Edward Whitehouse

May 2006

PENSION

REFORM

PRIMERre-for´m

v.t. & i. 1. make (institution, procedure

etc.) better by removal or abandonment

of imperfections, faults or errors

primer n. 1. elementary book to

equip person with information

pe nsion n.

1. perio

dic paym

ent

made on ret

irement or

above

specified

age

2

Abstract

There are separate pension schemes for civil servants in about half of the world’s countries, including some of the largest developing economies, such as Brazil, China and India. In the higher-income, OECD countries, spending on pensions for public-sector workers makes up one quarter of total pension spending. In less developed countries, this proportion is usually higher. Yet, very little has been written on the design and reform of civil-service pension plans, especially when compared with the voluminous literature on national pension programs.

This paper compares civil service pension schemes across countries in terms of benefit provision and cost. We find that in many developing countries, these expenditures are a greater fiscal burden than in higher income countries where the tax base is larger. The paper also compares schemes within the same country covering private sector workers. Finally, we review key policy issues related to pension schemes covering civil servants as well as other public sector workers. In particular, we find that there is little justification for maintaining parallel schemes in the long run.

3

Civil-service pension schemes around the world

Robert Palacios and Edward Whitehouse1

May 2006

Edward Whitehouse works at the Social Policy Division of the OECD in Paris and Robert Palacios is Senior Pension Economist, Social Protection Department, World Bank. Correspondence: e-mail: [email protected] and Robert Palacios, World Bank, 1818 H St NW, Washington DC 20435; web-site: http://www.worldbank.org/pensions; e-mail: [email protected]. The authors are grateful to Larry Thompson of the Urban Institute and Robert Holzmann, Director of Social Protection at the World Bank for their helpful comments and advice. Montserrat Pallares-Miralles and Yvonne Sin of the World Bank have also provided valuable input. The paper has also benefited from comments at a seminar at the World Bank (July 2004), an Asian Development Bank/International Network of Pension Regulators and Supervisors meeting in Manila (March 2004), World Bank Institute workshops in Malta (June 2003) and Paris (September 2003) and a conference at the Centre for Pensions and Superannuation, University of New South Wales (March 2002). Initial research in this area by Whitehouse was financed by the Initiative for Policy Dialogue at Columbia University, New York.

PENSION

REFORM

PRIMERre-for´m

v.t. & i. 1. make (institution, procedure

etc.) better by removal or abandonment

of imperfections, faults or errors

primer n. 1. elementary book to

equip person with information

pe nsion n.

1. perio

dic paym

ent

made on ret

irement or

above

specified

age

4

Table of Contents 1. Introduction and overview....................................................................................................7

2. Key design features of civil service pension schemes .....................................................10

2.1 Institutional arrangements ..............................................................................................11

2.2 Eligibility criteria: pension age and length-of-service conditions .............................12

2.3 Replacement rates and indexation provisions .............................................................15

2.4 Sources and method of financing..................................................................................20

3. Reforming civil service pensions: key issues .........................................................................22

3.1 Fiscal impact .....................................................................................................................23

3.2 Labor market impact .......................................................................................................40

3.3 Dualism and integration..................................................................................................57

4. Sub-national government, public enterprises and military personnel ...............................64

5. Conclusion .................................................................................................................................73

6. Bibliography...............................................................................................................................76

Annex 1: Civil-service pension arrangements ..........................................................................81

Annex 2: Notes on tables ............................................................................................................84

Annex 3: Civil servants covered by DC schemes ....................................................................86

5

Tables

Table 1: Retirement age and service criteria for civil-service .....................................................14

Table 2: Accrual rates and maximum pension replacement rates for civil servants versus

replacement rate for national-scheme, full-career worker...................................................16

Table 3: Indexation procedures for pensions in payment, civil-service schemes.....................17

Table 4: Accrual rates and indexation provisions for DB civil service pensions for full career

workers in selected non-OECD countries, 2004 .................................................................19

Table 5: Central government employment, 1980s and 1990s ....................................................28

Table 6: Implicit pension debt of civil service and national schemes ........................................36

Table 7: Recent reforms to civil-service pension schemes in OECD countries.......................37

Table 8: Parametric reforms to national and civil service pension schemes ............................40

Table 9: Vesting periods for civil service schemes in selected countries ...................................44

Table 10: Portability and preservation of pension rights .............................................................45

Table 11: Integration of civil service pension schemes ................................................................61

Table 12: Structure of state pension schemes, United States .....................................................65

Figures

Figure 1: Institutional arrangements for civil-service pensions by region ................................12

Figure 2: Financing of civil servant versus national schemes ......................................................21

Figure 3: Expenditure on pensions of civil servants, high-income, OECD countries ...........24

Figure 4: Expenditure on civil-service pensions, non-OECD countries ...................................25

Figure 5: Expenditure on civil-service pensions, OECD countries ..........................................26

Figure 6: Expenditure on civil-service pensions, non-OECD countries ...................................27

Figure 7 Cumulative age distribution of civil servants and private-sector workers ...............29

6

Figure 8: Age distribution of pension scheme members..............................................................30

Figure 9: Spending on central-government wages and pensions, ...............................................33

Figure 10: Spending on civil service pensions, share of GDP, Bangladesh, Mexico, Nepal,

1992-2004...................................................................................................................................34

Figure 11: Spending on civil service pensions ...............................................................................34

Figure 12: Civil service wage compression, Nepal 1970-2003 ....................................................42

Figure 13: Value of accrued pension rights by age, Mauritius.....................................................46

Figure 14: The pension cost of moving jobs, Mauritius...............................................................47

Figure 15: Value of accrued pension rights by years of service, Cape Verde............................48

Figure 16: Pension cost of leaving a civil-service job, Cape Verde ............................................49

Figure 17: The pension cost of moving jobs, United Kingdom .................................................50

Figure 18: The pension cost of moving jobs, Germany...............................................................51

Figure 19: Job mobility in different sectors ..................................................................................52

Figure 20: Pension spending for civil servants and military in India and Pakistan ..................70

Figure 21: Age distribution of pensioners in Lebanon.................................................................71

7

Civil-service pension schemes around the world Robert Palacios and Edward Whitehouse

1. Introduction and overview

Civil servants and other public-sector employees — in the military, education,

publicly owned enterprises etc. — were often among the first groups of workers to be

covered by government-sponsored pension schemes (see Box below). In a handful of

countries — including Bangladesh, Bhutan, Botswana, Eritrea, Lebanon and the Maldives —

public-sector employees are still the only group covered by a formal pension scheme.

The rationale for providing pensions for government employees was somewhat

different from that behind the creation of national pension schemes.2 Among the objectives

particular to schemes for government workers were the following:

• securing the independence of public servants;

• making a career in public service attractive;

• shifting the cost of remunerating public servants into the future; and

• retiring older civil servants in a politically and socially acceptable way.

When mandatory pension coverage was expanded to the private sector, there often

seemed little point in including civil servants — who already had their own arrangements —

in new national schemes. Civil servants have also proved powerful in protecting their own

financial interests. Furthermore, while civil-service pension schemes share some of the

social-policy goals of national pension programmes, they must also accommodate the

government’s human-resources policy as an employer. For these reasons, special

retirement-income schemes for the public sector have often persisted. The issue of

2 Throughout this paper, the term ‘national pension scheme’ is used to refer to plans that cover private-sector employees. The coverage of these plans can vary, with some also covering public-sector workers, the self-employed etc.

8

‘dualism’3 — whether civil-service schemes are integrated with national schemes covering

private sector workers or are separate — is a central policy question in those countries where

parallel systems remain.

This paper focuses on countries with separate civil-service pension schemes (or

where only civil servants are covered). Although schemes covering sub-national

governments — local authorities and states in federal countries — and public-sector

enterprises are discussed, the focus is on federal level civil servants. Similarly, pension

arrangements for the military are sometimes integrated with other public-sector workers and

sometimes provided separately. Again, the focus is, where possible, on the civil-service

pension program.

The objective is, first, to review the data and information available on civil-service

pensions at a global level; and, second, to provide some guidance as to good policies and

practices. The main policy issues fall into three broad categories. First, what is the impact

of civil servant pensions on fiscal policy and how does it differ from other schemes? The

second is how civil-service pensions affect labor markets, which also touches on general

questions of civil-service remuneration and compensation. While both topics are also

relevant for a diagnosis of a national pension scheme, closer inspection reveals analysis and

reform of civil servants’ pensions pose special challenges. The third area of interest —

whether maintaining administratively separate schemes for public-sector workers is justified

— has already been noted. Our general conclusion is that the costs of ‘dualism’ generally

outweigh the benefits, especially in countries with small populations and/or limited

pension-system coverage. However, there are obstacles to integration, such as administrative

complexity, fiscal implications and the political economy of such a change.

The paper is structured as follows. Section 2 reviews the design of civil service

schemes around the world and compares them to national schemes where information is

available. The general finding is that civil service pension schemes offer more generous

terms, tend to have lower funding ratios and have higher per member liabilities than other

3 In practice, some countries have many more than two, parallel schemes. For example, some cover contractual workers in the public sector under a different program from permanent officials. Others have separate schemes for the military and for quasi-autonomous institutions, such as schools and universities.

9

schemes. In many countries, civil service pensions are becoming a major fiscal burden,

threatening to crowd out other programs, especially in low-income countries with limited tax

bases. Indeed, many of the lowest-income countries have already requested technical

assistance and financial support for reform of public-sector pension schemes from the

World Bank and other international organizations.

In Section 3, we address the three policy questions raised above: fiscal implications,

labor-markets effects and the rationale for dualism. The differences between analysis of

national pension schemes (for private-sector workers) and of civil-service programs have

important implications for the type of reforms — parametric and systemic — that can be

contemplated.

Section 4 discusses pension schemes that cover employees within the broadly

defined public sector other than federal civil servants. The most important of these are

those for the military, public-sector enterprises and sub-national government. We find that

many of the arguments regarding dualism apply here as well. This section argues that

customized solutions within an integrated system are possible, even for groups with risks

that are difficult to pool, such as the military.

Section 5 summarizes the results of the study and draws some tentative conclusions

as to general policy advice.

10

Box. A brief history of early pension schemes

The military was typically the first to receive pension coverage, especially with regard

to disability and survivor benefits. The English and Spanish governments were already

providing pensions to their veterans in the 17th century and a naval pension was set up in the

United States before it had even ratified its Constitution in 1787.4

In his study of the origins of the British civil service pension scheme, Raphael (1964)

finds that the first provisions were made on a discretionary and individual basis.5 These

evolved into a more formal system with the first superannuation fund for public sector

workers introduced in 1712 for customs officials. In 1810, the foundation of the British civil

servants scheme was legislated by Parliament. While the parameters described in the original

Act would be changed many times subsequently, the underlying model of a generous and

non-contributory pension scheme survived nearly two centuries and was inherited by dozens

of former British colonies.

2. Key design features of civil service pension schemes

This section reviews the main rules and parameters of civil-service pension

programs. The parameters include eligibility criteria, the defined benefit formula and

contributions from the employee and from the government as employer. Where possible,

comparisons with the national scheme that covers other formal sector workers are

presented.

4 Clark, Craig and Wilson (1999). 5 According to his research, the first person awarded a civil service pension was Martin Horsham, an employee in the Port of London in 1684.

11

2.1 Institutional arrangements

With information for 158 countries, a little more than half can be categorized as

having separate retirement-income arrangements for civil servants.6 (The Tables in Annex 1

provide more details on individual countries.) Figure 1 shows substantial regional variation

in the prevalence of parallel schemes. They are found throughout South Asia (seven

countries) and in most of Africa (32 out of 39 countries). They are more common than

integrated schemes in the Middle East/North Africa and East Asia. Integrated schemes are

more common in Latin America and are universal in Eastern Europe/Central Asia. The

regional patterns mostly reflect historical differences. For example, Anglophone African and

South Asian scheme were inherited from British colonial rule. In contrast, integration was a

natural arrangement under socialism in Eastern Europe and the FSU.

There are, naturally, many gray areas in this analysis. This is because of the

complexity of most countries’ pension arrangements.

In 12 OECD countries, for example, civil servants are covered by the national

pension scheme but have their own, top-up retirement-income arrangements. These

countries are counted as ‘integrated’ in Figure 1. This group includes Canada, Ireland and

Spain — with additional defined-benefit pensions for civil servants — and the United States

— which has a top-up defined-contribution arrangement, known as the Thrift Savings Plan,

and a legacy system. In many of these countries, many private-sector workers have

voluntary top-up arrangements, often with similar rules to the civil-service scheme. In two

OECD countries — Australia and the United Kingdom — civil servants are covered by part

of the mandatory pension arrangements that cover private-sector workers. The integrated

model with special top up schemes is not common outside the OECD countries and we

cannot cite any examples.

6 Note that this understates the role of parallel civil service schemes since countries that are in a transition to an integrated scheme (for example, covering only new civil servants in the national program) are counted as already integrated.

12

Figure 1: Institutional arrangements for civil-service pensions by region (per cent of and number of countries with integrated or separate programs)

0 25 50 75 100

Eastern Europe/Central Asia

Latin America/Caribbean

OECD

East Asia

Middle East/North Africa

Africa

South Asia

SeparateIntegrated

7

32 7

12 15

27

13 12

9 6

11 7

Source: authors’ calculations.

2.2 Eligibility criteria: pension age and length-of-service conditions

Table 1 shows the pension eligibility age in civil-service schemes; data for national

schemes are shown for comparison where available. The normal retirement age is found to

be the same or lower for civil servants in most countries. Furthermore, evidence for a range

of developing countries suggests that civil servants have a longer life expectancy than the

rest of the population. This further adds to the longer average duration of retirement of civil

servants compared with others arising from the earlier pension eligibility age.

The age criteria for pension receipt have often not changed over many years or even

decades, despite increasing life expectancy. (The same can, of course, be said for many

13

national schemes.) However, a few countries have increased the age recently, as in the case

of Senegal where normal retirement age was increased from 55 to 60 in 2001.

The mean normal pension age for men in the civil service is 58.6. In some cases, the

age is lower for women. Again, different ages between the sexes are still often found in

national schemes.

Eligibility is sometimes tied only to length of service, but more rarely than in the

past. For example, Brazil introduced a pension eligibility age in 1998 and Turkey has been

phasing in such a condition since 1999. It is still the case in Mexico — where men can retire

at any age after 30 years of service and women after 28 years — and in Iran — where civil

servants can retire regardless of age after 20/30 years (women/men). In the Maldives,

individuals can receive pensions after 20 years without leaving active service. They can

receive a second or even third pension each time they meet the length of service condition.

14

Table 1: Retirement age and service criteria for civil-service versus national pension schemes, 2004

Civil-service scheme National scheme

Minimum Normal Years of service Minimum Normal Years of service

High-income OECD countries Australia 55-60 55 65 Austria 60 56.5/61.5 60/65 Belgium 60 60 65 Canada 55 65 25 60 65 Denmark 60 67 67 Finland 60 63-65 60 65 France 60 56 60 Germany 62/63 65 63 65 Greece 60 57 65 Iceland 60 65 67 Ireland 65 66 Japan 65 25 55 65 Luxembourg 57 65 Netherlands 61 65 60 65 Norway 62 67 62 67 Portugal 60 36 55 65 Spain 60 30 60 65 Sweden 60 65 61 65 Switzerland 60 62 63 64/65 United Kingdom

50 60 65

United States 62 67 Latin America/Caribbean Brazil 55/60 Mexico 55 15 60 65 Paraguay 50 60 30 60 25 Africa Burkina Faso 53 60 55 15 Burundi 55/60 55 15 Cameroon 60 15 Cape Verde 60 60/65 3 Cote D’Ivoire 55/60 Ethiopia 55 10 no scheme Kenya 50 55 10 50 55 Malawi 55 20 no scheme Mauritius 60 15 60 Nigeria 50 60 10 Senegal 60 60 Togo 55 15 Zambia 50 55 10 55 Middle East/North Africa Bahrain none 60 15-25 45 55/60 15/20-10/15 Djibouti 55 25 55 25

15

Iran none 60 20/30-0 none 60/55 20/30-10 Lebanon 60 25 no scheme Morocco none 60 21/15-0 60 15 Tunisia 50 60 15 50 60 30-10 West Bank/Gaza none 60 20-15 no scheme Yemen none 55/60 30-15 none 55/60 30/25-15 South Asia Bhutan 60 no scheme Nepal 50 58 20 no scheme India 60 58 Maldives none no scheme Pakistan 60 Sri Lanka 60 55 East Asia/Pacific China 50/55 55/60 30 55/60 20 Indonesia 50 56 20 Korea 60 65 Malaysia 50 55 10 Philippines 60 65 15 Thailand 50 10 55 15

Note: where pension ages differ between men and women, the ages are shown F/M. Similarly, where the contribution requirement differs between men and women, they are shown F/M. Where the contribution requirement is stricter for early retirement than it is for claiming the pension at the normal pension age, the years are shown early-normal

Where there is a combination of age and service conditions, the service period

requirement is typically not binding. Some two-thirds of countries require service of 21

years or less. Most of these countries still operate a system of lifetime civil-service

employment with maximum ages of entry to the public sector. People will therefore have

typically reached the years-of-service requirement when they reach the pension age.

However, the years-of-service requirements and vesting rules may have an important impact

on flexibility, mobility and equity in certain cases. This is discussed later in Section 3.

2.3 Replacement rates and indexation provisions

The vast majority of civil service pension schemes are of the defined-benefit type.

This section looks at their benefit formulae and their provisions for uprating pensions in

payment (indexation).

16

Table 2 shows, first, the accrual rates in civil-service pension schemes in selected

OECD countries (including some schemes where there is a supplementary pension in

addition to the national scheme, i.e., partial integration). These are the pension entitlement

(as a proportion of the relevant earnings base) that is awarded for each year of service.

Usually, these are linear: that is, a single rate applied to each year of service. The table also

gives the pension replacement rate for a full-career worker in the civil service. This averages

a little more than 75 per cent, with a range from 50 to 100 per cent. The table also gives the

replacement rate under the national pension scheme for a full-career worker earning the

economy-wide average.7

In EU countries, the terms of civil service schemes are in many respects similar to

those of national pension schemes. In Finland, the Netherlands and Sweden, for example,

occupational schemes for private-sector employees offer the same or very similar terms as

the public-sector scheme (in the first case by law and in the second and third, by collective

agreements).

Table 2: Accrual rates and maximum pension replacement rates for civil servants versus replacement rate for national-scheme, full-career worker

Country Accrual rate (civil service)

Maximum replacement rate

National scheme

OECD countries Australia 1.65-3.4 66-88 52 Austria 2 80 80 Belgium 1.667 75 60 Canada 2 90 56 Finland 1.5 60 60 France 2 75 71 Germany 1.875 75 46 Greece 1.714 69 Iceland 1.9 76 73 Italy — 80 66 Luxembourg 1.667 83 71 Norway 2.2 66 53 Portugal 2 80 Spain — 95 88 Sweden 0.33/2.17 73 76 Switzerland — 65 58 United Kingdom 1.25 67 37

Note: the accrual rate varies with the earnings level in Sweden

7 Details of the calculation are given in Whitehouse (2004) and OECD (2004).

17

In a few countries, there are sizeable differences. In Germany, for example, a

full-career, private-sector worker on average earnings can expect a replacement rate of

around 40 per cent compared with 75 per cent for the civil-service plan. In the United

Kingdom, the replacement rate from the basic scheme plus the public, earnings-related

scheme for a similar worker would be around 35 per cent, compared with 67 per cent from

the civil service scheme. The former civil servant would receive the basic pension on top,

worth around 15 per cent of average earnings currently. The civil service scheme is also

more generous than the benefits arising from mandatory provision for private-sector

workers in Spain and Switzerland. In all these countries, some private-sector employers

offer occupational plans that can give replacement rates nearer to those applying in civil-

service pension schemes.

Indexation of pensions in payment tends to be more favourable in civil-service

schemes in OECD countries than those applied in the main national scheme. The latter are

nearly always based on prices (Table 3). Of the six countries that index pensions of civil

servants to wages, three have either price (France, Brazil and Mexico) or discretionary

adjustments (Turkey) in the other scheme. Naturally, this indexation is only more favourable

than uprating in line with prices if real wages rise over time.

Table 3: Indexation procedures for pensions in payment, civil-service schemes

Prices Civil service earnings Economy-wide earnings

Combination

Australia Austria Norway Belgium Canada France Denmark Iceland Germany Finland Italy Brazil Greece Spain Mexico Luxembourg Sweden Turkey Netherlands Switzerland Portugal United Kingdom

Table 4 compares accrual rates and indexation methods for schemes covering public

and private sector workers in 32 middle and low income countries. Again, the pattern is that

conditions in civil service schemes are more generous. Indeed, in several countries, there is

no pension scheme for private-sector workers. Accrual rates are on average more than 20

18

per cent lower for private workers in the formal sector than they are for civil servants.

These accrual rates are based on full career comparisons and therefore do not take into

account some of the non-linear features of benefit formulae being compared.

19

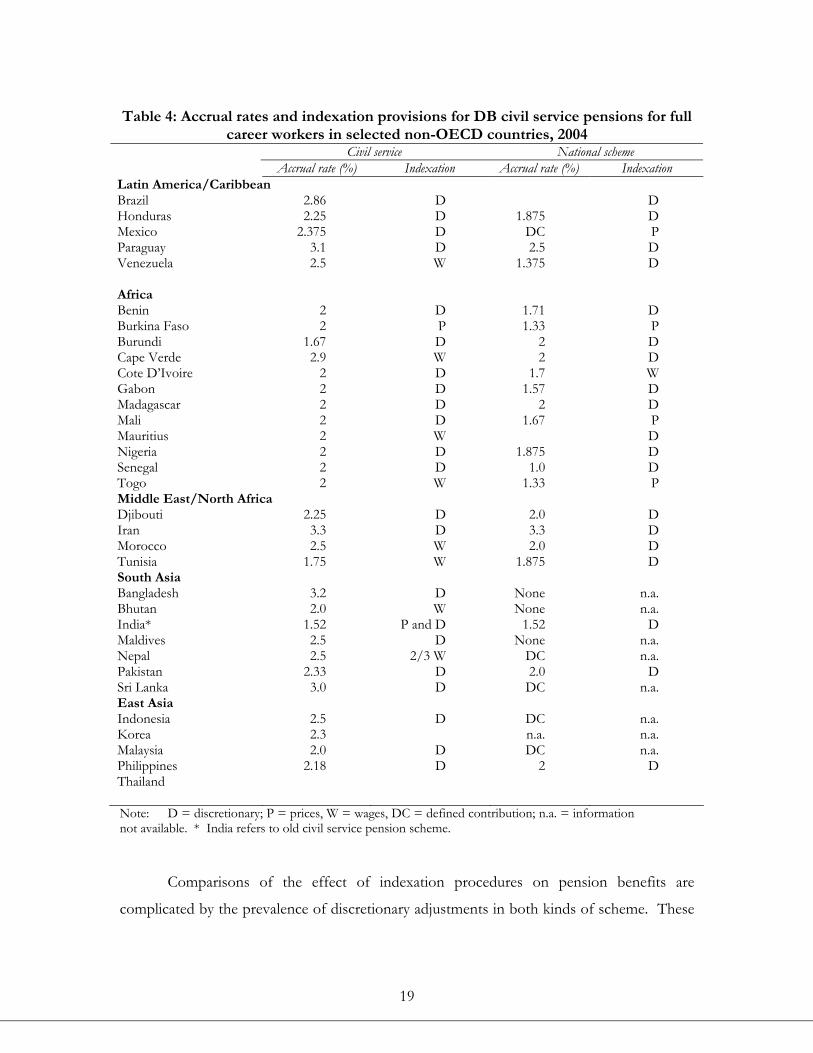

Table 4: Accrual rates and indexation provisions for DB civil service pensions for full career workers in selected non-OECD countries, 2004

Civil service National scheme Accrual rate (%) Indexation Accrual rate (%) Indexation

Latin America/Caribbean Brazil 2.86 D D Honduras 2.25 D 1.875 D Mexico 2.375 D DC P Paraguay 3.1 D 2.5 D Venezuela 2.5 W 1.375 D Africa Benin 2 D 1.71 D Burkina Faso 2 P 1.33 P Burundi 1.67 D 2 D Cape Verde 2.9 W 2 D Cote D’Ivoire 2 D 1.7 W Gabon 2 D 1.57 D Madagascar 2 D 2 D Mali 2 D 1.67 P Mauritius 2 W D Nigeria 2 D 1.875 D Senegal 2 D 1.0 D Togo 2 W 1.33 P Middle East/North Africa Djibouti 2.25 D 2.0 D Iran 3.3 D 3.3 D Morocco 2.5 W 2.0 D Tunisia 1.75 W 1.875 D South Asia Bangladesh 3.2 D None n.a. Bhutan 2.0 W None n.a. India* 1.52 P and D 1.52 D Maldives 2.5 D None n.a. Nepal 2.5 2/3 W DC n.a. Pakistan 2.33 D 2.0 D Sri Lanka 3.0 D DC n.a. East Asia Indonesia 2.5 D DC n.a. Korea 2.3 n.a. n.a. Malaysia 2.0 D DC n.a. Philippines 2.18 D 2 D Thailand Note: D = discretionary; P = prices, W = wages, DC = defined contribution; n.a. = information not available. * India refers to old civil service pension scheme.

Comparisons of the effect of indexation procedures on pension benefits are

complicated by the prevalence of discretionary adjustments in both kinds of scheme. These

20

ad-hoc changes in benefit levels tend to reflect the financial condition of each pension fund

or, in the case of public-sector workers, the budget situation more generally. Their level is

also influenced by the relative political strength of civil servants and their representative

organizations. Where automatic indexation is present, however, it usually favors former civil

servants over members of the national pension scheme.

In practice, lack of automatic indexation — in both civil-service and national pension

programs — leads to large and discrete changes in the real value of pensions. In the former

case, these are often tied to similarly dramatic changes in civil-service pay. In India, for

example, pension increases have been negotiated along with wages and other benefits for

civil servants every decade or so as part of the pay-commission system that has prevailed for

most of the last century. The result is an unpredictable income stream for pensioners and

large income differences between cohorts depending on the year that they happen to retire.

Another interesting indexation practice is differential adjustment in low and high

pension values. This can be achieved either by raising lower pensions with a higher

percentage adjustment or by increasing all pensions by flat amounts. This practice parallels

the wage compression that has been typical in many developing-country civil services in the

last few decades (see below).

2.4 Sources and method of financing

A third aspect of pension system design that often varies between public- and

private-sector schemes is the type of financing.

The first important distinction is the extent to which schemes accumulate reserves to

meet their future liabilities. Civil-service schemes are generally financed on a pure, pay-as-

you-go basis. Less than one in four plans has accumulated any reserves. In contrast, slightly

more than half of national schemes have some reserves.

As in the case of national schemes, recent reform trends have led to more funding in

the form of new defined contribution schemes. Recent examples include Thailand (1997),

Panama (1998), Botswana (2001), Hong Kong (2001), India (2004), Nigeria (2004) and

21

Australia (2005). (Annex 3 lists the countries in which civil servants participate in either an

integrated or a parallel DC scheme.) The pattern of funding also reflects the fact that many

of the national schemes with fully funded components are found in Latin America and

Eastern Europe. In the case of Eastern Europe, national schemes already covered civil

servants albeit often with different rules for different groups of workers. The Latin

American reforms that introduced mandatory, defined-contribution plans integrated separate

civil service schemes during the reform process (with the exception of Mexico).

Figure 2: Financing of civil servant versus national schemes

Civil servant schemes

PAYGO/unfunded

partially funded

fully funded

National schemes

fully funded

partially funded

PAYGO/unfunded

Source: authors’ calculations.

A second issue in the financing of the schemes is the role of contributions from

employers (i.e., the government in the case of civil-service schemes) and employees. Around

one in four of the unfunded schemes are ‘non-contributory’8 in the sense that there are no

explicit contributions levied on either employer or employee. The government simply picks

up the bill for civil-service pensions. They are found almost exclusively in former British

colonies in the Caribbean, sub-Saharan Africa and South Asia.

8 Note that the term ‘non-contributory’ is also used in the pension literature to refer to social-assistance or basic, universal pensions that are typically financed from general revenues and paid to all citizens meeting an age and/or income requirement.

22

To a certain extent, whether or not pension spending is financed through

contributions, as opposed to direct budget support, is immaterial. This is particularly clear

with employer contributions from the government where it would simply entail re-labeling

the flows with no impact on consolidated deficits. Even in the case of an employee

contribution, it can be argued that since civil service wages are not determined freely and

negotiations are based on net wages, the incidence of an employee contribution would still

fall on the budget. On the other hand, the lack of an earmarked contribution reduces

transparency and can make certain reforms more difficult – including integration of civil-

service and national schemes.

The important point to be taken from this brief look at financing arrangements is

that pre-funding of retirement-income liabilities is less common for civil servants’ pensions

than for national programs. Combined with the greater generosity that characterizes

civil-service schemes and the large share of the formal sector working in low-income

countries’ public sector, the burden of civil-service pensions on the budget may be

significant. Just how much so is explored in the next section.

3. Reforming civil service pensions: key issues

A growing number of countries with separate civil service pension schemes are

considering different reform options. These efforts are largely motivated by fiscal pressures.

Pay-as-you-go civil-service schemes are maturing, resulting in an increase in the ratio of

pensioners to workers. While there is significant variation across countries, there is a general

upwards trend in spending on civil service pensions. This section presents available figures

on the magnitude of the pension share in public spending and on the demographic

development of civil-service and national schemes. It also considers the options and the

arguments for reducing the cost of pensions to the government budget. It will become

apparent that there are important differences in how parametric reforms affect the fiscal

situation when the scheme in question covers civil servants rather than the private sector.

23

Likewise, changes to the pension scheme for civil servants must take into account

the specific labor-market and human-resource considerations that arise when the

government is both the employer and the plan sponsor. While private-sector workers are

typically mobile (between jobs), the emphasis in the public sector has been on stability:

ensuring that all workers remain in the public sector for a considerable period, if not their

whole career. More recently, the government has increasingly required a flexibility that

traditional pension arrangements cannot deliver: for example, in public-sector reform

(outsourcing, downsizing, divestiture, privatization etc.) and in making efficient use of scarce

human capital (recruitment of private-sector expertise).

The third topic of this section is the institutional arrangements for civil-service

retirement incomes: specifically, ‘dualism’ in public-sector pension provision versus

integration with the national pension system. This section explores some of the practical

issues in a policy of integration, including fiscal and labor-market effects.

3.1 Fiscal impact

The last section provided evidence suggesting that civil servants’ pension benefits

were generous relative to those covering the private sector. They were also less likely to

have accumulated reserves to offset liabilities. The demographic position of civil-service

pension schemes are often less favorable than national programs (i.e., civil servants tend to

have a higher median age and the schemes are at a later stage of maturation). As a result, the

share of the budget devoted to civil-service pensions has grown rapidly in many countries.

This in turn has often motivated reform proposals.

Current spending levels

The OECD countries currently spend an average of nearly two per cent of GDP on

pensions for civil servants and other public-sector workers. But, as Figure 3 shows, there is

a large variation around this mean. The differences appear to be only partly related to the

24

generosity of benefits. For example, expenditures are low despite high accrual rates in

Canada and Spain. The relative size of the civil service is a better predictor.

Figure 3: Expenditure on pensions of civil servants, high-income, OECD countries

(per cent of GDP)

0 0.5 1 1.5 2 2.5 3 3.5 4

Ireland (00)

Spain (00)

Japan (00)

Netherlands (00)

Denmark (00)

Canada (01)

Australia (01)

Germany (00)

United States (01)

Finland (00)

United Kingdom (00)

France (00)

Belgium (98)

Austria (00)

Source: OECD Social Expenditures Database

This ratio also varies greatly across low- and middle-income countries. Figure 4

shows a range from less than 0.5 per cent of GDP to more than two per cent of GDP. The

average spending on civil-service pensions is around 1.2 percent of GDP, or about 60 per

cent of the OECD average.

25

Figure 4: Expenditure on civil-service pensions, non-OECD countries (per cent of GDP)

0.0% 1.0% 2.0% 3.0% 4.0% 5.0%

Nepal (05)Bangladesh (02)

Iran (01)Venezuela (01)Indonesia (02)Pakistan (03)Mexico (01)Korea (97)

Philippines (97)Cameroon (01)

Senegal (04)China (02)Benin (98)

Morocco (02)Cape Verde (04)

Kenya (02)Jordan (02)Nigeria (02)Malaw i (99)

India (04)Mauritius (00)Sri Lanka (02)

Turkey (03)Zimbabw e (01)

Tunisia (02)Brazil (04)

per cent of GDP

Average 1.33

Source: World Bank pension database. India includes state level pension spending.

The ratio of spending to GDP provides an incomplete picture of the fiscal burden of

civil-service pension schemes. In OECD countries, tax revenues average nearly 37 per cent

of GDP.9 Revenues are more limited in most developing countries. Ultimately, both the

wage and pension bills of the public sector are constrained by the revenues available to the

government and its ability to borrow. It follows, therefore, that the opportunity cost of

paying civil-service pensions is more accurately captured by the share of available public

money that this expenditure consumes. A better indicator of the fiscal pressure of

9 OECD (2004b).

26

civil-service pension spending than its ratio to GDP is therefore its ratio to government

revenues. This is shown in Figure 5 and Figure 6. In the OECD countries, it varies between

2.5 and 7.5 per cent of general government revenues, with an average of five per cent.

In developing countries, the range is much larger: from two to 12 per cent of

revenues. The average is around six per cent: significantly higher than the average in the

OECD countries. In Brazil and Sri Lanka, one tenth or more of available revenues are used

to finance civil service pensions. (Note that the figure for India understates the fiscal burden

since it excludes state civil service pensions and Indian states depend heavily on federal

transfers.)

Figure 5: Expenditure on civil-service pensions, OECD countries (per cent of government revenues)

0 2.5 5 7.5 10

Denmark (00)

Spain (00)

Netherlands (00)

Ireland (00)

Canada (01)

Japan (00)

Australia (01)

Germany (00)

Finland (00)

United States (01)

France (00)

United Kingdom (00)

Belgium (98)

Austria (00)

Source: OECD Social Expenditures database; OECD Revenue Statistics

27

Figure 6: Expenditure on civil-service pensions, non-OECD countries (per cent of government revenues)

0% 5% 10% 15%

Mexico (01)Nepal (05)

Indonesia (02)Iran (01)

Cameroon (01)Pakistan (03)

Philippines (97)Nigeria (02)

Morocco (02)Korea (97)

Jordan (02)Bangladesh (02)

Kenya (02)Cape Verde (04)

Senegal (04)Mauritius (00)

Benin (98)Tunisia (02)Malawi (99)Turkey (03)

Sri Lanka (02)India (04)Brazil (04)

per cent of revenues

average = 6.8%

Source: World Bank pension database. Data for India apply to federal level only.

Age distribution and internal demographics

Table 5 shows that the growth in the number of civil servants has not kept up with

the growth of the population in the 1990s. In both developing and OECD countries,

central-government employment has fallen relative to population by a full percentage point.

This is equivalent to a decline (again, relative to population) of around a third in the OECD

countries and 45 per cent in the developing economies.

28

Table 5: Central government employment, 1980s and 1990s (per cent of total population)

early 1980s early 1990s Africa 1.8 1.1 Asia 2.6 1.1 Latin America 2.4 1.5 All developing countries 2.2 1.2 OECD 2.9 1.9

Source: Heller and Tait (1983) and Schiavo-Campo, de Tommaso and Mukherjee (1997b)

As a result of these growth patterns, we would expect that the internal demographics

of civil service schemes would diverge from that of the general population and from those of

the national pension scheme in particular. We would expect that in many countries civil

servants would be older, on average, than the national labor force and that the base of the

contributor pyramid may not be expanding over time. Finally, civil-service schemes often

started earlier than national schemes did.

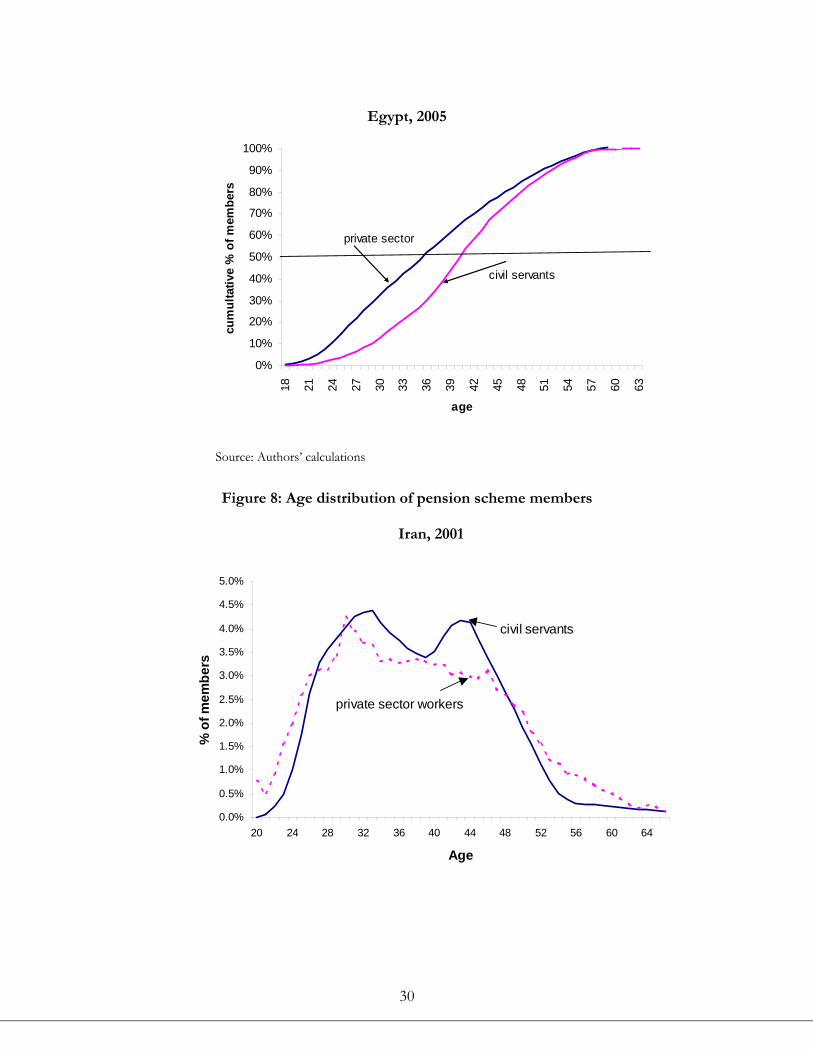

Evidence of the age structure of the civil service is difficult to find. Here, we present

detailed age distribution from three countries – Brazil, Egypt and Iran – based on data

collected by the World Bank for the purposes of projecting pension spending.

Figure 7 and Figure 8 below compare the age distribution for members of the

pension schemes covering private sector workers with the age distribution of civil servants.

In Brazil and Egypt, the expected pattern emerges: the median age of civil servants is higher

by 10 and 5 years, respectively. The scheme covering private sector workers looks much

more like a pyramid with an expanding population base while the civil service bulges in the

40+ age brackets, probably reflecting past hiring expansions followed by more recent

stagnation.

Iran’s civil service and private formal sector in contrast, do appear to have similar age

profiles. The common feature in all three countries is that the private sector distribution has

longer tails at each end of the age range. This would be expected given the tendency for

governments to hire graduates and to place minimum age restrictions as well as mandated

retirement ages.

29

Figure 7 Cumulative age distribution of civil servants and private-sector workers

Brazil, 1998

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

20 23 26 29 32 35 38 41 44 47 50 53 56 59 62 65 68 71 74

age

cum

ulat

ive

shar

e of

mem

bers

civil servants

private sector

Iran, 2001

0%10%20%30%40%50%60%70%80%90%

100%

1 4 7 10 13 16 19 22 25 28 31 34 37 40 43 46 49 52

age

cum

ulat

ive

shar

e of

mem

bers

civil servants

private sector

30

Egypt, 2005

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

18 21 24 27 30 33 36 39 42 45 48 51 54 57 60 63

age

cum

ulta

tive

% o

f mem

bers

civil servants

private sector

Source: Authors’ calculations

Figure 8: Age distribution of pension scheme members

Iran, 2001

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

5.0%

20 24 28 32 36 40 44 48 52 56 60 64

Age

% o

f mem

bers

civil servants

private sector workers

31

Brazil, 1998

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

19 22 25 28 31 34 37 40 43 46 49 52 55 58 61 64 67 70

age

per c

ent o

f mem

bers civil servants

private sector

Egypt, 2005

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

18 21 24 27 30 33 36 39 42 45 48 51 54 57 60 63

age

per c

ent o

f mem

bers

Civil servantsprivate sector workers

Source: Authors’ calculations

32

Both of these factors — late entry and early retirement — are likely to affect the

internal demographics of many civil service schemes in countries with dual pension systems.

In addition, as civil service jobs are more stable, it is likely that ‘contribution densities’ are,

on average, higher in civil service schemes.10 In defined benefit schemes, a higher average

contribution period will generally translate into higher benefits and will allow the worker to

meet the vesting requirements at an earlier age. Both of these factors would lead to earlier

retirement. Finally, some countries have used early retirement as part of a civil service

downsizing exercise. This too would also tend to reduce the proportion of older members

relative to the private sector scheme.

Recent spending trends

While growth in the civil service, along with wage bills has often slowed or even

stopped in developing countries, the pension bill for public-sector employees has often

continued to grow rapidly. This is not surprising, given the long lag between the reduction

in employment and the reduction in the number of retired civil servants (and their

survivors). This ‘inertia’ in pension spending can even be exacerbated when the pension

scheme is used to facilitate ‘downsizing’ (for example, through special incentives to retire

early).

10 The age distribution of workers covered is a snapshot of members in a particular year. The greater the rotation in membership, the lower will be the average contribution period.

33

Figure 9: Spending on central-government wages and pensions, Brazil 1987-1998

0

50

100

150

200

250

300

350

400

450

500

1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998

Inde

x 19

87=1

00

wage bill

pension bill

Source: World Bank (2004).

Data on trends in civil-service pension spending in some of the larger developing

countries shows a rapid increase compared to wages, the government budget and national

income. An extreme example can be seen in Figure 9. This shows the pattern in Brazil

between 1987 and 1998. In this case, spending on pensions grew twice as fast as wages.

Recall from Figure 6 above, that Brazil ranked first in civil service pension spending for the

countries where data are available. The pension burden contributed significantly to fiscal

woes faced by Brazil and has been the target of reforms for almost a decade. Despite

attempts to rein in spending however, little progress has been made.

Figure 10 shows civil service pension spending rising in Bangladesh, Mexico and

Nepal in the 1990s. (Note that Mexican state government employees are almost double the

federal figure and as such these figures are a significant underestimate of the total burden of

public-sector pensions.) Although data are not available for many countries, we would

anticipate this pattern to be repeated elsewhere. Figure 11 shows the same indicator for

India from 1990-2004. Most growth is due to spending on pensions for state level civil

servants where employment expanded in the 1970s and 1980s.

34

Figure 10: Spending on civil service pensions, share of GDP, Bangladesh, Mexico, Nepal, 1992-2004

0.0%

0.1%

0.2%

0.3%

0.4%

0.5%

0.6%

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002

per c

ent o

f GD

P Nepal

Mexico - federal only

Bangladesh

Source: Government budget data; IMF IFS statistics. Data for Bangladesh includes military pensions that represented on average about ten per cent of total spending.

Figure 11: Spending on civil service pensions

as share of GDP, India 1990-2003

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

1990

-91

1991

-92

1992

-93

1993

-94

1994

-95

1995

-96

1996

-97

1997

-98

1998

-99

1999

-2000

2000

-2001

2001

-2002

2002

-2003

2003

-2004

per c

ent o

f GD

P

Total

states

central

defense

Source: Government of India budget documents and authors’ calculations.

35

Unfunded liabilities

Pension policy has a long lead time: the rules and parameters today will affect

members’ benefits and so governments’ liabilities for decades to come. Periodic reviews of

the long-term financial position of pension schemes — particularly those financed on a

pay-as-you-go or partially funded basis — are an essential input to the policy-making

process. Some countries have not carried out such reviews either of their national or

public-sector pension programs. Others assess the financial situation of the national pension

scheme but not the civil-service plan. Many countries have therefore called on the World

Bank and other international organizations to help in preparing long-term projections of the

finances of both national and civil-service pension schemes.

Table 6 shows a number of financial indicators for four countries’ national and

civil-service pension plans. The second indicator, shown for a larger range of systems above,

is the current spending as a proportion of GDP.

However, this indicator does not capture the ‘inter-temporal’ nature of the pension

promise. Nor does it reflect the demographic challenges that will be faced by pension

systems in the future. Projections of future spending, based on today’s policies over

parameters and rules, can be summarized in a single number. This is essentially the net

present value of future pension spending commitments. It is commonly known as the

‘implicit pension debt’, or IPD. 11

The IPD name is designed to show that pension commitments are a kind of debt

with some characteristics in common with conventional public-sector debt, such as

government bonds. Unlike conventional debt, however, the implicit debt accruing in

pension promises is not reported on the government’s balance sheet. But it can still place

important limits on fiscal policy. Indeed, the IPD is often large relative to conventionally

defined public debt. While the estimates in Table 6 are sensitive to discount rates and other

assumptions, the magnitudes of the IPD are striking under any reasonable values for these

variables. For example, Turkey and Brazil have liabilities for civil service schemes equivalent

to 75 and 92 percent of GDP, respectively.

36

Table 6: Implicit pension debt of civil service and national schemes (selected countries)

Implicit pension

debt (% of GDP) Current spending

(% of GDP)

Coverage (% of labor

force)

IPD/coverage

Civil service

National Civil service

National Civil service

National Civil service

National

Brazil 1998 92 284 1.7 6.2 2 27 46.0 10.5 Iran 2001 38 64 0.5 0.7 8 32 4.1 2.0 Korea 1995 7 33 0.2 0.3 1 23 7.0 1.4 Philippines 1997 17 90 0.2 0.8 3 40 5.7 2.3 Turkey 1997 75 71 1.7 2.5 5 25 15.0 2.8

Source: Holzmann et al. (2004); Robalino (2006).

The IPD of national pension programs is three times that of the civil-service scheme

in Brazil and around five times higher in Korea and the Philippines. However, national

schemes in all four cases cover many more workers than the civil-service scheme does, as

shown by the third indicator in Table 6. The IPD divided by the coverage rate shown as the

final indicator in Table 6, adjusts for the number of workers. By this measure, the average

IPD per civil servant covered is more than double that of the average private sector worker

in Iran and the Phillipines and four-to-five times higher in the other three countries.

Improving civil service scheme finances

The measures that can be taken to reduce civil service pension liabilities are broadly

the same as those that can be applied for national schemes. Table 7 illustrates most of the

alternatives through the changes adopted in a range of OECD countries. It is clear that

most are motivated by fiscal pressures, since they either reduce the generosity of pensions,

reduce the number of beneficiaries by increasing retirement age or increase contribution

revenues.

11 See Holzmann, Palacios and Zviniene (2003) for a discussion of the measurement and reporting of implicit pension debt and estimates for a sample of developing countries.

37

Table 7: Recent reforms to civil-service pension schemes in OECD countries

Reform Countries Increase in pension age Finland, Sweden Restrictions on early retirement Germany, Italy, Sweden Reduced pension generosity or increased service requirement

Austria, France, Germany, Greece, Finland, Portugal

Change in uprating procedure Italy, Sweden Integration of civil-service with general state scheme

Austria, Greece, Spain

Increase in contribution rates Austria, Finland, Greece, Italy, Netherlands, Portugal, Sweden

Introduction of some form of pre-funding Belgium, Denmark, Finland, Italy, Sweden

Source: authors.

Some ‘parametric reforms’ will almost certainly reduce pension liabilities regardless

of the type of pension scheme. Less generous indexation and reductions in accrual rates are

prime examples. On the other hand, the impact of measures intended to increase the

effective retirement age have more complex effects. If, for example, the relationship

between contributions and benefits implies an unsustainably high rate of return, a higher

retirement age may simply add to the liability as the worker accrues more years of service

towards his or her benefit calculation. Short term finances improve, but the intrinsic

imbalance over the long term still results in an increase in the total liability. Even when the

direct impact is clearly positive (due to the combined impact of having a greater number of

contributions and fewer years of pension), there may be indirect effects in terms of spending

on other programs such as disability, unemployment and social assistance that offset savings

from the overall fiscal perspective.

The ultimate fiscal impact of an increase in the retirement age for civil service

pension schemes is even more difficult to measure. Intuitively, the government can either

pay a wage or a pension to the same individual. Since a pension is normally lower than the

salary, later retirement would lead to higher spending. However, this assumes that there is

no link between retirement and the decision to hire new civil servants. If the retiring

employee was replaced by a new hire, the fiscal effect would be equivalent to the difference

between the retiring worker’s final wage and the sum of the new hire’s wage and the retiring

38

worker’s pension. The equation becomes even more complicated when measured over time

in which case the age-earnings profiles and pension indexation experience would have to be

taken into account and a present value calculated.12

The discussion bears close resemblance to the literature on public sector

downsizing.13 In both cases, the ultimate fiscal impact depends on the government’s hiring

policy and a reasonable assumption about the counterfactual in the absence of any changes.

In the case of downsizing, the changes might involve severance payments or early retirement

options while in a standard parametric reform the typical option considered would be

increasing effective retirement age. Regardless of the chosen route, the ultimate fiscal effect

will depend on government hiring practices. In many cases, if not the majority , downsizing

exercises were eventually undermined by new hiring. We are not aware of similar studies

that look at the aftermath of an increase in the civil service retirement age, although casual

observation would suggest a similar outcome.14

A final consideration is how changes to the contribution rate affect civil service

versus national pension plans. Obviously, when the contribution rate is increased for a

national plan, the direct impact is to improve the finances of the pension scheme. There

may be indirect negative effects due to the distortionary effects of a higher tax on labor, but

in general, the consolidated fiscal deficit will be reduced.

In contrast, an increase in the contribution rate for a civil service pension scheme has

an ambiguous effect, especially with regard to the employer share. It could be argued that an

increase in the employee contribution improves both the finances of the scheme and the

overall fiscal situation. However, for this to be the case, the net wage would have to be

permanently reduced. Most incidence analysis of labor taxes in the private sector finds that

workers bear most of the burden due to the relative elasticities of labor demand and supply.

This framework does not apply to civil service wage structures, however. To the extent that

the net wage of civil servants is the product of negotiation and bears little relation to a

12 Note that this analysis is focused only on fiscal aggregates and says nothing with regard to the productivity of the civil service which may be significantly affected by a change in the age composition. We return to the human resource considerations in the Section 3.1. 13 See Rama (1999).

39

market-determined outcome, the increase in the employee contribution to a civil service

pension scheme may not actually result in fiscal savings.

At the same time, an increase in the employer contribution may improve the pension

schemes finances, but it achieves nothing from the overall fiscal perspective. This simply

re-labels the part of the budget used to finance civil service pensions. In a national scheme,

in contrast, the fiscal impact is unambiguously positive (ignoring any general equilibrium

effects).

Table 8 summarizes the comparison of parametric reforms as applied to national

versus civil-servant pension schemes. In the case of retirement age, the wage-bill effect

implies a different sustainability effect when compared to the national scheme. Raising the

retirement age while continuing to hire at the same rate in the civil service will result in a

larger wage-plus-pension bill. It is also important to note that contributions from the

government as employer may make the pension scheme more sustainable, but at the cost of

fiscal sustainability more generally.. In the case of national schemes collecting contributions

from private, formal-sector workers, any increase in contributions will raise revenues and

increase sustainability (albeit at a potential cost in terms of demand and supply for labor as

the tax wedge grows).

14 For example, in Senegal, a sudden increase in the retirement age did not affect plans to hire a large number of new civil servants.

40

Table 8: Parametric reforms to national and civil service pension schemes

Reform National CS Accrual rate Same effect Indexation Same effect Retirement age disability, social assistance

etc. can undermine gains effect on accruals (same as

national?), CS pay bill Employee contributions positive (ex. notional accounts,

DC) positive (but can be

undermined by pay changes) Employer contributions positive (ditto) relabelling only

Source: authors.

We conclude this section with the following observations:

• The fiscal burden of civil service pensions is significant and growing;

• The implicit pension debt attributable to civil servants is disproportionately large when compared to their importance in the covered labor force;

• Special considerations must be made when assessing parametric changes to civil service pension schemes, especially with regard to the broad fiscal impact of changing the retirement age; and

• Defined contribution schemes are becoming more popular as a way of introducing some fiscal discipline for civil service pension schemes. India’s reform of 2004 is the most important example at the moment. They also promise advantages in terms of the labor market issues discussed in the next section.

3.2 Labor market impact

Two issues stand out with regard to the interaction between civil-service pensions

and the labor markets. Both are related to the human-resource policy of the public sector:

attracting productive workers to the civil service and retaining them. The first issue is the

relative compensation of civil servants vis à vis their private-sector counterparts. The second

is the incentives and disincentives that pensions can generate for moving between public-

and private-sector employment.

41

Differences in compensation

Pensions are an important part of the compensation package offered to civil

servants. At typical replacement rates and pension eligibility ages, the pension promise is

worth around 30-35 per cent of earnings. The question as to whether this generous pension

promise attracts high-quality staff is an empirical one.

There are numerous studies of differentials in earnings between the public and

private sectors for a range of countries. These use econometric tests to estimate the

difference in wages for individuals with similar characteristics that can be attributed to being

in the public or the private sector.

Unfortunately, these studies have generally not taken account of the differences in

pension values and eligibility conditions.15 Nevertheless, they do shed light on the question

of whether additional benefits, such as a more generous pension scheme, are needed to

address disparities between remuneration in the two sectors. The short answer to this

question is ‘no’.16

In developing countries, public-sector employees with the same human capital and

experience generally earn more than their private sector counterparts.17 This suggests that

any further advantage provided to civil servants through pension or other benefits are not

needed in order to compete with the private sector. In fact, the additional compensation

would only exacerbate unjustified compensation differentials and unnecessarily increase the

cost of government.

The main exception to this finding is reserved for those civil servants with the most

human capital. Several studies have found that highly educated workers tend to earn less

than their private-sector equivalents. While an interesting finding with important public

15 Pensions are only one of a host of other non-wage benefits that often differ between public and private sectors as noted in Schiavo-Campo, de Tommaso and Mukherjee (2003). Nevertheless, it will generally be quantitatively most important. 16 A World Bank study prepared as part of technical assistance to the Government of Pakistan in 2005 did include pensions in a public-private compensation differential analysis. It found that the more generous pension benefits of the civil servants exacerbated positive wage differentials for the vast majority of civil servants. See World Bank (2006). 17 See Glinskaya et al. (2004) for a review of the results in the literature.

42

policy implications, the fact is that only a small share of the civil service falls into this

category, perhaps five to 10 per cent.18

This finding is undoubtedly linked to ‘wage compression’ in the civil service.

Compression was observed during the 1970s and 1980s due to more rapid wage increases

for lower-ranking civil servants. Figure 12 provides a dramatic example of this

phenomenon. Salaries of the lowest grade civil servants grew three times as fast as the

higher echelons between 1970 and the early 1990s. Since then, the ratio has stabilized.

Public-sector pensions — in their current form — are a very ineffective way of

dealing with this problem. While pensions do increase the remuneration of the workers with

the highest human capital, they also increase the compensation of the vast majority. Since

pensions are directly related to wages through the benefit formula, they simply reinforce the

compression of wages.

Figure 12: Civil service wage compression, Nepal 1970-2003

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

1970 1973 1976 1979 1982 1985 1988 1991 1994 1997 2000 2003

Ratio of salaries of second highest grade officers to lowest ranking civil servants in Nepal

Source: World Bank internal data.

18 It is also worth noting that there is likely to be a positive correlation between non-wage benefits and the rank of the civil servant that cannot be observed.

43

To conclude, the evidence rejects the proposition that more generous pensions are

justified in order for the public sector to compete for human resources. There are wage

differentials favoring the private sector, but mainly among the most educated civil servants.

Even when the case could be made to the contrary, a wage increase, rather than a

distortionary and parallel pension-scheme would seem to be the appropriate tool to address

the disparity.

Mobility

The second possible human-resource issue is the tenure of civil servants.

Governments, once they have attracted the correct staff, will wish to retain them. They

might also want to prevent conflicts of interest involving staff using information and

experience from public service in the private sector.19

The pension system penalizes mobile workers relative to those with full civil-service

careers in two ways. The first is through long vesting periods. People who leave the civil

service before their pension rights are ‘vested’ receive nothing from the system. The

minimum length of service to qualify for a pension benefit is shown for a range of countries

in Table 9. It varies enormously: from one year or less to 25 years.

19 The most common examples are procurement and regulators (for example, of utilities).

44

Table 9: Vesting periods for civil service schemes in selected countries

Length of service required OECD countries Non-OECD countries Zero/ less than one year

Canada Finland Netherlands Sweden Switzerland United Kingdom

Iran Morocco

Five years Belgium Germany Ireland Italy

10 years Cape Verde Hong Kong

15 years Austria France Portugal Spain

Bahrain Mauritius Senegal Tunisia Philippines West Bank/Gaza Yemen

20 years India 25 years Djibouti

Lebanon Source: authors.

Notes: India pays a partial pension after 10 years’ service. Mauritius pays a lump sum of one year’s salary after 10 years’ service. Senegal pays a partial pension after 15 years and a full pension after 30 years. Hong Kong pays a ‘short service gratuity’ to civil servants leaving with less than 10 years’ service

The second way in which the pension system impedes mobility is through the

treatment of ‘early leavers’. These are people whose pension rights are vested but who leave

the civil service before retirement. Table 10 shows how different countries treat such

workers. In Finland, the Netherlands and Sweden, for example, there is full transferability.

Workers move to private-sector mandatory (or quasi-mandatory) occupational plans with

similar benefits to the civil-service plan. In France, there is full ‘preservation’ of rights.

Workers’ accrued rights are indexed in line with civil service pay between leaving and

retirement. In other cases, moving jobs entails a pension ‘cost’. The following sections aim

to quantify these costs for some example countries.

45

Table 10: Portability and preservation of pension rights

Treatment Country Details Full transferability Finland

Sweden Netherlands

Workers transfer to private-sector mandatory (or quasi-mandatory) occupational plans with similar benefits

Full preservation France Workers’ accrued rights are indexed in line with civil service pay between leaving and retirement

Partial preservation United Kingdom Workers’ accrued rights are indexed in line with prices between leaving and retirement

Deferral without preservation Hong Kong Mauritius

Workers’ accrued rights are frozen in nominal terms

Loss of privilege Germany Cape Verde

Workers lose civil service pension rights but are credited with rights in national scheme

Source: authors.

The pension cost of leaving a civil-service job is defined as the difference between

the value of accrued pension rights on leaving and the value of accrued pension rights

conditional on staying until retirement. The streams of pension defined benefits can then be

converted to a net present value using standard actuarial techniques.

Figure 13 plots accrued pension rights by age for Mauritius. The dotted line shows

the value of accrued rights if the civil servant stays until retirement. This is simply a straight

line: each extra year adds 1/50th of final salary to the eventual pension benefit. The solid line

shows the value of accrued rights if the individual were to leave his or her job at that age.

Up to ten years’ service, the pension is zero. At that point, people become eligible for a

lump sum of one year’s salary. At 15 years’ service, people are eligible for a deferred pension

benefit. This is based on their current salary, with no adjustment to reflect pre-retirement

increases in the cost and standard of living. (Note that the modeling assumes 2.5 per cent

inflation and 2.5 per cent annual real earnings growth.) This is therefore still much lower

than the accrued rights would be if the individual were to remain until retirement.

Figure 14 converts these results into a measure of the cost of moving jobs. This is

the difference between the two values of accrued pension rights, discounted back from

retirement to current age (at a real discount rate of two per cent). The cost has been

normalized as a proportion of the current salary. On this measure, the penalty to mobility is

46

large at young ages because leaving results in a pension of zero while staying to retirement

gives multiples of pre-retirement salary for each year of service. The pre-retirement salary is

obviously much higher than current pay. The cost falls back once the individual is eligible

for a lump-sum payment, but the penalty for leaving just before pension rights are vested

reaches nearly eight times current salary. After vesting, there is still a large cost to moving

jobs because the deferred pension is based on current nominal earnings. As retirement age

approaches, the loss of pension benefit due to the difference in salary at retirement age and

current salary diminishes.

Figure 13: Value of accrued pension rights by age, Mauritius

age25 30 35 40 45 50 55 60

Value of accrued pension

leaving job

staying toretirement

lump sumdeferred pension

Source: Piggott and Whitehouse (2001).

47

Figure 14: The pension cost of moving jobs, Mauritius

age25 30 35 40 45 50 55 60

0

2

4

6

8 Cost of leaving,proportion ofearnings

Source: Piggott and Whitehouse (2001).

Figure 15 shows the net present value of accrued pension rights by years of service

for Cape Verde. The solid, grey line shows the civil service pension. This is a straight line,

reflecting the linear accrual of 2.94 per cent of final salary for each year of service. (This is

also because the discount rate that we have assumed is the same as the rate of growth of

individual earnings.)

The solid, black line shows the scheme for private-sector workers, the INPS. The

line jumps at three years because the individual becomes entitled to 24.5 per cent of the best

three of the final five years of salary at that point. It is then a straight line, again reflecting

the linear accrual and the equality of the discount rate and the rate of earnings growth.

48

Figure 15: Value of accrued pension rights by years of service, Cape Verde

0

2

4

6

8

10

12

14

16

18

0 5 10 15 20 25 30

Civil servicepension

INPS

Return ofcontributions

Discounted value of accrued pension rights,multiple of final salary

Years of service Source: authors’ calculations.

Individuals who leave with fewer than ten years of service have their contributions

returned. This is shown by the grey dotted line. From then onwards, they are

retrospectively transferred to the INPS if they leave before retirement. Thus, the true

schedule for benefits for a civil servant is the grey dotted line for the first ten years, then the

solid black line until they reach retirement, then the benefit is given by the grey, solid line.

We can therefore calculate a cost of leaving a civil service job at any point prior to

retirement, which is the difference between the value of accrued pension rights were the

individual to stay to retirement (the grey line) and the benefits actually received, as described

in the previous paragraph. The results of this calculation are shown in Figure 16.

49

Figure 16: Pension cost of leaving a civil-service job, Cape Verde

0

2

4

6

8

10

12

0 5 10 15 20 25 30Years of service

Difference in discounted valueof pension rights between moving jobs and staying to retirement,proportion of current salary

Return ofcontributions