Embed Size (px)

Citation preview

Claims Interest Group Claims Quorum

Knowledge versus training—what’s the difference? Does it matter?

I think that knowledge is the understanding of a concept. It is being learned on a subject. For example, one can be knowledgeable on the subject of construction labor, materials, and techniques. Sources of knowledge can include formal education, basic curiosity, and life experiences.

Training is specific to a task. It involves learning how to do something. No doubt, training has been an important part of our claims careers. An example of training is learning how to operate a property estimating software program. A training source could be a formal training session through an employer. The combination of these two examples, knowledge plus training, puts an adjuster in a position to write a quality property damage estimate that leads to a fair settlement of an insurance claim.

My career has included working as an adjuster, a manager, and an executive for a number of insurance companies. As a manager and an executive, I felt like I had the duty to provide training for individuals in my area of responsibility within the organization.

Knowledge is the responsibility of the individual. There is no shortage of opportunities for education offered by the insurance industry. Each claim presents a learning experience when we are open to it.

Understanding the difference between training and knowledge matters because growth in knowledge is an individual responsibility.

The 2013 CPCU Society Annual Meeting is October 26–29 in New Orleans. With over thirty educational sessions to choose from, you can experience training and knowledge while there. I hope to see you in New Orleans.

What’s in This Issue

Message From the Chair . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

West Fertilizer Company Explosion in Texas: The Importance of NFPA 921 in Fire and Explosion Subrogation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2

Loss Ratio—Better or Worse . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

Customer Service—What Does It Mean to Have a Customer Care Claim Service Attitude? . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

Using Social Media To Your Advantage: New Ways To Investigate Insurance Claims . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

Claims Interest Group Announces Schedule of Events for the Annual Meeting . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

The Cartoon Wars—Or—The Day The Theme Park Worlds Stood Still . . . . . . . . . . . . . . . . . . . . . 13

Point by Point Analysis—Ring of Fire or Arson Most Foul . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15

www.CPCUSociety.org | Visit us online.

Volume 31 | Number 3 | September 2013

Message From the Chairby James W. Beckley, CPCU, AIC, ARe, AIM

James W. Beckley, CPCU, AIC, ARe, AIM, is senior vice president of claims for American Agricultural Insurance Company, Schaumburg, Illinois. Beckley began his insurance career in 1980 with North Carolina Farm Bureau Mutual Insurance Company. From 1992 to 2004, he served at Farm Bureau Mutual Insurance Company of Idaho as vice president of claims. His current duties at American Agricultural Insurance Company include serving Farm Bureau client companies for their property-casualty reinsurance claims.

CPCU Society Claims Interest Group | Claims Quorum | September 20132

West Fertilizer Company Explosion in Texas:The Importance of NFPA 921 in Fire and Explosion Subrogationby Gary L. Wickert

Gary L. Wickert is an insurance trial lawyer and a partner at the law firm of Matthiesen, Wickert & Lehrer, S.C. He is an expert on insurance subrogation and has written several books and legal treaties concerning subrogation. Wickert also speaks nationally and internationally on subrogation and motivational topics. For more information, please contact Wickert at [email protected].

The following is reprinted with permission from Gary L. Wickert, Matthiesen, Wickert & Lehrer, S.C.

On April 17, 2013, a fire and explosion of historic proportions at the West Fertilizer Company in West, Texas ignited as much as 270 tons of ammonium nitrate being stored at the facility. The resulting blast left a 90-foot-wide crater and caused an estimated $125 million in damage. The blast killed 15 people, injured at least 200, and leveled both the plant and hundreds of homes and businesses. Matthiesen, Wickert & Lehrer, S.C. (MWL) was quickly engaged to hire experts, conduct an investigation, and aggressively subrogate for damages to over 275 nearby homes and businesses – some of which were completely destroyed. As we gather and prepare experts for the long investigation and litigation to follow, we are reminded of the importance of preserving evidence, avoiding and preventing spoliation, and selecting the appropriate experts whose investigation and opinions must comply with NFPA 921: Guide for Fire and Explosion Investigations.

Almost without exception, effective fire and explosion investigation and subrogation requires the involvement of competent origin and cause experts and one or more forensic

We’re always looking for quality article content for the Claims Interest Group newsletter. If you or someone you know has knowledge in a given insurance area that could be shared with other insurance professionals, we’re interested in talking with you.

Don’t worry about not being a journalism major. We have folks who can arrange and edit the content to publication-ready status. Here are some benefits of being a contributing writer to Claims Quorum:

• Sharing knowledge with other insurance professionals

• Gaining exposure as a thought leader or authority on a given subject

• Expanding your networking base

• Experiencing overall career development

To jump on this opportunity, please email either James W. Beckley, CPCU, AIC, ARe, AIM, at [email protected] or Denise Brown, CPCU, AINS, AIC, at [email protected].

Get Exposed

experts, depending on the nature of the loss. As much care should be taken in the selection of these experts as in the actual investigation and preparation for litigation and trial. Many origin and cause investigators in the U.S. are certified, either by the National Professional Qualifications Board through the National Fire Protection Association (NFPA) or by passing the Certified Fire Investigation (CFI) Program sponsored by the International Association of Arson Investigators. Private investigator licensing is controlled by each state. Forty-two (42) states and the District of Columbia have licensing requirements for private investigators. The stated purpose of licensing is to regulate the industry and to keep the unqualified out of the profession. Thirty-one (31) states’ laws contain language that specifically requires a private investigator’s license to investigate or reconstruct traffic accidents in private practice. For example, under the definition of private investigator, these states defines “private investigator” as the investigation by a person or persons for the purpose of obtaining information with reference to any of the following matters:

• Thecausesandoriginof,orresponsibilityfor, fires, libels, slanders, losses, accidents, damage or injuries to real or personal property; and

CPCU Society Claims Interest Group | Claims Quorum | September 2013 3

• Thebusinessofsecuringevidencetobeused before investigating committees or boards of award or arbitration or in the trial of civil or criminal cases and the preparation therefor.

Employees of any government agency, attorneys, insurance adjusters, and full time “in-house” investigators for insurance companies are generally exempt from the licensing requirement.

Forensic engineers are also essential players in piecing the fire and explosion puzzle together. Every step of the investigation must be undertaken with one thing in mind – testifying before a judge and jury. Depending on the nature of the incident, it may be necessary to engage electrical engineers, structural engineers, mechanical engineers, metallurgical engineers, fire protection engineers, and/or fire safety engineers. These engineers are engaged not only to prove who is responsible for the loss, but they are also engaged in many situations to prove damages, establish a causal relationship between the incident and the subrogation claim payments, to prove a lack of negligence on the part of the insured, or a variety of other purposes that all join forces to ensure a full subrogation recovery. Just as it is important for a coach and quarterback to be on the same page with regard to a game plan, it is just as important for all players on the subrogation team to be pulling in one direction with one goal in their sights. A professional engineer, however, is often prohibited from going beyond their expertise into areas of origin and cause investigators and vice versa. Some states will prohibit an engineer from testifying if they are not licensed private investigators or licensed engineers in the forum state. Pennsylvania Lumbermen’s Ins. Corp. v. Landmark Electric, 1993 WL 541644 (Ohio App. 1993).

Just as in a football game, however, the subrogation game must be played by established rules. In preparing and presenting expert testimony in depositions or at trial, rules of evidence play a significant role. You can’t win a football game without knowing the rules, and the same is true for the game of subrogation. All expert testimony is governed by the applicable state and federal rules of

evidence, and trial judges – acting as the game’s referees – determine who gets to play and who doesn’t. For years, the admissibility of expert scientific evidence was subject to the Frye test, based on Frye v. United States, 293 F. 1013 (D.D.C. 1923). Under the Frye test, only expert scientific evidence based on “generally accepted” principles in the scientific community was admissible. In 1973, the Federal Rules of Evidence were adopted. Rule 702 of the Federal Rules of Civil Procedure governs federal cases and is the basis on which evidence in many states is ruled on. It provides as follows:

Rule 702. Testimony by Expert Witnesses

A witness who is qualified as an expert by knowledge, skill, experience, training, or education may testify in the form of an opinion or otherwise if:

(a) The expert’s scientific, technical, or other specialized knowledge will help the trier of fact to understand the evidence or to determine a fact in issue;

(b) The testimony is based on sufficient facts or data;

(c) The testimony is the product of reliable principles and methods; and

(d) The expert has reliably applied the principles and methods to the facts of the case.

The Frye test was superseded by the U.S. Supreme Court decision in Daubert v. Merrell Dow Pharmaceuticals, Inc., 113 S.Ct. 2786 (1993). Daubert was a product liability action in which the plaintiffs sought to establish that the ingestion of a prescription drug caused birth defects. The Court limited its analysis to “scientific” knowledge and found that expert testimony must possess scientific validity to establish evidentiary reliability. Further, the Court found that “all relevant evidence is admissible” and that relevant evidence must “assist the trier of fact to understand the evidence or determine a fact in issue.” While the Court did not adopt “a definitive checklist or test” to determine the reliability of expert scientific testimony, it articulated four important factors:

1. Whether the theory or techniques can be (and has been) tested;

2. Whether the techniques or theory has been subjected to peer review and publication;

3. Whether the techniques employed by the expert have a known or potential rate of error and standards controlling the technique’s operations; and

4. Whether the theory or technique employed by the expert has been generally accepted by the scientific community.

The Daubert Court limited its decision to “scientific” knowledge and didn’t specify whether it would apply to technical or other specialized knowledge. The Daubert standard is now the law in federal court and in over half the states. However, the Frye standard remains the law in some jurisdictions. The Supreme Court in Kumho Tire Co., Ltd. v. Carmichael, 119 S.Ct. 1167 (1999) addressed expert testimony by a mechanical engineer in a defective tire case and held that a trial court’s ability to scrutinize and rule on the admissibility extended to all expert witnesses, not just scientific experts. As a result of these two decisions and the proliferation of spoliation of evidence claims, additional guidance was called for in fire and explosion cases.

The National Fire Protection Association was organized over 100 years ago in order to promote good scientific techniques and improve fire protection and prevention. But it wasn’t until 1992 that they published their first NFPA 921: Guide for Fire and Explosion Investigations. It concerned the determination of the origin and cause of fires and explosions and its purpose was to serve as a fire investigation guide and help improve the fire investigation process for both government and private sector employees with fire investigation responsibilities. NFPA 921: Guide for Fire and Explosion Investigations is made up of 19 chapters with two appendices. The chapters include: Administration; Basic Methodology; Basic Fire Science; Fire Patterns; Legal Considerations; Planning the Investigation; Sources of Information; Recording the Scene; Physical Evidence; Safety; Origin Determination; Cause Determination; Explosions; Electricity and Fire; Investigation of Motor Vehicle

continued on page 4

CPCU Society Claims Interest Group | Claims Quorum | September 20134

West Fertilizer Company Explosion in Texas:The Importance of NFPA 921 in Fire and Explosion Subrogationcontinued from page 3

Fires; Management of Major Investigation; Incendiary Fires; Appliances; and Referenced Publications.

NFPA 921: Guide for Fire and Explosion Investigations is only a “guide”, but it is fast becoming the standard by which fire investigations are judged. More and more it is accepted as a “peer-reviewed and generally accepted standard in the fire investigation community.” Tunnell v. Ford Motor Co., 330 F. Supp. 2d 707 (W.D. Va. 2004). Most courts are beginning to recognize that if properly applied, it provides a reliable fire causation determination methodology. Notably, NFPA 921 § 18.1 (“Fire Cause Determination”) provides that fire cause determination is the process of identifying the first fuel ignited, the ignition source, the oxidizing agent, and the circumstances that resulted in the fire. Fire cause determination generally follows origin determination. Consequently, a fire origin and causation expert will typically opine on two separate issues: the fire’s point of origin and its cause.

One of the greatest systemic faults within the subrogation industry is the fact that subrogation counsel – who are familiar with who is and who isn’t a qualified expert – are often brought into the game late, saddled with experts chosen by the insurance company months or years before they receive the file and long after the evidence is gone and the damaged building is repaired or rebuilt. The importance of selecting the right expert for the right loss cannot be over-emphasized. For simple losses a simple cause and origin expert might be sufficient. For more complex losses, such as the West Fertilizer Company explosion, it may be necessary to hire electrical, mechanical, chemical, or structural engineers for a number of reasons that go far beyond the cause of the fire. It is important to avoid “experts” who have never worked a day in the field in which they claim to be an expert, such as an automotive engineer who has never been trained at the manufacturer level or worked a career as a Field Service Engineer. It is said that such experts are referred to as “all horn and no driveshaft.”

An expert’s opinion is also only as good as the quality of the data used to arrive at that opinion. Far too often experts use words such as “undetermined”, “suspected”, or “possible” in their written reports – forever damaging recovery potential in that case. These words mean the expert doesn’t know what caused the fire and should serve as a warning that the expert’s opinion likely will not survive a challenge. If a hypothesis cannot be proven, it cannot be tested and is therefore unreliable. The process of eliminating all accidental causes of a fire resulting in the conclusion that human action is the culprit is limited to a very narrow set of circumstances. Any opinion of origin or cause (especially the latter) must be proven by the data or the fire must be classified as “undetermined” – a word which is not ordinarily followed by a recovery.

Any cause and origin expert used by the subrogation industry should be familiar with and willing to comply with NFPA 921: Guide for Fire and Explosion Investigations and Kirk’s Fire Investigation, the most widely used textbook in the field, written by John D. DeHaan, an expert from California. If your expert doesn’t have a copy of these two resources handy, find a new expert. Over the last 30 years, MWL has compiled a database of more than 25,000 experts from across the northern hemisphere, categorized and searchable by scientific discipline, geography, and cost. If you have a need for an expert in a particular jurisdiction, have losses resulting from the explosion at the West Fertilizer Company in Texas, or any subrogation questions, please contact Gary L. Wickert at [email protected].

CPCU Society Claims Interest Group | Claims Quorum | September 2013 5

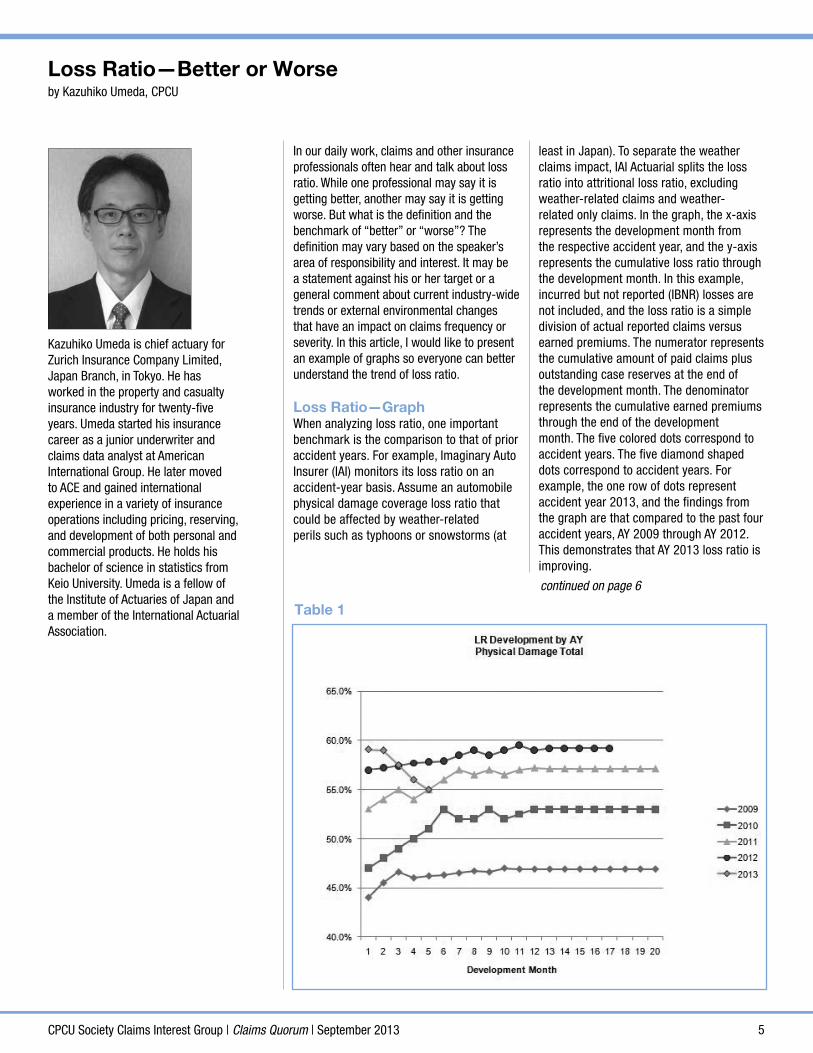

Loss Ratio—Better or Worseby Kazuhiko Umeda, CPCU

Kazuhiko Umeda is chief actuary for Zurich Insurance Company Limited, Japan Branch, in Tokyo. He has worked in the property and casualty insurance industry for twenty-five years. Umeda started his insurance career as a junior underwriter and claims data analyst at American International Group. He later moved to ACE and gained international experience in a variety of insurance operations including pricing, reserving, and development of both personal and commercial products. He holds his bachelor of science in statistics from Keio University. Umeda is a fellow of the Institute of Actuaries of Japan and a member of the International Actuarial Association.

In our daily work, claims and other insurance professionals often hear and talk about loss ratio. While one professional may say it is getting better, another may say it is getting worse. But what is the definition and the benchmark of “better” or “worse”? The definition may vary based on the speaker’s area of responsibility and interest. It may be a statement against his or her target or a general comment about current industry-wide trends or external environmental changes that have an impact on claims frequency or severity. In this article, I would like to present an example of graphs so everyone can better understand the trend of loss ratio.

Loss Ratio—GraphWhen analyzing loss ratio, one important benchmark is the comparison to that of prior accident years. For example, Imaginary Auto Insurer (IAI) monitors its loss ratio on an accident-year basis. Assume an automobile physical damage coverage loss ratio that could be affected by weather-related perils such as typhoons or snowstorms (at

continued on page 6

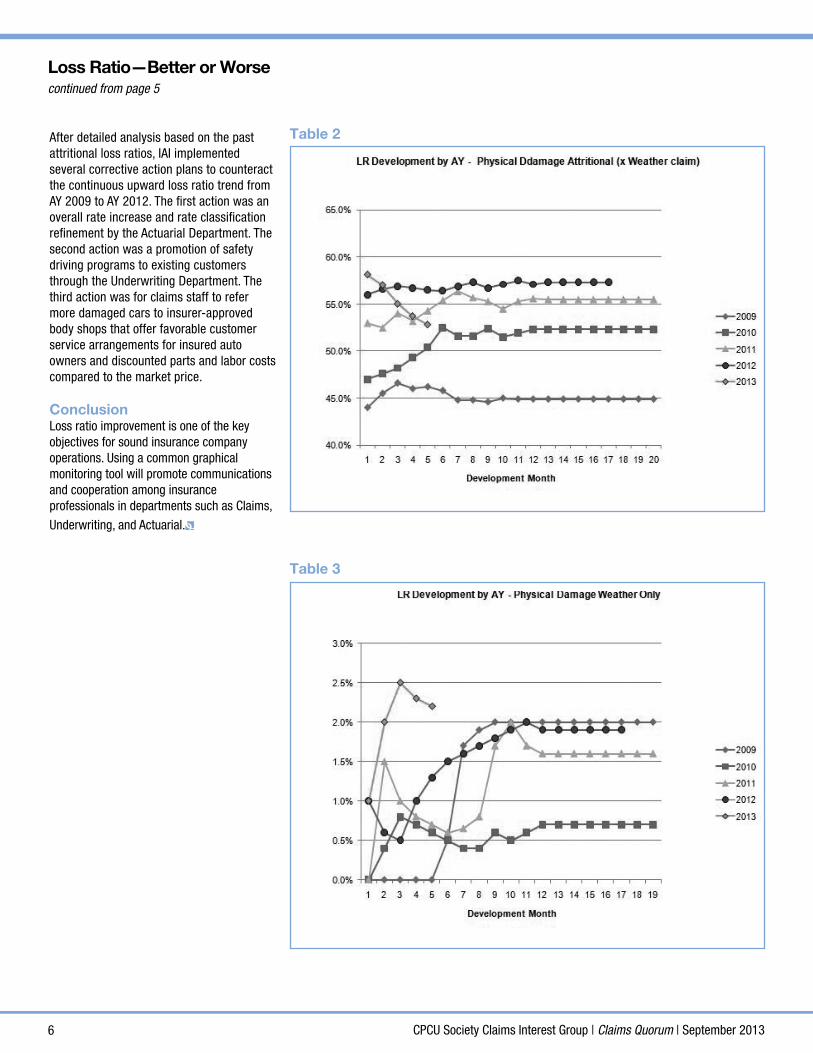

least in Japan). To separate the weather claims impact, IAI Actuarial splits the loss ratio into attritional loss ratio, excluding weather-related claims and weather-related only claims. In the graph, the x-axis represents the development month from the respective accident year, and the y-axis represents the cumulative loss ratio through the development month. In this example, incurred but not reported (IBNR) losses are not included, and the loss ratio is a simple division of actual reported claims versus earned premiums. The numerator represents the cumulative amount of paid claims plus outstanding case reserves at the end of the development month. The denominator represents the cumulative earned premiums through the end of the development month. The five colored dots correspond to accident years. The five diamond shaped dots correspond to accident years. For example, the one row of dots represent accident year 2013, and the findings from the graph are that compared to the past four accident years, AY 2009 through AY 2012. This demonstrates that AY 2013 loss ratio is improving.

Table 1

CPCU Society Claims Interest Group | Claims Quorum | September 20136

After detailed analysis based on the past attritional loss ratios, IAI implemented several corrective action plans to counteract the continuous upward loss ratio trend from AY 2009 to AY 2012. The first action was an overall rate increase and rate classification refinement by the Actuarial Department. The second action was a promotion of safety driving programs to existing customers through the Underwriting Department. The third action was for claims staff to refer more damaged cars to insurer-approved body shops that offer favorable customer service arrangements for insured auto owners and discounted parts and labor costs compared to the market price.

ConclusionLoss ratio improvement is one of the key objectives for sound insurance company operations. Using a common graphical monitoring tool will promote communications and cooperation among insurance professionals in departments such as Claims,

Underwriting, and Actuarial.

Table 3

Table 2

Loss Ratio—Better or Worsecontinued from page 5

CPCU Society Claims Interest Group | Claims Quorum | September 2013 7

Customer Service—What Does It Mean to Have a Customer Care Claim Service Attitude?by Rick Plunkett, CPCU, CIC, SCLA

Rick Plunkett has over 25 years multi-line claims experience in personal and commercial lines, including large or complex losses, coverage issues, and litigated cases. He has attended depositions and trials and settled numerous cases at mediation. Plunkett has extensive experience in management. He is knowledgeable in multi-state jurisdictions and managing multiple locations, as well as interacting with independent agents, independent adjusters, experts, and various service providers.

Plunkett has claim training, claim audit, and catastrophe duty experience. He has earned the CPCU, CIC, SCLA, AIC, and AIM designations.

A few years ago, I read a book titled It’s Called Work for a Reason! written by Larry Winget. In one of his chapters, “You Gotta Serve Somebody,” he covers customer service. He begins the chapter by asserting that customer service is a worn-out topic and he is “sick” of talking and hearing about it. Why does he feel this way? He believes that it is a subject beaten to death “and yet nothing seems to work” because the customer service that we receive is generally still bad. He contends that customer service is actually not that hard. I admit that I have to agree. His definition is rather simple: Do what you say you are going to do when you say you are going to do it in the way you said you were going to do it.

So why is there so much bad customer service? Winget’s answer is complacency. We are so used to receiving bad service that we see it as the expected. We put up with it, he contends, because we fear that if we complain, it only gets worse.

This reminds me of a personal experience from several years ago. My wife and I decided to visit a nearby eating establishment. We arrived in eager anticipation (after all, this was one of our favorite brand-name establishments), but that eagerness quickly dissipated. We were soon to get a customer service (or lack thereof) experience of a lifetime from something as simple as trying to get eating utensils.

After ordering a couple of salads, we realized we didn’t receive any forks. I went to the service counter and, after several moments of not having my presence acknowledged, cleared my throat and caught the attention of an employee working the cash register. She stared at me with a “What do you want?” look on her face, so I explained my dilemma (salads but no forks). She replied, “I don’t do forks.” After I managed to get her attention again (you can imagine my growing frustration), I asked for the person who did indeed do forks. She begrudgingly left and returned with the manager, who was equally unenthusiastic. When I described my dilemma

again, the manager said they must be out of forks. I asked her to look for some, but she refused, insisting that if they had any, they would be at the condiment station. When I asked her what she expected me to do, she actually replied, “I guess you’ll have to do the best you can.” My frustration was almost intolerable, but rather than cause a scene (the temptation was real), I simply returned to my seat where my wife and I proceeded to eat our salads with our spoons and fingers.

You may think the story ends here, but it does not. Just as we were nearing the end of our meal, I heard a commotion behind me and turned to find the manager restocking the condiment station with—you guessed it—a large box of forks! We finished our meal and left, but not without me muttering something about poor customer service and questioning our patronizing that particular establishment again. How could customer service be that poor? Yet it happens every day.

“What,” may you ask, “has all this to do with insurance claims?”

When an insurance company sells insurance policies, it does so with an expectation of service for the policyholder should a claim arise. Customer service is a future anticipation. When that time comes, we, as claim handlers, bring the policy to life. It is the service that we provide (proper response and handling of claims) that brings meaning to the policy.

Our goal as claim handlers is rather straightforward—resolve claims promptly and fairly. If we keep that one simple objective intently in focus, we will avoid most problems. Do what is right, and do it as quickly as we can—that is what I try to keep in front of my claims staff. Along with one more thing—do it with a little personality. Be friendly. Show people you care. Explain the process. Those go a long way towards making the claim process much more agreeable (or at least much less painful) for those presenting claims.

continued on page 8

CPCU Society Claims Interest Group | Claims Quorum | September 20138

Customer Service—What Does It Mean to Have a Customer Care Claim Service Attitude?continued from page 7

Why is this necessary? I believe most people face one or more of the following four factors when contacting an insurance company in a loss situation:

1. Something unpleasant or upsetting has just happened. No one likes seeing their property damaged, having to report about injured individuals, or having a claim made against them that is not their fault.

2. They have reservations or concerns about the process. How long is this going to take? What inconveniences am I going to have to endure? How much “red tape” will I face? A lot of anxiety can surface from not knowing the process.

3. Some individuals have a negative attitude towards insurance companies generated by misunderstandings, misconceptions, or because of the few instances where insurance companies have acted improperly. Unfortunately, a negative stereotype can harm the claim process, or at least make it more difficult.

4. The belief that in order to get a fair settlement, one must demand what is coming to him or her in an overly assertive or aggressive fashion when pursuing a claim against an insurance company. This probably arises more so from a feeling of needing to do what is necessary to protect one’s interest rather than simply from a nasty personality.

The above creates a dilemma for the claim handler. Not in all cases, but in many instances, the adjuster faces an individual who is not overly warm and inviting, but, instead, is frustrated, upset, doubting the whole process, worried over the outcome, and may be somewhat demanding. In such instances, human nature would dictate that an adjuster is put off by the lack of warmth and aggressive attitude. Herein lies an opportunity for claim handlers to shine. Rather than follow a path of what might be expected of the claim handler (unenthusiastic, rather matter of fact, and uninspired claim service), the claim handler can decide to “win the person over” with some outstanding customer service and quality claim handling.

This path results from the adjuster realizing that what they are experiencing with the policyholder or claimant does not result from any attack on them personally, but is because of frustration from the loss and concerns or questions about the outcome. At this moment, the claim handler has an opportunity to handle the claim in such a fashion to bring a “sigh of relief” to the individual with whom they are dealing, especially from a first-party claim perspective. In other words, it is trying to make the claim process as painless as possible. In doing so, as claim handlers, we make prompt contact, explain the process, do what we say we were going to do, and resolve claims in a timely manner while exhibiting a likeable personality with some genuine empathy.

An element of good customer service is not only going about our work in a way to avoid problems, but to respond appropriately when a genuine issue or concern has occurred. As human beings, we are not perfect, but we should take ownership when problems or concerns arise and do what we can to remedy the situation. Therefore, in many instances what starts out not so well can end on a positive note.

As claim professionals, I encourage you to take customer service seriously and to be committed to providing the best service possible. The ongoing challenge is not to be satisfied with the status quo, but to continually search for ways to improve processes and service. Roger Staubach said, “There are no traffic jams along the extra mile.”

Go that extra mile.

EndnoteLarry Winget, It’s Called Work for a Reason!: Your Success Is Your Own Damn Fault (New

York: Gotham, 2007), p. 172

CPCU Society Claims Interest Group | Claims Quorum | September 2013 9

Using Social Media To Your Advantage:New Ways To Investigate Insurance ClaimsBy Matthew Smith, Esq.

Matthew J. Smith, Esq., is the founder and president of Smith, Rolfes & Skavdahl Company, L.P.A., an insurance services law firm based in Cincinnati, Ohio, with six offices and providing insurance law services across the United States. He is a frequent lecturer across the country on the ethics of insurance claim investigations.

Note: The following is reprinted with permission. © Entire contents copyright 2013 by Claims Management magazine, a publication of The CLM. All rights reserved.

Is social media a fad or the biggest shift in society since the Industrial Revolution? I was attending an insurance conference in Washington, D.C. when that question flashed on the screen. It was a question I had never considered though I had lectured for years on the effect of electronic communications on insurance claims. Certainly I had never considered the impact of social media in the context of being more than the latest “fad” of communications. However, it did not take me long to fully comprehend the question of social media’s impact on our society is worth a much deeper analysis and its impact may be much more far-reaching than we comprehend today.

Most of us now use, or at least are aware of, the phenomena of social media. Even those from an older generation may not fully understand its implications, but recognize at least on some level its impact on our society. Today’s leaders such as Facebook™, Twitter™ and LinkedIn™ all may eventually fade away as technology and newer trends evolve, but the basic concept of social media is here to stay. Each new generation of the post Industrial Revolution era has developed their own “unique” form of communication, ranging from slang to different genres of music, but none has had the economic or world-wide impact social media has spawned in less than a decade. The future of this newest form of communication appears unbounded.

To understand the impact of social media, we must first consider an historical perspective. To reach fifty million users, the medium of radio required thirty-eight years, television thirteen, and the Internet only four. Facebook™ added double that number, signing on one hundred million users in less than nine months. If it were a country, Facebook™ would be the fourth largest in the world. The most recent statistics show

one of eight newly-married Americans met via social media. We are truly in a new era of communication, and the question for those of who handle insurance claims is not how we adapt, but how we thrive and utilize this new technology to investigate claims and battle against insurance fraud. To date, we have not done a very good job of keeping up with these new trends, or understanding how to use these new avenues to our strategic advantage.

The value of social media as an insurance investigation tool is unequalled in recent history. It affects all aspects of the insurance industry from how agents market and secure policies, through underwriting, and especially how we investigate insurance claims. The adage, “everyone wants to tell everything to everybody” remains true. Think of the person who tells you their life story while sitting next to you on an airplane, only because they know they will never see you again. In today’s era of communication, the way people are telling things they would not ordinarily say is via social media postings. Therein lays a wealth of information.

We have seen both fire and theft claims withdrawn when at an Examination Under Oath the claimant is shown postings found on Facebook™. In one case, an internet posting by the teenage son of a business owner on the morning of a building fire led to filing a petition to compel the son’s testimony. The insured refused to allow his son to testify since he was not an insured on the commercial policy. While “legally correct,” the judge ruled sufficient concern existed on the social media posting to grant the insurer’s petition compelling the son to testify and ordering the insurer not to make any coverage decision until the son complied. While rare, these are the first bold steps in creating new insurance law for the electronic era.

Utilizing social media effectively begins before the claim ever occurs. ISO and other similar organizations, and insurers themselves, are just beginning to consider what policy provisions need to updated, added or

continued on page 10

CPCU Society Claims Interest Group | Claims Quorum | September 201310

eliminated to comport with the electronic era. Making changes to the policy contract is only the beginning. It will take decades for courts to fully address and interpret the changes we are only beginning to consider today. By comparison, we have more than a century of case law interpreting policy terms, conditions, duties and exclusions. In the time it takes most lawsuits to go from filing to resolution, social media will add more users than the entire population of the U.S. and Canada combined! By the time current law has any chance of “catching up,” we may well be onto the next and newest form of electronic communication. Reality is, however, everything from the policy application process through the issuance or renewal of policies and the provisions contained in the written contract of insurance are changing at a greater pace than ever before in the insurance industry.

Consider whether your company has updated policy language to include in the duty to cooperate provisions even the most basic of steps such as providing electronic data, retrieval of information from computers and providing access to electronic communications including texts or social media postings. Most claim investigation authorization forms are outdated and do not include specific reference to allowing access to social media postings and electronic communications or retrieval of electronic data. In an abundance of caution, carriers should include authorization to access public social media postings and the duty of the claimant to provide access to private postings which may be relevant to the investigation. It is easier to change these types of authorization and claim forms than to undertake re-writing of the insurance policy which may require many layers of corporate review and also state insurance department approval.

These same investigative “updates” need to be considered in matters as simple as taking of recorded statements. When statements are taken, are you routinely asking the right questions of both claimants and witnesses to determine if around the time of the accident or incident any texts were sent, postings were made concerning the occurrence of the claim, or electronic photos were taken or sent? We have successfully downloaded incriminating text messages sent in the minutes before a fire, and on one claim retrieved cell phone pictures taken the night before the fire going room-by-room photographing all contents, including the interiors of drawers and closets. Adjusters, investigators and attorneys taking statements should secure as part of background information contact data including email addresses and identifying information for accounts on social media sites such as Facebook™, Twitter™ or Digg™ to name but a few.

An entire new industry exists to assist the insurance industry in the age of social media. While SIU or claims teams may not have the time, resources or ability to monitor a claimant’s social media postings “24/7,” there are companies which will do so for a fee. These companies will monitor primary, secondary and even obscure social media sites, blogs and forums tracking specific individuals by their email addresses or “user names”. Even if a post is made and immediately removed, or altered, these companies are often able to image the site and preserve the posting for later use in investigation or litigation. Many companies also provide background checks and reviews of social media postings by potential jurors before they are seated for trial. Attorneys provide the court-issued jury questionnaires and these companies will have sufficient data to locate, analyze and report any incriminating comments or evidence of bias a potential juror may not otherwise candidly disclose. These services will also monitor juror postings during and after the trial to identify actions in violation of the judge’s instructions, or posting opinions on the case or a potential verdict. Immediately after verdict, when released from service, often jurors may post quite candid comments on the case, witnesses, parties or attorneys in

Using Social Media To Your Advantage: New Ways To Investigate Insurance Claimscontinued from page 9

CPCU Society Claims Interest Group | Claims Quorum | September 2013 11

the case they just ruled upon. Even if you are not using these services, it is crucial to be aware your opponent may do so.

As part of an insurance investigation, also ask whether social media or electronic postings have been altered or deleted relative to the claim. You should specifically be questioning about services such as Reputation.Com, Reputation Builders and similar services promising to “clean up” a person’s social media or electronic postings. While this may often be done for employment purposes, it also affords a potentially fraudulent claimant the ability to attempt to “erase” something they wish they had never posted. These are the types of simple questions we often fail to ask because we are not keeping up with technology.

The duty also rests on investigative attorneys to be well-versed in all forms of new electronic communication, and covering these same areas of inquiry fully when questioning witnesses in both EUOs and depositions. Once a claim enters litigation, the insurance company and counsel have many more “tools” available to secure valuable electronic information. Many companies in today’s emerging social media and electronic communications fields will not release information, even with a signed authorization. Cell phone companies and social media sites are equally concerned about privacy issues, and frequently require subpoenas for release of records.

Written discovery, whether interrogatories or requests to produce, also must be updated to address new areas of communication. Background identification questions should be modified to include email addresses and social media identifiers as routinely as mailing addresses or telephone numbers. Specific questions, based on the facts of the case, should be included relevant to social media, electronic, cell phone or other emerging forms of communication. Even the mostly ignored definition section of written discovery should be updated to include definitions of terms including “social media,” “text messages” or “electronic communications”. Our Firm routinely includes written instructions detailing the

steps required to access and produce a complete copy of the respondent’s Facebook™ archive.

Attorneys and insurance companies need to be aware of the new area emerging regarding admissibility of social media evidence at trial. In the same manner debate raged a generation ago over whether photocopies were admissible in lieu of an original, battles are being fought today concerning electronic communications. Questions arise such as “what constitutes the original of a social media posting?” or “is the posting admissible at all if you prove it is from the person’s account, but they deny it is their posting?” Courts are sorting-out these issues to decide whether evidence should be admitted, excluded or admitted subject to potential impeachment or rehabilitation by the person claiming they did not actually make the posting.

The insurance industry has never been known to move forward rapidly or adapt quickly to change. The social media revolution is here and will remain for most of our work life expectancies. Fifteen years ago, we would have thought the idea “absurd” of emailing information concerning a claim or lawsuit. Today, most insurers are moving toward email as the primary method of communication concerning policy issues and claims. While those in a generation raised on letters sent via U.S. Mail and telephone calls may find this technology daunting, the reality is they will soon be replaced by a new generation being raised on social media and which already finds emails “outdated.” The generation which prefers texting and tweeting over emails will replace today’s adjusters and investigators in the workplace. The reality of the first “tweeted claim” is not in the future, but was actually received in our law firm six months ago.

The new reality of social media is here, and it may be the largest societal shift in more than a century. How we use this technology will define whether we stay ahead in the battle against insurance fraud or allow time and technology to pass us by. The future is now and we must face the challenge to adapt,

prepare or be left behind.

CPCU Society Claims Interest Group | Claims Quorum | September 201312

Claims Interest Group Announces Schedule of Events for the Annual Meetingby Kimberly Riordan

Kimberly A. Riordan, CPCU, AIC, is a litigation manager with Electric Insurance Company in Beverly, Mass. She is vice chair of the Claims Interest Group.

The Claims Interest Group is excited to host the following events at this year’s Annual Meeting.

“Oops…That’s English, but It Sounds Foreign to Me”Although the world would be boring if everyone were the same, communicating would certainly be easier! In the real world of cultural diversity and global business, insurance professionals must be sensitive to international differences. This session will help you navigate around the pitfalls of approaching an international claim by making cultural assumptions, introduce you to resources that mitigate claims culture clash and to technologies that improve claims handling processes, address cross-cultural differences, and detail regulatory requirements associated with cross-border claims. Test your knowledge of foreign terms through a fun quiz, and leave feeling much worldlier than when you came! Cosponsored with the International Insurance Interest Group. (Sunday, October 27, 2013; 10:00 a.m. to 11:30 a.m.)

“One if by Land, Two if by Sea: Cargo Theft Trends and the Impact on Claims”Cargo theft drains billions of dollars from the United States economy each year. The direct and indirect costs associated with it affect the insurance, retail, manufacturing, and transportation sectors. Largely unrecognized, it is a complex problem that has proved exceptionally difficult to curtail. Set against the backdrop of the busy port of New Orleans, this presentation will include a panel of experts with various perspectives who can share insight and real-life experiences on how cargo theft affects the way business is conducted, as well as best practices for investigating and adjusting cargo claims, recovering costs and merchandise, and mitigating risks. (Monday, October 28, 2013; 10:30 a.m. to 12:15 p.m.)

“Why Can’t We All Get Along? Claims Conundrums From All Perspectives”It is hardly a secret that claims personnel from insurance agencies and companies can experience tension when servicing mutual policyholders. What is not so well-known is how to establish ways to get along so that both mutual and competing interests are respected. Attendees of this interactive session will explore three claims scenarios from various perspectives and leave with agreed-upon best practices and methods of communicating. Come with an open mind and be prepared to release tension! (Tuesday, October 29, 2013; 8:00 to 10:00 a.m.)

“Swimming Upstream Against the New Wave of Social Media Claims”Please join us as well for the Claims Interest Group luncheon on Sunday, October 27, 2013, from 11:45 a.m. to 1:00 p.m. Our speaker will be Nancy Sylvester, CPCU, ARM-P, managing director of the Public Sector Division of Arthur J. Gallagher. Sylvester was named a “Power Broker” by Risk and Insurance in 2012 and 2013 as well as a “Responsibility Leader” by Liberty Mutual via Risk and Insurance in 2012. She has been awarded the “Women to Watch”

designation by Business Insurance and has been quoted numerous times in business insurance publications. Sylvester has received numerous awards from Gallagher, including the London Award for her work with Gallagher in the Lloyds of London Market, and several top producer honors. As a former risk manager and now leader within the property-casualty brokerage community, Sylvester presents regularly at conferences on claims, risk management, and other insurance topics.

Sylvester’s presentation at the Claims Interest Group luncheon will engage the audience in a discussion of changes in claims response driven by social media, and risk management challenges in the twenty-first century. How do we, as claims personnel, influence the communities and organizations we serve and bring common sense to differences that were incomprehensible ten years ago?

We look forward to seeing you in New Orleans

for another successful Annual Meeting!

continued on page 14

CPCU Society Claims Interest Group | Claims Quorum | September 2013 13

The Cartoon Wars—Or—The Day The Theme Park Worlds Stood StillBy Stanley Lipshultz, CPCU, J.D.

Stanley L. Lipshultz, CPCU, J.D., is a consultant and expert witness. He has been in the insurance industry for more than 40 years, including 30 years as a defense attorney for agents and brokers. Lipshultz is a past president of the CPCU Society District of Columbia Chapter and has served the Society as chair of the Diversity Committee; chair of the Coverage, Litigators, Educators & Witnesses Interest Group; and governor. He has been a speaker at numerous CPCU Society Annual Meetings and Seminars, and frequently makes presentations to agents and brokers.

Note: The following fictitious account depicts a claim scenario with hypothetical circumstances through an entertaining approach. While reading the facts of this case, readers should evaluate the handling of the claim and consider how they, as claims professionals, would provide guidance regarding denying or paying it. Please email analyses to Denise Brown, [email protected], who will publish the best one in the next issue of Claims Quorum.

Sosumi Golf & Aerospace subsidiary Animation Enterprises (AE) is a world-recognized leader in the development of cartoon technology. The inventors at AE have worked on a method of generating three-dimensional physical holographic images for use in theme parks. Holograms don’t get sick, go on strike, or need medical or dental benefits or their own 401K. They are not temperamental, and they are more realistic. The miniature Princess Leia hologram

projected by R2-D2 in Star Wars was an early creation of AE.

The cartoon characters are brought to life by the use of cutting-edge laser technology and computer-controlled emitters strategically placed in the parks. Because the use of the emitter technology is still not widely known, most visitors, and even the local government authorities, believe the holograms are actually costumed employees. Real people. Over a period of several years, human costumed cartoon characters have been phased out by management and replaced by the holographic images. By 2011, many theme parks had completely converted to holographic characters. The changeover was a well-kept secret, known only to a few. Even the costumed park employees did not know what had replaced them.

Ara N. Omitian is the most well-known insurance agent in the country, maybe even North America. His ancestor, Noah Omitian, was not only the first insurance agent in the New World, he wrote the first property policy that provided coverage for the Liberty Bell. Ara was the broker for Sosumi, which, by the way, is the largest global conglomerate in the world. Cyrus, “Sy” Onara, president of Sosumi, introduced Ara to the risk managers and CFOs of several of the largest theme parks in the United States and quickly became their exclusive insurance broker. Ara’s major insurer, Shifting Sands Mutual Insurance Company, worked with him to develop a national theme park program that quickly became the industry standard. Shifting Sands, being a bureau company, used standard forms for the package with its own manuscripted endorsements tailored to the theme park industry. While Shifting Sands’ underwriters had not been tagged as prescient, a cyber-security component was included in the theme park insurance package. As a result, nearly every major theme park was insured with Shifting Sands.

The holograms’ (actually the controllers’) work consisted of maneuvering their characters’ avatars around a big, sunny park filled with children and their parents. Making people smile. Waving. Being hugged by little

(and big) children. Having group pictures taken. Because the holograms were cartoon characters, they had three fingers on each hand—the industry standard. This was a holdover from the early days of cartoon animation when the animator had to hand draw twenty-four frames for each second of film, and then each frame had to be separately inked and painted. A simple labor-saving device. No one at the park noticed or cared about this anomaly. No one, that is, except Upto Nogood, Ph.D.

Dr. Nogood is one of the best cartoonist-scientists and computer geniuses of the twenty-first century. As a cartoonist, he was unsuccessful and fired from every major cartoon studio. Even though his talents as a scientist and computer wizard were widely recognized, he harbored a grudge against all those who failed to recognize his artistic talents.

Nogood is employed by Digiclone, a leading biotechnology company, to supervise its top-secret project for the cloning of human fingers and toes for transplants. He worked with several live viruses that were believed to accelerate the cloning process. Working in secrecy, on his own time and without the knowledge of his superiors, Nogood perfected a computer virus that mirrored a live virus. This computer virus was to be used to infect the hologram computer programs. It was designed to cause a fourth finger to appear on each hand of the cartoon characters.

The computer virus had a few flaws, including the mimicking of a bad flu on the holograms and a self-destruct tendency after fourteen months. Neither of these bugs was known until after the virus was unleashed. Nogood was in a hurry.

After visiting a number of theme parks, Nogood determined that security for the computer control rooms was essentially nonexistent. Using his credentials as a cartoonist-scientist, he was welcomed into the hologram control rooms across the country as a respected observer. Nogood was then able to introduce his virus by distracting the technicians and inserting a flash drive

CPCU Society Claims Interest Group | Claims Quorum | September 201314

The Cartoon Wars—Or—The Day The Theme Park Worlds Stood Stillcontinued from page 13

containing the virus into the main control server.

Beginning March 2011, the holographic cartoon characters began to sprout an extra finger on each hand. As these characters developed extra fingers, they also exhibited human flu-like symptoms and simply stopped functioning. As a result of the effect of the virus on the holographic employees, many parks were forced to shut down, some for weeks or months at a time until the cause of the problem was isolated. Pictures of the flu-infested four-fingered cartoon icons went viral. As everyone believed these were costumed humans, a primordial panic started to blossom about this flu spreading globally. Once the virus was finally detected, it was quarantined and destroyed. The holograms were reprogrammed; the flu-like symptoms and the extra fingers vanished. The theme parks reopened but to a greatly reduced number of patrons, causing considerable losses in revenue. The Florida parks, because of their large numbers, were the hardest hit—and they were about to face a problem of even greater magnitude: public servants serving the public.

Believing that the flu was a real threat, similar to the bird flu, for which there was no cure,

law enforcement and other civil authorities were very concerned, nervous even, about the possibility of the flu spreading. After several emergency sessions of local and national government officials, it was decided to shut down any theme park that employed cartoon-type characters. The justification was obvious: public safety was involved. An order was issued on June 1, 2011, closing, until further notice, all amusement and theme parks. The parks have yet to reopen.

Rather than reveal the secret of the cartoon holograms, the theme park owners submitted claims to Shifting Sands Mutual for losses, mostly business interruption. The workers’ compensation insurers (for the few remaining costumed human characters) are having just as difficult a time trying to decide whether cartoon characters can have compensable claims as they are about the nature of the injury. This case is focusing on Shifting Sands Mutual, which, as the largest theme park insurer, has received hundreds of claims for business interruption and property damage from its hundreds of insured theme parks across the nation.

Shifting Sands took a stout position: claim upon claim, denied! No business interruption coverage for the deluge of claims submitted

by theme parks across the country. Losses were totaling up to hundreds of millions of dollars. While awaiting the results of the anticipated skirmishes between Shifting Sands’ lawyers and their own, the theme park managers made a pragmatic decision. They decided to present property damage claims for the virus-infected holographic caricatures that inhabited the parks. The battery of attorneys for the theme parks extracted a promise, a guarantee that these claims would be kept in the strictest confidence by the claims personnel at Shifting Sands. Needles to say, there was no precedent for these claims, and there was a lot of head scratching about how to handle them. What are the holograms? Where was the coverage? Property? Electronic data processing? Business interruption?

The senior vice president, claims, of Shifting Sands was heard to say during one of many claims conferences, “Deny them all! We are not paying for a bunch of cartoons, even if they can walk and talk.” Meanwhile, Ara N. Omitian was on the precipice of exhaustion, racing across the country from one account to another, trying to calm his insureds by telling them, in his own inimitable way, “Don’t worry, everything is covered.”

And so, the battle lines are drawn, and the Cartoon Wars have begun. A class action lawsuit is brought for breach of contract for Shifting Sands’ refusal to pay for business interruption brought on by the closure because of civil authority and for property damage to the computer cartoon holograms.

You are retained as a claims consultant on behalf of Shifting Sands Mutual to assist in the coverage determination. Because the largest component of the claims is business interruption, your opinion is vital in assisting in the defense. Shifting Sands has downplayed the other claims, but is any other coverage applicable to the damaged holograms? Is the introduction of the virus and its effects covered?

The author retains all right title and interest and copyright ownership to the names of individuals, companies, and characters depicted in this article.

CPCU Society Claims Interest Group | Claims Quorum | September 2013 15

Point by Point Analysis—Ring of Fire or Arson Most FoulBy Clint Goodison, CPCU, AIC, AINS

Clint Goodison is risk manager for the Edmonds School District, Lynnwood, Wash., and the primary contact for the district’s risk pool. Goodison has more than twenty years of technical leadership experience in risk management, claims administration, and risk policy development. His background in claims administration and management of regional offices enables him to deal with organizations’ day-to-day insurance issues and big-picture needs.

In addition to holding a bachelor’s degree in business management, Goodison has earned the CPCU, AIC, and AINS professional designations.

Congratulations to Clint Goodison, CPCU, AIC, AINS, of Edmonds School District Number 15 for his response to the Claims Quiz published in the June issue of Claims Quorum. How does his comprehensive evaluation compare with yours?

Summary of Investigative Deficiencies:Jack neglected to interview the loan officer at Remington Steale to determine the size and terms of the loan of almost $7 million outstanding to Robophydeaux and Calliope. He totally discounted Calliope’s narrative of the last-minute preparations and made no attempt to locate any of the contractors who worked on the Sunday before the loss to verify her explanation. After Calliope was accused of arson, Current, who had accidently caused the fire, appeared. He had been afraid

to come forward because neither he nor his small company had liability insurance. The charges against Calliope were ultimately dismissed. Shifting Sands maintained its denial, per the account of the case: “…outside counsel opined that, because of the different standards of proof for criminal and civil trials, Shifting Sands should easily be able to establish Calliope as the arsonist.”

Shifting Sands intended to rely on the following:

An opinion from outside counsel that the company should continue to deny the claimConsidering the facts provided, I believe the Washington courts (as well as other states’ courts) would find that the insurer acted in bad faith in its unreasonable reliance on such an opinion. I would try to find other contrary cases and opinions to refute outside counsel’s opinion and to determine if any contrary opinions were readily available to Shifting Sands. Arguably, Shifting Sands unreasonably placed its own interests above Calliope’s interests.

Calliope’s unsavory financial history, including bankruptcy and a trail of unpaid billsCalliope’s attorney should argue relevance and make a motion in limine to suppress introduction of such evidence, as the probative value of this evidence is outweighed by the prejudice it would cause.

A questionable cause and origin of the fireCalliope’s attorney would need to hire an expert to refute Shifting Sands’ C&O expert. Presumably Current (the electrician) had a conscience, as he appeared after Calliope was charged with arson. I can only presume that his testimony was an important factor in the dismissal of the arson charge. His testimony at a civil trial should be sufficient to sway the jury in Calliope’s favor.

The electrician’s testimony—but, as a contractor, of course the electrician could not admit guilt, regardlessAgain, presumably Current had a conscience, so if properly questioned (during discovery and at trial), he probably would tell the truth. I’m also going to presume that Current gave a favorable (to Calliope) statement that led to

the dismissal. Presuming so, I would make every attempt to introduce the statement into evidence at the civil trial. At the very least, the statement would help to develop Current’s testimony.

Potential savings to the company of millions of dollarsHere again, Shifting Sands put its interests ahead of Calliope’s interests. If successfully argued, the jury may find that the insurer acted in bad faith to the detriment of its insured, Calliope.

Previous multimillion-dollar claims paid on behalf of a company with the same name and that manufactured the same productObjection, relevance. This matter involves a new owner, a new loss, and a new set of unrelated facts. Need I say more?

The preponderance of the evidence standard of proof if Calliope sues Shifting Sands for breach of contract, which would favor the insurerIt’s true that a civil lawsuit has a lesser burden of proof, but that is a two-way street, as Calliope need only prove, by the preponderance of the evidence, that Shifting Sands wrongfully, unreasonably, and in bad faith denied her claim.

Now it’s your turn. What would you do?Interview the loan officer to determine the size and terms of the loan, etc., to attack Shifting Sands’ motive theory; locate and interview the contractors to verify Calliope’s accounting of the night before the fire and provide her with an alibi; interview Current and develop the evidence to prove that his negligence was the cause of the fire. Proceed as outlined above and prepare for trial.

CPCU Society 720 Providence Road, Suite 100Malvern, PA 19355-3433

The Claims Interest Group newsletter is published by the CPCU Society’s Claims Interest Group.

Claims Interest Grouphttp://claims.CPCUSociety.org

ChairmanJames W. Beckley, CPCU, AIC, ARe, AIMAmerican Agricultural Insurance Company Email: [email protected]

EditorDenise Brown, CPCU, AINS, AIC InterWest Insurance Services, Inc. [email protected]

CPCU Society720 Providence Road, Suite 100Malvern, PA 19355-3433 (800) 932-CPCU (2728) www.CPCUSociety.org

Statements of fact and opinion are the responsibility of the authors alone and do not imply an opinion on the part of officers, individual members, or staff of the CPCU Society.

©2013 Society of Chartered Property and Casualty Underwriters

CPCU is a registered trademark of The Institutes.

FacebookLinkedIn

Address Service Requested

Claims Interest GroupClaims Quorum