Embed Size (px)

Citation preview

8/8/2019 Class Notes Eco 366

http://slidepdf.com/reader/full/class-notes-eco-366 1/14

8/27/2010 4:38:00 PM

1

Chapter1: Investments Background and Issues

y INVESTMENT: Current commitment of money or other resources in expectation of reapingfuture benefits.

y REAL ASSETS VS FINANCIAL ASSETS

y Real Asset: Asset used to produce goods and services (land, buildings, equipment,)

y Financial Assets: Claims on real assets or the income generated by them ( stocks, bonds)

A TAXONOMY OF FINANCIAL ASSETS:

y Three broad types of financial assets:

o Debt: (Fixed-income or debt securities) promise to pay a specified cash flow over a

specific period. The investment performance of debt securities typically is least

closely tied to the financial condition of the issuer.

o Equity: (Common Stock) represents an ownership share in a corporation. If the firm

is successful, equitys value will rise. Tend do be riskier than debt securities.

o Derivatives: (Options and futures contracts): Securities that provide payoff that

depends on values of other assets

FINANCIAL MARKETS AND THE ECONOMY

y The Informational Role of Financial Markets ( market analysis based on firms performance )

y Consumption Timing ( shift consumption power from high-earning to low-earning periods)

y Allocation of Risk ( allows investors to decide if they want to take risk)

y Separation of Ownership and Management ( more efficient management )

o AGENCY PROBLEM: Conflict between managers and stockholders.THE INVESTMENT PROCESS

y PORTOFLIO: collection of investment assets

y ASSET ALLOCATION: Allocation of an investment portfolio across broad asset classes (such

as stocks, bonds , real estate, commodities, etc)

y SECURITY SELECTION: Choice of specific securities within ach asset class.

y SECURITY ANALYSIS: Analysis of the value of securities

o TOP-DOWN Portfolio Creation: Starts with asset allocation, and then decides about

particular securities to include in portfolio

o BOTTOM-UP Portofio Creation: The portfolio is constructed from the securities that

seem attractively priced without as much concern for the resultant asset allocation.

Such a technique can result in unintended bets on one or another sector of the

economy.

MARKETS ARE COMPETITIVE

y The Risk-Return Trade-Off: higher-risk assets priced to offer higher expected returns than

lower-risk assed

8/8/2019 Class Notes Eco 366

http://slidepdf.com/reader/full/class-notes-eco-366 2/14

2

y Efficient Markets: We rarely expect to find bargains in security markets. Usually prices

reflect all the information available to investors concerning the value of the security.

o PASSIVE MANANGEMENT: Buying and holding a diversified portfolio without

attempting to identify mispriced securities

o ACTIVE MANAGEMENT: Attempting to identify mispriced securities or to forecast

broad market trends

THE PLAYERS

y Three Major Players:

o FIRMS: Are net borrowers, They raise capital now to pay for investment in plant and

equipment. The income generated by those real assets provides the returns to

investors who purchase the securities issued by the firm

o HOUSEHOLDS: typically are net savers. They purchase the securities issued by the

firms that need to raise funds

o GOVERMENTS: Can be borrowers or lenders. If deficit, then borrower.

y Financial Intermediaries: Institutions that connect borrowers and lenders by accepting fundsfrom lenders and loaning funds to borrowers.

y Investment Companies: Firms managing funds for investors. An investment company may

manage several mutual funds

y Investment Bankers: Firms specializing in the sale of new securities to the public, typically by

underwriting the issue.

o PRIMARY MARKET: A market in which new issues of securities are offered to the

public

o SECONDARY MARKET: A market in which previously issued securities are traded

among investors.

RECENT TRENDS:

y Globalization: Tendency toward a worldwide investment environment and the integration of

international capital markets

y Securitization: Pooling loans into standardized securities backed by those loans, which can

be then traded like any other security

o PASS-THROUGH SECURITIES: Pools of loans (such as home mortgage loans) sold in

one package. Owners of pass-troughs receive all of the principal and interest

payments made by the borrowers.

y Financial Engineering: creation of new securities by bundling and unbundling securities into

a composite security. Also, the process of creating and designing securities with custom-tailored characterisitcs.

o BUNDLING (combining) UNBUNDLING (breaking up). Creation of new securities from

primitive and derivatives securities.

8/8/2019 Class Notes Eco 366

http://slidepdf.com/reader/full/class-notes-eco-366 3/14

3

CHAPTER2: ASSET CLASSES AND FINANCIAL INSTRUMENTS

THE MONEY MARKET: is a subsector of the debt market. It consists of very short-term debt securities(

highly marketable ). It includes short-term, highly liquid and low-risk debt instruments

y TREASURY BILL: (T-Bill) is most marketable of all money market instruments. The

government raises money by selling bills to the public. They are issued at a discount from

face value and return the face amount at maturity. T-bills sell in minimum denominations of

$1000. While income earned on T-bills is taxable at the federal level, it is expemt from all

state and local taxes.

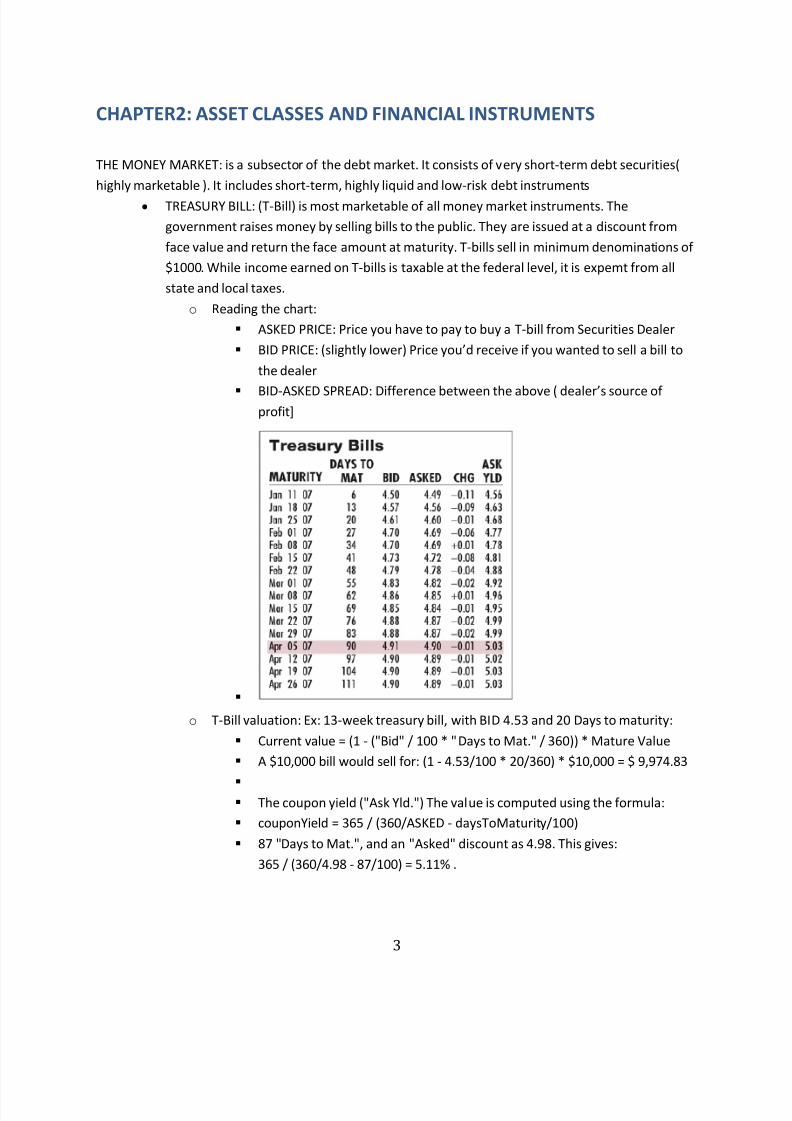

o Reading the chart:

ASKED PRICE: Price you have to pay to buy a T-bill from SecuritiesDealer

BID PRICE: (slightly lower) Price youd receive if you wanted to sell a bill to

the dealer

BID-ASKED SPREAD: Difference between the above ( dealers source of profit]

o T-Bill valuation: Ex: 13-week treasury bill, with BID 4.53 and 20 Days to maturity:

Current value = (1 - ("Bid" / 100 * "Days to Mat." / 360)) * Mature Value

A $10,000 bill would sell for: (1 - 4.53/100 * 20/360) * $10,000 = $ 9,974.83

The coupon yield ("Ask Yld.") The value is computed using the formula:

couponYield = 365 / (360/ASKED - daysToMaturity/100)

87 "Days to Mat.", and an "Asked" discount as 4.98. This gives:

365 / (360/4.98 - 87/100) = 5.11% .

8/8/2019 Class Notes Eco 366

http://slidepdf.com/reader/full/class-notes-eco-366 4/14

4

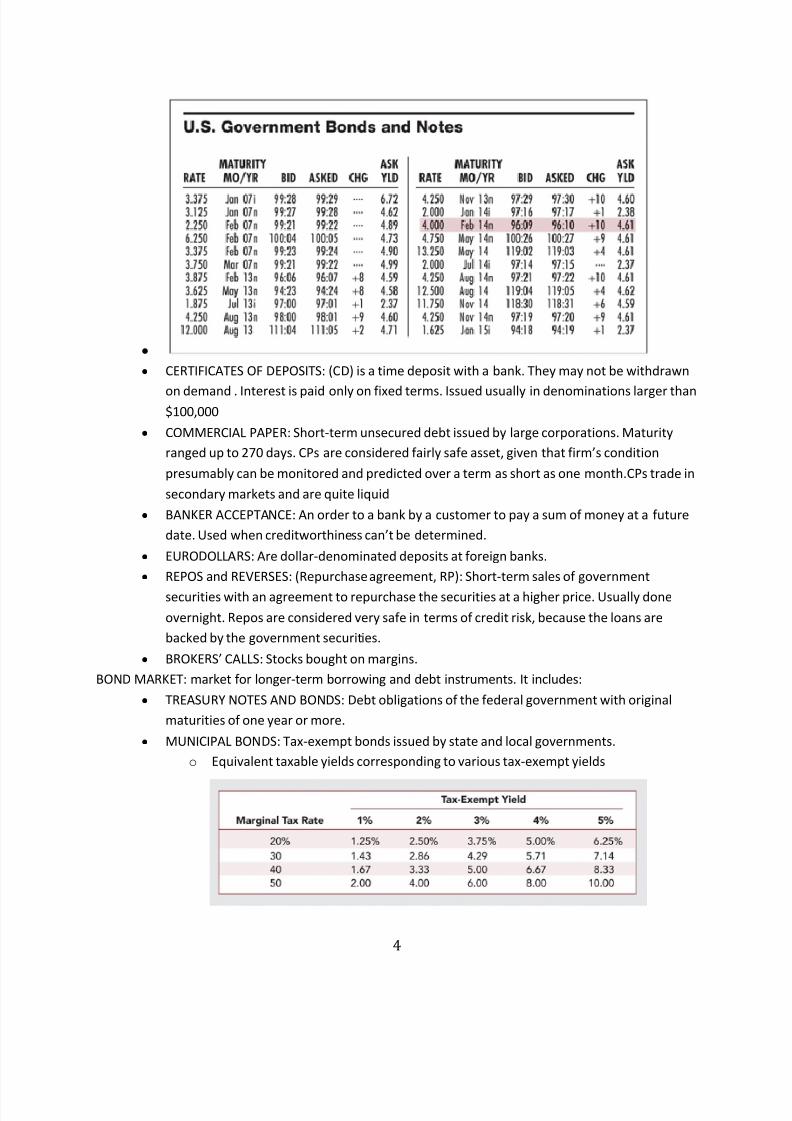

y y CERTIFICATES OF DEPOSITS: (CD) is a time deposit with a bank. They may not be withdrawn

on demand . Interest is paid only on fixed terms. Issued usually in denominations larger than$100,000

y COMMERCIAL PAPER: Short-term unsecured debt issued by large corporations. Maturity

ranged up to 270 days. CPs are considered fairly safe asset, given that firms condition

presumably can be monitored and predicted over a term as short as one month.CPs trade in

secondary markets and are quite liquid

y BANKER ACCEPTANCE: An order to a bank by a customer to pay a sum of money at a future

date. Used when creditworthiness cant be determined.

y EURODOLLARS: Are dollar-denominated deposits at foreign banks.

y REPOS and REVERSES: (Repurchase agreement, RP): Short-term sales of government

securities with an agreement to repurchase the securities at a higher price. Usually done

overnight. Repos are considered very safe in terms of credit risk, because the loans are

backed by the government securities.

y BROKERS CALLS: Stocks bought on margins.

BOND MARKET: market for longer-term borrowing and debt instruments. It includes:

y TREASURY NOTES AND BONDS: Debt obligations of the federal government with original

maturities of one year or more.

y MUNICIPAL BONDS: Tax-exempt bonds issued by state and local governments.

o Equivalent taxable yields corresponding to various tax-exempt yields

8/8/2019 Class Notes Eco 366

http://slidepdf.com/reader/full/class-notes-eco-366 5/14

5

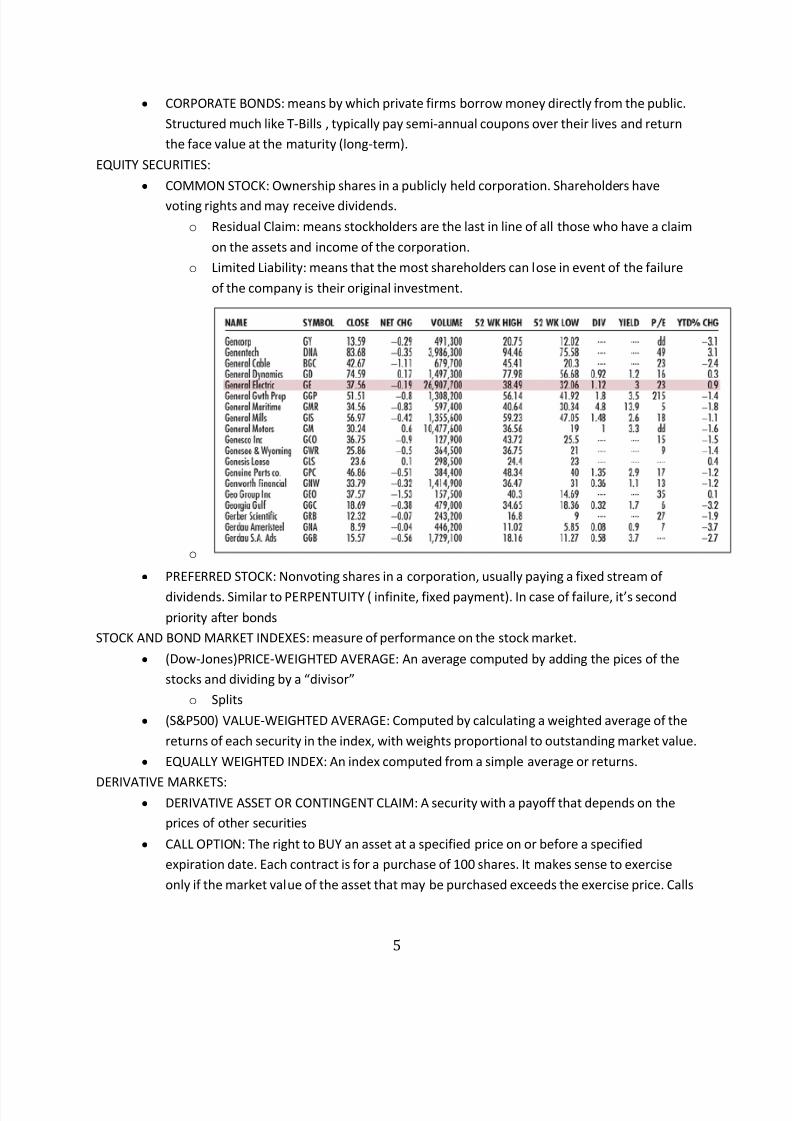

y CORPORATE BONDS: means by which private firms borrow money directly from the public.

Structured much like T-Bills , typically pay semi-annual coupons over their lives and return

the face value at the maturity (long-term).

EQUITY SECURITIES:

y COMMON STOCK: Ownership shares in a publicly held corporation. Shareholders have

voting rights and may receive dividends.

o Residual Claim: means stockholders are the last in line of all those who have a claim

on the assets and income of the corporation.

o Limited Liability: means that the most shareholders can lose in event of the failure

of the company is their original investment.

o y PREFERRED STOCK: Nonvoting shares in a corporation, usually paying a fixed stream of

dividends. Similar to PERPENTUITY ( infinite, fixed payment). In case of failure, its second

priority after bonds

STOCK AND BOND MARKET INDEXES: measure of performance on the stock market.

y (Dow-Jones)PRICE-WEIGHTED AVERAGE: An average computed by adding the pices of the

stocks and dividing by a divisor

o Splits

y (S&P500) VALUE-WEIGHTED AVERAGE: Computed by calculating a weighted average of the

returns of each security in the index, with weights proportional to outstanding market value.

y EQUALLY WEIGHTED INDEX: An index computed from a simple average or returns.

DERIVATIVE MARKETS:y DERIVATIVE ASSET OR CONTINGENT CLAIM: A security with a payoff that depends on the

prices of other securities

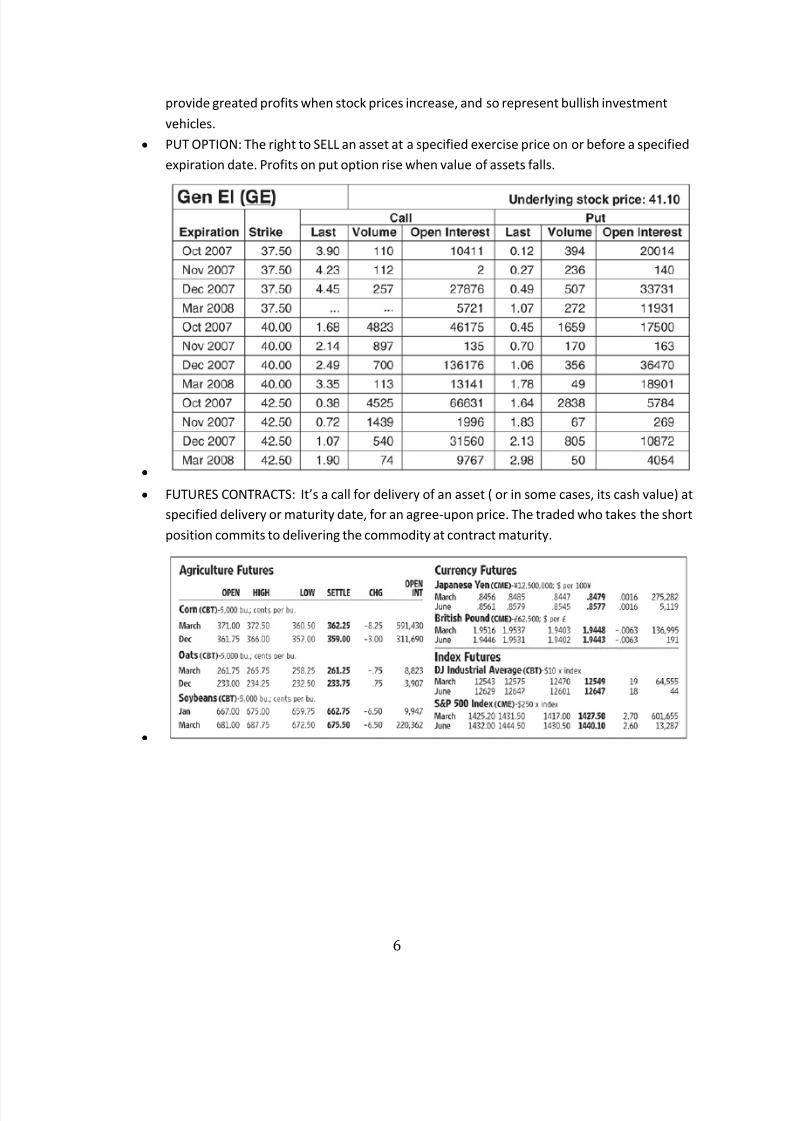

y CALL OPTION: The right to BUY an asset at a specified price on or before a specified

expiration date. Each contract is for a purchase of 100 shares. It makes sense to exercise

only if the market value of the asset that may be purchased exceeds the exercise price. Calls

8/8/2019 Class Notes Eco 366

http://slidepdf.com/reader/full/class-notes-eco-366 6/14

6

provide greated profits when stock prices increase, and so represent bullish investment

vehicles.

y PUT OPTION: The right to SELL an asset at a specified exercise price on or before a specified

expiration date. Profits on put option rise when value of assets falls.

y y FUTURES CONTRACTS: Its a call for delivery of an asset ( or in some cases, its cash value) at

specified delivery or maturity date, for an agree-upon price. The traded who takes the short

position commits to delivering the commodity at contract maturity.

y

8/8/2019 Class Notes Eco 366

http://slidepdf.com/reader/full/class-notes-eco-366 7/14

7

CHAPTER 3: SECURITIES MARKETS

y IPO: Initial Public Offering is a first sale of stock by a formerly private company

y UNDERWRITERS: Underwriters purchase securities from the issuing company and resell

them.

y PROSPECTUS: A description of the firm and the security it is issuing.

y Shelf Regulation: Introduced in 1982, improved rule 415 which allows firms to register

securities and gradually sell them to the public for two years following the initial

registrations.

y PRIVATE PLACEMENT: Primary offerings in which shares are sold directly to a small group of

institutional or wealthy investors. Private placements can be far cheaper than public

offerings.

y IPOs:

o Once initial comments by SEC come in, the Investment bankers organize roadshows

in which they travel around the country to publicize the imminent offering. Theygenerate interest among potential investors and provide information about the

offering and price at which they will be able to market the securities.

o Large investors communicate their interest, and the process of polling potential

investors is called bookbuilding.

o IPOs commonly are underpriced compared to the price at which they could be

marketed. Such underpricing is reflected in pirce jumps that occur on the date when

the share are first traded in public security markets.

o While explicit costs of an IPO tend to be around 7%, of the funds raised, such

underpricing should be viewed as another cost of the issue.

HOW SECURITIES ARE TRADED:

y Types of Markets:

o DIRECT SEARCH MARKET: is the least organized market. Buyers and sellers must

seek each other out directly. (ex. Sale of an old fridge thru Craigslist)

o BROKERED MARKET: Brokers find it profitable to offer search services to buyers and

sellers. ( ex. Real estate market)

o DEALER MARKET: Markets in which traders specializing in particular assets buy and

sell for their own accounts, and sell them for profit. Saves time in search, makes

money on the bid-ask spread. (ex. OTC securities market)

o AUCTION MARKET: A market where all traders meet at one place to buy or sell anasset. Advantage is that no one need to search across dealers to find the best price.

People arrive at mutually agreeable prices and save the bid-ask spread.

y Types of Orders:

o Market Orders: Orders to buy or sale that are to be executed immediately at current

market price.

o Price-contingent Orders: Orders specifying at which price to execute.

8/8/2019 Class Notes Eco 366

http://slidepdf.com/reader/full/class-notes-eco-366 8/14

8

LIMIT BUY ORDER: Instructs the broker to buy X number of shares when

price is at or below the stipulated price.

LIMIT SELL ORDER: Instructs the broker to sell X number of shares if and

when the stock price rises above specified limit.

STOP-LOSS ORDER: Instructs the broker to sell the stock if its price falls

below a stipulated level ( it lets you stop further losses when prices are

falling)

STOP-BUY ORDER: Specifies that stock should be bought when its price rises

above a limit.

o SHORT SALE: Sale of securities you dont own but have borrowed from your broker

o TRADING MECHANISMS:

OTC MARKET: An informal network of brokers and dealers who negotiate

sales of securities

ECNs: Computer networks that allow direct trading without the need for

market makers. SPECIALIST MARKET: A trader who makes a market in the shares of one or

more firms and who maintains a fair and orderly market by dealing

personally in the market.

BLOCK TRANSACTIONS: Large transactions in which at least 10,000 shares of

stock are bought or sold.

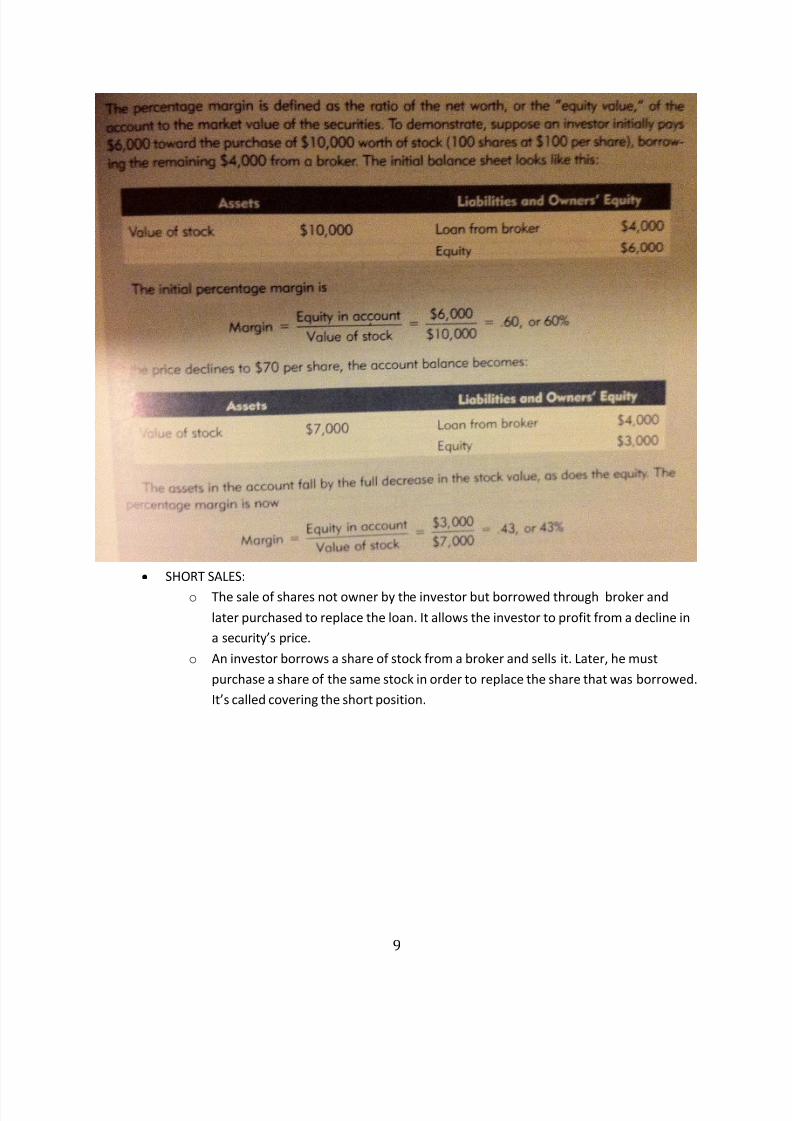

y BUYING ON MARGIN:

y MARGIN: Describes securities purchase with money borrowed in part from a broker. The

margin is the net worth of the investors account.

8/8/2019 Class Notes Eco 366

http://slidepdf.com/reader/full/class-notes-eco-366 9/14

9

y SHORT SALES:

o The sale of shares not owner by the investor but borrowed through broker and

later purchased to replace the loan. It allows the investor to profit from a decline in

a securitys price.

o An investor borrows a share of stock from a broker and sells it. Later, he must

purchase a share of the same stock in order to replace the share that was borrowed.

Its called covering the short position.

8/8/2019 Class Notes Eco 366

http://slidepdf.com/reader/full/class-notes-eco-366 10/14

10

CHAPTER 4: Mutual Funds and Other Investment Companies

y INVESTMENT COMPANIES: are financial intermediaries that invest the funds of individual in

securities or other assets. Key functions include:

o Record Keeping and administration: issue reports, keep track of capital gains,

dividends,

o Diversification and divisibility: By pooling their money, investment companies

enable investors to hold fractional shares of many different securities. They act like

a large investor, even when shareholder is too small to do so.

o Professional Management: They have full-time staff of security analysts and

portfolio managers, who attempt to achieve superior investment results for their

investors.

o Lower transaction costs: They trade large blocks of securities, achieving substantial

savings on brokerage fees and commissionsy NET ASSET VALUE: (NAV) Assets minus liabilities expressed on a per-share basis

o

y TYPES OF INVESTMENT COMPANIES:

o Unit Investment Trusts: Money pooled from many investors that is invested in a

portfolio fixed for the life of the fund

o Managed Investment Companies: There are two types, closed-end and open-end.

Theres a board of directors elected by the shareholders, which later hires

management company for a fee ranging from .2% to 1.5% of asset values.

o LOAD: A sales commission charged on a mutual fund

o OPEN-END FUND: A fund that issues or redeems its shares at net asset value. When

investors wish to cash out their shares, they sell them back to the fund at NAV.

o CLOSE-END FUND: Shares may not be redeemed, but instead are traded at prices

that can differ from NAV. Funds dont redeem or issue shares. If investors want to

cash out, they must sell their shares to other investors. Shares are traded at an

organized exchange and can be purchased thru brokers .

8/8/2019 Class Notes Eco 366

http://slidepdf.com/reader/full/class-notes-eco-366 11/14

11

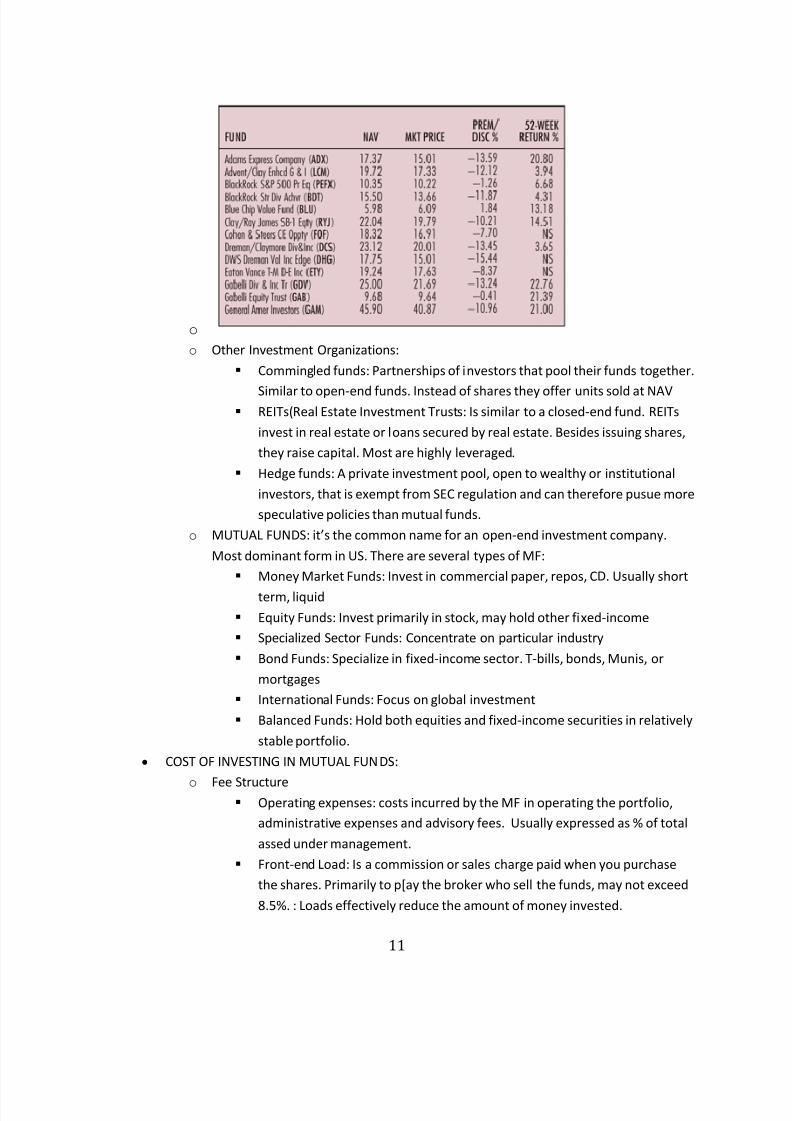

o o Other Investment Organizations:

Commingled funds: Partnerships of investors that pool their funds together.

Similar to open-end funds. Instead of shares they offer units sold at NAV REITs(Real Estate Investment Trusts: Is similar to a closed-end fund. REITs

invest in real estate or loans secured by real estate. Besides issuing shares,

they raise capital. Most are highly leveraged.

Hedge funds: A private investment pool, open to wealthy or institutional

investors, that is exempt from SEC regulation and can therefore pusue more

speculative policies than mutual funds.

o MUTUAL FUNDS: its the common name for an open-end investment company.

Most dominant form in US. There are several types of MF:

Money Market Funds: Invest in commercial paper, repos, CD. Usually short

term, liquid

Equity Funds: Invest primarily in stock, may hold other fixed-income

Specialized Sector Funds: Concentrate on particular industry

Bond Funds: Specialize in fixed-income sector. T-bills, bonds, Munis, or

mortgages

International Funds: Focus on global investment

Balanced Funds: Hold both equities and fixed-income securities in relatively

stable portfolio.

y COST OF INVESTING IN MUTUAL FUNDS:

o Fee Structure Operating expenses: costs incurred by the MF in operating the portfolio,

administrative expenses and advisory fees. Usually expressed as % of total

assed under management.

Front-end Load: Is a commission or sales charge paid when you purchase

the shares. Primarily to p[ay the broker who sell the funds, may not exceed

8.5%. : Loads effectively reduce the amount of money invested.

8/8/2019 Class Notes Eco 366

http://slidepdf.com/reader/full/class-notes-eco-366 12/14

12

Ex: each $1000 paid fro a fund with a 6% load, results in sales

charge of $60 and fund investment of only $940. You need

cumulative returns of 6.4% of your net investment (60/940=.064)

just to break even

Back-end Load: Is a redemption or exit fee incurred when you sell your

shares. Typically around 5-6%, they are known as contingent deferred sales

charges)

12b-1 charges: limited to 1% of NAV, are used to pay for distribution costs,

advertising, promotional literature, commission paid to brokers who sell the

fund to investors.

o Mutual Fund Returns

Soft dollars: The value of research services brokerage house provides free

of charge in exchange for the investment managers business Turnover: The ratio of trading activity of a portfolio to the assets of the

portfolio

Exchange-traded Funds: (ETF) Offshoots of mutual funds that allow

investors to trade index portfolios.

8/8/2019 Class Notes Eco 366

http://slidepdf.com/reader/full/class-notes-eco-366 13/14

8/27/2010 4:38:00 PM

13

8/8/2019 Class Notes Eco 366

http://slidepdf.com/reader/full/class-notes-eco-366 14/14

8/27/2010 4:38:00 PM

14

Table of contents of 8th ed:

Part 1: Elements of Investments

1 Investments: Background and Issues

2 Asset Classes and Financial Instruments

3 Securities Markets

4 Mutual Funds and Other Investment Companies

Part 2: Portfolio Theory

5 Risk and Return: Past and Prologue

6 Efficient Diversification

7 Capital Asset Pricing and Arbitrage Pricing Theory

8 The Efficient Market Hypothesis

9 Behavioral Finance and Technical Analysis

Part 3: Debt Securities

10 Bond Prices and Yields

11 Managing Bond PortfoliosPart 4: Security Analysis

12 Macroeconomic and Industry Analysis

13 Equity Valuation

14 Financial Statement Analysis

Part 5: Derivative Markets

15 Options Markets

16 Option Valuation

17 Futures Markets and Risk Management

Part 6: Active Investment Management

18 Portfolio Performance Evaluation

19 Globalization and International Investing

20 Hedge Funds

21 Taxes, Inflation, and Investment Strategy

22 Investors and the Investment Process