Embed Size (px)

Citation preview

1

1

CLASSIFYING & SOURCING

PAYMENTS TO FOREIGN INDIVIDUALS

CLASSIFYING & SOURCING

PAYMENTS TO FOREIGN INDIVIDUALS

Presented By:Presented By:Michael Sattin Michael Sattin

Payroll ServicesPayroll Services

2

2

TODAY’S AGENDA• What does Classifying & Sourcing mean?• Why are Classifying & Sourcing important?• How does Classifying & Sourcing relate to

income for NRA?• Review of various payment categories

•Define and describe each payment•Source the income•Appropriate payment Venue•Documentation for each payment

3

3

What does Classifying & Sourcing Mean?

Classify:– to assign to a category

Source:- a point of origin or procurement

Merriam-Webster DEFINITIONS:

4

4

Why are Classifying & Sourcing Important?

Classify It is the basis in which income is

taxed

Source A NRA for tax purposes is subject to

U.S. tax on U.S. sourced income

5

5

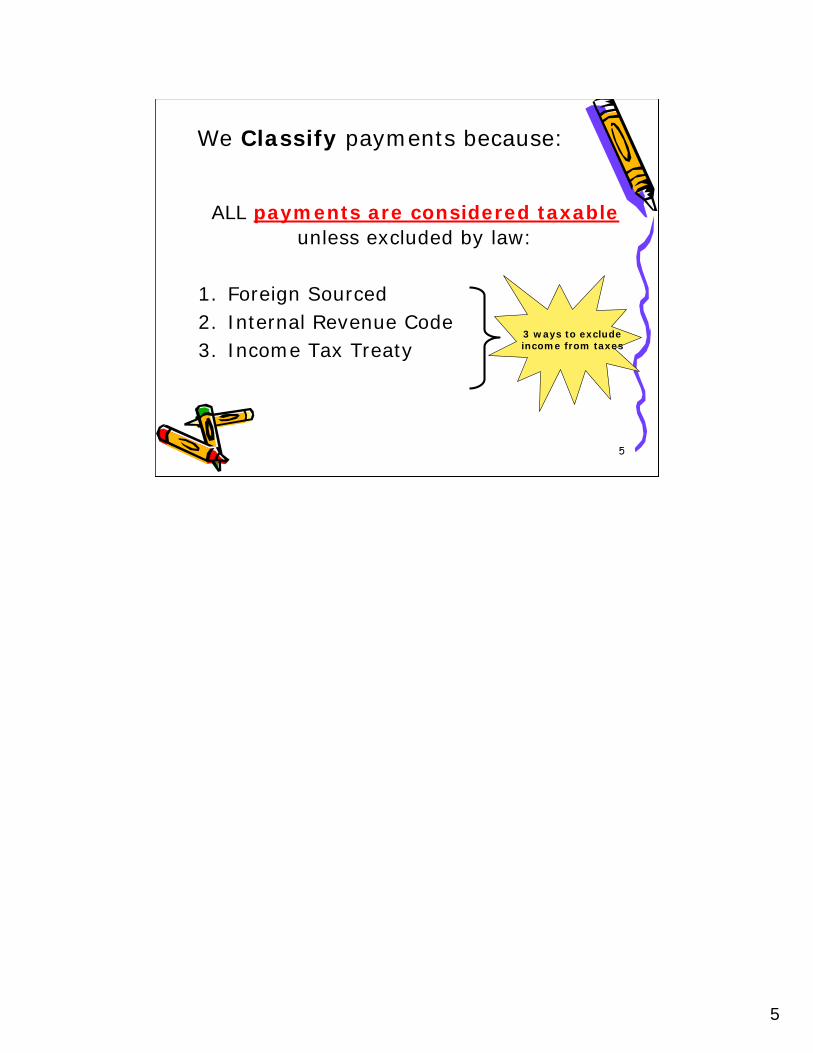

We Classify payments because:

ALL payments are considered taxableunless excluded by law:

1. Foreign Sourced2. Internal Revenue Code3. Income Tax Treaty

3 ways to exclude income from taxes

6

6

Various Payments UC Pays to NRA

• Compensation– Wages, Salaries– Benefits

(Fringe/Health)• Awards

– Prize• Fellowship/Scholarship

– Service portion of F/S• Stipend• Lecture Fee

SERVICE NON SERVICE

• Travel• Pensions• Prizes• Awards• Reimbursements• Royalties• F/S• Visa Fees• Rents• Honorarium

7

7

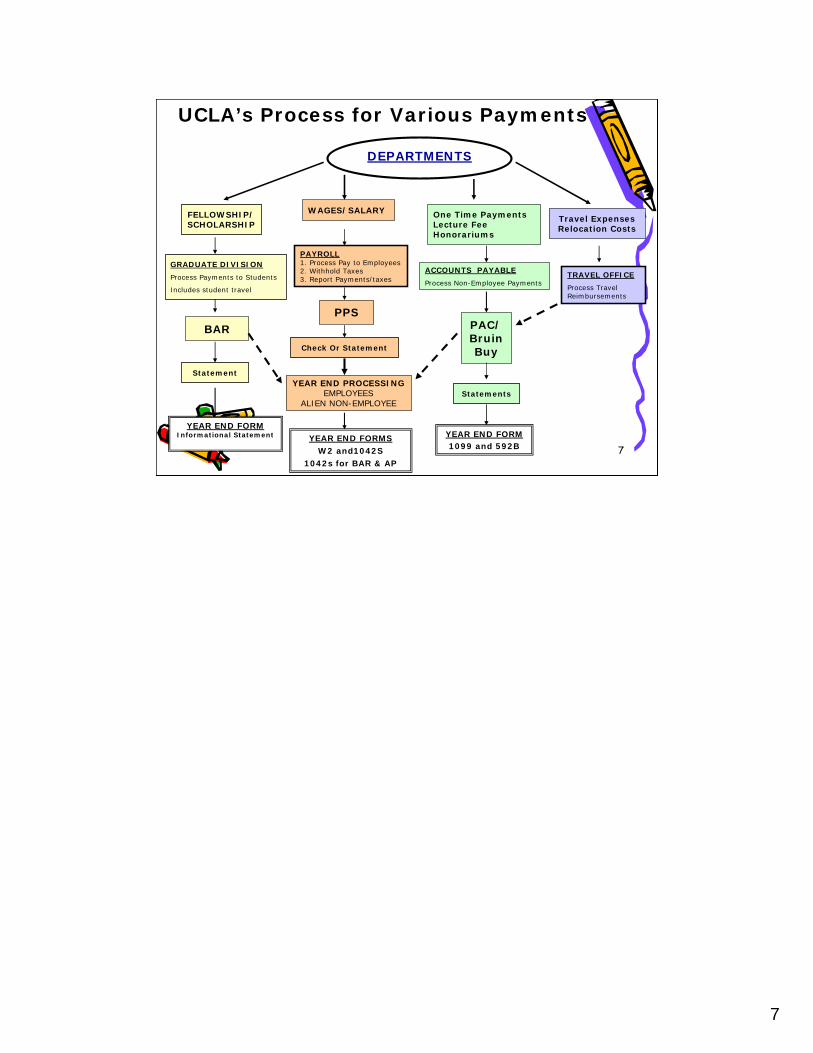

UCLA’s Process for Various Payments

DEPARTMENTS

One Time PaymentsLecture FeeHonorariums

ACCOUNTS PAYABLE

Process Non-Employee Payments

Statements

YEAR END FORM1099 and 592B

Travel ExpensesRelocation Costs

TRAVEL OFFICE

Process Travel Reimbursements

PPS

FELLOWSHIP/SCHOLARSHIP

BAR

Statement

YEAR END FORMInformational Statement

PAYROLL1. Process Pay to Employees2. Withhold Taxes3. Report Payments/taxes

Check Or Statement

YEAR END FORMSW2 and1042S

1042s for BAR & AP

WAGES/SALARY

GRADUATE DIVISION

Process Payments to Students

Includes student travel

YEAR END PROCESSINGEMPLOYEES

ALIEN NON-EMPLOYEE

PAC/Bruin Buy

8

8

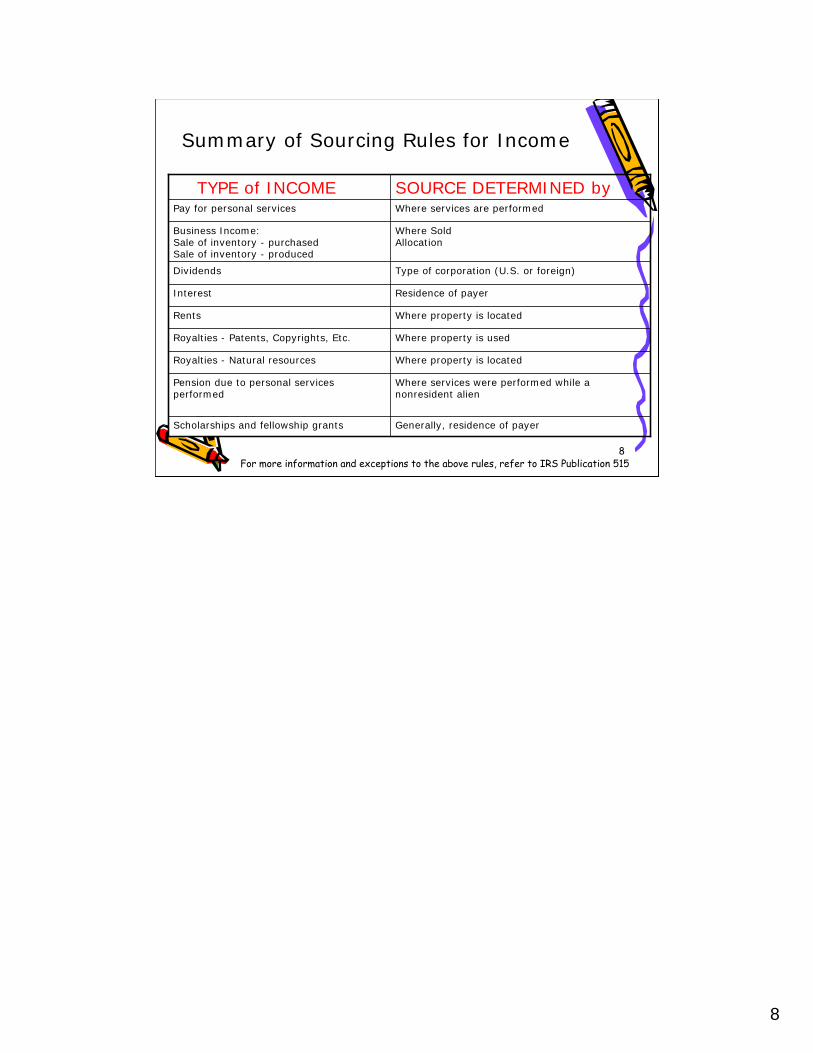

Summary of Sourcing Rules for Income

Where services were performed while a nonresident alien

Pension due to personal services performed

Generally, residence of payer Scholarships and fellowship grants

Where property is located Royalties - Natural resources

Where property is used Royalties - Patents, Copyrights, Etc.

Where property is located Rents

Residence of payer Interest

Type of corporation (U.S. or foreign) Dividends

Where SoldAllocation

Business Income:Sale of inventory - purchasedSale of inventory - produced

Where services are performed Pay for personal services

SOURCE DETERMINED byTYPE of INCOME

For more information and exceptions to the above rules, refer to IRS Publication 515

9

9

REVIEW OF VARIOUS PAYMENTS

REVIEW OF VARIOUS PAYMENTS

•• EmploymentEmployment•• Independent Personal ServicesIndependent Personal Services•• Scholarship/Fellowship Scholarship/Fellowship •• Prize and AwardsPrize and Awards•• RoyaltiesRoyalties•• ReimbursementsReimbursements•• PensionsPensions

10

10

FOR EMPLOYMENTFOR EMPLOYMENT

11

11

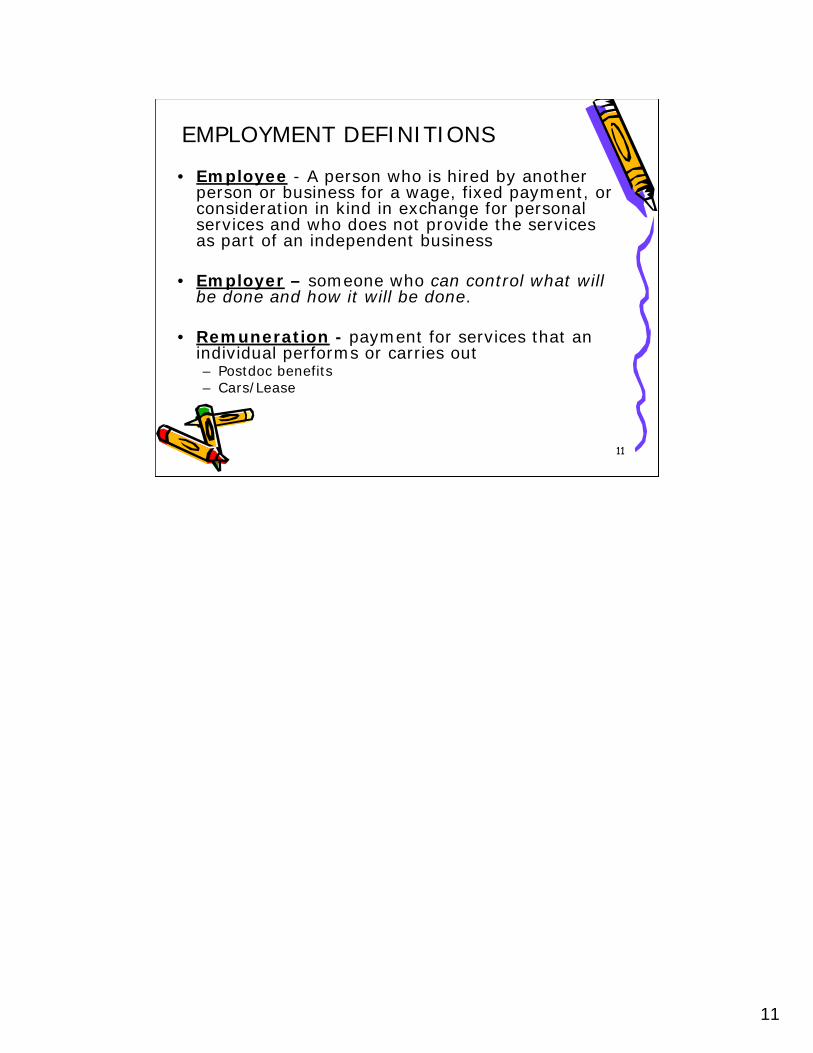

EMPLOYMENT DEFINITIONS

• Employee - A person who is hired by another person or business for a wage, fixed payment, or consideration in kind in exchange for personal services and who does not provide the services as part of an independent business

• Employer – someone who can control what will be done and how it will be done.

• Remuneration - payment for services that an individual performs or carries out– Postdoc benefits– Cars/Lease

12

12

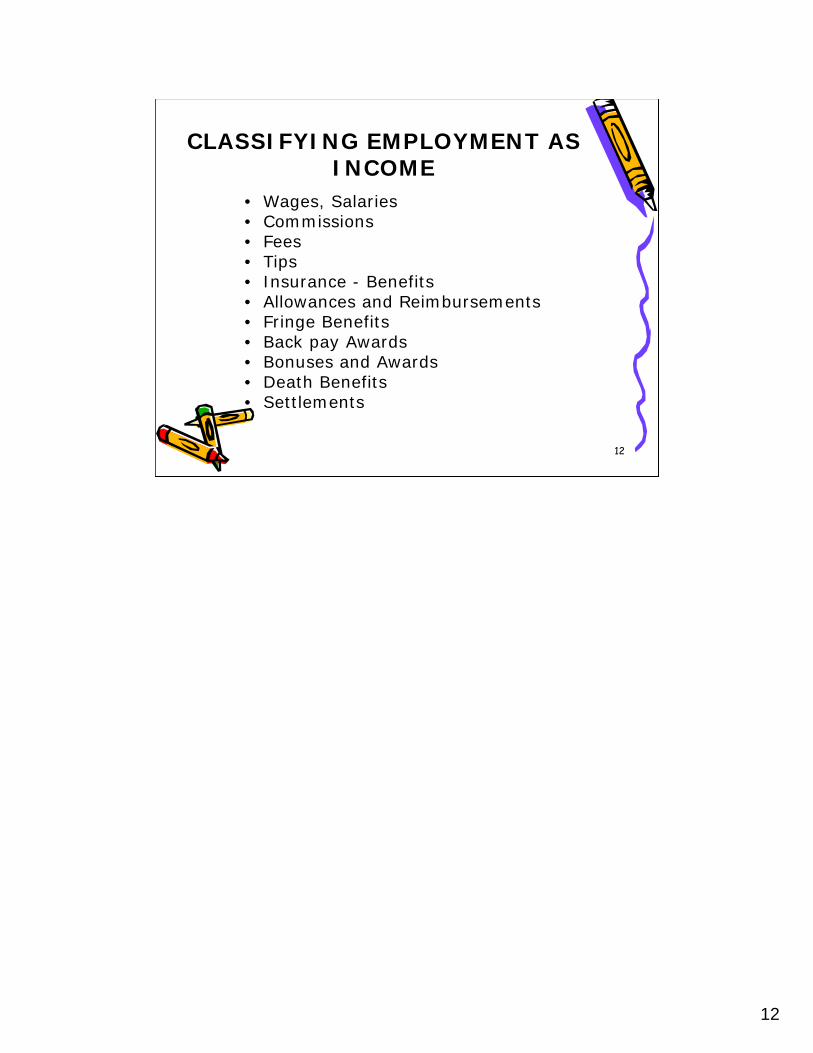

CLASSIFYING EMPLOYMENT AS INCOME

• Wages, Salaries• Commissions• Fees• Tips• Insurance - Benefits• Allowances and Reimbursements• Fringe Benefits• Back pay Awards• Bonuses and Awards• Death Benefits• Settlements

13

13

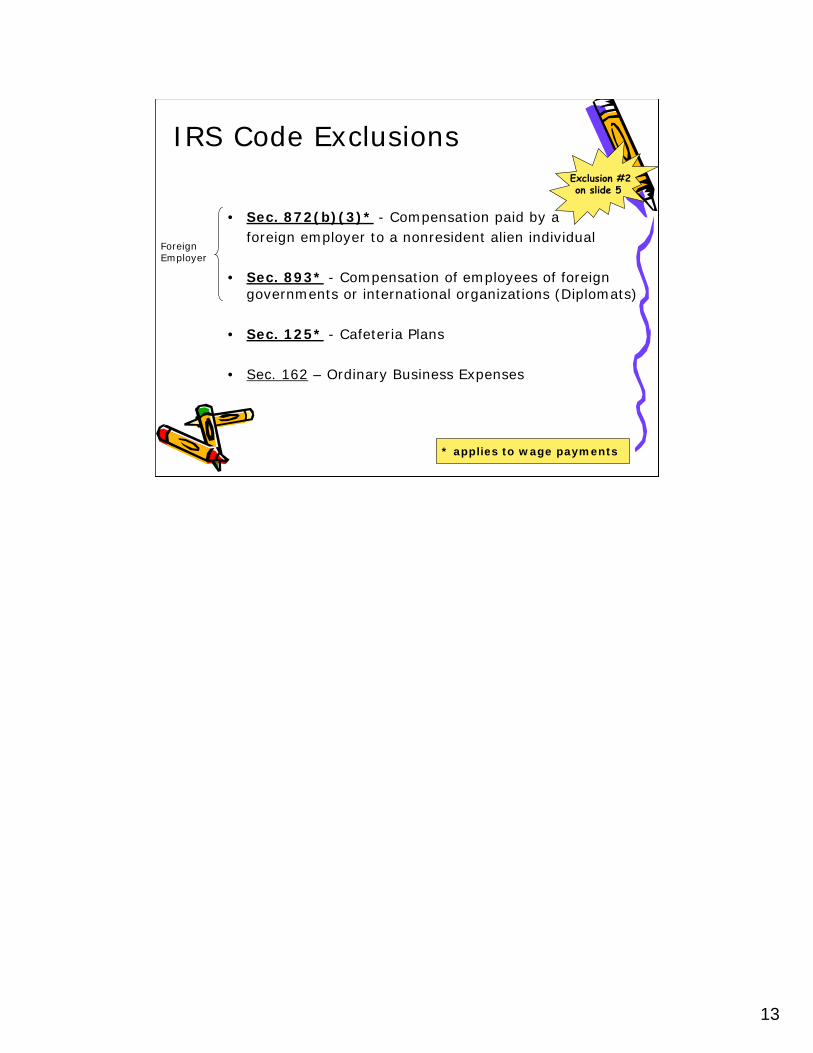

• Sec. 872(b)(3)* - Compensation paid by a foreign employer to a nonresident alien individual

• Sec. 893* - Compensation of employees of foreign governments or international organizations (Diplomats)

• Sec. 125* - Cafeteria Plans

• Sec. 162 – Ordinary Business Expenses

IRS Code Exclusions Exclusion #2on slide 5

* applies to wage payments

ForeignEmployer

14

14

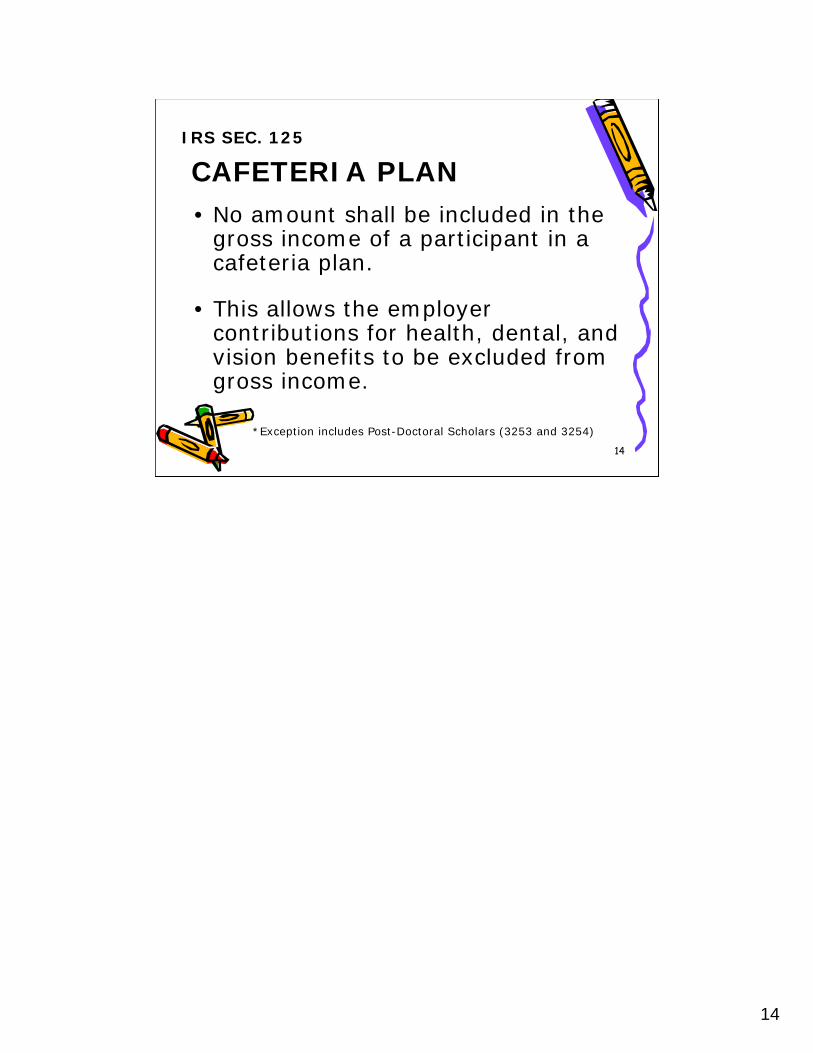

• No amount shall be included in the gross income of a participant in a cafeteria plan.

• This allows the employer contributions for health, dental, and vision benefits to be excluded from gross income.

IRS SEC. 125

CAFETERIA PLAN

*Exception includes Post-Doctoral Scholars (3253 and 3254)

15

15

An agreement between the U.S. and another country that allows either a reduced rate of withholdings or exemption from federal tax withholding.

IRS Federal Income

Tax Treaty Exclusion Exclusion #3On slide 5

Tax treaties for wages recognized at UCLA are • Employment - Income Code 18• Student Employment – Income Code 19

16

16

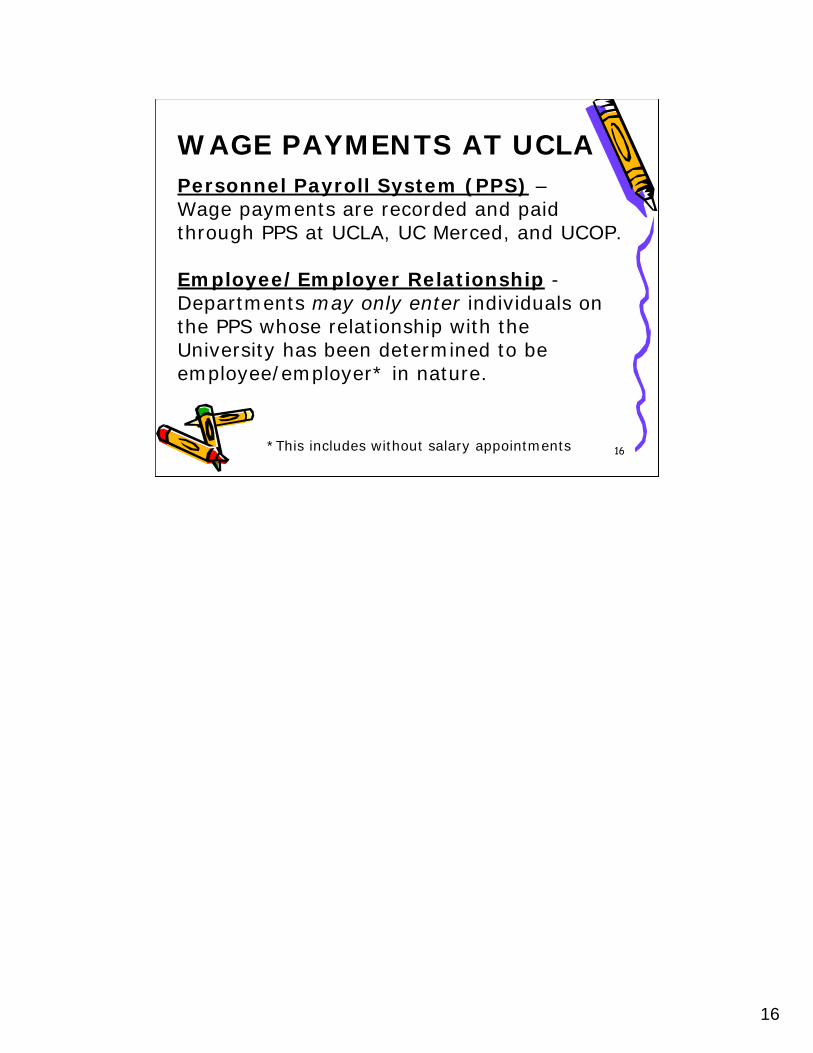

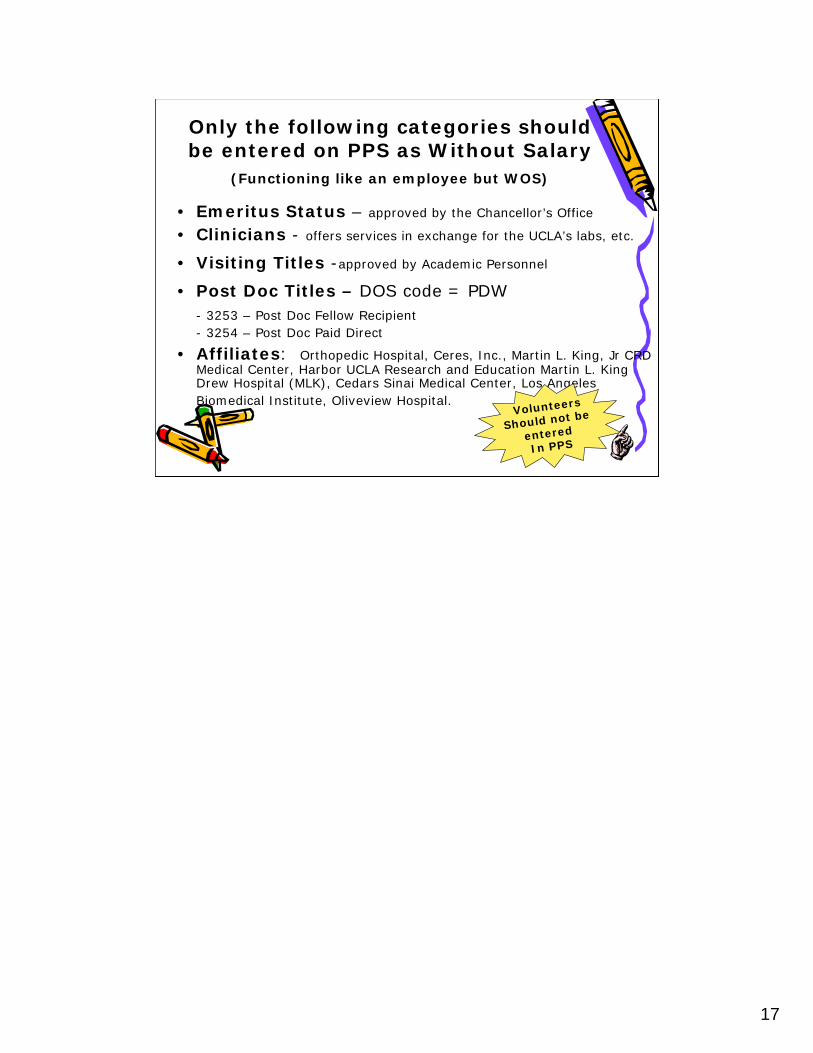

WAGE PAYMENTS AT UCLAPersonnel Payroll System (PPS) –Wage payments are recorded and paid through PPS at UCLA, UC Merced, and UCOP.

Employee/Employer Relationship -Departments may only enter individuals on the PPS whose relationship with the University has been determined to be employee/employer* in nature.

*This includes without salary appointments

17

17

Only the following categories should be entered on PPS as Without Salary

(Functioning like an employee but WOS)

• Emeritus Status – approved by the Chancellor’s Office

• Clinicians - offers services in exchange for the UCLA’s labs, etc.

• Visiting Titles -approved by Academic Personnel

• Post Doc Titles – DOS code = PDW- 3253 – Post Doc Fellow Recipient- 3254 – Post Doc Paid Direct

• Affiliates: Orthopedic Hospital, Ceres, Inc., Martin L. King, Jr CRD Medical Center, Harbor UCLA Research and Education Martin L. King Drew Hospital (MLK), Cedars Sinai Medical Center, Los Angeles Biomedical Institute, Oliveview Hospital.

Volunteers

Should not be

entered

In PPS

18

18

Employment vs. Non-Employment

IRS assumes that all payments made for services are to employees.

Departments are responsible for defining the work individuals will be paid for and properly classifying them as employees or independent contractors.

Departments are required to apply guidelines from Business and Finance Bulletin 77 in order to make a correct determination.

19

19

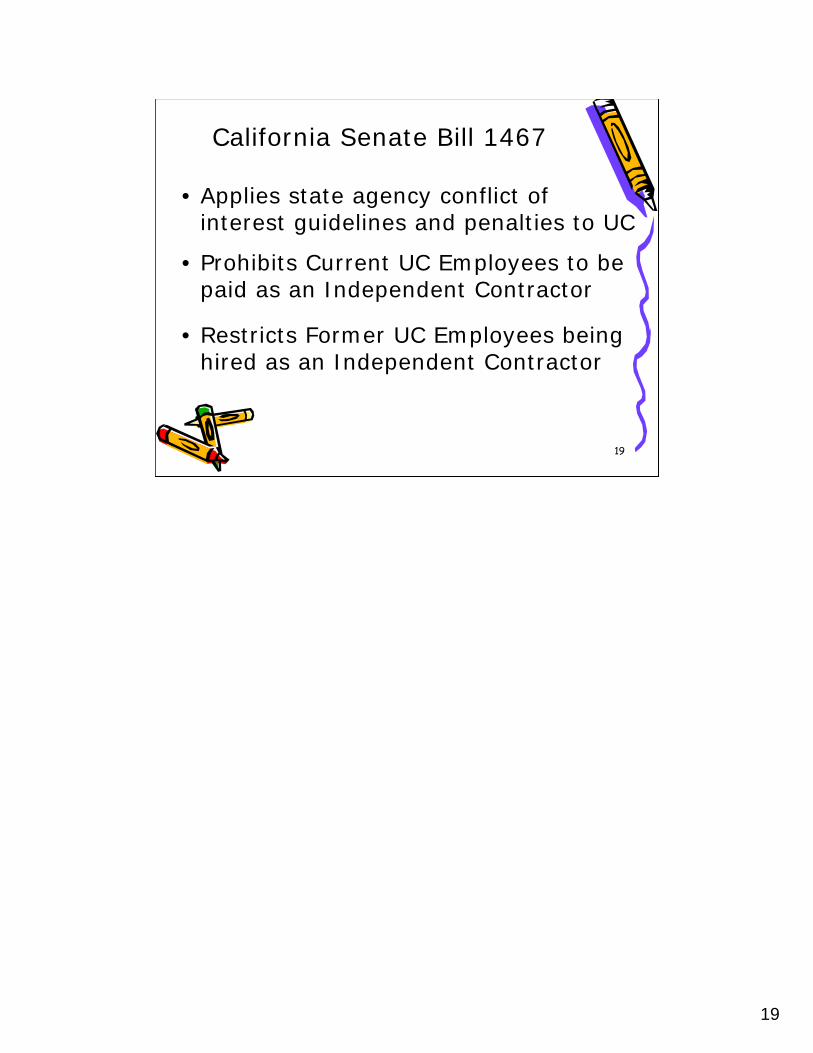

California Senate Bill 1467

• Applies state agency conflict of interest guidelines and penalties to UC

• Prohibits Current UC Employees to be paid as an Independent Contractor

• Restricts Former UC Employees being hired as an Independent Contractor

20

20

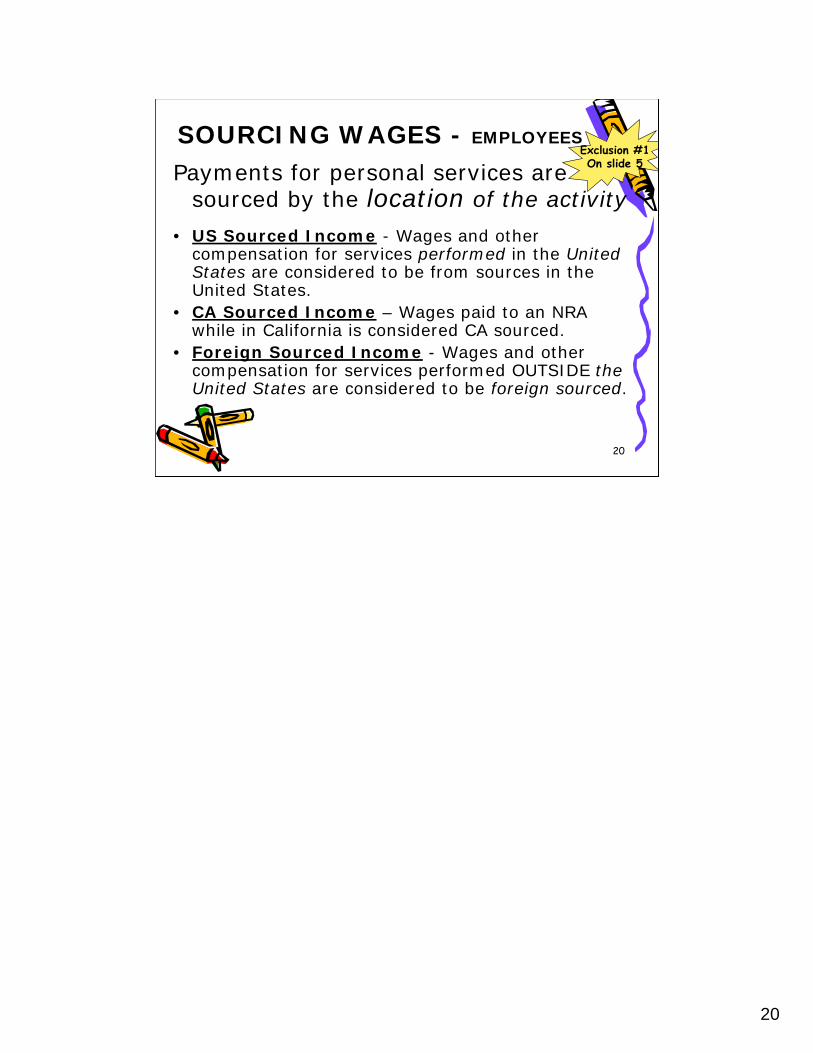

Payments for personal services are sourced by the location of the activity

• US Sourced Income - Wages and other compensation for services performed in the United States are considered to be from sources in the United States.

• CA Sourced Income – Wages paid to an NRA while in California is considered CA sourced.

• Foreign Sourced Income - Wages and other compensation for services performed OUTSIDE the United States are considered to be foreign sourced.

SOURCING WAGES - EMPLOYEESExclusion #1On slide 5

21

21

Independent Personal Services

Independent Personal Services

22

22

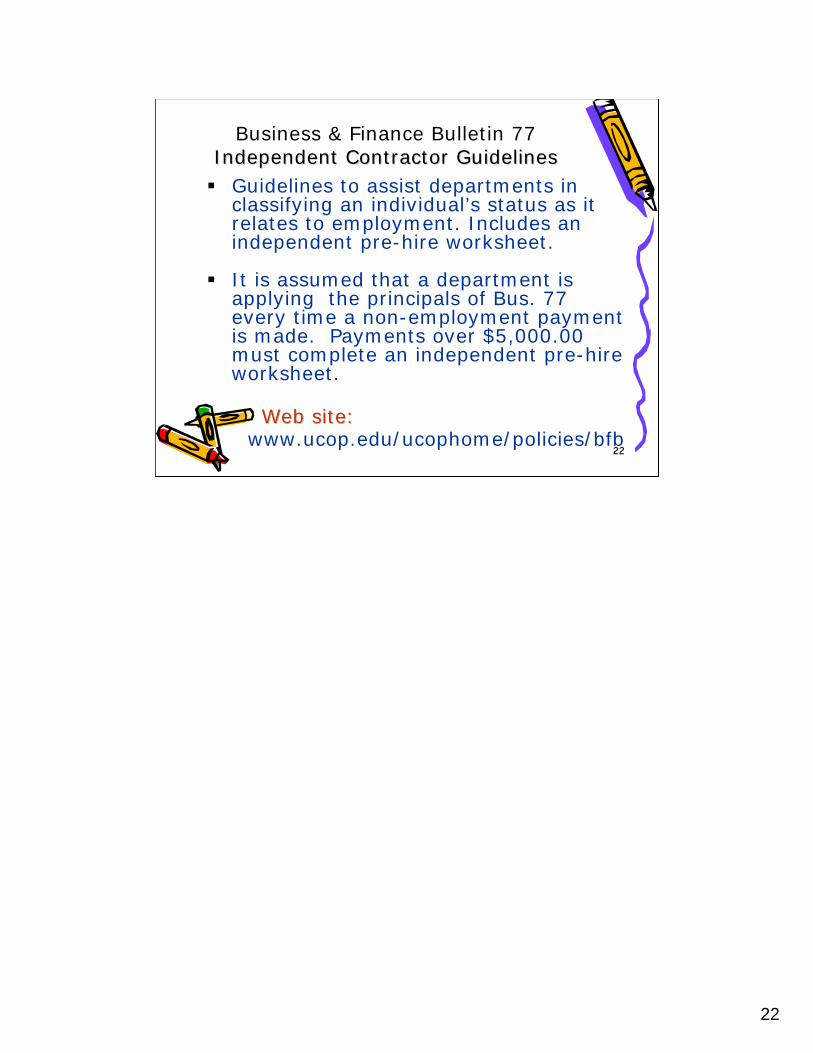

Business & Finance Bulletin 77Independent Contractor GuidelinesIndependent Contractor Guidelines Guidelines to assist departments in

classifying an individual’s status as it relates to employment. Includes an independent pre-hire worksheet.

It is assumed that a department is applying the principals of Bus. 77 every time a non-employment payment is made. Payments over $5,000.00 must complete an independent pre-hire worksheet.

Web site:Web site:www.ucop.edu/ucophome/policies/bfb

23

23

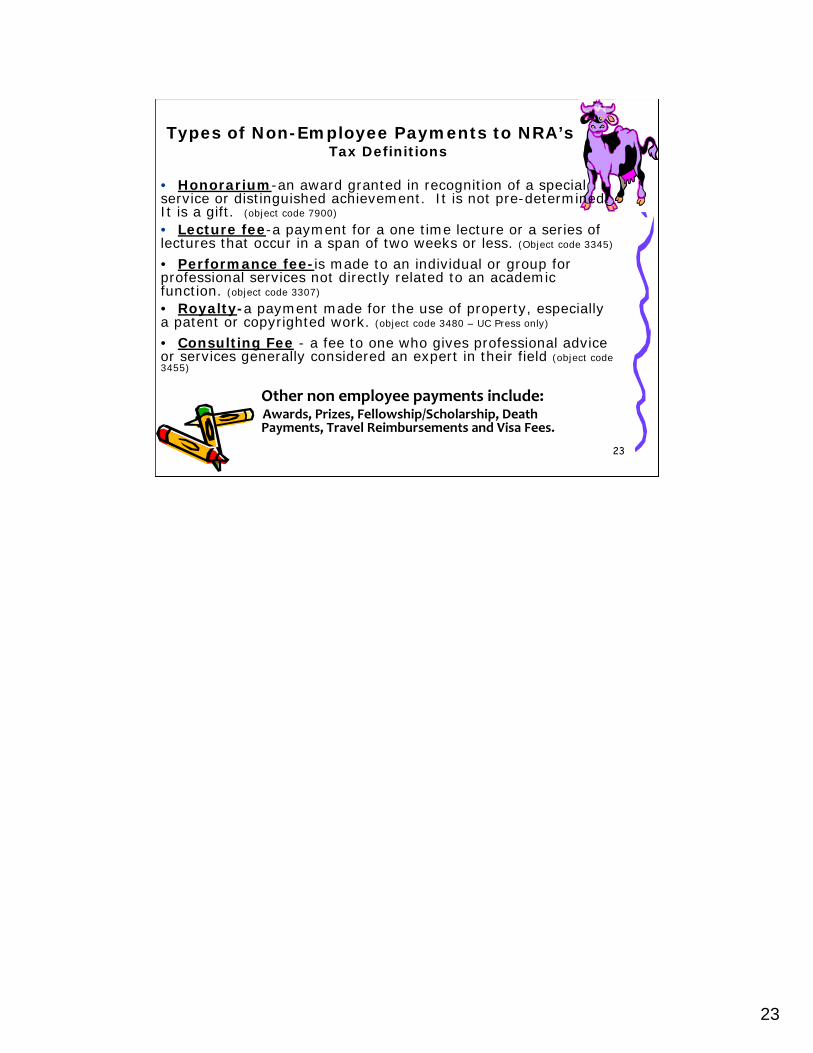

Types of Non-Employee Payments to NRA’sTax Definitions

• Honorarium-an award granted in recognition of a special service or distinguished achievement. It is not pre-determined. It is a gift. (object code 7900)

• Lecture fee-a payment for a one time lecture or a series of lectures that occur in a span of two weeks or less. (Object code 3345)

• Performance fee-is made to an individual or group for professional services not directly related to an academic function. (object code 3307)

• Royalty-a payment made for the use of property, especially a patent or copyrighted work. (object code 3480 – UC Press only)

• Consulting Fee - a fee to one who gives professional advice or services generally considered an expert in their field (object code 3455)

Other non employee payments include:Awards, Prizes, Fellowship/Scholarship, Death Payments, Travel Reimbursements and Visa Fees.

24

24

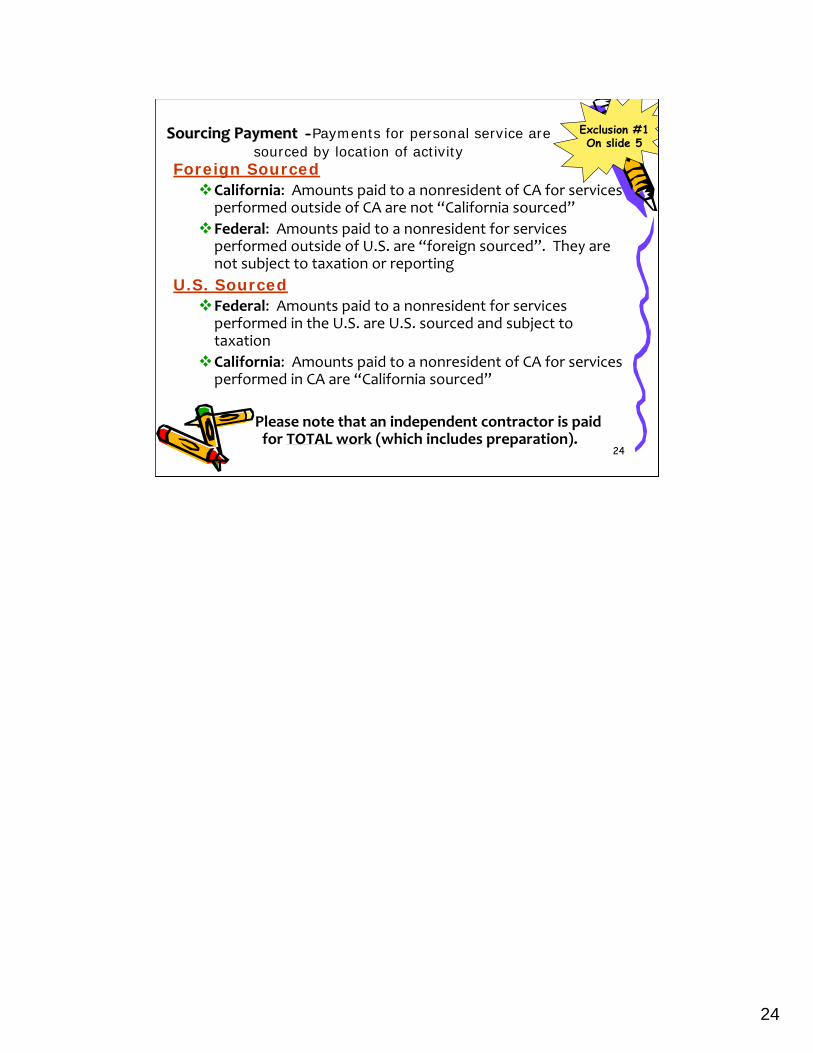

Sourcing PaymentSourcing Payment --Payments for personal service are sourced by location of activity

Foreign SourcedCalifornia: Amounts paid to a nonresident of CA for services

performed outside of CA are not “California sourced”

Federal: Amounts paid to a nonresident for services performed outside of U.S. are “foreign sourced”. They are not subject to taxation or reporting

U.S. SourcedFederal: Amounts paid to a nonresident for services

performed in the U.S. are U.S. sourced and subject to taxation

California: Amounts paid to a nonresident of CA for services performed in CA are “California sourced”

Please note that an independent contractor is paid for TOTAL work (which includes preparation).

Exclusion #1On slide 5

25

25

An agreement between the U.S. and another country that allows for a reduced rate or an exemption of federal tax withholding.

IRS Federal Income

Tax Treaty ExclusionExclusion #3On slide 5

Recognized Tax treaties for non-employee payments at UCLA include:

• Independent and Personnel ServicesIncome Code 16

26

26

Prizes and AwardsPrizes and Awards

27

27

Two Categories1. Prizes which are in the nature of a

Scholarship/Fellowship (S/F). Funds are to be used to defray the expenses of study, training or research.

2. Prizes not in the nature of a S/F. Funds are given as recognition for a special achievement, special skill/knowledge or an award won in a contest. These can be either Employee, or Non-Employee based awards.

Prizes and Awards ~

28

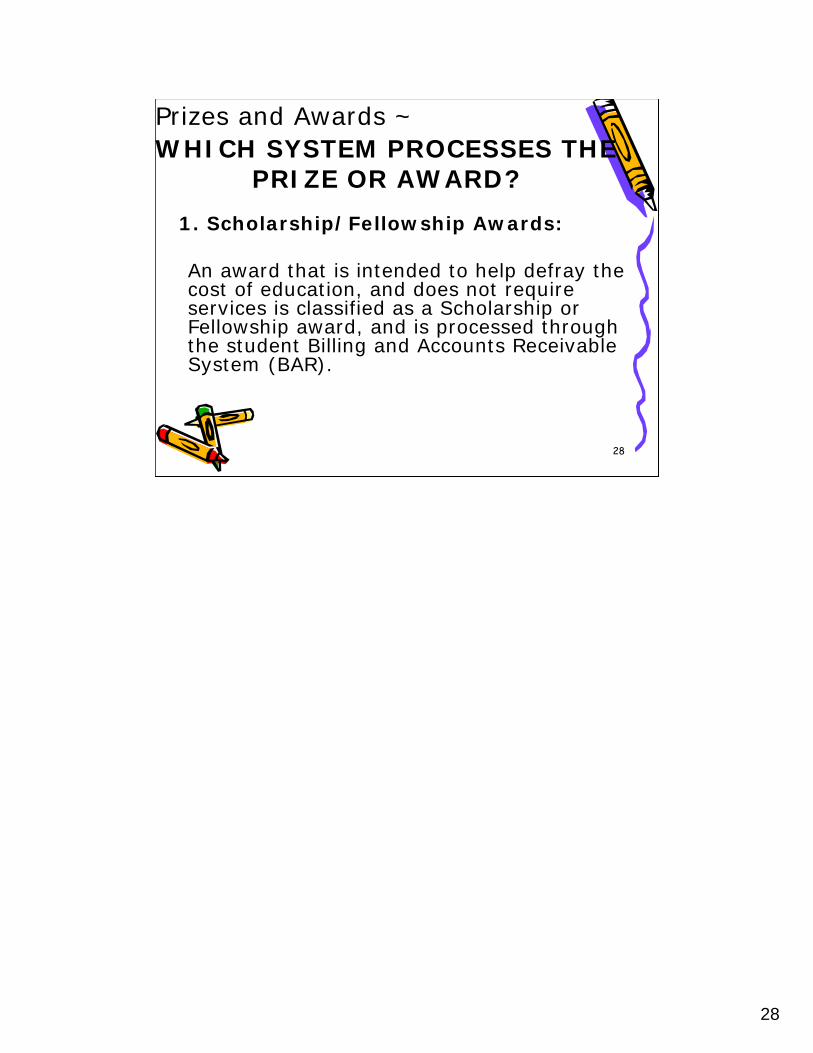

28

WHICH SYSTEM PROCESSES THE PRIZE OR AWARD?

1. Scholarship/Fellowship Awards:

An award that is intended to help defray the cost of education, and does not require services is classified as a Scholarship or Fellowship award, and is processed through the student Billing and Accounts Receivable System (BAR).

Prizes and Awards ~

29

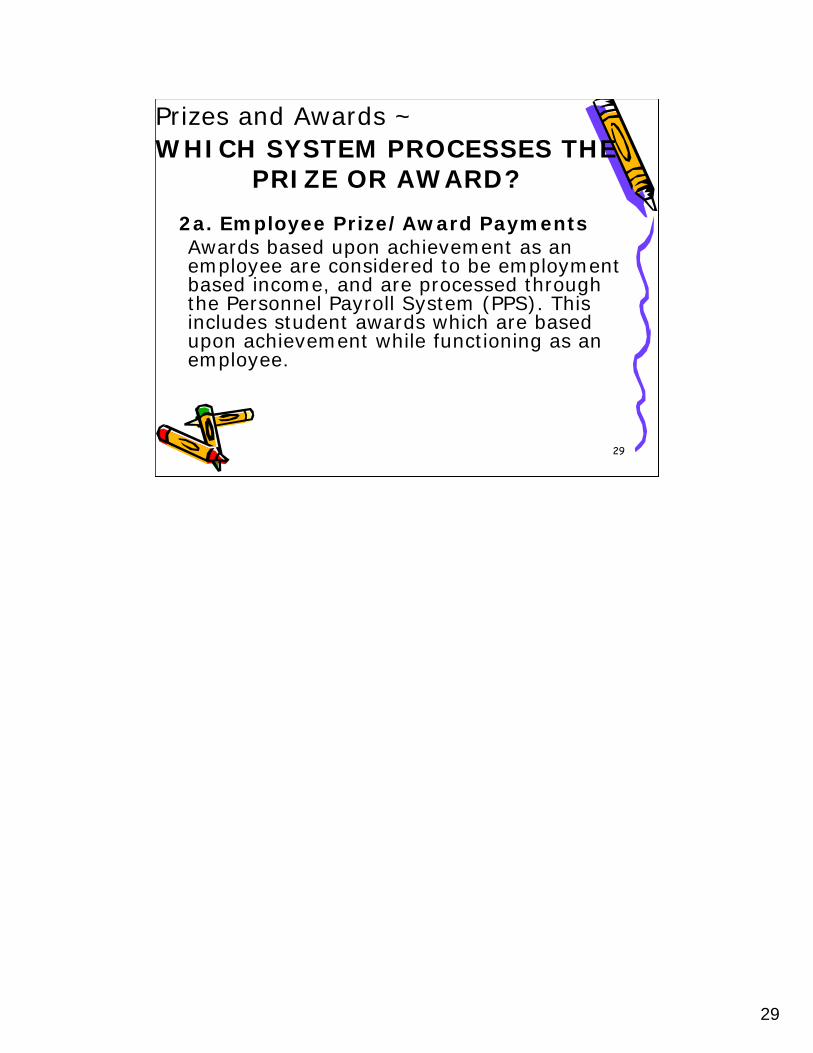

29

WHICH SYSTEM PROCESSES THE PRIZE OR AWARD?

2a. Employee Prize/Award PaymentsAwards based upon achievement as an employee are considered to be employment based income, and are processed through the Personnel Payroll System (PPS). This includes student awards which are based upon achievement while functioning as an employee.

Prizes and Awards ~

30

30

WHICH SYSTEM PROCESSES THE PRIZE OR AWARD?

2b. Non-Employee Cash Prize/AwardPrizes and Awards which are based upon a past achievement unrelated to employment and not intended to defray the cost of education. Non-Employee Cash Prize/Award payments are processed through the BruinBuy system.

Prizes and Awards ~

31

31

The sourcing rules for prize/award payments depend on the type of award being issued:

• Fellowship/Scholarship awards are sourced based upon both the location of the payor and the activity (see Fellowship/Scholarship sourcing rules).

• Employee based awards are sourced based upon the location of the activity that had merited the award.

• Non-Employee Cash Prize/Awards are sourced based upon where the location of the payor.

SOURCING INCOMEPrizes and Awards

Exclusion #1On slide 5

32

32

TAX TREATY EXCLUSION

Dependent upon the country that the recipient is from and the article from the country’s treaty, as well as the income classification based upon the type of award.

Prizes and Awards ~ Exclusion #3

33

33

Scholarship/FellowshipScholarship/Fellowship

34

34

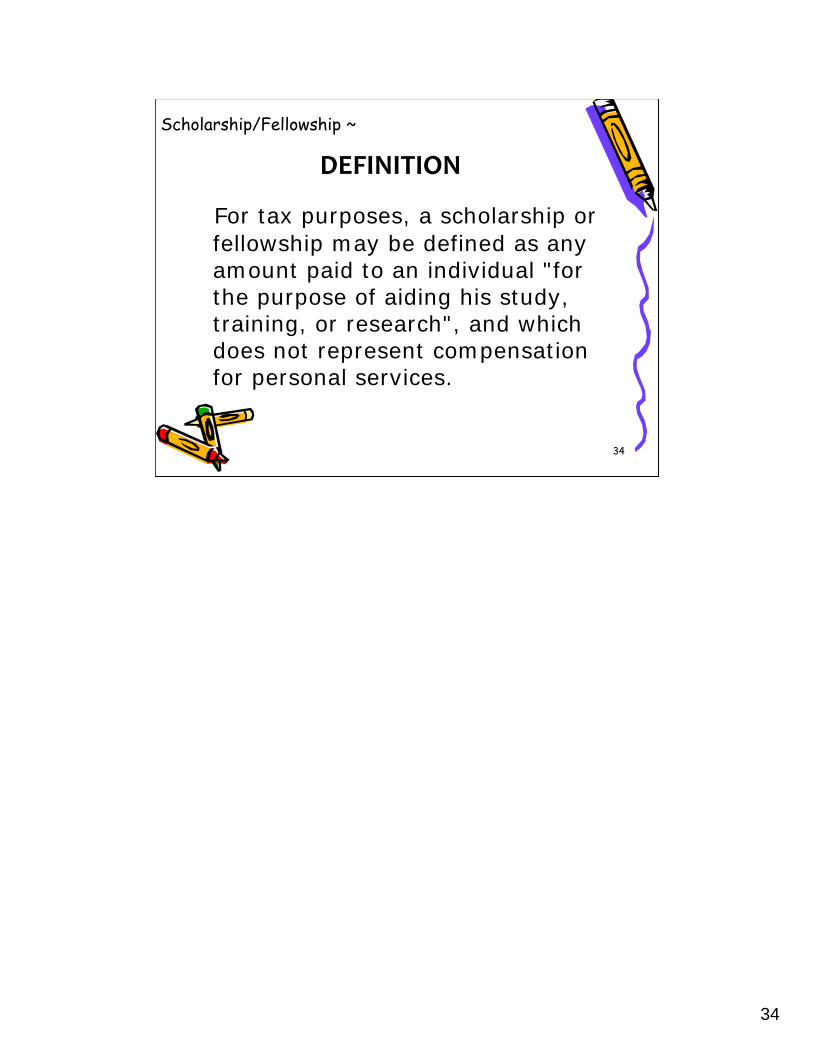

Scholarship/Fellowship ~

For tax purposes, a scholarship or fellowship may be defined as any amount paid to an individual "for the purpose of aiding his study, training, or research", and which does not represent compensation for personal services.

DEFINITION

35

35

1) Are paid through the Billing Account Receivable System

2) Some are paid through Bruin Buy because the recipient is not a student or PostDoc of UCLA

MOST SCHOLARSHIP/FELLOWSHIP PAYMENTS AT UCLA

36

36

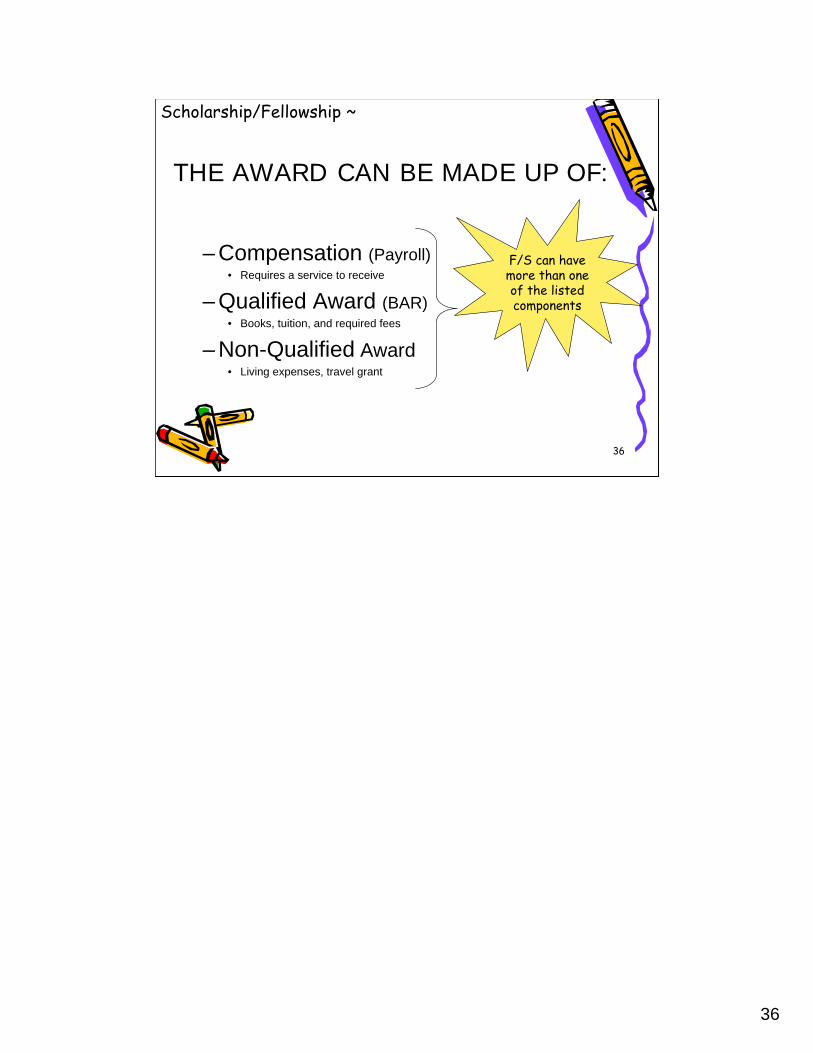

Scholarship/Fellowship ~

– Compensation (Payroll)• Requires a service to receive

– Qualified Award (BAR)• Books, tuition, and required fees

– Non-Qualified Award• Living expenses, travel grant

THE AWARD CAN BE MADE UP OF:

F/S can have more than one of the listed components

37

37

Example of Scholarship/Fellowship Award

Breakdown of income

Payment classificationDescription of Award

$5000 on a 1042sUnqualified Award Scholarship/Fellowship

$5,000 for living expenses or stipend

0 excludedQualified Award Scholarship/Fellowship

$15,000 for tuition, books, and required fees

$10,000 on a W-2

(reported on W-2)

Compensation-Employment

The award requires Joe to work in the lab 10 hours per week for 2 years. The value is $10,000

Joe Bruin receives an award of $30,000.

38

38

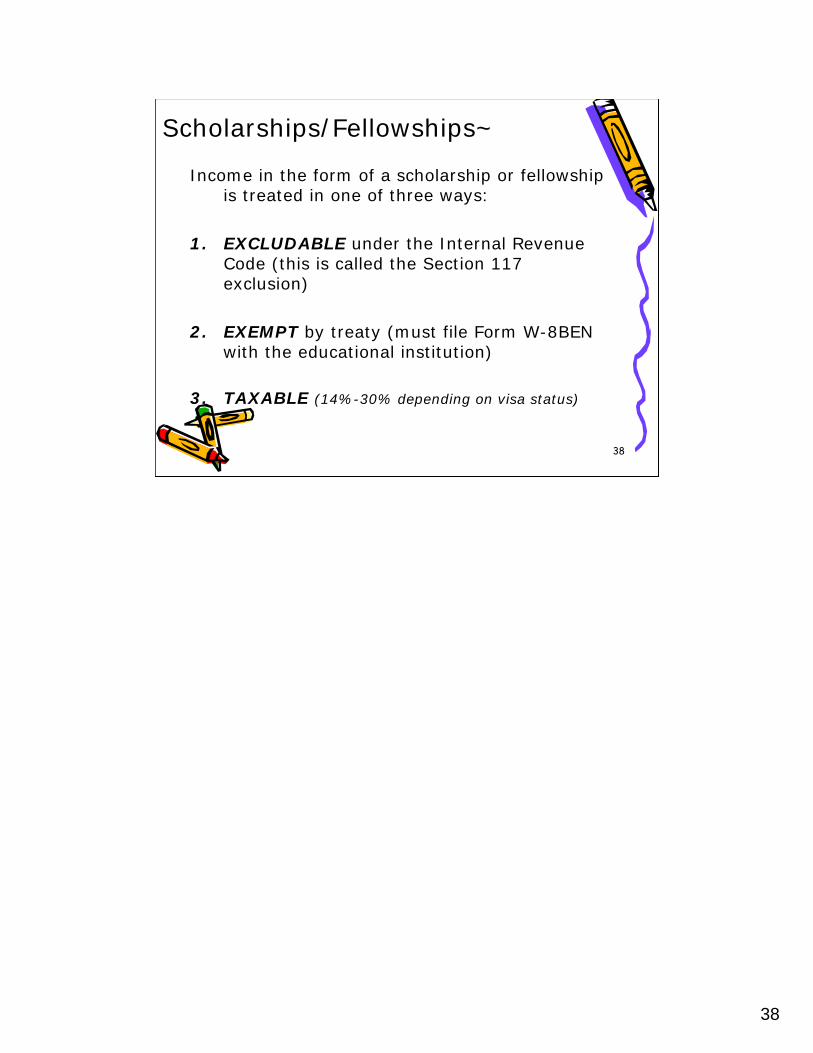

Income in the form of a scholarship or fellowship is treated in one of three ways:

1. EXCLUDABLE under the Internal Revenue Code (this is called the Section 117 exclusion)

2. EXEMPT by treaty (must file Form W-8BEN with the educational institution)

3. TAXABLE (14%-30% depending on visa status)

Scholarships/Fellowships~

39

39

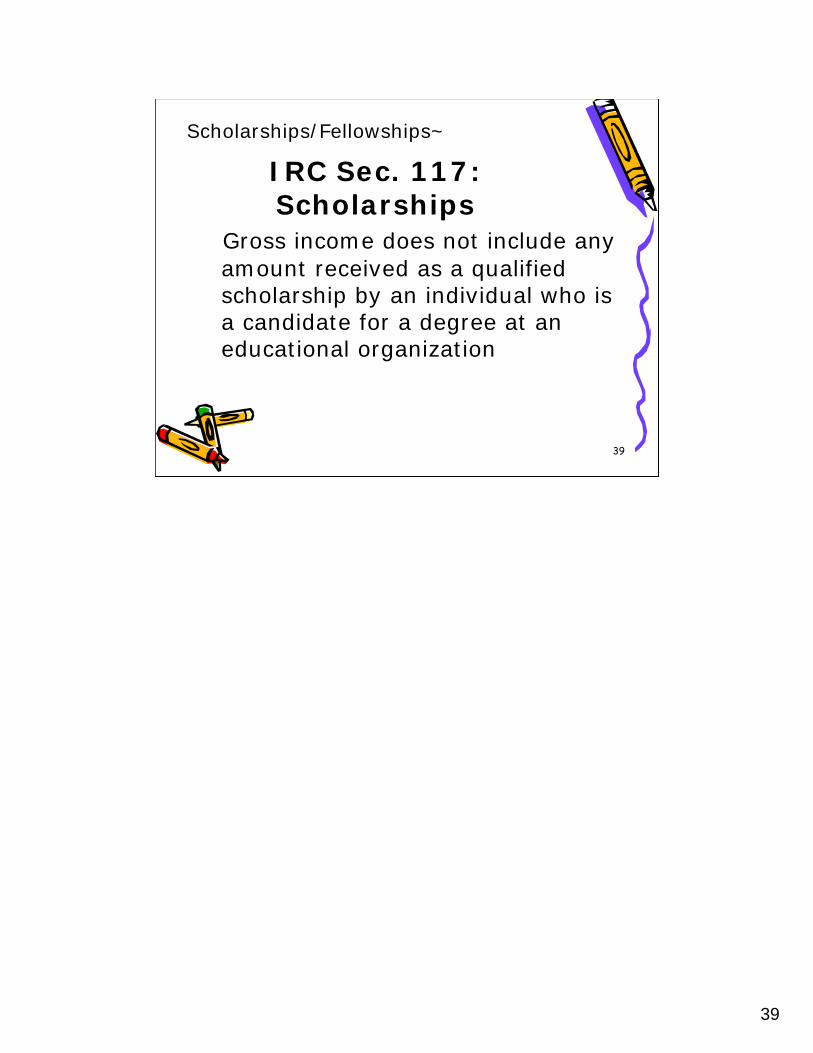

IRC Sec. 117:Scholarships

Gross income does not include any amount received as a qualified scholarship by an individual who is a candidate for a degree at an educational organization

Scholarships/Fellowships~

40

40

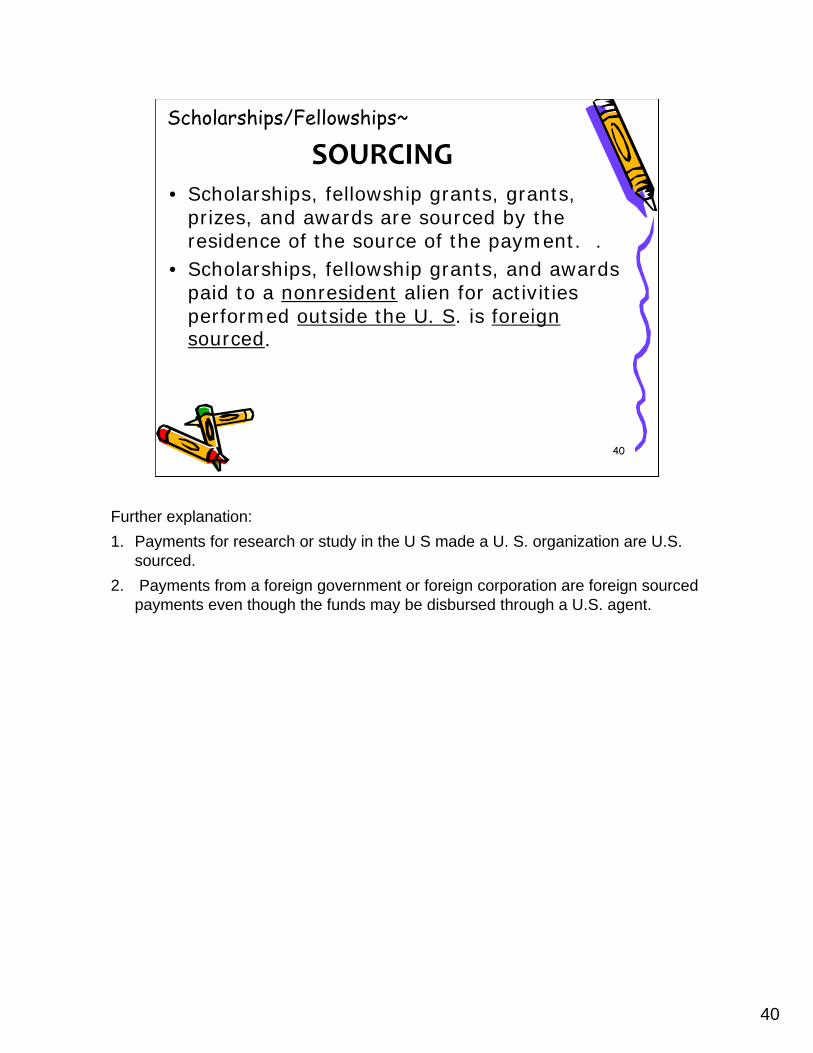

SOURCING• Scholarships, fellowship grants, grants,

prizes, and awards are sourced by the residence of the source of the payment. .

• Scholarships, fellowship grants, and awards paid to a nonresident alien for activities performed outside the U. S. is foreign sourced.

Scholarships/Fellowships~

Further explanation:

1. Payments for research or study in the U S made a U. S. organization are U.S. sourced.

2. Payments from a foreign government or foreign corporation are foreign sourced payments even though the funds may be disbursed through a U.S. agent.

41

41

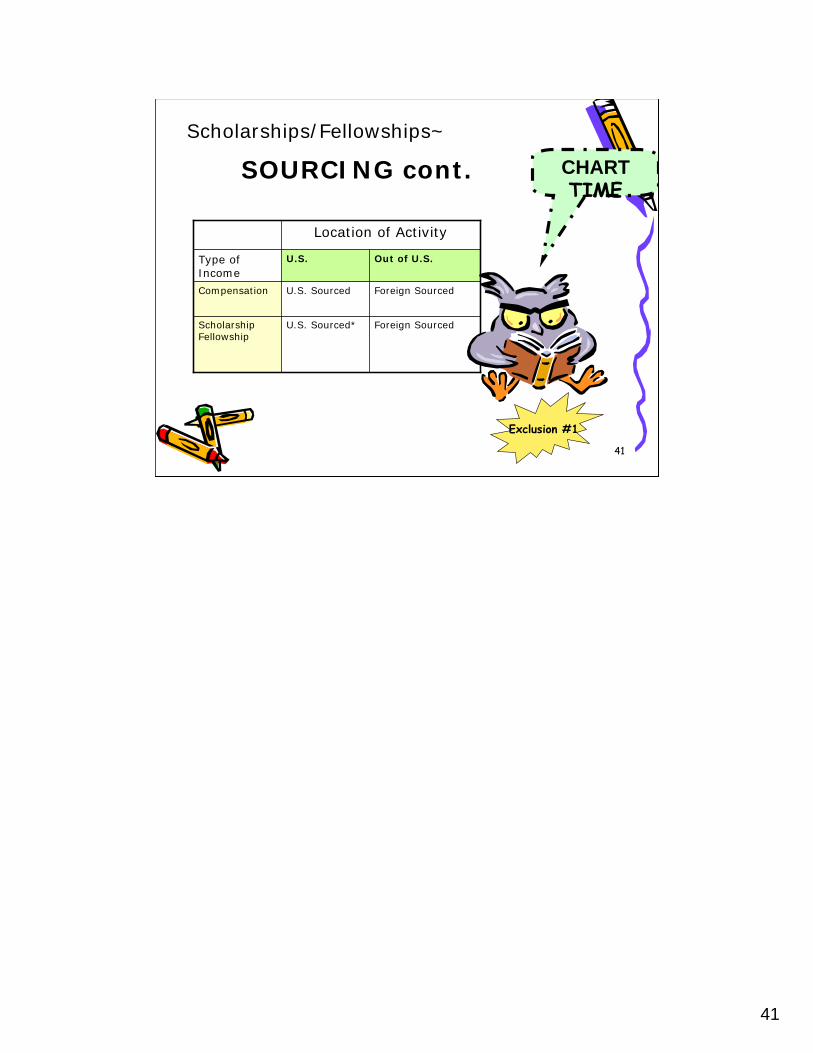

SOURCING cont. CHARTTIME

Foreign SourcedU.S. Sourced* Scholarship Fellowship

Foreign SourcedU.S. SourcedCompensation

Out of U.S.U.S.Type of Income

Location of Activity

Scholarships/Fellowships~

Exclusion #1

42

42

RoyaltiesRoyalties

43

43

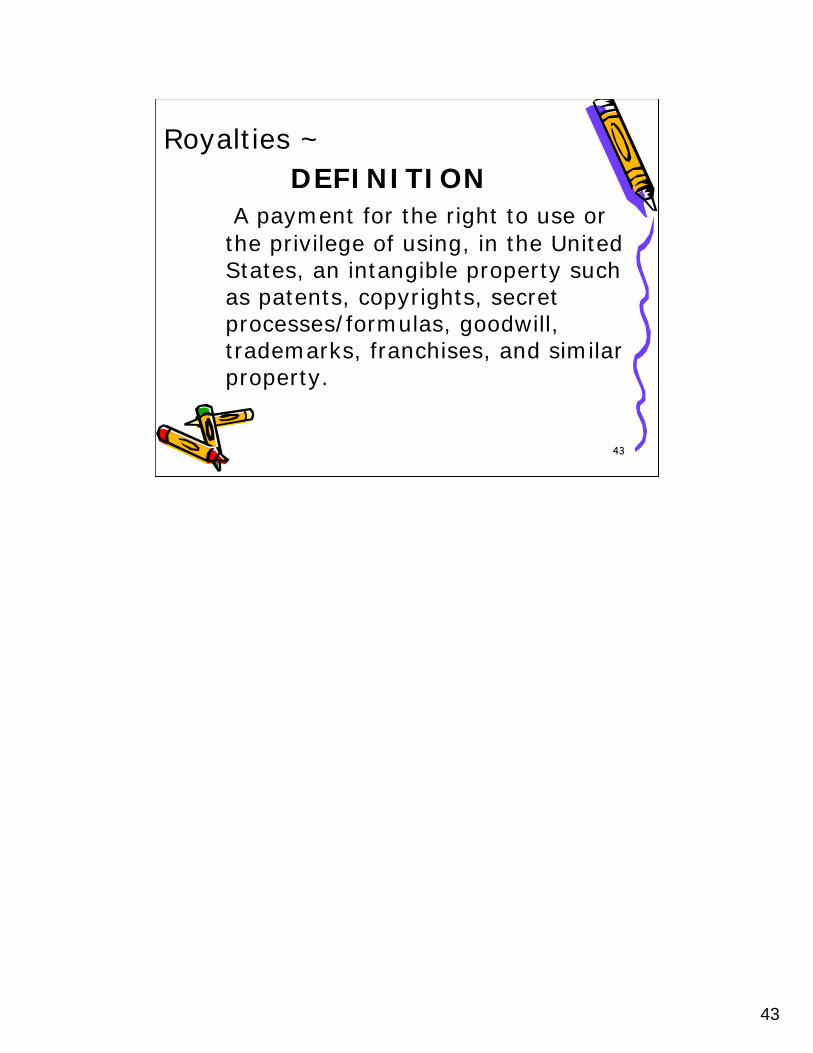

Royalties ~

A payment for the right to use or the privilege of using, in the United States, an intangible property such as patents, copyrights, secret processes/formulas, goodwill, trademarks, franchises, and similar property.

DEFINITION

44

44

RoyaltiesA royalty payment is sourced by it’s type:1. For use of natural resource it is where

the property is located.2. For use of copyright, etc. it is where

the property is used.

Sourcing of incomeRoyalties

Exclusion #1

Royalties are payments for the use of, or for the privilege of using, in the United States, intangible property such as patents, copyrights, secret processes and formulas, goodwill, trademarks, franchises, and similar property.

45

45

TAX TREATY EXCLUSIONIndustrial royalties (Income Code 10)Copyright Royalties (Income Code 12)

Under certain tax treaties, different rates may apply to royalties for information concerning industrial, commercial, and

scientific expertise.

Royalties ~Exclusion #3

46

46

Royalty payments are always paid through Accounts Payable -Bruin Buy System.

Royalties

47

47

ReimbursementsReimbursements

48

48

Reimbursements ~

To pay back or compensate (another party) for money spent or losses incurred.

DEFINITION

49

49

Reimbursements are created in Express and then processed by

the Bruin Buy system.

50

50

Generally not required if payment meets the conditions under the

accountable plan rule.

SOURCING OF INCOME

Reimbursements ~

51

51

Types of Reimbursable Expense per UC Policy

Travel Expense

- Business and Finance G28

- Express

Relocation Expense

- Business and Finance G13

- Payroll

- Bruin Buy

Visa Fees

52

52

Exclusion From Income

Reimbursements of Travel Expense Exclusion #2

Payments made to the purpose of defraying or reimbursing the deductible travel and lodging expenses of such nonresident alien individuals are excludible from the gross income of such nonresident alien individuals and are not reportable to the IRS by the payers of such payments, on the condition that the requirements of the accountable plan rules are met.

The requirements of the accountable plan rules are found in Treasury Regulation 1.62-2

53

53

Requirement of Payee1. Establish:

• the business purpose and • connection of the expenses;

2. Substantiate the expenses claimed to the payer within a reasonable period of time; and

3. Return any amounts to the payer which are over and above the substantiated business expenses within a reasonable period of time.

ACCOUNTABLE PLAN RULEIRS SEC. 162

Exclusion #2

54

54

Reimbursement of Relocation Expenses

• Recruitment- Not Taxable. Paid through Express

• House hunting – All taxable. Paid through EDB

• Moving of household goods - Travel• Travel to New Job –

•Transportation cost - Not Taxable. Paid through Express

•Lodging - Not Taxable. Paid through Express

•Meals – All taxable. Paid through EDB

• Temporary Living Expense

•All Taxable. Goes Through P/R as MOV

55

55

Alpha type visas - not taxable income and the fee is paid through Accounts Payable.

Permanent Resident – may be taxable. Depends on what the employee does for UCLA

Reimbursement of Visa Fees

If the foreign nationals employment is vital to further the University’s mission; then visa fees may be reimbursable.

56

56

PensionsPensions

57

57

Pensions ~

Regular payments made to retired people and to some widows and disabled people, either by the state or from an investment fund.

DEFINITION

58

58

A pension earned for services performed in the United States is U.S. sourced income.

A pension earned for services performed outside the United States is Foreign Sourced.

Pensions ~SOURCING

Exclusion #1

59

59

Pensions Payments are administered and paid by

UCOP and Fidelity.

60

60

You are now an expert on the different You are now an expert on the different types of payments made to nonresident types of payments made to nonresident alien and the particular rules for each of alien and the particular rules for each of

those payments. those payments.

Congratulations!

You made it to the end of class!